What is the Fluoropolymer Alternatives Market Size?

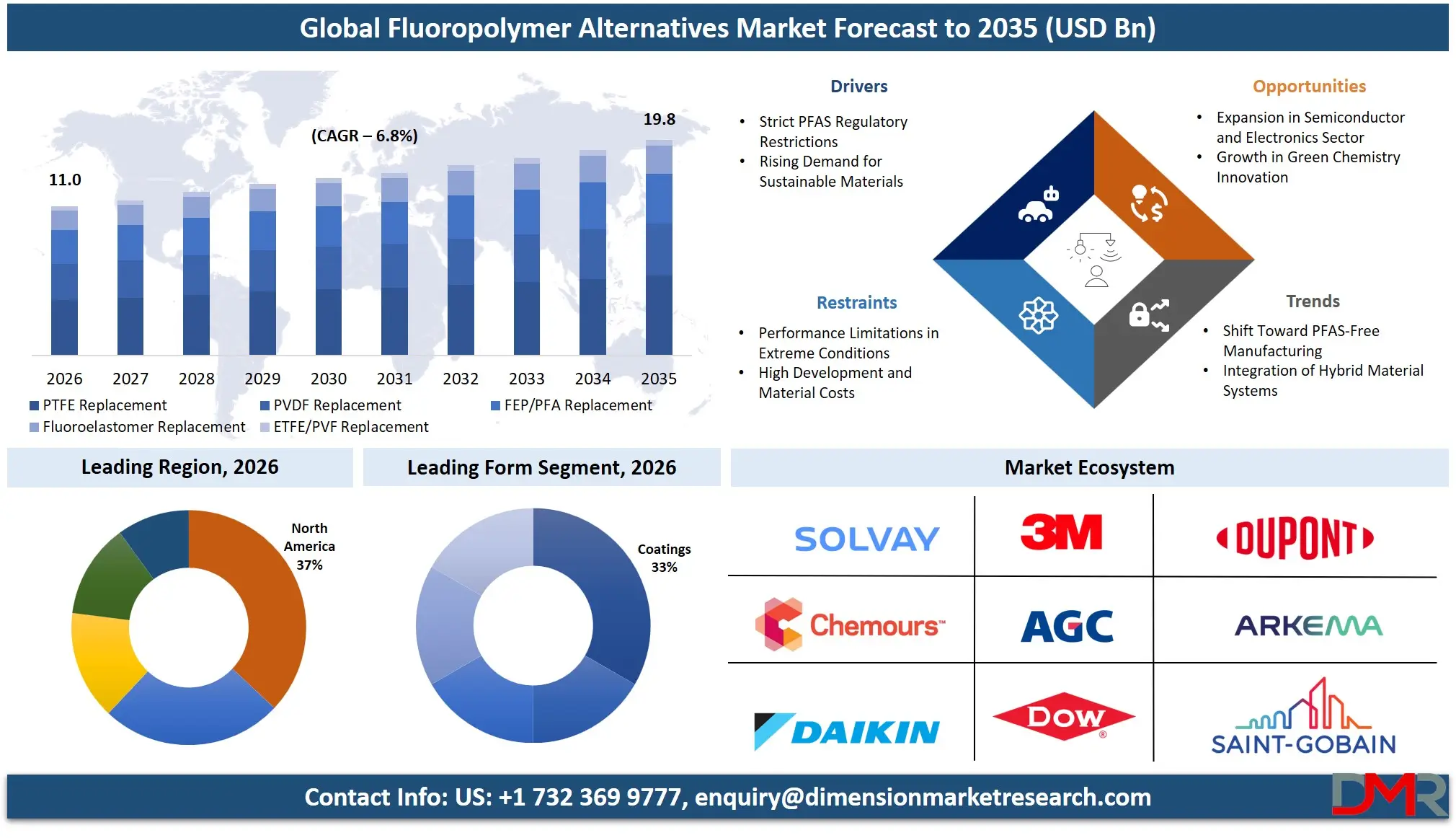

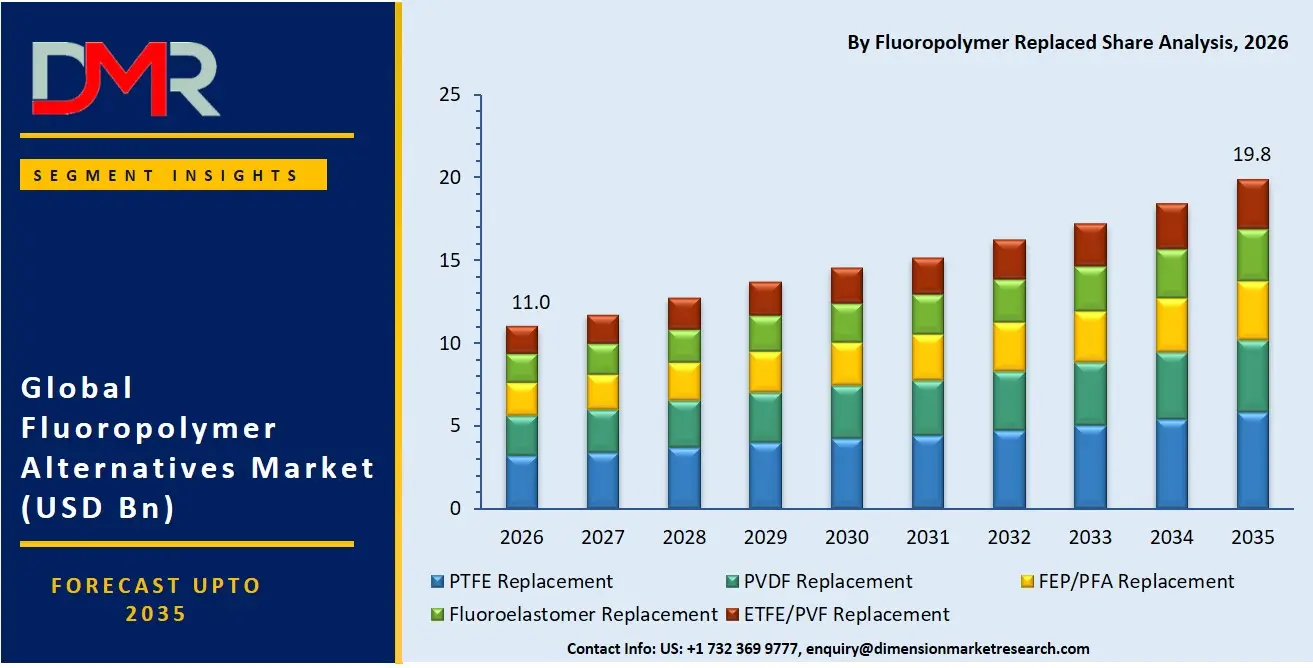

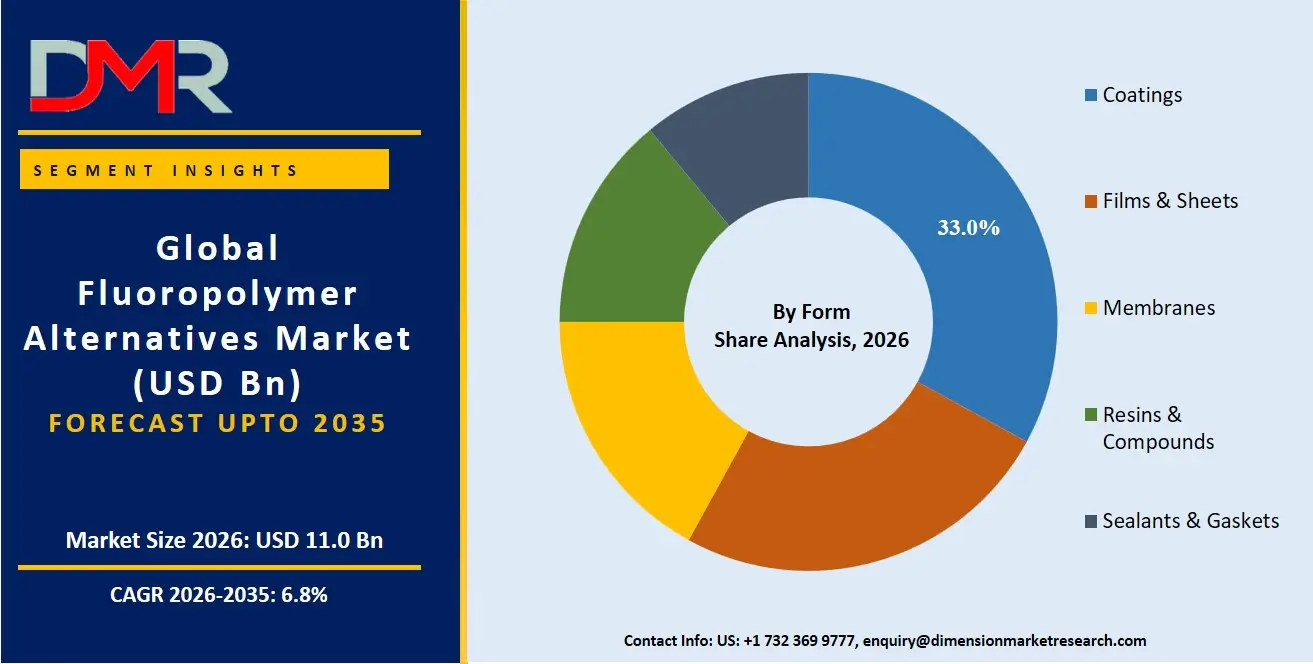

The Fluoropolymer Alternatives Market size is expected to be USD 11.0 billion in 2026 and increase at a compound annual growth rate of 6.8% to USD 19.8 billion in 2035 due to increasing demand for regulations from governmental organizations against PFAS chemicals.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The fluoropolymer alternatives market comprises state-of-the-art products designed for use in an industrial setting and that may serve as a replacement for conventional fluoropolymers like PTFE, PVDF, and FEP. The fluoropolymer alternatives market encompasses silicone-based products, polyolefin-based products, engineering thermoplastics, thermoplastic elastomers, biodegradable products, and ceramic formulations. The growth of this market is driven by growing PFAS compound regulations and sustainability issues in certain industries. Some of the market trends include PFAS-free products, biodegradable products, and advanced polymers.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

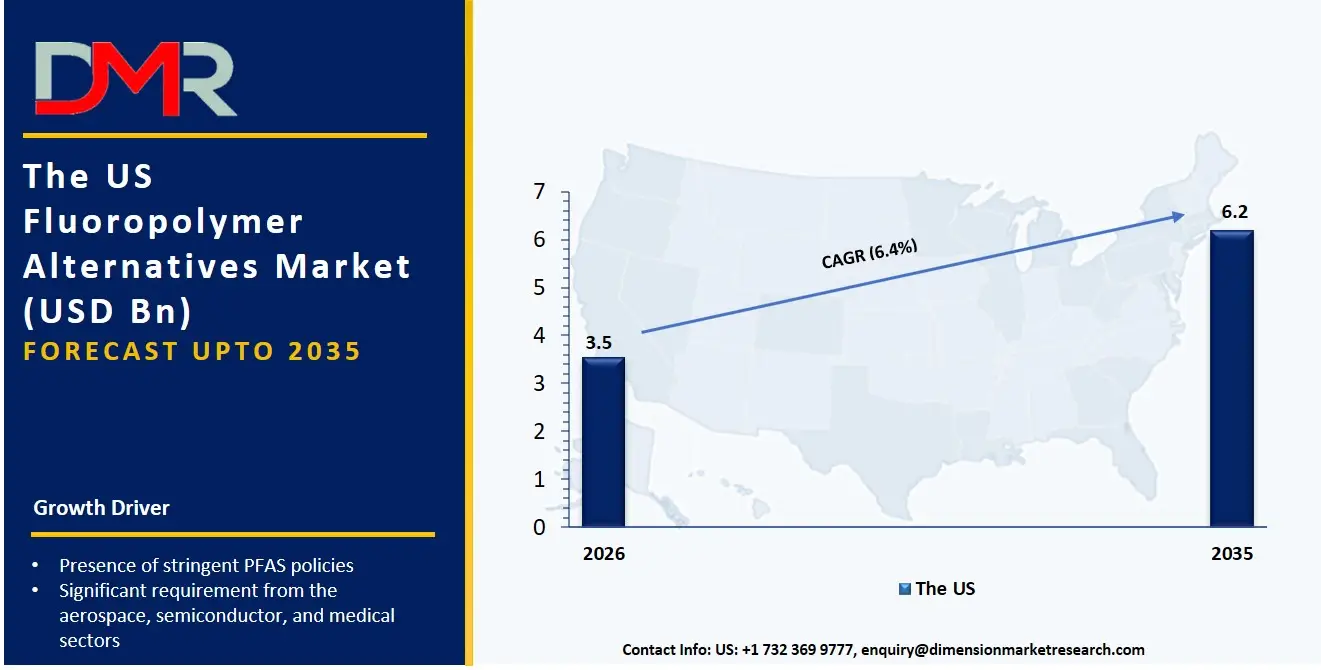

The US Fluoropolymer Alternatives Market

The US Fluoropolymer Alternatives Market size is estimated to be USD 3.5 billion in 2026 and is expected to increase at a CAGR of 6.4% over the forecast period.

The U.S. represents an advanced market, where the presence of stringent PFAS policies, along with a significant requirement from the aerospace, semiconductor, and medical sectors, acts as major drivers. Government organizations like the Environmental Protection Agency are imposing stringent policies encouraging the use of non-PFAS fluoropolymers in products. A large amount of research expenditure, expertise in materials science, and robust industry presence have fast-tracked the process of adoption.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Europe Fluoropolymer Alternatives Market

The Europe Fluoropolymer Alternatives Market size is estimated to be USD 3.0 billion in 2026 and is expected to increase at a CAGR of 6.1% over the forecast period.

In the Europe market, key factors impacting innovation are the European Green Deal and restrictions on harmful substances via REACH laws that include restrictions on fluorinated substances. The sectors adopting innovative practices in these regards include automotive, chemicals, and packaging. Incentives for innovation come from environmental regulations and circular economy practices. Rapid adoption occurs mainly in Western Europe, especially in Germany, France, and the Nordic countries.

Japan Fluoropolymer Alternatives Market

The market size of Japan Fluoropolymer Alternatives will be USD 550 million in 2026 and at a CAGR of 6.7% in the forecast period.

There are opportunities for the Japan market owing to the high demand in the electronics, automobile, and precision manufacturing industries. Japan places a premium on high-performance engineering materials as well as environmental compliance. There are government policies promoting green chemistry and innovation in the industry that are driving the substitution process. The drawbacks are the cost involved in developing engineering materials and their stringent performance specifications.

Key Takeaways

- Market Size & Forecast: The Fluoropolymer Alternatives Market size is projected to reach USD 11.0 billion in 2026 and is anticipated to have a value of USD 19.8 billion in 2035.

- Growth Rate & Outlook: The Fluoropolymer Alternatives Market size is set to grow at a compound annual growth rate of 6.8% during the forecast period of 2026 to 2035.

- Primary Growth Drivers: Some of the major growth drivers in the market include Strict Regulations Against PFAS Compounds, and more.

- Key Market Trends: Some of the major trends in the market are Implementation of Change to PFAS-Free Manufacturing and more.

- By Form: The coatings segment is anticipated to get the majority share of the Fluoropolymer Alternatives market in 2026.

- By Fluoropolymer Replaced: The PTFE Replacement segment is expected to get the largest revenue share in 2026 in the Fluoropolymer Alternatives market.

- By End User Industry: The electronics & semiconductor segment is expected to get the largest revenue share in 2026 in the Fluoropolymer Alternatives market.

- Regional Leadership: North America is set to lead the Fluoropolymer Alternatives market with an estimated 37.0% share in 2026.

What is the Fluoropolymer Alternatives?

Fluoropolymer alternatives are products that have been developed as substitutes for fluoropolymers and PFASs in various industrial processes and consumer goods. The main objective of these products is to provide the same characteristics such as chemical resistance, thermal stability, low friction, and efficient processing in a manner that considers environmental issues, health, and regulatory requirements. The alternatives include silicone additives, polyolefin-based materials, bio-based products, ceramic coatings, and others in different industries.

Use Cases

- Chemical Processing Equipment: Polymer-based alternatives can be applied for pipelines, sealing, and coating to prevent corrosion without increasing PFAS utilization in chemical processing facilities.

- Electronic and Semiconductors: Polymer-based alternatives can act as insulators and offer thermal stability in semiconductor manufacturing where extremely clean and highly functional polymers are required.

- Medical Devices: Polymer-based alternatives that are biocompatible can be used for tubing, implants, and coating applications while complying with regulations against fluorinated polymers.

- Automotive Components: Polymer-based alternatives that are lightweight can be used for fuel line components, wiring insulation, and coating applications.

How AI Is Transforming the Fluoropolymer Alternatives Market

AI is becoming increasingly influential in facilitating faster innovation of fluoropolymer substitutes because of its ability to simulate materials, predict properties, and optimize chemical formulas within a shorter time frame. This technology enables scientists to discover new non-fluorinated formula compounds much faster than conventional methods. AI can also assist in predicting essential attributes of materials such as durability, chemical resistance, thermal stability, and environmental impact prior to mass production.

During manufacturing processes, AI is helping companies boost efficiency levels by optimizing production processes, minimizing wastage, and ensuring scalability. In addition, AI helps companies reduce manufacturing costs and maintain material consistency. Besides production, AI can also enhance supply chain management through demand prediction, inventory control, logistics optimization, and operational monitoring.

Market Dynamic

Driving Factors in the Fluoropolymer Alternatives Market

Strict Regulations Against PFAS Compounds

The increasing demand for regulations from governmental organizations against PFAS chemicals represents another significant push factor behind the emergence of alternative materials based on fluoropolymers. The governments' attempts to introduce various bans, limitations, and regulation procedures are driving industries such as chemicals manufacturing, electronic devices production, and textiles to switch to environmentally friendly material systems. Companies have been working hard on researching and developing innovative high-quality substitutes that can perform similarly but comply with stricter regulation policies.

Restraints in the Fluoropolymer Alternatives Market

Constraints on Performance in Extreme Conditions

One such constraint includes the fact that although there may be various alternatives to fluoropolymer materials that may not be able to provide the same high levels of chemical, thermal, and abrasion resistance shown by traditional fluoropolymer materials, there is definitely some performance constraints in terms of extreme conditions such as in semiconductor processing or in aggressive chemical reactions.

Opportunities in the Fluoropolymer Alternatives Market

Expanding Opportunities in the Semiconductor and Electronics Industry

The semiconductor sector offers a promising prospect in that there is a rising demand for high-end PFAS-free materials. Fluoropolymer substitutes have been developed for applications in insulation, wafer fabrication, and clean room environments. There is a fast-growing need for electronics used in AI, EVs, and 5G infrastructure, which means that those who produce high-quality and thermally-stable materials will benefit from their market share.

Trends in the Fluoropolymer Alternatives Market

Change to PFAS-Free Manufacturing

A significant trend is the worldwide move to PFAS-free manufacturing. Businesses are altering their manufacturing procedures to remove fluorine-containing chemicals from their products. The move is being propelled by regulation, environmental sustainability concerns, and corporate ESG policies. Industries are moving towards using safer materials for coating, filtration, and sealing that maintain functionality without posing health risks.

Research Scope and Analysis

The research scope of Fluoropolymer Alternatives Market is the detailed analysis based on the kind of alternative material, fluoropolymer substitute, form, application, and end-user industry across the key geographic regions of the world. Some of the factors considered while conducting this research are demand drivers, regulation effects, innovations in technology, sustainability practices, and others that affect the growth of the market.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Alternative Material Type Analysis

Engineered Thermoplastics occupy the top spot with a projected market share of about 31% in 2026 because of the outstanding performance characteristics of these materials regarding strength, heat resistance, and versatile use. Engineering plastics like PEEK and polyimides are popular in electronics and chemicals sectors, thus propelling their market leadership. Silicone elastomers come next, owing to their versatility and thermal stability. The most promising emerging category of engineered materials is that of biodegradable & PFAS-free, which can be attributed to legal regulations. Growing investments in green chemistry and circular economy concepts are helping this category gain momentum.

By Fluoropolymer Replaced Analysis

PTFE-based substitutes have a projected market share of 29% in 2026 owing to the growing importance of alternative products for non-stick surfaces, seals, and industrial goods. The strong regulation against PFAS chemicals is one of the driving forces. PVDF substitutes are the fastest growing category, attributed to high demands for such alternatives in batteries and energy storage systems. Alternatives to FEP and PFA are witnessing growth in the semiconductor and electronics sector owing to the requirement for high-purity raw materials.

By Form Analysis

Coatings have the largest market share, estimated at 33% in 2026, owing to their application in corrosion resistance, nonstick coating, and protective applications in the industry. Films and sheets have been experiencing robust growth on account of their application in the electronics and packaging industry. Membranes are increasingly becoming popular in filtration and water treatment applications. Resins and compounds find extensive applications in manufacturing engineered parts. Sealants and gaskets continue to be indispensable in automotive and chemical processing industries.

By Application Analysis

Applications of non-stick & surface protection occupy the highest market share, contributing to 35% of the global market in 2026, on account of the use of these polymers in cookware and machinery protection. Applications like chemical process equipment occupy the third-largest market share on account of their corrosion resistance properties. Semiconductors and battery energy storage components are some of the fastest-growing segments owing to the rise in the demand for alternative materials for AI hardware, EVs, and others.

By End User Industry Analysis

The largest market share belongs to electronics & semiconductors, contributing 34%, owing to the need for efficient insulating properties and environmentally friendly production material. The largest market growth will be experienced in the automotive & transportation industry, attributed to the growing demand for electric vehicle usage. Another reason why chemical processing will maintain its position as an important end-use industry is because of the material's resistance to corrosion. The healthcare sector will grow due to the increased use of biocompatible material.

The Fluoropolymer Alternatives Market Report is segmented on the basis of the following:

By Alternative Material Type

- Silicone-Based Materials

- Silicone elastomers

- Silicone coatings

- Polysiloxanes

- Polyolefin-Based Materials

- Polyethylene (PE)

- Polypropylene (PP)

- UHMWPE

- Engineering Thermoplastics

- PEEK

- PPS

- Polyimides (PI)

- Polyamides (PA)

- Thermoplastic Elastomers (TPEs)

- Bio-Based & PFAS-Free Materials

- Bio-based coatings

- Cellulose-based materials

- Bio-surfactants

- Ceramic & Hybrid Materials

- Ceramic coatings

- Sol-gel coatings

- Polymer composites

By Fluoropolymer Replaced

- PTFE Replacement

- PVDF Replacement

- FEP/PFA Replacement

- Fluoroelastomer Replacement

- ETFE/PVF Replacement

By Form

- Coatings

- Films & Sheets

- Membranes

- Resins & Compounds

- Sealants & Gaskets

By Application

- Non-Stick & Surface Protection

- Chemical Processing Components

- Wire & Cable Insulation

- Membranes & Filtration

- Semiconductor Components

- Packaging Barriers

- Medical Components

- Textile Finishing

- Battery & Energy Storage Components

By End-Use Industry

- Electronics & Semiconductors

- Automotive & Transportation

- Chemical Processing Industry

- Energy & Power

- Healthcare & Medical

- Food & Beverage Processing

- Textiles

- Packaging

- Industrial Manufacturing

Regional Analysis

Leading Region in the Fluoropolymer Alternatives Market

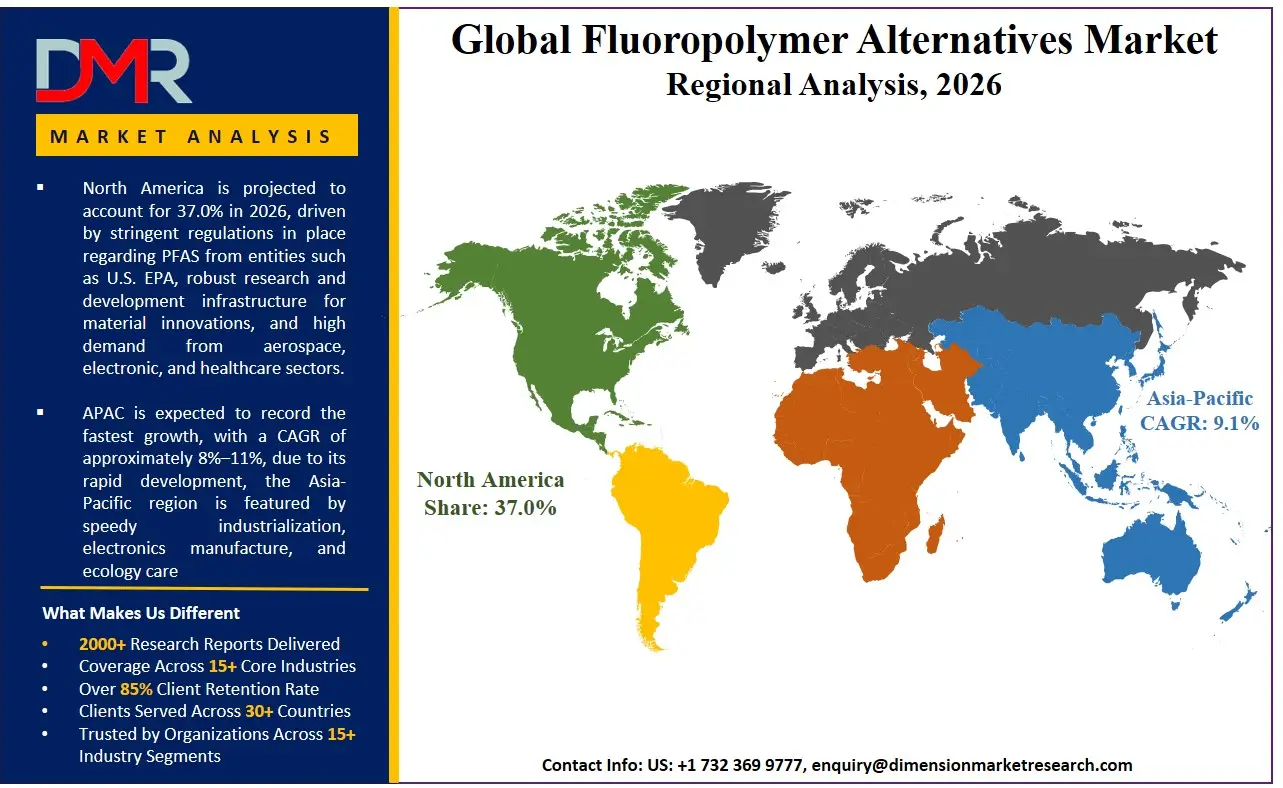

North America occupies the top spot with a market share of around 37% globally in 2026 owing to stringent regulations in place regarding PFAS from entities such as U.S. EPA, robust research and development infrastructure for material innovations, and high demand from aerospace, electronic, and healthcare sectors. North America has a highly developed innovation ecosystem and receives substantial venture capital investments for material innovation. In addition, there is quick commercialization of green chemistry innovations in North America. Industrial hubs in North America facilitate quick adoption of innovative fluoropolymer substitutes.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest Growing Region in the Fluoropolymer Alternatives Market

Due to its rapid development, the Asia-Pacific region is featured by speedy industrialization, electronics manufacture, and ecology care. China, India, South Korea, and other countries invest heavily in the development of sustainable materials and contemporary manufacturing technologies. In addition, government subsidies on the development of green technology applications and semiconductors have become important factors in promoting growth. Due to high demand from the car industry, the package industry, and the electronics sector, fluoropolymer alternatives application has been boosted.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

Innovation plays a key role in the Fluoropolymer Alternatives market, where businesses concentrate on developments in material sciences, PFAS-free compounds, and improvements in performance characteristics. Business-to-business collaboration between corporations and scientific organizations or industrial consumers is prevalent in order to hasten product commercialization. High research and development expenses and strict certification criteria are among the difficulties. To maintain an edge over competitors, it is crucial to develop a scalable product line that satisfies regulatory requirements and matches the efficiency of existing fluoropolymers.

Some of the prominent players in the global Fluoropolymer Alternatives are:

- Daikin Industries

- The Chemours Company

- 3M

- Solvay

- Arkema

- AGC Inc.

- Saint-Gobain

- Dow

- W. L. Gore & Associates

- DuPont

- Celanese

- BASF

- Evonik Industries

- Momentive Performance Materials

- Shin-Etsu Chemical

- Elkem

- Clariant

- Honeywell

- Victrex

- Covestro

- Other Key Players

Recent Developments

- In September 2025, The company launched DOWSIL™ 5-1050 Polymer Processing Aid, which is silicon-based as opposed to fluoropolymers used in making other polymer processing aids for film packaging. This product was designed specifically for polyethylene film extrusion and has properties such as reducing melt fracture, decreasing die-lip deposits, reducing die pressure, and optimizing film aesthetics without violating any regulations. It is offered in masterbatch form for use in existing extrusion operations and conforms to both European Union and U.S. standards for food contact.

- In September 2025, The polyethylene resins introduced by NOVA Chemicals include non-fluorinated polymer processing aids (NF-PPA), which provide performance similar to conventional fluoro-polymer processing aids and help meet emerging international standards. The Surpass, Sclair, and Novapol PE series of resins enhance process reliability, minimize die fouling, and sustain film properties for use in packaging. Compatible with current resin formulations, the products allow for manufacturing without fluoropolymers and have secured regulatory approval in North America, Latin America, Europe, and China.

- In April 2025, Chemours Company has made strategic partnerships with SRF Limited for the purpose of ensuring a stronger presence of their supply chain throughout the world as well as better access to their facilities for producing fluoropolymer and fluoroelastomer. This partnership will enable Chemours to improve its flexibility and secure the supply of materials needed for their business operations in semiconductor, automotive, aerospace, chemical processing, and oil and gas industries.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 11.0 Bn |

| Forecast Value (2035) |

USD 19.8 Bn |

| CAGR (2026–2035) |

6.8% |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Alternative Material Type, By Fluoropolymer Replaced, By Form, By Application, By End-Use Industry |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Fluoropolymer Alternatives Market?

▾ The Fluoropolymer Alternatives Market size is expected to reach USD 11.0 billion by 2026 and is projected to reach USD 19.8 billion by the end of 2035.

What is the CAGR of the Fluoropolymer Alternatives Market from 2026 to 2035?

▾ The market is growing at a CAGR of 6.8 percent over the forecasted period.

What factors are driving the growth of the Fluoropolymer Alternatives Market?

▾ Strict Regulations Against PFAS Compounds, and more are the factors driving the growth of the Fluoropolymer Alternatives Market.

What are the major trends in the Fluoropolymer Alternatives Market?

▾ Change to PFAS-Free Manufacturing, and more are some of the major trends in the market.

Who are the key players in the Fluoropolymer Alternatives Market?

▾ Some of the key players in the Fluoropolymer Alternatives Market include 3M, Solvay, DoW, and more

How is the Fluoropolymer Alternatives Market segmented?

▾ The Fluoropolymer Alternatives Market is segmented by alternative material type, fluoropolymer replaced, form, application, end-use industry.

Which region held the largest share of the Fluoropolymer Alternatives Market in 2026?

▾ North America is set to lead the Fluoropolymer Alternatives market with an estimated 37.0% share in 2026.

Which region is expected to grow the fastest in the Fluoropolymer Alternatives Market?

▾ Asia Pacific is the fastest-growing region in the Fluoropolymer Alternatives market during the forecast period.