Market Overview

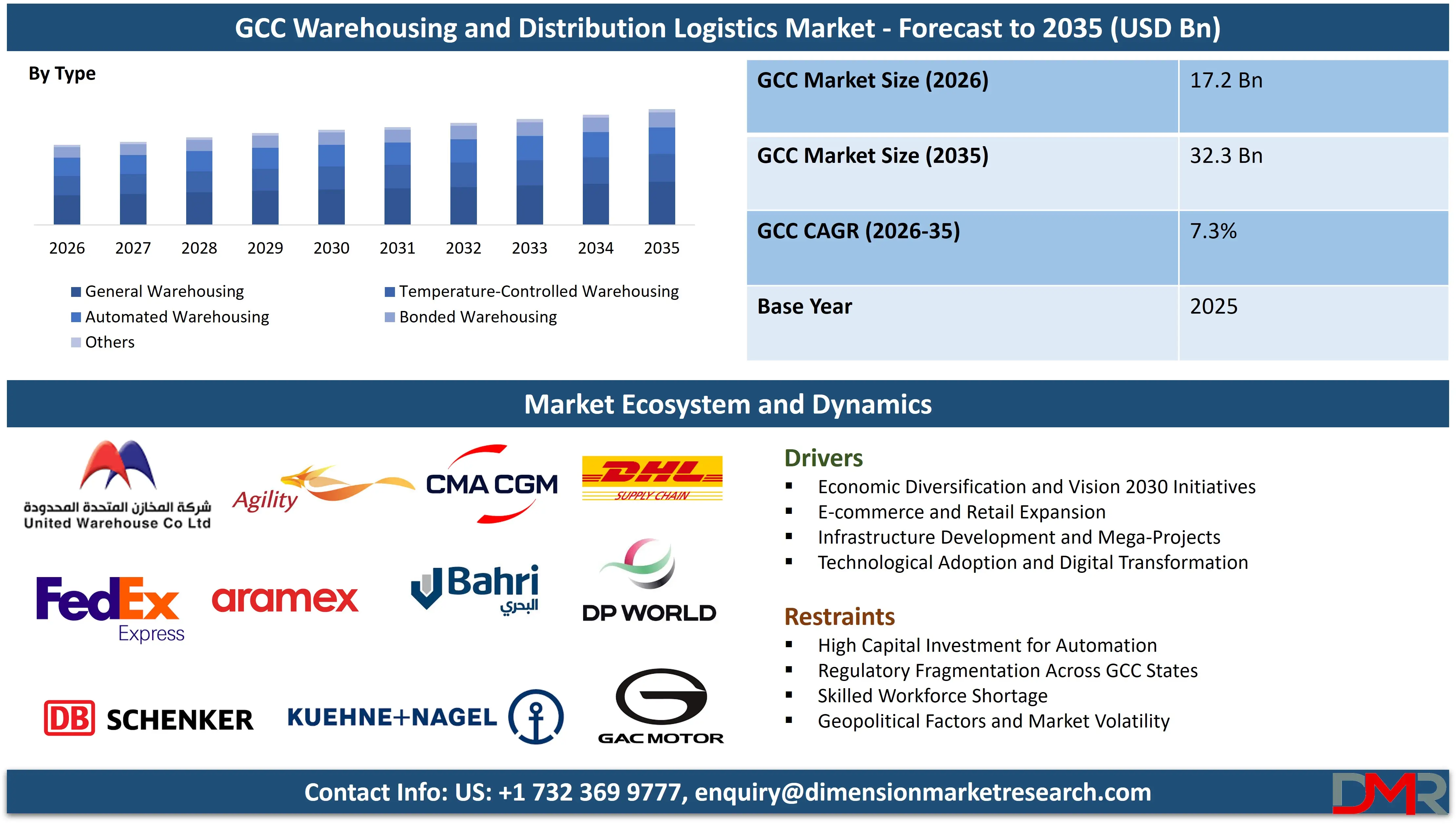

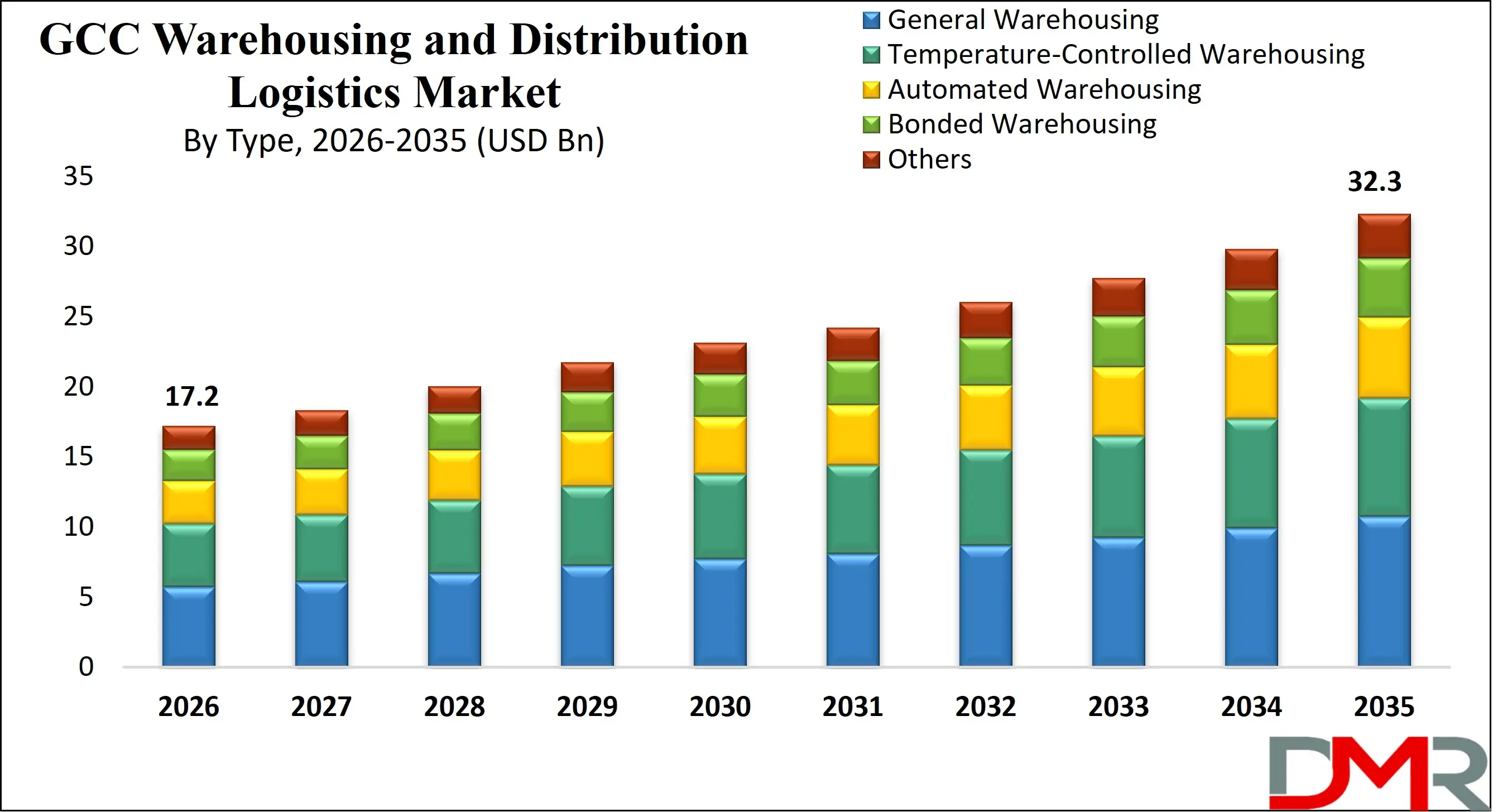

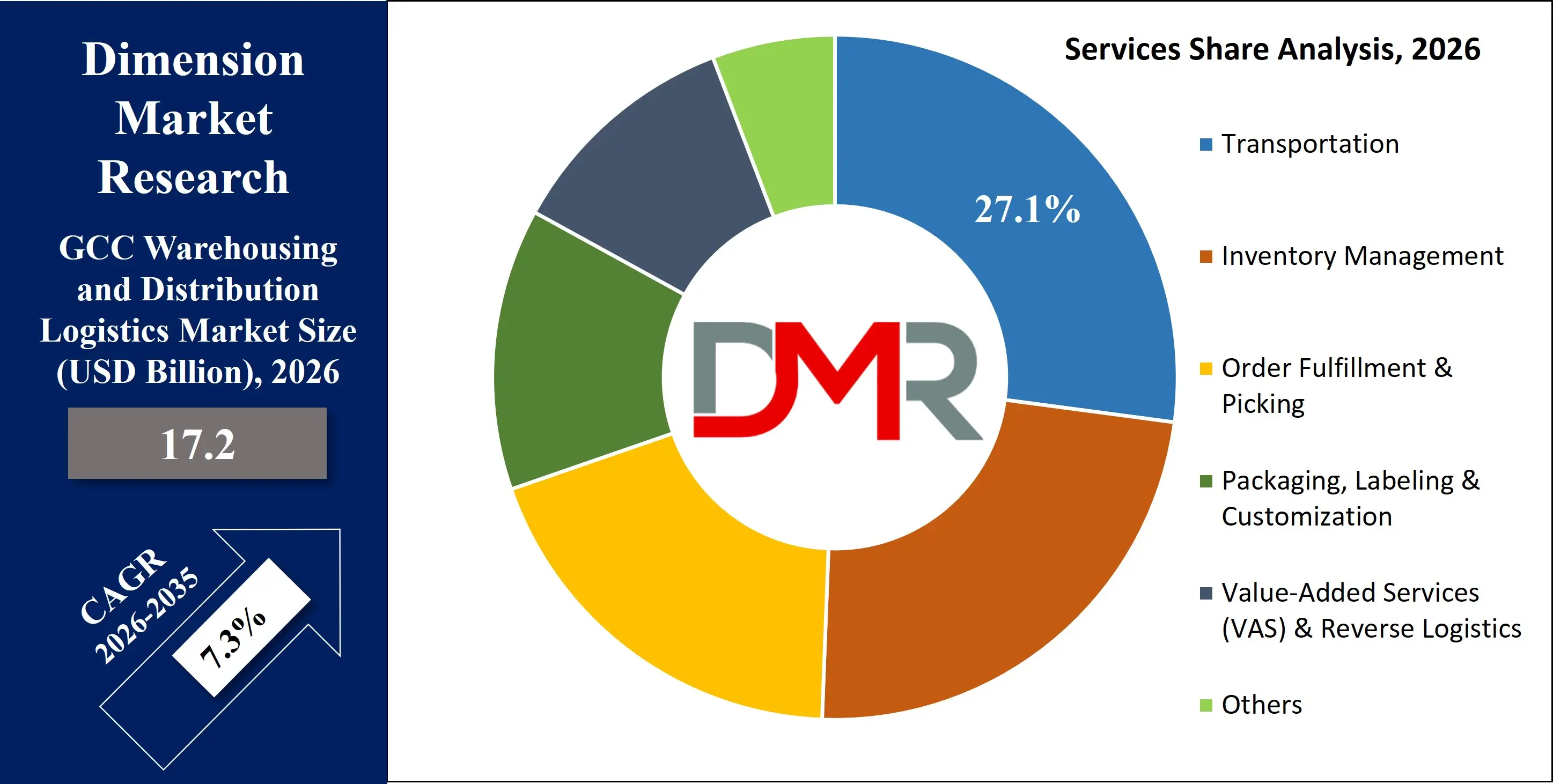

The GCC Warehousing and Distribution Logistics Market is projected to reach USD 17.2 billion in 2026 and is expected to grow at a CAGR of 7.3% from 2026 to 2035, attaining a value of USD 32.3 billion by 2035. The market's robust growth is driven by the rapid expansion of e-commerce, strategic investments in transportation infrastructure, economic diversification plans under various Vision 2030 initiatives, and the GCC's pivotal role as a global trade and logistics hub.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Warehousing and distribution logistics enable seamless supply chain operations through advanced automated storage and retrieval systems (AS/RS), multi-modal transportation networks, and integrated logistics management platforms, supporting the region's booming retail, manufacturing, and FMCG sectors. The sector addresses critical challenges related to inventory optimization, last-mile delivery efficiency, and cross-border trade facilitation.

Technological advancements, including warehouse management systems (WMS), IoT-enabled tracking, automated guided vehicles (AGVs), blockchain for supply chain transparency, and AI-driven demand forecasting, are transforming the market into a highly efficient and scalable ecosystem. Integration of robotics and automation for picking, packing, and sorting is reshaping operational productivity and accuracy.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Growing government initiatives promoting logistics free zones, smart port developments, and public-private partnerships (PPPs) further accelerate market growth. However, barriers such as high initial automation costs, regional geopolitical factors, regulatory variances across GCC states, and skilled workforce shortages remain. Despite these limitations, the convergence of digital transformation, infrastructure modernization, and sustainability mandates positions the GCC warehousing and logistics sector as a central driver of regional economic transformation through 2035.

GCC Warehousing and Distribution Logistics Market: Key Takeaways

- Strong Regional Market Growth Outlook: The GCC Warehousing and Distribution Logistics Market is expected to be valued at USD 17.2 billion in 2026 and is projected to reach USD 32.3 billion by 2035, showcasing robust expansion supported by economic diversification, e-commerce boom, and infrastructure megaprojects.

- High CAGR Driven by Digital Transformation: The market is expected to grow at an impressive CAGR of 7.3% from 2026 to 2035, fueled by accelerated adoption of automation, IoT integration, AI in supply chain management, and increasing trade volumes.

- UAE Maintains Regional Dominance: The UAE is expected to capture the largest share of the GCC market in 2026, supported by its world-class ports (Jebel Ali, Khalifa), extensive free zones, high digital adoption, and early integration of automation and AI in logistics.

- Rapid Advancement in Logistics Technologies: Innovations including AI-driven warehouse management, blockchain for customs clearance, autonomous mobile robots (AMRs), and drone-assisted inventory checks are significantly accelerating efficiency, accuracy, and scalability of logistics services.

- Growing E-commerce and Retail Sector Boosts Adoption: Rising consumer demand for fast delivery, expansion of regional e-commerce giants like Noon and Amazon.ae, and growth of omnichannel retail are driving sustained demand for modern, scalable warehousing and last-mile distribution solutions.

GCC Warehousing and Distribution Logistics Market: Use Cases

- E-commerce Fulfillment Centers: Dedicated warehouses utilizing automated sorting, robotic picking, and real-time inventory tracking to enable same-day and next-day delivery for online retail orders across the GCC.

- Temperature-Controlled Logistics for Pharmaceuticals: Specialized cold chain warehouses with IoT-enabled temperature monitoring ensuring integrity of vaccines, biologics, and medicines during storage and distribution.

- Bonded Warehousing and Re-export Hubs: Free zone warehouses offering deferred customs duties, facilitating regional re-export activities and serving as consolidation points for international trade.

- Automated Storage for Manufacturing Support: High-bay automated warehouses integrated with manufacturing plants for just-in-time (JIT) supply of raw materials and components.

- Last-Mile Delivery Optimization Hubs: Urban micro-fulfillment centers and dark stores strategically located to reduce delivery times and costs in dense metropolitan areas like Dubai, Riyadh, and Doha.

GCC Warehousing and Distribution Logistics Market: Stats & Facts

- The GCC Secretariat notes that over 35% of regional trade flows through UAE ports, reinforcing how integrated warehousing and distribution networks are critical for the GCC's position as a global trade corridor, especially as regional non-oil trade volumes grow at ~7% annually.

- The World Bank Logistics Performance Index (LPI) ranks the UAE among the top 10 globally, highlighting advanced infrastructure, customs efficiency, and logistics competence that drive warehousing investments, while Saudi Arabia and Qatar show the most significant LPI improvement in recent years.

- The GCC Pharmaceutical Industry Analysis notes cold chain logistics demand is growing over 15% annually, driven by increased healthcare spending and local pharmaceutical production; temperature-controlled warehouse space is expected to double by 2030.

- According to GCC Industrialization Surveys, over 40% of manufacturing firms plan to invest in automated warehouse solutions in the next five years to support operational efficiency and Industry 4.0 integration.

- The International Air Transport Association (IATA) reports GCC airports handle over 25% of global air cargo, creating immense demand for high-speed, airport-adjacent logistics parks and distribution centers for time-sensitive goods.

GCC Warehousing and Distribution Logistics Market: Market Dynamic

Driving Factors in the GCC Warehousing and Distribution Logistics Market

Economic Diversification and Vision Plans

The strategic economic diversification agendas under various GCC Vision 2030 plans are major drivers for logistics market growth. Reducing dependency on oil revenues necessitates the development of robust non-oil sectors like manufacturing, tourism, and retail, all of which require sophisticated logistics support. Mega-projects such as NEOM, Red Sea Project, Qiddiya, and Dubai Expo City generate massive demand for construction logistics, material warehousing, and ongoing operational supply chains. National programs like Saudi Arabia's NIDLP and the UAE's Operation 300bn explicitly target logistics as a key economic pillar, channeling significant public and private investment into infrastructure, technology, and sectoral development.

E-commerce and Retail Expansion

The unprecedented growth of e-commerce and the evolution of omnichannel retail in the GCC are fundamentally transforming warehousing and distribution needs. Consumers increasingly expect faster delivery times, flexible returns, and seamless shopping experiences. This drives demand for strategically located fulfillment centers, urban last-mile hubs, and highly automated warehouses capable of processing high order volumes efficiently. The rise of local e-commerce platforms and the strong presence of international players are accelerating investments in logistics real estate and technology, making this a primary growth engine for the market.

Restraints in the GCC Warehousing and Distribution Logistics Market

High Capital Investment for Automation

While automation is a key trend, the high upfront capital expenditure required for automated storage and retrieval systems (AS/RS), robotics, and integrated software platforms can be a significant barrier, particularly for small and medium-sized logistics operators. The total cost of ownership, including maintenance, software updates, and specialized training, can strain profitability in a competitive market with tight margins. This financial hurdle can slow the pace of technological adoption across the entire sector, potentially creating a divide between large, well-funded players and smaller, traditional operators.

Regulatory Fragmentation and Skilled Workforce Shortage

Despite GCC economic integration efforts, regulatory and customs procedures still vary across member states, adding complexity and cost to cross-border distribution. Inconsistent standards for warehousing, labeling, and transport can create inefficiencies. Furthermore, the region faces a pronounced shortage of skilled logistics professionals adept at managing advanced technologies like WMS, AI, and robotics. This talent gap can impede the optimal implementation and operation of modern logistics solutions, restricting market growth potential.

Opportunities in the GCC Warehousing and Distribution Logistics Market

Adoption of Green and Sustainable Logistics

There is a significant opportunity for growth in green logistics initiatives, driven by both regional sustainability goals (like UAE Net Zero 2050, Saudi Green Initiative) and global supply chain pressures. This includes the development of LEED-certified warehouses with solar power, energy-efficient lighting, and water recycling systems. Opportunities also exist for electric and hydrogen-fueled fleets for distribution, carbon footprint tracking solutions, and reverse logistics programs for waste reduction and recycling. Companies that pioneer sustainable practices can gain competitive advantage, attract partnerships, and comply with evolving regulations.

Expansion of Cold Chain Logistics

The growth of pharmaceuticals, perishable food imports, and specialty chemicals in the GCC creates a major opportunity for temperature-controlled logistics. There is increasing demand for cold storage warehouses, refrigerated transportation, and end-to-end monitoring solutions. Investments in modern cold chain infrastructure, particularly with real-time IoT tracking for quality assurance, can capture value in this high-margin, specialized segment and support food security and healthcare objectives across the region.

Trends in the GCC Warehousing and Distribution Logistics Market

Micro-Fulfillment and Dark Stores

To overcome last-mile delivery challenges in urban areas, retailers and logistics providers are increasingly deploying micro-fulfillment centers (MFCs) and dark stores. These small, automated warehouses located within city limits are dedicated to online order picking and packing, enabling delivery within hours. This trend reduces delivery costs, lowers road congestion, and enhances customer satisfaction, becoming a critical component of urban logistics strategy in dense GCC cities.

Digital Twins and Supply Chain Visibility

The use of digital twin technology is emerging as a key trend for optimizing warehouse design and operations. A digital twin is a virtual replica of a physical warehouse that simulates processes, tests layouts, and predicts bottlenecks. Coupled with IoT sensors and AI analytics, it provides unprecedented real-time visibility into inventory levels, equipment status, and workflow efficiency across the entire supply chain. This enables proactive decision-making, reduces downtime, and improves overall operational resilience.

GCC Warehousing and Distribution Logistics Market: Research Scope and Analysis

By Type Analysis

General Warehousing is projected to dominate the GCC market due to its versatility and high demand from a broad range of sectors including retail, FMCG, construction, and general trading. These warehouses provide essential storage space for non-specialized goods and form the backbone of the region's distribution networks. Their dominance is reinforced by the ongoing construction boom and the expansion of trade volumes, which require vast amounts of flexible storage space. While other specialized segments are growing faster, the sheer volume and fundamental need for general warehousing ensure it holds the largest market share.

Temperature-Controlled Warehousing is anticipated to be the fastest-growing segment within the type category. This growth is driven by the region's harsh climate, rising food safety standards, expanding pharmaceutical sector, and increasing imports of perishable goods. Investments in advanced cold chain infrastructure with multi-temperature zones and real-time monitoring are rising significantly to cater to this demand.

By Service Analysis

Transportation Management is poised to be the largest service segment, as it represents the core link between warehouses and end consumers or businesses. This includes first-mile, middle-mile, and last-mile logistics. Its dominance is driven by the GCC's geographic expanse, the need to connect ports and airports with hinterlands, and the critical importance of last-mile delivery for e-commerce. Efficiency gains through route optimization software, fleet management systems, and multi-modal integration are key focuses within this segment.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Inventory Management ranks as the second-largest service segment due to its critical role in optimizing stock levels, reducing carrying costs, and preventing stockouts or overstock situations. The adoption of cloud-based Warehouse Management Systems (WMS) and AI-driven demand forecasting tools is transforming this service from a manual tracking exercise into a strategic, data-driven function that enhances overall supply chain responsiveness and efficiency.

By End User Analysis

Retail & E-commerce are anticipated to dominate the warehousing and distribution logistics market as the primary end-users. This sector's explosive growth, driven by changing consumer behavior and digital adoption, creates relentless demand for modern fulfillment centers, efficient returns processing (reverse logistics), and agile last-mile delivery networks. The need for speed, accuracy, and scalability makes this segment the largest investor in automated and technology-driven logistics solutions.

Manufacturing is the second-largest end-user segment. A growing regional manufacturing base, supported by industrial strategies like Saudi Arabia's NIDLP and the UAE's Operation 300bn, requires sophisticated logistics for raw material inbound, work-in-progress storage, and finished goods outbound. Just-in-Time (JIT) and lean manufacturing principles are increasing the integration between production lines and automated warehouse systems.

The GCC Warehousing and Distribution Logistics Market Report is segmented on the basis of the following

By Type

- General Warehousing

- Temperature-Controlled Warehousing

- Automated Warehousing

- Bonded Warehousing

- Others

By Service

- Transportation

- Inventory Management

- Order Fulfillment & Picking

- Packaging, Labeling & Customization

- Value-Added Services (VAS) & Reverse Logistics

- Others

By End User

- Retail & E-commerce

- Manufacturing

- Food & Beverage

- Pharmaceuticals & Healthcare

- Automotive

- Chemicals

- Construction

- Others

Regional Analysis

The GCC Warehousing and Distribution Logistics Market shows diverse regional dynamics across the Gulf Cooperation Council countries, including Saudi Arabia, the United Arab Emirates, Qatar, Kuwait, Oman, and Bahrain. The region’s strategic geographic location between Asia, Europe, and Africa positions it as a major international logistics corridor. Strong maritime routes, large seaports, and expanding air cargo hubs enable efficient trade connectivity, making the GCC an important distribution gateway for global supply chains. Government initiatives aimed at economic diversification and trade expansion have also accelerated the development of modern logistics infrastructure across the region.

Saudi Arabia represents the dominant logistics hub within the GCC due to its large domestic market, extensive industrial base, and strong government support for logistics development. National transformation programs are encouraging the establishment of integrated logistics zones, advanced warehousing parks, and improved transport corridors. These developments are strengthening the country’s role as a regional distribution center connecting major production and consumption markets across the Middle East.

The United Arab Emirates plays a crucial role as a regional trade and re-export hub. Its advanced port infrastructure, free trade zones, and multimodal transport connectivity allow companies to operate regional distribution centers serving markets across the Middle East, Africa, and South Asia. Favorable regulatory frameworks and strong foreign investment have further supported the expansion of warehousing facilities and third-party logistics services in the country.

Other GCC countries, including Qatar, Kuwait, Oman, and Bahrain, are also strengthening their logistics capabilities through port expansions, infrastructure modernization, and trade facilitation initiatives. These economies are focusing on improving supply chain efficiency and attracting international logistics operators. Overall, regional collaboration and infrastructure investment continue to position the GCC as an emerging global hub for warehousing and distribution logistics.

By Region

- United Arab Emirates (UAE)

- Saudi Arabia (KSA)

- Qatar

- Kuwait

- Oman

- Bahrain

Impact of Artificial Intelligence in the GCC Warehousing and Distribution Logistics Market

- AI for Demand Forecasting and Inventory Optimization: AI analyzes historical sales data, market trends, and external factors (like seasonality, promotions) to predict future demand with high accuracy. This optimizes stock levels across the network, reduces excess inventory, and minimizes stockouts.

- AI-Powered Warehouse Robotics: AI algorithms guide Autonomous Mobile Robots (AMRs) and robotic arms for tasks like picking, sorting, and palletizing. These systems learn from operation patterns, optimize travel paths in real-time, and collaborate safely with human workers, dramatically increasing throughput and accuracy.

- Intelligent Transportation Management: AI optimizes delivery routes by processing real-time data on traffic, weather, fuel costs, and delivery windows. It enables dynamic route adjustments, improves fleet utilization, and reduces last-mile delivery costs and times.

- Predictive Maintenance for Logistics Assets: AI monitors data from sensors on warehouse equipment (conveyors, forklifts, AS/RS) and vehicles to predict potential failures before they occur. This minimizes unplanned downtime, extends asset life, and reduces maintenance costs.

- AI-Enhanced Yard Management: AI streamlines yard operations by automatically scheduling dock appointments, tracking trailer locations in real-time, and optimizing the flow of goods between the yard and the warehouse, reducing truck turnaround times and congestion.

GCC Warehousing and Distribution Logistics Market: Competitive Landscape

The GCC Warehousing and Distribution Logistics Market is moderately fragmented and highly competitive, featuring a mix of global third-party logistics (3PL) giants, regional powerhouse conglomerates, and specialized technology-driven players. Leading international firms like DHL Supply Chain, DB Schenker, Kuehne+Nagel, and Agility dominate the market with their integrated service offerings, global networks, and advanced technological capabilities. Regional giants such as DP World (UAE), Aramex (UAE), and Bahri (KSA) leverage deep local expertise and extensive infrastructure assets.

A key competitive trend is the vertical integration of services, where port operators and free zone developers also offer end-to-end logistics solutions. Technology-focused innovators and automation specialists are also gaining prominence by partnering with traditional players to deploy AI, robotics, and IoT solutions.

Some of the prominent players in the GCC Warehousing and Distribution Logistics Market are

- DHL Supply Chain

- DB Schenker

- Kuehne+Nagel

- Agility

- DP World

- Aramex

- Bahri Logistics

- GAC

- CEVA Logistics (CMA CGM)

- FedEx Express

- United Warehousing Company (UWC) - KSA

- RSA Logistics (UAE)

- Tristar Transport

- LSC Warehousing & Logistics - KSA

- Al-Futtaim Logistics

- Other Key Players

Recent Developments in the GCC Warehousing and Distribution Logistics Market

- November 2025: DP World inaugurated a state-of-the-art, fully automated temperature-controlled warehouse in Jebel Ali. The facility utilizes robotic palletizing and AI-driven inventory management, targeting the growing pharmaceutical and perishable food logistics sectors and strengthening Dubai's cold chain capabilities.

- October 2025: The Saudi Arabian Railways (SAR) unveiled plans for a major expansion of its integrated logistics parks in Riyadh and Dammam. The expansion focuses on integrating rail sidings with automated warehousing to offer seamless multi-modal solutions, supporting NIDLP objectives.

- October 2025: Agility entered a strategic partnership with a leading robotics company to deploy autonomous mobile robots (AMRs) across its key fulfillment centers in Kuwait and the UAE, aiming to boost picking efficiency by 40% and reduce operational costs.

- September 2025: Aramex opened a new AI-powered regional sorting and distribution hub in Dubai South. The hub features computer vision for package sorting and real-time data analytics to optimize cross-border e-commerce parcel flows across the GCC.

- August 2025: AD Ports Group completed a strategic acquisition to expand its integrated logistics footprint across the GCC, gaining access to a network of general and bonded warehouses in Oman, Saudi Arabia, and Qatar.

- June 2025: The 2025 GCC Logistics Tech Summit showcased innovations in green warehousing, electric last-mile vehicles, and blockchain for sustainable supply chain tracking, reflecting the region's growing commitment to eco-friendly logistics.

- March 2025: Bahrain launched the development of a new dedicated "Logistics City" near Khalifa Bin Salman Port, featuring bonded warehousing, light manufacturing units, and commercial spaces to attract 3PLs and support re-export activities.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 17.2 Bn |

| Forecast Value (2035) |

USD 32.3 Bn |

| CAGR (2026–2035) |

7.3% |

| The US Market Size (2026) |

USD 97.0 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors, etc. |

| Segments Covered |

By Type (General Warehousing, Temperature-Controlled Warehousing, Automated Warehousing, Bonded Warehousing, Others), By Service (Transportation, Inventory Management, Order Fulfillment & Picking, Packaging, Labeling & Customization, Value-Added Services (VAS) & Reverse Logistics, Others), By End User (Retail & E-commerce, Manufacturing, Food & Beverage, Pharmaceuticals & Healthcare, Automotive, Chemicals, Construction, Others) |

| Regional Coverage |

United Arab Emirates (UAE), Saudi Arabia (KSA), Qatar, Kuwait, Oman, and Bahrain |

| Prominent Players |

DHL Supply Chain, DB Schenker, Kuehne+Nagel, Agility, DP World, Aramex, Bahri Logistics, GAC, CEVA Logistics (CMA CGM), FedEx Express, United Warehousing Company (UWC) - KSA, RSA Logistics (UAE), Tristar Transport, LSC Warehousing & Logistics - KSA, Al-Futtaim Logistics, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days, and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the GCC Warehousing and Distribution Logistics Market?

▾ The GCC Warehousing and Distribution Logistics Market size is estimated to have a value of USD 17.2 billion in 2026 and is expected to reach USD 32.3 billion by the end of 2035.

What is the growth rate in the GCC Warehousing and Distribution Logistics Market?

▾ The market is growing at a CAGR of 7.3 percent over the forecasted period of 2026 to 2035.

Which country accounted for the largest GCC Warehousing and Distribution Logistics Market?

▾ The United Arab Emirates (UAE) is expected to have the largest market share in the GCC Warehousing and Distribution Logistics Market.

Who are the key players in the GCC Warehousing and Distribution Logistics Market?

▾ Some of the major key players in the GCC Warehousing and Distribution Logistics Market are DHL Supply Chain, DB Schenker, Kuehne+Nagel, Agility, DP World, Aramex, Bahri Logistics, and many others.