What is the Global Fog Networking Market Size?

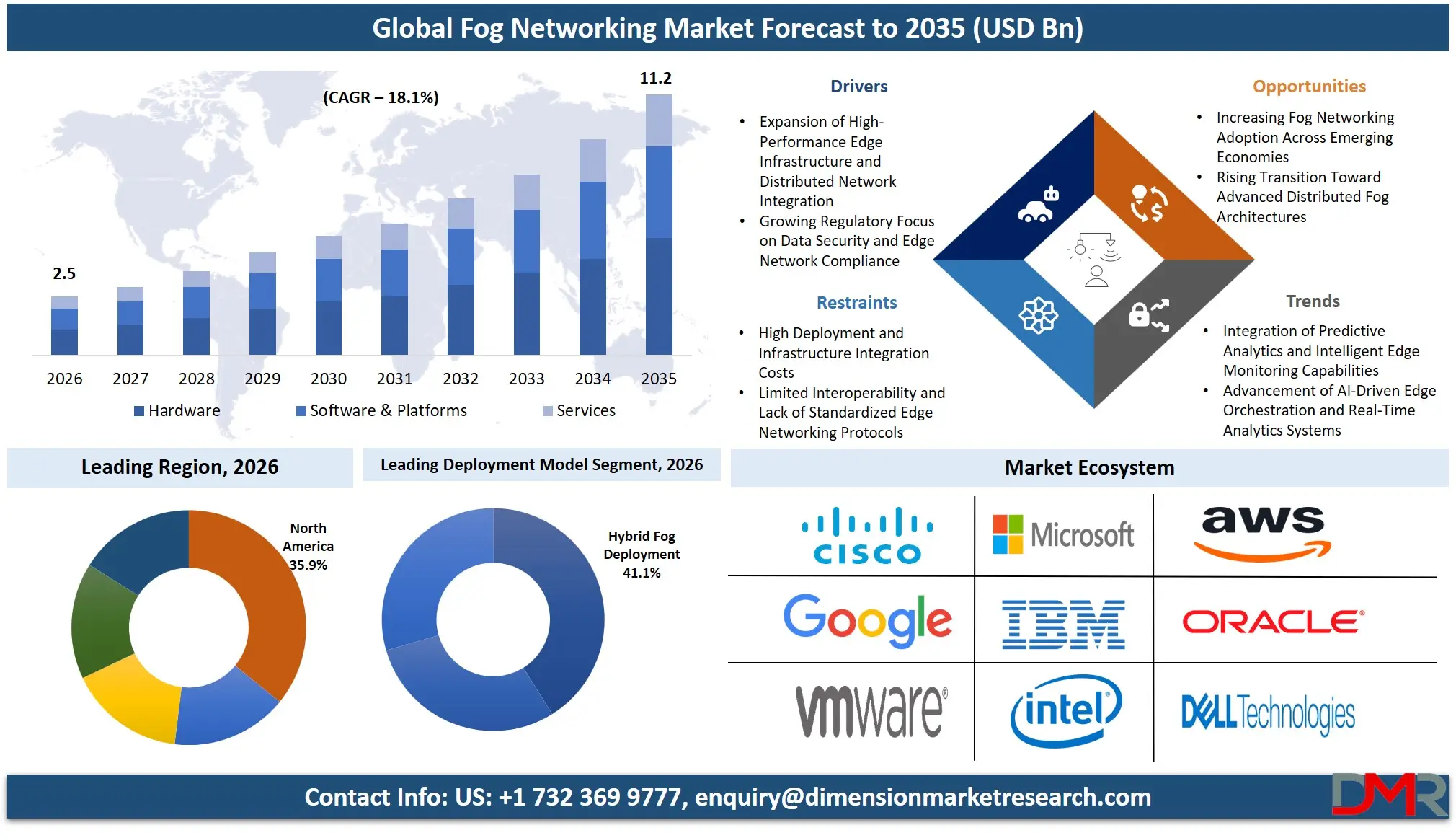

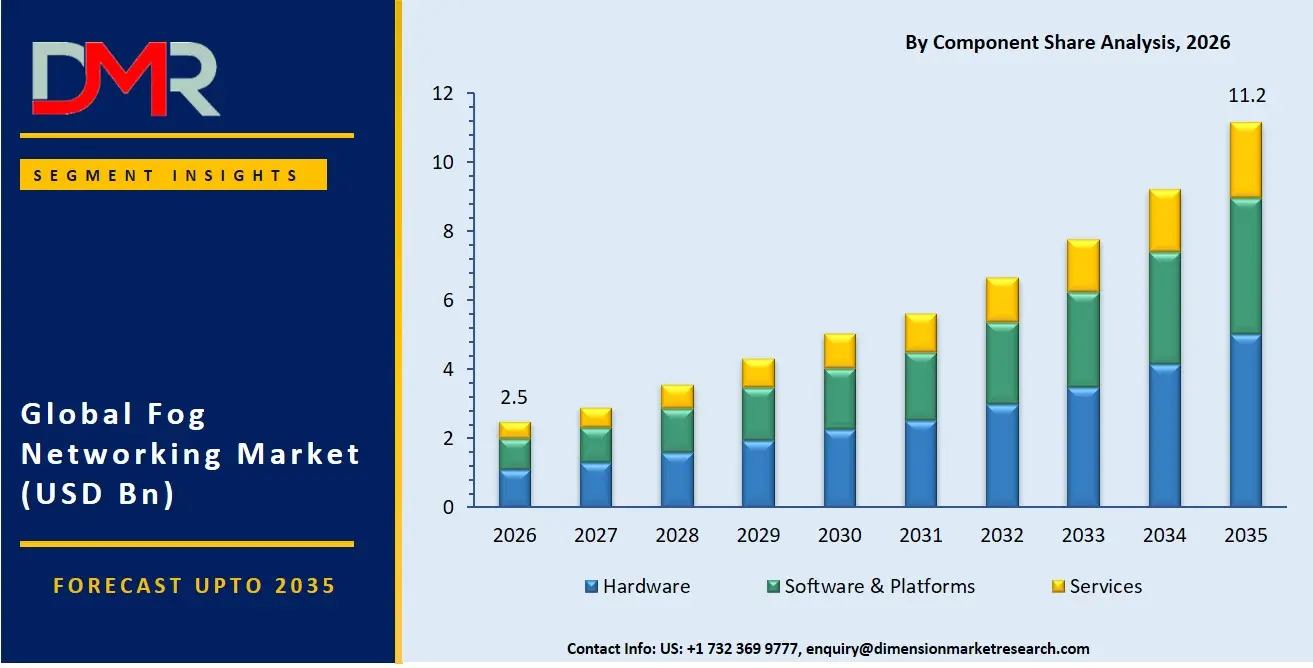

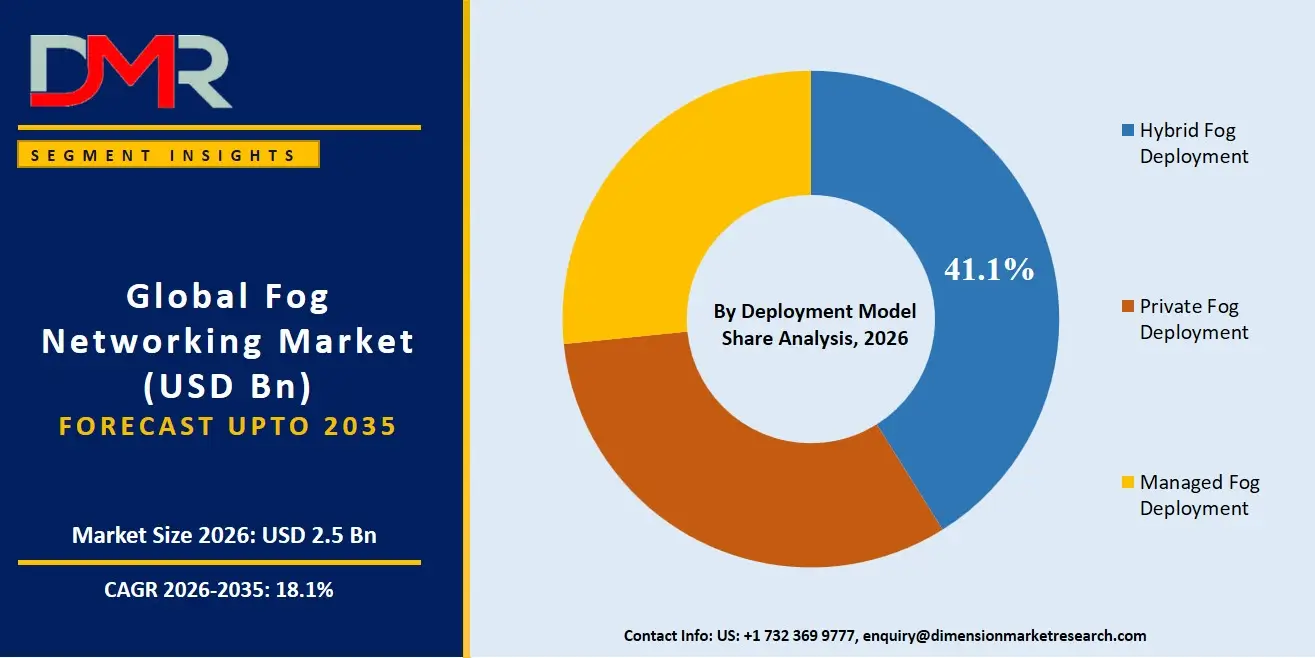

The Global Fog Networking Market size is estimated at USD 2.5 billion in 2026 and is projected to reach USD 11.2 billion by 2035, exhibiting a CAGR of 18.1% during the forecast period, driven by the rising use of real-time edge node performance degradation monitoring and automated workload validation, decentralized fog deployment patterns in modular industrial architectures, and connected governance and compliance management systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The global fog networking market is expanding because of increasing use of high-fidelity node compatibility testing and latency profiling in detecting and analyzing anomalous data traffic patterns, increasing regulatory mandates, which reduce the chance of network congestion during industrial operations and speed up compliance audits for new edge deployments, and more funding in automating privacy-preserving data logging.

Some other reasons for expansion in this market include new technologies in runtime workload stability management, node congestion prediction through behavior analytics, automated data lifecycle handling, high-volume edge data platforms, and improved cross-vendor data-sharing rules. The digital shift in industrial automation and batch processing has been helpful in speeding up product development and making sensitive edge transaction management easier. This includes low-power wide-area network analytics research. In addition, government plans focusing on preventing industrial cyber incidents and the secure data materials economy have ensured steady research in fog networking systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

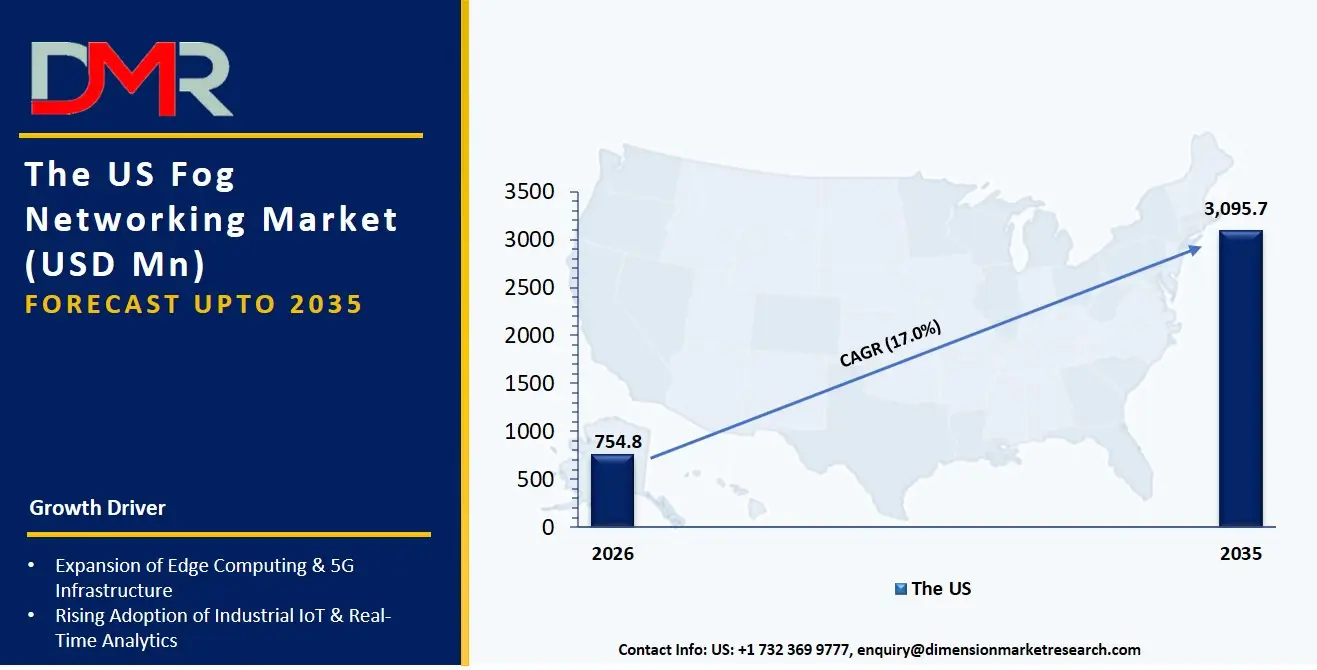

The US Fog Networking Market

The US Fog Networking Market is estimated to grow to USD 754.8 million in 2026 with a compound annual growth rate of 17.0% during the forecast period.

The US market is shaped by major federal and state-level programs promoting resilient edge architectures, secure digital adoption supported by DOE and NIST, and DOD-led edge modernization initiatives. These programs encourage the use of high-bandwidth data processing, real-time latency protection, and predictive compliance software for network blending. Automated network safety platforms are being rapidly adopted, and the US continues to invest in better data sharing between R&D labs, encrypted data audit systems, and reliable congestion detection tools for fog networking platforms. Service providers are also influenced by laws like NIST cybersecurity frameworks, FCC regulations, and national digital edge strategies to offer services that ensure network safety, rule-following, and smooth integration across hybrid and modular edge environments.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Europe Fog Networking Market

The European Fog Networking Market is estimated to be valued at USD 677.5 million in 2026, witnessing growth at a CAGR of 17.2%, during the forecast period.

Europe's fog networking market is well-established, shaped by EU-wide policies such as the NIS2 Directive, GDPR, and national policies to support sustainable digital markets (e.g., Germany's Industry 4.0 edge plans and France's national cloud-edge strategies). Countries are also making network safety management more flexible to align operator and customer demands and enable the sharing of anonymized edge data across borders. The market grows due to new tools like software for real-time bandwidth validation and risk scoring systems for network stability. Use is made easier by teamwork between public and private groups and shared digital safety rules. Manufacturers have access to technologies such as industrial edge fine-tuning, latency interaction modeling, and secure network audit logging, and Europe is at the forefront of the digitisation of safe and efficient fog network operations.

Japan Fog Networking Market

The Japan Fog Networking Market is projected to be valued at USD 142.8 million in 2026, progressing at a CAGR of 19.6%, during the period spanning from 2026 to 2035.

Japan's fog networking market is well developed, with high-bandwidth edge data platforms, connected secure network blending management systems, and a wide array of network aging simulation software tools. National focus on automation, efficiency, and network integrity is delivered via congestion activity models and smart network protection. Growth opportunities are helped by government measures under the Green Growth Strategy by Japan's Ministry of Economy, Trade and Industry (METI), and continued investment in edge cloud modernization. AI-driven network research, multi-party analytics for application-specific edge data sharing, and virtualized secure edge environments all need effective fog networking software to keep pace with high-volume data processing. Higher costs for validating new fog systems and connecting them with older infrastructure are significant, but there are opportunities for the export of Japanese fog networking technologies to the Asian and Pacific markets.

Key Takeaways

- Market Size & Forecast: The Global Fog Networking Market is estimated to be valued at USD 2.5 billion in 2026 and is expected to grow to USD 11.2 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 18.1% in the forecast period.

- Primary Growth Drivers: The availability of new edge processing technologies that use real-time degradation detection, the need to speed up compliance results and improve success rates of edge data sharing, and more government investment in a national secure data material infrastructure are key growth drivers.

- Key Market Trends: The real-time profiling of network stability risks, LPWAN data handling, and the shift to AI-driven edge formulation platforms and automated digital asset inventory management are key market trends.

- By Component: The Software & Platforms segment is expected to take the largest revenue share in the global fog networking market in 2026.

- By Deployment Model: Managed Fog Deployment is expected to take the largest revenue share in 2026 in the fog networking market.

- By Application: The Industrial Automation segment is estimated to take the lead in 2026 with the largest share in the fog networking market.

- Regional Leadership: North America is estimated to take the lead in 2026 with 35.9% share in the fog networking market.

What is Fog Networking?

Fog Networking refers to a combination of edge-driven and real-time monitoring technologies that provide industrial operators, network managers, and compliance entities with enhanced capabilities beyond basic cloud computing, including helping to protect edge data during transmission, preventing network congestion via intelligent load balancing, and enabling secure multi-party edge analytics. They include edge orchestration software, asset performance management platforms, network optimization tools, and visualization systems. These platforms use modern systems such as real-time latency validation, digital asset inventory management software, and remote network advisory to manage, verify, and track sensitive edge events and results. To improve network safety outcomes, manage workload variability and application-specific programs, and expand protection into customized digital coverage to support individual plant designs and promote the development of secure edge products.

Use Cases

- Market Stability for Daily Operations: Fog networking platforms can provide market-balancing benefits through software (encrypted data analytics, attestation) and control systems to reduce network congestion risk and support settlement of secure edge transactions in minutes, compared to days that it would take with only manual network handling.

- Long-Term Sensitive Edge Asset Management: Long-term data on ongoing network stability issues, including node intermittency, bandwidth price spikes, or network degradation, are studied to better understand market performance and to help plan long-term software-based edge care.

- Workload Load Balancing: Network safety is handled through fog networking platforms and smart software in modular plant and corporate settings to support market capacity balance for high-volume edge workloads.

- Government & Regulated Programs: Faster fog networking software development helps data innovation and development of targeted secure edge programs; government programs, through smart monitoring of national edge data materials, advance national network protection strategies and help the adoption of operational standards.

How AI Is Transforming the Global Fog Networking Market?

Artificial intelligence (AI) is being used progressively more often in fog networking platforms to improve edge demand forecasting, find safety quality trends in network traffic patterns, and automatically spot unusual degradation patterns in edge data cycles. It also allows faster network latency verification because it can handle digital edge submissions on a large scale. Encrypted network audit logs are easier to study and help registries find integration issues, reduce mistakes, and improve the overall accuracy of network certification. This has resulted in operations being cost-effective, quicker, and more efficient than the old manual review method.

AI is also strengthening research and development by improving network risk assessment and enabling more accurate capacity planning for edge blending. It helps network operators predict how many secure edge batches will be needed, find possible node activity delays, and monitor the performance of network safety frameworks more effectively. In addition, automation of routine network compliance checks and performance tracking is reducing operational workload, lowering administrative costs, and improving overall efficiency. This is leading to better financial results and more stable operations across the fog networking production chain.

Market Dynamics

Key Drivers of the Global Fog Networking Market

Expansion of High-Performance Edge Infrastructure and Distributed Network Integration

The market is growing with the rise of advanced distributed edge architectures for fog networks, better management of sensitive real-time data processes, and a closer connection between network performance monitoring and secure edge integration. Fog networking platforms provide real-time data that allows monitoring of node activity, helping to identify latency issues early, and checking network stability performance much faster. This has improved operational efficiency and reduced human errors and infrastructure management costs. At the same time, demand for more automated network management is being supported by growing activity in predictive analytics for the assessment of individual network risks, as edge computing further digitizes workload orchestration and distributed data processing tasks.

Growing Regulatory Focus on Data Security and Edge Network Compliance

There is increasing emphasis on network security, data integrity, and regulatory compliance within the fog networking ecosystem. Regulations and frameworks such as the EU NIS2 Directive, GDPR, FCC policies, and edge infrastructure modernization initiatives in key markets are encouraging stronger network governance practices and more structured edge security processes. These developments are supporting the need for systems that can offer continuous monitoring of sensitive edge data and standardized reporting capabilities. At the same time, ongoing efforts to improve interoperability of network performance data and reduce verification complexities are strengthening the need for more efficient management systems across both public and private sector participants.

Restraints in the Global Fog Networking Market

High Deployment and Infrastructure Integration Costs

The deployment of fog networking systems remains costly, requiring significant investment in orchestration software, node activity validation technologies, system integration, testing, and alignment with existing enterprise workflows. In addition, compliance with data regulations such as GDPR and other regional frameworks increases deployment complexity. These factors raise upfront costs and can limit adoption, particularly among small and medium-sized enterprises and new market entrants.

Limited Interoperability and Lack of Standardized Edge Networking Protocols

The market continues to face fragmentation in terms of edge data formats and network management procedures. Although some regions have implemented structured digital edge management systems, many network operators still rely on a combination of legacy infrastructure and modern automated edge platforms. The absence of standardized latency and interoperability protocols limits the exchange of network performance data between enterprises and fog vendors and creates inefficiencies in deployment, integration, and infrastructure management.

Growth Opportunities in the Global Fog Networking Market

Increasing Fog Networking Adoption Across Emerging Economies

Developing economies such as Brazil, Indonesia, Nigeria, the UAE, and Vietnam are gradually strengthening their edge computing and fog networking ecosystems. These regions present long-term growth opportunities due to increasing industrial automation adoption, rising awareness of edge security initiatives, and ongoing modernization of digital infrastructure. These markets have relatively limited legacy infrastructure and are more adaptable to scalable, technology-driven fog networking platforms.

Rising Transition Toward Advanced Distributed Fog Architectures

The shift toward secure edge infrastructure, decentralized computing environments, and real-time network monitoring is driving the adoption of advanced fog architectures. These systems enable centralized edge data visibility, improved coordination between network operators and enterprise users, and faster distributed infrastructure management. Advanced fog deployments are increasingly becoming a strategic priority among modern network providers as operational efficiency becomes an important competitive factor.

Global Fog Networking Market Trends

Integration of Predictive Analytics and Intelligent Edge Monitoring Capabilities

Fog networking platforms are increasingly incorporating data-driven technologies to identify network degradation patterns and improve accuracy in distributed infrastructure management. These systems allow network operators to better analyze edge node traffic behavior, streamline management of decentralized network environments, and enhance overall network performance. This transition is gradually making the industry more proactive and data-driven in network optimization instead of relying solely on reactive operational practices.

Advancement of AI-Driven Edge Orchestration and Real-Time Analytics Systems

The adoption of AI-enabled edge orchestration systems is becoming a fundamental component of modern network infrastructure operations. These systems support real-time network monitoring, centralized edge resource management, and improved coordination among distributed network participants. Advanced fog platforms are enhancing the efficiency and responsiveness of infrastructure providers operating across multiple regions by reducing dependence on manual network processes and enabling more scalable, distributed operations.

Research Scope and Analysis

The global fog networking market is witnessing strong growth driven by rising adoption of industrial automation, edge optimization, and increasing demand for high-safety and high-efficiency edge networks. The market is segmented based on component, deployment model, service model, connectivity technology, application, and end user.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Component Analysis

The Software & Platforms segment is likely to continue dominating the market in 2026, accounting for approximately 61.8% of the global fog networking market share. This is due to its key role in enabling high-fidelity edge simulation, a wide operating parameter range, and long-term network stability, and its usefulness in various industrial settings where operational efficiency is needed. Within Software & Platforms, the Edge Orchestration & Analytics Platforms sub-segment holds the largest share, driven by high deployment volumes, automated demand for stable edge connectivity, and compliance requirements. The Services segment is driven by its key role in enabling successful deployment, with Integration & Deployment Services leading, followed by Consulting and Support & Maintenance. Hardware remains a foundational segment, including fog nodes and gateways.

By Deployment Model Analysis

The Hybrid Fog Deployment segment is likely to continue holding the lead in 2026, accounting for approximately 41.1% of the global fog networking market share, driven by rising demand for scalable edge architectures that combine cloud flexibility with on-premises data control and security. This segment reflects the increasing shift toward agile and distributed edge computing environments across enterprises and telecom operators. The Private Fog Deployment segment is the second-largest, supported by strong adoption in government, defense, and highly regulated industries where data sovereignty and localized processing are critical. Managed Fog Deployment remains an important segment, driven by growing demand for outsourced infrastructure management, operational scalability, and reduced IT complexity.

By Service Model Analysis

The Infrastructure as a Service (IaaS) segment is expected to dominate with around 44.2% market share in 2026, driven by its irreplaceable role in providing on-demand compute and storage at the edge, enabling real-time data processing and latency reduction. IaaS supports customized edge deployment plans because it can offer multiple levels of resource scaling, capacity amounts, and yearly stability plans, delivering fast results while keeping edge data within secure registry systems. The Platform as a Service (PaaS) segment is the second-largest, driven by demand for application development and deployment environments. Software as a Service (SaaS) is the fastest-growing, witnessing strong growth with increasing needs for ready-to-use edge analytics and remote monitoring.

By Connectivity Technology Analysis

The Cellular segment is the largest connectivity technology in 2026, accounting for 32.7% share, driven by the need for wide-area coverage, low latency, and reliable connectivity for mobile and remote edge nodes. Industrial operators are adopting cellular-connected fog nodes for visibility and control over their distributed assets. The Wi-Fi segment is the second-largest, supported by enterprise and indoor deployment proliferation. Ethernet remains a steady segment for fixed industrial networks, while LPWAN and Bluetooth are the fastest-growing for low-power sensor networks and short-range device connectivity, respectively.

By Application Analysis

The Industrial Automation segment is the largest application in 2026, accounting for approximately 35.8% share, driven by the need for real-time process control, predictive maintenance, and quality consistency in manufacturing environments. Industrial operators are adopting fog networking platforms for visibility and control over their production parameters. The Smart Cities & Infrastructure segment is the second-largest, supported by traffic management, public safety, and utility monitoring mandates. Connected Vehicles & Transportation remains a strong segment driven by V2X communication and autonomous driving needs, while Connected Healthcare and Energy & Utilities are the fastest-growing due to regulatory pressure and remote monitoring requirements.

By End User Analysis

The Enterprises segment is the largest in 2026, accounting for approximately 44.3% share, driven by the need for enterprise-wide edge transformation, multi-site standardization, and significant IT budgets. Enterprises are adopting fog platforms to optimize global operations and ensure operational excellence. The Telecom Operators segment is the second-largest, supported by investments in network edge computing and 5G rollout. The Government & Public Sector and Healthcare Providers segments are the fastest-growing, driven by smart city initiatives and remote patient monitoring needs, respectively.

The Global Fog Networking Market Report is segmented based on the following:

By Component

- Hardware

- Software & Platforms

- Services

By Deployment Model

- Private Fog Deployment

- Managed Fog Deployment

- Hybrid Fog Deployment

By Service Model

- Infrastructure as a Service (IaaS)

- Platform as a Service (PaaS)

- Software as a Service (SaaS)

By Connectivity Technology

- Wi-Fi

- Ethernet

- Cellular

- Bluetooth

- LPWAN

By Application

- Industrial Automation

- Smart Cities & Infrastructure

- Connected Healthcare

- Connected Vehicles & Transportation

- Energy & Utilities

- Retail

By End User

- Telecom Operators

- Enterprises

- Government & Public Sector

- Healthcare Providers

Regional Analysis

Largest Region in the Fog Networking Market

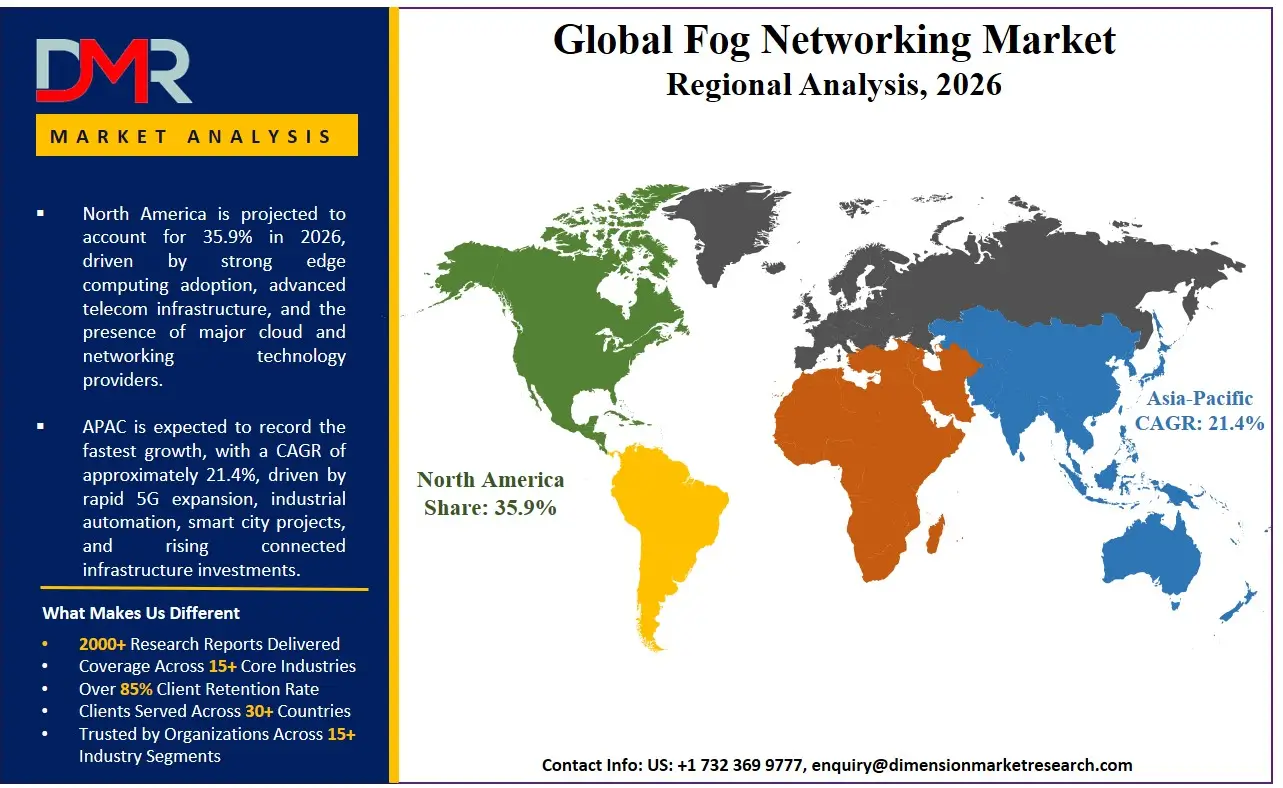

It is projected that North America will lead the global fog networking market, with a market share of about 35.9% in 2026. The region's dominance is driven by the presence of major edge software vendors, strong regulatory frameworks such as NIST cybersecurity guidelines mandating edge security, and early adoption of AI-driven edge orchestration and predictive maintenance technologies across industrial and telecom sectors. North America benefits from significant investment in industrial edge digitalization, the highest concentration of brownfield modernization projects in the US manufacturing belt, and strong government support through DOE funding for industrial decarbonization. The region is also home to major telecom operators and engineering firms, enabling rapid deployment of fog networks. The widespread adoption of advanced fog networks for smart manufacturing, refinery optimization, and connected vehicle infrastructure continues to reinforce the region's market leadership.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Region in the Fog Networking Market

Asia-Pacific is the fastest-growing region, supported by aggressive domestic industrial automation expansion in China and India, substantial government funding for smart factory and Industry 4.0 initiatives, and increasing investments in greenfield manufacturing complexes that integrate fog networks from the initial design phase. The region is witnessing rapid growth in modular plant construction, driving demand for cloud-based edge simulation and process optimization software. Asia-Pacific is also at the forefront of AI-driven edge deployment in high-growth sectors like electric vehicle manufacturing and semiconductors. The region benefits from lower labor costs, driving faster ROI on automation, along with rising corporate commitments to operational excellence and safety compliance. Moreover, increasing data regulations and the need to reduce industrial cyber incidents in rapidly industrializing economies are expected to keep Asia-Pacific's growth momentum as the highest CAGR region during the forecast period.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The fog networking market is highly competitive, with new ideas and strategic partnerships shaping the competitive environment. To gain an advantage, companies and providers are focused on developing better fog platforms (such as AI-powered edge simulation, automated latency detection systems, and software development kits for network safety management), smart node activity analytics, and cloud-based edge degradation monitoring. There are high barriers to entering the market due to the large amount of money needed for regulatory approval, specialized edge networking knowledge, and the need for mature software systems and rule-following.

Strategic approaches to increase market presence include partnerships with industrial research groups and digital registries, mergers between fog software providers and edge manufacturers, and long-term support contracts with customers and government institutions. Additionally, research and development in digital data-sharing rules and flexible edge simulation designs are important for staying competitive and meeting the changing needs of the fog networking community.

Some of the prominent players in the Global Fog Networking Market are:

- Cisco Systems, Inc.

- Microsoft Corporation

- Amazon Web Services, Inc.

- Google LLC

- International Business Machines Corporation

- Oracle Corporation

- VMware, Inc.

- Intel Corporation

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Huawei Technologies Co., Ltd.

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- Qualcomm Incorporated

- AT&T Inc.

- Schneider Electric SE

- Fujitsu Limited

- NEC Corporation

- SAP SE

- ADLINK Technology Inc.

- Other Key Players

Recent Developments

- April 2026: Microsoft Corporation expanded Azure Edge AI capabilities through updates to Azure IoT Edge and Azure Arc, enabling unified deployment and management of AI workloads across distributed edge environments, improving real-time analytics, low-latency inference, and centralized governance across industrial and enterprise fog computing systems.

- March 2026: International Business Machines Corporation (IBM) enhanced IBM Edge Application Manager with deeper integration of watsonx AI, enabling automated deployment, monitoring, and lifecycle management of AI models across distributed edge nodes, strengthening real-time decision-making in industrial IoT, telecom, and enterprise fog computing environments.

- February 2026: Amazon Web Services, Inc. (AWS) upgraded AWS Wavelength and AWS Outposts to support ultra-low-latency edge computing for 5G networks, enabling real-time AI inference closer to users across telecom infrastructure, supporting applications in autonomous systems, smart manufacturing, and connected healthcare ecosystems.

- November 2025: Cisco Systems, Inc. launched Cisco Unified Edge, a next-generation edge computing platform integrating compute, networking, storage, and security to support distributed agentic AI workloads at the network edge, enabling real-time inference closer to factories, hospitals, and retail environments while strengthening its fog and edge computing infrastructure.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 2.5 Bn |

| Forecast Value (2035) |

USD 11.2 Bn |

| CAGR (2026–2035) |

18.1% |

| The US Market Size (2026) |

USD 754.8 Mn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Component, By Deployment Model, By Service Model, By Connectivity Technology, By Application, By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Fog Networking Market?

▾ The Global Fog Networking Market is estimated to be valued at USD 2.5 billion in 2026 and is expected to reach USD 11.2 billion by the end of 2035.

What is the CAGR of the Global Fog Networking Market from 2026 to 2035?

▾ The market is growing at a CAGR of 18.1% over the forecasted period.

What factors are driving the growth of the Global Fog Networking Market?

▾ The market is driven by advances in real-time edge degradation detection and automated safety enforcement, regulatory pressure to speed up network compliance results and reduce latency mistakes, and increased government investment in a national secure data material infrastructure.

What are the major trends in the Global Fog Networking Market?

▾ The key market trends include the adoption of real-time network stability tracking and LPWAN data analysis, along with a growing shift toward AI-driven edge orchestration platforms and data-enabled digital asset inventory management systems.

Which region held the largest share of the Global Fog Networking Market in 2026?

▾ North America is expected to account for the largest market share in 2026, with a share of about 35.9%.

Which region is expected to grow the fastest in the Global Fog Networking Market?

▾ Asia Pacific is the fastest-growing region in the market during the forecast period.

Who are the key players in the Global Fog Networking Market?

▾ Some of the major key players in the Global Fog Networking Market are Cisco Systems, Inc., Microsoft Corporation, IBM, Google LLC, Intel Corporation, VMware, Inc., and many others.

How is the Global Fog Networking Market segmented?

▾ The market is segmented by component, deployment model, service model, connectivity technology, application, and end user.