Market Overview

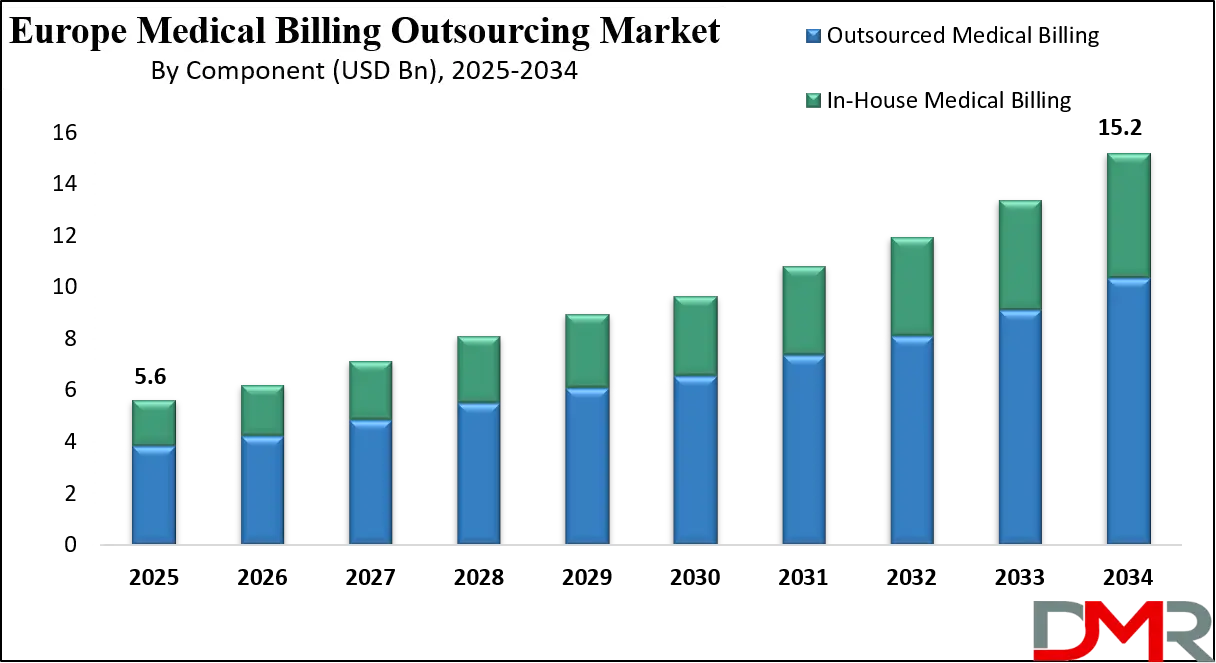

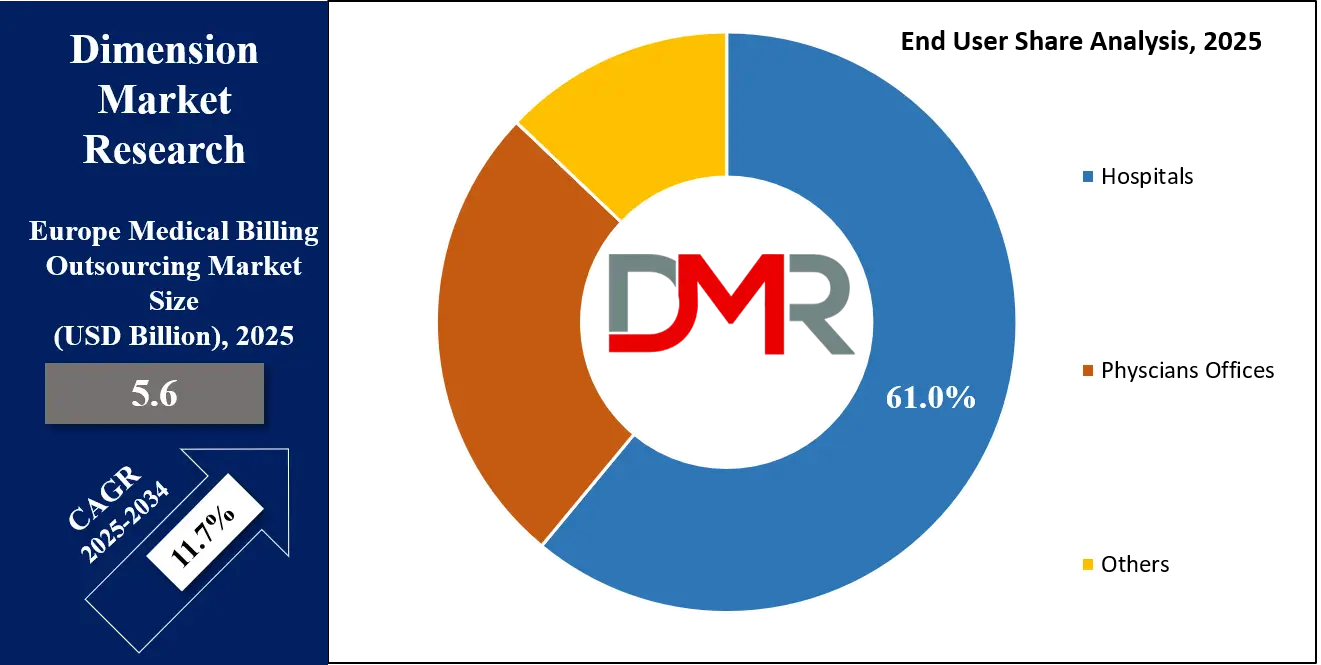

The Europe Medical Billing Outsourcing Market size is projected to reach USD 5.6 billion in 2025 and grow at a compound annual growth rate of 11.7% from there to reach a value of USD 15.2 billion in 2034.

The Europe medical billing market centers on the services and technologies that manage and streamline the billing process for healthcare providers across Europe—covering activities from patient registration, insurance verification, coding, claims processing, through to payment posting and account receivables. At its core, medical billing refers to submitting and following up on healthcare provider claims to insurance companies or payers for reimbursement of services delivered. The European ecosystem includes public hospitals, physician practices, and outsourced billing service providers, all supported by digital healthcare transformation and regulatory initiatives.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Over recent years, this market has been shaped by increasing complexity in payer systems, rising administrative cost pressures in national health systems, and a growing push by providers to outsource non‑core administrative tasks to specialist vendors. For instance, many European providers are shifting from in‑house billing operations toward outsourced models to gain efficiency and allow clinical staff to focus on care delivery.

The key developments include the migration toward cloud‑based billing platforms, integration with electronic health records (EHRs), and the adoption of advanced coding and denial‑management workflows. This technology adoption is enabling faster claim submission, lower error rates and improved revenue cycle metrics. As European healthcare systems increasingly emphasize cost‑effectiveness and value‑based care, medical billing solutions are becoming central to ensuring cash flow, regulatory compliance and operational efficiency.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Looking ahead, the European medical billing market is expected to evolve with stronger outsourcing partnerships, richer automation, and greater use of analytics and AI‑enabled processes. These changes promise to reduce billing cycle times, improve reimbursement accuracy and support providers in meeting regulatory, data‑privacy and interoperability requirements — thereby reinforcing the importance of medical billing as a strategic administrative service in European healthcare.

Europe Medical Billing Outsourcing Market: Key Takeaways

- Market Growth: The Europe Medical Billing Outsourcing Market size is expected to grow by USD 9.0 billion, at a CAGR of 11.7%, during the forecasted period of 2026 to 2034.

- By Component: The outsource medical billing segment is anticipated to get the majority share of the Europe Medical Billing Outsourcing Market in 2025.

- By End User: The Hospitals segment is expected to get the largest revenue share in 2025 in the Europe Medical Billing Outsourcing Market.

- Use Cases: Some of the use cases of Medical Billing Outsourcing includes process optimization, predictive modeling & simulation, and more.

Europe Medical Billing Outsourcing Market: Use Cases

- Patient registration & insurance verification – Automating patient demographic capture and payer eligibility checks, enabling faster claim submission and reduced billing delays.

- Coding & charge entry services – Specialist teams perform accurate medical coding (ICD, CPT) and charge capture, ensuring proper claim documentation and minimizing denials.

- Claims processing & payment posting – End‑to‑end handling of claim submission, tracking, appeals and payment‑posting to streamline the revenue cycle for providers.

- Denial management & accounts receivable (A/R) follow‑up – Monitoring rejected or unpaid claims, implementing corrective actions, and driving faster resolution and cash collection.

Stats & Facts

- In Europe’s healthcare systems, administrative and non‑clinical overhead in many countries accounts for around 8‑10% of total healthcare spending.

- In Germany alone, outsourced medical billing is the largest component segment and the country is projected to lead the regional European outsourcing market.

- According to regulatory and industry analysis, the migration of European healthcare providers to cloud‑based billing software is accelerating, particularly in Germany, UK and France.

Market Dynamic

Driving Factors in the Europe Medical Billing Outsourcing Market

Rising complexity in billing & reimbursement processes

European healthcare providers face increasingly complex payer systems, multi‑payer environments, and tighter compliance requirements. This complexity is driving demand for specialised billing services and outsourcing models, as providers seek to reduce in‑house administrative burdens and shore up cash flow. The need to manage coding accuracy, claim denials, and diverse insurance rules is pushing adoption of third‑party billing vendors and automated platforms.

Digital transformation and cloud adoption in healthcare

As European healthcare systems increasingly digitise, medical billing is following suit with cloud‑based platforms, integrated EHR‑billing systems and analytics‑driven workflows. This shift supports faster claims submission, improved compliance (including GDPR and healthcare data regulations), and lower costs of ownership for providers. The digital push is creating a favourable environment for forward‑looking billing service providers and technology vendors.

Restraints in the Europe Medical Billing Outsourcing Market

Fragmented healthcare systems and regulatory heterogeneity

Europe consists of multiple national healthcare systems, each with different reimbursement rules, coding standards, data‑privacy laws and languages. This fragmentation increases implementation complexity and cost for pan‑European billing service providers, slowing standardisation and scale.

Reluctance of providers to outsource critical functions

Some hospitals and physician practices still prefer to retain in‑house billing operations due to concerns over data security, loss of control, vendor reliability and regulatory compliance. This resistance limits the penetration of outsourced models and slows the pace of transition toward managed billing services across the region.

Opportunities in the Europe Medical Billing Outsourcing Market

Expansion of outsourcing and managed services models

As providers aim to focus on care delivery rather than administrative tasks, there is growing opportunity for billing service providers to offer full‑service outsourcing — from front‑end registration through to denial management. European providers under cost pressure are increasingly open to outsourcing non‑core processes, creating a growth runway.

Automation, analytics & AI‑enabled billing workflows

With advances in machine learning and analytics, billing vendors can deliver smarter services: predictive denial prevention, automated coding and real‑time revenue cycle analytics. This creates opportunity to differentiate via technology and deliver improved outcomes for providers, lower error rates and faster cash conversion.

Trends in the Europe Medical Billing Outsourcing Market

Cloud and SaaS‑based billing platforms gaining traction

A growing trend in Europe is moving from on‑premises billing systems to cloud‑based or SaaS billing platforms which offer scalability, easier updates and lower upfront cost. This enables providers of all sizes (hospitals, physician offices) to adopt advanced billing capabilities without large capital investment.

Geographical outsourcing diversification & cost optimisation

Service providers are increasingly looking to Eastern European countries (e.g., Poland, Romania) to deliver cost‑efficient billing services for Western Europe, leveraging multilingual staff, lower wage costs and strong regulatory frameworks. This pan‑European service delivery model is becoming more common.

Impact of Artificial Intelligence in Europe Medical Billing Outsourcing Market

- Automated coding and claim submission – AI engines can analyse clinical documentation and assign correct billing codes, reducing manual errors and speeding up claim submission.

- Predictive denial analytics – Machine learning models can identify claims at high risk of rejection and suggest corrective actions or documentation improvements before submission.

- Revenue cycle optimisation – AI‑driven dashboards and algorithms enable providers to monitor billing bottlenecks in real time, forecast cash flow and prioritise accounts receivable follow‑up.

- Automated patient registration & eligibility verification – Intelligent systems can auto‑validate patient demographics, insurance status and payer rules, reducing front‑end delays and errors.

- Chatbots and virtual assistants for billing queries – AI‑powered interfaces can handle routine billing questions from patients or providers, freeing up human staff to focus on complex cases and improving patient experience.

Research Scope and Analysis

By Component Analysis

Outsourced Medical Billing is the leading segment in the component category, accounting for approximately 68% of the European market share in 2025. The continued dominance of this segment stems from the growing preference of healthcare providers to delegate complex billing operations to third-party vendors. These vendors offer specialised expertise, scalable technologies, and compliance with regional regulatory frameworks, helping providers improve billing accuracy, reduce claim denials, and ensure timely reimbursements. With rising administrative burdens and the need for operational efficiency, outsourcing remains a strategic choice, especially among large hospitals and healthcare systems.

In-house Medical Billing, while a smaller segment, is emerging as the fastest-growing component in the market. This trend is particularly noticeable among smaller clinics and physician offices that are adopting user-friendly billing software and automation tools. These organisations aim to retain control over billing workflows while lowering costs associated with external vendors. The flexibility offered by cloud-based systems and EHR-integrated platforms is enabling this shift. Despite slower overall growth compared to outsourcing, this segment reflects the decentralised needs of independent practices across Europe.

By Service Type Analysis

Front-End Services lead the service type segmentation, with an estimated 42% market share in 2025. These services include patient registration, insurance verification, and prior authorization — all of which form the foundation of the billing process. Errors at this stage often lead to claim rejections and delayed payments, making accuracy and automation here a priority. As a result, healthcare organisations are increasingly investing in technologies and services that optimise front-end workflows to reduce downstream revenue leakage and administrative overhead.

Back-End Services represent the fastest-growing category, covering functions such as accounts receivable management, denial management, payment posting, and patient statements. With rising volumes of medical claims, complex payer rules, and increasing scrutiny of denied claims, providers are placing greater emphasis on robust back-end capabilities. The integration of analytics, AI-powered tracking, and automated follow-up processes is fuelling this segment’s expansion, particularly among providers looking to shorten revenue cycles and boost collection rates.

By End User Analysis

Hospitals are the leading end-user segment in the Europe medical billing market, commanding about 61% market share in 2025. These institutions generate high volumes of medical claims across multiple departments and service lines, making efficient billing operations critical. Hospitals also deal with multi-payer systems and stringent compliance requirements, leading to increased adoption of comprehensive billing solutions — both outsourced and in-house. Their focus on reducing administrative burdens while maintaining compliance continues to drive strong demand in this segment.

Physician Offices, though a smaller segment, are witnessing the fastest growth due to shifting market dynamics. Smaller practices are increasingly adopting digital billing tools, EHR-integrated platforms, and even partial outsourcing to handle complex insurance requirements. As these providers face mounting pressure to reduce costs and improve operational agility, they are moving away from traditional billing methods. This transformation is especially noticeable in private practices and outpatient specialty clinics across the region.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Europe Medical Billing Outsourcing Market Report is segmented on the basis of the following:

By Component

- Outsourced Medical Billing

- In-house Medical Billing

By Service Type

- Front-End Services

- Patient Registration

- Insurance Verification

- Prior Authorization

- Middle-End Services

- Medical Coding

- Charge Entry

- Claims Processing

- Back-End Services

- Accounts Receivable Management

- Denial Management

- Payment Posting

- Patient Statements

By End User

- Hospitals

- Physician Offices

- Others

European Countries Analysis

Within Europe, national healthcare systems vary significantly in structure, reimbursement practices and administrative overheads — making country‑level analysis vital. Germany remains the largest market for medical billing services in Europe, supported by a complex multi‑payer system, high administrative cost pressures and the largest number of hospitals and physician practices. The UK and France also feature prominently, with strong private healthcare sectors, growing billing outsourcing adoption and mature digital health infrastructures.

Meanwhile, countries such as Italy, Spain and parts of Eastern Europe (Poland, Romania) are exhibiting faster growth in outsourced billing services as younger healthcare infrastructure, regulatory reforms and cost cutting drive adoption. Overall, the European landscape is characterised by a mix of mature markets and emerging outsourcing hubs, enabling service providers to operate pan‑regionally with multilingual capabilities and regulatory compliance.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Region

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Competitive Landscape

Within Europe, national healthcare systems vary significantly in structure, reimbursement practices and administrative overheads making country‑level analysis vital. Germany remains the largest market for medical billing services in Europe, supported by a complex multi‑payer system, high administrative cost pressures and the largest number of hospitals and physician practices. The UK and France also feature prominently, with strong private healthcare sectors, growing billing outsourcing adoption and mature digital health infrastructures.

Meanwhile, countries such as Italy, Spain and parts of Eastern Europe (Poland, Romania) are exhibiting faster growth in outsourced billing services as younger healthcare infrastructure, regulatory reforms and cost cutting drive adoption. Overall, the European landscape is characterised by a mix of mature markets and emerging outsourcing hubs, enabling service providers to operate pan‑regionally with multilingual capabilities and regulatory compliance.

Some of the prominent players in the Europe Medical Billing Outsourcing Market are:

- R1 RCM

- Optum

- Conifer Health Solutions

- athenahealth

- Veradigm

- Experian Health

- CareCloud

- AGS Health

- Omega Healthcare

- GeBBS Healthcare Solutions

- Access Healthcare

- Sutherland

- Firstsource

- WNS Global Services

- EXL Service

- Genpact

- Cognizant

- Accenture

- Tata Consultancy Services (TCS)

- Wipro

- HCLTech

- NTT DATA

- Other Key Players

Recent Developments

- In April 2025, Knack RCM announced the acquisition of PPM Partners (a U.S.‑based specialist in anesthesia revenue‑cycle management), strengthening its footprint in specialty medical billing and claims services.

- In February 2025, Machinify, Inc., a provider of AI-powered healthcare payment solutions, was acquired by New Mountain Capital in a strategic deal aimed at integrating the platform into broader revenue-cycle management offerings.

Report Details

| Report Characteristics |

| Market Size (2025) |

USD 5.6 Bn |

| Forecast Value (2034) |

USD 15.2 Bn |

| CAGR (2025–2034) |

11.7% |

| Historical Data |

2019 – 2023 |

| Forecast Data |

2026 – 2034 |

| Base Year |

2024 |

| Estimate Year |

2025 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors, etc. |

| Segments Covered |

By Component (Outsourced Medical Billing and In-house Medical Billing), By Service Type (Front-End Services, Middle-End Services, and Back-End Services), By End User (Hospitals, Physician Offices, and Others)

|

| Regional Coverage |

Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe |

| Prominent Players |

R1 RCM, Optum, Conifer Health Solutions, athenahealth, Veradigm, Experian Health, CareCloud, AGS Health, Omega Healthcare, GeBBS Healthcare Solutions, Access Healthcare, Sutherland, Firstsource, WNS Global Services, EXL Service, Genpact, Cognizant, Accenture, Tata Consultancy Services (TCS), Wipro, HCLTech, NTT DATA, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days, and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Europe Medical Billing Outsourcing Market?

▾ The Europe Medical Billing Outsourcing Market size is expected to reach a value of USD 5.6 billion in 2025 and is expected to reach USD 15.2 billion by the end of 2034.

Who are the key players in the Europe Medical Billing Outsourcing Market?

▾ Some of the major key players in the Europe Medical Billing Outsourcing Market are TCS, HCL, Wipro, and others

What is the growth rate in Europe Medical Billing Outsourcing Market?

▾ The market is growing at a CAGR of 11.7 percent over the forecasted period.