Market Overview

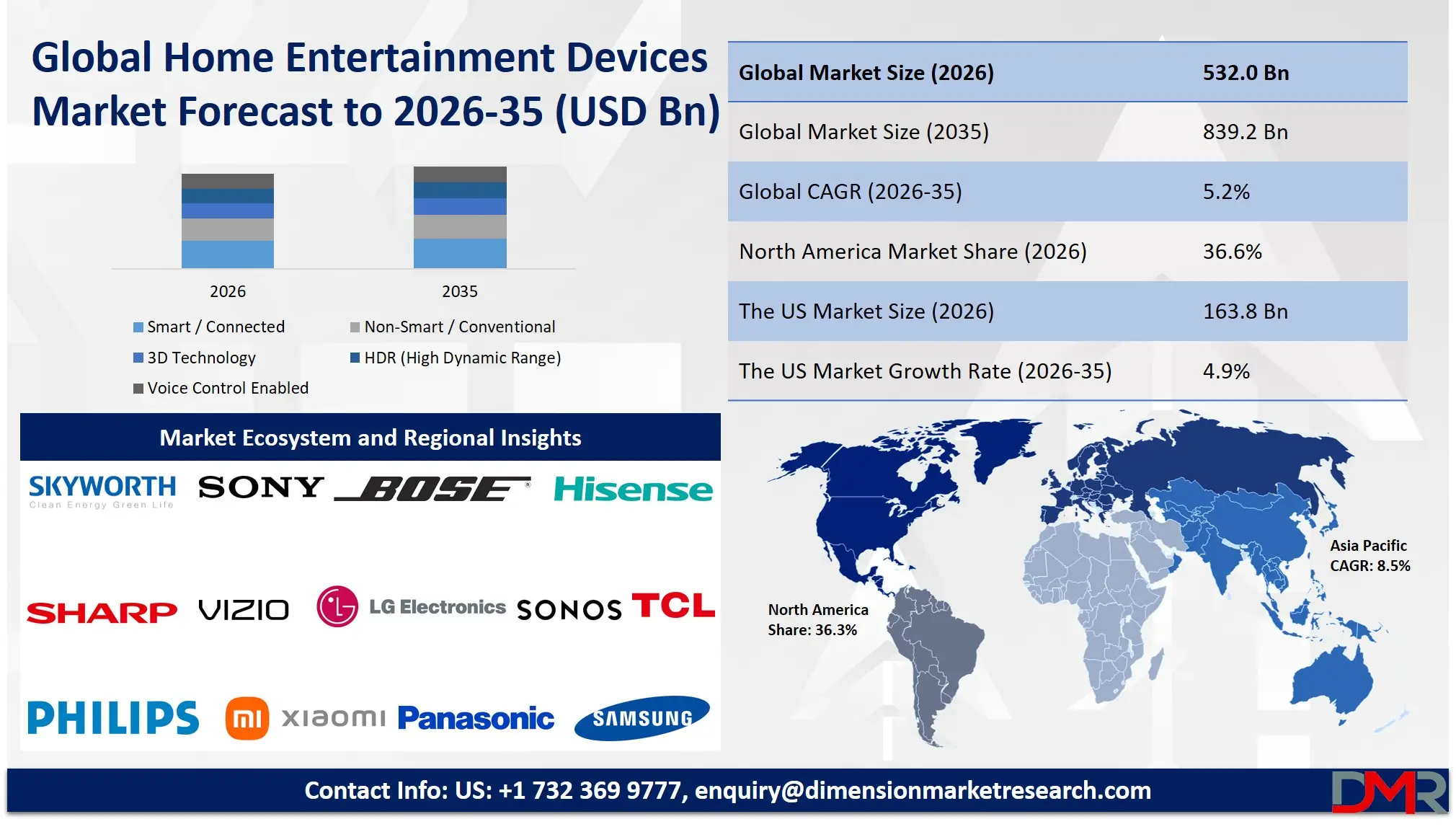

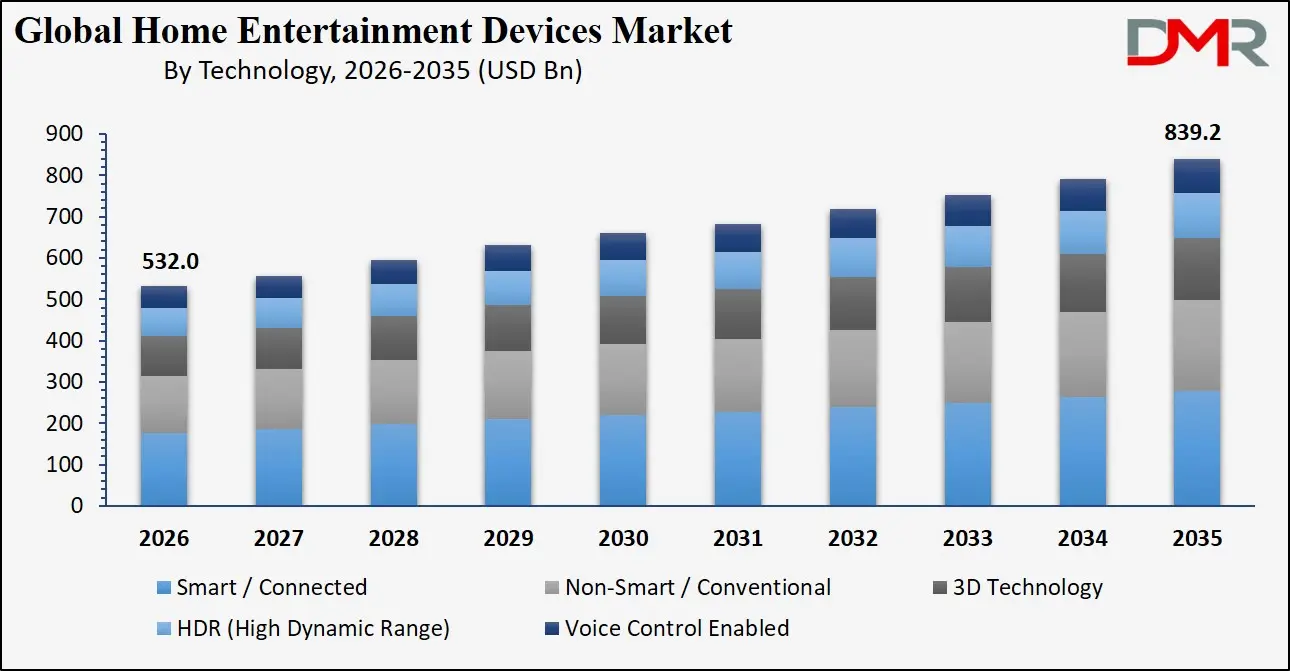

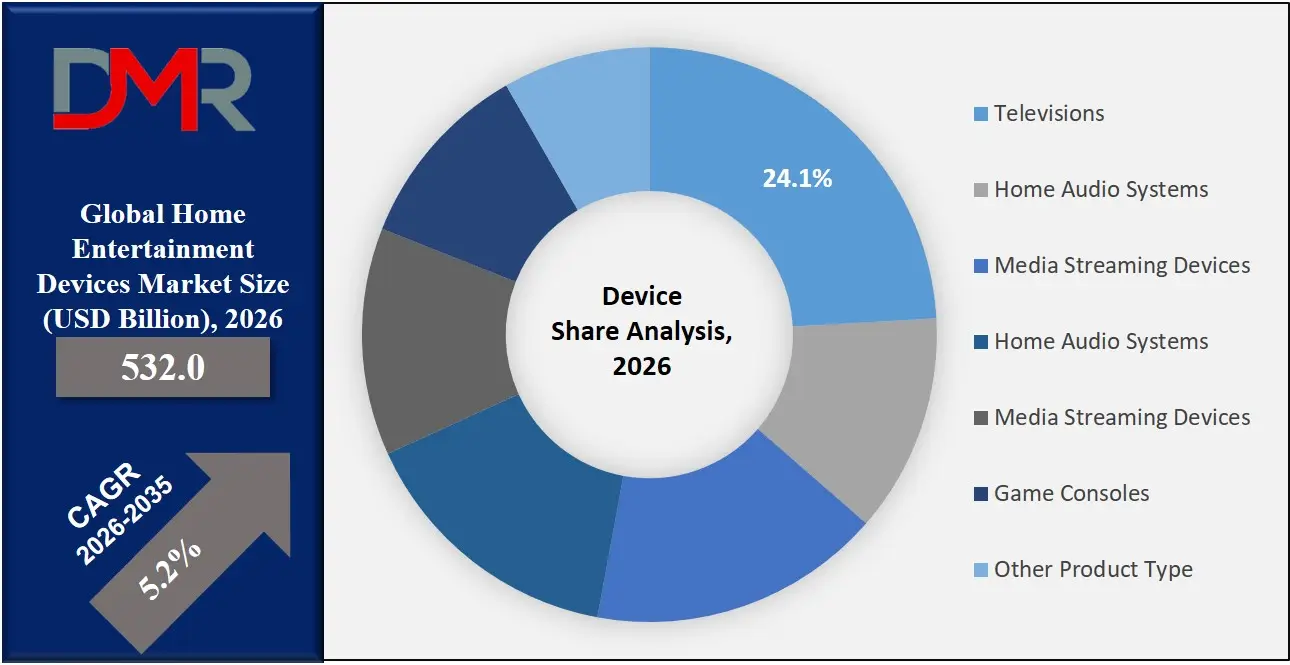

The Global Home Entertainment Devices Market is set for substantial expansion, reaching an estimated USD 532.0 billion in 2026 and projected to grow at a strong CAGR of 5.2% from 2026 to 2035, to a market value of USD 839.2 billion by 2035. This robust growth trajectory is fueled by the accelerating consumer demand for immersive viewing experiences, the proliferation of high-speed internet, and the rapid evolution of display and audio technologies.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Rising consumer disposable income, coupled with a growing preference for premium, large-screen smart TVs, high-fidelity audio systems, and integrated smart home ecosystems, is compelling manufacturers to innovate continuously. The expansion of Over-The-Top (OTT) streaming platforms, the availability of 4K/8K content, and cloud gaming services is significantly increasing demand for devices capable of delivering superior picture and sound quality.

Additionally, technological advancements such as OLED, QLED, and MicroLED displays, alongside Dolby Atmos and object-based sound, are driving replacement cycles and premiumization. Businesses are increasingly integrating voice control, AI-based content recommendations, and seamless connectivity with IoT devices to enhance user engagement and brand loyalty. Government initiatives promoting local manufacturing and digital infrastructure are also contributing to market accessibility and affordability.

The shift towards larger screen sizes, smart connectivity features, and energy-efficient devices is enabling both luxury and mass-market segments to access cutting-edge home entertainment solutions. As work-from-home and hybrid lifestyles persist, driving multi-purpose use of entertainment devices for gaming, fitness, and social connection, the Home Entertainment Devices Market is expected to witness sustained growth through 2035, driven by technological convergence and evolving consumer lifestyles.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Growing government support for digital content creation and broadcasting standards further accelerates global adoption. However, barriers such as supply chain volatility for semiconductor components, intense price competition, product commoditization, and varying consumer adoption rates in emerging economies remain. Despite these limitations, the convergence of display technology, streaming services, and AI-powered user interfaces positions home entertainment devices as a central pillar of modern digital lifestyles through 2035.

The US Home Entertainment Devices Market

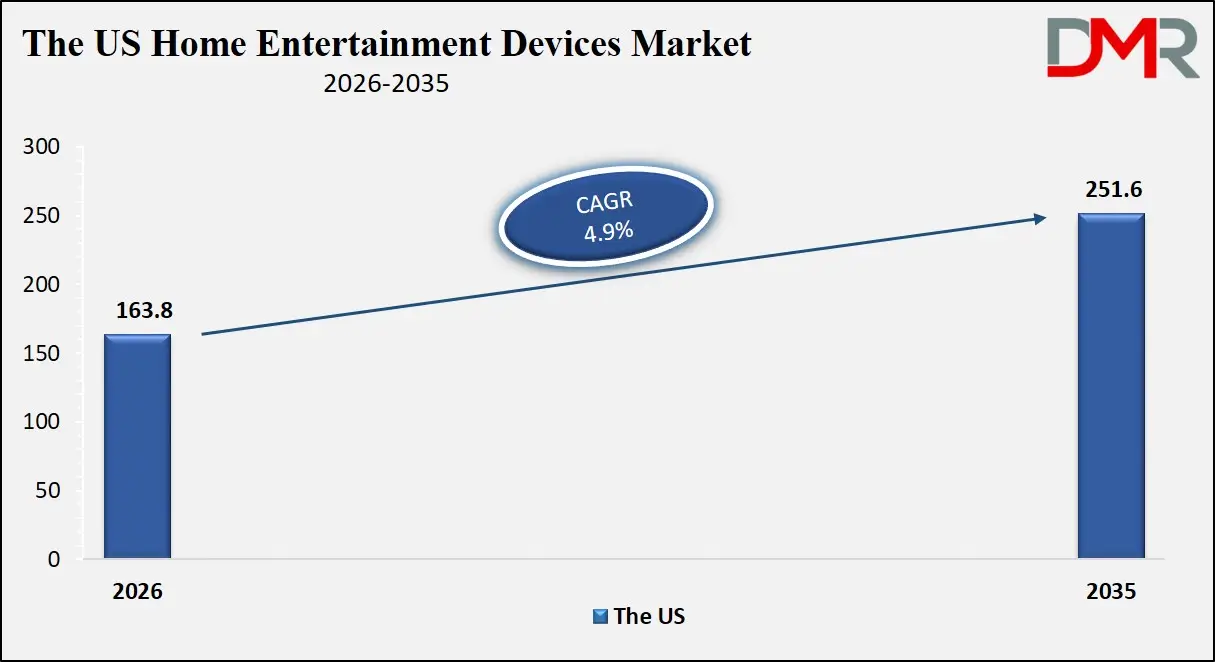

The U.S. Home Entertainment Devices Market is projected to reach USD 163.8 billion in 2026 and grow at a CAGR of 4.9%, reaching USD 251.6 billion by 2035. The U.S. leads global adoption due to its high consumer spending power, early adoption of cutting-edge technologies like 8K and Dolby Vision, and a mature ecosystem of content providers like Netflix, Disney+, and Apple TV+.

The proliferation of streaming services and consumer desire for cinematic experiences at home fuels demand for premium smart TVs, soundbars, and wireless multi-room audio systems. Major technology firms such as Apple, Amazon, and Google are integrating their platforms (tvOS, Fire TV, Google TV) directly into devices, enhancing the smart home entertainment hub.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

U.S. regulatory support for next-generation broadcasting standards (ATSC 3.0 – "NextGen TV") encourages investment in compatible devices. The market is witnessing a shift towards direct-to-consumer sales channels and subscription-based models for content, driving the need for devices that offer seamless integration and superior user interfaces. The rise of competitive gaming and e-sports has further intensified the focus on high-refresh-rate displays and low-latency audio, positioning the U.S. as a critical innovator and trendsetter in this space.

The Europe Home Entertainment Devices Market

The Europe Home Entertainment Devices Market is projected to be valued at approximately USD 133.0 billion in 2026 and is projected to reach around USD 203.0 billion by 2035, growing at a CAGR of about 4.8% from 2026 to 2035. Europe's market strength is anchored by its strong design sensibility, focus on energy efficiency (Ecodesign regulations), and a diverse consumer base with varying content consumption habits.

Countries such as Germany, the U.K., France, and the Nordic region are widely adopting premium devices, driven by high disposable incomes and a strong broadcasting heritage. The U.K.'s demand for high-quality sports broadcasting and the EU's emphasis on digital sovereignty influence the development of local content platforms and device compatibility.

Europe's high broadband penetration, cross-border streaming services, and a mature market for home cinema systems drive the demand for sleek, high-performance, and sustainable entertainment solutions. Consumer awareness regarding product repairability and environmental impact is growing, encouraging manufacturers to focus on circular economy principles. With a sophisticated user base and a regulatory landscape that prioritizes consumer rights and privacy, Europe remains a highly advanced and essential region for home entertainment devices.

The Japan Home Entertainment Devices Market

The Japan Home Entertainment Devices Market is anticipated to be valued at approximately USD 53.2 billion in 2026 and is expected to attain nearly USD 75.0 billion by 2035, expanding at a CAGR of about 3.9% during the forecast period. Japan's technologically savvy population and the government's push for "Society 5.0," which integrates digital technologies into daily life, are driving the adoption of advanced entertainment devices, making them a cornerstone of the modern, connected home.

The Ministry of Internal Affairs and Communications (MIC) actively supports the development of 8K broadcasting and next-generation broadcasting infrastructure, promoting the adoption of compatible ultra-high-definition displays. Japan's leadership in display panel technology and consumer electronics miniaturization, driven by giants like Sony and Panasonic, provides a robust foundation for premium device manufacturing.

Japan's concept of "omotenashi" (hospitality) translates into user-centric device design, with intuitive interfaces and space-saving solutions. Major corporations are integrating home entertainment devices into broader smart home ecosystems, from voice-activated televisions to connected audio systems. Companies are deploying advanced features to cater to an aging population, such as voice control and simplified remotes, ensuring the integrity and accessibility of digital entertainment. Japan's cultural emphasis on quality, design, and technological precision positions it as a high-growth, quality-focused market.

Global Home Entertainment Devices Market: Key Takeaways

- Strong Global Market Growth Outlook: The Global Home Entertainment Devices Market is expected to be valued at USD 532.0 billion in 2026 and is projected to reach USD 839.2 billion by 2035, showcasing rapid expansion supported by rising demand for premium home entertainment experiences.

- High CAGR Driven by Technological Adoption: The market is expected to grow at an impressive CAGR of 5.2% from 2026 to 2035, fueled by the accelerating adoption of 8K displays, immersive audio technologies, and the increasing convergence of AI and IoT in consumer electronics.

- Strong Growth Trajectory in the United States: The U.S. Home Entertainment Devices Market stands at USD 163.8 billion in 2026 and is projected to reach USD 251.6 billion by 2035, expanding at a CAGR of 4.9% due to high consumer spending and a mature streaming ecosystem.

- Regional Dominance: North America is expected to capture approximately 36.6% of the global market share in 2026, supported by strong consumer purchasing power, early technology adoption, and a robust content creation industry.

- Rapid Advancement in Device Technologies: Innovations including MicroLED and QD-OLED displays, AI-powered upscaling, object-based audio formats like Dolby Atmos, and seamless integration with smart home platforms are significantly enhancing the viewing and listening experience.

- Growing Streaming and Gaming Demand Boosts Adoption: The rising global consumption of OTT content, cloud gaming, and virtual reality, coupled with the desire for a "theater-at-home" experience, is driving sustained demand for high-performance, large-screen, and immersive audio devices.

Global Home Entertainment Devices Market: Use Cases

- Home Cinema Experience: Families and enthusiasts use large-screen 4K/8K TVs or ultra-short-throw projectors paired with soundbars or AV receivers to recreate a cinematic experience at home for movies and live sports.

- Immersive Gaming: Gamers utilize high-refresh-rate displays, low-latency gaming monitors, and spatial audio headsets or systems to gain a competitive edge and enjoy an immersive experience with next-gen consoles and PC gaming.

- Social and Fitness Hub: Households use smart displays and TVs for interactive fitness classes, karaoke nights, and social video calls, transforming the living room into a multi-purpose activity center.

- Multi-Room Audio Streaming: Consumers use wireless speakers and sound systems throughout the home, streaming music and podcasts via Wi-Fi or Bluetooth, creating a seamless audio environment controlled by smartphone apps.

- Ambient and Secondary Viewing: Smart displays and tablets are used in kitchens and bedrooms for casual content viewing, recipe following, or as smart home control centers, expanding entertainment beyond the main living area.

Global Home Entertainment Devices Market: Stats & Facts

Eurostat (Statistical Office of the European Union)

- In 2024, 58% of EU individuals (aged 16–74) used an internet-connected TV.

- 70% of EU individuals used at least one Internet of Things (IoT) device in 2024.

- 20% of EU individuals used a game console connected to the internet.

- 19% of EU individuals used internet-connected home audio systems or smart speakers.

- Among EU youth (16–24 years), 67% used internet-connected TVs.

- Among EU youth (16–24 years), 40% used game consoles.

- In 2023, 93% of EU households had internet access.

- 90% of EU households had broadband internet access in 2023.

- In 2023, 74% of EU individuals purchased goods or services online.

- Online purchasing increased from 65% in 2020 to 74% in 2023.

OECD (Organisation for Economic Co-operation and Development)

- Across OECD countries, 96% of 15-year-olds live in homes with at least three digital devices.

- In OECD economies, over 95% of households have access to a television.

- The majority of OECD households report owning multiple screen-based entertainment devices.

- Broadband penetration across OECD countries exceeded 80% of households in recent reporting years.

- Fiber broadband subscriptions account for more than 35% of total fixed broadband in OECD countries.

U.S. Census Bureau (American Community Survey)

- In 2023, 97% of U.S. households had at least one television.

- 92% of U.S. households had a computer device (desktop, laptop, or tablet).

- 95% of U.S. households had broadband internet subscriptions.

- Over 85% of U.S. households reported streaming video usage.

Federal Communications Commission (FCC), United States

- Over 94% of the U.S. population has access to fixed broadband service.

- More than 80% of U.S. households subscribe to fixed broadband services.

Statistics Bureau of Japan

- Over 95% of Japanese households own a television set.

- Internet penetration in Japanese households exceeds 90%.

- More than 80% of Japanese households subscribe to broadband internet.

- Smart device ownership (including smart TVs and connected devices) continues to rise annually in Japan.

Ministry of Internal Affairs and Communications (Japan)

- Over 70% of Japanese households use internet-based video streaming services.

- Digital device usage among individuals aged 13–59 exceeds 85%.

Ofcom (UK Communications Regulator)

- In the UK, 91% of households have a television set.

- Over 70% of UK households own a smart TV.

- More than 60% of UK households use streaming devices connected to TVs.

International Telecommunication Union (ITU)

- In 2023, 67% of the global population used the internet.

- Global household internet penetration reached approximately 66% worldwide.

- Fixed broadband subscriptions globally surpassed 1.4 billion.

Global Home Entertainment Devices Market: Market Dynamics

Driving Factors in the Global Home Entertainment Devices Market

Proliferation of OTT and High-Quality Content

The explosive growth of streaming services like Netflix, Disney+, and Amazon Prime, which are investing heavily in original 4K and HDR content, is a primary driver. Consumers are compelled to upgrade their devices to fully appreciate this content. This, coupled with the rise of high-fidelity music streaming (Tidal, Apple Music Lossless), fuels demand for advanced displays and high-resolution audio systems that can deliver a truly immersive experience, turning living rooms into personal theaters.

Technological Advancements and Premiumization

Continuous innovation in display (OLED, QLED, Mini-LED, MicroLED) and audio (Dolby Atmos, DTS:X) technologies creates a strong pull for replacement purchases. Features like higher refresh rates (120Hz+), faster processors for smart TVs, AI-powered upscaling, and seamless connectivity (HDMI 2.1, Wi-Fi 6E) appeal to tech-savvy consumers and enthusiasts. This "premiumization" trend allows manufacturers to maintain higher average selling prices despite market maturity.

Restraints in the Global Home Entertainment Devices Market

Supply Chain Volatility and Component Costs

The industry is highly susceptible to global supply chain disruptions, particularly for critical components like semiconductors, display panels, and specialized chips. Shortages can lead to production delays, increased costs, and inventory challenges, which are often passed on to consumers. Geopolitical tensions and logistics bottlenecks can further exacerbate these issues, creating market uncertainty and impacting the affordability of devices.

Product Commoditization and Price Erosion

In mature product categories like entry-level and mid-range TVs, intense competition has led to significant price erosion and commoditization. This makes it difficult for brands to differentiate themselves and maintain profitability. The influx of numerous low-cost brands, particularly from emerging markets, intensifies price wars, potentially compromising product quality and after-sales support, which can affect long-term consumer trust.

Opportunities in the Global Home Entertainment Devices Market

Expansion into Emerging Digital Economies

Emerging markets in Asia-Pacific, Latin America, and Africa represent major growth opportunities due to rapid urbanization, rising middle classes, and increasing disposable incomes. As internet infrastructure improves and OTT platforms localize content, demand for affordable smart TVs, soundbars, and streaming devices is set to surge. Developing localized features, partnering with regional content providers, and offering flexible financing options can unlock this massive consumer base.

Integration with the Metaverse and Immersive Tech

The convergence of home entertainment with virtual and augmented reality (VR/AR) creates a new frontier. High-end displays and spatial audio systems are essential for powering immersive metaverse experiences, social VR platforms, and augmented reality gaming from home. Developing devices optimized for these new digital spaces, such as low-latency, high-fidelity headsets and haptic feedback systems, represents a significant future growth vector.

Trends in the Global Home Entertainment Devices Market

The Rise of the "Hero" TV and Ecosystem Lock-In

Consumers are increasingly investing in a single, large, premium "hero" TV for their main living area, which serves as the centerpiece of their digital life. This device is not just for content viewing but acts as a smart home hub, a gaming display, and an art frame. Brands are leveraging this by creating closed ecosystems (e.g., Apple, Samsung, LG) where the TV seamlessly integrates with their own soundbars, speakers, and smart home devices, encouraging brand loyalty and repeat purchases.

Sustainability and Eco-Conscious Consumerism

Environmental concerns are becoming a significant purchasing factor. Consumers are increasingly interested in devices made with recycled materials, featuring energy-efficient components (higher energy ratings), and designed for longer life and repairability. Manufacturers are responding by launching "green" product lines, reducing packaging waste, and offering take-back or trade-in programs, making sustainability a key brand differentiator.

Global Home Entertainment Devices Market: Research Scope and Analysis

By Device Type Analysis

The Television (TV) segment is projected to dominate the Global Home Entertainment Devices Market, accounting for the largest revenue share compared to audio systems, projectors, and streaming devices. This dominance is primarily driven by the TV's role as the central hub of the home entertainment experience. Consumers consistently prioritize investment in the largest and most advanced screen for their living rooms to watch movies, sports, and stream content.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Modern smart TVs have evolved beyond mere displays; they now integrate streaming apps, voice assistants, and gaming features directly into the platform. Advanced capabilities such as 4K/8K resolution, OLED/Mini-LED panel technology, high dynamic range (HDR), and high refresh rates provide a compelling reason for consumers to upgrade. The declining cost of large-screen panels has also made features like 65-inch and 75-inch TVs accessible to a broader market.

Additionally, the shift toward smart home integration has positioned the TV as a central visual interface for IoT devices, video calls, and even digital art displays. While soundbars and streaming sticks serve as complementary devices, the TV remains the primary purchase. As content quality and display technology continue to advance, the Television segment is expected to maintain its leadership position, driven by continuous innovation and its central role in digital lifestyles.

By Technology Analysis

Smart/Connected technology is expected to dominate the market, as it has become the standard feature across almost all new home entertainment devices. Consumers expect their TVs, soundbars, and projectors to offer built-in Wi-Fi, access to streaming apps, and compatibility with voice assistants like Alexa and Google Assistant. This technology transforms standalone devices into connected ecosystem components.

Smart platforms (e.g., webOS, Tizen, Google TV, Roku TV) provide a unified user interface for content discovery and device control, significantly enhancing user convenience. They also enable features like content recommendations, software updates, and multi-room audio synchronization. This connectivity is crucial for accessing the vast library of OTT content, which is the primary use case for modern entertainment devices.

While non-smart displays still exist for commercial or ultra-budget applications, their market share is rapidly diminishing. The integration of smart technology is no longer a premium differentiator but a baseline consumer expectation, ensuring its dominant position in the market and its role in driving engagement and recurring content revenue for ecosystem providers.

By Price Range Analysis

The Mid-Range segment is anticipated to dominate the market, offering the optimal balance of advanced features, performance, and affordability for the mass consumer. This segment captures buyers who seek superior technology such as 4K resolution, QLED displays, and Dolby Atmos support without the significant price premium of flagship models.

Mid-range devices typically incorporate last cycle's premium technology, making features like large-screen 4K and advanced audio codecs accessible to a wider audience. This price band benefits most from the rapid commoditization of technology, where high-end features quickly trickle down. Major brands focus their volume sales in this range, competing on brand value, software experience, and design.

While the premium segment drives innovation and brand prestige, and the entry-level segment ensures market penetration, the mid-range segment generates the largest revenue volume. It caters to the majority of global households looking for a significant upgrade in their entertainment experience at a justifiable price point, ensuring its continued dominance throughout the forecast period.

By Distribution Channel Analysis

Online retail/e-commerce is projected to dominate the distribution channel segment. The convenience of browsing extensive catalogs, comparing prices, reading user reviews, and having large, heavy items like TVs delivered directly to the home has made online channels the preferred purchase method for a growing number of consumers.

E-commerce platforms often offer competitive pricing, exclusive online deals, and flexible financing options, which are highly attractive to buyers. The proliferation of direct-to-consumer (D2C) channels by major brands (e.g., Samsung, Sony, LG) also allows for stronger customer relationships and control over the brand experience. Detailed product videos and virtual room planners help overcome the inability to physically see the product.

While brick-and-mortar stores remain important for hands-on demos and immediate gratification, their role is increasingly shifting to a "showrooming" function, with the final transaction often occurring online. The continuous improvement in logistics and customer-friendly return policies further solidifies the online channel's leading position in the home entertainment market.

By Screen Size Analysis

The 55-inch to 65-inch segment is forecasted to dominate the market, as this size range has become the new standard for the average living room. Falling panel prices have made these formerly "large" screens highly affordable, offering a truly immersive experience without overwhelming most residential spaces. This size is ideal for enjoying 4K content, as the benefits of higher resolution are most visible on larger screens at typical viewing distances.

This segment benefits from being the "sweet spot" for feature adoption. Premium features like OLED, 120Hz refresh rates, and advanced HDR formats are widely available in this size class, attracting both mainstream and enthusiast buyers. It is the primary battleground for major TV brands, driving volume and revenue.

While screens under 43-inch cater to bedrooms and smaller apartments, and screens above 75-inch represent a growing premium niche, the 55-65 inch range captures the largest share of consumer spending. As manufacturing efficiencies continue to improve, this segment is expected to maintain its dominant position as the go-to choice for primary family room entertainment.

By Application Analysis

Media Streaming and broadcasting are the dominant applications, as this represents the fundamental use case for the vast majority of home entertainment devices. Televisions, soundbars, and streaming devices are primarily purchased to watch content from broadcast TV, cable/satellite, and, most importantly, OTT streaming services like Netflix, YouTube, and Disney+.

The user experience for streaming, from the ease of launching apps to the quality of picture and sound for streamed content, is the primary factor driving consumer satisfaction and brand loyalty. Device manufacturers deeply integrate streaming platforms and optimize their hardware for this purpose. Features like dedicated remote buttons for streaming services underscore its importance.

While gaming, music streaming, and fitness applications are growing rapidly and serve as important secondary purchase drivers, media streaming remains the core daily activity for the vast majority of users. As the volume and quality of streamed content continue to explode, this application will continue to dominate the functional purpose of home entertainment devices.

By End-Use Analysis

The Residential sector is expected to dominate the end-use segment by an overwhelming margin. Home entertainment devices are, by definition, consumer products designed for personal use within households. The purchase decisions are driven by individual and family preferences for leisure, relaxation, and social connection within the home.

Within the residential sector, factors like home size, interior design, household income, and the age of family members heavily influence purchasing patterns. The rise of multi-generational homes and the increasing amount of time spent at home have solidified the need for high-quality entertainment solutions. Marketing efforts are overwhelmingly targeted at residential consumers, emphasizing lifestyle enhancement and personal enjoyment.

While commercial applications (hospitality, corporate lobbies, digital signage) do contribute to the market, they are dwarfed by the sheer volume of devices sold to millions of households globally. The residential end-use will maintain its dominant share, driven by continuous population growth, household formation, and the ever-present consumer desire for a better home entertainment experience.

The Global Home Entertainment Devices Market Report is segmented on the basis of the following:

By Device Type

- Televisions

- Smart TVs

- Non-Smart TVs

- LED TVs

- OLED TVs

- QLED TVs

- Home Audio Systems

- Soundbars

- AV Receivers

- Home Theater Systems

- Wireless Speakers

- Media Streaming Devices

- Streaming Sticks

- Set-Top Boxes

- Game Consoles

- Home Audio Systems

- Soundbars

- AV Receivers

- Home Theater Systems

- Wireless Speakers

- Headphones

- Media Streaming Devices

- Streaming Sticks

- Set-Top Boxes

- Media Players

- Smart Streaming Boxes

- Game Consoles

- Home Consoles

- Handheld Gaming Devices

- Other Product Type

By Technology

- Smart / Connected

- Non-Smart / Conventional

- 3D Technology

- HDR (High Dynamic Range)

- Voice Control Enabled

By Price Range

- Entry-Level / Budget

- Mid-Range

- Premium / High-End

By Distribution Channel

- Online Retail

- E-Commerce Marketplaces

- Brand Websites

- Online Electronics Stores

- Offline Retail

- Specialty Electronics Stores

- Supermarkets / Hypermarkets

- Multi-Brand Retail Stores

- Brand Exclusive Stores

By Application

- Media Streaming & Broadcasting

- Gaming

- Music Streaming

- Fitness & Wellness

- Others

By End-Use

Impact of Artificial Intelligence in the Global Home Entertainment Devices Market

- AI-Powered Picture and Sound Optimization: AI algorithms analyze ambient light and room acoustics, or the specific genre of content being played, to automatically adjust picture settings (brightness, contrast, color) and sound modes for an optimal viewing and listening experience in real-time.

- Personalized Content Recommendations: Integrated AI on smart platforms learns individual and household viewing habits to curate and recommend movies, shows, and music from across different streaming services, creating a unified and personalized discovery interface.

- AI-Driven Voice Assistants and Control: Advanced natural language processing enables more intuitive and conversational voice control for searching content, adjusting volume, controlling smart home devices, and getting information, making the TV a central smart home concierge.

- Upscaling Lower-Resolution Content: AI-driven upscaling technology (e.g., on Sony Bravia Core or NVIDIA Shield) uses deep learning to analyze and reconstruct lower-resolution (HD/SD) content, adding detail and texture to make it appear remarkably close to true 4K or 8K quality.

- Predictive Maintenance and Support: AI can monitor device performance and predict potential hardware failures, such as a failing backlight or overheating components. This allows for proactive customer support alerts or automated diagnostics, improving user satisfaction and reducing warranty costs.

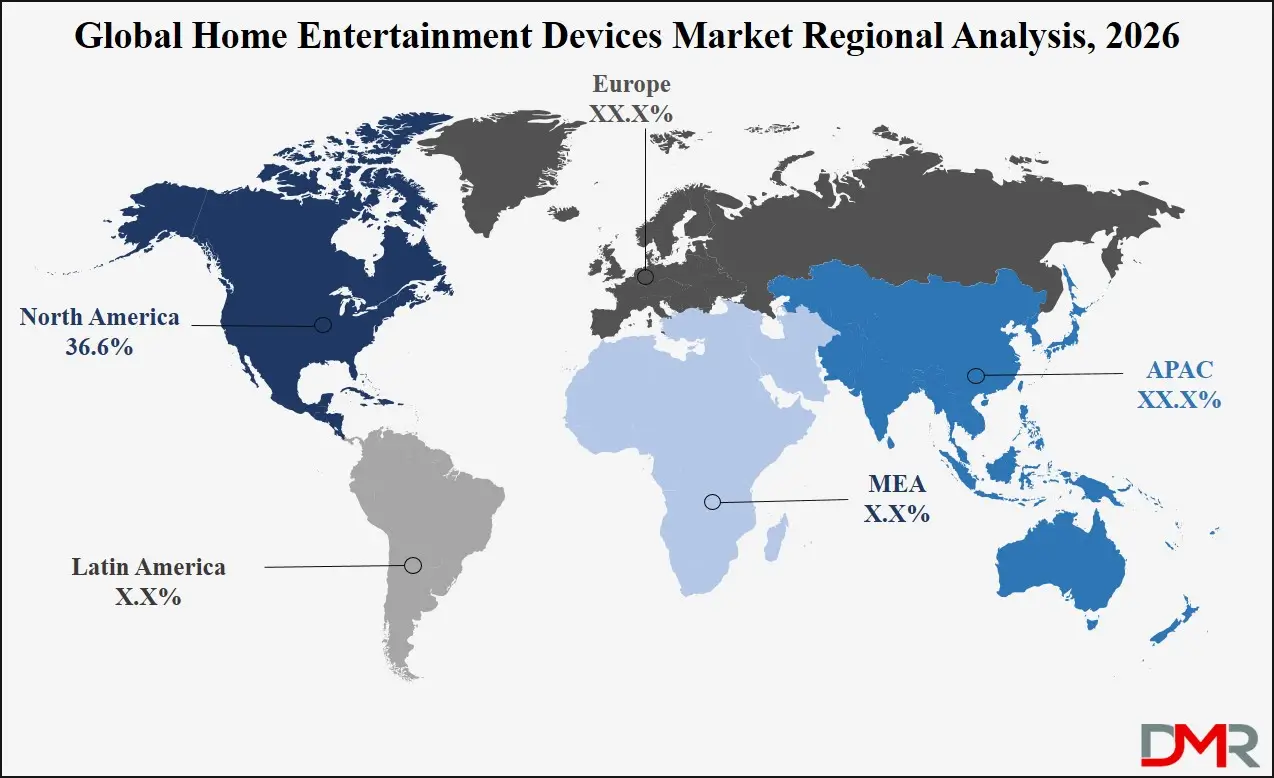

Global Home Entertainment Devices Market: Regional Analysis

Region with the Largest Revenue Share

North America is projected to dominate the regional segment with the highest market share, as it is anticipated to hold 36.6% of the total market revenue by the end of 2026. This is due to its high consumer disposable income, mature digital infrastructure with widespread high-speed internet, and the early, deep-rooted adoption of OTT streaming culture. The region is home to the world's largest technology and content creation companies, driving ecosystem development and consumer demand for the latest premium devices. Strong consumer awareness and a "bigger is better" attitude towards screen sizes and audio further strengthen demand.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The United States, in particular, accounts for the largest share within North America due to its massive consumer electronics market and high volume of premium device sales. Although Asia Pacific is the fastest-growing region, North America continues to hold the largest revenue share due to the high average selling price of devices and the rapid turnover of technology.

Region with the Highest CAGR

Asia-Pacific holds the highest CAGR and is poised to achieve rapid market share growth due to its massive and growing middle-class population, rapid urbanization, and booming consumer electronics manufacturing sector. Countries like China, India, and Southeast Asian nations are seeing a surge in demand for smart TVs and audio devices as disposable incomes rise and digital infrastructure expands. Government initiatives promoting local manufacturing and affordable internet access are creating fertile ground for adoption. The region's price sensitivity is being addressed by local and regional brands offering feature-rich devices at aggressive price points, supported by booming e-commerce platforms. This, combined with an immense volume of first-time buyers and upgraders, positions APAC as the fastest-growing market for home entertainment devices.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Home Entertainment Devices Market: Competitive Landscape

The Global Home Entertainment Devices Market is highly competitive and features a mix of massive multinational conglomerates, specialized audio companies, and agile, low-cost regional players. Leading players like Samsung Electronics, LG Electronics, and Sony Corporation dominate the television and overall home entertainment space, leveraging their vertical integration in display panels and broad product portfolios. Pure-play audio innovators such as Bose, Sonos, and Harman International (Samsung) drive the premium audio segment with specialized, high-fidelity products.

Chinese giants like Hisense, TCL, and Xiaomi have rapidly gained global market share through aggressive pricing, feature-rich products, and strong supply chain management, challenging the dominance of the traditional leaders. Technology and streaming companies like Amazon, Google, and Roku are also key players, providing the operating systems and streaming platforms that power smart devices, and in some cases, producing their own hardware (e.g., Amazon Fire TV, Google Chromecast).

Some of the prominent players in the Global Home Entertainment Devices Market are:

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- Sony Corporation

- Hisense Co., Ltd.

- TCL Technology Group Corporation

- Xiaomi Corporation

- Panasonic Corporation

- Bose Corporation

- Sonos, Inc.

- Vizio Inc.

- Koninklijke Philips N.V.

- Sharp Corporation

- Skyworth Group Co., Ltd.

- Bang & Olufsen

- Harman International Industries, Inc.

- Amazon.com, Inc.

- Google LLC

- Roku, Inc.

- Apple Inc.

- Other Key Players

Recent Developments in the Global Home Entertainment Devices Market

- January 2026: Samsung Electronics unveiled its new line of MicroLED TVs at CES 2026, featuring modular, bezel-less designs and AI-powered processing, targeting the ultra-luxury home cinema segment.

- November 2025: Sony announced a strategic partnership with a leading automotive manufacturer to integrate its Bravia Core streaming service and entertainment suite into next-generation electric vehicle rear-seat entertainment systems.

- October 2025: LG Display showcased its third-generation OLED panel technology, boasting a 40% increase in brightness and improved energy efficiency, signaling a major upgrade for premium TVs in 2026.

- September 2025: Amazon expanded its Fire TV ambient experience, allowing the TV to function as a digital art frame, personal photo slideshow, and smart home dashboard when not in use, enhancing its utility beyond active viewing.

- August 2025: TCL announced the opening of a new, large-scale manufacturing plant in Vietnam to diversify its supply chain and meet growing demand for its TVs in Western markets.

- July 2025: Sonos acquired a specialist AI audio startup to enhance its Trueplay tuning technology, aiming to deliver even more personalized and immersive spatial audio experiences tailored to individual room acoustics.

- June 2025: Hisense launched its first-ever tri-chroma laser projector for the consumer market, bringing ultra-short-throw, 4K projection with a wider color gamut to a more accessible price point.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 532.0 Bn |

| Forecast Value (2035) |

USD 839.2 Bn |

| CAGR (2026–2035) |

5.2% |

| The US Market Size (2026) |

USD 163.8 Bn |

| Historical Data |

2020 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Device Type (Televisions, Home Audio Systems, Media Streaming Devices, Game Consoles, Other Product Type), By Technology (Smart/Connected, Non-Smart/Conventional, 3D Technology, HDR (High Dynamic Range), Voice Control Enabled), By Price Range (Entry-Level/Budget, Mid-Range, Premium/High-End), By Distribution Channel (Online Retail, Offline Retail), By Application (Media Streaming & Broadcasting, Gaming, Music Streaming, Fitness & Wellness, Others), By End-Use (Residential, Commercial) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Samsung Electronics Co., Ltd., LG Electronics Inc., Sony Corporation, Hisense Co., Ltd., TCL Technology Group Corporation, Xiaomi Corporation, Panasonic Corporation, Bose Corporation, Sonos, Inc., Vizio Inc., Koninklijke Philips N.V., Sharp Corporation, Skyworth Group Co., Ltd., Bang & Olufsen, Harman International Industries, Inc., Amazon.com, Inc., Google LLC, Roku, Inc., Apple Inc., and Other Key Players |

Frequently Asked Questions

How big is the Global Home Entertainment Devices Market?

▾ The Global Home Entertainment Devices Market size is estimated to have a value of USD 532.0 billion in 2026 and is expected to reach USD 839.2 billion by the end of 2035.

What is the growth rate in the Global Home Entertainment Devices Market?

▾ The market is growing at a CAGR of 5.2 percent over the forecasted period of 2026-2035.

What is the size of the US Home Entertainment Devices Market?

▾ The US Home Entertainment Devices Market is projected to be valued at USD 163.8 billion in 2026. It is expected to witness subsequent growth as it holds USD 251.6 billion in 2035 at a CAGR of 4.9%.

Which region accounted for the largest Global Home Entertainment Devices Market?

▾ North America is expected to have the largest market share in the Global Home Entertainment Devices Market with a share of about 36.6% in 2026.

Who are the key players in the Global Home Entertainment Devices Market?

▾ Some of the major key players in the Global Home Entertainment Devices Market are Samsung Electronics, LG Electronics, Sony Corporation, Hisense, TCL, Xiaomi, Bose, and Sonos, among many others.