Market Overview

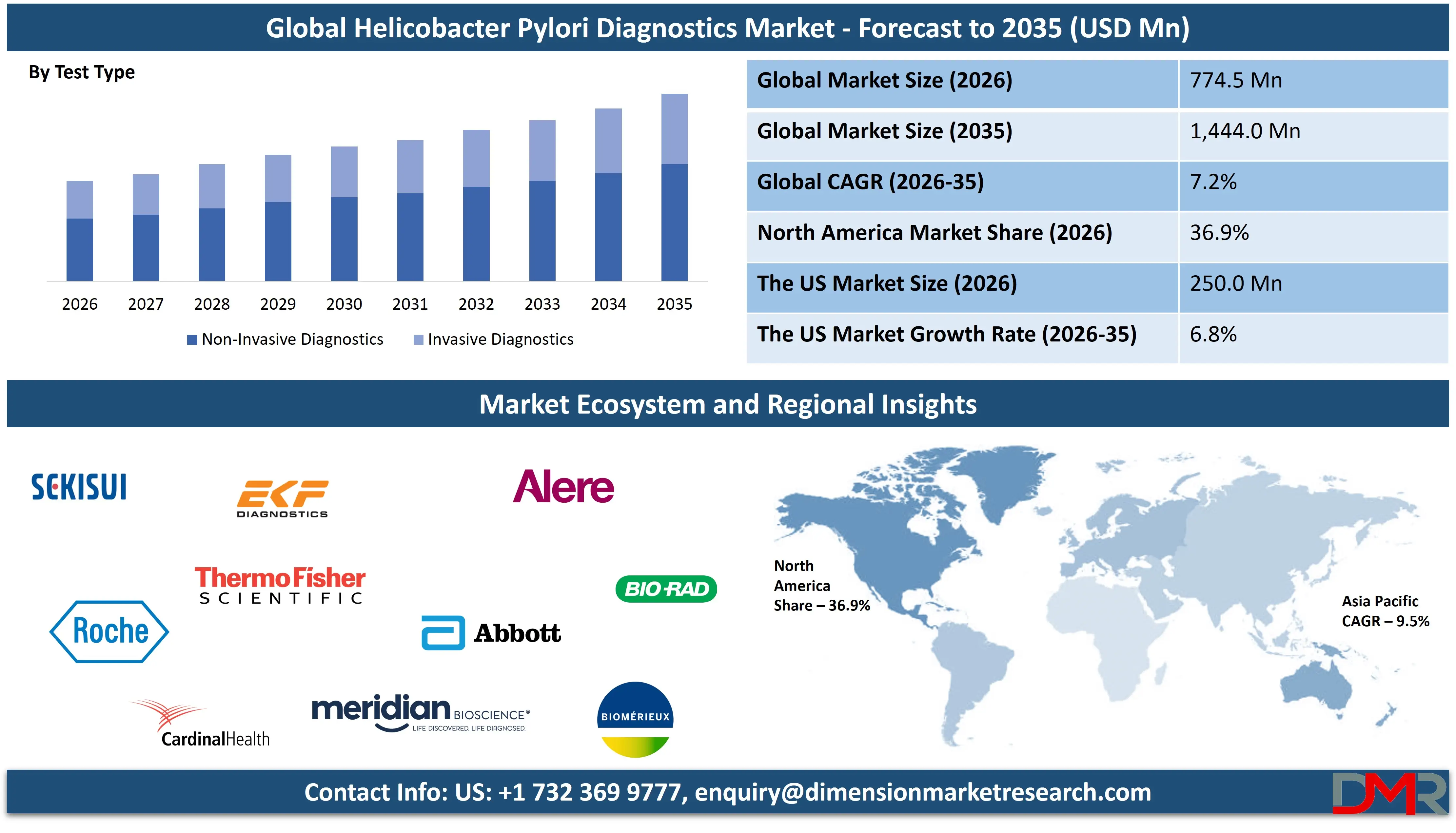

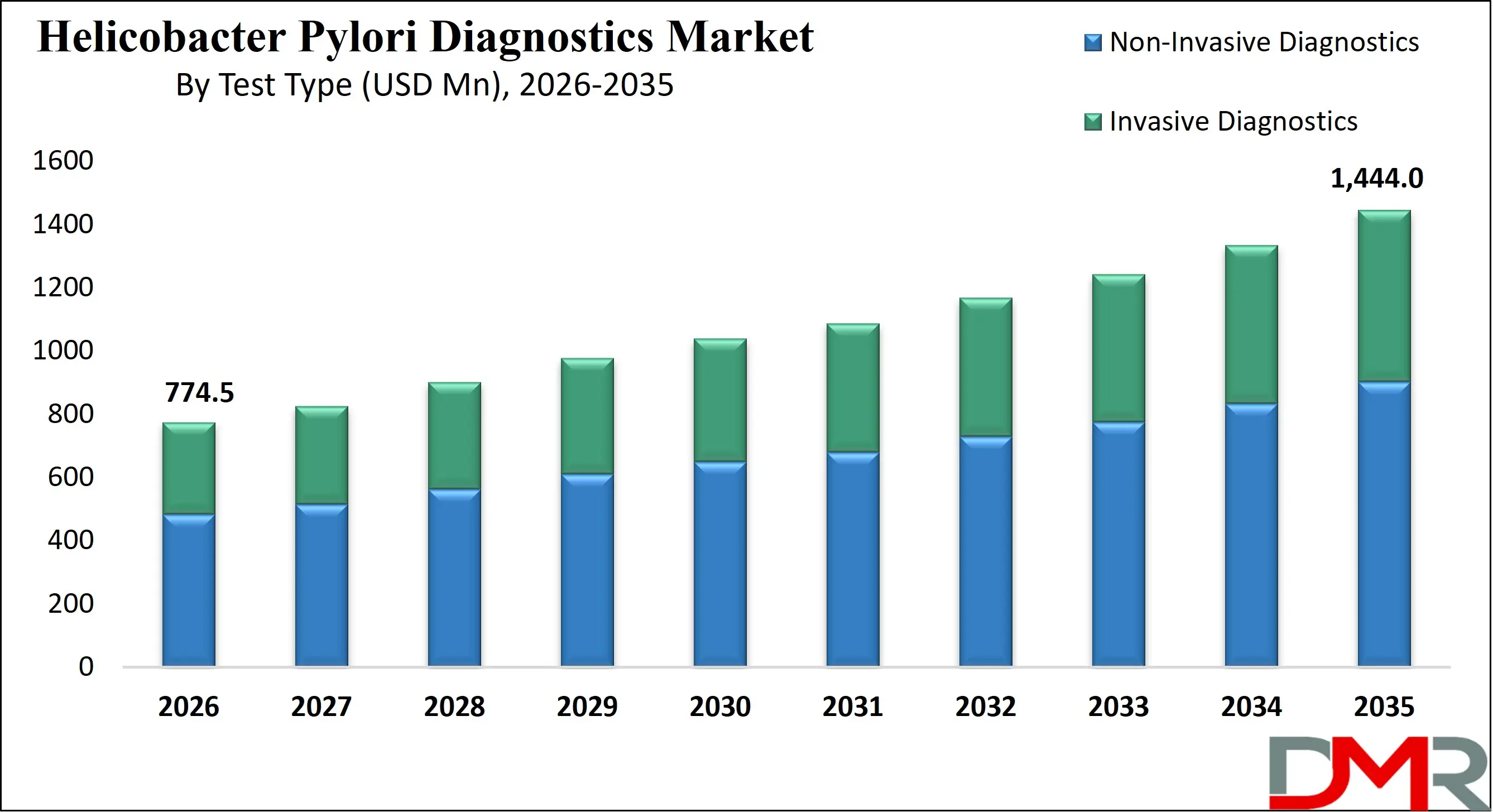

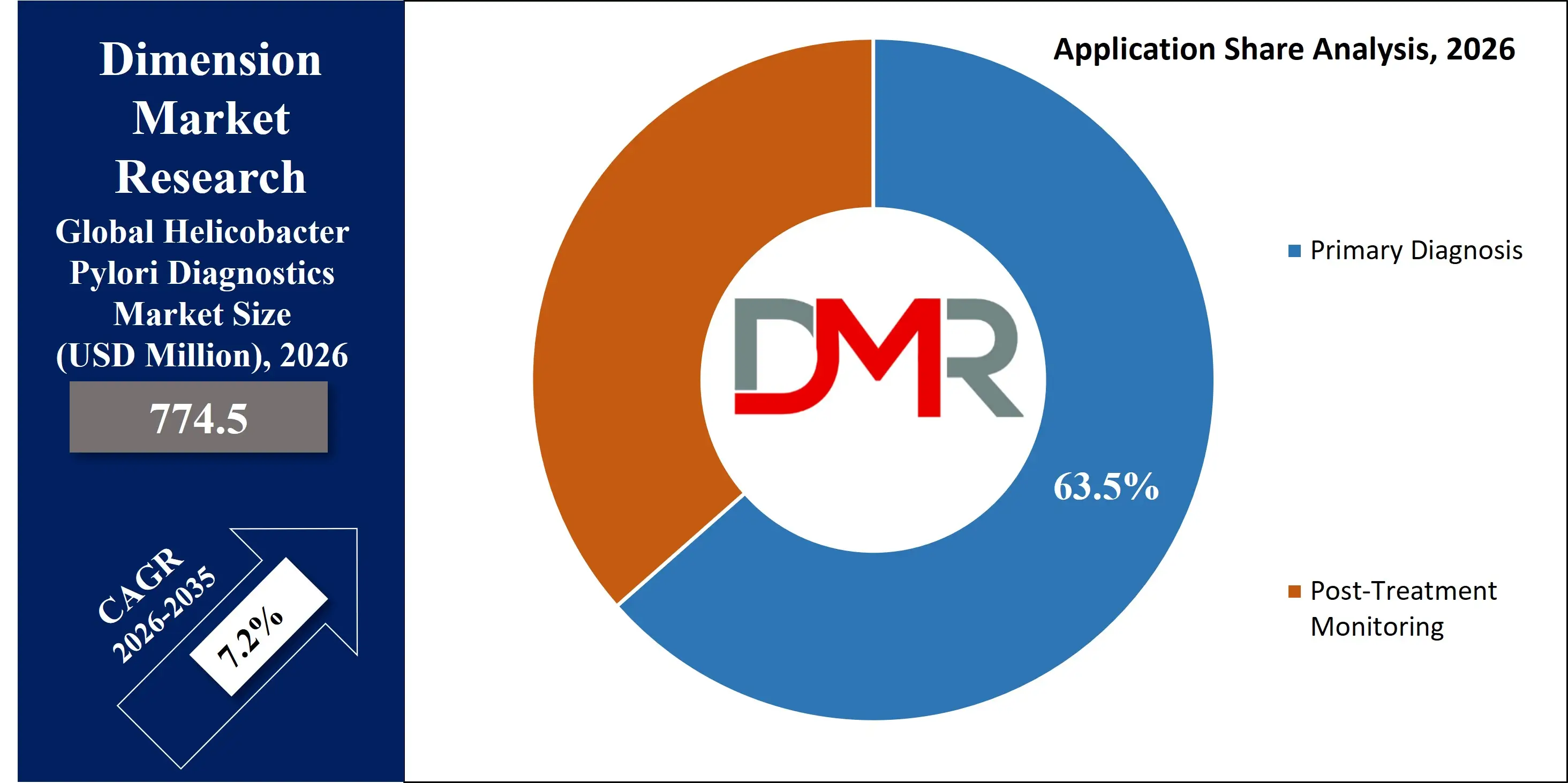

The Global Helicobacter Pylori Diagnostics Market size is projected to reach USD 774.5 million in 2026 and grow at a compound annual growth rate of 7.2% to reach a value of USD 1,444.0 million in 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Helicobacter Pylori Diagnostics comprises a variety of medical testing methods designed to identify infection caused by Helicobacter pylori, a bacterium strongly linked to peptic ulcers, chronic gastritis, and gastric cancer. The field includes invasive procedures such as endoscopic biopsy-based tests—rapid urease testing, histology, and culture, as well as non-invasive techniques like urea breath tests, stool antigen assays, serological tests, and PCR-based molecular diagnostics. These solutions are utilized in hospitals, diagnostic laboratories, and point-of-care environments to support timely and accurate detection.

It plays a critical role within gastroenterology and infectious disease diagnostics because of the widespread prevalence of H. pylori and its association with serious gastrointestinal complications. Increasing public awareness of digestive health, broader screening initiatives, and a stronger focus on early cancer prevention are fueling demand for reliable testing options. Continuous improvements in immunoassays and molecular technologies are enhancing sensitivity, specificity, and result turnaround times, making diagnostics more dependable and accessible.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Ongoing technological progress, particularly in automation and molecular amplification platforms, is streamlining laboratory operations and enabling detection of antibiotic resistance mutations. Healthcare systems are increasingly favoring non-invasive, patient-centric testing approaches, encouraging a shift away from conventional serology toward stool antigen and breath-based diagnostics. At the same time, strategic collaborations, digital reporting integration, and expanded antimicrobial resistance surveillance efforts are shaping innovation, accessibility, and long-term growth across the sector.

The US Helicobacter Pylori Diagnostics Market

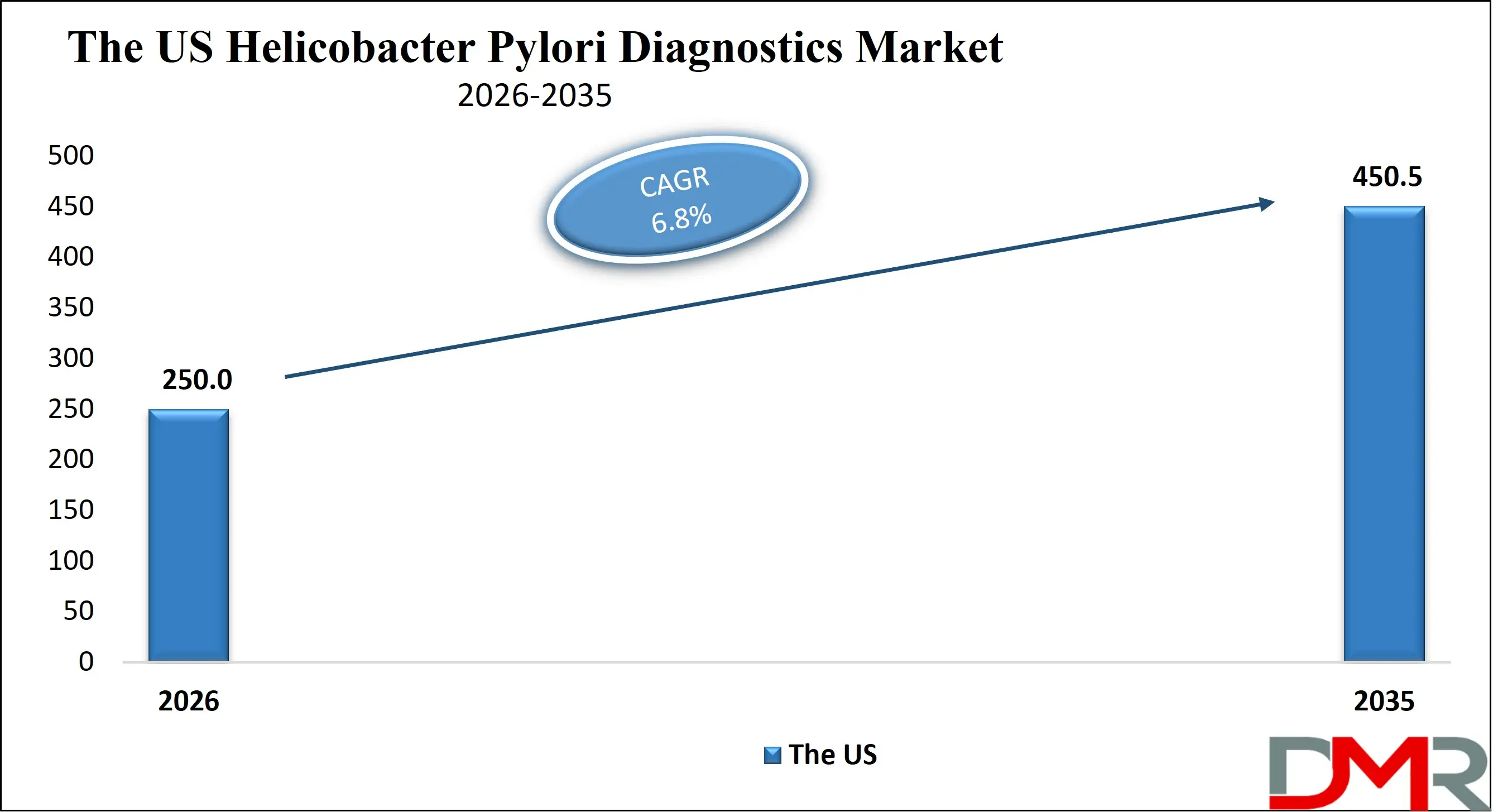

The US Helicobacter Pylori Diagnostics Market size is projected to reach USD 250.0 million in 2026 at a compound annual growth rate of 6.8% over its forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

In the US, the market is driven by advanced healthcare infrastructure, high awareness levels, and established reimbursement frameworks. Strong presence of leading diagnostic manufacturers and reference laboratories supports rapid adoption of molecular and breath test technologies. Clinical guidelines promoting test-of-cure strategies and antibiotic resistance monitoring further stimulate demand. Government-backed cancer prevention initiatives and insurance coverage for non-invasive diagnostics contribute to steady growth. Market competition centers on accuracy, turnaround time, and integration with electronic health record systems.

Europe Helicobacter Pylori Diagnostics Market

Europe Helicobacter Pylori Diagnostics Market size is projected to reach USD 193.6 million in 2026 at a compound annual growth rate of 7.1% over its forecast period.

Across Europe, growth is influenced by structured screening programs and policy frameworks aligned with preventive healthcare goals, including initiatives linked to the European Green Deal’s broader health sustainability agenda. Countries such as Germany, France, and Italy emphasize early detection to reduce gastric cancer burden. Regulatory standards under CE marking facilitate innovation while ensuring safety. Increasing adoption of stool antigen and molecular diagnostics reflects the region’s focus on accurate, non-invasive testing and antimicrobial stewardship programs.

Japan Helicobacter Pylori Diagnostics Market

Japan Helicobacter Pylori Diagnostics Market size is projected to reach USD 38.7 million in 2026 at a compound annual growth rate of 7.0% over its forecast period.

In Japan, high gastric cancer incidence and national screening programs significantly influence demand. Government-supported eradication policies and insurance coverage for H. pylori testing and treatment accelerate uptake. Technological sophistication and strong domestic diagnostic manufacturing capabilities support rapid innovation. Urbanization and aging demographics increase routine endoscopic examinations, sustaining invasive diagnostic use. However, cost pressures and strict regulatory approval processes present challenges, while opportunities lie in advanced molecular resistance profiling and automated laboratory systems.

Helicobacter Pylori Diagnostics Market: Key Takeaways

- Market Growth: The Helicobacter Pylori Diagnostics Market size is expected to grow by USD 619.7 million, at a CAGR of 7.2%, during the forecasted period of 2027 to 2035.

- By Test Type: The non-invasive diagnostics segment is anticipated to get the majority share of the Helicobacter Pylori Diagnostics market in 2026.

- By Application: The Primary diagnostics segment is expected to get the largest revenue share in 2026 in the Helicobacter Pylori Diagnostics market.

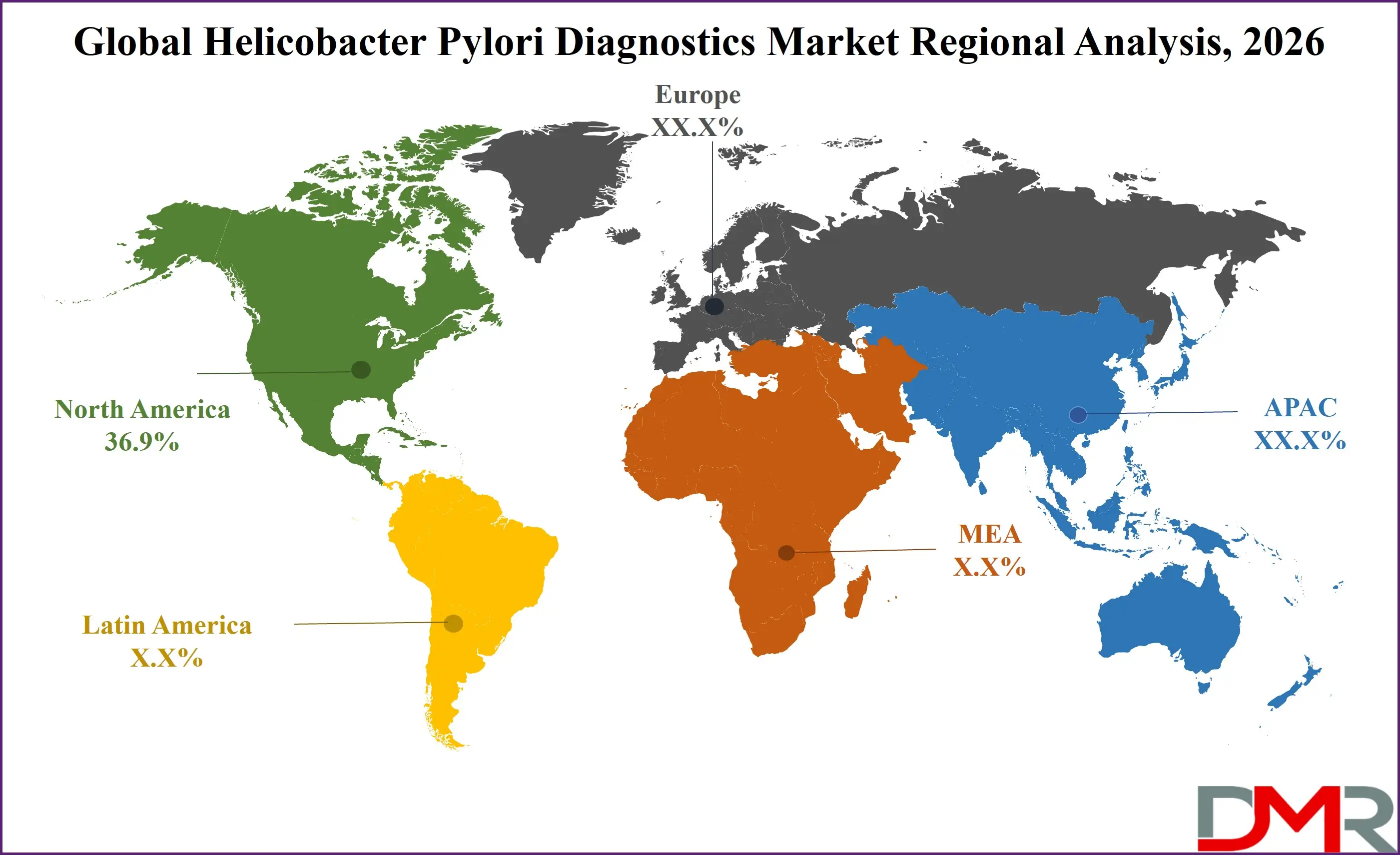

- Regional Insight: North America is expected to hold a 36.9% share of revenue in the global Helicobacter Pylori Diagnostics market in 2026.

- Use Cases: Some of the use cases of Helicobacter Pylori Diagnostics include primary diagnostics, point of care testing, and more.

Helicobacter Pylori Diagnostics Market: Use Cases

- Primary Diagnosis: Detection of active infection in symptomatic patients using breath, stool, or biopsy-based tests for accurate clinical decision-making.

- Post-Treatment Monitoring: Test-of-cure verification to confirm eradication after antibiotic therapy and prevent recurrence.

- Gastric Cancer Risk Screening: Early identification in high-risk populations to reduce long-term malignancy incidence.

- Antibiotic Resistance Detection: Molecular assays identifying clarithromycin and other resistance mutations to guide targeted therapy.

- Epidemiological Surveillance: Monitoring infection prevalence trends for public health planning.

- Point-of-Care Testing: Rapid diagnosis in outpatient and remote settings for immediate treatment decisions.

- Clinical Research Applications: Supporting trials focused on novel eradication regimens and vaccine development.

Stats & Facts

- World Health Organization reported in 2024 that over 50% of the global population is infected with H. pylori.

- Centers for Disease Control and Prevention stated in 2024 that approximately 30–40% of the US population carries H. pylori.

- National Cancer Institute noted in 2025 that H. pylori infection is the strongest known risk factor for non-cardia gastric cancer.

- European Centre for Disease Prevention and Control reported in 2024 that antimicrobial resistance rates in H. pylori exceed 15% for clarithromycin in several EU states.

- Ministry of Health, Labour and Welfare (Japan) confirmed in 2025 continued national insurance coverage for H. pylori eradication therapy.

- Organisation for Economic Co-operation and Development indicated in 2024 that preventive screening expenditure in member countries rose by over 6% year-on-year.

- World Bank highlighted in 2025 that healthcare spending accounts for more than 10% of GDP in high-income economies.

- National Institutes of Health reported in 2024 expanded funding for gastrointestinal infection research.

- Eurostat recorded in 2024 that cancer screening participation rates increased in multiple EU nations.

- Global Antimicrobial Resistance Surveillance System (WHO) emphasized in 2025 that rising resistance trends require improved diagnostic stewardship.

Market Dynamic

Driving Factors in the Helicobacter Pylori Diagnostics Market

Rising Global Burden of Gastric Disorders

The increasing incidence of peptic ulcers, chronic gastritis, and gastric malignancies is a primary force accelerating demand for accurate diagnostic solutions. H. pylori remains a major etiological factor behind non-cardia gastric cancer, prompting health systems to prioritize early detection and eradication. Expanding screening programs, especially in high-risk populations, are encouraging routine testing. Furthermore, aging populations in developed countries and improving healthcare access in emerging economies are contributing to higher diagnostic volumes. Growing clinical emphasis on test-of-cure confirmation to prevent recurrence and complications further reinforces consistent utilization across healthcare settings.

Technological Advancements in Molecular and Non-Invasive Testing

Continuous innovation in PCR-based assays, real-time molecular platforms, and high-sensitivity immunoassays is reshaping the diagnostic landscape. Enhanced accuracy, faster turnaround times, and improved detection of antibiotic resistance mutations are strengthening clinician confidence. Automation in laboratories is reducing manual errors and improving throughput efficiency. Non-invasive methods such as urea breath and stool antigen tests are gaining preference due to patient comfort and convenience. These technological improvements lower repeat testing rates and optimize treatment pathways, directly influencing adoption patterns and overall market momentum.

Restraints in the Helicobacter Pylori Diagnostics Market

High Cost of Advanced Molecular Diagnostics

While molecular tests provide superior sensitivity and resistance profiling, their higher costs compared to conventional serology or stool antigen methods limit widespread adoption in low- and middle-income countries. Capital investment in PCR instruments, skilled personnel training, and quality assurance systems increases operational expenditure for laboratories. Reimbursement disparities across regions further restrict access. Smaller healthcare facilities may rely on traditional methods due to financial constraints, slowing penetration of advanced solutions and creating uneven adoption rates globally.

Variability in Clinical Guidelines and Testing Practices

Differences in national screening recommendations and treatment protocols create inconsistencies in testing frequency and method selection. In some regions, empirical treatment without confirmatory diagnostics remains common, reducing test utilization. Limited awareness among patients and primary care providers about test-of-cure importance also impacts repeat testing rates. Additionally, false positives or negatives associated with certain test types can affect clinical trust, necessitating confirmatory testing and complicating decision-making processes.

Opportunities in the Helicobacter Pylori Diagnostics Market

Expansion in Emerging Economies

Rapid healthcare infrastructure development in Asia-Pacific, Latin America, and parts of the Middle East presents substantial untapped potential. Increasing government healthcare spending and expanding insurance coverage are improving diagnostic accessibility. Rising urbanization and awareness campaigns about gastrointestinal health further stimulate demand. Local manufacturing partnerships and cost-effective rapid test kits can accelerate market penetration. These regions also exhibit high infection prevalence, creating sustained long-term demand for scalable and affordable diagnostic platforms.

Integration of Resistance Profiling and Personalized Medicine

Growing antimicrobial resistance challenges are driving the need for tailored eradication therapies. Molecular assays capable of detecting specific resistance mutations offer a significant growth avenue. Personalized treatment strategies improve eradication success rates and reduce recurrence, strengthening clinical outcomes. Integration of resistance diagnostics with digital health systems and electronic reporting platforms enhances surveillance and stewardship programs, opening opportunities for premium diagnostic offerings.

Trends in the Helicobacter Pylori Diagnostics Market

Shift Toward Non-Invasive and Point-of-Care Solutions

Healthcare providers are increasingly favoring patient-friendly diagnostic approaches that minimize discomfort and reduce procedural risks. Urea breath tests and stool antigen tests are witnessing higher demand compared to biopsy-based techniques in routine cases. Portable and rapid point-of-care kits enable immediate results in outpatient clinics and rural settings. This shift supports decentralized healthcare delivery models and improves early intervention rates.

Digitalization and Laboratory Automation

Advanced laboratory information systems, automated sample processing, and integrated reporting platforms are enhancing workflow efficiency. Digital connectivity enables real-time result sharing between laboratories and physicians, supporting faster treatment decisions. Automation reduces human error and improves reproducibility. The incorporation of multiplex molecular panels capable of detecting multiple gastrointestinal pathogens alongside H. pylori is also gaining momentum, expanding diagnostic value propositions.

Impact of Artificial Intelligence in Helicobacter Pylori Diagnostics Market

- AI-Assisted Image Analysis: AI algorithms enhance histology slide interpretation accuracy by identifying bacterial presence with higher precision.

- Predictive Treatment Modeling: Machine learning models forecast antibiotic resistance patterns to support personalized therapy decisions.

- Workflow Optimization: AI-driven laboratory management systems streamline sample tracking and reduce turnaround times.

- Quality Control Automation: Intelligent systems detect anomalies in test results, minimizing false positives and negatives.

- Clinical Decision Support: AI tools integrate patient history and diagnostic data to recommend appropriate test pathways.

- Epidemiological Surveillance: AI analyzes population-level data to predict infection trends and resistance hotspots.

- Resource Allocation: Healthcare providers use AI analytics to optimize testing resource distribution in high-prevalence regions.

- Point-of-Care Enhancement: AI-enabled portable devices improve rapid result interpretation in decentralized settings.

Research Scope and Analysis

By Test Type Analysis

Non-Invasive Diagnostics is projected to hold 62.4% market share in 2026, making it the dominant segment. The growing preference for patient-friendly, cost-effective, and repeatable testing methods drives its leadership. Urea breath tests and stool antigen tests offer high sensitivity and specificity without requiring endoscopy, increasing patient compliance. The segment benefits from rising outpatient testing, expanding screening initiatives, and demand for post-treatment monitoring. Technological advancements in breath analyzers and immunoassays further strengthen performance reliability. Additionally, reimbursement support in developed regions encourages adoption, positioning non-invasive methods as the standard first-line diagnostic approach.

Invasive Diagnostics represents a critical but comparatively smaller segment, primarily utilized in complex or high-risk cases requiring endoscopic evaluation. Rapid urease tests, histology, and culture remain essential for definitive diagnosis and antimicrobial susceptibility assessment. Although growth is slower than non-invasive methods, demand persists in tertiary care centers where biopsy-based confirmation is clinically necessary. Increasing integration of molecular techniques with biopsy samples enhances diagnostic precision and supports targeted treatment strategies.

By Technology Analysis

Immunoassays are projected to account for 48.7% of the market share in 2026, maintaining leadership due to their widespread adoption, affordability, and ease of implementation across laboratories and point-of-care settings. ELISA and lateral flow assays are extensively used for stool antigen and serological testing, offering reliable sensitivity and rapid turnaround times. Their compatibility with automated platforms and minimal infrastructure requirements make them suitable for both developed and emerging markets. Continuous improvements in antibody specificity and kit stability further enhance diagnostic accuracy. Strong demand from outpatient clinics and decentralized healthcare facilities reinforces this segment’s dominance in routine screening and follow-up testing applications.

Molecular Diagnostics is the fastest-growing technology segment, driven by increasing demand for high-precision detection and antibiotic resistance profiling. PCR and real-time PCR platforms enable direct identification of bacterial DNA and mutation analysis, supporting personalized eradication therapies. Although relatively cost-intensive, their clinical value in resistance surveillance and treatment optimization is expanding adoption in tertiary care centers. Ongoing advancements in isothermal amplification and compact molecular systems are improving accessibility and reducing operational complexity.

By End User Analysis

Hospitals & Clinics are expected to hold 54.2% market share in 2026, leading due to high patient inflow, access to advanced diagnostic infrastructure, and routine integration of H. pylori testing within gastroenterology departments. Endoscopy-based diagnostics and confirmatory molecular testing are predominantly performed in hospital settings. The availability of skilled professionals and reimbursement support strengthens segment growth. Increasing emphasis on early gastric cancer detection and structured eradication programs further contributes to sustained testing volumes within these facilities.

Diagnostic Laboratories represent the fastest-growing segment, fueled by outsourcing trends and rising demand for specialized testing services. Reference laboratories equipped with automated immunoassay and molecular platforms provide cost efficiencies and high-throughput capabilities. Expansion of centralized laboratory networks and improved logistics systems are accelerating sample processing efficiency. Growing collaborations with hospitals and clinics enhance test accessibility and broaden market penetration.

By Application Analysis

Primary Diagnosis is anticipated to command 63.5% of the market share in 2026, as initial detection remains the fundamental step in infection management. Increasing awareness of gastrointestinal disorders and expanding screening programs are driving high test volumes. Non-invasive methods such as urea breath and stool antigen tests are widely utilized for first-line detection. Early identification helps prevent complications including ulcers and malignancies, reinforcing demand. Integration with routine health check-ups and preventive care initiatives supports continued segment dominance.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Post-Treatment Monitoring is the fastest-growing application segment, supported by rising antimicrobial resistance and updated clinical guidelines recommending confirmation of eradication. Physicians increasingly rely on non-invasive tests to verify therapeutic success. Improved compliance with follow-up testing enhances repeat diagnostic demand. Growing awareness of recurrence risks and treatment failures strengthens adoption across both developed and emerging healthcare systems.

The Helicobacter Pylori Diagnostics Market Report is segmented on the basis of the following

By Test Type

- Invasive Diagnostics

- Rapid Urease Test (RUT)

- Histology

- Culture

- Non-Invasive Diagnostics

- Urea Breath Tests (UBT)

- Stool Antigen Tests

- Serological Tests

- Molecular Tests (PCR-based)

By Technology

- Immunoassays

- ELISA

- Lateral Flow Assays

- Molecular Diagnostics

- PCR & Real-Time PCR

- Isothermal Amplification

- Breath Test Technology

By End User

- Hospitals & Clinics

- Diagnostic Laboratories

- Point-of-Care Settings

By Application

- Primary Diagnosis

- Post-Treatment Monitoring (Test-of-Cure)

Regional Analysis

Leading Region in the Helicobacter Pylori Diagnostics Market

North America is projected to account for 36.9% of the global market share in 2026, maintaining its leading position. Strong healthcare infrastructure, advanced diagnostic technologies, and favorable reimbursement policies contribute to sustained growth. High awareness levels regarding gastric cancer prevention and routine screening practices increase testing volumes. Presence of established diagnostic manufacturers and continuous R&D investment further strengthen regional dominance. Supportive regulatory frameworks and emphasis on antimicrobial resistance monitoring enhance adoption of molecular diagnostics and non-invasive testing solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest Growing Region in the Helicobacter Pylori Diagnostics Market

Asia-Pacific is emerging as the fastest-growing region, driven by high infection prevalence and expanding healthcare infrastructure. Countries such as China and India are witnessing rising healthcare spending and growing awareness of early diagnosis. Government-led screening initiatives and urbanization trends are boosting demand for both non-invasive and molecular tests. Increasing private sector investment and local manufacturing capabilities are enhancing affordability. The region’s large population base and improving insurance coverage position it for accelerated long-term growth.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive landscape of the Helicobacter Pylori Diagnostics Market is driven by continuous innovation, product portfolio expansion, and strategic collaborations aimed at strengthening market positioning. Companies focus on improving diagnostic accuracy, enhancing test sensitivity and specificity, reducing turnaround times, and integrating automation to differentiate their offerings. Significant investments are directed toward molecular resistance detection technologies and advanced point-of-care solutions to address growing clinical demand. High regulatory compliance requirements, strict quality standards, and capital-intensive manufacturing processes act as major entry barriers. To expand geographic reach and distribution capabilities, firms actively collaborate with hospitals, diagnostic laboratories, and healthcare networks. Ongoing research and development initiatives, along with targeted expansion into emerging economies with high infection prevalence, remain central strategies for sustaining long-term competitive advantage and market growth.

Some of the prominent players in the global Helicobacter Pylori Diagnostics are

- Thermo Fisher Scientific

- Abbott Laboratories

- F. Hoffmann-La Roche

- Bio-Rad Laboratories

- Meridian Bioscience

- bioMérieux

- Cardinal Health

- Quidel Corporation

- Sekisui Diagnostics

- DiaSorin S.p.A.

- EKF Diagnostics

- Halyard Health

- Agilent Technologies

- Medline Industries

- Coris BioConcept

- Certest Biotec

- Alere Inc.

- MP Biomedicals

- Biomerica

- Mobidiag

- Other Key Players

Recent Developments

- In January 2026, AIG Hospitals has launched PYtest, a non-invasive diagnostic tool designed to detect active Helicobacter pylori infections. Developed by Nobel Laureate Barry Marshall, the test will be offered at the hospital’s Gachibowli and Banjara Hills locations. Helicobacter pylori is one of the most widespread bacterial infections in India, linked to chronic gastritis, peptic ulcers, gastric cancer, and MALT lymphoma. Traditionally, diagnosis has relied on invasive endoscopic methods, frequently leading to delayed or overlooked detection.

- In August 2025, Biomerica, Inc. announced that the United Arab Emirates Ministry of Health and Prevention has authorized its Fortel® Ulcer Test for at-home use, broadening access to convenient diagnostic solutions in the region. The 10-minute rapid test identifies antibodies to Helicobacter pylori, a bacterium linked to peptic ulcers, indigestion, and many gastric cancer cases. With this approval, consumers across the UAE can now perform the test privately and conveniently without visiting a healthcare facility.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 774.5 Mn |

| Forecast Value (2035) |

USD 1,444.0 Mn |

| CAGR (2026–2035) |

7.2% |

| The US Market Size (2026) |

USD 250.0 Mn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors, etc. |

| Segments Covered |

By Test Type (Invasive Diagnostics, Non-Invasive Diagnostics), By Technology (Immunoassays, Molecular Diagnostics, Breath Test Technology), By End User (Hospitals & Clinics, Diagnostic Laboratories, Point-of-Care Settings), By Application (Primary Diagnosis, Post-Treatment Monitoring (Test-of-Cure)) |

| Regional Coverage |

North America – US, Canada; Europe – Germany, UK, France, Russia, Spain, Italy, Benelux, Nordic, Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, Rest of MEA |

| Prominent Players |

Thermo Fisher Scientific, Abbott Laboratories, F. Hoffmann-La Roche, Bio-Rad Laboratories, Meridian Bioscience, bioMérieux, Cardinal Health, Quidel Corporation, Sekisui Diagnostics, DiaSorin S.p.A., EKF Diagnostics, Halyard Health, Agilent Technologies, Medline Industries, Coris BioConcept, Certest Biotec, Alere Inc., MP Biomedicals, Biomerica, Mobidiag, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days, and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Helicobacter Pylori Diagnostics Market?

▾ The Global Helicobacter Pylori Diagnostics Market size is expected to reach USD 774.5 million by 2026 and is projected to reach USD 1,444.0 million by the end of 2035

Which region accounted for the largest Global Helicobacter Pylori Diagnostics Market?

▾ North America is expected to have the largest market share in the Global Helicobacter Pylori Diagnostics Market, with a share of about 36.9% in 2026.

How big is the Helicobacter Pylori Diagnostics Market in the US?

▾ The US Helicobacter Pylori Diagnostics market is expected to reach USD 250.0 million by 2026.

The US Helicobacter Pylori Diagnostics market is expected to reach USD 250.0 million by 2026.

▾ Some of the major key players in the Global Helicobacter Pylori Diagnostics Market include Roche, Thermofisher, abbott and others

What is the growth rate in the Global Helicobacter Pylori Diagnostics Market?

▾ The market is growing at a CAGR of 7.2 percent over the forecasted period.