Market Overview

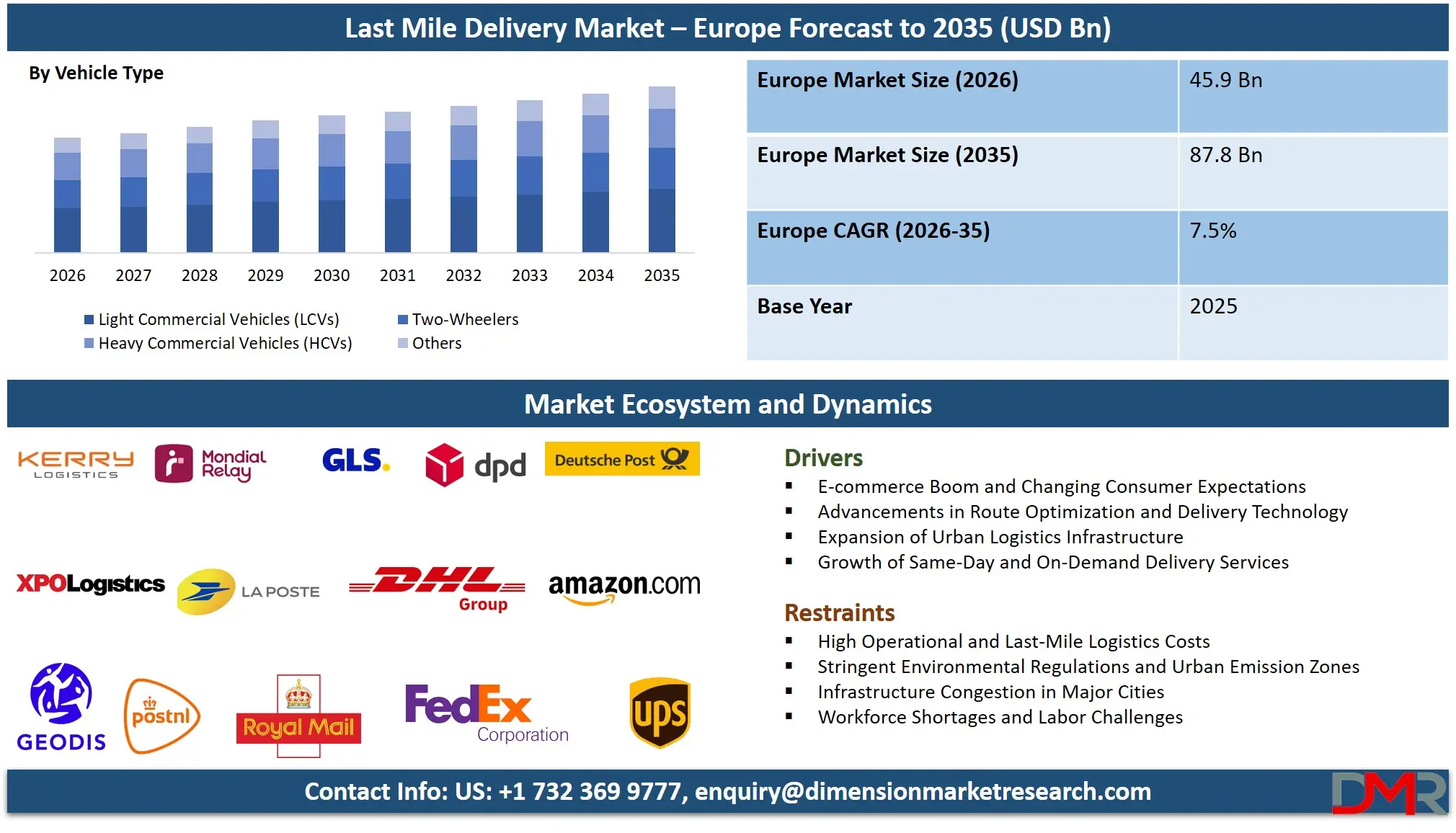

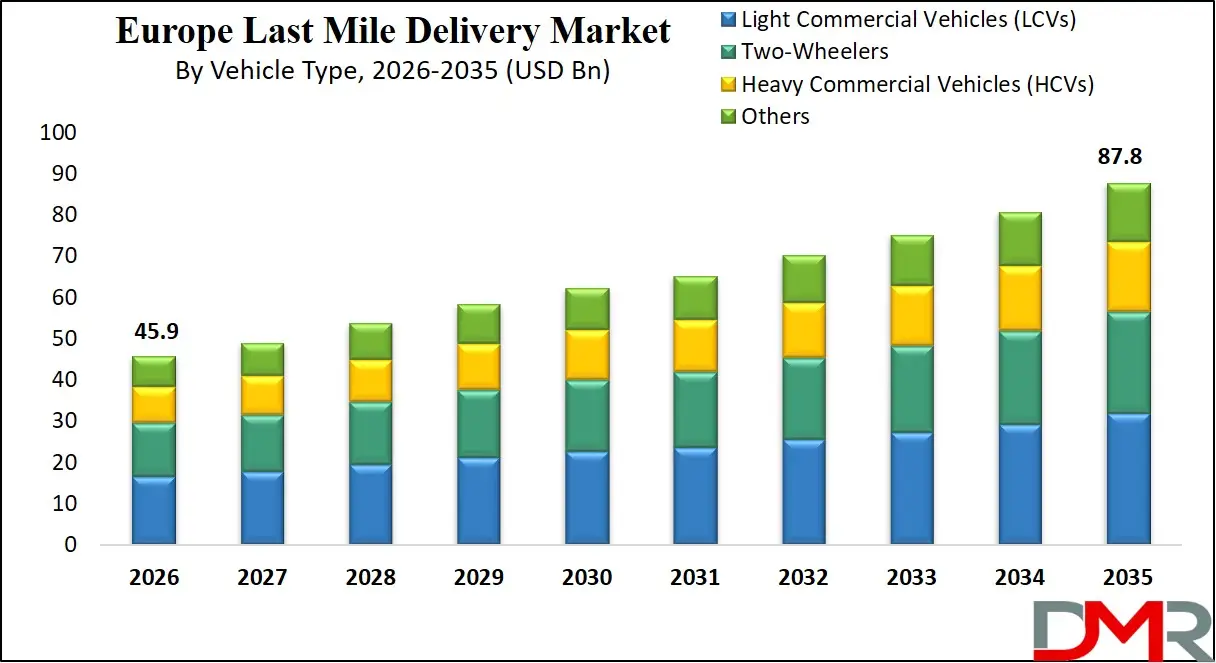

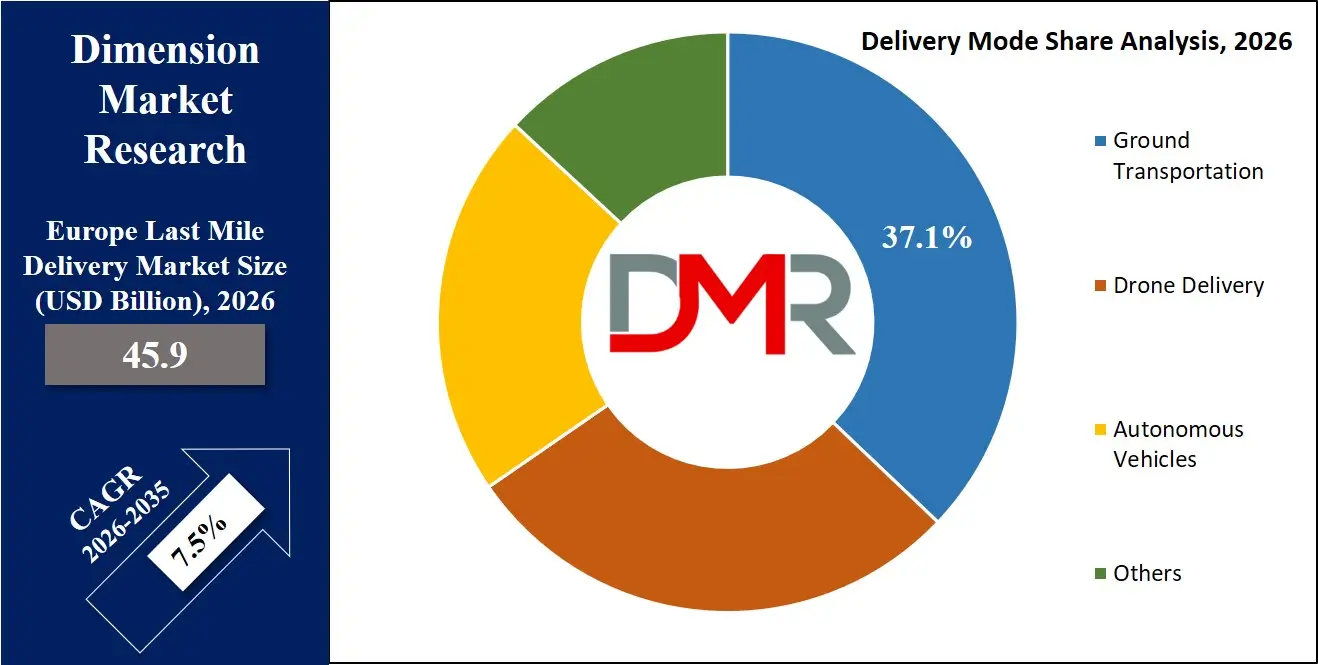

The Europe last mile delivery market is projected to reach approximately USD 45.9 billion by 2026 and further expand to USD 87.8 billion by 2035, growing at a CAGR of 7.5%. This segment represents the final and most complex stage of the logistics chain, where goods are transported from distribution centers to end consumers. Its importance has increased significantly due to the rapid rise of e-commerce, evolving consumer expectations for faster deliveries, and regulatory emphasis on sustainability. Europe's dense urban environments and diverse infrastructure create both operational challenges and opportunities, driving continuous innovation across the sector.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

In recent years, the market has undergone a major transformation with the integration of advanced technologies such as Artificial Intelligence (AI), the Internet of Things (IoT), and automated route optimization systems. These innovations enable logistics providers to enhance delivery efficiency, reduce operational costs, and offer real-time tracking to customers. The surge in online shopping, accelerated by the pandemic, has further intensified the demand for same-day and next-day delivery services. As a result, companies are increasingly investing in micro-fulfillment centers, urban warehouses, and alternative delivery models to meet consumer expectations.

Sustainability has emerged as a key focus area, strongly influenced by the European Union's Green Deal objectives. Logistics companies are actively adopting eco-friendly practices, including the deployment of electric vehicles, cargo bikes, and low-emission delivery solutions. The development of urban micro-hubs and consolidation centers is also helping reduce congestion and carbon emissions in city centers. Additionally, digitalization is enabling predictive analytics and demand forecasting, allowing companies to optimize delivery networks and improve overall service levels.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Despite strong growth prospects, the market faces several challenges. A persistent shortage of delivery drivers across Europe is increasing labor costs and operational pressures. Moreover, the fragmented regulatory environment across different countries adds complexity to cross-border logistics operations. High fuel costs and the significant investment required for fleet electrification, along with limited charging infrastructure, further constrain market expansion.

Overall, the European last mile delivery market plays a crucial role in supporting the region's economy and retail ecosystem. With continued advancements in technology, rising e-commerce penetration, and increasing focus on sustainable logistics, the market is expected to witness sustained growth. Innovations such as autonomous delivery vehicles and drones are likely to further redefine the sector, ensuring its pivotal role in the future of commerce.

Europe Last Mile Delivery Market: Key Takeaways

- Market Value: The Europe Last Mile Delivery Market size is estimated to have a value of USD 45.9 billion in 2026 and is expected to reach USD 87.8 billion by the end of 2035.

- By Delivery Mode Segment Analysis: Ground transportation is anticipated to dominate this segment, holding the largest market share in 2026, driven by its established infrastructure and flexibility.

- By Vehicle Type Segment Analysis: Light Commercial Vehicles (LCVs) are projected to dominate the vehicle type segment in the European market, serving as the backbone for urban and suburban deliveries.

- By Service Type Segment Analysis: The B2C segment is anticipated to dominate the service type segment, fueled by the continuous surge in e-commerce and direct-to-consumer models.

- By Delivery Time Frame Segment Analysis: Standard (2-5 days) delivery is projected to hold a leading position, but same-day and next-day delivery are the fastest-growing segments.

- By Application Segment Analysis: The E-commerce/Retail sector is projected to dominate the application segment, reflecting the high volume of goods purchased online.

- By End-User Segment Analysis: Large Enterprises are projected to be the dominant end-user segment, owing to their high delivery volumes and complex logistics needs, though SMEs represent a rapidly growing area.

- Key Players: Some of the major key players in the Europe Last Mile Delivery Market are DHL Group, Amazon Logistics, La Poste Group, Royal Mail, DB Schenker, Geopost (DPDgroup), GLS, and many others.

- Market Growth Rate: The market is growing at a CAGR of 7.5 percent over the forecasted period.

Impact of Iran Conflict on Europe Last Mile Delivery Market

- Fuel Cost Inflation Pressure: Rising crude oil prices due to Iran conflict increase transportation expenses, forcing European last mile delivery providers to optimize routes, adopt fuel-efficient fleets, and implement cost-control strategies to maintain margins and service reliability.

- Cross-Border Supply Chain Disruptions: Geopolitical tensions create uncertainties in international trade routes, delaying shipments into Europe and impacting last mile timelines, prompting logistics companies to strengthen regional warehousing and improve inventory buffering strategies.

- Increased Security and Compliance Measures: Stricter customs checks and security protocols slow down cargo movement across borders, increasing administrative burdens and compliance costs for European last mile operators while requiring advanced tracking and documentation systems.

- Currency Volatility and Pricing Adjustments: Fluctuations in currency values driven by geopolitical instability affect import costs and contract pricing, pushing European delivery firms to revise pricing models and adopt financial hedging strategies.

- Higher Insurance and Risk Costs: Insurance premiums rise for shipments passing through sensitive regions, increasing overall logistics expenses and encouraging companies to reassess routing, partnerships, and risk mitigation frameworks.

Europe Last Mile Delivery Market: Use Cases

- E-commerce Fulfillment: Managing the high volume of consumer goods from online retailers, requiring optimized routes, flexible delivery windows, and seamless return processes to ensure customer satisfaction.

- Grocery & Food Delivery: Handling perishable and time-sensitive items with strict temperature controls, demanding ultra-fast delivery times, and sophisticated logistics to maintain freshness and quality.

- Healthcare Supply Chain: The time-critical and secure delivery of pharmaceuticals, medical devices, and diagnostics to hospitals, clinics, and patients, which requires specialized cold chain capabilities and rigorous compliance.

- Urban Parcel Delivery: Efficiently delivering a high density of parcels in congested city centers, often utilizing micro-hubs, cargo bikes, and electric vehicles to navigate traffic and low-emission zones.

Europe Last Mile Delivery Market: Stats & Facts

Eurostat

- Around 1 in 3 EU online shoppers faced delivery-related issues, including delays and incorrect items.

- The average parcel delivery time in the UK is about 1.27 business days.

- Low-value e-commerce imports (below about USD 160 equivalent) reached 4.17 billion items in the EU.

- Germany leads Europe in outbound parcel traffic volume.

- The EU third-party logistics market is valued at approximately USD 194–195 billion.

- Fuel contributes about 24.2% of last-mile delivery costs.

European Commission

- The EU aims for zero-emission urban logistics by 2030.

- Over 70% of the EU population lives in urban areas, increasing last-mile demand.

- Cross-border e-commerce represents more than one-third of EU online trade.

- Digital Single Market policies are improving cross-border logistics efficiency.

International Energy Agency

- Transport accounts for around 25% of Europe's CO₂ emissions.

- Electrification of logistics fleets is growing rapidly across Europe.

European Environment Agency

- Urban freight contributes to up to 25% of transport-related CO₂ emissions in cities.

- Last-mile logistics accounts for 10–15% of urban traffic flows.

- Freight demand in Europe is projected to increase significantly by 2050.

World Bank

- Efficient logistics systems can reduce total logistics costs by up to 30%.

- Logistics performance is a key driver of economic competitiveness.

OECD

- Parcel volumes in Europe are experiencing double-digit annual growth due to e-commerce.

- Urban logistics inefficiencies can increase delivery costs by up to 50%.

- Demand for same-day delivery is rapidly increasing across Europe.

European Central Bank

- E-commerce growth is a major contributor to logistics sector expansion.

- Faster delivery expectations are intensifying competition among retailers.

UNCTAD

- Europe is among the largest e-commerce markets globally.

- Digital adoption is accelerating logistics innovation and efficiency.

European Cyclists' Federation

- Cargo bikes can handle up to 50% of urban deliveries in dense cities.

- Cargo bikes can reduce delivery emissions by up to 90%.

EU Consumer & Digital Behavior Data

- 21.3% of German consumers use parcel lockers for deliveries.

- 24.3% of Spanish consumers prefer click-and-collect delivery.

- 29% of French Gen Z consumers prefer AI-based delivery tracking systems.

Europe Last Mile Delivery Market: Market Dynamic

Driving Factors in the Europe Last Mile Delivery Market

E-commerce Expansion and Consumer Expectations

The sustained growth of e-commerce across Europe is the primary engine driving the last mile delivery market. As consumers increasingly purchase a wider array of goods online, from fashion to furniture, the volume of parcels requiring delivery continues to rise. This growth is compounded by rising consumer expectations for speed (same-day/next-day), transparency (real-time tracking), and convenience (flexible delivery options). These expectations force constant innovation and investment in logistics networks, making efficient last mile delivery a critical success factor for retailers and brands.

EU Digital Single Market and Green Deal Initiatives

The European Union's strategic initiatives are powerful growth drivers for the sector. The Digital Single Market aims to remove cross-border barriers, facilitating easier and more cost-effective e-commerce and parcel delivery across member states. Concurrently, the European Green Deal is accelerating investment in sustainable logistics, funding green infrastructure projects, and creating a regulatory framework that rewards low-emission delivery solutions. These initiatives provide a stable, long-term vision and a supportive policy environment for growth and innovation.

Restraints in the Europe Last Mile Delivery Market

Persistent Driver Shortage and Labor Costs

A chronic and pervasive challenge across Europe is the shortage of qualified delivery drivers. This shortage is driven by demanding working conditions, high turnover, and increasing competition from other sectors. The resulting upward pressure on wages significantly impacts the profitability of last mile operators. The reliance on a large, flexible workforce makes the sector vulnerable to labor market fluctuations, hindering the scalability of operations and increasing overall service costs.

Regulatory Complexity and Urban Restrictions

Navigating the patchwork of regulations across EU member states and even within cities is a significant operational burden. This includes varying rules on low-emission zones, delivery curfews, vehicle size restrictions, and driver working hours. As cities increasingly implement measures to reduce traffic congestion and pollution, logistics providers face growing operational constraints. Complying with these diverse and often changing regulations requires significant administrative effort and fleet flexibility, acting as a major restraint on seamless operations.

Opportunities in the Europe Last Mile Delivery Market

Technological Integration and Automation

The integration of advanced technologies like AI for route optimization, machine learning for demand forecasting, and autonomous vehicles presents a significant opportunity to revolutionize last mile efficiency. AI-driven platforms can dynamically reroute deliveries, predict delays, and optimize load factors, substantially cutting costs and delivery times. Startups and established players are increasingly testing autonomous delivery robots and drones, particularly in controlled urban and suburban environments, offering a pathway to lower labor costs and solve the driver shortage issue.

Expansion of Specialized Delivery Services

The growing complexity of consumer needs is creating opportunities for specialized last mile services. The cold chain logistics segment is expanding rapidly due to the growth of online grocery, meal kits, and direct-to-consumer pharmaceuticals. Similarly, the demand for bulky or high-value item delivery (e.g., furniture, electronics) with assembly and installation services is on the rise. Providers who can offer these value-added, specialized services can capture higher margins and build stronger customer loyalty.

Trends in the Europe Last Mile Delivery Market

Sustainability-Driven Logistics

The last mile delivery sector in Europe is at the forefront of the green logistics movement, driven by stringent EU environmental regulations and growing consumer demand for eco-friendly options. Companies are rapidly transitioning their fleets to electric vehicles (EVs), deploying cargo bikes for city-center deliveries, and establishing urban micro-hubs to consolidate goods. This shift towards sustainability is not only a regulatory necessity but also a competitive differentiator, with companies increasingly marketing their green credentials. The trend is accelerating investment in charging infrastructure, alternative fuel technologies, and software to optimize routes for maximum efficiency and minimal emissions.

Rise of Omnichannel and Flexible Delivery

The lines between online and offline retail are blurring, leading to a surge in omnichannel logistics. Consumers now expect seamless options such as "click-and-collect," buy-online-return-in-store, and flexible, time-definite delivery windows. This trend forces retailers and logistics providers to integrate their inventory and delivery systems across all channels. The demand for flexibility also extends to delivery locations, with a rise in parcel lockers, neighborhood pickup points, and evening or weekend delivery slots, transforming the last mile into a highly customer-centric experience.

Europe Last Mile Delivery Market: Research Scope and Analysis

By Delivery Mode Analysis

Ground transportation is projected to dominate the delivery mode segment in the Europe Last Mile Market, holding the largest share in 2026. Its dominance is driven by the unparalleled flexibility and well-established infrastructure of road networks, which are essential for serving the dense and varied urban and suburban landscapes across the continent. Ground transportation, encompassing everything from vans and trucks to cargo bikes, remains the primary method for fulfilling the high volume of e-commerce, B2B, and B2C deliveries.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The extensive network of roads allows for direct, door-to-door service, which is critical for meeting consumer expectations for convenience and speed. While drone and autonomous vehicle segments are nascent, they represent emerging growth areas, with ground transportation continuing to be the operational backbone due to its reliability, cost-effectiveness for most delivery types, and ability to handle diverse cargo sizes. The ongoing investments in electric ground vehicles and urban logistics hubs further solidify this mode's dominant position.

By Vehicle Type Analysis

Light Commercial Vehicles (LCVs) are anticipated to dominate the vehicle type segment in the European market in 2026. LCVs, such as vans and small trucks, are the workhorses of last mile logistics due to their optimal balance of cargo capacity, maneuverability, and operational cost. Their size is ideal for navigating the narrow streets and traffic congestion common in European cities, while still offering sufficient space for the high volume of parcels and goods from e-commerce and retail deliveries. The increasing electrification of LCVs is also accelerating their adoption, as logistics providers seek to comply with urban low-emission zones and meet sustainability goals. Two-wheelers (including scooters and cargo bikes) are a fast-growing segment, particularly for food delivery and small parcels in dense urban cores, while Heavy Commercial Vehicles (HCVs) are more prevalent for bulk deliveries to distribution hubs and large businesses, not directly in the final consumer-facing leg.

By Service Type Analysis

The B2C (Business-to-Consumer) segment is projected to dominate the service type segment, driven by the unprecedented growth of e-commerce across Europe. The shift in consumer behavior towards online shopping for a vast array of products, from clothing and electronics to groceries, generates the largest volume of last mile deliveries. This segment is characterized by high parcel volumes, complex logistics due to delivery to individual residences, and intense pressure for fast, flexible, and transparent delivery options. The B2C segment's growth is also fueled by the proliferation of direct-to-consumer brands and the expansion of marketplaces. While B2B (Business-to-Business) remains a significant and stable segment, it is the sheer scale and continuous growth of B2C volumes that make it the dominant force in the market. The C2C (Consumer-to-Consumer) segment, driven by peer-to-peer marketplaces, is also growing but remains a smaller niche.

By Delivery Time Frame Analysis

Standard (2-5 days) delivery is projected to hold a leading position in the delivery time frame segment in 2026, as it continues to represent the backbone of e-commerce fulfillment for non-urgent, cost-conscious purchases. This delivery option offers the most cost-effective solution for both retailers and consumers, and it is widely used for a majority of online orders. However, the fastest-growing segments are same-day and next-day delivery, driven by consumer expectations for speed and convenience. The rise of on-demand culture, particularly in grocery and food delivery, has made same-day delivery a critical competitive battleground, especially in major metropolitan areas. While next-day delivery is rapidly becoming a standard expectation for a wide range of goods, standard delivery retains its leadership based on the sheer volume of orders for which rapid speed is not a primary requirement.

By Application Analysis

The E-commerce/Retail sector is projected to dominate the application segment in the European last mile market in 2026. This dominance is a direct reflection of the retail industry's fundamental transformation. E-commerce encompasses a massive range of product categories, generating the highest parcel volumes of any sector. Last-mile delivery is the critical, customer-facing component of the entire online retail experience. The efficiency, speed, and reliability of this final leg directly impact customer satisfaction and brand loyalty, making it a core strategic focus for retailers. The Grocery & Food Delivery segment is a significant and high-growth area, characterized by its demand for ultra-fast delivery times and specialized handling. The Healthcare & Pharmaceuticals segment, while smaller in volume, is critical due to its requirements for security, compliance, and cold chain integrity, representing a high-value niche with strong growth potential.

By End-User Analysis

Large Enterprises are projected to dominate the end-user segment in the European market, driven by the scale and complexity of their logistics needs. These organizations, including multinational retailers, large e-commerce platforms, and major corporations across various industries, handle massive daily shipment volumes. They require sophisticated, integrated, and often customized last mile solutions that can be deployed at scale across multiple regions. Large enterprises have the capital to invest in advanced technology, negotiate high-volume contracts with logistics providers, and maintain complex, multi-modal distribution networks. However, the Small and Medium Enterprises (SMEs) segment is a rapidly growing area. The surge in direct-to-consumer brands, artisan goods, and local online businesses has created a significant demand for scalable, flexible, and cost-effective last mile solutions tailored to the needs of smaller companies.

The Europe Last Mile Delivery Market Report is segmented on the basis of the following:

By Delivery Mode

- Ground Transportation

- Drone Delivery

- Autonomous Vehicles

- Others

By Vehicle Type

- Light Commercial Vehicles (LCVs)

- Two-Wheelers

- Heavy Commercial Vehicles (HCVs)

- Others

By Service Type

By Delivery Time Frame

- Next-day Delivery

- Same-day Delivery

- Standard (2-5 days)

By Application

- E-commerce/Retail

- Grocery & Food Delivery

- Healthcare & Pharmaceuticals

- Documents & Parcels

- Others

By End-User

- Retail Customers

- SMEs

- Large Enterprises

Impact of Artificial Intelligence in the Europe Last Mile Delivery Market

- Route Optimization: AI algorithms dynamically calculate optimal delivery routes by analyzing real-time traffic, weather, and order density, significantly reducing fuel consumption, delivery times, and operational costs for fleets.

- Demand Forecasting: Machine learning models accurately predict delivery volumes and consumer demand patterns, enabling logistics providers to optimize resource allocation, workforce planning, and inventory placement in urban micro-hubs.

- Enhanced Customer Experience: AI powers real-time tracking, personalized delivery windows, and proactive communication systems, giving customers precise visibility and control, which increases satisfaction and reduces failed delivery rates.

- Autonomous Operations: AI is the core technology enabling autonomous delivery vehicles, drones, and robotics, facilitating the development of cost-effective, scalable solutions that address persistent driver shortages.

- Predictive Fleet Maintenance: AI analyzes vehicle sensor data to predict mechanical failures before they occur, minimizing downtime, extending vehicle lifespan, and ensuring higher reliability for time-sensitive deliveries.

Europe Last Mile Delivery Market: Regional Analysis

The European last mile delivery market exhibits distinct regional characteristics shaped by varying economic conditions, infrastructure maturity, and regulatory frameworks. Western Europe, led by Germany, France, and the Benelux countries, represents the most mature and competitive market. These nations benefit from advanced logistics infrastructure, high e-commerce penetration, and strong regulatory emphasis on sustainability. Germany, as Europe's largest economy, serves as a central logistics hub, while France and the Netherlands leverage their strategic positions for cross-border distribution. The region leads in electric vehicle adoption and micro-hub development.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Northern Europe, including the UK, Sweden, and Denmark, demonstrates exceptionally high consumer demand for rapid delivery services, with same-day and next-day options becoming standard expectations. These markets are at the forefront of sustainable urban logistics innovation. Southern Europe Italy, Spain, and Portugal is experiencing accelerated growth driven by increasing e-commerce adoption and infrastructure modernization. The region presents significant expansion opportunities as digital transformation progresses.

Eastern Europe, encompassing Poland, Czech Republic, and Hungary, represents the fastest-growing segment, fueled by rising disposable incomes, expanding e-commerce, and substantial EU-funded infrastructure investments. These emerging markets offer attractive growth potential for logistics providers seeking to expand their footprint across the continent.

By Region

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Europe Last Mile Delivery Market: Competitive Landscape

The competitive landscape of the Europe Last Mile Delivery Market is characterized by a mix of global logistics giants, national postal operators, specialized couriers, and a wave of innovative tech-enabled startups. Major players like DHL Group, Geopost (DPDgroup), Amazon Logistics, and La Poste Group dominate with their extensive networks, scale, and diversified service portfolios. Competition is intense, with players vying for market share through service differentiation, technological innovation, and strategic partnerships. A key battleground is sustainability, with companies heavily promoting their green fleets and carbon-neutral delivery options. The rise of platform-based, crowdsourced delivery models is introducing a new layer of competition, particularly for on-demand services like food and grocery delivery. Mergers, acquisitions, and strategic alliances are common strategies for expanding geographical reach, acquiring new technology, and strengthening market positions. While the market leaders hold significant sway, there is ample space for niche players specializing in areas like cold chain, heavy goods, or hyper-local deliveries.

Some of the prominent players in the Europe Last Mile Delivery Market are:

- DHL Group

- United Parcel Service Inc.

- FedEx Corporation

- Amazon.com Inc.

- La Poste Group

- DPDgroup

- Royal Mail

- Deutsche Post DHL

- PostNL

- GLS Group

- Mondial Relay

- XPO Logistics

- GEODIS

- InPost

- Hermes Europe

- Seven Senders

- Urbantz

- Woop

- LogiNext

- Kerry Logistics Network Limited

- Other Key Players

Recent Developments in the Europe Last Mile Delivery Market

- October 2024: DHL Group announced a major expansion of its electric vehicle fleet across major European cities, investing to deploy 5,000 new electric vans and cargo bikes, aiming to reduce its carbon footprint in urban logistics.

- September 2024: Geopost (DPDgroup) launched a new autonomous drone delivery pilot program in a rural region of France, focusing on delivering urgent medical supplies and spare parts, demonstrating the potential for alternative delivery modes in hard-to-reach areas.

- August 2024: Amazon Logistics began testing a fleet of autonomous delivery robots for sidewalk deliveries in select neighborhoods in Germany and the UK, marking a significant step in the commercial application of this technology for last mile e-commerce.

- November 2023: InPost announced the installation of over 5,000 new automated parcel lockers across Southern Europe, expanding its out-of-home delivery network and offering consumers a convenient and secure alternative to home delivery.

- July 2023: Royal Mail unveiled a cloud-based, AI-powered route optimization platform for its delivery network, leveraging big data and machine learning to dynamically adjust delivery routes, reduce fuel consumption, and improve operational efficiency.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 45.9 Bn |

| Forecast Value (2035) |

USD 87.8 Bn |

| CAGR (2026–2035) |

7.5% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Component (Solutions and Services), By Size (Small & Medium-sized Enterprises and Large Enterprises), By Industry Vertical (Public Sector, Pharmaceuticals, Media & Entertainment, IT & Telecommunication, BFSI, and Others Industry Verticals), By Delivery Mode (Ground Transportation, Drone Delivery, Autonomous Vehicles, and Others), By Vehicle Type (Light Commercial Vehicles, Two-Wheelers, Heavy Commercial Vehicles, and Others), By Service Type (B2C, B2B, and C2C), By Delivery Time Frame (Next-day Delivery, Same-day Delivery, and Standard [2–5 days]), By Application (E-commerce/Retail, Grocery & Food Delivery, Healthcare & Pharmaceuticals, Documents & Parcels, and Others), and By End-User (Retail Customers, SMEs, and Large Enterprises) |

| Regional Coverage |

Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe |

| Prominent Players |

DHL Group, United Parcel Service Inc., FedEx Corporation, Amazon.com Inc., La Poste Group, DPDgroup, Royal Mail, Deutsche Post DHL, PostNL, GLS Group, Mondial Relay, XPO Logistics, GEODIS, InPost, Hermes Europe, Seven Senders, Urbantz, Woop, LogiNext, Kerry Logistics Network Limited, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Europe Last Mile Delivery Market?

▾ The Europe Last Mile Delivery Market size is estimated to have a value of USD 45.9 billion in 2026 and is expected to reach USD 87.8 billion by the end of 2035.

Who are the key players in the Europe Last Mile Delivery Market?

▾ Some of the major key players in the Europe Last Mile Delivery Market are DHL Group, Amazon Logistics, La Poste Group, Royal Mail, DB Schenker, Geopost (DPDgroup), GLS, and many others.

What is the growth rate in the Europe Last Mile Delivery Market?

▾ The market is growing at a CAGR of 7.5 percent over the forecasted period.