Market Snapshot

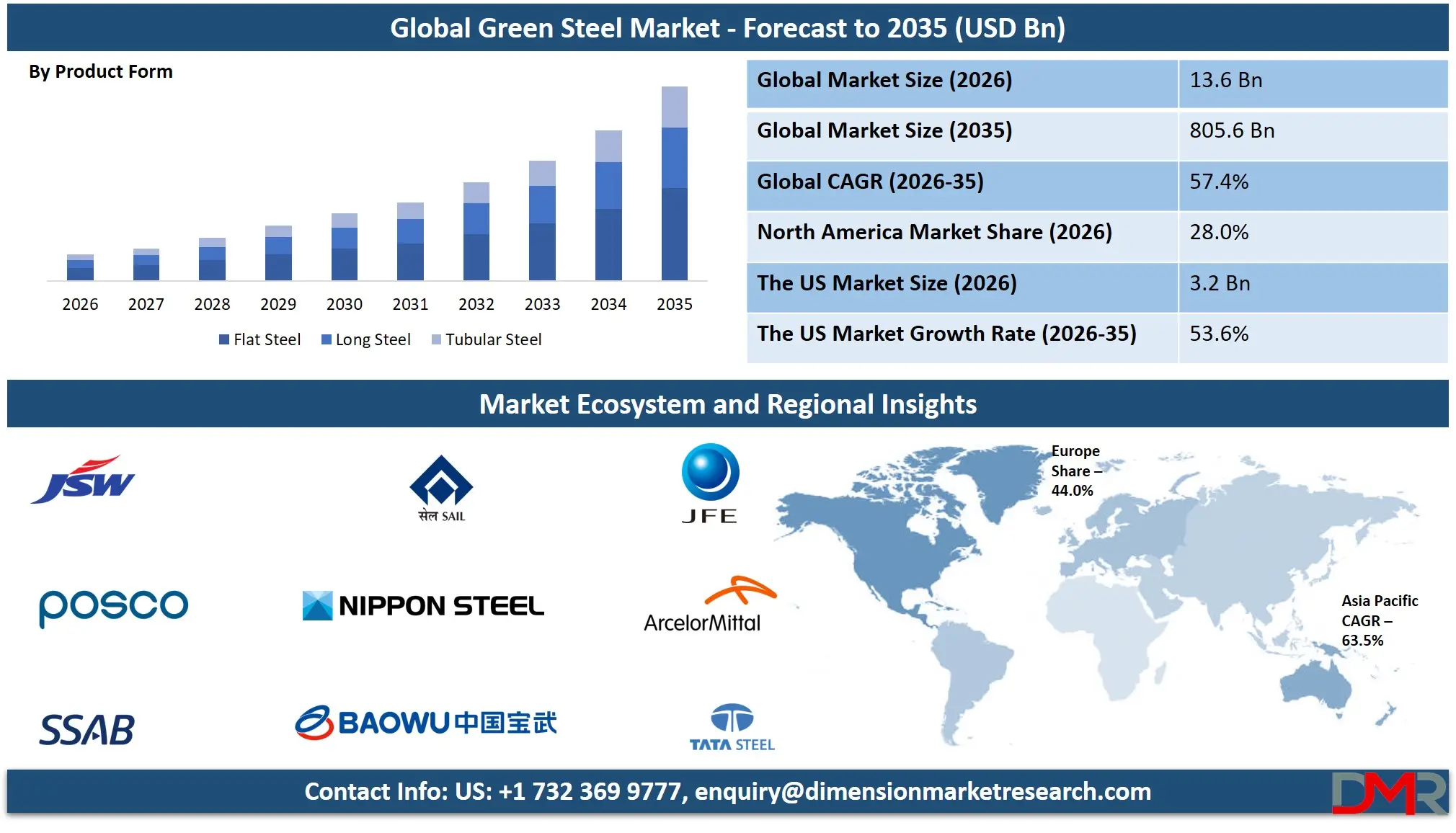

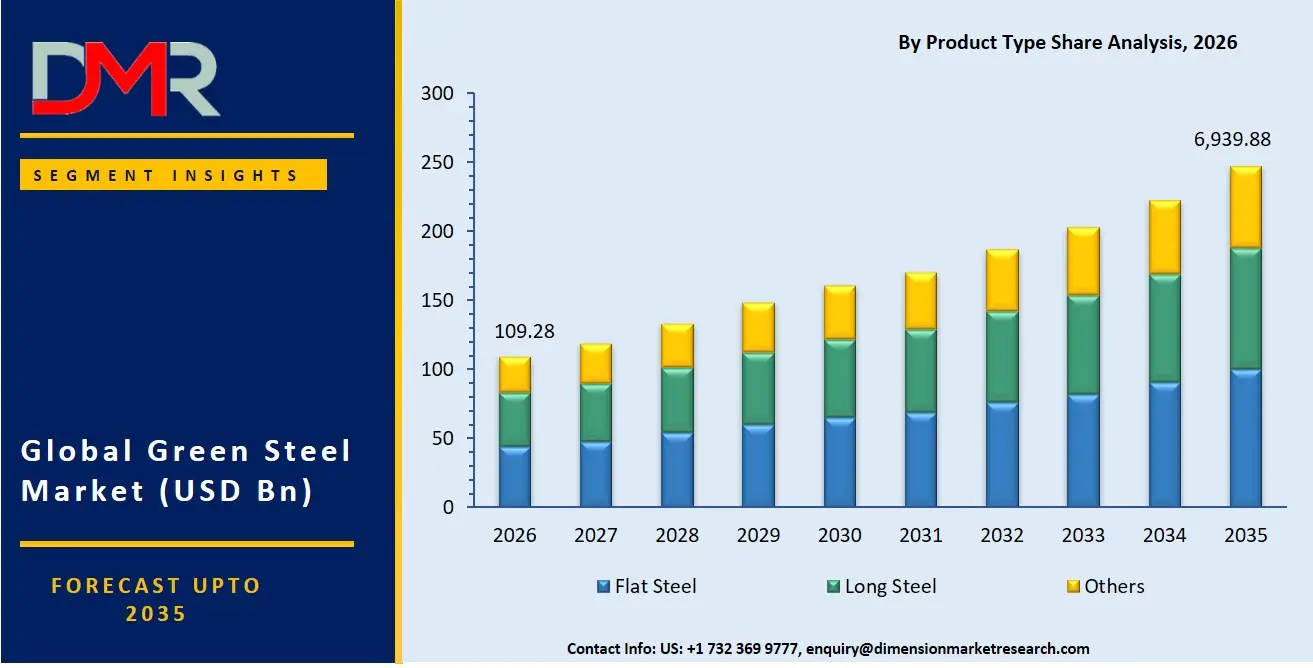

- The market size is USD 68.90 Billion in 2025, reached USD 109.28 Billion in 2026, and is projected to hit USD 6,939.88 Billion by 2035 at a CAGR of 58.6%.

- By Product Type: Flat Steel led with a 40.6% share in 2025.

- By Production Technology: Hydrogen Direct Reduced Iron (H2-DRI) + Electric Arc Furnace (EAF) led with a 62.4% share in 2025.

- By End-use Industry: Building & Construction led with a 39.8% share in 2025.

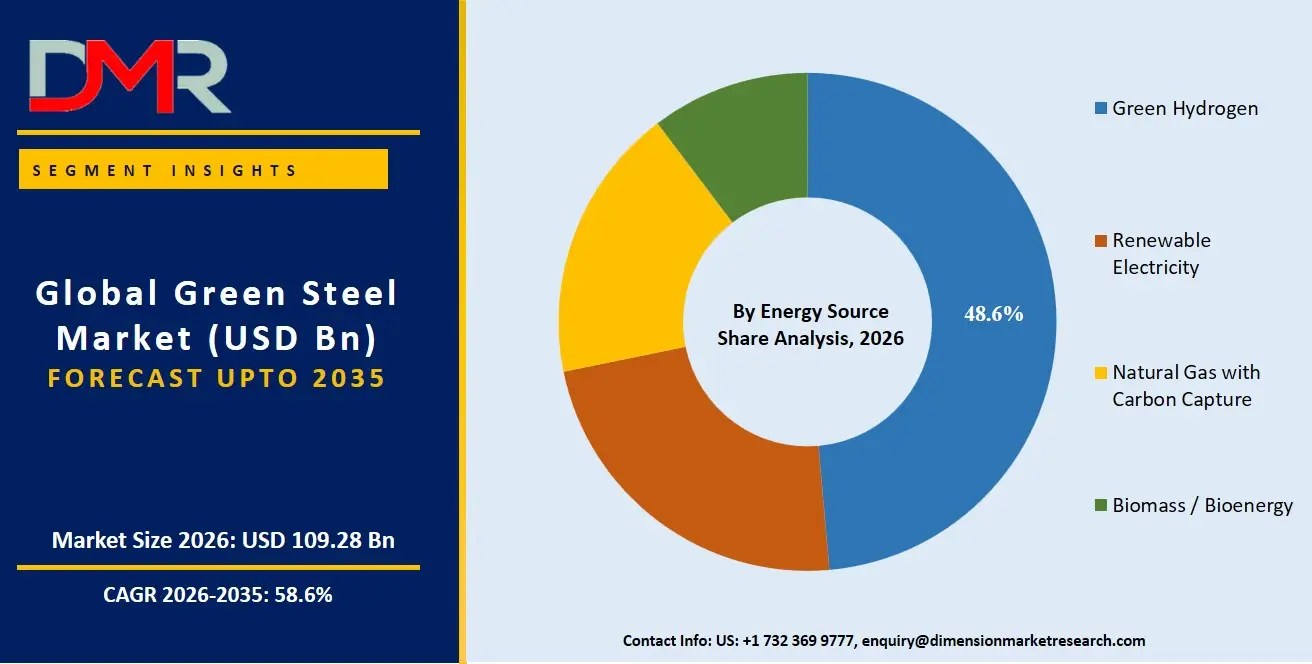

- By Energy Source: Green Hydrogen led with a 48.6% share in 2025.

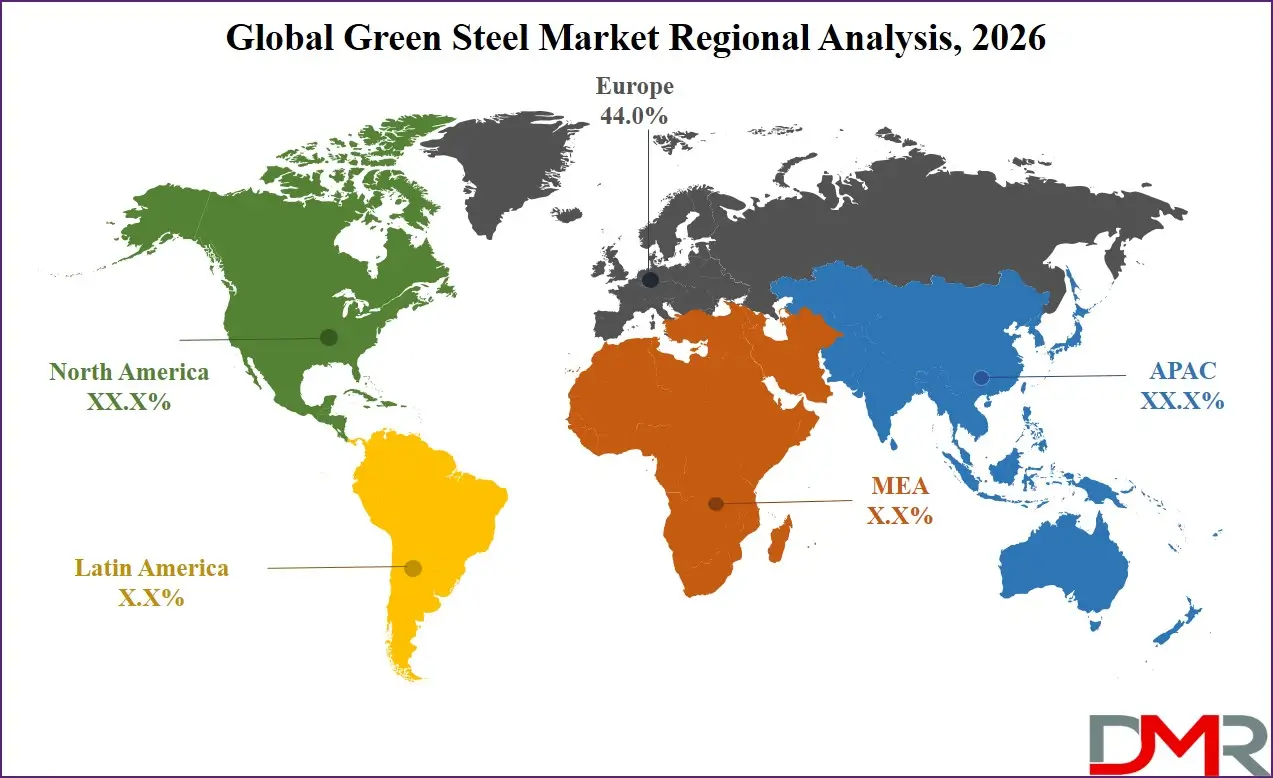

- By Region: Europe led with a 42.8% share, valued at USD 29.49 Billion, in 2025.

- Key players include ArcelorMittal, SSAB AB, China Baowu Steel Group, Tata Steel Limited, and voestalpine AG, among others.

Market Overview

The green steel market covers steel produced through production routes that substantially reduce carbon emissions relative to the conventional blast-furnace and basic-oxygen-furnace process. Products range across flat steel, long steel, structural steel, and reinforcement bar. Production technologies span hydrogen-based direct-reduced iron paired with electric arc furnaces, scrap-based EAF routes, carbon capture systems, and emerging molten oxide electrolysis. The market excludes conventionally produced steel, even where partial scrap use or efficiency improvements reduce emissions at the margin.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Steel production accounts for roughly 7–9% of global CO₂ emissions, making decarbonization of this sector a central challenge for national net-zero commitments. Green steel occupies the overlap between industrial decarbonization policy, energy transition infrastructure, and heavy manufacturing supply chains. As reported by MIDREX, the MIDREX/EAF production combination already delivers roughly half the CO₂ output of a conventional blast-furnace/basic-oxygen-furnace route, with process gas containing approximately 55% hydrogen and 36% carbon monoxide. That performance advantage is drawing procurement commitments from automotive and construction buyers who face Scope 3 reporting obligations under frameworks such as the EU's Corporate Sustainability Reporting Directive.

Market Size and Forecast

The Global Green Steel Market size is estimated at USD 109.28 Billion in 2026 from USD 68.90 Billion in 2025, and is projected to reach USD 6,939.88 Billion by 2035, exhibiting a CAGR of 58.6% during the forecast period.

The headline CAGR reflects a market at an early-commercial inflection. Base-year volumes remain concentrated among a small number of operating facilities, and the explosive forecast growth assumes rapid capacity scaling as hydrogen infrastructure, electrolyzer output, and renewable power grids reach industrial scale. MIDREX plants produced 82.170 million metric tonnes of direct reduced iron in 2025, a 7.78% increase over the 76.239 million metric tonnes recorded in 2024, confirming that DRI output momentum is building ahead of the green-steel ramp. Forecast assumptions rest on continued cost compression, policy enforcement of carbon pricing, and the translation of announced capacity investments into commissioned assets before 2030.

Downside risk concentrates in two areas. Delays to green hydrogen infrastructure and grid expansion would constrain production at hydrogen-DRI plants before merchant markets for green steel reach sufficient liquidity. Upside scenarios hinge on EU carbon border adjustment pricing accelerating demand pull from European buyers faster than the base forecast assumes.

Product Type Analysis

Flat Steel accounted for 40.6% of product type demand in 2025, the highest of any category.

Flat steel's dominance reflects its central role in automotive body panels, appliance casings, and the structural skin of commercial buildings. Automotive original equipment manufacturers in Europe and North America have signed low-carbon steel supply frameworks that explicitly prioritize flat steel grades. Green flat steel commands the highest procurement volumes because the buyers writing Scope 3 commitments are concentrated in industries that consume flat products.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Long steel, structural steel, and reinforcement bar collectively cover the construction and infrastructure segments, where public procurement rules and project finance covenants are beginning to embed carbon requirements. The natural-gas-based direct-reduction plus EAF route can reduce CO₂ emissions by approximately 60% versus conventional blast-furnace/basic-oxygen-furnace production, as reported by TERI, giving long-steel producers a commercially viable pathway before full green hydrogen supply arrives. Green hydrogen in the DRI process can save nearly 2 tonnes of CO₂ for every tonne of steel produced, according to HydrogenEra, creating a clear upgrade trajectory from gas-DRI to hydrogen-DRI as hydrogen costs fall. Fastest growth within the product type segment is expected in reinforcement bar and structural sections, driven by renewable energy infrastructure build-out and public construction pipelines in South and Southeast Asia.

Production Technology Analysis

With a 62.4% share in 2025, Hydrogen Direct Reduced Iron + Electric Arc Furnace outpaced all other production technology categories.

H2-DRI+EAF holds its dominant position because it offers the most direct pathway to near-zero Scope 1 and Scope 2 emissions in primary steelmaking. Procurement contracts from automotive and construction buyers increasingly specify H2-DRI provenance, creating a commercial pull that reinforces the technology's share concentration.

Scrap-based EAF represents the second largest category and carries the lowest capital barrier to green steel production. The technology relies on scrap availability rather than hydrogen supply, making it immediately deployable where urban metal stocks are sufficient. CCUS and molten oxide electrolysis remain early-stage, with commercial viability dependent on cost reductions and infrastructure investment that sits beyond the 2026–2030 planning horizon for most operators.

End-use Industry Analysis

Building & Construction led the end-use industry segment with a 39.8% share in 2025.

Construction's share leadership reflects both the sector's absolute scale as a steel consumer and the speed at which public and private project finance frameworks are incorporating embodied-carbon limits. Green public procurement standards in the EU and the UK are directing low-carbon steel into infrastructure and commercial buildings before voluntary corporate sustainability commitments in other sectors have fully matured.

Automotive is the fastest-growth end-use application, driven by OEM Scope 3 reduction targets and the visible reputational stakes attached to electric vehicle manufacturing. Industrial equipment, renewable energy infrastructure, and consumer appliances are each pulling distinct demand streams. Renewable energy infrastructure is the highest-growth sub-category within that group, as wind turbine towers and solar mounting structures require structural steel whose carbon content is entering tender specifications.

Energy Source Analysis

A 48.6% share made Green Hydrogen the clear leader across energy source categories in 2025.

Green hydrogen's dominant share is partly structural: H2-DRI+EAF is the dominant production technology, and every plant in that category requires hydrogen as its primary reductant. As electrolyzer costs fall and renewable electricity capacity expands, the economics of green hydrogen production are improving faster than most 2020-era forecasts projected.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Renewable electricity as a direct energy input powers scrap-based EAF operations and supports the electrolysis step in hydrogen production. Natural gas with carbon capture functions as a bridge energy source, allowing operators to reduce emissions by 50–60% while green hydrogen supply infrastructure catches up to demand. Biomass and bioenergy occupy a niche role where regional feedstock availability and sustainability certification standards limit scalability at industrial volumes.

Key Market Segments

By Product Type

- Flat Steel

- Long Steel

- Structural Steel

- Reinforcement Steel (Rebar)

- Others

By Production Technology

- Hydrogen Direct Reduced Iron (H2-DRI) + Electric Arc Furnace (EAF)

- Electric Arc Furnace (EAF) using Scrap

- Carbon Capture, Utilization & Storage (CCUS)

- Molten Oxide Electrolysis (MOE)

By End-use Industry

- Building & Construction

- Automotive

- Industrial Equipment

- Renewable Energy Infrastructure

- Consumer Appliances

- Others

By Energy Source

- Green Hydrogen

- Renewable Electricity

- Natural Gas with Carbon Capture

- Biomass / Bioenergy

Regional Analysis

Europe led the regional segment with a 42.8% share, valued at USD 29.49 Billion, in 2025.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Europe's leadership reflects the combined effect of the EU Emissions Trading System, national industrial decarbonization subsidies, and the impending full enforcement of the Carbon Border Adjustment Mechanism. The HYBRIT Demonstration plant in Sweden is designed to produce approximately 1.3 million tonnes of fossil-free steel per year — roughly a quarter of Sweden's total steel output — with potential to prevent more than 14 million tonnes of CO₂ over its first ten years, according to the European Commission. Germany, Sweden, and the Netherlands are home to the majority of announced and operating green steel capacity in the region, anchored by coordinated government co-financing and grid infrastructure planning.

Asia-Pacific is the fastest-growing region, driven by China Baowu, POSCO, and Nippon Steel's capacity announcements and by India's construction and public infrastructure pipeline. Unlike Europe, Asia-Pacific green steel growth spans a wider range of production technologies, including scrap-EAF in urban markets and hydrogen-DRI at coastal export hubs. Latin America, the Middle East, and Africa are emerging as green DRI export platforms rather than domestic green steel consumers, with renewable energy cost advantages enabling competitive hydrogen production for supply into carbon-constrained import markets.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Driver: EU Carbon Pricing and Buyer Scope 3 Commitments Pulling Demand

The EU Carbon Border Adjustment Mechanism begins pricing embedded emissions in imported steel from 2026, creating a direct cost disadvantage for blast-furnace producers exporting into Europe. Green steel producers gain a pricing floor advantage that conventional routes cannot replicate without deep capital investment. The German Federal Government pledged €55 million to support ArcelorMittal's first industrial-scale hydrogen-based DRI demonstrator in Hamburg, a signal that public co-financing is available to close the investment risk gap at scale, as reported by MIDREX.

Stegra's Boden facility reduces the carbon footprint of hydrogen-based direct-reduced iron by 95% compared with conventional blast-furnace processes, as reported by CINEA. Once fully operational, that same facility is expected to eliminate approximately 7 million tonnes of CO₂ annually. Numbers at that scale give procurement teams at automotive OEMs and construction developers the Scope 3 reduction evidence they need to justify long-term green steel supply contracts.

Restraint: Capital Intensity and Infrastructure Gaps Slow Capacity Build

Replacing long-lived blast-furnace assets with hydrogen-DRI and EAF capacity requires capital expenditure at a scale that strains balance sheets even for the largest integrated steelmakers. IECC's 2030 base-case analysis estimates the H₂-DRI/EAF green steel route at approximately US$562 per tonne versus US$536 per tonne for the blast-furnace/basic-oxygen-furnace route — a premium of roughly US$26 per tonne, or about 5%. That gap narrows as hydrogen costs fall, but the crossover point remains sensitive to electrolyzer scaling timelines and renewable electricity tariffs.

Insufficient green hydrogen supply infrastructure at industrial scale compounds the capital problem. A plant committing to H2-DRI production today must either secure a long-term hydrogen supply agreement or invest upstream in electrolysis capacity, adding a second large capital requirement. High-voltage grid connection at industrial sites is a third bottleneck, particularly in markets where grid infrastructure planning lags behind announced steel decarbonization timelines.

Opportunity: Export Hubs and Certified Supply Agreements Open New Revenue Streams

Renewable-rich regions in the Middle East, North Africa, and India can produce green DRI and hot-briquetted iron at a structural cost advantage relative to European producers constrained by higher electricity tariffs. HyIron inaugurated Africa's first zero-emissions iron-production facility at the Oshivela site in Namibia in April 2025, using renewable electricity and green hydrogen — a concrete example of the export hub model moving from concept to operational asset. CPI's modelling estimates India's cumulative green-steel subsidy outlay between 2026 and 2032 at INR 8,340 crore, with 67% directed at hydrogen operating-cost reduction and 33% at capital-cost relief, according to Climate Policy Initiative data.

Certified low-carbon supply agreements for European automotive OEMs represent a parallel revenue stream. HYBRIT's technology, once fully operational, could reduce Sweden's CO₂ emissions by roughly 10% and Finland's by 7%, cutting between 35 and 50 million tonnes of global steel emissions per year, per Vattenfall data. Scrap-optimized EAF networks in mature urban markets — where post-consumer steel stocks are abundant — offer a capital-light circular steel pathway that complements hydrogen-DRI at scale.

Market Trends

EAF Leads Revenue, Hydrogen-DRI Advances, and CBAM Hardens Trade Rules

Electric arc furnace production is emerging as the leading revenue segment in green steel, driven by lower capital barriers and immediate scrap availability in mature markets. Hydrogen-based direct reduction is advancing from pilot demonstrations toward post-2030 commercial deployment, with Thyssenkrupp reporting its tkH2Steel plant can save up to 3.5 million tonnes of CO₂ per year when operating on hydrogen, as confirmed by Thyssenkrupp. Embedded-carbon reporting under CBAM is becoming a core supplier-qualification requirement, and Asia-Pacific green steel capacity is scaling faster than any other region.

Market Competition Overview

The green steel market is fragmented at the production level but consolidating rapidly around a small group of large integrated steelmakers who have committed capital to hydrogen-DRI and EAF transitions. Established blast-furnace producers dominate current output, but their competitive position shifts as CBAM enforcement reduces the cost advantage of carbon-intensive routes in the European import market. Scrap-based EAF operators hold a structural speed advantage: they can deliver green steel credentials today without waiting for hydrogen infrastructure, and their capital requirements are an order of magnitude below those of greenfield DRI plants.

Early contracted supply is a key competitive differentiator. Stegra reports that 50% of its initial planned annual production volume of 2.5 million tonnes has been contracted to customers willing to pay a defined green premium, as cited by Hydrogen Tech World. Producers who secure long-term offtake agreements before 2027 will lock in anchor revenue streams that justify further capacity expansion, while late movers face a contracting market for premium-priced certified green steel as supply increases.

Company Profiles

ArcelorMittal is positioned as the scale leader in the transition, deploying hydrogen-DRI technology across multiple geographies while using existing integrated plant footprints to manage the pace of blast-furnace retirement. The Hamburg hydrogen-DRI plant is planned to produce more than 1 million tonnes of zero-carbon-emissions steel per year by 2030, saving approximately 800,000 tonnes of CO₂ annually, as reported by MIDREX. That facility, combined with EU co-financing frameworks, gives ArcelorMittal a first-mover cost base in certified European green steel that competitors building from scratch will struggle to match before 2032.

SSAB AB pursues a differentiated strategy through the HYBRIT joint venture, targeting fossil-free steel with a carbon intensity below 0.05 kg CO₂e per kg of steel across Scope 1, 2, and upstream iron-ore Scope 3 emissions, as confirmed by SSAB. Tata Steel Nederland's April 2025 announcement of a new direct-reduction plant and electric-arc furnace to replace one blast furnace and coke-and-gas plant at IJmuiden signals that the transition pathway is being executed by a second-tier group of major producers in parallel with the frontrunners.

Key Players

- ArcelorMittal

- SSAB AB

- China Baowu Steel Group

- Tata Steel Limited

- voestalpine AG

- Tenaris

- Salzgitter AG

- Thyssenkrupp Steel

- Nucor Corporation

- Nippon Steel Corporation

- POSCO

- JFE Steel Corporation

- JSW Steel

- H2 Green Steel

- Liberty Steel Group

- HBIS Group

- Boston Metal

- Emirates Steel Arkan

- Other Key Players

Recent Developments

- January 2025, The European Commission allocated €175 million to the Research Fund for Coal and Steel, including a €100 million clean-steel call for pilot and demonstration projects covering near-zero-carbon technologies such as CCUS, process intensification, and CO₂-neutral iron-ore reduction.

- June 2025, The German Federal Government committed €55 million to ArcelorMittal's Hamburg hydrogen-DRI demonstrator, which is designed to use hydrogen with a purity exceeding 95% in the direct-reduction process.

- July 2025, Tata Steel broke ground on its £1.25 billion electric-arc-furnace project at Port Talbot, Wales, with £500 million of UK government support, replacing blast-furnace steelmaking with scrap-based production.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 68.90 Billion |

| Market Value (2026) |

USD 109.28 Billion |

| Forecast Revenue (2035) |

USD 6,939.88 Billion |

| CAGR (2026 to 2035) |

58.6% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020 to 2024 |

| Forecast Period |

2026 to 2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Product Type (Flat Steel, Long Steel, Structural Steel, Reinforcement Steel (Rebar), Others), By Production Technology (H2-DRI + EAF, EAF using Scrap, CCUS, MOE), By End-use Industry (Building & Construction, Automotive, Industrial Equipment, Renewable Energy Infrastructure, Consumer Appliances, Others), By Energy Source (Green Hydrogen, Renewable Electricity, Natural Gas with Carbon Capture, Biomass / Bioenergy) |

| Regional Analysis |

North America – US and Canada; Europe – Germany, France, The UK, Spain, Italy, and Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, and Rest of APAC; Latin America – Brazil, Mexico, and Rest of Latin America; Middle East & Africa – GCC, South Africa, and Rest of MEA |

| Competitive Landscape |

ArcelorMittal, SSAB AB, China Baowu Steel Group, Tata Steel Limited, voestalpine AG, Tenaris, Salzgitter AG, Thyssenkrupp Steel, Nucor Corporation, Nippon Steel Corporation, POSCO, JFE Steel Corporation, JSW Steel, H2 Green Steel, Liberty Steel Group, HBIS Group, Boston Metal, Emirates Steel Arkan, Other Key Players |

| Customization Scope |

Customization for segments and region or country level will be provided. Additional customization can be done based on requirements. |

| Purchase Options |

Three license options: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF). |

Frequently Asked Questions

What is the biggest investment opportunity in Green Steel Market ?

▾ Renewable-rich export hubs in the Middle East, North Africa, and India represent the highest-return entry point. Green DRI and hot-briquetted iron produced at low hydrogen cost in these regions can be exported into carbon-constrained European markets where CBAM enforcement creates a structural price premium for low-emissions feedstock. First movers who secure offtake agreements before 2028 will establish cost positions that late entrants cannot replicate.

Who are the top companies in Green Steel Market ?

▾ ArcelorMittal and SSAB AB lead on technology deployment and certified green steel volume. China Baowu Steel Group, Tata Steel Limited, Thyssenkrupp Steel, POSCO, and Nucor Corporation hold significant market positions across production technologies and geographies. H2 Green Steel and Boston Metal represent the pure-play emerging entrants building from greenfield hydrogen-first platforms.

Which segment is growing fastest in Green Steel Market and why?

▾ The Hydrogen Direct Reduced Iron plus Electric Arc Furnace production technology segment is growing fastest, supported by its 62.4% share dominance and rapid capacity announcements across Europe and Asia-Pacific. Buyers specifying near-zero Scope 1 and Scope 2 emissions in steel procurement are directing long-term supply contracts toward H2-DRI producers ahead of any other technology route.

Which region is growing fastest in Green Steel Market and why?

▾ Asia-Pacific is the fastest-growing region, driven by capacity commitments from China Baowu, POSCO, Nippon Steel, and JFE Steel alongside India's expanding public infrastructure pipeline. Unlike Europe, where growth is policy-mandated, Asia-Pacific growth reflects both regulatory pressure and genuine export ambition, particularly in green DRI production for supply into the European and North American markets.

What is the biggest challenge holding Green Steel Market ?

▾ Insufficient green hydrogen supply infrastructure at industrial scale is the primary constraint. The IECC estimates the H2-DRI/EAF route carries a cost premium of approximately US$26 per tonne over conventional blast-furnace production, and that gap cannot close without large-scale electrolyzer deployment and dedicated renewable power procurement. Until hydrogen supply chains reach the throughput required by major steelmakers, capacity build-out will run behind announced targets.