A HUD (Heads-Up Display) is a technology developed with a focus on reducing driver distractions by projecting critical vehicle information onto the windshield instead of separate dashboard screens.

At start designed for the military, HUDs have evolved to become a part of civilian cars, owing to technological advancements. The earliest HUDs used CRT displays, while the second generation employed solid-state light sources like LED for backlighting LCD projections, a technology mainly found in commercial aircraft.

The Global Head-Up Display Market has experienced rapid expansion over recent years, particularly within automotive and aerospace sectors. Due to an increasing need for improved driver and pilot safety, manufacturers are installing HUDs into vehicles and aircraft to display crucial information directly in front of drivers' lines of sight reducing distractions - revolutionizing how information is conveyed within vehicles and aircraft.

An integral driver of growth has been the proliferation of augmented reality (AR) technologies among automakers. They are using AR features in HUDs for real-time navigation, hazard detection and advanced driver-assistance systems (ADAS). This trend improves user experience while increasing appeal of HUD systems in consumer vehicles.

HUD systems also present exciting opportunities in military and aviation fields, where HUDs play an essential role for pilot safety, situational awareness, and operational efficiency. With growing investments in both military and commercial aircraft fleets comes increased demand for advanced HUD solutions; further supported by technological innovations like lightweight high-resolution displays that offer better overall experiences.

Recent advancements in the Head-Up Display (HUD) Market highlight the growing integration of augmented reality (AR) in automotive and aviation sectors. Companies like BMW and Tesla are enhancing driving experiences with AR HUDs, while aerospace manufacturers are equipping more aircraft with HUD systems for improved pilot safety, situational awareness, and operational efficiency.

As per electroiq LCD technology remains the dominant player in the display market, holding 50% of the total market share. As the demand for higher-resolution displays like 4K and 8K grows, it is expected to reach a peak of $24 billion USD. Companies such as Samsung continue to lead with advanced display technologies like OLED and LED.

Sustainability is becoming increasingly important for manufacturers of display panels. The Asia Pacific region accounts for the largest market share in display technologies, with 30.5% of the global market share in 2023. As innovation in OLED and micro-LED technologies continues, the market dynamics are shifting towards more energy-efficient, high-performance displays.

Key Takeaways

- Market Growth: Head-up display market expected to grow from USD 3.1 billion in 2023 to USD 18.5 billion by 2032, at a CAGR of 22.1%.

- Safety Focus: HUDs reduce driver distraction by projecting vital vehicle info onto the windshield, boosting both driver and pilot safety in automotive and aviation sectors.

- Tech Integration: Augmented reality features in HUDs enhance real-time navigation, hazard detection, and user experience, making modern vehicles and aircraft more appealing.

- Product Leadership: Windshield HUDs dominate the product segment, offering a seamless and clutter-free dashboard experience mainly in high-end vehicles.

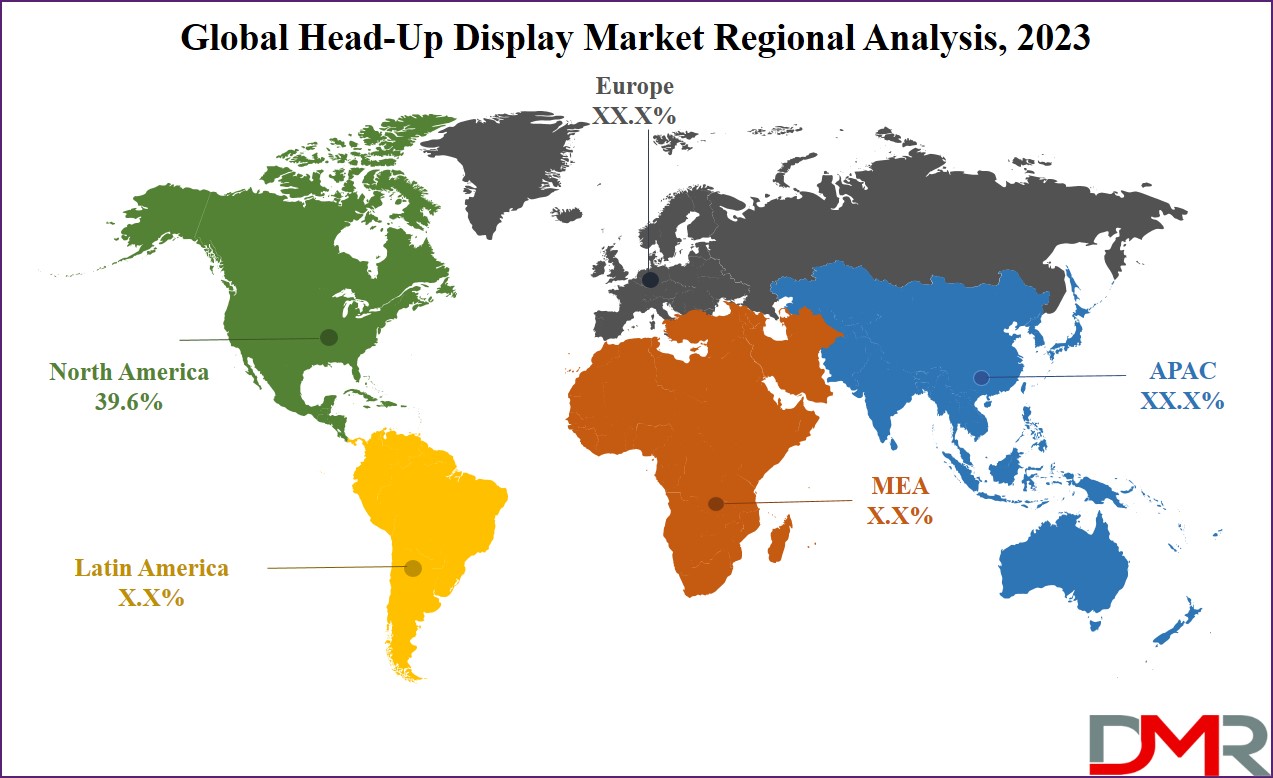

- Regional Dominance: North America leads market share with 39.6% revenue in 2023, driven by luxury vehicle adoption and investment in advanced safety technologies.

- Application Trends: The Automotive segment is the primary market driver, especially premium and luxury cars with integrated driver assistance systems, followed by steady growth in aviation.

- Display Technology: Digital HUDs using LCD, DLP, or OLED are preferred for their compact design, high efficiency, and advanced features; LCD tech holds 50% of display market share.

- Challenges & Opportunities: High power consumption and costs constrain market growth, but evolving energy-efficient displays and sustainability trends offer future opportunities.

Use Cases

- Driver Safety Enhancement : HUDs in cars and aircraft project critical information directly in the driver's or pilot’s line of sight, lowering distraction and improving safety during operation.

- Fleet Performance Monitoring : Commercial vehicle fleets use HUD systems for real-time monitoring of vehicle performance, route management, and essential operational data to improve productivity and safety.

- Premium Vehicle Differentiation : High-end cars adopt windshield HUDs for a sleek dashboard and integration with advanced driver-assistance, appealing to premium buyers and boosting market competitiveness.

- AR Navigation Aid : Augmented reality HUDs offer context-aware, interactive navigation and hazard detection for drivers and pilots, adding value to both automotive and aviation industries.

- Flight Simulator Training : Aviation sector employs HUD technology in simulators to recreate real-world navigation and operations, enhancing pilot preparedness and situational awareness.

- Aftermarket Upgrades : Combiner glass HUDs allow easy installation and upgrades for older vehicles, providing advanced display features without built-in systems for broader market accessibility.

Market Dynamic

The growing focus on road safety stands out as a major driver for the increase in the need for HUD technology. Traditional dashboards often need drivers to divert their attention from the road, leading to delays in reactions & potential safety hazards.

HUDs solve this problem by providing important information directly within the driver's line of sight, making it simple to access crucial data like navigation instructions, speed, & warning signals without the need to look away, which improved safety aspect has become highly appealing to both individuals & automotive manufacturers, who are keen on enhancing vehicle safety by reducing distractions.

Also, In the current tech-savvy world, consumers anticipate seamless integration of technology into their daily lives, such as vehicles. Features like real-time data, smartphone connectivity, & interactive capabilities have transitioned from luxuries to necessities.

HUDs meet these beliefs by providing a blend of convenience, modernity, & an interactive driving experience, creating a new standard for what people look for in a modern vehicle, which aligns with contemporary consumer preferences and significantly fuels the need for head-up displays in the market. However, challenges like high power consumption & the associated costs still act as significant growth constraints for this market.

Research Scope and Analysis

By Product

The product of the market includes windshield HUD, combiner glass HUD, & collision warning-only HUD, with windshield HUD being the dominant segment in driving the growth of the market. In a windshield HUD, the

display is seamlessly integrated into the vehicle's windshield, projecting major information directly into the driver's natural line of sight, which removes the requirement for extra screens or displays, offering a cleaner & less cluttered dashboard, mainly used in high-end vehicles, windshield HUDs provide a sleek & convenient solution.

Moreover, combiner glass HUD utilizes a discrete transparent screen or combiner placed between the driver & the windshield for projecting information, which is generally more cost-efficient & simpler to install in comparison to windshield HUDs, offering flexibility as the combiner glass can be adjusted or removed as required. Combiner glass HUDs are often found in aftermarket HUD solutions, allowing their integration into vehicles lacking built-in HUD systems.

By Type

The terms of type market are categorized into conventional HUD & augmented reality (AR) based HUD, with conventional HUDs holding the majority of the market share in 2023. Conventional HUDs are the customized version of this technology, projecting critical information directly into the user's line of sight. They typically display basic data like speed, fuel levels, & rudimentary navigation instructions on a see-through surface, like a windshield or combiner glass.

The displayed information remains static & doesn't adapt to real-time changes. Conventional HUDs are generally more affordable and easy to deploy, making them handy to most vehicle owners, as their primary goal is to lower distractions by presenting crucial information within the driver's direct view, ultimately enhancing safety & operational efficiency.

Moreover, AR (augmented reality) based HUDs provide a more high-end iteration of head-up display technology. AR-based systems cover computer-generated information in the real-world environment, enabling the displayed data to interact with the real surroundings, which provides a more dynamic & context-aware user experience.

However, AR-based HUDs typically need advanced hardware & software components, including cameras, sensors, & computational units, making them a more expensive option compared to conventional HUDs.

By Technology

The market for head-up displays (HUDs) based on technology comprises two key segments: CRT-based HUDs & digital HUDs, with digital HUDs having the lead in the segment in 2023 in terms of revenue share.

Digital HUDs portray the new evolutionary step in this technology, including LCD (liquid crystal display), DLP (digital light processing), or OLED (organic light-emitting diode) technologies to project information.

These digital HUDs are preferred due to their compact design, lightweight, energy efficiency, superior resolution, & capability to display more complex data, like full-color graphics & even video in a few instances.

They are easy to couple into modern vehicles & aircraft owing to their smaller size & less power consumption, as well as they easily support advanced features like AR, enhancing the overall user experience.

By Application

The global market based on its applications is categorized into segments like automotive, aviation, wearables, & others. Among these, the automotive application segment is driving the growth of the market & is anticipated to hold a substantial market share in the coming future. Within the automotive segment, there are sub-categories, including premium/luxury cars, sports cars, & basic & mid-segment cars.

Among these, the premium/luxury cars sub-segment is expected to have a significant portion of the automotive market in the coming years, which is attributed to the integration of head-up displays with driver assistance systems, a technology highly adopted by many car manufacturers, which is anticipated to drive the market growth for these displays.

In addition, the aviation segment is also expected to have steady growth, as a majority of commercial aircraft use head-up display systems to enhance landing & takeoff operations, and the growth of flight simulators further contributes to this segment's expansion. However, developing transparent displays that offer better visibility in both daylight & nighttime conditions remains a significant challenge for manufacturers.

The Head-Up Display Market Report is segmented on the basis of the following:

By Product

- Windshield HUD

- Combiner Glass HUD

- Collision Warning Only HUD

By Type

- Conventional HUD

- Augmented Reality Based HUD

By Technology

- CRT Based HUD

- Digital HUD

By Application

- Aviation

- Automotive

- Wearables

- Others

Regional Analysis

North America takes the lead in market share with a substantial

39.6% share in terms of revenue in 2023. The region's strong demand for head-up displays (HUDs) is majorly being driven by the growth in the making of luxury vehicles, emphasizing the importance of HUD technology.

Furthermore, the increase in awareness of safety features in vehicles is contributing to market growth in North America. In addition, the usage of HUDs in commercial fleets for live monitoring of vehicle performance, route details, & essential data is making a positive impact on the market.

In addition, North America is expected to maintain steady growth during the forecasted period due to factors like high investments in R&D (research and development), government initiatives, & the incorporation of advanced technologies. These elements together contribute to the region's continued expansion in the HUD market.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The head-up display (HUD) market experiences a moderate level of consolidation, with both global & regional companies competing. These players are managing their product offerings, creating innovative products, & extending their presence in many countries. Leading manufacturers are aiming at research & development efforts to build advanced HUD systems, focusing on increasing profits.

Like, in May 2022, Panasonic introduced that Nissan Motor Co., Ltd. had chosen their 11.5-inch windshield head-up display (WS HUD) for the latest Ariya

electric vehicle (EV), which projects essential information onto the car's windshield, including details like navigation guidance, vehicle speed, & advanced driver-assistance features.

Some of the prominent players in the global Head-Up Display Market are:

- Continental AG

- Yazaki Corp

- BAE System

- Nippon Seiki

- Valeo

- Thales Group

- Panasonic Corp

- DENSO Corp

- Robert Bosch

- HUDWAY LLC

- Other Key Players

Recent Developments

- In September 2025, Visteon and FUTURUS announced a partnership to develop next-generation AR HUD, Windshield HUD, and Panoramic HUD systems for cars, aiming to advance cockpit technology.

- In June 2023, Honeywell acquired Saab’s head-up display assets to enhance its avionics offerings, integrating new HUD technology for improved pilot safety and functionality.

- In May 2022, BAE Systems launched LiteWave, a compact and lightweight HUD for aircraft cockpits, using waveguide technology to improve situational awareness and safety.

- In July 2025, major automotive manufacturers increased investments in AI-powered HUDs with advanced sensor integration, driving growth in safety and connectivity features for HUD-equipped vehicles.

- In 2025, the automotive sector saw expanding rollout of head-up displays in premium and mid-range vehicles, spurred by product launches featuring augmented reality, advanced driver assistance, and immersive driving features.

Report Details

| Report Characteristics |

| Market Size (2023) |

USD 3.1 Bn |

| Forecast Value (2032) |

USD 18.5 Bn |

| CAGR (2023–2032) |

22.1% |

| Historical Data |

2017 – 2022 |

| Forecast Data |

2023 – 2032 |

| Base Year |

2022 |

| Estimate Year |

2023 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product (Windshield HUD, Combiner Glass HUD, and Collision Warning Only HUD), By Type (Conventional HUD and Augmented Reality Based HUD), By Technology (CRT Based HUD and Digital HUD), By Application (Aviation, Automotive, Wearables, and Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Continental AG, Yazaki Corp, BAE System, Nippon Seiki, Valeo, Thales Group, Panasonic Corp, DENSO Corp, Robert Bosch, HUDWAY LLC, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |