Market Overview

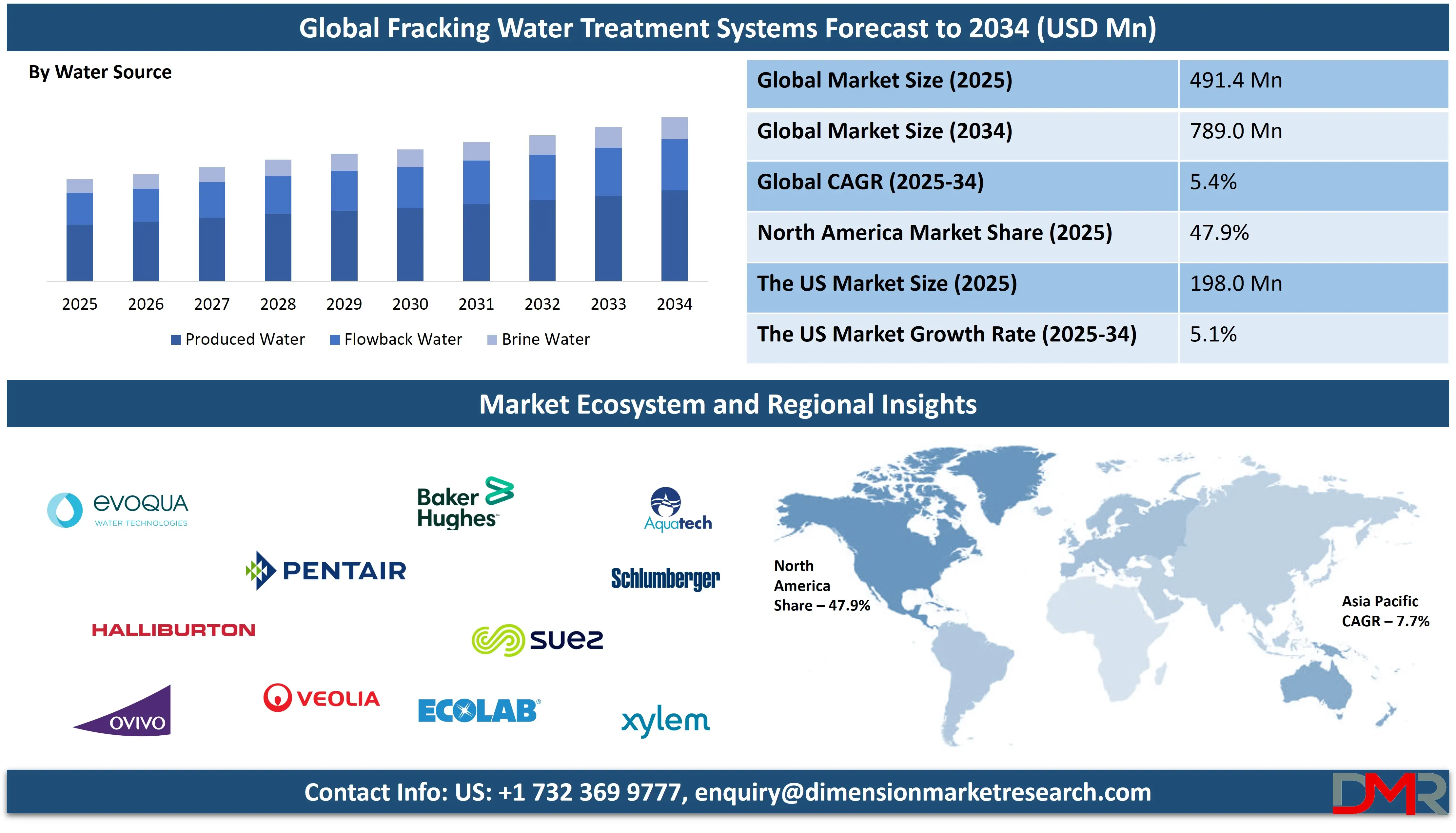

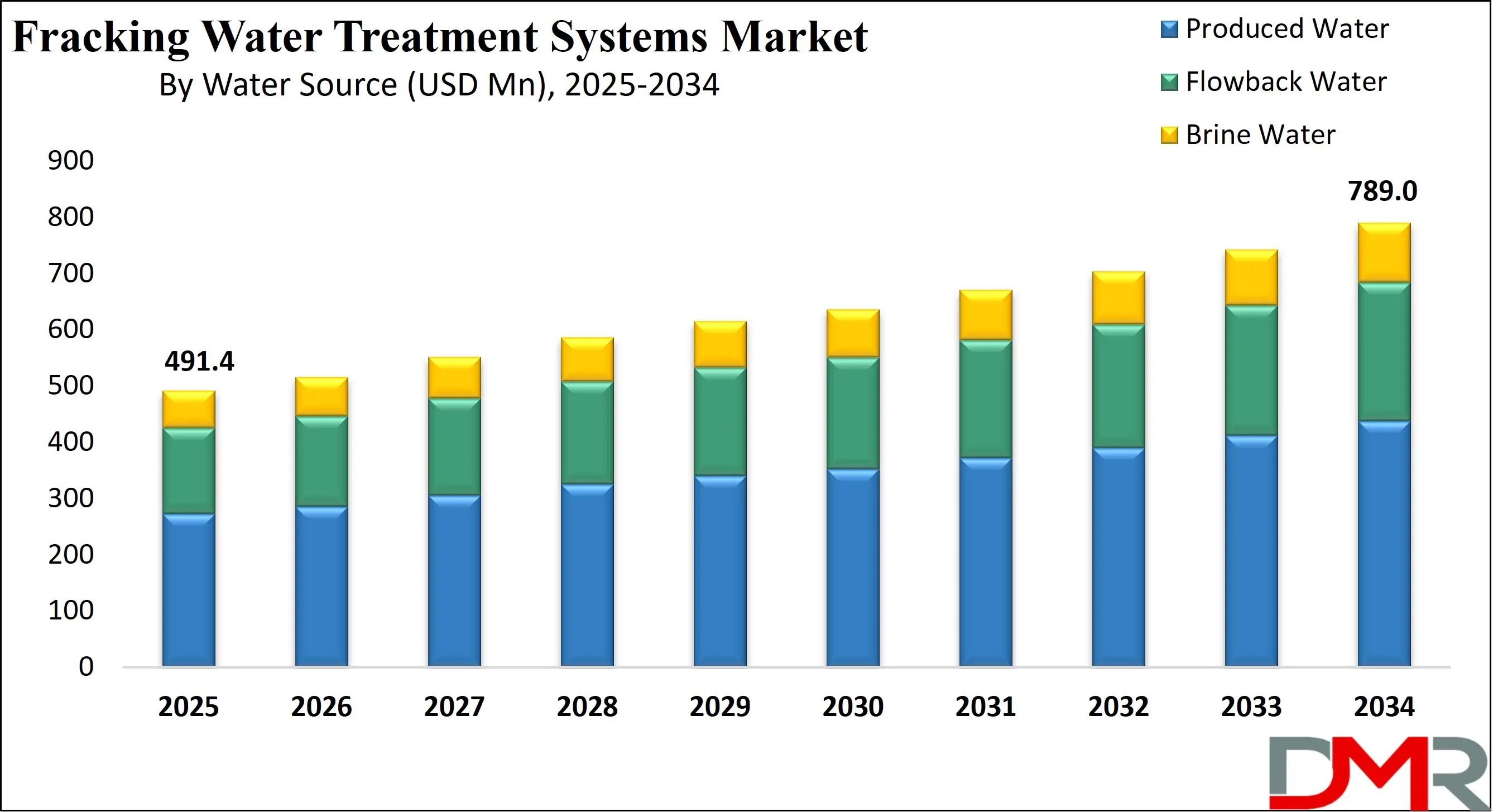

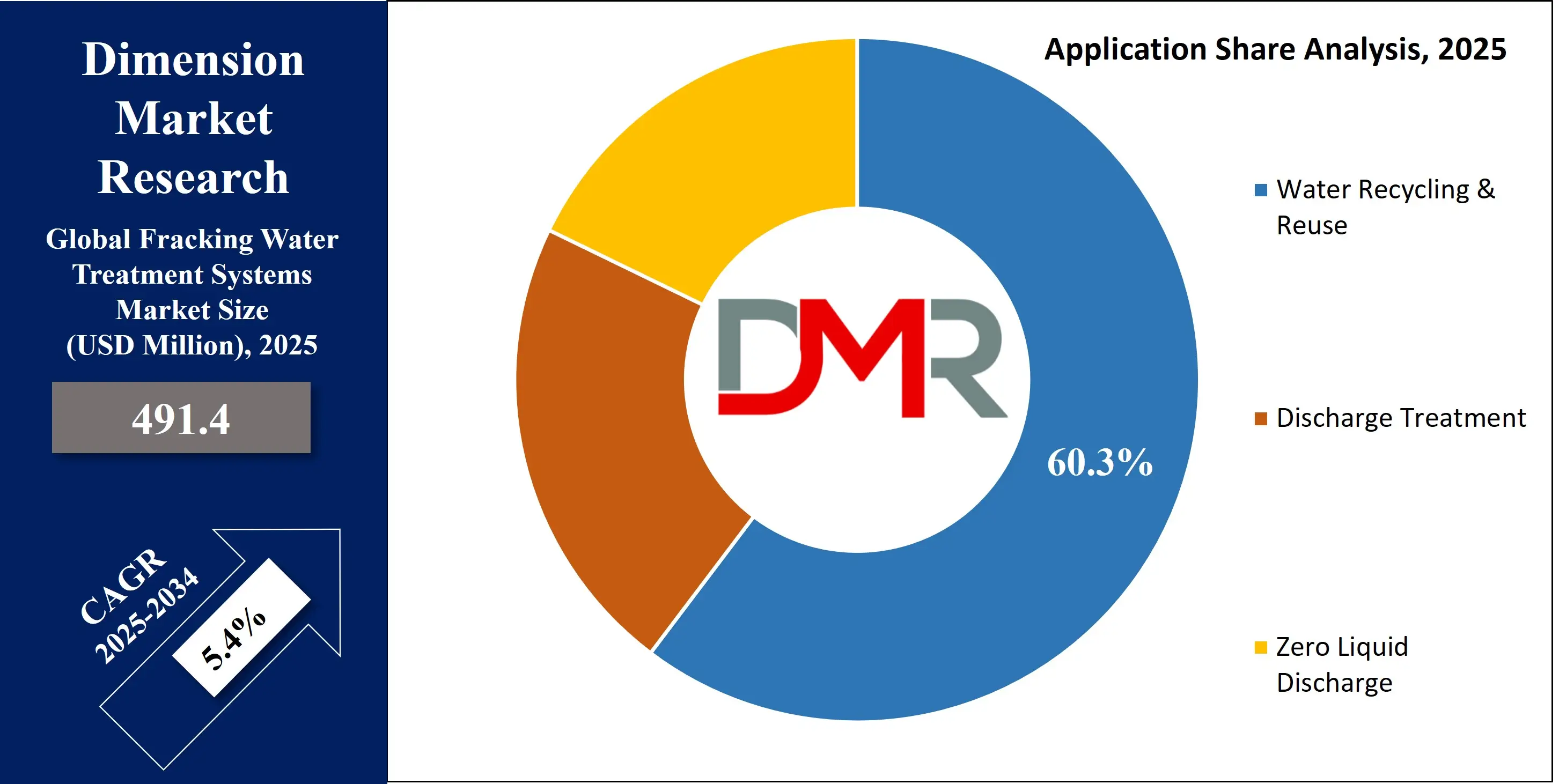

The Global Fracking Water Treatment Systems Market size is projected to reach USD 491.4 million in 2025 and grow at a compound annual growth rate of 5.4% to reach a value of USD 789.0 million in 2034.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fracking water treatment systems comprise technologies, equipment, and services used to treat wastewater generated during hydraulic fracturing operations. This includes produced water, flowback water, and brine water containing suspended solids, hydrocarbons, salts, heavy metals, and chemical additives. The market includes physical, chemical, thermal, membrane, and hybrid treatment systems that enable water recycling, safe discharge, or zero liquid discharge. These systems are critical to the oil and gas industry as water management has become a central operational and environmental concern, especially in water-stressed regions where shale development is expanding.

The market’s growth is shaped by increasing environmental regulations, rising disposal costs, and growing emphasis on sustainable water use. Oil and gas operators are adopting advanced treatment technologies to minimize freshwater consumption and reduce dependency on deep-well injection. Digital monitoring, automation, and modular system design are improving operational efficiency and scalability. The shift toward mobile and on-site treatment solutions reflects industry demand for cost-effective and flexible water management approaches across drilling locations.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Also, recent market evolution highlights a transition toward advanced membrane technologies, zero liquid discharge systems, and integrated treatment platforms. Strategic investments, technology partnerships, and innovation in resource recovery are expanding the role of treatment systems beyond compliance toward value creation. As regulatory scrutiny intensifies, the market continues to mature with a focus on sustainability, efficiency, and long-term operational resilience.

The US Fracking Water Treatment Systems Market

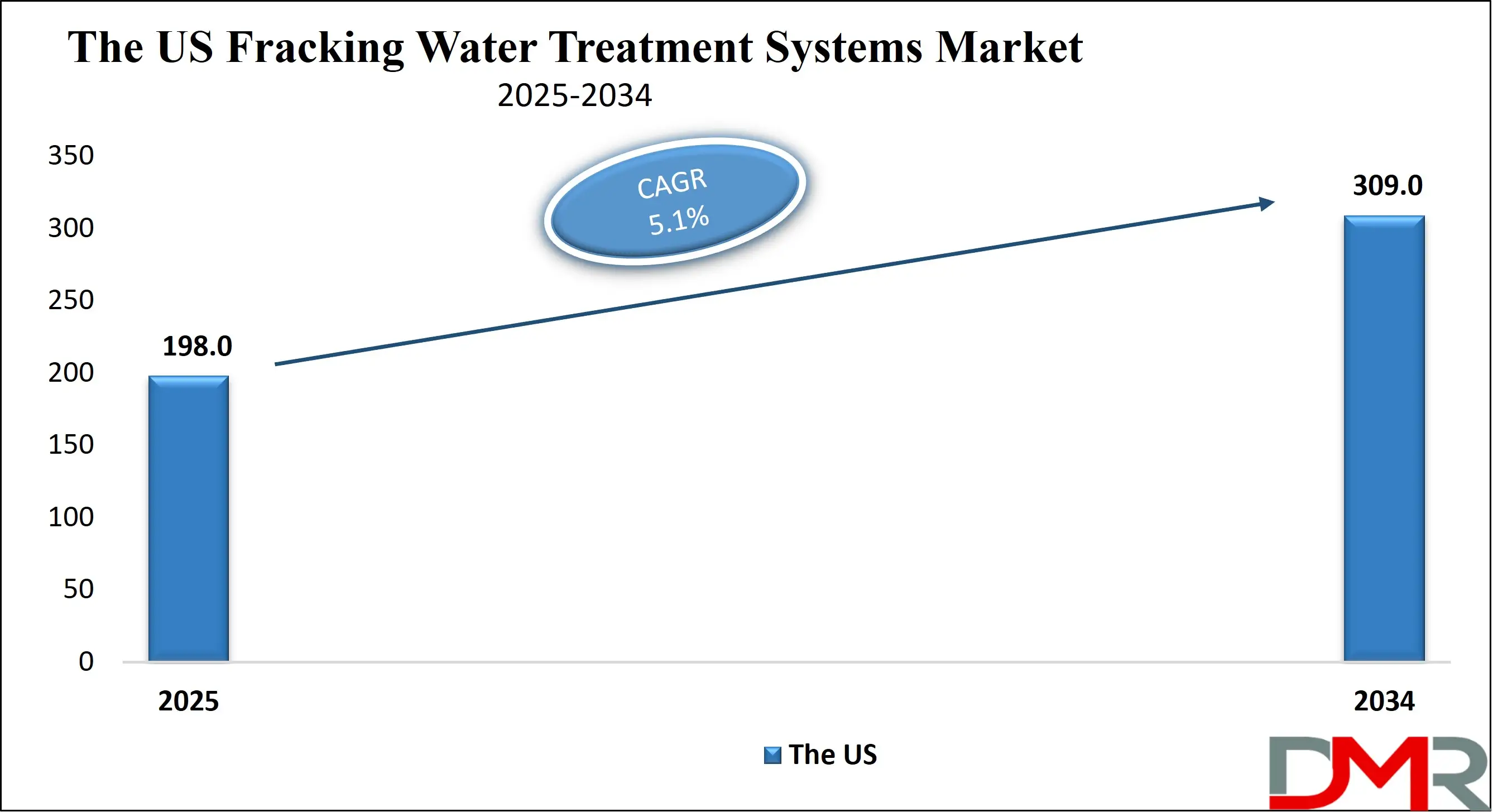

The US Fracking Water Treatment Systems Market size is projected to reach USD 198.0 million in 2025 at a compound annual growth rate of 5.1% over its forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The United States represents the largest and most developed market for fracking water treatment systems due to extensive shale oil and gas production across major basins. High volumes of produced and flowback water have driven strong demand for advanced treatment and recycling solutions. Regulatory oversight related to wastewater disposal and reuse has encouraged widespread adoption of on-site and centralized treatment systems. The presence of established oilfield service providers and technology innovators supports continuous advancement in treatment efficiency. Government incentives promoting responsible energy production and water reuse further strengthen market growth, making the U.S. the primary hub for technological innovation and system deployment.

Europe Fracking Water Treatment Systems Market

Europe Fracking Water Treatment Systems Market size is projected to reach USD 108.1 million in 2025 at a compound annual growth rate of 5.0% over its forecast period.

Europe’s market is shaped by stringent environmental regulations and strong sustainability priorities, which influence the adoption of water treatment solutions in limited fracking operations. Regional policies emphasize groundwater protection, waste minimization, and safe wastewater management, encouraging the use of advanced treatment technologies. While overall shale activity remains moderate, investments in water treatment infrastructure are rising to ensure compliance with strict discharge standards. Innovation is driven by engineering expertise and environmental alignment, with gradual adoption supported through pilot projects and regulatory frameworks focused on environmental protection.

Japan Fracking Water Treatment Systems Market

Japan Fracking Water Treatment Systems Market size is projected to reach USD 24.6 million in 2025 at a compound annual growth rate of 6.0% over its forecast period.

Japan’s market is influenced by advanced industrial water treatment expertise and strong government emphasis on water efficiency and environmental protection. Although fracking activity is limited, Japan’s leadership in membrane filtration, automation, and precision engineering supports adoption of advanced treatment systems. Government initiatives promoting water recycling and resource efficiency drive technological development. Urbanization, infrastructure modernization, and industrial growth further support market potential. Challenges include limited domestic shale reserves, but opportunities exist through technology innovation and export-oriented system development.

Fracking Water Treatment Systems Market: Key Takeaways

- Market Growth: The Fracking Water Treatment Systems Market size is expected to grow by USD 273.8 million, at a CAGR of 5.4%, during the forecasted period of 2026 to 2034.

- By Water Source: The produced water segment is anticipated to get the majority share of the Fracking Water Treatment Systems Market in 2025.

- By Application: Water Recycling & Reuse segment is expected to get the largest revenue share in 2025 in the Fracking Water Treatment Systems Market.

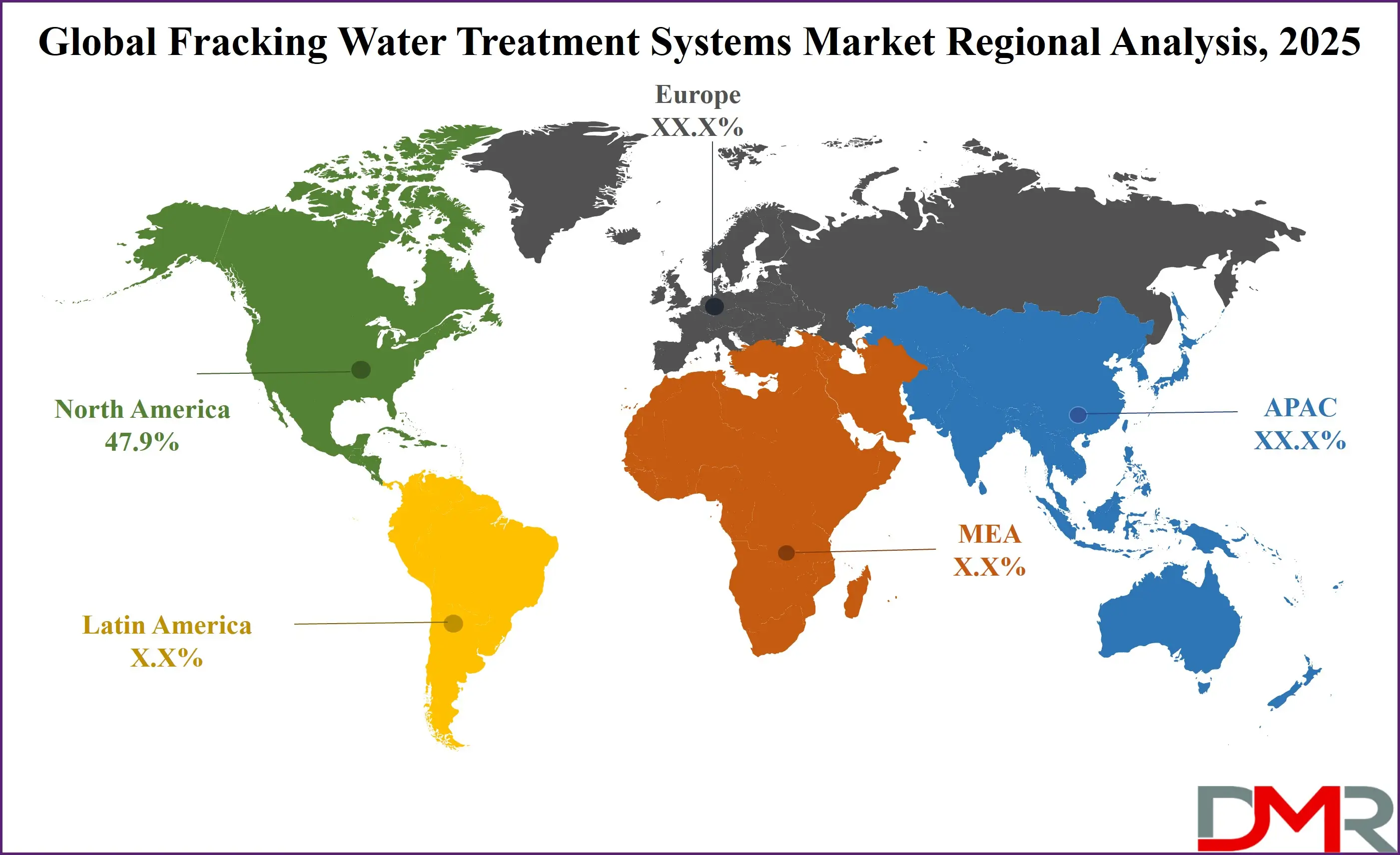

- Regional Insight: North America is expected to hold a 47.9% share of revenue in the Global Fracking Water Treatment Systems Market in 2025.

- Use Cases: Some of the use cases of Fracking Water Treatment Systems include produced water recycling, zero liquid discharge, and more.

Fracking Water Treatment Systems Market: Use Cases

- Produced Water Recycling: Treatment systems enable reuse of produced water in fracturing operations, reducing freshwater demand and disposal costs.

- Flowback Water Treatment: Rapid treatment of flowback water improves operational efficiency and minimizes storage requirements.

- Zero Liquid Discharge: Advanced thermal and hybrid systems eliminate liquid waste while recovering usable water and solids.

- Environmental Compliance: Systems ensure wastewater meets regulatory standards for discharge or reuse.

- Mobile Field Operations: Skid-mounted and trailer-mounted systems allow treatment at remote drilling locations.

- Salinity and Contaminant Removal: Membrane and chemical technologies remove salts, hydrocarbons, and dissolved contaminants.

- Resource Recovery: Treatment systems enable extraction of valuable minerals from wastewater streams.

Stats & Facts

- U.S. Energy Information Administration reports shale gas production exceeded 75% of total U.S. dry gas output in 2024.

- U.S. Environmental Protection Agency states wastewater generation can exceed 20,000 barrels per hydraulically fractured well.

- International Energy Agency reports water reuse rates in shale operations surpassed 55% in 2024.

- U.S. Department of Energy indicates on-site treatment reduces wastewater transportation costs by up to 40%.

- Bureau of Land Management highlights increased enforcement of produced water disposal regulations in 2025.

- European Commission reports rising investment in advanced wastewater treatment under sustainability programs.

- Japan Ministry of Economy, Trade and Industry notes increased adoption of membrane-based industrial water treatment systems in 2024.

- U.S. Geological Survey identifies produced water as the largest waste stream by volume in oil and gas operations.

- International Water Association reports membrane filtration efficiency improved by over 30% since 2023.

- U.S. Energy Department notes increased adoption of zero liquid discharge systems across shale basins in 2025.

Market Dynamic

Driving Factors in the Fracking Water Treatment Systems Market

Regulatory Pressure and Environmental Compliance

Stringent environmental regulations governing wastewater disposal and groundwater protection are a primary driver of market growth. Governments and regulatory agencies enforce strict limits on wastewater discharge, reuse, and injection, compelling operators to adopt advanced treatment solutions. Compliance requirements increase demand for reliable systems that ensure consistent treatment quality and traceability. As public scrutiny of fracking operations intensifies, companies are investing in treatment infrastructure to mitigate environmental risks, avoid penalties, and maintain social license to operate.

Rising Water Scarcity and Cost Optimizatio

Growing water scarcity in shale-producing regions has increased the economic and operational importance of water recycling. Transporting and disposing of wastewater is costly, particularly in remote locations. Fracking water treatment systems reduce freshwater sourcing and trucking costs while improving operational efficiency. Recycling treated water for reuse lowers overall water management expenses and enhances supply reliability, making advanced treatment solutions a cost-effective strategy for operators.

Restraints in the Fracking Water Treatment Systems Market

High Capital and Operating Costs

Advanced treatment technologies such as membrane filtration, thermal evaporation, and zero liquid discharge systems require significant capital investment. High upfront costs and ongoing maintenance expenses can limit adoption, particularly among smaller or independent operators. Energy-intensive processes also increase operating costs, impacting profitability. These financial constraints may delay system upgrades or restrict adoption to large-scale projects with sufficient capital availability.

Technological and Infrastructure Limitations

Variability in wastewater composition presents technical challenges for treatment system performance. High salinity, complex chemical mixtures, and fluctuating volumes require adaptable and robust systems. Limited infrastructure in remote drilling areas further complicates deployment. Inadequate technical expertise and system integration challenges can reduce treatment efficiency and slow market penetration.

Opportunities in the Fracking Water Treatment Systems Market

Expansion of Zero Liquid Discharge Systems

Zero liquid discharge technologies present significant growth opportunities as operators seek to eliminate wastewater disposal entirely. These systems align with sustainability goals by maximizing water recovery and minimizing environmental impact. Advancements in thermal and hybrid technologies are improving efficiency and lowering costs, making ZLD systems more commercially viable and attractive to operators.

Resource Recovery and Value Creation

Emerging technologies enable recovery of valuable minerals and salts from wastewater streams. This transforms treatment systems from cost centers into value-generating assets. Growing demand for critical minerals enhances the attractiveness of integrated recovery solutions, opening new revenue streams and improving overall project economics.

Trends in the Fracking Water Treatment Systems Market

Adoption of Modular and Mobile Treatment Systems

Operators increasingly prefer modular and mobile systems that allow rapid deployment and scalability. These systems reduce infrastructure requirements, support remote operations, and improve cost efficiency. Flexibility in system configuration enables adaptation to varying wastewater volumes and compositions.

Digitalization and Smart Water Management

Integration of sensors, automation, and data analytics is transforming system operation. Digital monitoring improves treatment precision, predictive maintenance, and regulatory reporting. Smart water management enhances system reliability and reduces downtime, supporting long-term operational optimization.

Impact of Artificial Intelligence in Fracking Water Treatment Systems Market

- Process Optimization: AI algorithms analyze real-time data to optimize treatment parameters and improve efficiency.

- Predictive Maintenance: AI predicts equipment failures, reducing downtime and maintenance costs.

- Water Quality Monitoring: Machine learning models enhance detection of contaminants and treatment performance.

- Energy Optimization: AI minimizes energy consumption in thermal and membrane systems.

- Automated Compliance Reporting: AI streamlines regulatory documentation and reporting accuracy.

- Adaptive Treatment Control: Systems automatically adjust to changing wastewater composition.

- Operational Cost Reduction: AI-driven optimization lowers chemical usage and operational expenses.

Research Scope and Analysis

By Water Source Analysis

Produced water dominates the fracking water treatment systems market because it is generated continuously throughout the productive life of a shale well. In 2025, this segment accounts for approximately 55.4% of total market share, reflecting its high treatment demand and long-term management requirements. Increasing restrictions on deep-well injection and rising mandates for water reuse have strengthened adoption of advanced treatment solutions for produced water. Technologies such as membrane filtration, chemical treatment, and hybrid systems are widely implemented to manage high salinity and complex contaminants. The ability to recycle produced water multiple times reduces freshwater dependency and operational costs, supporting its sustained leadership.

Flowback water represents the fastest-growing water source segment due to the large volumes generated immediately after hydraulic fracturing operations. Although its overall share is lower than produced water, demand is rising rapidly as operators prioritize early-stage water management. Flowback water contains high concentrations of chemical additives, suspended solids, and hydrocarbons, requiring rapid and effective treatment. The growing use of mobile and high-capacity treatment systems supports this segment’s expansion. As drilling activity intensifies and operational timelines shorten, efficient flowback water treatment is becoming critical for regulatory compliance and cost control.

By Treatment Technology Analysis

Physical treatment technologies lead the market due to their operational simplicity and cost effectiveness in removing suspended solids and particulate matter. In 2025, physical treatment accounts for approximately 42.8% of the total market share, reflecting its widespread adoption as a primary treatment stage. Filtration, sedimentation, and membrane-based systems are commonly used to improve water quality before advanced processing. These technologies are adaptable to varying wastewater compositions and volumes, making them suitable across different shale basins. Continuous advancements in membrane durability and filtration efficiency further strengthen the role of physical treatment in fracking water management.

Hybrid treatment systems are expanding rapidly as operators seek higher treatment efficiency and greater adaptability. These systems combine physical, chemical, and thermal technologies to address complex wastewater characteristics. While holding a smaller share than physical treatment, hybrid solutions are gaining traction due to their ability to meet stringent regulatory standards. Their flexibility allows customization based on site-specific water chemistry. As zero liquid discharge objectives and reuse targets increase, hybrid systems are emerging as a preferred solution for advanced and large-scale fracking water treatment applications.

By System Type Analysis

Fixed treatment systems dominate the market due to their suitability for long-term, high-volume wastewater management. In 2025, fixed systems hold approximately 58.6% of the total market share, driven by deployment at centralized treatment facilities and major production sites. These systems offer consistent performance, higher capacity, and lower operating costs over extended periods. Fixed installations support integration of advanced technologies such as membrane filtration and zero liquid discharge solutions. Operators with sustained drilling activity favor fixed systems to achieve long-term cost optimization, regulatory compliance, and operational stability.

Mobile treatment systems are the fastest-growing system type due to their flexibility and rapid deployment capabilities. Although their market share remains lower than fixed systems, adoption is accelerating across remote and temporary drilling locations. Skid-mounted and trailer-mounted units allow on-site treatment, reducing transportation and disposal costs. These systems are especially valuable during early-stage operations when flowback volumes are high. Increasing drilling activity in remote regions and demand for scalable, cost-efficient solutions continue to drive strong growth in mobile treatment systems.

By Deployment Model Analysis

Equipment sales dominate the deployment model as operators invest in owned water treatment infrastructure. In 2025, equipment sales account for approximately 51.2% of the total market share, reflecting preference for long-term ownership and operational control. Large oil and gas operators favor capital investment to customize systems according to site-specific needs. Ownership also provides greater flexibility in system upgrades and reuse strategies. Advancements in treatment efficiency and equipment lifespan further support this model. Equipment sales remain strong among operators focused on long-term planning and sustained production activity.

Water treatment as a service is growing rapidly as operators aim to minimize upfront capital expenditure. Although its share is lower than equipment sales, adoption is increasing among small and mid-sized operators. This model provides access to advanced technologies, operational expertise, and regulatory compliance without ownership risk. Service-based deployment offers predictable costs and scalability. Market volatility and the need for flexible water management solutions are accelerating acceptance of outsourced water treatment services.

By Application Analysis

Water recycling and reuse represent the leading application segment, accounting for approximately 60.3% of the market share in 2025. This dominance is driven by water scarcity, rising disposal costs, and sustainability commitments. Recycling treated wastewater reduces freshwater sourcing and lowers operational expenses. Regulatory incentives further promote reuse practices across shale basins. Advanced treatment technologies enable high-quality recycled water suitable for repeated fracturing operations. As operators focus on environmental responsibility and cost efficiency, recycling and reuse remain central to fracking water management strategies.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Zero liquid discharge is the fastest-growing application segment as regulatory pressure on wastewater disposal intensifies. Although its current market share is smaller, adoption is increasing rapidly. ZLD systems eliminate liquid waste by recovering reusable water and converting residuals into solid by-products. These systems help operators comply with strict environmental regulations and reduce reliance on disposal wells. Improvements in thermal and hybrid technologies are enhancing feasibility, driving strong future growth.

By End User Analysis

Oil and gas operators dominate the end-user segment, accounting for approximately 63.7% of the market share in 2025. As primary generators of fracking wastewater, operators invest heavily in treatment systems to ensure compliance, cost control, and water reuse. Large operators prefer in-house or dedicated treatment infrastructure to support continuous production. Increasing drilling activity and regulatory oversight further strengthen this segment’s leadership. Water management has become a strategic priority, reinforcing operator-driven demand.

Water treatment service providers are experiencing rapid growth by offering outsourced and specialized treatment solutions. While holding a smaller share than operators, their role is expanding as outsourcing gains acceptance. These providers deliver end-to-end services, including treatment, recycling, and compliance support. Their flexibility and technological expertise make them attractive to operators seeking efficiency and reduced operational burden.

The Fracking Water Treatment Systems Market Report is segmented on the basis of the following

By Water Source

- Produced Water

- Flowback Water

- Brine Water

By Treatment Technology

- Physical Treatment

- Filtration

- Membrane Technology

- Chemical Treatment

- Coagulation and Flocculation

- Advanced Oxidation

- Thermal Treatment

- Evaporation

- Crystallization

- Hybrid Treatment

By System Type

- Fixed Treatment Systems

- On-site Systems

- Centralized Systems

- Mobile Treatment Systems

- Skid-mounted Units

- Trailer-mounted Units

By Deployment Model

- Equipment Sales

- Water Treatment as a Service

- Lease and Rental

By Application

- Water Recycling and Reuse

- Discharge Treatment

- Zero Liquid Discharge

By End User

- Oil and Gas Operators

- Onshore Operators

- Independent Operators

- Water Treatment Service Providers

Regional Analysis

Leading Region in the Fracking Water Treatment Systems Market

North America remains the leading region in the fracking water treatment systems market due to extensive shale oil and gas development, particularly across major onshore basins. In 2025, the region accounts for approximately 47.9% of the global market share, reflecting high wastewater volumes and strong regulatory oversight. Well-established infrastructure, advanced treatment technologies, and widespread adoption of water recycling practices support regional dominance. Operators in North America invest heavily in fixed and mobile treatment systems to reduce freshwater dependency and disposal costs. Stringent environmental regulations and emphasis on sustainable operations continue to drive innovation, reinforcing the region’s leadership position.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest Growing Region in the Fracking Water Treatment Systems Market

Asia-Pacific is the fastest-growing region in the fracking water treatment systems market, driven by industrial expansion, rising energy demand, and increasing concerns over water scarcity. Although its current market share is lower than North America, growth momentum is accelerating due to supportive government initiatives and infrastructure development. Countries in the region are investing in advanced water treatment technologies to improve wastewater reuse and environmental compliance. Rapid urbanization and industrialization further increase demand for efficient water management solutions. As regulatory frameworks strengthen and technological adoption rises, Asia-Pacific is expected to record the highest growth rate over the forecast period.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The fracking water treatment systems market is moderately consolidated, characterized by high entry barriers arising from significant capital requirements, stringent regulatory compliance, and the need for specialized technical expertise. Market participants emphasize technology innovation to improve treatment efficiency and address complex wastewater compositions. Service differentiation through customized solutions, modular system offerings, and integrated water management services is widely adopted. Long-term contracts with oil and gas operators provide revenue stability and strengthen client relationships. Continuous investment in research and development, strategic partnerships, and digital capabilities enables companies to enhance operational performance and sustain competitive positioning.

Some of the prominent players in the global Fracking Water Treatment Systems are

- Veolia

- SUEZ

- Schlumberger

- Halliburton

- Baker Hughes

- Ecolab

- Xylem

- Ovivo

- Pentair

- Aquatech International

- Evoqua Water Technologies

- Kurita Water Industries

- DuPont Water Solutions

- Fluence Corporation

- Thermax

- Wartsila Water Systems

- IDE Technologies

- GE Vernova

- Calgon Carbon

- LANXESS

- Other Key Players

Recent Developments

- In December 2025, SPL announced that the company has acquired Franklin Analytical, Inc., an established environmental testing laboratory in Chambersburg, Pennsylvania, which expands SPL’s environmental laboratory footprint deeper into South Central Pennsylvania, strengthening local support for municipal, industrial, and consulting clients across the region with a focus on faster turnaround times and a broader menu of services. Also, Franklin Analytical’s Chambersburg location will continue to operate with its existing team, providing continuity in service while gaining access to SPL’s broader network, expanded capabilities, and investments in quality and turnaround time.

- In April 2025, Shapiro Administration announced the investment of USD 242.8 million for 32 drinking water and wastewater projects across 23 counties through the Pennsylvania Infrastructure Investment Authority, which include replacing lead service lines, rehabilitating aging systems, upgrading service capabilities, extending service to more communities, and minimizing environmental contaminants through compliance with current regulatory levels.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 491.4 Mn |

| Forecast Value (2035) |

USD 789.0 Mn |

| CAGR (2026–2035) |

5.4% |

| The US Market Size (2026) |

USD 198.0 Mn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors, etc. |

| Segments Covered |

Segments Covered By Water Source (Produced Water, Flowback Water, and Brine Water), By Treatment Technology (Physical Treatment, Chemical Treatment, Thermal Treatment, and Hybrid Treatment), By System Type (Fixed Treatment Systems and Mobile Treatment Systems), By Deployment Model (Equipment Sales, Water Treatment as a Service, and Lease & Rental), By Application (Water Recycling and Reuse, Discharge Treatment, and Zero Liquid Discharge), By End User (Oil and Gas Operators and Water Treatment Service Providers) |

| Regional Coverage |

North America – US, Canada; Europe – Germany, UK, France, Russia, Spain, Italy, Benelux, Nordic, Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, Rest of MEA |

| Prominent Players |

Veolia, SUEZ, Schlumberger, Halliburton, Baker Hughes, Ecolab, Xylem, Ovivo, Pentair, Aquatech International, Evoqua Water Technologies, Kurita Water Industries, DuPont Water Solutions, Fluence Corporation, Thermax, Wartsila Water Systems, IDE Technologies, GE Vernova, Calgon Carbon, LANXESS, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days, and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Fracking Water Treatment Systems Market?

▾ The Global Fracking Water Treatment Systems Market size is expected to reach USD 491.4 million by 2025 and is projected to reach USD 789.0 million by the end of 2034.

Which region accounted for the largest Global Fracking Water Treatment Systems Market?

▾ North America is expected to have the largest market share in the Global Fracking Water Treatment Systems Market, with a share of about 47.9% in 2025.

How big is the Fracking Water Treatment Systems Market in the US?

▾ The US Fracking Water Treatment Systems market is expected to reach USD 198.0 million by 2025.

Who are the key players in the Fracking Water Treatment Systems Market?

▾ Some of the major key players in the Global Fracking Water Treatment Systems Market include Veolia, SUEZ, Xylem, and others

What is the growth rate in the Global Fracking Water Treatment Systems Market?

▾ The market is growing at a CAGR of 5.4 percent over the forecasted period.