Market Overview

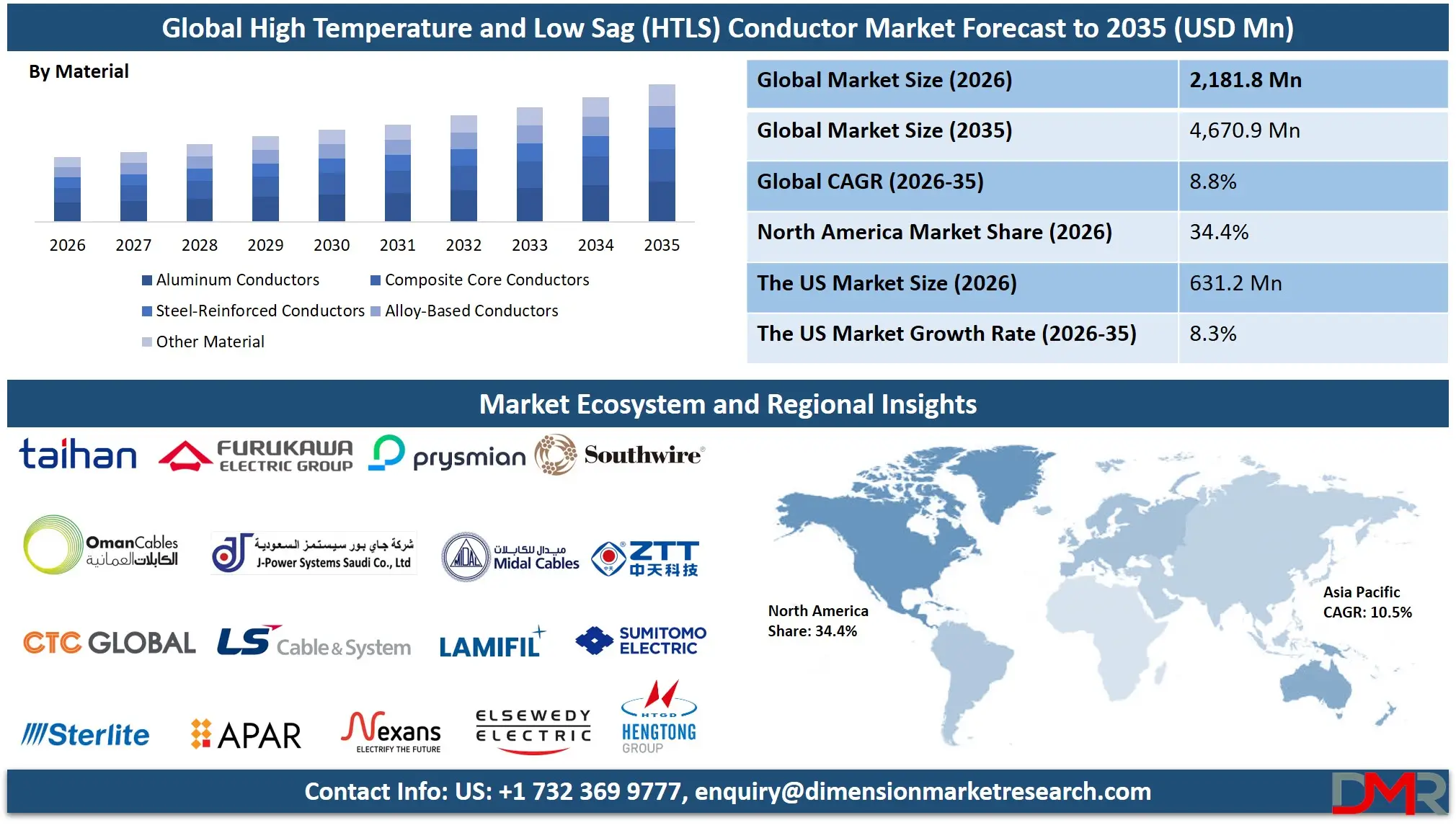

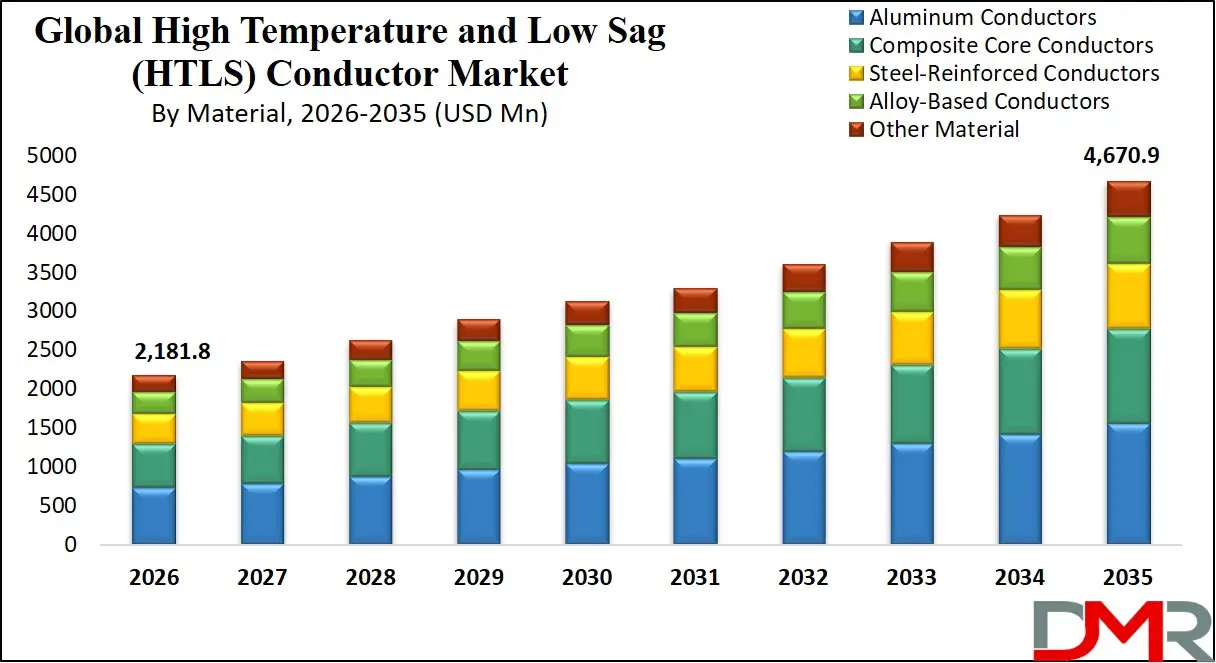

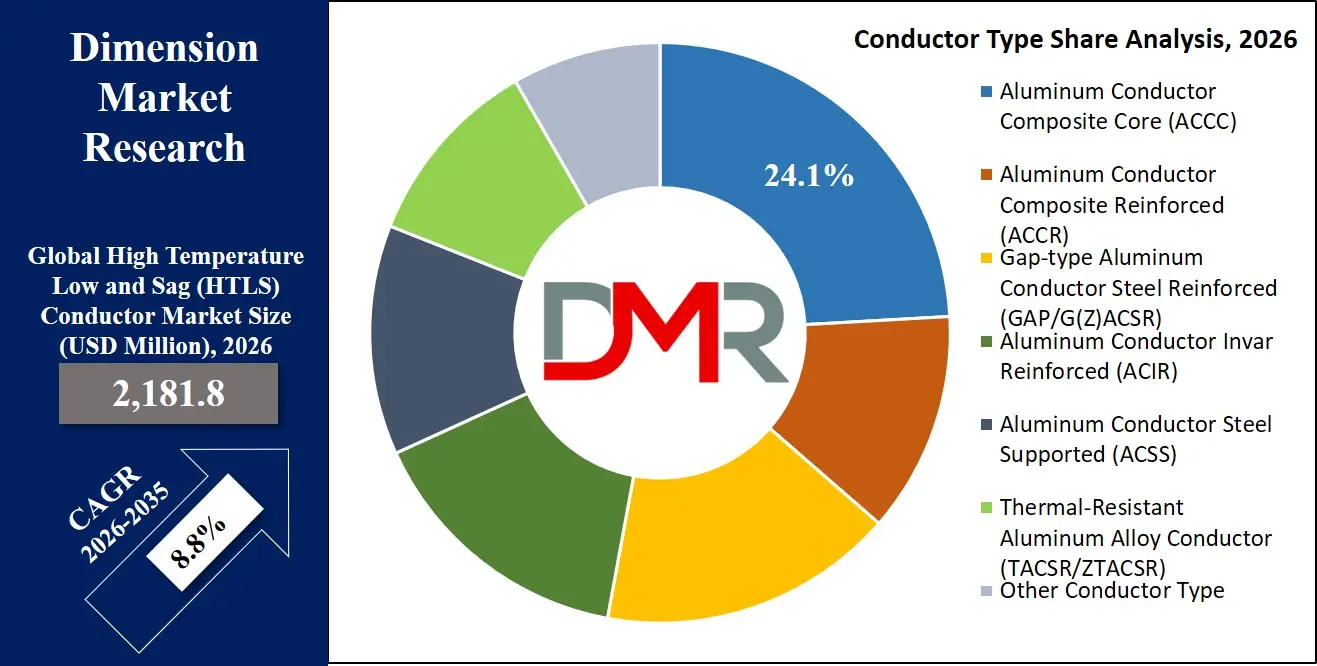

The Global High Temperature and Low Sag (HTLS) Conductor Market is set for substantial expansion, reaching an estimated USD 2,181.8 million in 2026 and projected to grow at a strong CAGR of 8.8% from 2026 to 2035, to a market value of USD 4,670.9 million by 2035. This robust growth trajectory is fueled by the accelerating need for grid modernization, renewable energy integration, and the replacement of aging transmission infrastructure with high-capacity, efficient conductors.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Rising global electricity demand, coupled with the urgent need to upgrade existing transmission corridors without acquiring new rights-of-way, is compelling utilities and grid operators to implement advanced HTLS conductors. These conductors offer significantly higher current-carrying capacity (ampacity) than conventional conductors while operating at lower sag levels, making them ideal for reconductoring projects.

Additionally, stringent government regulations and investments aimed at enhancing grid reliability and integrating large-scale renewable energy sources (wind and solar) into the transmission network are further accelerating market adoption. Utilities are increasingly deploying Aluminum Conductor Composite Supported (ACCS), Aluminum Conductor Composite Reinforced (ACCR), and Gap-type conductors to overcome transmission bottlenecks and improve grid efficiency.

The development of advanced composite core materials, corrosion-resistant designs, and innovative manufacturing processes is enabling the production of more durable and efficient HTLS conductors. As global energy policies prioritize decarbonization and the expansion of smart grid infrastructures, the HTLS Conductor Market is expected to witness sustained growth through 2035, driven by the need for reliable, high-capacity power transfer.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Growing government initiatives promoting cross-border interconnections and offshore wind farm connections further accelerate global adoption. However, barriers such as high initial material costs, complex installation requirements compared to conventional conductors, and technical challenges related to connector compatibility and thermal expansion remain. Despite these limitations, the convergence of material science, advanced manufacturing, and utility-scale project financing positions HTLS conductors as a central pillar of global energy infrastructure development through 2035.

The US High Temperature and Low Sag (HTLS) Conductor Market

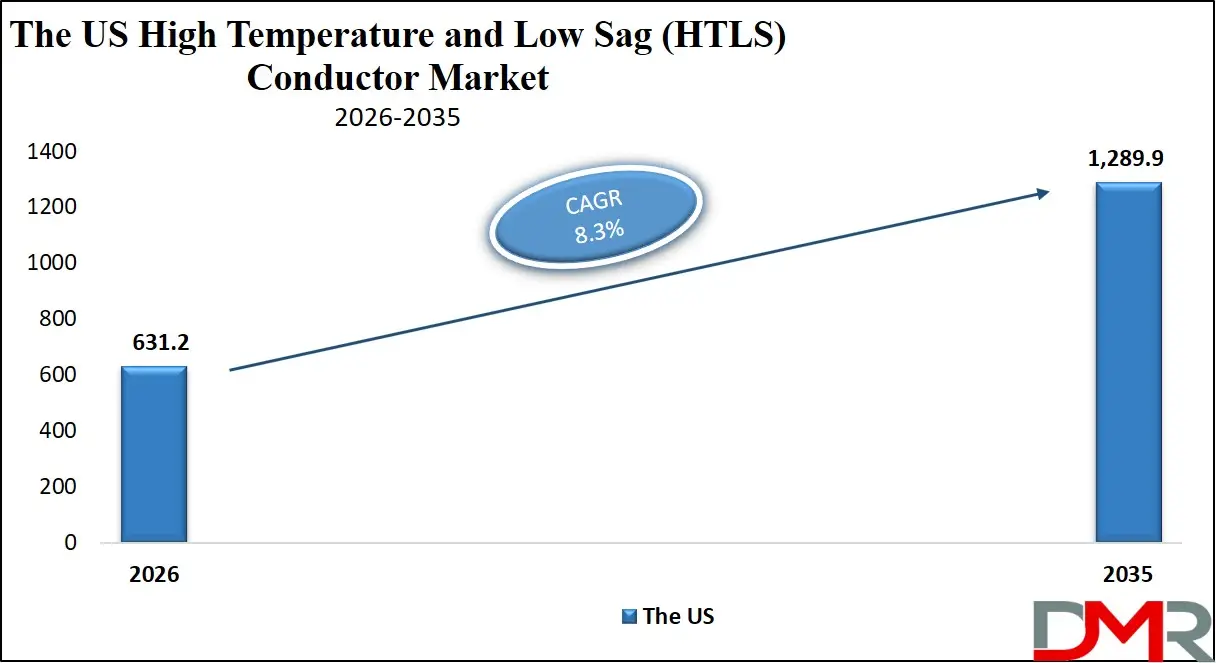

The U.S. High Temperature and Low Sag (HTLS) Conductor Market is projected to reach USD 631.2 million in 2026 and grow at a CAGR of 8.3%, reaching USD 1,289.9 million by 2035. The U.S. leads global adoption due to its aging transmission infrastructure, the rapid growth of renewable energy zones, and strong regulatory support from the Federal Energy Regulatory Commission (FERC) and the Department of Energy (DOE).

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The need to relieve congestion on existing transmission lines and connect remote solar and wind farms to population centers fuels demand for high-capacity conductors. Major investor-owned utilities, transmission developers, and regional grid operators such as PJM, MISO, and CAISO are increasingly specifying HTLS solutions for reconductoring projects to maximize existing tower footprints.

U.S. policy support through the Infrastructure Investment and Jobs Act, which allocates billions for grid resilience and expansion, encourages investment in advanced grid technologies. The market is witnessing a shift toward composite core conductors that offer higher strength-to-weight ratios and reduced line losses, enhancing overall grid efficiency. The rise in extreme weather events has further intensified the focus on grid hardening, positioning the U.S. as a critical innovator in this space.

The Europe High Temperature and Low Sag (HTLS) Conductor Market

The Europe High Temperature and Low Sag (HTLS) Conductor Market is projected to be valued at approximately USD 414.5 million in 2026 and is projected to reach around USD 777.6 million by 2035, growing at a CAGR of about 7.2% from 2026 to 2035. Europe's growth is anchored by its ambitious renewable energy targets (REPowerEU), the need to interconnect national grids, and strict environmental regulations that limit the acquisition of new transmission corridors.

Countries such as Germany, the U.K., France, and Spain are widely adopting HTLS conductors, driven by the need to integrate offshore wind energy and manage increasing cross-border power flows. The European Network of Transmission System Operators for Electricity (ENTSO-E) emphasizes grid upgrades to facilitate the energy transition, further necessitating advanced conductor technologies.

Europe's focus on reducing carbon emissions and improving grid resilience drives the demand for efficient, high-capacity reconductoring solutions. Funding and support for trans-European energy networks (TEN-E) encourage cross-border collaboration and the standardization of grid technologies. With a sophisticated utility sector and a regulatory landscape that prioritizes renewable integration, Europe remains a highly advanced and essential region for HTLS conductor deployment.

The Japan High Temperature and Low Sag (HTLS) Conductor Market

The Japan High Temperature and Low Sag (HTLS) Conductor Market is anticipated to be valued at approximately USD 122.2 million in 2026 and is expected to attain nearly USD 221.7 million by 2035, expanding at a CAGR of about 6.8% during the forecast period. Japan's focus on grid resilience following natural disasters (typhoons, earthquakes) and its strategy to restart and optimize its power generation mix are driving the adoption of robust, high-capacity transmission technologies.

The Ministry of Economy, Trade and Industry (METI) actively supports the development of a more resilient and flexible national grid, promoting the use of advanced conductors to reinforce existing lines. Japan's leadership in material science and high manufacturing standards provides a robust foundation for deploying high-performance conductors like ACCC and gap-type conductors.

Japan's energy policy, balancing energy security and decarbonization, drives the need to efficiently transmit power from regional generation sources to major consumption centers like Tokyo and Osaka. Companies are deploying HTLS conductors to upgrade aging lines constructed decades ago, ensuring the integrity and capacity of the grid. Japan's cultural emphasis on quality and reliability positions it as a high-growth, quality-focused market for HTLS solutions.

Global High Temperature and Low Sag (HTLS) Conductor Market: Key Takeaways

- Strong Global Market Growth Outlook: The Global High Temperature and Low Sag (HTLS) Conductor Market is expected to be valued at USD 2,181.8 million in 2026 and is projected to reach USD 4,670.9 million by 2035, showcasing rapid expansion supported by global grid modernization and renewable integration.

- Steady CAGR Driven by Grid Modernization: The market is expected to grow at a CAGR of 8.8% from 2026 to 2035, fueled by accelerating investments in transmission infrastructure, the need for grid efficiency, and the replacement of aging assets.

- Strong Growth Trajectory in the United States: The U.S. HTLS Conductor Market stands at USD 631.2 million in 2026 and is projected to reach USD 1,289.9 million by 2035, expanding at a CAGR of 8.3% due to significant grid congestion and large-scale renewable energy targets.

- Regional Dominance: North America is expected to capture approximately 34.4% of the global market share in 2026, supported by substantial utility investments, a mature energy sector, and proactive government funding for grid resilience.

- Rapid Advancement in Conductor Technologies: Innovations including advanced composite core materials (carbon fiber, ceramic), gap-type conductor designs, and corrosion-resistant aluminum alloys are significantly enhancing ampacity, reducing thermal sag, and improving the longevity of transmission lines.

- Renewable Energy Integration Boosts Adoption: The global push to connect utility-scale solar and wind farms to the grid, coupled with the need to resolve transmission bottlenecks without lengthy permitting for new lines, is driving sustained demand for high-performance HTLS reconductoring solutions.

Global High Temperature and Low Sag (HTLS) Conductor Market: Use Cases

- Reconductoring Aging Transmission Lines: Utilities replace old ACSR conductors with HTLS on existing towers to double or triple line capacity without structural modifications, solving rights-of-way constraints.

- Renewable Energy Integration: Connecting remote wind and solar farms to the main transmission grid requires high-capacity lines; HTLS conductors efficiently handle the variable and high power output from these sources.

- Urban Grid Reinforcement: In densely populated cities where building new towers is impossible, utilities use HTLS conductors to upgrade underground and overhead feeders to meet growing urban electricity demand.

- Cross-Border Interconnections: International power exchange projects use HTLS conductors to maximize power transfer capacity within limited corridor widths, enhancing energy trading and grid stability.

- Industrial Power Supply: Large industrial complexes (mining, smelting) with high and constant power demands utilize dedicated HTLS lines to ensure reliable and sufficient electricity supply for their operations.

Global High Temperature and Low Sag (HTLS) Conductor Market: Stats & Facts

Central Electricity Authority (CEA), Government of India

- HTLS conductors can operate at continuous temperatures of up to 250°C, significantly higher than conventional transmission conductors.

- Conventional ACSR conductors typically operate at around 85°C, while AAAC conductors operate at around 95°C.

- HTLS conductors are capable of doubling the current carrying capacity of existing transmission lines.

- Conductors account for approximately 30–40% of the total cost of overhead extra-high-voltage transmission lines.

- The indicative minimum conductor diameter for 400 kV HTLS conductors is around 28.62 mm.

- The indicative minimum conductor diameter for 220 kV HTLS conductors is around 25 mm.

- Maximum DC resistance for a 400 kV HTLS conductor is approximately 0.05552 ohm/km at 20°C.

- Maximum DC resistance for a 220 kV HTLS conductor is approximately 0.06868 ohm/km at 20°C.

North Eastern Regional Power Committee (NERPC), Government of India

- HTLS conductors typically operate within a temperature range of 150°C to 250°C.

- Reconductoring with HTLS conductors can increase transmission capacity of existing corridors by up to two times.

- HTLS technology allows reuse of existing towers and transmission infrastructure, reducing the need for new construction.

- Advanced conductors such as HTLS provide significantly higher current carrying capacity per cross-section area compared with conventional conductors.

International Energy Agency (IEA)

- Approximately 1,500 GW of global solar and wind projects are waiting for grid connections, increasing the need for higher-capacity transmission technologies.

- Global electricity demand increased by about 2.2% in 2023, creating additional pressure on transmission infrastructure.

- Electricity consumption worldwide is expected to grow by nearly 3% annually through the mid-2020s, increasing demand for grid expansion technologies.

- Global renewable electricity generation accounted for around 30% of total power generation in 2023.

GridLab (Energy Systems Research Organization)

- More than 90,000 miles of advanced conductors, including HTLS, have been deployed globally.

- Reconductoring with advanced conductors can increase line capacity by up to 100% without building new transmission corridors.

- Upgrading existing lines using advanced conductors can cost less than 50% of building new transmission infrastructure.

- Reconductoring projects using advanced conductors can reduce project completion time by more than 50% compared with new line construction.

IEEE (Institute of Electrical and Electronics Engineers)

- Advanced conductors such as ACCR and ACCC can deliver up to twice the ampacity of conventional ACSR conductors.

- ACSS conductors can provide approximately 1.6 times the current carrying capacity of traditional ACSR conductors.

- Some HTLS conductor designs are capable of operating continuously at temperatures of around 210°C.

- HTLS conductors demonstrate significantly lower thermal expansion compared with traditional aluminum-steel conductors.

Power Grid Corporation of India Limited (PGCIL)

- India has deployed more than 5,000 km of HTLS conductors across its transmission network.

- Orders have been placed for over 12,000 km of HTLS transmission lines in India.

- Around 4,600 km of HTLS installations in India utilize Invar-reinforced conductors.

- Approximately 4,000 km of HTLS installations use ACCC technology.

- Nearly 3,300 km of HTLS lines use GAP-type conductors.

- About 500 km of HTLS conductors installed in India use ACSS technology.

Electric Power Research Institute (EPRI)

- Advanced conductors can increase ampacity by up to 2.5 times compared with conventional conductors.

- HTLS conductors can significantly reduce sag under high temperature conditions, improving safety clearances.

- Reconductoring with advanced conductors can increase transmission efficiency while maintaining existing tower structures.

Global High Temperature and Low Sag (HTLS) Conductor Market: Market Dynamic

Driving Factors in the Global High Temperature and Low Sag (HTLS) Conductor Market

Aging Grid Infrastructure and Capacity Expansion Needs

A significant portion of the global transmission grid was built over 40-50 years ago and is struggling to meet modern electricity demand. HTLS conductors offer a cost-effective solution by allowing utilities to upgrade line capacity without the lengthy and expensive process of acquiring new rights-of-way or building new towers. This "reconductoring" approach is essential for relieving grid congestion and preventing blackouts in rapidly growing urban and industrial centers.

Integration of Renewable Energy Sources

The global energy transition hinges on connecting large-scale, often remote, renewable generation (solar, wind) to population centers. Conventional lines frequently lack the capacity to handle this new power influx. HTLS conductors, with their superior ampacity, are critical for unlocking renewable energy zones, reducing curtailment, and ensuring that clean energy reaches the grid efficiently, directly supporting national decarbonization goals.

Restraints in the Global High Temperature and Low Sag (HTLS) Conductor Market

High Initial Material and Installation Costs

HTLS conductors are significantly more expensive than conventional ACSR conductors due to advanced materials like carbon fiber and specialized metal matrices. This higher upfront capital expenditure can be a deterrent for cash-constrained utilities, especially when weighed against the long-term operational savings. Furthermore, specialized installation techniques and fittings require trained labor and specific hardware, adding to the initial project complexity and cost.

Technical Challenges and Standardization Gaps

The long-term performance of some composite core materials under varying environmental and load conditions is still being studied. Issues such as core-seating in fittings, galvanic corrosion between dissimilar materials, and higher thermal expansion rates of the aluminum strands relative to the core require meticulous engineering. The lack of universal standards for testing and installation across different HTLS technologies can also create uncertainty for utilities.

Opportunities in the Global High Temperature and Low Sag (HTLS) Conductor Market

Expansion into Emerging Markets with High Demand Growth

Emerging markets in Asia-Pacific, Africa, and Latin America are experiencing rapid urbanization and industrial growth, leading to soaring electricity demand. Countries like India, Vietnam, Nigeria, and Brazil are investing heavily in expanding and upgrading their transmission backbones. These regions often face the challenge of quickly building capacity, making the high-capacity, same-tower solution offered by HTLS conductors an extremely attractive proposition for both greenfield and brownfield projects.

Development of Hybrid and Advanced Core Materials

Ongoing research into new, lower-cost composite materials and hybrid designs (e.g., combining carbon and glass fibers) promises to reduce the cost premium of HTLS conductors. Innovations aimed at improving resistance to high-temperature creep, enhancing corrosion resistance, and developing all-aluminum alloy high-temperature conductors present significant opportunities for market expansion by making the technology accessible to a wider range of applications.

Trends in the Global High Temperature and Low Sag (HTLS) Conductor Market

Dominance of Composite Core Conductors

Conductors utilizing carbon fiber and hybrid composite cores, such as ACCC and ACCR, are gaining the largest market share due to their exceptional strength-to-weight ratio, near-zero thermal sag, and high ampacity. The trend is shifting from traditional steel-reinforced solutions to these advanced composite cores for critical backbone transmission projects.

Focus on Grid Hardening and Resilience

With the increasing frequency of extreme weather events (wildfires, hurricanes, ice storms), grid operators are prioritizing resilience. HTLS conductors, often designed to operate at higher temperatures with less sag, also offer greater strength and durability against mechanical stresses, making them a preferred choice for hardening critical transmission corridors against climate risks.

Global High Temperature and Low Sag (HTLS) Conductor Market: Research Scope and Analysis

By Conductor Type Analysis

The Aluminum Conductor Composite Core (ACCC) segment is projected to dominate the conductor type category within the High Temperature and Low Sag (HTLS) Conductor market. ACCC conductors utilize a lightweight carbon and glass fiber composite core surrounded by trapezoidal aluminum strands. This design provides significantly higher conductivity and mechanical strength compared to traditional steel-reinforced conductors. One of the main reasons for the dominance of ACCC conductors is their ability to operate at high temperatures while maintaining minimal sag, which allows transmission utilities to increase the power carrying capacity of existing lines without replacing towers or expanding rights-of-way.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

ACCC conductors are widely used in reconductoring projects where aging transmission infrastructure needs to be upgraded to support increasing electricity demand. The composite core offers high tensile strength and very low thermal expansion, enabling the conductor to maintain safe ground clearance even when operating at elevated temperatures. In addition, ACCC conductors allow utilities to improve grid reliability and reduce transmission losses due to their higher aluminum content and improved conductivity.

Another factor supporting their dominance is their increasing deployment in renewable energy integration projects. As countries expand wind and solar generation capacity, transmission networks require conductors capable of carrying higher loads from remote generation sites to demand centers. ACCC technology is well suited for this purpose because it can increase line capacity by two times or more compared with conventional conductors.

Due to these advantages, ACCC conductors are widely adopted by utilities in regions experiencing rapid grid expansion and modernization, particularly in Asia-Pacific and North America. Their combination of high ampacity, durability, and compatibility with existing transmission infrastructure makes them the leading conductor type in the HTLS conductor market.

By Material Analysis

Aluminum conductors is expected to dominate the material segment of the HTLS conductor market because aluminum remains the most widely used material in overhead power transmission systems worldwide. Aluminum provides an optimal balance of electrical conductivity, weight, corrosion resistance, and cost effectiveness, making it highly suitable for large-scale transmission infrastructure. Even in advanced HTLS conductor technologies, aluminum strands form the outer conducting layer responsible for carrying the majority of the electrical current.

The primary reason for aluminum's dominance is its high conductivity relative to its weight. Aluminum weighs significantly less than copper while still offering strong electrical performance, allowing utilities to construct long-distance overhead lines without placing excessive mechanical stress on transmission towers. This lightweight characteristic is especially important in HTLS conductors, which are designed to carry higher electrical loads at elevated temperatures.

Aluminum also exhibits excellent corrosion resistance in outdoor environments, which is critical for overhead transmission lines exposed to varying weather conditions. This property reduces maintenance requirements and increases the lifespan of transmission infrastructure. In addition, aluminum is widely available globally and can be produced at a relatively lower cost compared to many alternative conductive materials.

Another factor contributing to aluminum's dominance is its compatibility with various HTLS conductor designs, including composite-core, steel-reinforced, and alloy-based conductors. These technologies rely on aluminum strands for current conduction while using advanced core materials to improve mechanical performance and reduce sag.

Because of its superior balance of performance, durability, and affordability, aluminum continues to serve as the primary conductive material in modern HTLS conductor systems. Its widespread adoption across global transmission networks ensures that aluminum-based conductors remain the leading material segment in the HTLS conductor market.

By Voltage Level Analysis

The Extra High Voltage (EHV) segment is expected to dominate the voltage level category of the HTLS conductor market. EHV transmission lines typically operate at voltage levels above 220 kV and are used for transporting large volumes of electricity across long distances between generation facilities and major consumption centers. HTLS conductors are particularly well suited for these networks because they can carry significantly higher current loads while maintaining minimal sag even at elevated temperatures.

The increasing demand for electricity worldwide has led to the expansion of large-scale power generation facilities, including renewable energy projects located far from urban demand centers. As a result, transmission utilities require high-capacity lines capable of delivering bulk electricity efficiently over long distances. HTLS conductors provide the necessary performance improvements to meet this demand without requiring extensive infrastructure replacement.

Another reason for the dominance of the EHV segment is the growing need to upgrade existing high-voltage transmission corridors. Many countries are experiencing rapid growth in electricity consumption, which places pressure on aging transmission networks originally designed for lower power capacities. By replacing conventional conductors with HTLS conductors, utilities can significantly increase the power transfer capacity of EHV lines while utilizing existing towers and rights-of-way.

EHV transmission systems also require conductors with strong mechanical properties and stable thermal performance. HTLS conductors are designed to maintain structural integrity under high thermal loads, reducing the risk of excessive sag that could compromise safety clearances.

Because of their ability to enhance transmission efficiency, increase ampacity, and support long-distance power delivery, HTLS conductors are increasingly deployed in EHV networks worldwide. This widespread application makes the Extra High Voltage segment the dominant category in the HTLS conductor market.

By Application Analysis

Power transmission are poised to represent the dominant application segment in the High Temperature Low Sag conductor market. Transmission networks form the backbone of national electricity systems, carrying power from generation plants to regional substations and distribution networks. As electricity demand continues to grow globally, transmission operators are increasingly adopting HTLS conductors to enhance the capacity and efficiency of existing transmission lines.

HTLS conductors are particularly valuable in transmission applications because they allow utilities to significantly increase the current carrying capacity of overhead lines while maintaining safe ground clearances. Traditional conductors tend to sag when operating at higher temperatures, which limits their maximum load capacity. In contrast, HTLS conductors are specifically engineered to operate at elevated temperatures with minimal sag, enabling transmission operators to move larger volumes of electricity through existing corridors.

Another factor contributing to the dominance of power transmission applications is the growing need for grid modernization. Many countries are upgrading aging transmission infrastructure to improve reliability, reduce energy losses, and accommodate new energy sources. HTLS conductors provide an efficient solution for these upgrades because they can be installed on existing towers without requiring extensive structural modifications.

Transmission networks are also playing a critical role in integrating renewable energy resources such as wind and solar power. These energy sources are often located in remote areas far from demand centers, requiring long-distance high-capacity transmission lines. HTLS conductors enable utilities to handle the fluctuating and high-volume power flows associated with renewable generation.

Due to their ability to enhance transmission efficiency, increase line capacity, and support large-scale energy integration, HTLS conductors are most extensively used in power transmission systems, making this application segment the dominant category in the global market.

By End-Use Industry Analysis

Electric utilities are expected to dominate the end-use industry segment in the High Temperature Low Sag conductor market. Electric utilities are responsible for generating, transmitting, and distributing electricity to residential, commercial, and industrial consumers. As electricity demand continues to increase due to population growth, urbanization, and industrial expansion, utilities are under pressure to expand the capacity and reliability of their power transmission networks.

HTLS conductors offer utilities an efficient and cost-effective solution for upgrading existing infrastructure. Instead of constructing entirely new transmission lines which can be expensive, time-consuming, and subject to regulatory restrictions utilities can replace conventional conductors with HTLS conductors to increase power transfer capacity within existing corridors. This approach significantly reduces project costs, construction time, and environmental impact.

Another factor driving utility dominance is the global transition toward renewable energy. Governments and energy regulators are encouraging utilities to integrate large-scale renewable power generation into national grids. Renewable energy facilities, particularly wind and solar farms, are often located in remote regions far from population centers. HTLS conductors enable utilities to transmit large amounts of electricity from these locations efficiently while maintaining stable grid operations.

Electric utilities also prioritize technologies that improve operational reliability and safety. HTLS conductors provide better thermal stability and reduced sag under high load conditions, helping maintain proper ground clearance and reducing the risk of outages.

Because utilities manage most of the world's transmission infrastructure and continuously invest in grid expansion and modernization, they represent the largest and most influential end-use industry in the HTLS conductor market.

The Global High Temperature and Low Sag (HTLS) Conductor Market Report is segmented on the basis of the following:

By Conductor Type

- Aluminum Conductor Composite Core (ACCC)

- Aluminum Conductor Composite Reinforced (ACCR)

- Gap-type Aluminum Conductor Steel Reinforced (GAP/G(Z)ACSR)

- Aluminum Conductor Invar Reinforced (ACIR)

- Aluminum Conductor Steel Supported (ACSS)

- Thermal-Resistant Aluminum Alloy Conductor (TACSR/ZTACSR)

- Other Conductor Type

By Material

- Aluminum Conductors

- Composite Core Conductors

- Steel-Reinforced Conductors

- Alloy-Based Conductors

- Other Material

By Voltage Level

- Low Voltage (LV)

- Medium Voltage (MV)

- High Voltage (HV)

- Extra High Voltage (EHV)

By Application

- Power Transmission

- Power Distribution

- Renewable Energy Grid Integration

- Grid Reconductoring / Capacity Upgrade

- Other Application

By End-Use Industry

- Electric Utilities

- Renewable Energy Integration

- Oil & Gas

- Mining & Metal Processing

- Railways & Transportation

- Other End-Use Industry

Impact of Artificial Intelligence in the Global High Temperature and Low Sag (HTLS) Conductor Market

- AI for Predictive Grid Analytics: AI algorithms analyze weather patterns, load forecasts, and real-time sensor data (e.g., from line monitors) to dynamically determine the optimal operating capacity of HTLS lines, maximizing renewable energy utilization while ensuring safety margins.

- AI-Driven Transmission Line Design: AI tools optimize the selection of conductor type and tower configurations for new projects, balancing cost, performance, and environmental impact by simulating thousands of scenarios, including thermal ratings and mechanical stresses.

- Predictive Maintenance and Failure Prevention: AI analyzes data from drone inspections, thermal imaging, and vibration sensors to predict potential issues like fitting fatigue, core degradation, or galloping events on HTLS lines, enabling proactive maintenance and preventing costly outages.

- Dynamic Line Rating (DLR) Optimization: AI integrates weather forecasts and real-time line conditions to accurately calculate dynamic line ratings, allowing grid operators to safely push more power through HTLS conductors during favorable conditions (e.g., high wind, low ambient temperature).

- Supply Chain and Manufacturing Optimization: AI is used by manufacturers to optimize the complex production processes of composite cores and aluminum stranding, reducing waste, improving quality control, and accelerating delivery times for large-scale infrastructure projects.

Global High Temperature and Low Sag (HTLS) Conductor Market: Regional Analysis

Region with the Largest Revenue Share

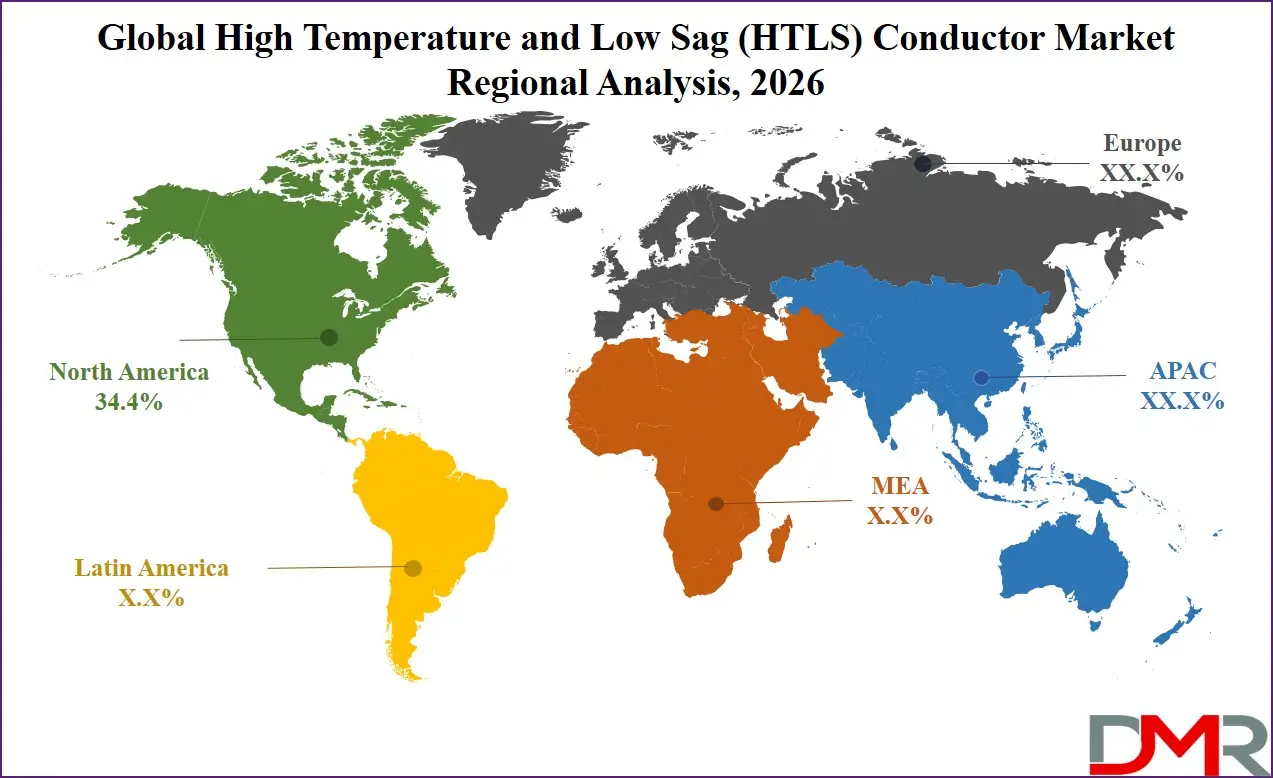

North America is projected to dominate the regional segment with the highest market share as it is anticipated to hold 34.4% of the total market revenue by the end of 2026. This is due to a large stock of aging transmission infrastructure requiring urgent upgrades, high levels of grid congestion, and substantial federal and state funding for grid modernization and resilience. The region is home to leading HTLS manufacturers and early-adopter utilities, driving technological advancements in conductor technology. Strong regulatory drivers from FERC and state-level renewable portfolio standards (RPS) compel utilities to seek high-capacity solutions. The United States, in particular, accounts for the largest share within North America due to its vast transmission network and significant investments in renewable energy interconnection zones.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Region with the Highest CAGR

Asia-Pacific holds the highest CAGR and is poised to achieve rapid market share growth due to its massive investments in new power generation, expanding transmission networks, and surging electricity demand from industrialization. Countries like China, India, and Indonesia are building extensive new transmission corridors (greenfield) and also beginning to upgrade their existing grids. India's "Green Energy Corridor" project and China's Ultra-High Voltage (UHV) network expansion require high-performance conductors for efficient long-distance power transfer. The region's focus on connecting remote renewable projects and expanding grid access in developing nations, combined with cost-sensitive manufacturing, positions APAC as the fastest-growing market for HTLS conductor systems.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global High Temperature and Low Sag (HTLS) Conductor Market: Competitive Landscape

The Global High Temperature and Low Sag (HTLS) Conductor Market is consolidated, featuring a mix of global wire and cable giants, specialized material science companies, and metal manufacturers. Leading players like Southwire Company, LLC and Elsewedy Electric leverage their extensive manufacturing capabilities and global supply chains. Specialized innovators such as CTC Global Corporation (pioneer of ACCC conductor) drive market dynamics with patented composite core technologies. Traditional cable manufacturers with a strong presence in the high-voltage sector, including Nexans, Prysmian Group, Sumitomo Electric Industries, Ltd., and LS Cable & System Ltd., offer a wide portfolio of HTLS solutions, including ACCC, ACCR, and Gap-type conductors. Regional players in Asia and the Middle East are also highly active, catering to local demand with cost-effective manufacturing and established utility relationships.

Some of the prominent players in the Global High Temperature and Low Sag (HTLS) Conductor Market are:

- Southwire Company, LLC

- Prysmian S.p.A.

- Nexans S.A.

- Sumitomo Electric Industries, Ltd.

- LS Cable & System Ltd.

- CTC Global Corporation

- Elsewedy Electric

- Lamifil N.V.

- ZTT International Limited

- Hengtong Group

- Midal Cables Ltd.

- APAR Industries Limited

- J-Power Systems Corp. (Sumitomo Electric)

- Furukawa Electric Co., Ltd.

- General Cable Technologies Corporation (Prysmian)

- Sterlite Power

- Oman Cables Industry (SAOG)

- Taihan Electric Wire Co., Ltd.

- KEC International Limited

- LUMPI-BERNDORF Draht- und Seilwerk GmbH

- Other Key Players

Recent Developments in the Global High Temperature and Low Sag (HTLS) Conductor Market

- October 2025: CTC Global announced a new, higher-strength version of its ACCC conductor core, designed for ultra-long span applications like major river crossings and mountainous terrain, improving safety and reducing tower counts.

- September 2025: Prysmian secured a major frame agreement with a European TSO to supply its advanced HTLS conductors for a 10-year grid upgrade program aimed at integrating North Sea offshore wind energy.

- August 2025: Southwire expanded its manufacturing facility in the United States to increase production capacity for its composite core HTLS conductors, responding to soaring demand from domestic grid modernization projects.

- July 2025: Nexans launched a new digital monitoring solution specifically designed for HTLS lines, integrating real-time temperature and sag sensors with a cloud-based analytics platform for dynamic line rating.

- June 2025: Sumitomo Electric announced a breakthrough in a new aluminum alloy with higher thermal resistance, enabling a new class of HTLS conductors with even greater ampacity and lower losses.

- May 2025: The Indian government's Power Grid Corporation awarded a significant contract to a consortium including APAR Industries for the supply of HTLS conductors for the crucial Leh-Haryana transmission line, enabling renewable power transfer from the Himalayas.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 2,181.8 Mn |

| Forecast Value (2035) |

USD 4,670.9 Mn |

| CAGR (2026–2035) |

8.8% |

| The US Market Size (2026) |

USD 631.2 Mn |

| Historical Data |

2020 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Conductor Type (Aluminum Conductor Composite Core (ACCC), Aluminum Conductor Composite Reinforced (ACCR), Gap-type Aluminum Conductor Steel Reinforced (GAP/G(Z)ACSR), Aluminum Conductor Invar Reinforced (ACIR), Aluminum Conductor Steel Supported (ACSS), Thermal-Resistant Aluminum Alloy Conductor (TACSR/ZTACSR), Other Conductor Type), By Material (Aluminum Conductors, Composite Core Conductors, Steel-Reinforced Conductors, Alloy-Based Conductors, Other Material), By Voltage Level (Low Voltage (LV), Medium Voltage (MV), High Voltage (HV), Extra High Voltage (EHV)), By Application (Power Transmission, Power Distribution, Renewable Energy Grid Integration, Grid Reconductoring / Capacity Upgrade, Other Application), and By End-Use Industry (Electric Utilities, Renewable Energy Integration, Oil & Gas, Mining & Metal Processing, Railways & Transportation, Other End-Use Industry). |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Southwire Company, LLC, Prysmian S.p.A., Nexans S.A., Sumitomo Electric Industries, Ltd., LS Cable & System Ltd., CTC Global Corporation, Elsewedy Electric, Lamifil N.V., ZTT International Limited, Hengtong Group, Midal Cables Ltd., APAR Industries Limited, J-Power Systems Corp. (Sumitomo Electric), Furukawa Electric Co., Ltd., General Cable Technologies Corporation (Prysmian), Sterlite Power, Oman Cables Industry (SAOG), Taihan Electric Wire Co., Ltd., KEC International Limited, LUMPI-BERNDORF Draht- und Seilwerk GmbH, and Other Key Players. |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global High Temperature and Low Sag (HTLS) Conductor Market?

▾ The Global High Temperature and Low Sag (HTLS) Conductor Market size is estimated to have a value of USD 2,181.8 million in 2026 and is expected to reach USD 4,670.9 million by the end of 2035.

What is the growth rate in the Global High Temperature and Low Sag (HTLS) Conductor Market?

▾ The market is growing at a CAGR of 8.8 percent over the forecasted period of 2026-2035.

What is the size of the US High Temperature and Low Sag (HTLS) Conductor Market?

▾ The US HTLS Conductor Market is projected to be valued at USD 631.2 million in 2026. It is expected to witness subsequent growth as it holds USD 1,289.9 million in 2035 at a CAGR of 8.3%.

Which region accounted for the largest Global High Temperature and Low Sag (HTLS) Conductor Market?

▾ North America is expected to have the largest market share in the Global High Temperature and Low Sag (HTLS) Conductor Market with a share of about 34.4% in 2026.

Who are the key players in the Global High Temperature and Low Sag (HTLS) Conductor Market?

▾ Some of the major key players in the Global High Temperature and Low Sag (HTLS) Conductor Market are Southwire Company, LLC, Prysmian S.p.A., Nexans S.A., Sumitomo Electric Industries, Ltd., CTC Global Corporation, Elsewedy Electric, and many others.