Market Snapshot

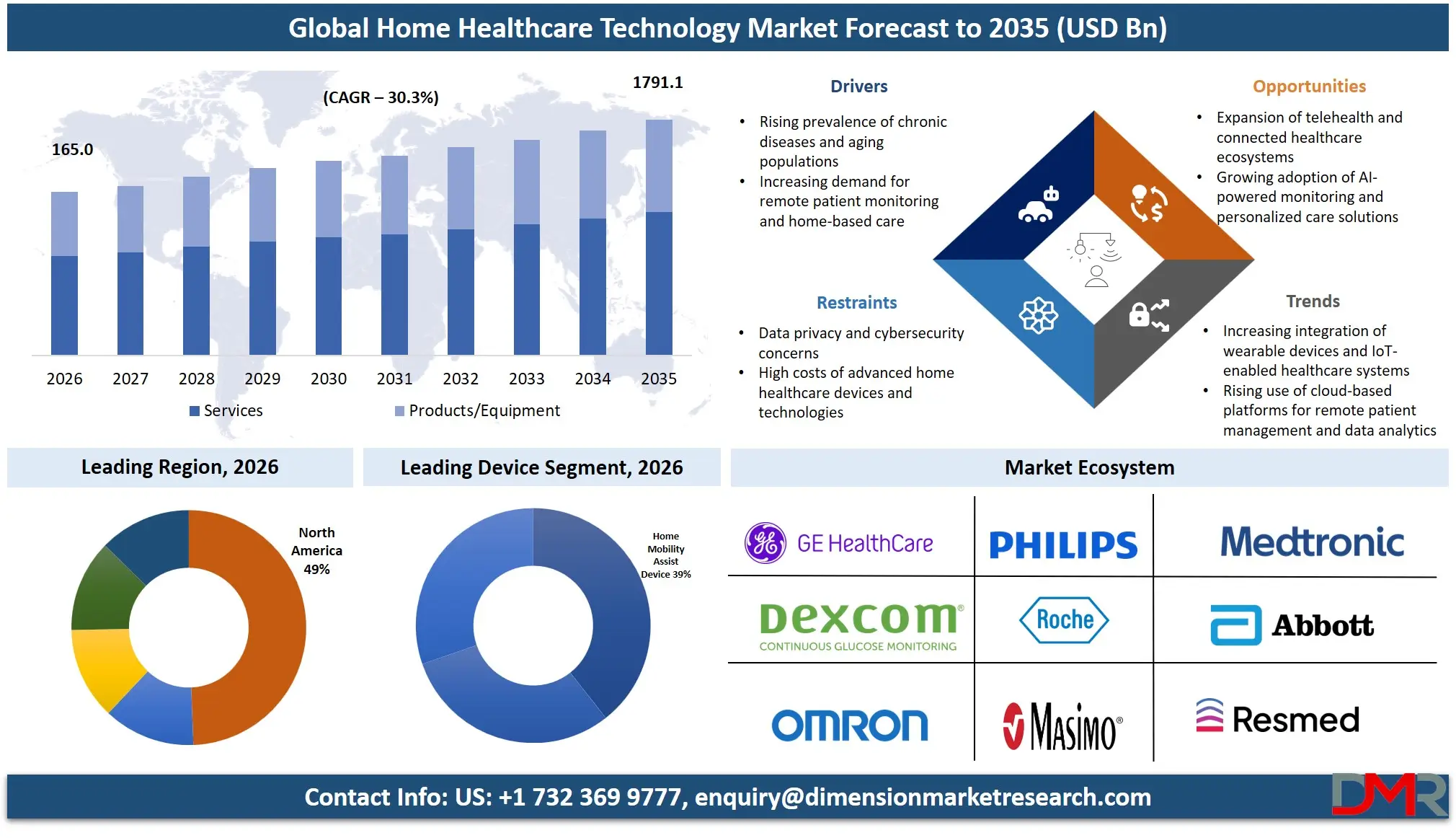

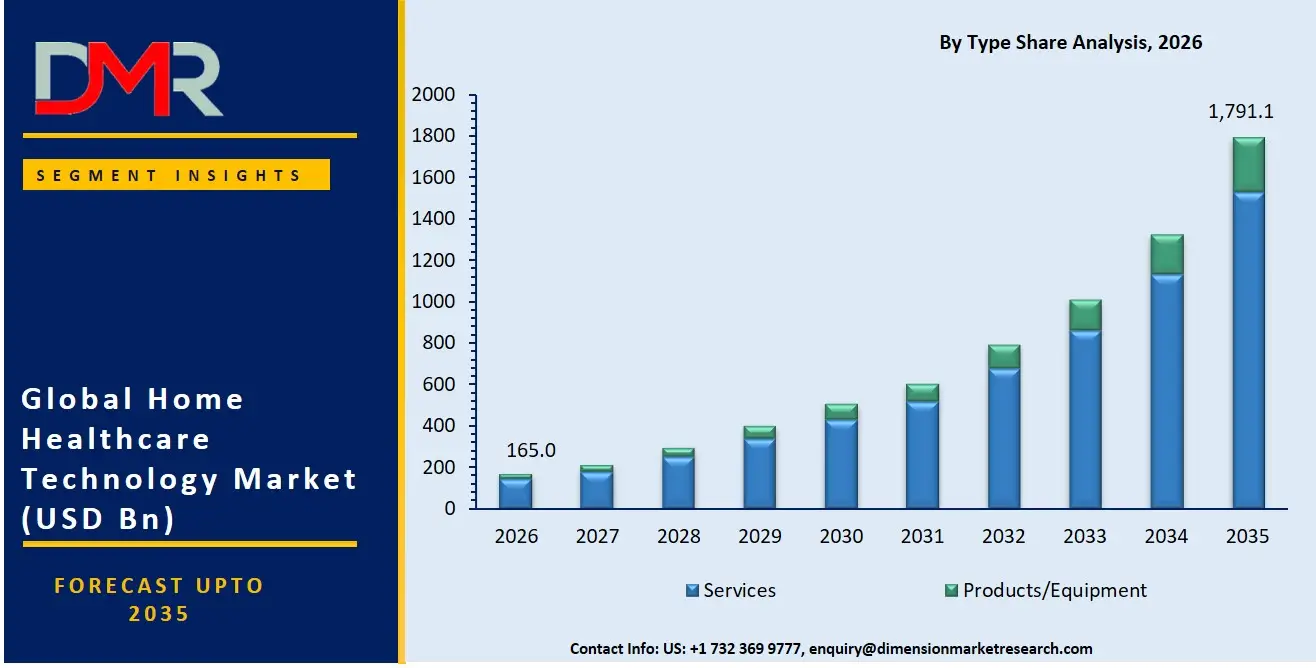

- The global Home Healthcare Technology Market is valued at USD 125.6 Billion in 2025, reached USD 165.0 Billion in 2026, and is projected to hit USD 1.79 Trillion by 2035 at a CAGR of 30.3%.

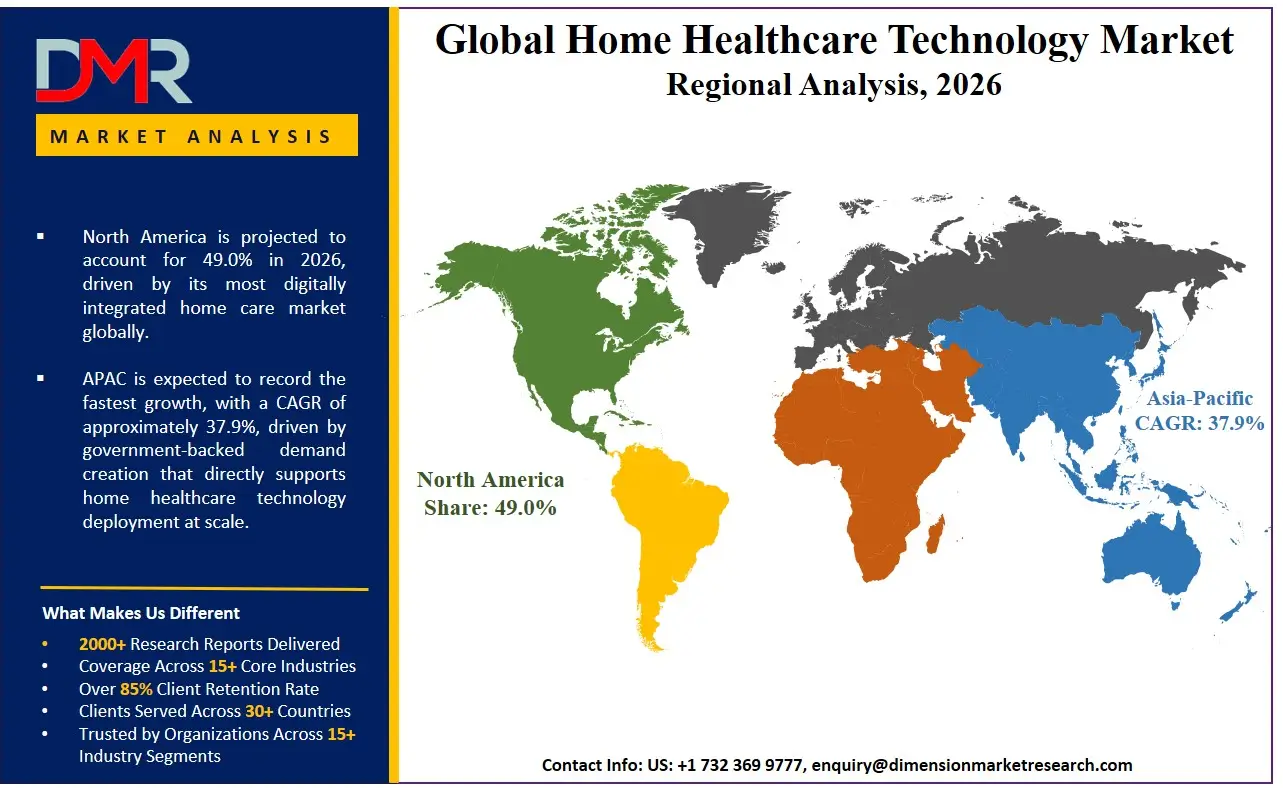

- North America holds the dominant regional position with a 49.0% revenue share in 2026, led by the United States.

- Services lead the By Type segment with an 85.2% revenue share in 2026.

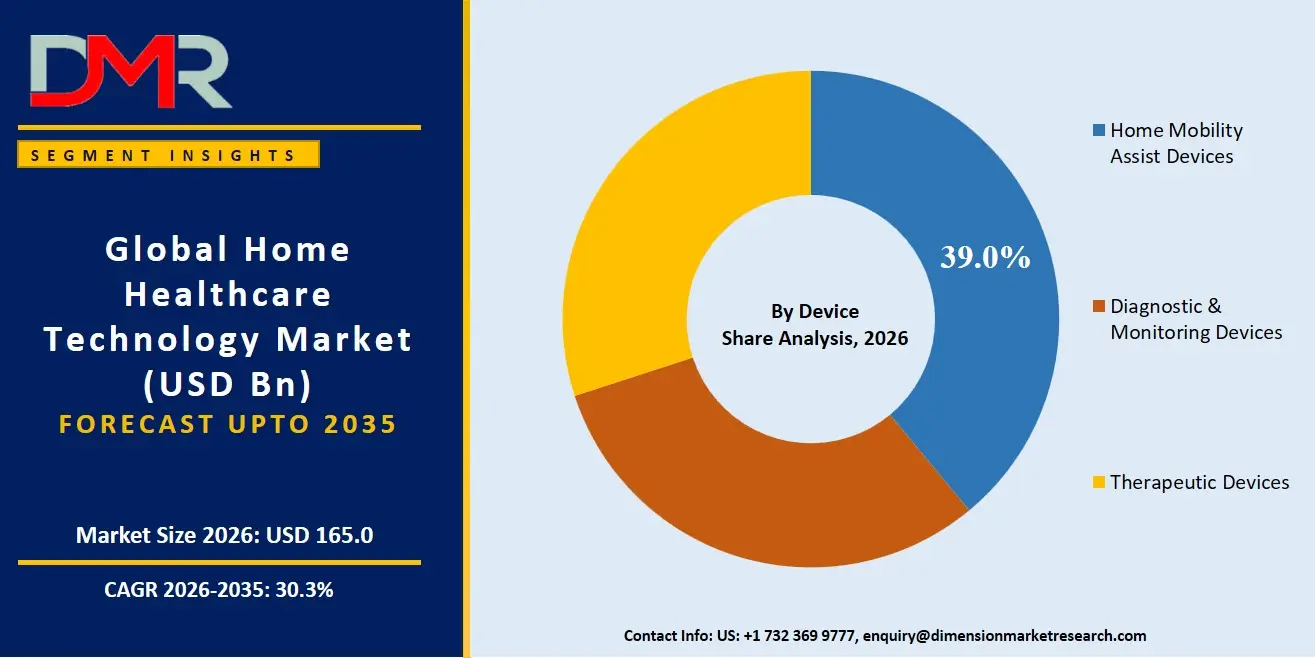

- Home Mobility Assist Devices leads the By Device segment with a 39.0% revenue share in 2026.

- Home Telehealth Monitoring Devices lead the By Telehealth Type segment with a 52.3% revenue share in 2026.

- Clinical Management Systems leads the By Software segment with a 46.5% revenue share in 2026.

- Cardiovascular Disorder and Hypertension lead the By Indication segment with a 26.12% revenue share in 2026.

- Skilled Nursing Care leads the By Service segment with a 48.5% revenue share in 2026.

- The U.S. market is valued at USD 56.6 billion in 2026 and is projected to reach USD 668.7 billion by 2035 at a CAGR of 28.4%.

Market Overview

The Home Healthcare Technology Market covers the full ecosystem of devices, services, software, and telehealth solutions delivered to patients in a home setting. Mobility assist devices, diagnostic tools, therapeutic equipment, skilled nursing services, remote patient monitoring platforms, and clinical management software all fall within its scope. Inpatient hospital services, institutional long-term care, and pharmaceutical manufacturing sit outside this boundary.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Home Healthcare Technology Market sits at the intersection of digital health, medical devices, and home-based care delivery. As healthcare systems shift spend toward lower-cost, outcome-driven models, home-based technology becomes a structural alternative to hospital admission. Budget implications flow directly to payers, providers, and device makers. Based on data from the HRSA State of the Health Workforce Report 2024, approximately 75 million people in the U.S. lived in a primary care Health Professional Shortage Area as of June 2024. For investors, that figure marks the addressable population for whom home healthcare technology is the primary care channel, not a supplementary option.

Data published by McKnight's Home Care confirms that U.S. home healthcare employment exceeded 1.7 million workers in May 2024, a rise of more than 9.5% versus May 2023. A workforce of this scale signals that service delivery infrastructure is being built in parallel with the technology layer. Both conditions must exist simultaneously for market scale-up to occur. As reported by Innolitics, FDA cleared 295 AI/ML-enabled medical devices in 2025, a record annual total, up from 253 in 2024 and 221 in 2023. A sustained acceleration in regulatory throughput directly expands the addressable product set for home-based care platforms, creating a broader device pipeline than any prior period in Home Healthcare Technology Market's history.

Market Size and Forecast

The Global Home Healthcare Technology Market size is estimated at USD 165.0 Billion in 2026 from USD 125.6 Billion in 2025, and is projected to reach USD 1.79 Trillion by 2035, exhibiting a CAGR of 30.3% during the forecast period.

A CAGR of 30.3% reflects structural market formation rather than organic expansion. Services already account for 85.2% of revenue in 2026, meaning any growth scenario must be assessed primarily through service volume expansion, not device unit sales. The forecast assumes sustained policy support, specifically the CMS Acute Hospital Care at Home waiver extended through September 30, 2030 under the Consolidated Appropriations Act of 2026, combined with continued AI device clearance throughput and telehealth adoption at scale. Each of these assumptions is policy-anchored, not speculative.

The U.S. market follows a more conservative path, forecast to reach USD 668.7 Billion by 2035 from USD 56.6 Billion in 2026 at a CAGR of 28.4%. The gap between the U.S. CAGR of 28.4% and the global CAGR of 30.3% tells a clear story. Growth leadership sits outside North America, in markets where structural build-out is still early. An upside scenario becomes credible if the AHCAH waiver program scales beyond its current approved hospital base and if RPM users reach the projected 115.5 million globally by 2027. A downside scenario centers on workflow integration failure. Peer-reviewed research published in 2026 identified data overload, ambiguous clinical responsibility, and poor EHR integration as the three core adoption blockers for remote patient monitoring, per PMC. If these barriers persist at scale, service utilization rates will lag device deployment and compress revenue per patient below forecast assumptions.

Market Dynamics

Federal Policy Certainty and AI Device Volume Expand the Commercial Base for Home-Based Acute Care

Congress extended the CMS Acute Hospital Care at Home waiver through September 30, 2030 under the Consolidated Appropriations Act of 2026. As of September 2025, 419 hospitals across 39 states held approved waivers, and 48,500 patients had been served under the program since November 2020, as confirmed by the AHA. A five-year reimbursement certainty window gives hospital systems the planning horizon needed to commit capital to home care infrastructure. Reimbursement certainty converts intent into budgeted investment.

FDA cleared a record 295 AI/ML-enabled medical devices in 2025, up from 253 in 2024 and 221 in 2023, as reported by Innolitics. This sustained clearance acceleration directly expands the qualified product set available to home care platforms. For market participants, a deeper cleared product pipeline means more procurement options, faster technology refresh cycles, and a broader clinical use case footprint than was commercially accessible in prior years.

Clinical Workflow Fragmentation and Retail Channel Failure Constrain Platform Scaling

Peer-reviewed research published in 2026 identified data overload, ambiguous clinical responsibility, and poor EHR integration as the three core adoption blockers for remote patient monitoring, per PMC. These are not technical problems that a software update resolves. They reflect deep workflow misalignment between home monitoring platforms and clinical decision-making structures. Until this integration gap closes, RPM device deployment will consistently outpace actual clinical utilization.

Best Buy Health divested its at-home technology acquisition back to the original founder in June 2025 following reported losses. This exit confirms that consumer-facing distribution models for home healthcare technology cannot sustain profitability without clinical integration. Retail channels lack payer contracting, clinical workflow embedding, and reimbursement access. Vendors who entered Home Healthcare Technology Market through consumer retail now face a complete channel rebuild to reach viable commercial scale.

AHCAH Clinical Evidence, FDA Software Guidance, and Emerging Market Demand Create Defined Expansion Pathways

A CMS study of the AHCAH initiative found beneficiaries receiving acute care at home had lower mortality rates than inpatient counterparts, per CMS. Lower mortality data embedded in federal policy creates a clinical evidence anchor that technology vendors can use directly in contract negotiations with health systems. Clinical outcomes data backed by CMS carries procurement weight that vendor-generated case studies cannot replicate.

FDA's January 6, 2025 Draft Guidance on AI-Enabled Device Software Functions, combined with the December 2024 Final Predetermined Change Control Plan Guidance, creates a formal lifecycle management pathway for software-enabled home monitoring devices. Vendors building AI-driven platforms can now update software without full re-review, compressing the product iteration cycle materially. The Philips and Medtronic February 2025 Memorandum of Understanding to train more than 300 cardiologists and radiologists in India on advanced imaging opens a clinician upskilling channel in one of Asia Pacific's highest-growth home healthcare markets. Clinician training at this scale creates a demand pull that device and platform vendors can follow with direct market entry.

Market Trends

Radiology AI Concentration, Transparency Standards, and Protocol-Driven RPM Frameworks Are Redefining Home Care Technology Deployment

Radiology-led AI software now dominates the home and ambulatory device pipeline. As reported by Intuition Labs, 81% of FDA's July 2025 AI-enabled device update covering 211 listings since September 2024 comprised radiology software. For early movers, this concentration signals that imaging-adjacent home monitoring capabilities represent the highest-volume product category for FDA-cleared AI deployment in home care. Vendors building outside radiology-adjacent use cases face a thinner cleared product pipeline and a narrower procurement window.

FDA's June 2024 Guiding Principles on Transparency for Machine Learning-Enabled Medical Devices establish a design-phase compliance expectation for connected home devices. FDA cleared DeepRhythmAI in December 2025 for remote cardiac monitoring and Empatica's EmbraceMini for neurology-focused home wearable use, extending AI-cleared home monitoring into cardiovascular and neurological indication categories simultaneously. Vendors who embed transparency documentation into product development rather than retrofitting it will face lower regulatory friction and faster buyer acceptance from risk-averse health systems and payers.

Procurement models and care delivery frameworks are shifting in parallel. Bundled monitoring-plus-consumables models are emerging as a revenue architecture that locks in recurring spend. Protocol-driven tiered-escalation RPM models are also emerging as the preferred care delivery framework, per a January 2026 PMC Narrative Review on Remote Patient Monitoring Care Delivery. Vendors who align product design and service contracts to structured escalation protocols will secure preferred-vendor positioning before the framework becomes a universal procurement requirement.

Type Analysis

Services leads the segment with an 85.2% share, reflecting a market where recurring care delivery generates far more commercial value than one-time device transactions. Skilled nursing, telehealth, and infusion therapy contracts structurally outperform equipment margins. Investors evaluating Home Healthcare Technology Market must assess service volume growth as the primary revenue driver, not device unit shipments.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Products and Equipment serves as the enabling hardware layer for service delivery. Its minority revenue position confirms that device sales alone do not build a defensible business in Home Healthcare Technology Market. Equipment vendors without an attached service contract or subscription model face margin compression as service providers bundle devices into recurring care offerings to retain patients and payers.

Device Analysis

Home Mobility Assist Devices leads the segment with a 39.0% share, reflecting the broadest patient population in home care. Mobility impairment spans cardiovascular disease, neurological disorders, and post-surgical recovery simultaneously. Broad clinical utility across multiple chronic conditions translates directly into volume leadership that single-indication device categories cannot match.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Diagnostic and Monitoring Devices represent the fastest-escalating category in clinical relevance. Remote monitoring of chronic conditions, including continuous glucose monitoring and cardiovascular tracking, depends entirely on this device class. Therapeutic Devices serve patients managing active treatment outside clinical settings, with demand growing directly alongside hospital-at-home program expansion as inpatient-level care shifts into the home setting.

Telehealth Type Analysis

Home Telehealth Monitoring Devices accounts for 52.3% of the segment, driven by chronic disease management volume requiring continuous patient data streams. Cardiovascular disorders, diabetes, and COPD each require ongoing physiological data capture that only monitoring hardware can provide at the frequency and fidelity clinical decision-making requires. Monitoring devices anchor the telehealth revenue structure in home care settings before services or software enter the commercial equation.

Home Telehealth Services deliver the clinical interaction layer on top of monitoring data, operating across a distribution channel that is already structurally embedded across U.S. hospital networks. Home Telehealth Software manages care coordination, data routing, and clinical decision support across the monitoring and service layers. FDA's January 6, 2025 Draft Guidance on AI-Enabled Device Software Functions creates a formal compliance pathway specifically for software functions in home-based monitoring, reducing product development risk and accelerating payer approval cycles for vendors operating in this layer.

Software Analysis

With a 46.5% share, Clinical Management Systems holds the strongest position due to provider-facing care coordination necessity at scale. Health systems managing hundreds of AHCAH-approved hospitals and complex home care workflows require integrated tools that connect clinical documentation, care scheduling, and compliance reporting into a single operational layer. Clinical management software becomes non-negotiable infrastructure before any other software category reaches procurement priority.

Agency Software supports home health agencies in scheduling, billing, compliance, and caregiver management across a structurally expanding user base. In August 2025, UnitedHealth Group agreed to divest 164 hospice and home health locations to resolve antitrust concerns over its USD 3.3 Billion acquisition of Amedisys. New operators taking over divested locations require purpose-built technology solutions to replace incumbent platforms, creating a direct near-term demand catalyst for agency and hospice software vendors. Hospice Solutions address end-of-life care coordination within home-based palliative settings, serving a patient population whose care complexity generates proportionally high software utilization per episode.

Indication Analysis

Cardiovascular Disorder and Hypertension leads with a 26.12% share, reflecting the highest-frequency chronic disease use case for remote patient monitoring. Continuous blood pressure, heart rhythm, and ECG data requirements make cardiovascular patients the most device-intensive indication group in home care. FDA clearance for DeepRhythmAI in December 2025 confirms active product development in remote cardiovascular AI tools, extending the cleared device pipeline for this dominant indication.

Diabetes and Kidney Disorders represent the second highest-volume indication group, with home-use CGM systems already generating multi-billion-dollar revenue streams. Respiratory Disease and COPD patients require ongoing oxygen therapy and medication adherence support, with demand expanding beyond chronic disease maintenance into acute episode management as hospital-at-home programs absorb respiratory cases previously requiring inpatient admission. Neurological and Mental Disorders are entering commercialization as a category, with Empatica's EmbraceMini receiving FDA 510(k) clearance in December 2025 for neurology-focused home wearable monitoring. Cancer patients increasingly receive treatment-adjacent monitoring at home, while Wound Care, Mobility Disorders, and Maternal Disorders each serve defined patient populations whose care complexity sustains recurring service and device revenue across the forecast period.

Service Analysis

Skilled Nursing Care captures 48.5% of segment demand, as licensed professional delivery creates a structural barrier that keeps this service category both high-value and high-margin. As reported by McKnight's Home Care, U.S. home healthcare employment exceeded 1.7 million workers in May 2024, up more than 9.5% year-over-year. Workforce supply at this scale provides the licensed delivery capacity that sustains dominant service volume without creating near-term capacity constraints.

Rehabilitation Therapy demand expands beyond post-discharge maintenance into active recovery as the AHCAH waiver shifts acute inpatient recovery into home settings, elevating the billing rate potential of this sub-segment. A 2023 clinician survey confirmed 45% of providers were already using RPM for acute monitoring including hospital-at-home, with 77% predicting broader RPM use, per Intuition Labs, signaling that Telehealth Services will absorb a growing share of care episodes previously handled through in-person skilled nursing visits. Infusion Therapy, Respiratory Therapy, and Unskilled Homecare each serve defined care populations, with Infusion Therapy's reimbursable patient pool expanding directly alongside the AHCAH program's 2030 extension and Unskilled Homecare facing the strongest margin pressure from labor commoditization among all service sub-segments.

Key Market Segments

By Type

- Services

- Products / Equipment

By Device

- Home Mobility Assist Devices

- Diagnostic and Monitoring Devices

- Therapeutic Devices

By Telehealth Type

- Home Telehealth Monitoring Devices

- Home Telehealth Services

- Home Telehealth Software

By Software

- Clinical Management Systems

- Agency Software

- Hospice Solutions

By Indication

- Cardiovascular Disorder and Hypertension

- Diabetes and Kidney Disorders

- Respiratory Disease and COPD

- Neurological and Mental Disorders

- Cancer

- Wound Care

- Mobility Disorders

- Maternal Disorders

By Service

- Skilled Nursing Care

- Rehabilitation Therapy

- Telehealth Services

- Infusion Therapy

- Respiratory Therapy

- Unskilled Homecare

Regional Analysis

North America held a dominant position in 2026 with a 49.0% revenue share of the global Home Healthcare Technology Market, anchored by the United States. Approximately 75% of U.S. hospitals adopted telehealth by 2024, per PMC, making North America the most digitally integrated home care market globally. The CMS AHCAH waiver extension through 2030, combined with the deepest AI-cleared device pipeline of any region, creates a structural procurement environment that no other geography currently replicates in density or policy certainty.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Asia Pacific represents the highest-growth opportunity region outside North America. NITI Aayog's 2024 Senior Care Reforms Position Paper calls for expanded tele-consultation, geriatric workforce capacity, and elderly-friendly housing, establishing government-backed demand creation that directly supports home healthcare technology deployment at scale. NHS England targets approximately 24,000 virtual ward beds across UK NHS Trusts, each supported by remote monitoring platforms, with UK virtual ward density reaching approximately 20 virtual ward beds per 100,000 population in 2024-2025, per JMIR. Europe's government-mandated build-out creates a durable procurement pipeline that commercial technology vendors can plan against with multi-year visibility. Latin America remains an early-stage market where affordability constraints at the device level will limit premium product penetration in the near term. The Middle East and Africa region presents concentrated opportunity in GCC states, where high per-capita healthcare spend supports chronic disease monitoring adoption, while sub-Saharan Africa remains a data-limited territory for near-term investment forecasting.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Competitive Landscape

The Home Healthcare Technology Market is moderately consolidated at the technology platform level but fragmented at the service delivery level. Large medical technology companies backed by multi-billion-dollar product portfolios and multi-year payer contracts dominate remote monitoring hardware and software. Home health service delivery remains distributed across thousands of regional agencies and providers. Competitive positioning at the platform level depends on FDA clearance depth, payer contract coverage, and clinical workflow integration rather than product breadth alone.

The July 2025 multi-year strategic partnership between Medtronic and Koninklijke Philips N.V. to integrate Nellcor, Microstream, and BIS technologies into Philips monitoring systems directly consolidates two previously independent competitive offerings into one bundled monitoring platform. Partnerships of this scale raise the competitive bar for all remaining independent monitoring vendors who cannot match the combined clinical coverage of an integrated ecosystem. Vendors who lock in multi-technology integration simultaneously raise the switching cost for buyers significantly.

Portfolio rationalization is reshaping the competitive structure from within. One major diversified healthcare player completed a USD 3.8 Billion divestiture of its kidney care unit in 2024 to concentrate on connected monitoring systems. These moves signal that market participants are concentrating resources into segments where they hold structural advantage rather than maintaining broad portfolio coverage that dilutes execution focus. Sprinter Health raised USD 55 Million in a Series B in May 2025, led by General Catalyst with participation from Andreessen Horowitz, Google Ventures, and Accel, to expand at-home preventative services across 18 U.S. states. Venture-backed challengers are targeting service-layer white space that incumbent hardware companies do not serve, creating parallel competitive pressure that the traditional device market structure does not fully capture.

Company Profiles

Honeywell International Inc. positions itself in home healthcare technology through building automation, connected sensor infrastructure, and remote monitoring integration capabilities. Its advantage lies in applying industrial-grade sensor and connectivity technology to clinical home environments, a cross-sector capability that pure medical device companies cannot replicate. Honeywell's primary risk is clinical credibility. Payers and health systems prioritize FDA-cleared medical device vendors over industrial technology companies entering the care delivery space without a deep regulatory clearance history.

Koninklijke Philips N.V. anchors its home healthcare position through the Connected Care segment, which generated approximately EUR 3.5 Billion (4.0 Billion) in annual revenue in 2024, with 58% from hospital and home patient monitoring, as reported by Philips. Q4 2025 adjusted EBITA margin improved 150 basis points to 16.5%, confirming that the July 2025 Medtronic integration strategy is delivering measurable commercial returns alongside clinical benefits. Philips enters the next phase of the forecast period with a bundled monitoring ecosystem that competitors cannot replicate quickly and a margin trajectory that validates the integration investment thesis.

Key Players

- Honeywell International Inc.

- Siemens Healthineers

- Koninklijke Philips N.V.

- Qualcomm Incorporated

- Schneider Electric

- GE HealthCare

- ResMed

- Becton, Dickinson and Company

- Medline Industries, Inc.

- Arkray, Inc.

- McKesson Medical-Surgical Inc.

- Fresenius Medical Care AG

- Medtronic plc

- Baxter International Inc.

- B. Braun Melsungen AG

- F. Hoffmann-La Roche AG

- 3M Healthcare (Solventum)

- ConvaTec Group PLC

- Hollister Inc.

- Mölnlycke Health Care

Supply Chain and Value Chain Analysis

The Home Healthcare Technology supply chain flows from component manufacturers, including sensor producers, semiconductor suppliers, battery systems, and wound care raw material providers, through medical device OEMs and software developers, into distribution networks, and finally to service providers and end patients. Maximum commercial value concentrates at the service delivery layer, not the device manufacturing stage. Services account for 85.2% of total market revenue, meaning device manufacturers who supply into Home Healthcare Technology Market without capturing service revenue through subscription or bundled care contracts operate in the lower-value tier of the chain regardless of product quality.

The biggest supply chain bottleneck sits at the clinical integration point rather than at any physical logistics node. Poor EHR integration identified as a core adoption blocker by peer-reviewed research means that vendors who control the EHR connectivity layer hold structural pricing power over device manufacturers and service providers who depend on their data architecture to activate clinical workflows. FDA regulatory clearance functions as a supply chain gate for the technology layer, with clearance concentration among a qualified vendor shortlist meaning the effective supply base for AI-enabled home monitoring is narrower than the total number of competing products suggests. Distribution channel control has shifted decisively toward payer-contracted and clinically embedded networks. The retail distribution model failed conclusively in June 2025, confirming that home healthcare technology cannot be sold through consumer retail channels at sustainable margins and that payer contracting and health system partnerships represent the only commercially proven distribution pathways.

Regulatory Landscape

The most consequential regulatory development in Home Healthcare Technology Market is the extension of the CMS Acute Hospital Care at Home waiver through September 30, 2030 under the Consolidated Appropriations Act of 2026. This policy extension converts a temporary waiver into a medium-term reimbursement framework, giving technology vendors a five-year procurement planning window tied directly to hospital-at-home program investment. Non-participation in AHCAH-compatible platform development now carries a direct commercial cost as health system procurement decisions align to the 2030 policy horizon.

FDA's AI/ML device clearance pipeline has become a primary commercial gating mechanism. As reported by Innolitics, 38 manufacturers secured two or more 510(k) AI/ML clearances in 2024, confirming that the cleared supplier pool is selective and that repeat-clearance firms hold a structural procurement advantage over first-time filers. Vendors without existing 510(k) clearances face an access barrier to health system procurement that regulatory status alone determines. FDA issued two pivotal AI software governance documents that reshape product development obligations directly. The January 6, 2025 Draft Guidance on AI-Enabled Device Software Functions and the December 2024 Final Predetermined Change Control Plan Guidance establish a formal lifecycle management framework. Software vendors updating AI algorithms in home monitoring devices must now design change control documentation into their development process or face re-clearance requirements that add significant time and cost to each product iteration cycle.

NHS England's virtual ward program targeting approximately 24,000 virtual ward beds across NHS Trusts operates under MHRA medical device oversight. For vendors seeking cross-border market entry into the UK alongside the U.S., compliance with both FDA and MHRA frameworks creates a parallel regulatory burden that structurally favors large established device manufacturers over smaller specialized entrants. FDA's June 2024 Guiding Principles on Transparency for Machine Learning-Enabled Medical Devices set a design-phase compliance standard for connected home care products that vendors cannot retrofit cost-effectively after product launch.

Investment and White Space Analysis

Active investment is flowing into AI-driven home care platforms and at-home preventative services with institutional conviction. In January 2025, Cera raised USD 150 Million in debt and equity led by BDT and MSD Partners and Schroders Capital to scale its AI-driven home healthcare platform across the UK market. In March 2025, Junction raised USD 18 Million to expand its API connecting labs with more than 500 wearable devices, enabling at-home health data integration across disparate monitoring platforms. These two rounds address opposite ends of the value chain: Cera at the service delivery layer, Junction at the interoperability infrastructure layer that every other vendor depends on.

Medical imaging and home-adjacent software represent a second concentration of capital at larger transaction scale. GE HealthCare announced the acquisition of Intelerad, a medical imaging software provider, for USD 2.3 Billion in cash in November 2025, with closing expected in H1 2026. Large-cap medtech companies are expanding from hardware into software-defined care models. Ambulatory and home imaging software sits at the highest-activity zone of current M&A spend, making it the most competitive white space for new entrants to navigate.

India's home healthcare market was estimated at a USD 5.4 Billion baseline growing at 19% CAGR, projected to reach USD 19.9 Billion, per NATHEALTH. The domestic supply chain technology infrastructure supporting Home Healthcare Technology Market remains underdeveloped relative to its output scale, while simultaneous policy push from NITI Aayog and industry investment from global medtech firms create the dual condition required for home healthcare technology scale-up in an emerging economy. At-home oncology care represents a smaller but structurally significant white space. Luminate closed a USD 15 Million Series A in September 2024 to develop at-home cancer care capabilities including a scalp-cooling chemo helmet. Cancer accounts for a distinct indication segment in Home Healthcare Technology Market, but at-home active treatment tools remain scarce relative to patient volume, making early positioning commercially advantageous before reimbursement pathways standardize.

Recent Developments

- November 2025: GE HealthCare. Acquisition announced. GE HealthCare announced its acquisition of medical imaging software provider Intelerad for USD 2.3 Billion in cash to expand into outpatient and home-adjacent care, with closing expected in H1 2026.

- May 2025: Sprinter Health. Funding round. Sprinter Health raised USD 55 Million in a Series B led by General Catalyst, with participation from Andreessen Horowitz, Google Ventures, and Accel, to expand at-home preventative healthcare services across 18 U.S. states.

- March 2025: Junction. Funding round. Junction raised USD 18 Million to expand its API connecting labs with more than 500 wearable devices, enabling at-home health data integration across disparate monitoring platforms.

- January 2025: Cera. Funding round. Cera raised USD 150 Million in a mix of debt and equity led by BDT and MSD Partners and Schroders Capital to scale its AI-driven home healthcare platform, one of the largest single funding rounds for a home-based care technology platform in the European market.

- September 2024: Luminate. Series A closed. Luminate closed a USD 15 Million Series A led by Artis Ventures, with participation from Metaplanet, 8VC, SciFounders, Faber, and Lachy Groom, to advance its scalp-cooling chemo helmet and at-home cancer care capabilities.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 125.6 Billion |

| Market Value (2026) |

USD 165.0 Billion |

| Forecast Revenue (2035) |

USD 1.79 Trillion |

| CAGR (2026 to 2035) |

30.3% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020 to 2024 |

| Forecast Period |

2026 to 2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Type (Services, Products/Equipment), By Device (Home Mobility Assist Devices, Diagnostic and Monitoring Devices, Therapeutic Devices), By Telehealth Type (Home Telehealth Monitoring Devices, Home Telehealth Services, Home Telehealth Software), By Software (Clinical Management Systems, Agency Software, Hospice Solutions), By Indication (Cardiovascular Disorder and Hypertension, Diabetes and Kidney Disorders, Respiratory Disease and COPD, Neurological and Mental Disorders, Cancer, Wound Care, Mobility Disorders, Maternal Disorders), By Service (Skilled Nursing Care, Rehabilitation Therapy, Telehealth Services, Infusion Therapy, Respiratory Therapy, Unskilled Homecare) |

| Regional Analysis |

North America – US and Canada; Europe – Germany, France, The UK, Spain, Italy, and Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, and Rest of APAC; Latin America – Brazil, Mexico, and Rest of Latin America; Middle East & Africa – GCC, South Africa, and Rest of MEA |

| Competitive Landscape |

Honeywell International Inc., Siemens Healthineers, Koninklijke Philips N.V., Qualcomm Incorporated, Schneider Electric, GE HealthCare, ResMed, Becton Dickinson and Company, Medline Industries Inc., Arkray Inc., McKesson Medical-Surgical Inc., Fresenius Medical Care AG, Medtronic plc, Baxter International Inc., B. Braun Melsungen AG, F. Hoffmann-La Roche AG, 3M Healthcare (Solventum), ConvaTec Group PLC, Hollister Inc., Mölnlycke Health Care |

| Customization Scope |

Customization for segments and region or country level will be provided. Additional customization can be done based on requirements. |

| Purchase Options |

Three license options: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |

Frequently Asked Questions

What is the biggest investment opportunity in Home Healthcare Technology Market?

▾ The market expands from USD 125.6 Billion in 2025 to USD 1.79 Trillion by 2035. The clearest white space lies in wearable device interoperability infrastructure, AI-native home care platforms for underserved mid-size providers, and at-home oncology tools. All three address documented gaps that current market offerings do not fully cover at commercial scale.

Who are the top companies in Home Healthcare Technology Market?

▾ Key players include Honeywell International Inc., Siemens Healthineers, Koninklijke Philips N.V., Qualcomm Incorporated, GE HealthCare, Medtronic plc, ResMed, Baxter International Inc., Fresenius Medical Care AG, and F. Hoffmann-La Roche AG, among others. Koninklijke Philips N.V. anchors its position through a Connected Care segment generating approximately €3.5 Billion in annual revenue with 58% from hospital and home patient monitoring.

Which segment is growing fastest in Home Healthcare Technology Market and why?

▾ Diagnostic and Monitoring Devices represent the fastest-escalating device category as AI-cleared home monitoring hardware becomes standard in remote care protocols. Cloud-based telehealth software and protocol-driven RPM platforms are accelerating adoption among mid-size and decentralized health systems that require rapid compliance updates and AI-integrated analytics without the infrastructure cost of on-premise deployments.

Which region is growing fastest in Home Healthcare Technology Market and why?

▾ Asia Pacific is the fastest-expanding regional block, driven by India's home healthcare market estimated at a USD 5.4 Billion baseline growing at 19% CAGR. Government policy from NITI Aayog and simultaneous industry investment from global medtech firms are creating the dual conditions required for home healthcare technology scale-up in one of the world's largest underserved care markets.

What is the biggest challenge holding Home Healthcare Technology Market back?

▾ Clinical workflow integration failure is the most immediate structural constraint. Peer-reviewed research published in 2026 identified data overload, ambiguous clinical responsibility, and poor EHR integration as the three core adoption blockers for remote patient monitoring, per PMC. Until platforms resolve this integration gap, RPM device deployment will consistently outpace actual clinical utilization and compress revenue per patient below forecast assumptions.