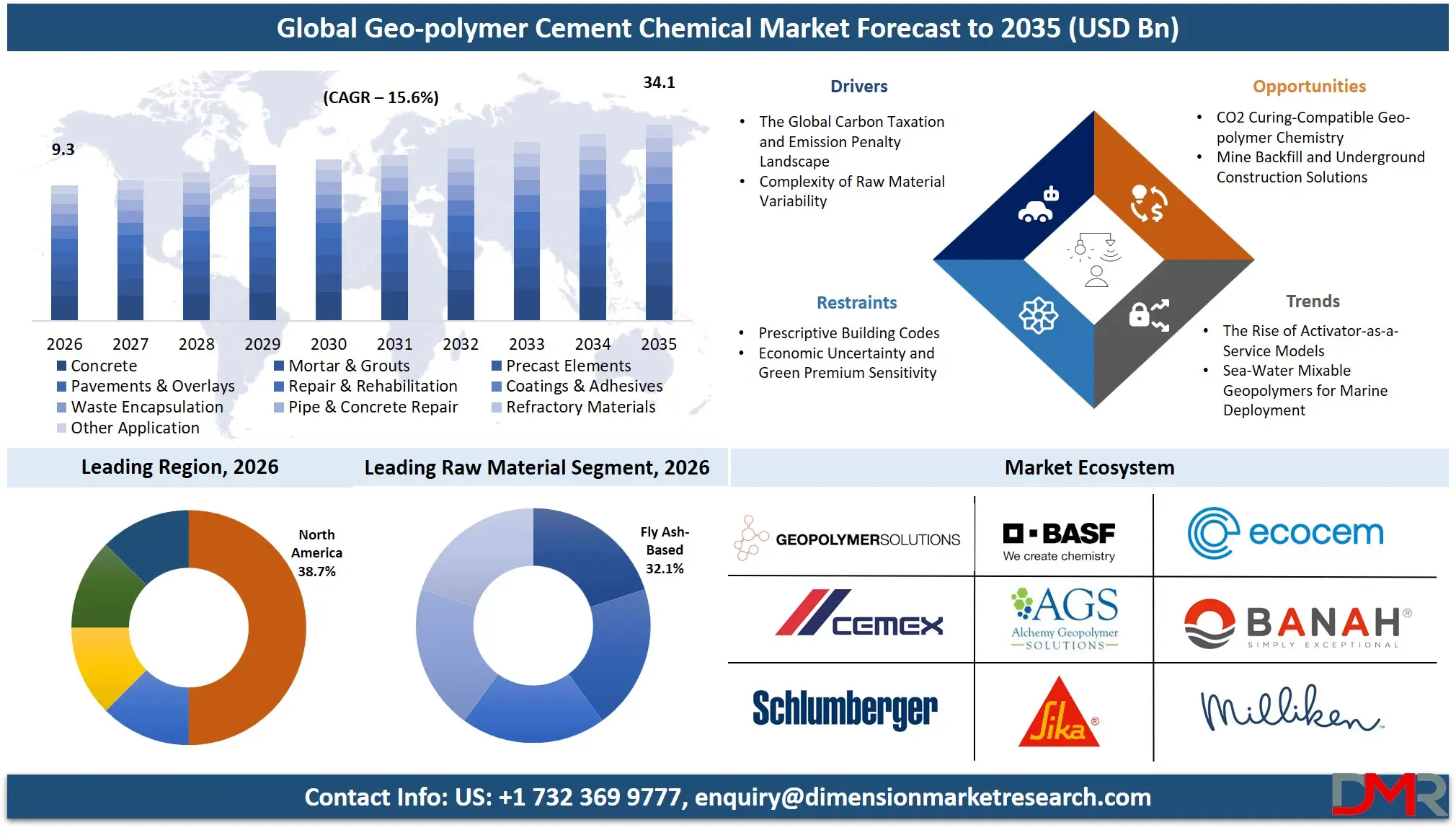

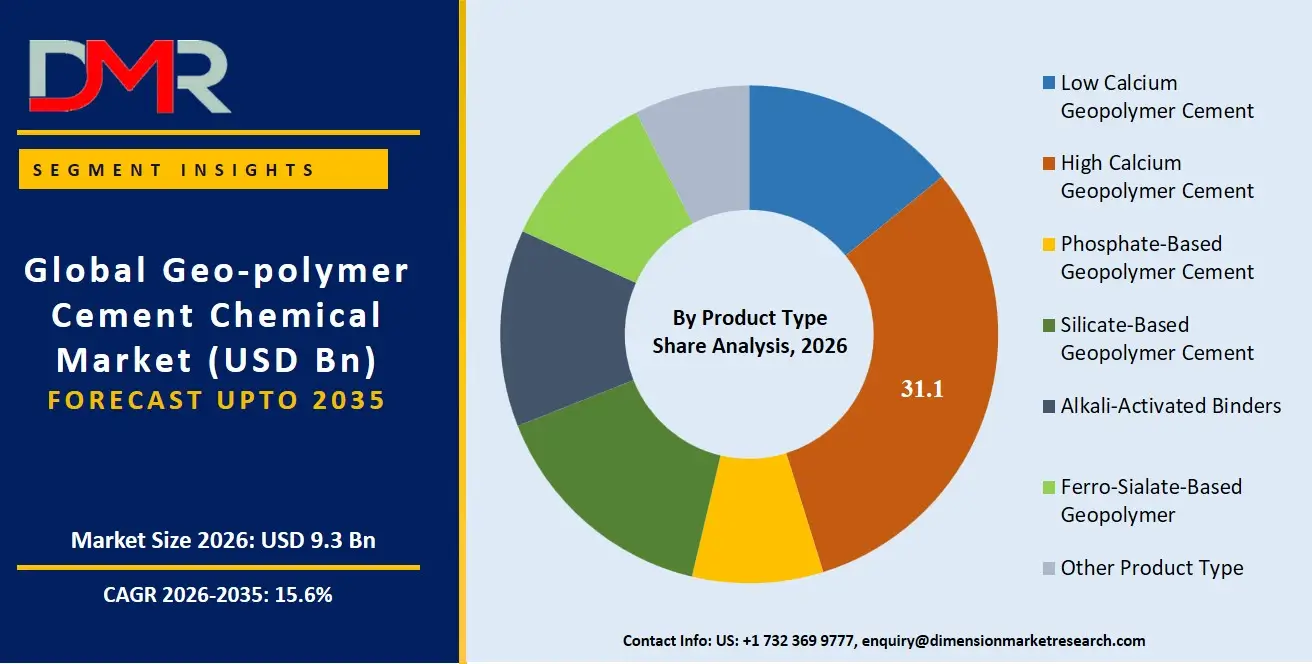

What is the Global Geo-polymer Cement Chemical Market Size?

The Global Geopolymer Cement Chemical Market is expected to reach a value of USD 9.3 billion in 2026, and it is further anticipated to reach USD 34.1 billion by 2035, growing at a CAGR of 15.6% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

There have been many changes in the geopolymer cement chemical market due to the fast pace in the adoption of sustainable materials as well as shifting from OPC (Ordinary Portland Cement) which is environmentally harmful to sustainable forms of cement. This market includes special chemicals used to formulate binders as well as source materials that are necessary for the formation of cement with an extremely low carbon footprint. The increased demand for circular economy principles and green buildings is what necessitates the need for special chemical knowledge. Construction companies as well as infrastructural agencies have been the main adopters. Fly ash-based and slag-based geopolymers have been the most common geopolymer materials due to waste valorization and high chemical durability respectively.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

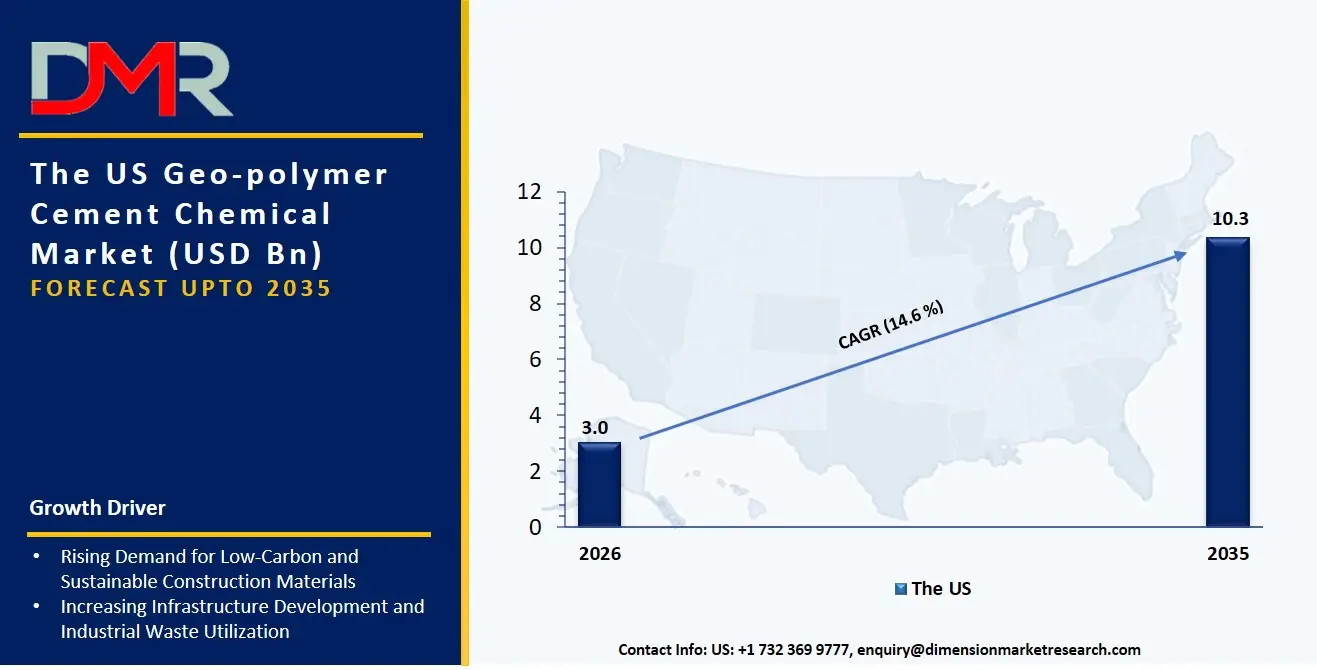

The US Geo-polymer Cement Chemical Market

The US Geopolymer Cement Chemical Market is projected to reach USD 3.0 billion in 2026 at a compound annual growth rate of 14.6% over its forecast period, which further expected to reach a value of USD 10.3 billion by 2035. The United States still stands out as the biggest and most sophisticated market for geopolymer cement chemicals owing to the ongoing modernization endeavors from federal government infrastructure schemes and increased presence of advanced materials manufacturing plants in the region. The market has mainly been characterized by high demand for geopolymer cement formulations with low calcium levels where enterprises target designing durable transportation infrastructures that experience little shrinkage and exhibit improved sulfate resistance properties. Moreover, the use of advanced chemical activators during precast activities is leading to similar demand for geopolymer cements with phosphate as the key raw material.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Europe Geo-polymer Cement Chemical Market

The Europe Geopolymer Cement Chemical Market is estimated to be valued at USD 2.7 billion in 2026 and is further anticipated to reach USD 9.5 billion by 2035 at a CAGR of 15.0%. The regulations that govern EU Emissions Trading Scheme (EU ETS) and Construction Product Regulations (CPR) are having a significant influence on the European market, thus making it necessary to adopt alkali-activated binders and standardized, performance-based chemical formulations. The rapid adoption of metakaolin-based and natural aluminosilicate-based geopolymer cement in Europe is also due to the attempts by the French and Italian restoration and heritage conservation industries to find a good balance between materials' compatibility and sustainability. In addition, initiatives such as the EU Green Deal are pushing chemical manufacturers to develop a special line of activators based on waste glass for a truly circular material life cycle.

The Japan Geo-polymer Cement Chemical Market

The Japan Geopolymer Cement Chemical Market is projected to be valued at USD 430.3 million in 2026 at a CAGR of 14.2%. The Japanese market has distinct features that stem from the national approach to seismic resistant construction and industrial waste management as a response to an ageing population and concrete infrastructure. This leads to the use of ready mix geopolymer cements made of ferro-sialate-based geopolymers as a huge part of total spending, where large conglomerates work on creating disaster-resistant constructions along with rapid setting mortar products. However, integration into local market conditions is vital as there is a significant requirement for bridging the gap between conventional techniques used in Japan and the new chemical activators system, creating another niche product category.

Key Takeaways

- Market Size & Forecast: The Global Geopolymer Cement Chemical market is projected to reach USD 9.3 billion in 2026, expanding dramatically to USD 34.1 billion by 2035, on account of the combined effects of rising decarbonization policies and the necessity to recycle industrial by-products as building materials.

- Growth Rate & Outlook: Global market growth rate is anticipated grow at CAGR of 15.6% driven by volatility in conventional cement market and increasing difficulty of formulation of activators' chemistry for different applications.

- Primary Growth Drivers: Main factors include industry transition towards low-carbon OPC to low CO2 alternatives, requirement for specially developed activator chemicals to avoid efflorescence and alkali-silica reactions, and development of precast production lines that require special mix and dry mixing technology.

- Key Market Trends: Major trends include growing importance of developing application-specific binder chemistries, application of artificial intelligence for optimizing activator chemistry blend in order to develop optimal mixing formula for locally available raw materials and phosphate-based geopolymer cements in aerospace industry.

- By Product Type Analysis: The High Calcium Geopolymer Cement type segment is poised to dominate owing to quick hardening, short curing duration, and enhanced durability of the product. Compatibility with traditional building methods, combined with wide usage in infrastructure and pre-cast applications, will lead to widespread use of geopolymer cement chemicals in industrial and commercial construction activities around the globe.

- By End-Use Industry Analysis: Infrastructure Development is projected to dominate owing to growing investments made for building bridges, roads, tunnels, airports, and utilities by governments. The government’s preference for using geopolymer cement chemicals in order to limit carbon emissions while making buildings durable will boost demand.

- Regional Leadership: North America is poised to dominate this market with 38.7% of the market share in 2026 due to its well-developed technological ecosystem that utilizes advanced material science to its fullest and makes it a leader in this market.

What is the Geopolymer Cement Chemical?

The Geopolymer Cement Chemicals are the unique raw materials supply, the activator mix development, and the binder formulation design that are provided by chemists, material scientists, and specialty consultants to support construction companies throughout their entire materials cycle. Such services, in contrast to ordinary cement consumption (powder itself), have something to do with the process of geopolymerization itself. This includes the provision of a source of raw materials to ensure a stable and reactive supply of aluminosilicates, the choice of the activator chemicals type to regulate dissolving and polycondensation reaction without halting construction activities, and formulation mixing to make sure that geopolymer binders could be used as replacement or supplement of existing OPC-based systems. The fact that over 75% of precast factories consider geopolymer use implies the need for chemical specialty to ensure rheological behavior and durability of constructions.

Use Cases

- Marine Infrastructure Rehabilitation in Coastal Cities: Port management employs expert chemical engineers to formulate slag-based and alkali-activated binder mortars used to rebuild deteriorated dock substructures, exhibiting excellent chloride resistance and fast-strength characteristics without any carbon emissions of conventional repair concrete mixes.

- Fireproofing Tunnel Linings in Transportation: Tunnel boring constructions deploy dry-mixed formulations and ferro-sialate geopolymer chemical additives for casting segmental lining structures that intrinsically possess fire-resistance up to 1,200°C without additional insulation boards and adhering to strict safety standards.

- Nuclear Waste Encapsulation in Energy: National energy laboratories employ phosphate geopolymer cements and a combination of alkali activation to engineer custom waste immobilizing matrices that chemically isolate radioactive isotopes, ensuring their structural stability over millions of years with zero degradation of matrix.

- Modular Housing Panel Production: Offsite building factories use ready-mixed formulations of fly ash geopolymer cements with automation processes for casting of housing panel units, allowing for a single-day mold turn-around and reducing their carbon footprint by 80%.

How AI is Transforming the Geo-polymer Cement Chemical Market?

The application of AI technologies in the geopolymer cement chemistry industry will accelerate the optimization process and quality control process for activator chemicals. With regard to activator chemical type development, the use of AI-powered spectroscopy will enable researchers to automatically determine how new aluminosilicate sources will react with the sodium hydroxide activator or potassium silicate activator, thereby saving time and lowering risks during the trial-mixing and testing phase. In the ready mix formulation domain, manufacturers can ensure mix design consistency and quality control by monitoring viscosity fluctuations on-site, prediction, determination of ultimate compressive strength, and recommendations for measures such as adjusting the water-glass modulus.

Raw material supply and lifecycle assessment initiatives are centered around the use of AI technology as well. Raw material analysis involves the use of intelligent compliance-monitoring software agents that constantly monitor the supply chain networks for fly ash and slag for heavy metal leaching risks, carbon content abnormalities, and vulnerability to interruptions in the network to maintain standard formulations in accordance with ASTM C618 and EN 450.

Market Dynamics

Key Drivers in the Global Geo-polymer Cement Chemical Market

The Global Carbon Taxation and Emission Penalty Landscape

Global corporations face higher regulatory fines due to CO2 emissions arising from production of OPC, which contributes approximately 8% of global anthropogenic CO2. Regulatory fines are rising at a faster rate compared to how efficient cement production facilities can become, causing a structural cost advantage that favors geopolymer binders over OPC within certain regions. There is therefore an emerging phenomenon whereby construction companies are enforcing use of alternative geopolymer binders instead of depending on regular cement supplies. Such material changes call for activator chemicals, material sourcing qualifications, and formulations specific to those materials. The expertise of the chemistry involved in these activities can be out-sourced by construction companies as a means of fast-tracking their path to net zero and avoiding penalties from carbon border adjustments.

Complexity of Raw Material Variability

Large-scale construction projects would also make use of aluminosilicate precursors from a number of sources of power plants and industries such as fly ash, ground granulated blast furnace slag, and silica fume in order for them not to depend on a single vendor and to be safe in terms of volume of supply. However, managing the chemical variation of these industrial by-products will be very difficult indeed. Material scientists will have to coordinate the reactive silica-to-alumina ratio, glass formation, and heavy metal passivation of different batches through different types of chemical activators. This may lead to major efflorescence, setting time variations, and even strength loss without the help of chemical experts. Hence, the growing demand of chemical activator design service has been observed.

Restraints in the Global Geo-polymer Cement Chemical Market

Prescriptive Building Codes

It is worth noting that most of the world's construction codes are based on prescriptive codes which are made exclusively for OPC chemistry and have been in existence for very long time, and are quite entrenched within liability and insurance framework. Such archaic codes are one of the greatest barriers against change, especially since geopolymers present themselves as more durable material for most environments. It would take a lot of effort as well as risks in changing codes which specify compliance requirements as well as test methods for new chemistries such as phosphates or ferro sialate based geopolymers. Certification requiring years and years of testing in practical application requires very long time for approvals and academic validation. Construction players fear liability, defects and potential legal battles.

Economic Uncertainty and Green Premium Sensitivity

Unstable economies and erratic real estate cycles have led to developers becoming more reluctant to invest in new materials technologies which appear to incur additional costs because of the green factor. While reducing embodied carbon is still considered a key strategy, the pressure is on the owners of projects to explain every single material cost incurred, and ensure that there is an immediate cost benefit when compared to OPC. There will be more scrutiny of the fees involved, especially with regard to the lengthy tests for the various custom activator chemicals provided by chemical suppliers.

Growth Opportunities in the Global Geo-polymer Cement Chemical Market

CO2 Curing-Compatible Geopolymer Chemistry

One of the most promising areas for development in the geopolymer cement chemical market is helping precast concrete producers develop specific binders which will be able to sequester carbon dioxide during the process of hardening to produce carbon sinks. While there have been a number of attempts from the producers to use low calcium geopolymer cements, now their interest is in special activator additives which will raise carbonation capacity while not affecting the protection properties of steel reinforcing structures. Special knowledge and experience in developing such sophisticated chemical systems require special know-how regarding mixed alkaline activators, sodium silicate-based accelerators, and nano-porosity manipulation. Such chemicals will enable precasters to launch carbon negative and high early strength product lines to help generate carbon credits and sell more materials.

Mine Backfill and Underground Construction Solutions

It is necessary to understand both the chemistry of geochemistry and the chemistry involved in underground operations to explain the increased involvement of chemical suppliers in searching for an alternative to OPC used in tailings backfill in mining. It refers to the highly sulfate environment of mines, high deep stope hydration temperature requirements, and the requirement of autonomous tailing backfilling operations. Therefore, there is a requirement for implementation partners in the mining industry who can understand the chemistry of slag geopolymer and the underground safety regulations.

Trends in the Global Geo-polymer Cement Chemical Market

The Rise of Activator-as-a-Service Models

The model of chemical supply is being increasingly considered by the makers of construction materials as an alternative approach to the conventional transactional bulk chemical procurement. The makers have been integrating the use of ready-mix geopolymer systems where the activator admixture chemicals are supplied in ready-mixed form to the batching plants as opposed to the approach where the caustic raw chemicals procurement, batching and handling are handled by different groups operating independently from each other. This makes it possible to batch in the same manner as plasticizers.

Sea-Water Mixable Geopolymers for Marine Deployment

It should be noted that coastal resilience is another aspect being developed in the choice of infrastructure as the governments are expected to meet their objective of coastal protection while avoiding disruptions to the logistics coming from island nations. It has become important for contractors to make use of geopolymer cements since they contribute towards increasing the durability of structures and lowering logistical costs through using the seawater and sea dredge aggregates that can be found locally. As a result, it has become essential to obtain chloride resistant geopolymer formulation services. Such chemicals are designed to ensure that the potassium silicate systems resist chloride induced reinforcement corrosion.

Research Scope and Analysis

The global geo-polymer cement chemical market report is segmented by product type, raw material, activator chemical type, formulation type, application, and end-use industry. The market includes alkali-activated binders, fly ash-based materials, silicate activators, ready-mix formulations, infrastructure applications, and construction demand across residential, commercial, and industrial sectors globally.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Product Type Analysis

The high calcium geo-polymer cement is poised to accounts for the largest share in terms of product type because of the faster development of strength and quicker curing process. Additionally, high calcium geopolymer cements can be used following the traditional techniques of construction. They find application mainly in building infrastructure and rapid constructions as they require high durability and a short curing time. The presence of blast furnace slag and other waste material that contains higher quantities of calcium further adds up to the production capability and efficiency. The reason behind choosing the high calcium formulation is the better resistance to chemical attack and mechanical strength.

By Raw Material Analysis

The geopolymer cement made out of fly ash is projected to lead the raw materials segment because fly ash is widely available from the coal-burning thermal power stations and provides better aluminosilicate composition needed for geopolymerization reaction. It considerably reduces the need for ordinary Portland cement and reduces carbon dioxide emissions and waste disposal by industries. The fly ash-based system gives better durability, chemical resistance, and good structural strength and thus becomes an ideal choice for construction purposes. Governments and environmental organizations are supporting fly ash usage in the construction of buildings. This can be seen in Asia Pacific and North America.

By Activator Chemical Type Analysis

The segment has been ruled by sodium silicate activators, owing to the superior reactivity, good bonding properties, and ability to increase compressive strength within geopolymer cement systems. Sodium silicate increases efficiency in the process of polymerization and provides thermal stability, durability, and chemical resistance. It has been extensively used within fly ash and slag-based geopolymer cement applications in structural concrete as well as precast applications. Sodium silicate is favored by manufacturers for its ability to provide better setting times and increased workability than other available activators. In addition, the compound is industrially feasible and readily available.

By Formulation Type Analysis

Formulation type category is led by ready mix geopolymer cement as they are poised to hold the most significant market share due to their ease of use, superior quality, and growing application in construction work projects. The reason why construction companies tend to go for ready mix formulations is that they minimize labor needs at construction sites, ensure precise batching, and fasten the project completion process. This type of geopolymer cement becomes increasingly useful in construction of urban infrastructures where efficiency of operations is of paramount importance. Apart from that, ready mix formulations of geopolymer cement contribute to sustainability efforts through minimizing carbon emissions, yet ensuring superior structural properties.

By Application Analysis

Concrete is anticipated to hold the highest share in the applications category since geopolymer cement is mainly applied as an eco-friendly substitute of conventional Portland cement for use in concrete manufacture. The application category is positively influenced by the growing worldwide requirement for sustainable building materials that offer great compressive strength, high durability, and chemical and heat resistance properties. Geopolymer concrete has been adopted extensively in infrastructure developments such as bridges, roads, tunnels, precast concrete, and industrial floors since it offers excellent life span and sustainability. Growth in infrastructure renewal projects and green buildings in developed as well as developing nations has been boosting demand.

By End-Use Industry Analysis

The infrastructure development segment is largely anticipated to dominated by the rise in the global emphasis on building more sustainable systems of transport networks, bridges, tunnels, airports, and other public utility systems. The increasing use of geopolymer cement chemicals by governments and construction companies has been witnessed for the sake of reducing the carbon footprint of cement manufacturing while at the same time improving their durability. Geopolymers exhibit an outstanding capacity to resist corrosion, chemicals, and high temperatures, making them extremely useful in constructing durable infrastructure assets. Public investment in building smart cities and infrastructures in regions like the Asia Pacific, Europe, and the Middle East also propels segmental growth.

The Global Geo-polymer Cement Chemical Market Report is segmented on the basis of the following:

By Product Type

- Low Calcium Geopolymer Cement

- High Calcium Geopolymer Cement

- Phosphate-Based Geopolymer Cement

- Silicate-Based Geopolymer Cement

- Alkali-Activated Binders

- Ferro-Sialate-Based Geopolymer

- Other Product Type

By Raw Material

- Fly Ash-Based

- Slag-Based

- Metakaolin-Based

- Silica Fume-Based

- Natural Aluminosilicate-Based

- Waste Glass-Based

- Other Raw Material

By Activator Chemical Type

- Sodium Hydroxide-Based

- Potassium Hydroxide-Based

- Sodium Silicate-Based

- Potassium Silicate-Based

- Phosphate Activators

- Mixed Alkali Activators

- Others

By Formulation Type

- Ready-Mix Geopolymer Cement

- Site-Mixed Geopolymer Cement

- Precast Geopolymer Cement

- Dry Mix Formulations

By Application

- Concrete

- Mortar & Grouts

- Precast Elements

- Pavements & Overlays

- Repair & Rehabilitation

- Coatings & Adhesives

- Waste Encapsulation

- Pipe & Concrete Repair

- Refractory Materials

- Other Application

By End-Use Industry

- Residential Construction

- Commercial Construction

- Industrial Construction

- Infrastructure Development

- Transportation Infrastructure

- Other End-User

Regional Analysis

Leading Region by Market Share

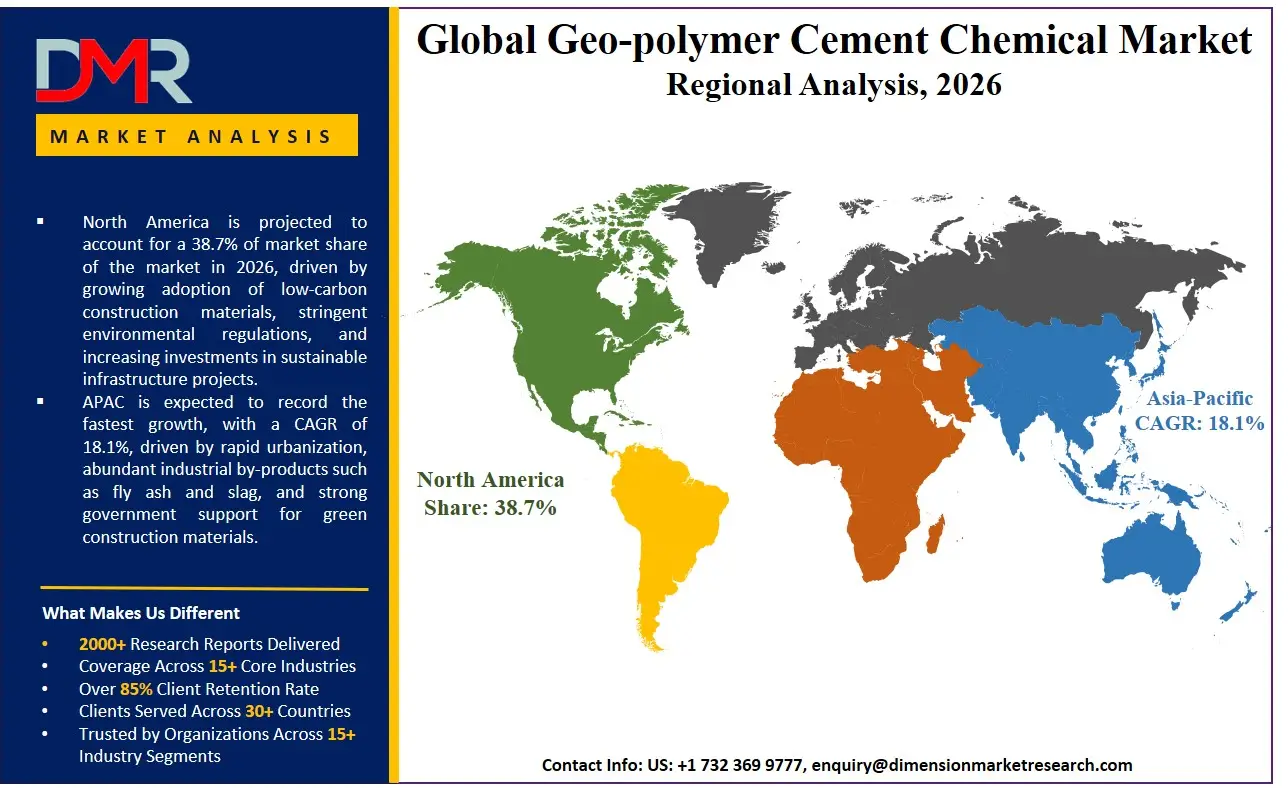

North America is poised to dominate the global geopolymer cement chemical market as it is projected to hold 38.7% of the market share by the end of 2026. The US, the dominant player in North America, holds the highest market share of geopolymer cement chemical due to the presence of unparalleled research centers for advanced materials science, combined with the proactive green procurement policies of the General Services Administration (GSA) and state Departments of Transportation. The region already boasts an existing ecosystem comprising global chemical conglomerates, specialty formulation companies, and plentiful availability of expertise in aluminosilicate chemistry and geopolymer technology. Federal spending on resilient infrastructure projects, advanced manufacturing of refractories, and eventual retirement of OPC manufacturing facilities are some of the factors driving further requirements of low calcium geopolymer cement and alkali-activated cements along with activator chemical development. In addition to this, the presence of venture capital funding for carbon tech start-ups needing chemical formulation services for timely commercialization and ASTM certification cannot be overlooked.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding geopolymer cement chemical market, owing to the massive infrastructure development drives being initiated by governments, and problems associated with industrial waste management in countries such as India, China, Japan and Southeast Asia. Due to rapid growth of economy, emergence of new middle-class consumers, and rapid development of the built environment, there is an urgent need for established companies in the industry to abandon their old and inefficient OPC kiln operations. Services related to site mixed geopolymer cement and geopolymer precast concrete consulting are highly sought after to facilitate transition into net-zero material businesses for these companies. There is also shortage of expertise in geopolymer chemicals in the region, which requires outsourcing activator chemicals types, dry mix designs, and waste chemistry services.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

In today's global geopolymer cement chemicals industry, there is an increasingly dynamic competitive environment populated by an heterogeneous mix of global players specializing in construction chemicals, subsidiaries of big cement companies, and small specialized firms dealing in geopolymer chemistry. The main ingredient in any successful strategy will be strategic partnerships that allow for joint development and early availability of next-generation, high reactivity raw materials through power utilities' fly ash or steel mills' slag. Consolidation in the market is moving forward quickly, with traditional cement and admixture firms acquiring geopolymer patents and activator blend expertise to survive. Intellectual property will play a bigger role as a differentiating factor in competition rather than commoditized raw materials or blending techniques, especially when we think about automatic activator dosing systems and formulation accelerators.

Some of the prominent players in the Global Geo-polymer Cement Chemical Market are:

- BASF SE

- CEMEX S.A.B. de C.V.

- Wagners

- Zeobond Pty Ltd

- PCI Augsburg GmbH

- Geopolymer Solutions LLC

- Alchemy Geopolymer Solutions LLC

- Banah UK Ltd

- SLB (Schlumberger Limited)

- Ecocem

- Sika AG

- Milliken & Company

- JSW Cement Limited

- Kiran Global Chems Limited

- Betolar Plc

- Cemvision

- Terra CO2 Technologies

- Pyromeral Systems

- UltraTech Cement Ltd

- CRH plc

- Other Key Players

Recent Developments

- January 2026: Sika AG expanded its Geopolymer Innovation Hub to enable Infrastructure Development and Industrial Construction customers to develop their own proprietary high calcium geopolymer binders with the aid of advanced mixed alkali activation techniques along with precast geopolymer cement formulation knowledge.

- November 2025: CRH plc enhanced its collaboration with the Progress Group and implemented advanced repair and rehabilitation solutions that use phosphated based geopolymer cement for its Transportation Infrastructure projects including retrofitting of bridges and rapid strength traffic re-opening criteria.

- October 2025: PQ Corporation bought a European geopolymer activators plant to expand their product range for on-site geopolymer cement mixing with sodium silicates and potassium silicate to cater to its refractory material and waste encapsulation projects in the mining industry.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 9.3 Bn |

| Forecast Value (2035) |

USD 34.1 Bn |

| CAGR (2026–2035) |

15.6% |

| The US Market Size (2026) |

USD 3.0 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Product Type, By Raw Material, By Activator Chemical Type, By Formulation Type, By Application, By End-Use |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Geopolymer Cement Chemical Market?

▾ The Global Geopolymer Cement Chemical market is poised to be valued at USD 9.3 billion in 2026 and is projected to reach USD 34.1 billion by 2035, driven by the universal need for specialized chemical formulations in sustainable construction, industrial waste valorization, and low-CO2 binder integration.

What is the CAGR of the Global Geopolymer Cement Chemical Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 15.6% from 2026 to 2035, reflecting the accelerating complexity of raw material supply chains and the persistent urgency of global carbon emission reduction in the built environment.

What factors are driving the growth of the Global Geopolymer Cement Chemical Market?

▾ Key drivers include the global carbon taxation and emissions penalty landscape, the imperative to upcycle industrial byproducts like fly ash and slag, the management complexity of raw material variability, and the surge in demand for application-specific geopolymer chemistries amid evolving green building code requirements.

Which region held the largest share of the Geopolymer Cement Chemical Market in 2026?

▾ North America, specifically the United States, is poised to hold 38.7% of market share in 2026, driven by a mature advanced materials research ecosystem and aggressive federal investment in Low Calcium Geopolymer Cement and Alkali-Activated Binders for resilient infrastructure.

Which region is expected to grow the fastest in the Geopolymer Cement Chemical Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid infrastructure development in China, India, and Southeast Asia, where Dry Mix Formulations and Ready-Mix Geopolymer Cement are critical for transitioning large-scale public works to circular economy operations.

What are the major trends in the Global Geopolymer Cement Chemical Market?

▾ Major trends include the integration of AI into activator design workflows, the rise of Activator-as-a-Service supply models, the demand for sea-water mixable geopolymer solutions, and the focus on Phosphate-Based Geopolymer Cements within extreme environment refractory applications.

Who are the key players in the Global Geopolymer Cement Chemical Market?

▾ Key players include global construction material firms like Holcim and CEMEX, specialty chemical companies like Sika and BASF, as well as pure-play technology developers like Wagners and Zeobond, alongside the material science divisions of industrial conglomerates.

How is the Global Geopolymer Cement Chemical Market segmented?

▾ The market is segmented by Product Type, Raw Material, Activator Chemical Type, Formulation Type, Application, and End-Use Industry.