Market Snapshot

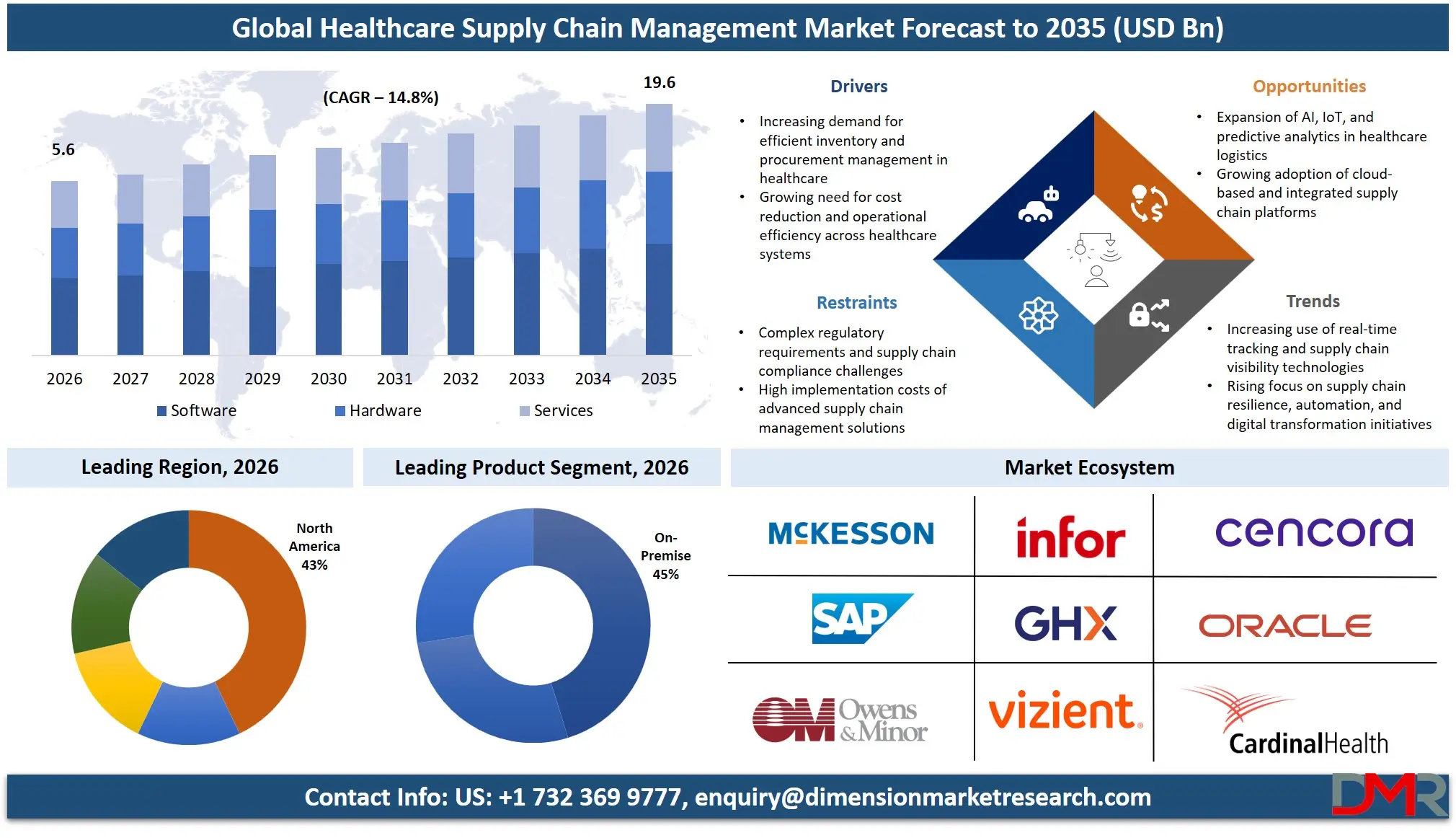

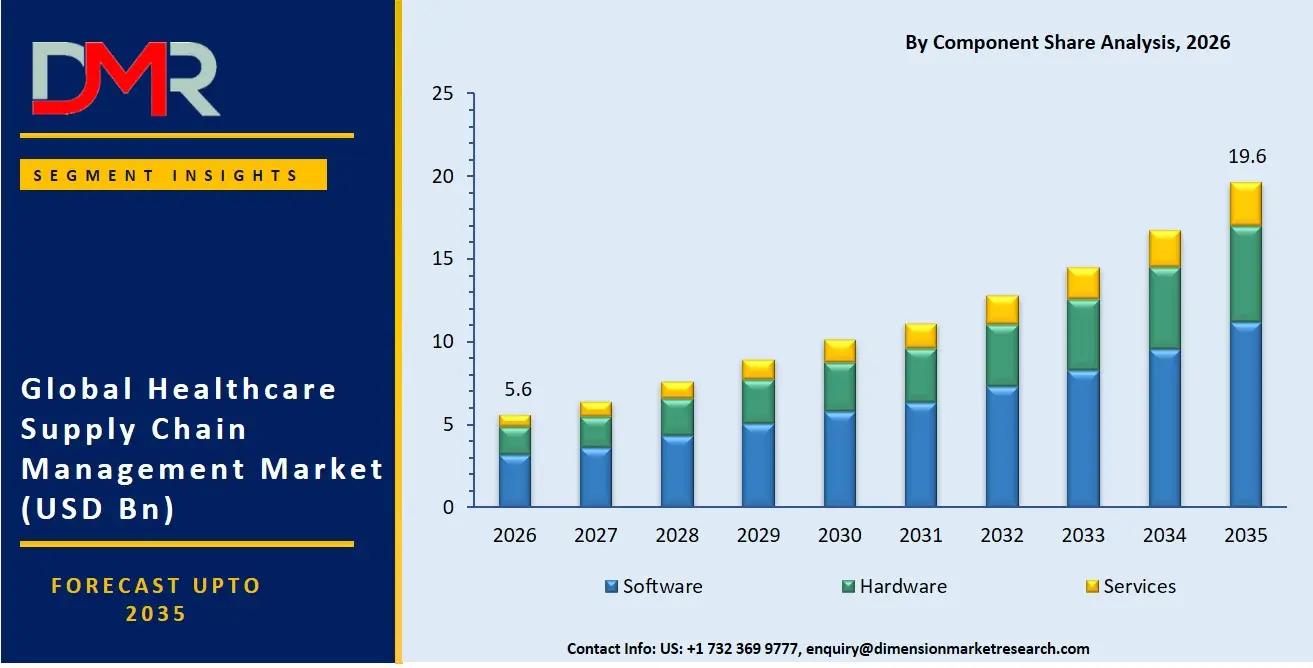

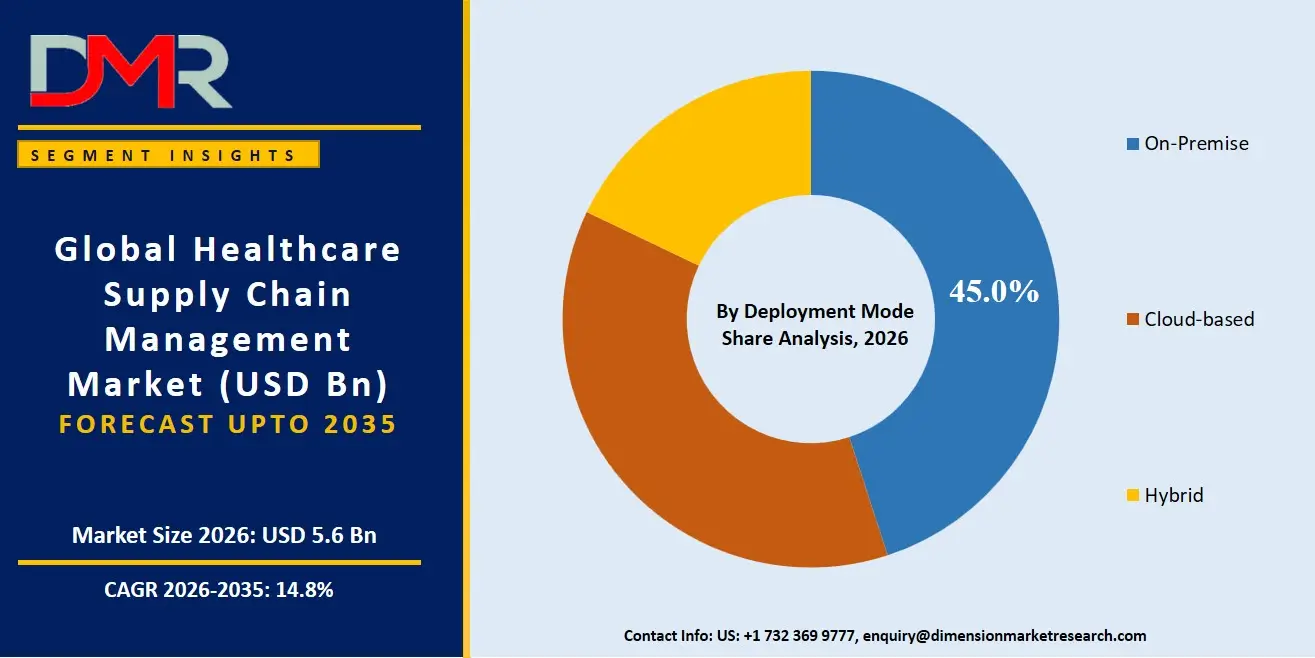

- The global Healthcare Supply Chain Management Market is valued at USD 4.9 Billion in 2025, reached USD 5.6 Billion in 2026, and is projected to hit USD 19.6 Billion by 2035 at a CAGR of 14.8%.

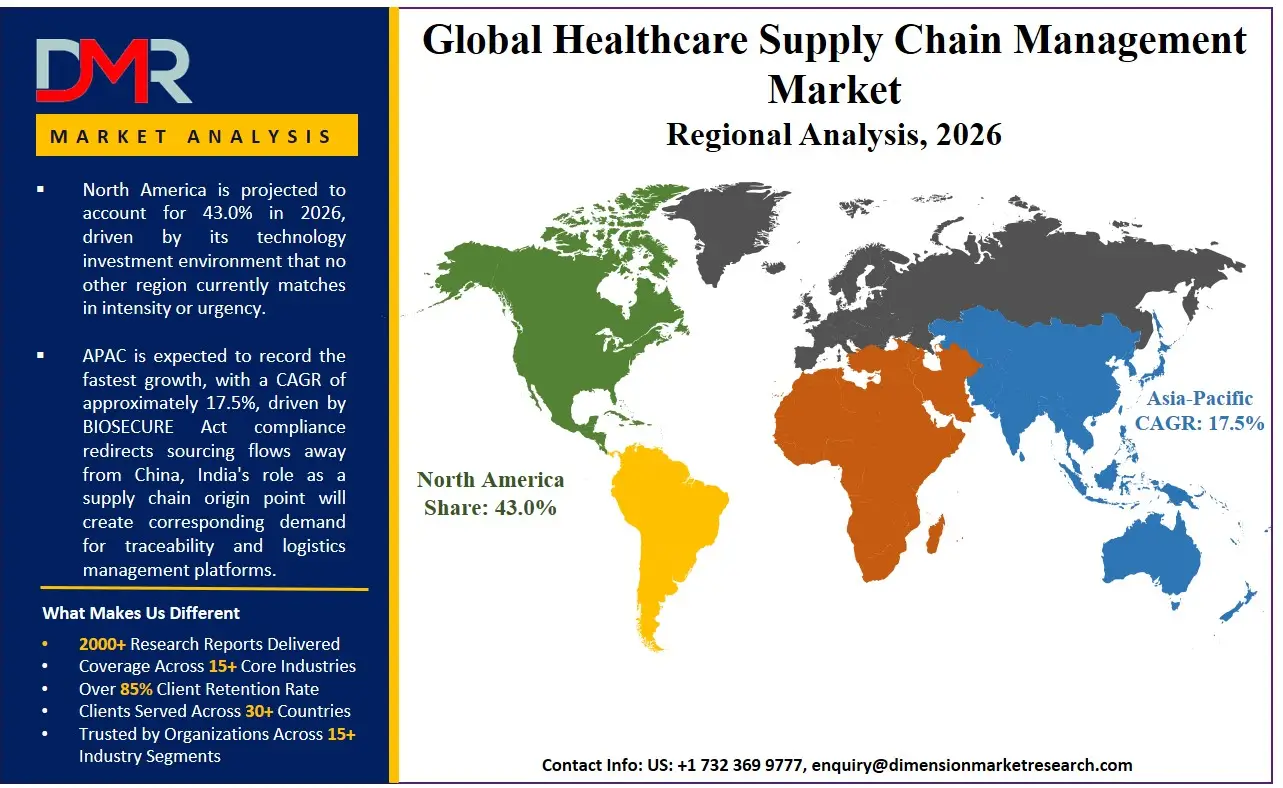

- North America holds the dominant regional position with a 43.0% revenue share in 2026, led by the United States at approximately 75% of the regional total.

- Software leads the By Component segment with a 56.9% revenue share in 2026.

- On-Premise holds the dominant position in the By Deployment Mode segment in 2026, preferred by large hospital networks and pharmaceutical manufacturers prioritizing data control.

- Healthcare Product Manufacturers lead the By End-User segment in 2026, driven by DSCSA compliance enforcement activating for this group first on May 27, 2025.

- Planning holds the dominant position in the By Function segment in 2026, as demand forecasting and inventory planning tools move to the center of supply chain operations.

- The U.S. market is valued at USD 1.8 billion in 2026 and is projected to reach USD 5.7 Billion by 2035 at a CAGR of 13.1%.

- China's market stands at USD 588.0 Million in 2026, projected to reach USD 2.3 Billion by 2035 at a CAGR of 15.4%.

Market Overview

The Healthcare Supply Chain Management market covers software platforms, hardware systems, and professional services that coordinate the procurement, tracking, distribution, and return of medical products. Pharmaceutical distribution, medical device logistics, inventory management, and traceability systems all fall within its scope. Clinical care itself sits outside this boundary, but every operational layer connecting manufacturers to patients falls inside it.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Healthcare Supply Chain Management Market connects pharmaceutical manufacturers, wholesale distributors, hospital systems, and dispensers into a single trackable flow. As drug complexity rises and regulatory oversight tightens, the operational backbone Healthcare Supply Chain Management Market provides becomes structurally irreplaceable. Based on data from a Medscape and HIMSS AI Adoption report, 60% of healthcare professionals surveyed in 2024 acknowledged AI's ability to uncover patterns beyond human detection. Platforms that embed this capability at the decision layer are no longer competing on features. They are competing on regulatory survival.

Federal mandates are accelerating technology adoption at a pace no organization can ignore. The Drug Supply Chain Security Act enforced phased compliance for manufacturers from May 27, 2025, wholesale distributors from August 27, 2025, and large dispensers from November 27, 2025, requiring interoperable electronic tracing across the entire distribution chain. The BIOSECURE Act, signed into law on December 18, 2025, restricts U.S. federal contracts with Chinese biotechnology companies of concern and creates a five-year window during which U.S. pharmaceutical sponsors must replace Chinese CDMO capacity. For supply chain software and logistics providers, both laws convert regulatory obligation into direct platform spending.

Market Size and Forecast

The Global Healthcare Supply Chain Management Market size is estimated at USD 5.6 Billion in 2026 from USD 4.9 Billion in 2025, and is projected to reach USD 19.6 Billion by 2035, exhibiting a CAGR of 14.8% during the forecast period.

A CAGR of 14.8% reflects structural transformation, not cyclical recovery. Regulatory mandates, digital integration requirements, and supply security concerns have converted technology-enabled supply chain management from a discretionary upgrade into a non-negotiable operational investment. Organizations across every node of the chain face simultaneous pressure from serialization compliance, shortage risk, and cybersecurity exposure. Each of these forces independently justifies platform investment. Together, they create a spending environment that sustains above-average growth across the full forecast window.

The U.S. market is forecast to grow faster than the global average at a CAGR of 13.1%, reaching USD 5.7 Billion by 2035. Countries that face concentrated regulatory intensity tend to lead adoption curves. The U.S. currently combines DSCSA enforcement, escalating FDA warning activity, and post-Change Healthcare cybersecurity mandates into a single compliance pressure stack that no other market currently matches. China's market is projected to grow at a CAGR of 15.4% through 2035, reaching USD 2.3 Billion. While below the global average, the absolute trajectory remains material as global sourcing patterns shift and traceability requirements extend further into Asian manufacturing networks.

Market Dynamics

FDA Enforcement and Drug Shortage Pressure Force Technology Investment

The FDA tracked 277 active drug shortages in late 2024, down from a record 323 in Q1 2024, as reported by the U.S. FDA. A reduction from a record high does not signal resolution. Ongoing strain at this level converts directly into demand for predictive analytics, automated reordering systems, and real-time inventory visibility tools. Organizations that depend on reactive procurement face direct exposure every time a shortage materializes without warning.

The FDA issued 105 warning letters in FY2024, the highest in five years, with inspection-based letters rising 21% from FY2023, as confirmed by the U.S. FDA. Recall sites concentrated in the U.S. at 48% and India at 41%. This enforcement intensity signals that supplier networks face escalating quality accountability. Healthcare organizations cannot manage this exposure through periodic audits. End-to-end supply chain visibility platforms become the only operationally credible response.

Cybersecurity Failures and Workforce Gaps Constrain Adoption Speed

On February 21, 2024, the ALPHV/BlackCat ransomware group attacked Change Healthcare, halting national claims, e-prescribing, and eligibility operations. As reported by the American Hospital Association, 94% of U.S. hospitals experienced cash flow disruptions. The American Medical Association found that 85% of physicians reported continuing claim payment disruptions and 79% could not receive electronic remittance advice. This single event exposed how concentration in one vendor creates systemic risk across the entire supply chain.

Workforce limitations slow the pace at which organizations can absorb new technology regardless of regulatory pressure. Research by ISPE in 2024 found that 80% of pharmaceutical manufacturers cited a gap between existing employee skills and the evolving requirements for reshoring and nearshoring builds. This skills shortfall directly delays implementation timelines for advanced supply chain platforms. Organizations may have the budget and the compliance mandate but lack the internal capability to deploy and operate these systems at the required pace.

BIOSECURE Act and Federal Transparency Mandates Open New Platform Opportunities

The BIOSECURE Act was signed into law on December 18, 2025, via the FY2026 NDAA. U.S. pharmaceutical sponsors must replace Chinese CDMO capacity with domestic or allied-nation production within five years. New sourcing platforms, vendor onboarding tools, and compliance-tracking software become required infrastructure for every affected sponsor. This is a defined, time-bound investment cycle with a clear start date and a compliance deadline that cannot be extended by commercial negotiation.

The HHS January 2024 white paper called for public FDA Establishment Identifier data and volume reporting to predict and prevent drug shortages. Providers that build FEI-compatible data layers into their platforms will hold a structural compliance advantage as this infrastructure requirement expands. The cyber-resilience gap that Change Healthcare exposed has opened a parallel market for specialized supply chain security services. Vendors who build verified, breach-resilient architectures are entering a buyer environment where security posture has become a primary procurement criterion.

Market Trends

AI Integration, DSCSA Serialization, and BIOSECURE Decoupling Reshape Supply Chain Architecture

Based on data from GHX's 2025 healthcare supply chain predictions, dynamic re-routing, real-time substitutions, and AI-driven risk modeling represent this year's primary operational shifts for hospital supply chains. Organizations that embed AI at the decision layer rather than the reporting layer gain measurable advantages in shortage response time and procurement accuracy. Platforms that use AI only for dashboards and summaries are already falling behind peers who use it to trigger automated purchasing responses.

Serialization is becoming the industry baseline. The Healthcare Distribution Alliance confirms that DSCSA requires unit-level traceability for approximately 4 billion prescription drug packages annually, using GS1 GTIN and GLN standards. Platforms that entered 2025 without validated serialization capabilities faced a credibility gap that feature updates alone cannot close. Early movers who built GS1-compatible serialization ahead of the mandate now hold an infrastructure lead that competitors cannot replicate quickly.

Health-ISAC's November 2024 whitepaper reported that the BIOSECURE Act has driven severance of U.S. and China pharma supply linkages, disrupting global pharmaceutical networks. Supply chain platforms that can onboard and manage Indian and allied-nation CDMOs at scale are better positioned to serve the transition that the BIOSECURE Act has made structurally inevitable. Vendors without multi-country supplier qualification and compliance-tracking capabilities will find themselves excluded from the largest sourcing infrastructure rebuild in a generation.

Component Analysis

Software leads the segment with a 56.9% share, reflecting a market where regulatory mandates make software the non-negotiable operational layer. Organizations cannot meet DSCSA traceability requirements through hardware or manual processes alone. Software investment is a legal necessity, not a competitive choice.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Hardware supports the physical execution layer of healthcare supply chain operations. Barcode scanners, RFID readers, and automated mobile robots enable real-time inventory transactions and cross-docking alerts. Hardware adoption ties directly to software deployments, meaning its growth follows enterprise platform decisions rather than leading them. Services encompass implementation, integration, training, and ongoing managed support. Professional services become the bridge between technology investment and operational readiness for organizations lacking in-house expertise.

Deployment Mode Analysis

With a dominant share in 2026, On-Premise deployment holds the strongest position due to data control priorities among large hospital networks and pharmaceutical manufacturers. Organizations with established IT infrastructure retain on-premise deployments to maintain direct control over sensitive procurement and patient-linked data. Caution toward externally hosted platforms remains high across this buyer segment.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Cloud-Based deployment is reshaping how mid-size and decentralized healthcare systems access supply chain capabilities. Cloud platforms lower upfront infrastructure costs and allow faster compliance updates, a meaningful advantage when regulatory timelines require rapid system changes. Hybrid deployment combines on-premise control with cloud scalability, allowing healthcare organizations to keep sensitive data locally while running analytics and reporting workloads in the cloud. Large health systems navigating both DSCSA traceability requirements and post-Change Healthcare cybersecurity mandates find this model particularly relevant.

End-User Analysis

Healthcare Product Manufacturers accounts for the largest share of the segment, driven by DSCSA compliance enforcement activating for manufacturers first on May 27, 2025. Manufacturers face the dual pressure of serialization compliance and quality enforcement simultaneously. Supply chain platform investment has become a regulatory priority for this group before any other end-user category.

Healthcare Providers represent the largest end-user category by operational scale, investing in end-to-end visibility tools that connect procurement, inventory, and claims processing into unified, breach-resilient architectures. Distributors occupy the critical middle layer of the healthcare supply chain, moving pharmaceutical and medical products between manufacturers and providers. DSCSA enforcement applied to wholesale distributors from August 27, 2025, requiring interoperable electronic tracing at the package level across every product handoff.

Function Analysis

Planning captures the dominant share of segment demand, as organizations that rely on reactive procurement face direct exposure to shortage events. Demand forecasting and inventory planning tools have moved to the center of supply chain operations. Organizations with predictive planning platforms can model risk and pre-position inventory before shortages materialize.

Sourcing functions manage vendor selection, contract management, and supplier qualification across pharmaceutical and medical product categories. The BIOSECURE Act is directly reshaping sourcing decisions by restricting U.S. federal contracts with Chinese biotechnology companies of concern, creating immediate demand for platforms that manage the transition to domestic and allied-nation suppliers. Delivery encompasses the physical and digital logistics layer that moves products from distribution centers to point-of-care locations. Return management covers reverse logistics for expired, recalled, or defective healthcare products, functioning as a compliance layer rather than a secondary operational tool for organizations facing FDA recall exposure.

Key Market Segments

By Component

- Software

- Hardware

- Services

By Deployment Mode

- On-Premise

- Cloud-Based

- Hybrid

By End-User

- Healthcare Product Manufacturers

- Healthcare Providers

- Distributors

By Function

- Planning

- Sourcing

- Delivery

- Return

Regional Analysis

North America held a dominant position in 2026 with a 43.0% revenue share of the global Healthcare Supply Chain Management Market, valued at USD 4.9 Billion globally. The United States accounts for approximately 75% of the regional share. DSCSA enforcement, escalating FDA warning activity, and post-Change Healthcare cybersecurity mandates collectively create a compliance-driven technology investment environment that no other region currently matches in intensity or urgency. Structural regulatory pressure of this density does not produce optional spending. It produces committed, multi-year platform budgets.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Asia Pacific is the market's fastest-expanding regional block. China's market is valued at USD 588.0 Million in 2026 and is forecast to reach USD 2.3 Billion by 2035 at a CAGR of 15.4%. India operates more than 3,000 pharmaceutical companies and 10,500 manufacturing units as of FY2025, ranking third globally by pharmaceutical output volume. As BIOSECURE-driven sourcing redirection channels more U.S. and European volume through Indian manufacturers, demand for traceability and logistics management platforms within the region will grow faster than the current installed base can absorb. Europe follows a steady technology refresh cycle, layering AI and cloud capabilities onto existing serialization infrastructure established under the EU Falsified Medicines Directive. Latin America and the Middle East and Africa present later-entry adoption profiles, where foundational software platforms rather than advanced AI modules will drive initial spending cycles.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Competitive Landscape

The Healthcare Supply Chain Management Market operates as a moderately fragmented structure. Large enterprise software vendors compete against specialized niche platforms, and traditional logistics firms are expanding into technology-enabled supply chain services through acquisition. No single player controls more than a small fraction of the total addressable market. Competitive positioning depends on vertical depth, regulatory expertise, and integration capability rather than scale alone.

Oracle's September 2025 announcement of AI-powered inventory management and procurement capabilities within its Fusion Cloud Applications suite added autonomous mobile robot integration, real-time cross-docking alerts, and EHR connectivity. Providers who lock in EHR and procurement integrations simultaneously raise switching costs for buyers significantly. Healthcare organizations already running Oracle clinical systems face a lower barrier to supply chain adoption, giving Oracle a built-in pipeline that competitors must actively displace.

DHL Supply Chain agreed to acquire SDS Rx in September 2025, a final-mile healthcare delivery provider operating from more than 200 U.S. locations serving long-term care, specialty pharmacies, and radiopharmacies. This marked DHL Supply Chain's second healthcare acquisition of 2025 alone. These moves signal that logistics conglomerates are consolidating the physical supply chain layer while software vendors consolidate the digital layer above it. Specialty platform providers are carving defensible positions through compliance-specific capabilities. Vendors with pre-built GS1 GTIN and GLN serialization modules gained immediate procurement relevance across manufacturers, distributors, and dispensers facing the 2025 DSCSA compliance deadline.

Company Profiles

Manhattan Associates holds a strong position in healthcare supply chain software through its warehouse management and supply chain execution platforms. The company's competitive advantage lies in its ability to integrate demand planning, inventory optimization, and order management within a unified architecture. For healthcare clients operating under DSCSA traceability requirements, a single-platform approach reduces integration risk and compliance complexity, giving Manhattan Associates a structural edge over point-solution competitors.

Blue Yonder Group, Inc. competes on AI-driven planning and fulfillment capabilities, targeting large healthcare distributors and manufacturers that require predictive analytics at scale. Its platform addresses shortage-risk modeling directly, a critical priority in a market where procurement failures translate into patient care disruption. Blue Yonder's risk is that its AI differentiation is increasingly matched by enterprise vendors embedding analytics natively, which may compress its standalone value proposition over the forecast period.

Key Players

- Manhattan Associates

- Blue Yonder Group, Inc.

- Oracle Cerner

- Jump Technologies

- LogiTag Systems

- Harris Affinity

- Premier Inc.

- Hybrent

- Arvato Systems

- Palantir Technologies

- InterSystems

- UFP Technologies

Supply Chain and Value Chain Analysis

The healthcare supply chain begins with raw material suppliers and active pharmaceutical ingredient manufacturers, then moves through contract development and manufacturing organizations, finished product manufacturers, wholesale distributors, and finally to healthcare providers and dispensers. McKesson's U.S. Pharmaceutical segment distributes one-third of pharmaceuticals used in North America, as stated in its FY2025 10-K, and reported Q3 FY2025 revenue of USD 89.4 Billion, up 19% year-over-year. Cencora's FY2025 revenue reached USD 321.3 Billion, with U.S. Healthcare Solutions alone contributing USD 285.0 Billion. These figures confirm that pharmaceutical distribution captures the bulk of financial flow, while software vendors capture the margin associated with compliance and analytics.

The most significant bottleneck in the current chain sits at the API sourcing level. Between 2018 and 2023, 258 unique active pharmaceutical ingredients went into national shortage in the U.S., as reported by the HHS ASPE. The BIOSECURE Act adds a geopolitical constraint on top of this structural fragility by restricting sourcing from Chinese biotechnology companies of concern. Cardinal Health's Global Medical Products and Distribution segment reported Q4 FY2025 revenue of USD 3.2 Billion, up 3.0% year-over-year, illustrating how physical distribution control remains concentrated among a small number of established players. Software platform vendors are steadily acquiring informational control through compliance tools and AI analytics, which represents a different but equally durable form of market power within the same chain.

Regulatory Landscape

The Drug Supply Chain Security Act represents the most operationally significant regulatory force currently active in Healthcare Supply Chain Management Market. Phased enforcement activated for manufacturers on May 27, 2025, wholesale distributors on August 27, 2025, and large dispensers on November 27, 2025, as confirmed by the U.S. FDA. According to the Healthcare Distribution Alliance, this mandate covers unit-level traceability for approximately 4 billion prescription drug packages annually, using GS1 GTIN and GLN standards. Non-compliance exposes organizations to FDA enforcement action, making this the market's most immediate regulatory spending catalyst.

The BIOSECURE Act, signed into law on December 18, 2025, via the FY2026 NDAA, restricts U.S. federal contracts with Chinese biotechnology companies of concern. U.S. pharmaceutical sponsors must replace Chinese CDMO capacity with domestic or allied-nation production within a five-year window. For supply chain technology providers, this law is not just a sourcing regulation. It is a platform rebuild mandate requiring new vendor qualification workflows, compliance tracking systems, and sourcing analytics tools across the entire affected sponsor base.

FDA quality enforcement is intensifying in parallel with traceability mandates. Recall sites in FY2024 were concentrated in the U.S. at 48% and India at 41%, as reported by the FDA. Organizations operating manufacturing or distribution sites in either country face the highest regulatory scrutiny. Supply chain platforms that integrate FDA warning letter data and recall tracking into their risk dashboards hold a measurable compliance advantage over platforms that treat quality monitoring as a separate workflow.

India's regulatory environment is directly relevant to global supply chains given the country's scale. The India-New Zealand Free Trade Agreement, finalized in December 2025, provides zero-duty access for Indian pharmaceutical exports across approximately 90 tariff lines, replacing duties of up to 5%. As India becomes a larger sourcing alternative under BIOSECURE-driven redirection, its domestic regulatory standards and export compliance frameworks become increasingly material to global supply chain risk assessments.

Investment and White Space Analysis

Current investment flow concentrates at two layers: AI-native software platforms and final-mile healthcare logistics. Clarium's total funding reached USD 43 Million through May 2025, backed by General Catalyst, Kaiser Permanente Ventures, and Texas Medical Center Ventures, targeting AI-powered hospital supply chain resiliency. The investor composition combines financial capital with strategic healthcare operators. Early-stage capital is moving toward platforms that address shortage prediction and vendor risk modeling simultaneously, signaling conviction that AI-native platforms will displace legacy systems rather than supplement them.

The most underserved segment in Healthcare Supply Chain Management Market is small and mid-size healthcare providers. Large integrated delivery networks and major distributors have the procurement scale and IT budgets to adopt enterprise platforms. Smaller hospital systems, independent pharmacies, and specialty clinics lack equivalent resources. The DSCSA compliance mandate applies to dispensers of all sizes, creating a forced-adoption dynamic in a segment that currently lacks adequate platform coverage. Vendors who build lightweight, compliance-first products for this tier will face limited direct competition from enterprise players.

India's pharmaceutical export base reached USD 30.5 Billion in FY2024-25, yet the domestic supply chain technology infrastructure supporting this manufacturing base remains underdeveloped relative to its global output scale. As BIOSECURE-driven sourcing redirection channels more U.S. and European volume through Indian manufacturers, demand for traceability, quality compliance, and logistics management platforms within India will grow faster than the current installed base can absorb. Platforms that establish reference deployments with major sponsors in 2026 and 2026 will hold procurement credibility that late entrants cannot replicate within the same transition window.

Recent Developments

- November 3, 2025: UPS. Acquisition completed. UPS completed its acquisition of Andlauer Healthcare Group at CAD 55.00 per share for a total purchase price of approximately CAD 2.2 Billion (approximately USD 1.6 Billion), with founder Michael Andlauer leading UPS Canada Healthcare and AHG operations.

- April 2, 2025: McKesson. Acquisition completed. McKesson completed its acquisition of an approximately 80% controlling interest in PRISM Vision Holdings for approximately USD 850 Million, with PRISM physicians retaining approximately 20% following the agreement signed February 4, 2025.

- January 2, 2025: Cencora. Acquisition completed. Cencora completed its USD 4.04 Billion acquisition of Retina Consultants of America, the largest specialty pharmaceutical supply chain integration of FY2025, expanding its specialty distribution and healthcare supply chain services footprint.

- August 2024: Clarium. Funding round and platform launch. Clarium raised USD 10.5 Million led by General Catalyst, alongside the launch of its Astra OS workflow platform for hospital supply chain operations.

- March 18, 2024: Cardinal Health. Acquisition completed. Cardinal Health completed its acquisition of Specialty Networks and its PPS Analytics platform, serving 11,500 providers including more than 7,000 physicians across 1,200 independent urology, gastroenterology, and rheumatology practices.

- February 21, 2024: Change Healthcare. Ransomware attack. The ALPHV/BlackCat group attacked Change Healthcare, halting national claims, e-prescribing, and eligibility operations. UnitedHealth reportedly paid approximately USD 22 Million (approximately 350 BTC) in ransom, with the breach affecting a platform that processed roughly half of all U.S. medical claims annually.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 4.9 Billion |

| Market Value (2026) |

USD 5.6 Billion |

| Forecast Revenue (2035) |

USD 19.6 Billion |

| CAGR (2026–2035) |

14.8% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020 to 2024 |

| Forecast Period |

2026 to 2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Component (Software, Hardware, Services), By Deployment Mode (On-Premise, Cloud-Based, Hybrid), By End-User (Healthcare Product Manufacturers, Healthcare Providers, Distributors), By Function (Planning, Sourcing, Delivery, Return) |

| Regional Analysis |

North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape |

Manhattan Associates, Blue Yonder Group Inc., Oracle Cerner, Jump Technologies, LogiTag Systems, Harris Affinity, Premier Inc., Hybrent, Arvato Systems, Palantir Technologies, InterSystems, UFP Technologies |

| Customization Scope |

Customization for segments and region or country level will be provided. Additional customization can be done based on requirements. |

| Purchase Options |

Three license options: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |

Frequently Asked Questions

What is the biggest investment opportunity in Healthcare Supply Chain Management Market?

▾ The market expands from USD 4.9 Billion in 2025 to USD 19.6 Billion by 2035. The clearest white space lies in AI-native platforms for smaller healthcare providers, BIOSECURE-compliant sourcing tools for U.S. pharmaceutical sponsors, and cyber-resilient supply chain architectures. All three address documented, regulation-created gaps that current offerings do not fully cover.

Who are the top companies in Healthcare Supply Chain Management Market?

▾ Key players include Manhattan Associates, Blue Yonder Group Inc., Oracle Cerner, Jump Technologies, LogiTag Systems, Harris Affinity, Premier Inc., Hybrent, Arvato Systems, Palantir Technologies, InterSystems, and UFP Technologies. Oracle's September 2025 AI platform update and Clarium's USD 43 Million in total funding reflect competitive intensity at both the enterprise and emerging player levels.

Which segment is growing fastest in Healthcare Supply Chain Management Market and why?

▾ Cloud-Based deployment is positioned for the fastest adoption trajectory as healthcare organizations require rapid compliance updates and AI-integrated analytics. Cloud-native platforms that bundle AI with compliance tools are accelerating adoption across mid-size and decentralized health systems that cannot absorb the infrastructure cost of on-premise deployments.

Which region is growing fastest in Healthcare Supply Chain Management Market and why?

▾ Asia Pacific is the fastest-expanding regional block, anchored by India's expanding pharmaceutical manufacturing base and BIOSECURE-driven sourcing redirection away from China. India operates more than 10,500 manufacturing units as of FY2025, and as more U.S. and European volume routes through Indian manufacturers, demand for traceability and logistics management platforms within the region will accelerate beyond current forecasts.

What is the biggest challenge holding Healthcare Supply Chain Management Market back?

▾ Cybersecurity vulnerability is the most immediate constraint. The February 2024 Change Healthcare ransomware attack disrupted cash flows for 94% of U.S. hospitals and exposed the absence of multi-factor authentication on infrastructure processing roughly half of all U.S. medical claims. Congressional scrutiny and CMS advance payment interventions confirmed that regulators now treat supply chain cyber-resilience as a public health infrastructure concern.