What is the Hyperscale Data Center Market Size?

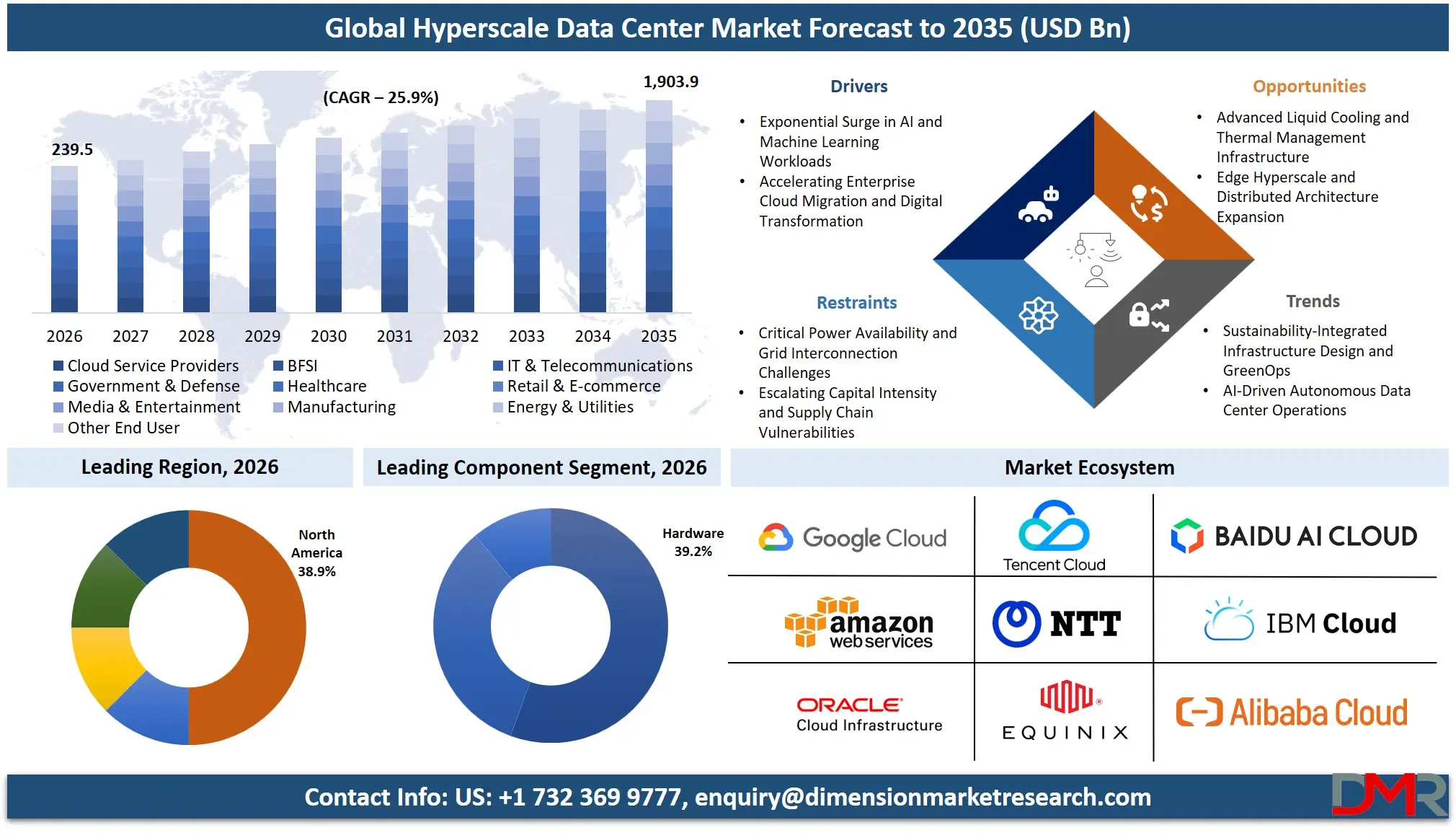

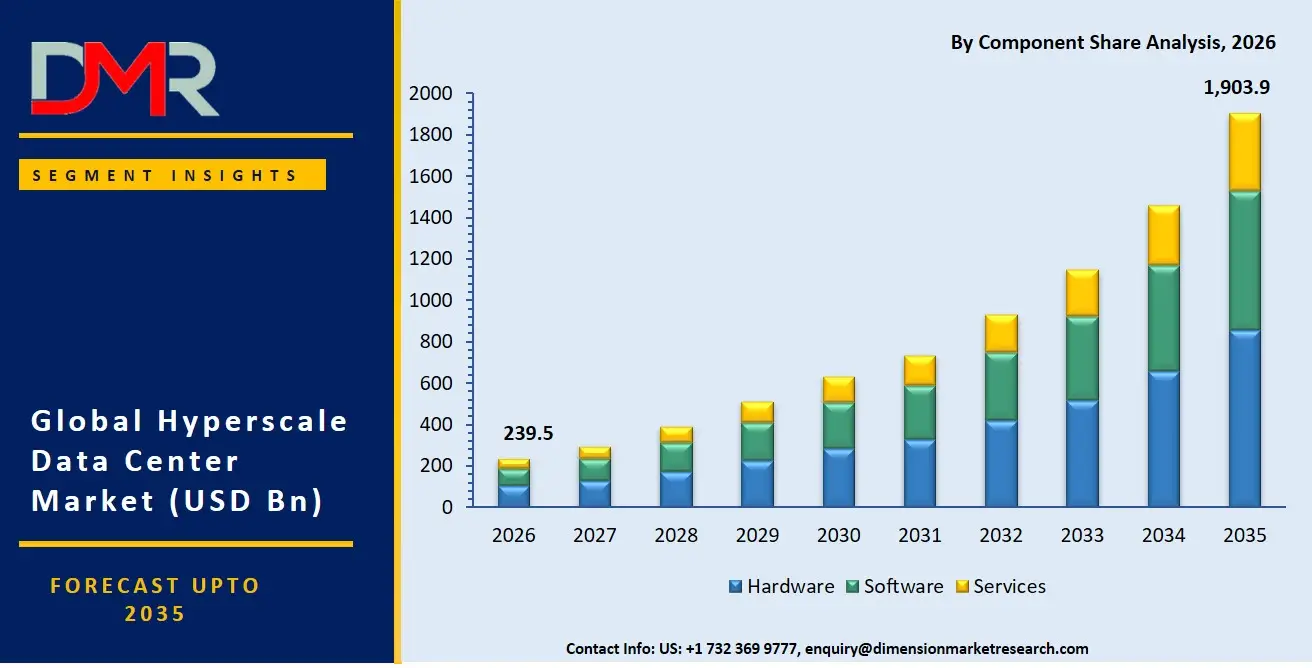

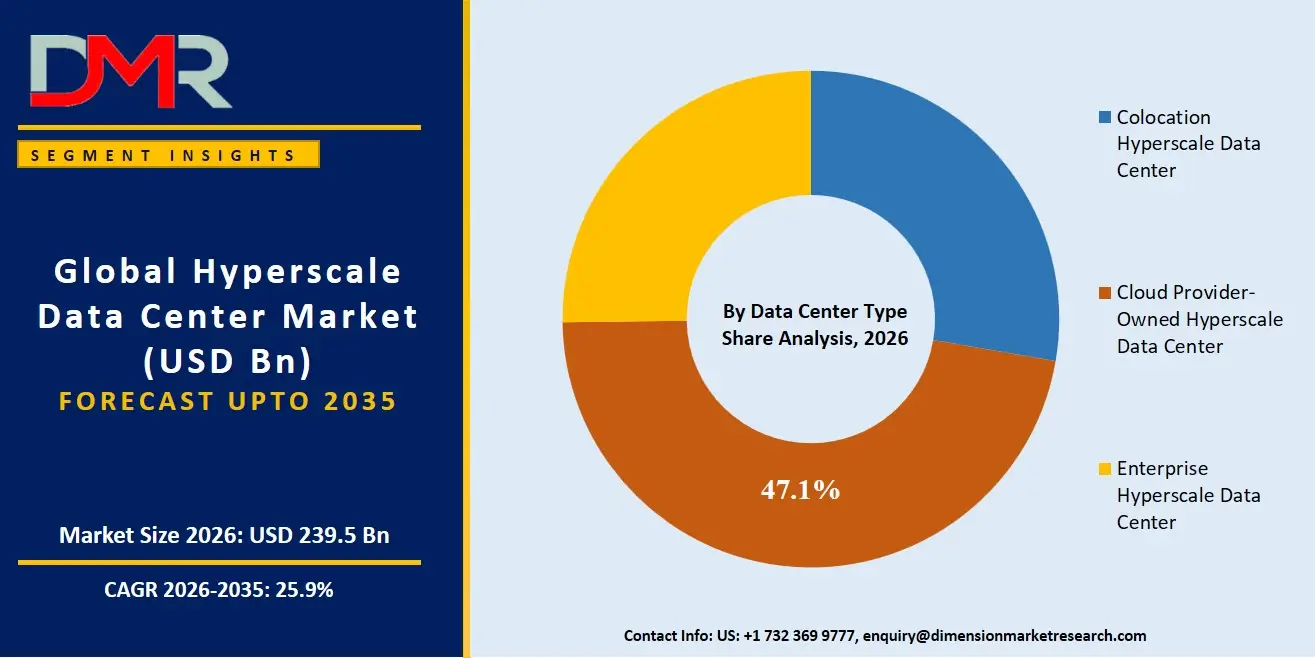

The Global Hyperscale Data Center Market is expected to reach a value of USD 239.5 billion in 2026, and it is further anticipated to reach USD 1,903.9 billion by 2035, growing at a CAGR of 25.9% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

There has been remarkable growth within the hyperscale data center market as organizations and CSPs speed up their digital transformation efforts while expanding their infrastructure presence worldwide. It consists of hardware elements such as electrical infrastructure, IT infrastructure, and mechanical infrastructure, along with software elements for management and monitoring purposes. Hyperscale data centers refer to huge-scale data centers created to provide scalable computing capacity through efficient, automated, and resilient infrastructure solutions with power consumption exceeding 10 MW. There is a rise in the need for hyperscale infrastructure as a result of the growing popularity of cloud computing, artificial intelligence, big data, and CDN services, which would require a large number of servers working together. The main users of hyperscale data centers continue to be CSPs, particularly those operating hybrid or public clouds because of their cost-saving features.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

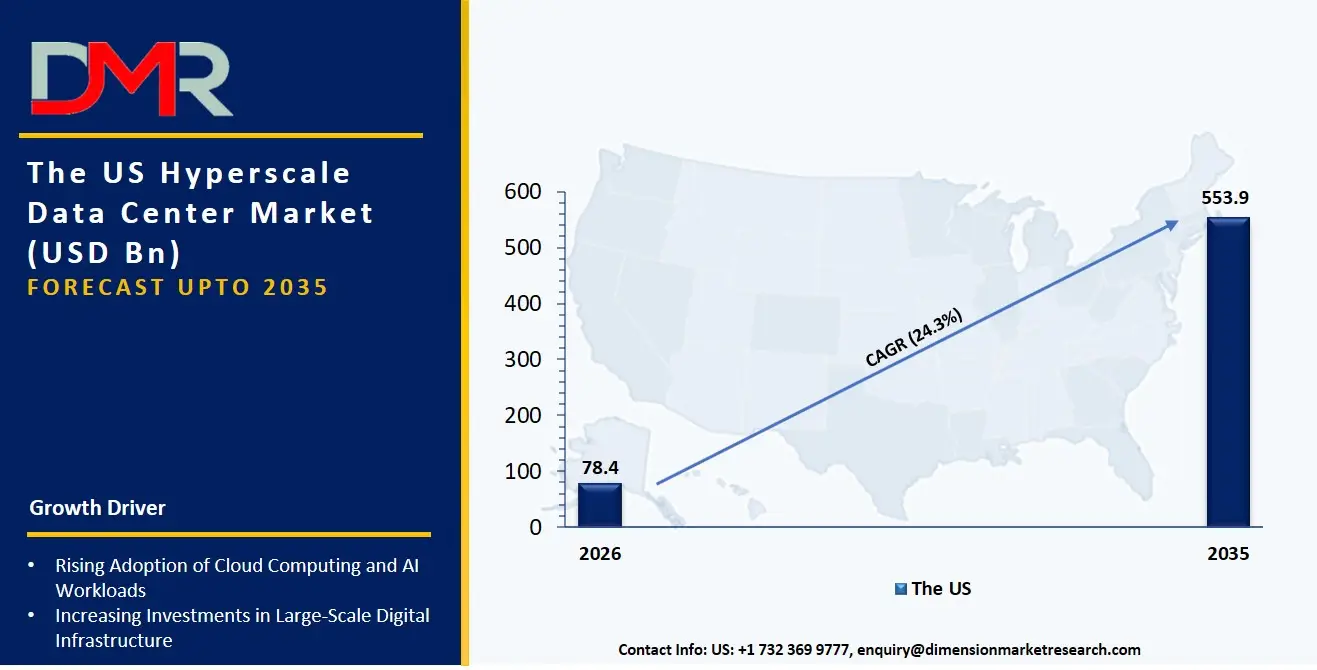

The US Hyperscale Data Center Market

The US Hyperscale Data Center Market is projected to reach USD 78.4 billion in 2026 at a compound annual growth rate of 24.3% over its forecast period by 2035. The US remains to be the largest and most advanced market in terms of hyperscale data centers due to the highly aggressive expansion plans being undertaken by top cloud service providers as well as the increasing presence of such facilities in strategic locations like Northern Virginia, Silicon Valley, Phoenix, and Dallas. The market has been marked by extremely high demand for IT infrastructure parts with the areas of server and network infrastructure receiving notable investments owing to the integration of AI-enabled hardware architecture designs by organizations. In addition, there has been an emerging high need for high-density electrical power infrastructure driven by the use of Generative AI training clusters that require the development of highly sophisticated UPS and PDUs with rack densities above 50-100kW.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Europe Hyperscale Data Center Market

The Europe Hyperscale Data Center Market is estimated to be valued at USD 67.5 billion in 2026 and is further anticipated to reach USD 523.6 billion by 2035 at a CAGR of 25.6%. The regulatory landscape, which comprises GDPR and the soon-to-be-introduced EU AI Act, has considerable influence on the European market and creates a demand for sovereign hyperscale infrastructure equipped with comprehensive security monitoring and data management systems that emphasize compliance. Growth in hybrid deployments is rapidly occurring in this region, as manufacturing and automotive sectors in Germany and France try to reconcile the needs of securing their operational technology with analytics from hyperscale deployments. Moreover, projects like GAIA-X present new demands for hyperscale operators, who must now create separate facilities within Europe to ensure data residency and compatibility, and thus must invest heavily in their mechanical infrastructure and highly efficient cooling systems.

The Japan Hyperscale Data Center Market

The Japan Hyperscale Data Center Market is projected to be valued at USD 15.1 billion in 2026 at a CAGR of 24.0%. Both the GDPR and the upcoming EU AI Act have a strong effect on the European market, and as a result, there is a need for a sovereign hyperscale infrastructure that is supported by security monitoring and management solutions focused on compliance. The growth of hybrid implementations in this region is fast-paced, as the manufacturing industry and automotive industry in Germany and France attempt to address both the requirement of security of operational technology and the use of analytics from hyperscale infrastructures. New projects such as GAIA-X have created new challenges for hyperscale companies, who now have to create different facilities in Europe in order to be able to support data residency, and hence, have had to make large investments into their mechanical infrastructure and cooling systems.

Key Takeaways

- Market Size & Forecast: According to projections, the Global Hyperscale Data Center market will be worth USD 239.5 billion by 2026 while growing drastically to USD 1,903.9 billion in value by 2035 due to the combined impact of rising enterprise adoption of AI technologies along with the mandate for scaling cloud infrastructure to cope with unprecedented data growth.

- Growth Rate & Outlook: Global market growth rate is estimated at a CAGR of 25.9% due to the enormous capital investment by hyperscale cloud providers, growing demand for edge computing solutions and high power densities that will require the development of novel electrical and mechanical infrastructures.

- Primary Growth Drivers: Key drivers include the migration of enterprises from their own data centers to cloud provider-owned hyperscale centers and colocation services, the requirement for efficient cooling solutions capable of handling AI workloads in excess of current thermal limits, as well as software-based management systems requiring additional capabilities.

- Key Market Trends: Growing market trends include the adoption of liquid and immersion cooling solutions for mechanical infrastructure, the utilization of AI solutions within infrastructure management software for automatic rectification of any problems, as well as the focus on sustainability for electrical infrastructure development.

- By Infrastructure Type Analysis: IT and electrical infrastructure are likely to see heavy investment, with the demand for advanced servers on the horizon driven by the increasing data gravity and intensive workload. There is an increasing need for mechanical infrastructure since the cooling system needs to be upgraded in response to high thermal loads posed by the deployment of AI accelerators, which go beyond typical CPU configurations.

- By Application Analysis: The applications with the highest gains are cloud computing and artificial intelligence, and machine learning owing to their immense need for computing and storage capabilities. The rapidly expanding categories include high-performance computing and big data analytics because of their applications in scientific analysis and financial calculations, as well as AI training.

- Regional Leadership: North America is predicted to lead the industry with 38.9% market share in 2026 owing to its advanced technological landscape and presence of hyperscale cloud service providers as well as energy infrastructure to facilitate the setting up of extensive data centers.

What is the Hyperscale Data Center?

Hyperscale data centers are large-scale data center architectures that are purposely designed to provide highly scalable computer systems that are capable of rapidly increasing their capacity to handle an ever-growing demand by containing hundreds of thousands of servers acting as one single entity. These structures, in contrast with the conventional enterprise data centers, are designed from scratch to achieve maximum efficiency, automation, and elasticity. Software platforms incorporate infrastructure management platforms aimed at resource optimization, cloud management platforms for managing workflows, and operational software dealing with data management and backup/disaster recovery purposes. Cloud services companies operate thousands of such facilities around the world which results in constant efforts towards hardware and software advancements that make massive investments into such infrastructure result in agility, not complexity.

Use Cases

- Hyperscale Training Facilities for AI Providers: Hyperscale training facilities with dedicated infrastructure comprising GPU and custom accelerators, along with liquid cooling and power distribution systems, are established by AI providers who need to build large-scale language models and other types of generative artificial intelligence using a lot of compute power.

- Global Content Delivery and Streaming Capabilities: Media and entertainment businesses use hyperscale colocation facilities with distributed network systems and edge computing to provide streaming services to millions of simultaneous users through the deployment of sophisticated performance management software and backup services.

- BFSI HPC Needs: The BFSI industry uses hyperscale facilities to enable real-time risk assessments, algorithmic trading, and fraud prevention, thereby relying on ultra-low latency networks, availability of electrical power infrastructure, and dedicated monitoring tools to comply with regulatory requirements.

- Sovereign Cloud Infrastructures for Governments: Enterprise-scale hyperscale data centers with physical security systems and cloud management software are set up by governments and defense organizations to ensure that they have sovereign control over their data, especially when they leverage artificial intelligence and big data applications.

How AI is Transforming the Hyperscale Data Center Market?

AI is revolutionizing the hyperscale data center industry through creating a unique need for custom hardware and, on the other hand, optimizing the operation of these facilities using advanced software. Workloads involving the use of AI create huge demands for GPU and other specialized accelerators, leading to the use of server infrastructure that requires much higher amounts of electricity compared to CPU servers, resulting in changes in the design of electrical infrastructure, such as high-capacity UPS and power distribution units able to handle power loads exceeding 100 kW per rack. Additionally, AI capabilities in infrastructure management and orchestration/automation software enable users to improve the effectiveness of cooling systems, anticipate hardware malfunctions, and automatically distribute workloads between different facilities for better energy efficiency.

Regarding mechanical infrastructure, the needs created by the emergence of AI involve innovations in both technologies and processes. Among them are direct-to-chip and immersion cooling systems used for efficient cooling of hardware whose heat dissipation requirements exceed the capabilities of air-based solutions, and AI-assisted platforms analyzing data from numerous sensors.

Market Dynamics

Key Drivers in the Global Hyperscale Data Center Market

Exponential Surge in AI and Machine Learning Workloads

The emergence of AI generation and large language model training has created a shift in hyperscale computing requirements to use special servers using GPU clustering which needs 5-10 times more power per rack than regular computing. The power infrastructure needs to support 50-100 kW rack density, while the mechanical infrastructure will need to adapt quickly, using advanced liquid cooling infrastructure that will replace air-cooled systems. Cloud companies are building new facilities at a capacity of over 101 MW, designed specifically for training AI, where network infrastructure will be built for handling the massive east-west traffic flow typical of AI distributed GPU clustering.

Accelerating Enterprise Cloud Migration and Digital Transformation

Organizations of all sectors continue migrating from on-site data centers to hyperscale data centers owned by cloud service providers as well as colocation hyperscale data centers due to the favorable economics of elastic infrastructure. Expansion of IT infrastructure is needed in such cases in terms of server infrastructure, storage infrastructure, and network infrastructure to support corporate workloads of cloud computing, big data analytics, and enterprise resource planning software. The BFSI sector, health care, and the government sector have been among the major movers in this regard and are demanding hyperscale data centers with features like security monitoring, data analytics, and disaster recovery.

Restraints in the Global Hyperscale Data Center Market

Critical Power Availability and Grid Interconnection Challenges

Requirements for electricity infrastructure in terms of modern hyperscale facilities over 101 MW are rapidly surpassing capabilities of existing local grid infrastructure, thus leading to delays in permitting and interconnection and causing development delays of years. Data center clusters such as those located in Northern Virginia, Dublin, and Singapore face severe power shortages that restrict their expansion, adding an extra layer of complexity due to renewable energy ambitions. UPSs, PDUs, and generators needed for highly concentrated facilities have imposed extraordinary requirements on electrical equipment manufacturers and utilities that fail to increase transmission capacities rapidly enough to serve hyperscale customers.

Escalating Capital Intensity and Supply Chain Vulnerabilities

Investments for the hyperscale data centers industry have never been higher as the cost per facility surpasses USD 1 billion; this imposes immense financial pressure on companies and necessitates more complex funding schemes. Supply chains for key elements such as advanced semiconductors, special cooling systems, and power generators still rely on a small number of suppliers, thus putting this industry at risk from potential geopolitical conflicts and sanctions. Mechanical elements such as advanced liquid and immersion cooling systems pose supply chain risks due to the high precision required for manufacturing. IT infrastructure technology evolves quickly, making it difficult for businesses to maintain a balance between standardization and specialized equipment.

Growth Opportunities in the Global Hyperscale Data Center Market

Advanced Liquid Cooling and Thermal Management Infrastructure

The move from conventional air cooling to direct liquid cooling and even full immersion cooling as densities increase to the point where air cooling is physically incapable of providing adequate cooling is an enormous business case of multiple billions of dollars. Providers of mechanical infrastructure that can validate and scale up liquid cooling solutions that can support power densities exceeding 101 MW will benefit from their innovations as cloud providers retrofit existing facilities and construct new cloud provider-owned hyperscale facilities specifically designed for liquid cooling AI infrastructures. The change will also include racks configured for liquid delivery, PDUs for higher densities, and software for thermal analytics.

Edge Hyperscale and Distributed Architecture Expansion

The advent of latency-dependent application areas such as autonomous vehicles, industrial internet-of-things (IoT), and augmented reality applications is pushing the need for scalable and distributed architectures that use consistent infrastructure at secondary and edge facilities while managing operations from a central location. This offers possibilities for modular electrical and mechanical infrastructure that can be rolled out quickly to multiple locations and managed using orchestration and automation software. Multi-market hyperscale colocation data centers are better poised for these opportunities, as well as equipment manufacturers whose offerings include prefabricated and repeatable infrastructures to minimize deployment times in edge locations.

Trends in the Global Hyperscale Data Center Market

Sustainability-Integrated Infrastructure Design and GreenOps

Environmental performance has changed from being a compliance issue to a critical design factor for hyperscale data centers, with facility owners integrating sustainability into all forms of infrastructure. Electricity infrastructure involves the use of solar power within the data center facility, with the use of energy storage systems (as opposed to generator-based electricity) alongside grid-connected uninterruptible power supplies that can serve as frequency regulation providers to power companies. Meanwhile, mechanical infrastructure is moving towards zero water-cooling systems with closed-loop infrastructure, with construction infrastructure using sustainable building materials such as low-carbon concrete and mass timber.

AI-Driven Autonomous Data Center Operations

Hyperscale operators are rolling out AI-based software solutions that will automate facilities by converting them into self-managed environments where human involvement is minimal. The infrastructure management system makes use of machine learning algorithms to detect hardware failures even days before their occurrence, allowing preventive maintenance that ensures maximum uptime at a low cost. The orchestration and automation systems constantly monitor the load distribution across the facilities, and performance management and security monitoring tools make use of artificial intelligence to automatically identify and resolve anomalies.

Research Scope and Analysis

The Global Hyperscale Data Center Market is segmented by component, deployment mode, power capacity, data center type, infrastructure type, organization size, application, and end user. Growing cloud adoption, AI workloads, edge computing expansion, and increasing enterprise digital transformation initiatives are driving demand across hyperscale infrastructure and advanced data center solutions globally.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Component Analysis

The hardware sector is poised to lead the components market of the global hyperscale data center industry owing to the enormous need for servers, storage systems, networking equipment, power generation, and cooling technology within hyperscale data centers. Hyperscale players keep upgrading their IT and electricity infrastructure for performing AI computations, cloud computing, and other data processing tasks. High usage of high density rack technology, liquid cooling solutions, and highly efficient UPS technology enhances the dominance of hardware in this segment. The growing adoption of cloud service providers and colocation players around the world is another factor that aids hardware dominance in the components segment.

By Deployment Mode Analysis

The cloud deployment segment is projected to leading the market for global hyperscale data centers due to the rising usage of various types of cloud services, including public, private, and hybrid clouds, by organizations across the world. Companies are swiftly moving their applications into the cloud as it offers scalability, flexibility, optimization, and remote access to resources. The hyperscale cloud providers are still focusing on developing data center infrastructures in terms of size and capabilities to cater to their digital transformation and artificial intelligence needs. The benefits offered by cloud deployments are making them more popular among companies, along with rising SaaS, IaaS, and edge computing needs.

By Power Capacity Analysis

Above 101 MW is expected to be the makes up the largest share of hyperscale data center services due to the need of hyperscale providers to have ultra-high-capacity data centers to accommodate artificial intelligence training, cloud computing, big data processing, and high performance computing applications. High-power capacity data centers ensure efficiency and capacity to host thousands of servers as well as cooling systems. Large technology players are building mega data centers with increased energy capacity in order to cater to the global increase in demand for digital services. Generative AI infrastructures and expanding cloud regions also encourage the growth of ultra-high-capacity data centers.

By Data Center Type Analysis

The ownership of data centers by cloud provider organizations is prevalent in the market because of the huge investments by top cloud organizations in constructing their infrastructure globally. The large cloud providers need dedicated data centers to accommodate the expanding cloud workloads, AI applications, video streaming, and digital services of enterprises. Ownership of data centers offers better control, cybersecurity measures, low latency, and efficient management of resources. Hyperscale cloud providers are located in proximity to demand zones for improved efficiency and scalability. Growth among North American, European, and Asia Pacific-based hyperscale cloud providers drives this market segment.

By Infrastructure Type Analysis

IT infrastructure is projected to take the largest share of infrastructure type due to the reason that the servers, storage, and networking hardware represent the core of the operation for the hyperscale data centers. Growth in cloud computing, AI processing, virtualization, and big data analytics demands constant upgrades of sophisticated IT infrastructure. Hyperscale providers must employ top-of-the-line computer processors, scalable storage, and fast networking hardware to handle large volumes of data traffic. Adoption of GPU-driven AI servers and new generation networking hardware results in increased investments into IT infrastructure.

By Organization Size Analysis

Large enterprises is anticipated to dominate as they have been at the forefront of the hyperscale data centers due to huge investments in cloud, AI platforms, cybersecurity, and large-scale digital transformation. These companies create huge amounts of data, thus needing scalable infrastructure. It is not surprising that large enterprises have adopted hyperscale data centers to boost efficiency and business continuity as well as flexibility in workloads. Sectors like BFSI, telecommunication, healthcare, and retail depend hugely on hyperscale data centers to analyze data in real time as well as engage customers. Financial strength of large enterprises also allows them to implement latest technologies such as AI, IoT, and edge computing.

By Application Analysis

Cloud computing is expected to lead the application part of the hyperscale data center market because of the increasing usage of cloud services around the world. Companies are now increasingly using cloud solutions for scaling their storage space, processing capacity, app hosting capabilities, and for collaborating remotely. The construction of hyperscale data centers enables businesses to handle increased loads of data for cloud-based apps and services. The provision of SaaS, PaaS, and IaaS by cloud service companies is contributing to increasing demands for such hyperscale centers. Moreover, the increasing trend of digitalization, the adoption of hybrid workplaces, and migration from on-premises to cloud infrastructure is solidifying the supremacy of cloud computing applications in hyperscale centers.

By End User Analysis

Cloud services providers are projected to have a dominant share in the end-user market because of the extensive spending they make on hyperscale infrastructure to cope with the growing cloud services needs around the globe. The providers keep on constructing huge facilities that can help to handle workloads related to artificial intelligence, big data analytics, content delivery, and other cloud enterprise services. The use of hybrid cloud computing systems, software-as-a-service, and edge computing services has further sped up hyperscale infrastructure deployment. Data centers that are highly scalable and power-efficient are chosen by the cloud providers so that low latency can be ensured.

The Global Hyperscale Data Center Market Report is segmented on the basis of the following:

By Component

- Hardware

- Electrical Infrastructure

- UPS Systems

- Power Distribution Units (PDU)

- Generators

- Other Electrical Infrastructure

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Mechanical Infrastructure

- Software

- Management

- Infrastructure Management

- Cloud Management

- Orchestration & Automation

- Monitoring

- Performance Monitoring

- Security Monitoring

- Network Monitoring

- Application Monitoring

- Operational

- Data Management & Analytics

- Backup & Disaster Recovery (DR)

- Services

- Professional Services

- Installation & Deployment

- Maintenance & Support

- Training & Education

- Managed Services

By Deployment Mode

- On-Premise

- Cloud-Based

- Hybrid

By Power Capacity

- 10-50 MW

- 51-100 MW

- Above 101 MW

By Data Center Type

- Colocation Hyperscale Data Center

- Cloud Provider-Owned Hyperscale Data Center

- Enterprise Hyperscale Data Center

By Infrastructure Type

- IT Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction Infrastructure

By Organization Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By Application

- Cloud Computing

- Big Data Analytics

- Artificial Intelligence & Machine Learning

- Content Delivery & Streaming

- Data Backup & Disaster Recovery

- High-Performance Computing (HPC)

- Virtualization

- Enterprise Resource Planning (ERP)

- Internet of Things (IoT)

- Edge Computing

- Business Continuity Management

- Web Hosting & Content Management

- Other Application

By End User

- Cloud Service Providers

- BFSI

- IT & Telecommunications

- Government & Defense

- Healthcare

- Retail & E-commerce

- Media & Entertainment

- Manufacturing

- Energy & Utilities

- Other End User

Regional Analysis

Leading Region by Market Share

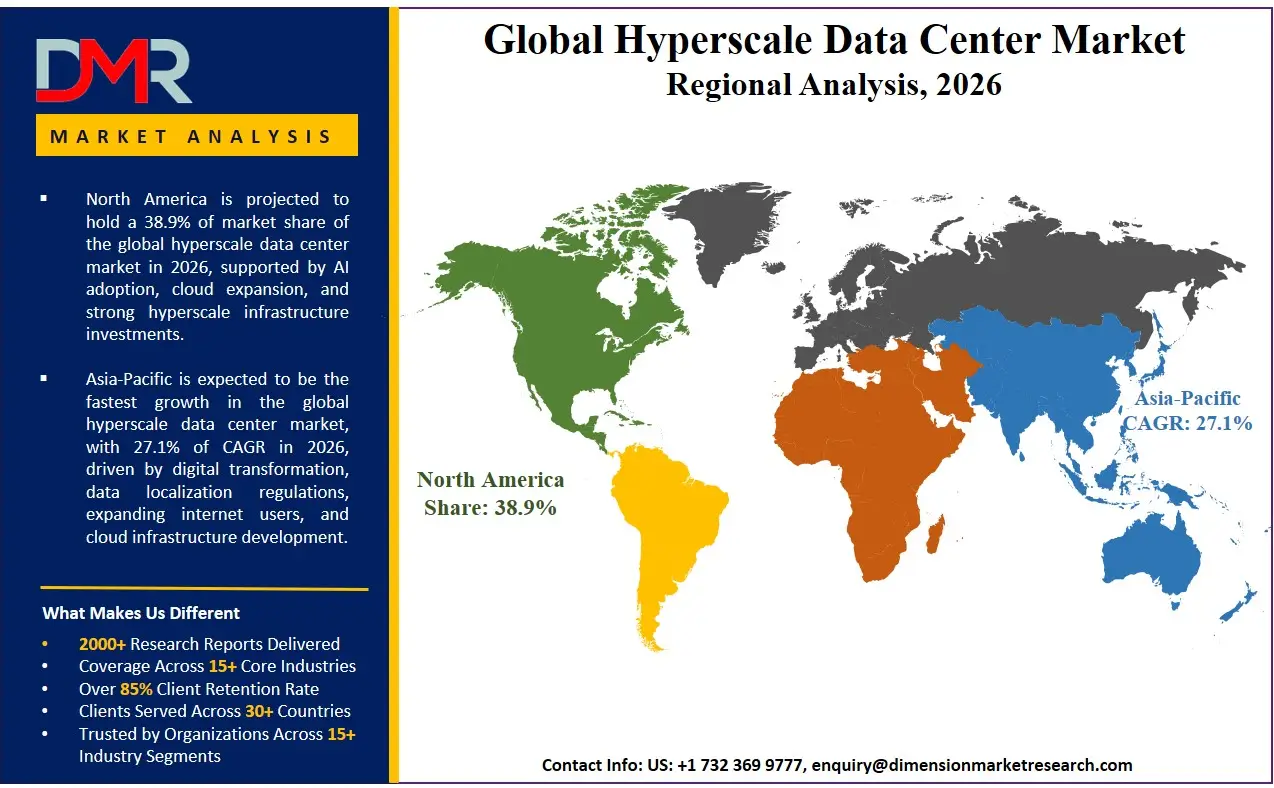

North America is poised to dominate the global hyperscale data center market as it is projected to hold 38.9% of the market share by the end of 2026. The United States, which leads North America, holds the largest share in hyperscale data center investments due to the unparalleled clustering of cloud services providers and aggressive growth plans of hyperscale players in critical regions such as Northern Virginia, Silicon Valley, Phoenix, Dallas, and Chicago. North America has a developed ecosystem of data center builders, general contractors, technology vendors, and engineering firms that allow quick deployment of facilities. Large enterprises' investments in artificial intelligence, cloud computing migrations, and digital transformations result in continuous demand for IT infrastructure in terms of server infrastructure, storage infrastructure, network infrastructure, as well as necessary electrical and mechanical infrastructure. In addition, favorable energy infrastructure and generally simpler permit requirements in certain regions still attract more hyperscale investments, but increasingly severe power availability issues start to pose significant threats in high concentration regions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

It is projected that the Asia Pacific region will be home to the fastest-growing hyperscale data centers owing to digital transformation efforts led by governments, the adoption of cloud, and the emergence of local cloud service providers in China, India, Japan, and the Southeast Asian region. With rapid economic development, increasing digitization by large populations, and expansion of the digital economy, cloud service providers and telecommunication firms are being urged to build hyperscale data centers in the region. Particularly high is the demand for services involving data management and analytics as well as cloud computing applications with enterprises undergoing digital transformation through replacement of old infrastructure and implementation of new services. There is an acute shortage of capacity from hyperscale data centers in the Asia Pacific market, which presents a unique opportunity for the establishment of hyperscale data centers owned by cloud providers as well as colocation hyperscale data centers.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The highly competitive nature of the global hyperscale data center market has turned into a highly dynamic one, owing to the wide variety of players who offer unique solutions from cloud service providers constructing proprietary data centers to colocation firms offering services to multi-tenants and unique equipment manufacturers offering products such as electrical infrastructure, IT infrastructure, and mechanical infrastructure, which form part of a hyperscale data center's architecture. The key to success for equipment manufacturers is strategic alliances with major cloud service providers and colocation companies because this will allow the manufacturer to secure the volumes needed to invest in research and development in cutting-edge technology such as liquid cooling systems and high density PDUs. Vertical integration continues to be an ongoing process as major cloud providers develop their proprietary server infrastructure, network infrastructure, and power and cooling technologies.

Some of the prominent players in the Global Hyperscale Data Center Market are:

- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud

- Meta Platforms

- Oracle Cloud Infrastructure (OCI)

- Alibaba Cloud

- IBM Cloud

- Apple

- Baidu AI Cloud

- Tencent Cloud

- Equinix

- Digital Realty

- NTT Global Data Centers

- QTS Realty Trust

- CyrusOne

- CoreWeave

- Switch

- GDS Holdings

- Yotta Infrastructure

- CtrlS Datacenters

- Other Key Players

Recent Developments

- January 2026: AWS expands its hyperscale data center infrastructure by launching new data centers that exceed 200 MW of power capacity in several regions around the world. The data centers include advanced liquid cooling and next-generation electrical infrastructures, which will enable hyperscale data center services capable of handling AI training workloads.

- November 2025: Microsoft launches new hyperscale facilities with unique mechanical infrastructure featuring water-free closed-loop cooling technology. These data centers have been outfitted with AI-powered comprehensive infrastructure management software platforms for their data centers worldwide.

- October 2025: Following a series of acquisitions, Equinix continues its hyperscale strategy by launching more colocation hyperscale data center facilities with the potential for over 101 MW of power capacity in various APAC markets and advanced security and network infrastructures to facilitate hybrid architecture needs.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 239.5 Bn |

| Forecast Value (2035) |

USD 1,903.9 Bn |

| CAGR (2026-2035) |

25.9% |

| The US Market Size (2026) |

USD 78.4 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Component, By Deployment Mode, By Power Capacity, By Data Center Type, By Infrastructure Type, By Organization Size, By Application, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Hyperscale Data Center Market?

▾ The Global Hyperscale Data Center market is poised to be valued at USD 239.5 billion in 2026 and is projected to reach USD 1,903.9 billion by 2035, driven by the universal need for scalable infrastructure to support cloud computing, artificial intelligence, and exponential data growth.

What is the CAGR of the Global Hyperscale Data Center Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 25.9% from 2026 to 2035, reflecting the accelerating demand for hyperscale infrastructure from cloud service providers and the increasing complexity of power and cooling requirements for AI workloads.

What factors are driving the growth of the Global Hyperscale Data Center Market?

▾ Key drivers include exponential data generation and cloud adoption, the proliferation of AI and high-performance computing workloads requiring specialized IT infrastructure and advanced cooling systems, and the global expansion strategies of major cloud service providers constructing cloud provider-owned hyperscale data centers across new geographic regions.

Which region held the largest share of the Hyperscale Data Center Market in 2026?

▾ North America, specifically the United States, is poised to hold 38.9% of market share in 2026, driven by a mature ecosystem of cloud service providers, established supply chains for electrical and mechanical infrastructure, and aggressive enterprise investment in cloud computing and AI-driven hyperscale capabilities.

Which region is expected to grow the fastest in the Hyperscale Data Center Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid digital transformation and cloud adoption in China, India, and Japan, where significant investment in cloud provider-owned and colocation hyperscale data centers is critical for supporting growing digital economies.

What are the major trends in the Global Hyperscale Data Center Market?

▾ Major trends include the transition to liquid cooling and immersion cooling systems within mechanical infrastructure, the integration of AI-powered software platforms for infrastructure management and orchestration and automation, the adoption of sustainability-driven electrical infrastructure designs, and the emergence of edge hyperscale deployments supporting latency-sensitive applications.

Who are the key players in the Global Hyperscale Data Center Market?

▾ Key players include hyperscale cloud service providers like AWS, Microsoft Azure, Google Cloud, and Alibaba Cloud, colocation operators like Equinix and Digital Realty, and specialized equipment manufacturers like Schneider Electric, Vertiv, and Eaton Corporation that supply the electrical infrastructure, cooling systems, and power distribution equipment essential for hyperscale operations.

How is the Global Hyperscale Data Center Market segmented?

▾ The market is segmented by Component, Deployment Mode, Power Capacity, Data Center Type, Infrastructure Type, Organization Size, Application, and End User