Market Snapshot

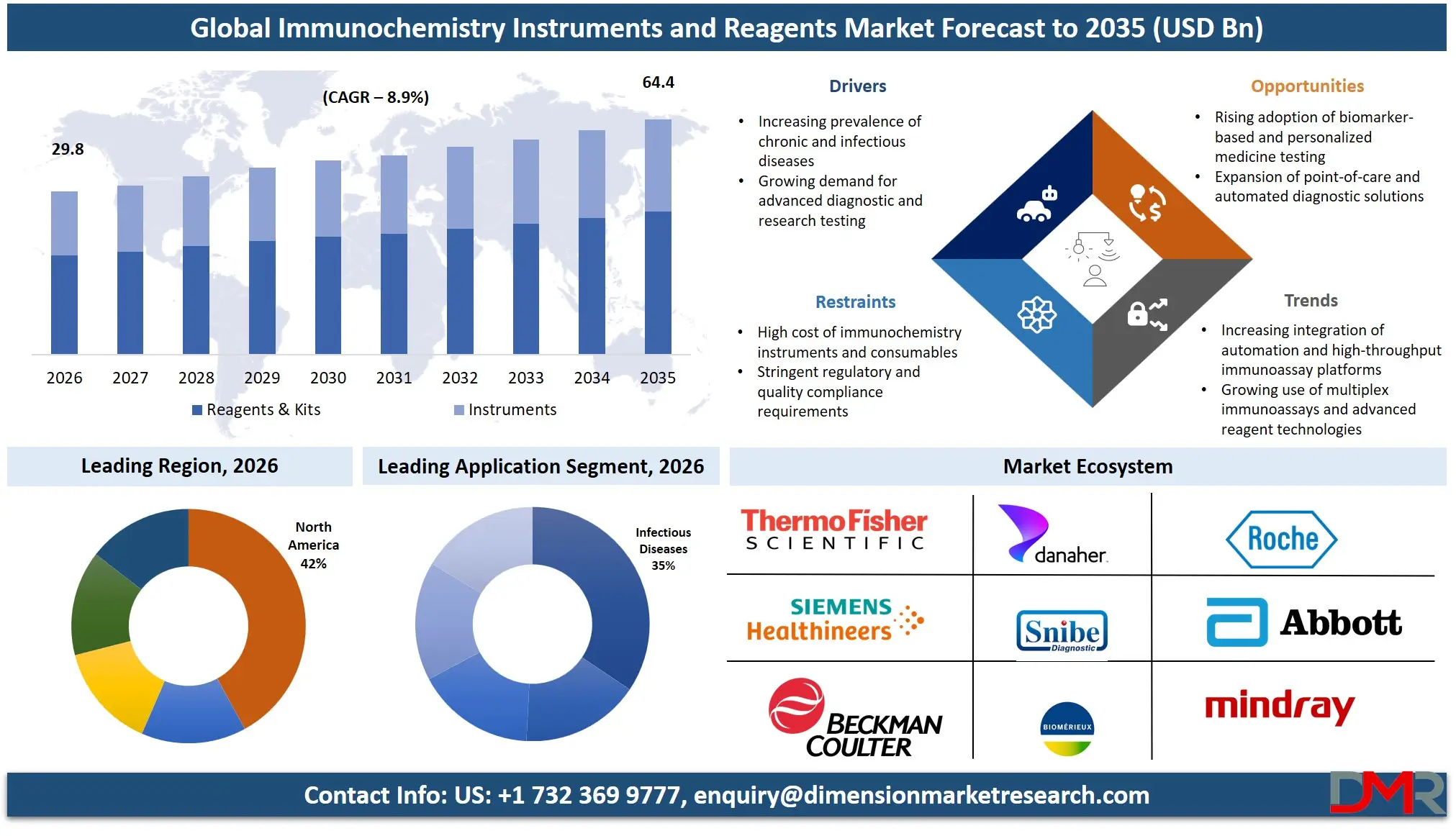

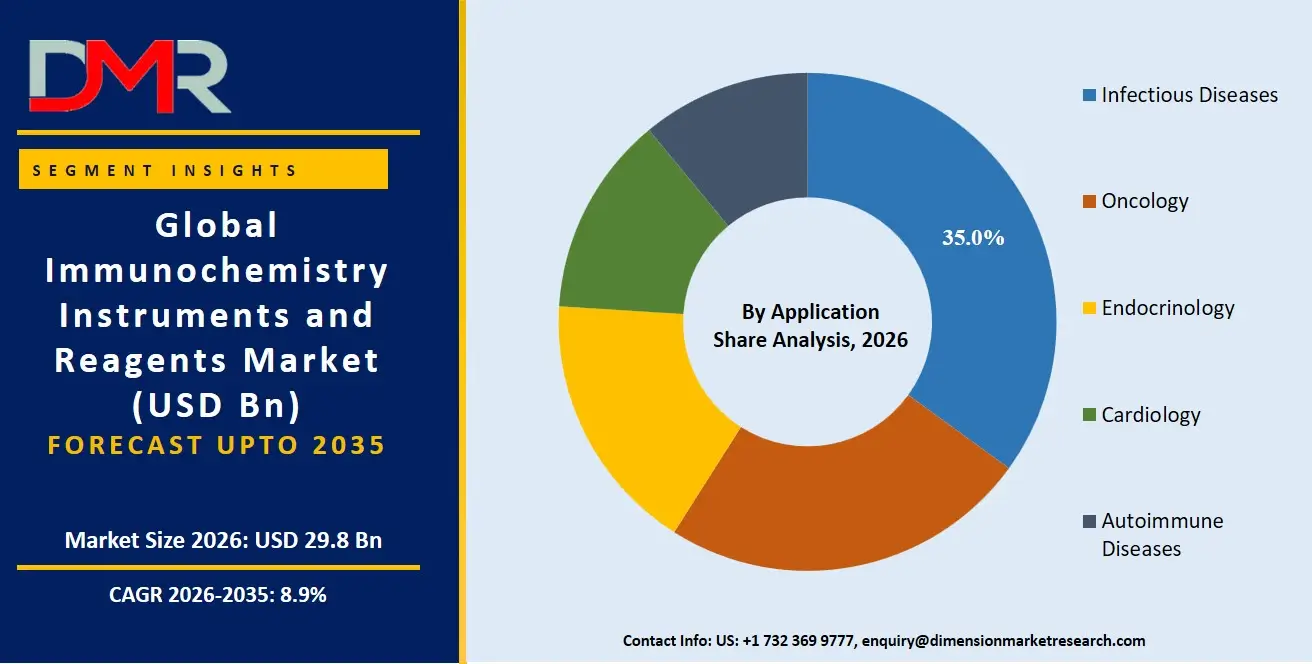

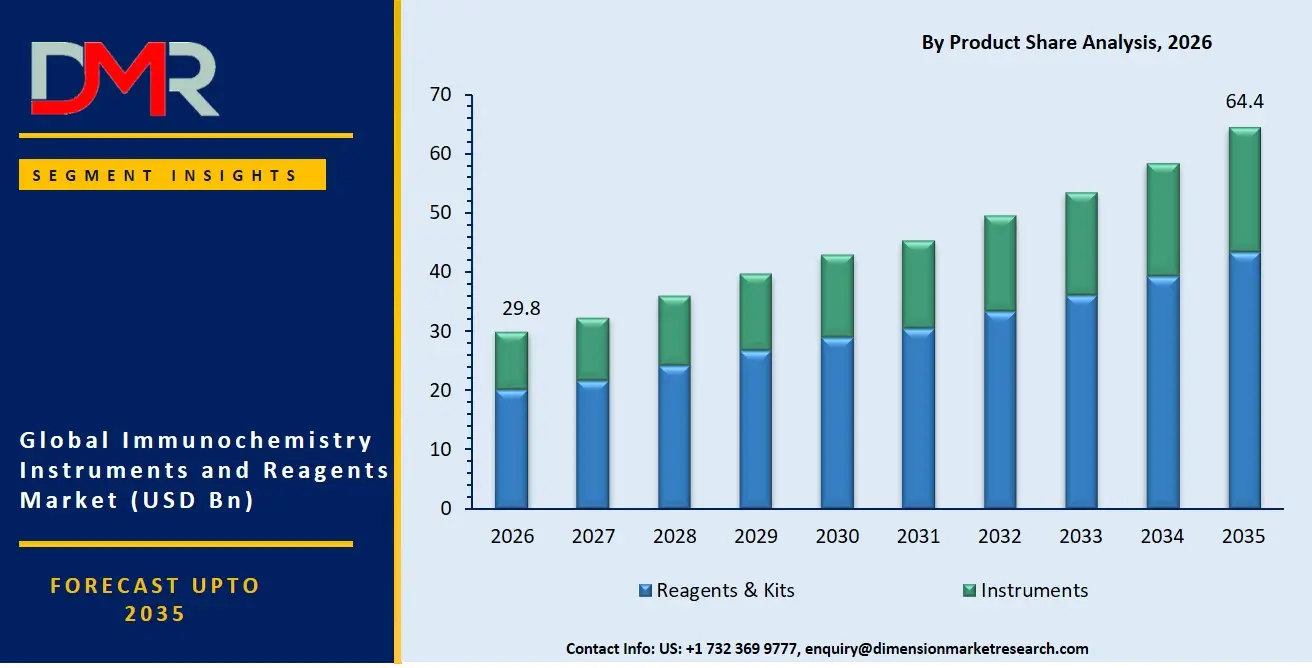

- The global Immunochemistry Instruments and Reagents Market is valued at USD 27.3 Billion in 2025, reached USD 29.8 Billion in 2026, and is projected to hit USD 64.4 Billion by 2035 at a CAGR of 8.9%.

- By Product, Reagents and Kits lead with a 67.2% revenue share in 2026.

- By Technology, CLIA (Chemiluminescent Immunoassay) leads with a 36.9% revenue share.

- By Application, Infectious Diseases is the top area with a 35.0% revenue share.

- By End-Use, Diagnostic Laboratories dominate with a 47.5% revenue share.

- By Test Type, Routine Testing leads with a 71.6% revenue share.

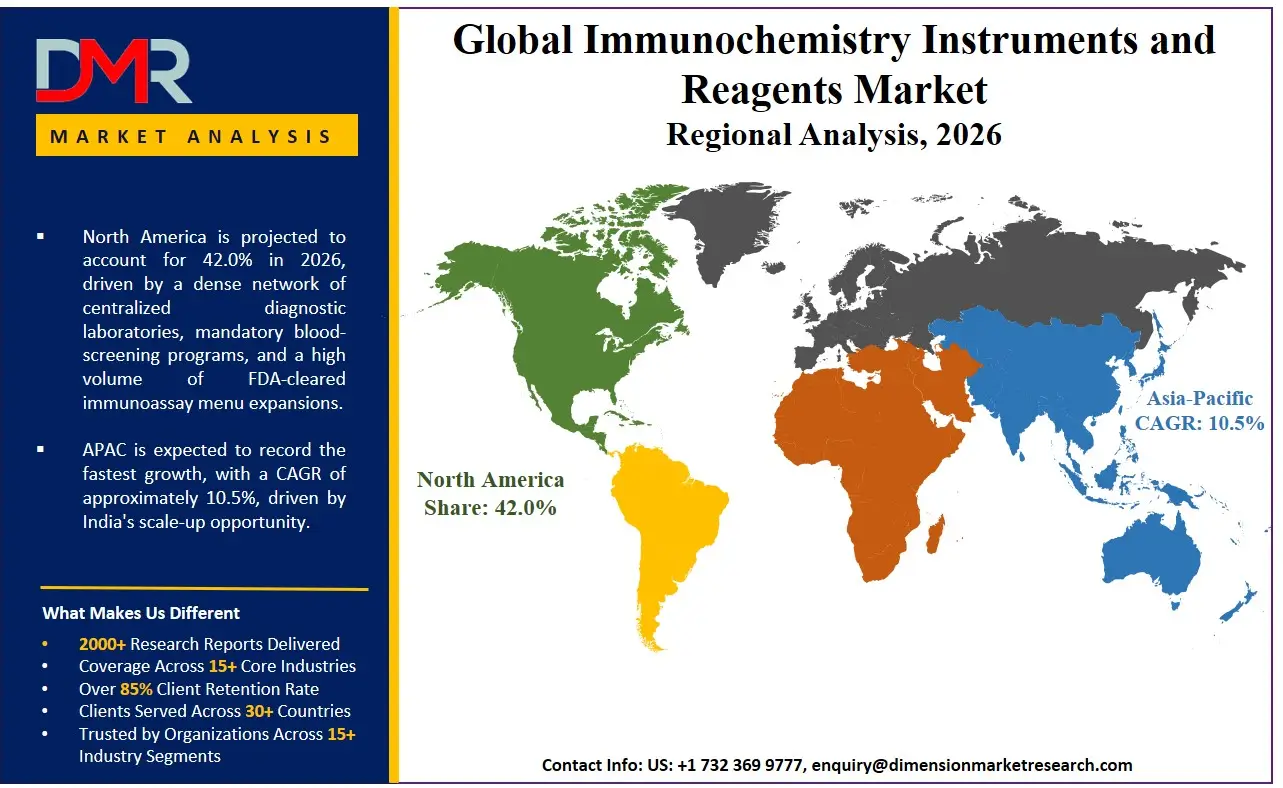

- North America holds the leading regional position with a 42.0% share, valued at USD 11.9 Billion in 2026.

- The US market alone is valued at USD 10.1 Billion in 2026, forecast to reach USD 20.4 Billion by 2035 at a CAGR of 7.9%.

Market Overview

The Immunochemistry Instruments and Reagents Market covers the full spectrum of automated analyzers, detection platforms, and consumable reagent kits used to identify and measure biological markers through antibody-antigen reactions. This includes instruments running CLIA, ELISA, Fluorescence Immunoassay, and RIA technologies, alongside the reagents and kits that enable each test. The market serves diagnostic laboratories, hospitals, academic and research institutes, and blood banks.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

This market does not include general clinical chemistry consumables unrelated to immunoassay principles, nor does it cover standalone molecular diagnostics platforms that use nucleic acid amplification rather than immunological detection. That boundary matters for buyers evaluating platform investment, since immunoassay and molecular testing serve overlapping but distinct clinical needs. Within the broader in vitro diagnostics industry, immunoassay testing represents one of the highest-volume and highest-value segments, positioning it as a structural backbone of routine clinical workflow rather than a specialty niche.

The reagents and kits segment controls a 67.2% revenue share, which signals a critical commercial dynamic. Every installed analyzer requires a continuous supply of matched reagents, creating non-discretionary, repeat procurement that compounds over the life of each instrument placement. Manufacturers that secure instrument installations effectively capture multi-year consumable spend, making platform penetration a higher-priority commercial objective than per-unit instrument margin.

Key Statistics

- Roche's Diagnostics Division posted full-year 2024 sales of CHF 14.3 Billion, with core operating profit up 12% at constant exchange rates to CHF 2.4 Billion. As reported by Roche's full-year 2024 results.

- Roche's Core Lab customer area generated CHF 8,004 Million in 2024, up 8% at constant exchange rates versus 2023, while COVID-19-related product sales fell from CHF 0.8 Billion to CHF 0.2 Billion in the same period. As reported by Roche.

- Bio-Rad's Clinical Diagnostics segment posted full-year 2024 net sales of USD 1,537.9 Million, up 3.7% currency-neutral, growing to USD 1,562.1 Million in 2026. As reported by Bio-Rad.

- DiaSorin's 9M 2025 total revenues were up 3% reported and 5% at CER, with ex-COVID immunodiagnostics revenues reaching EUR 616 Million in 9M 2025, up 6% at CER. As reported by DiaSorin.

- The India immunochemistry analyzers and reagents market was estimated at INR 3,750 crore in 2024, with reagents representing INR 3,435 crore of that total, meaning reagents account for over 91% of the market value. As per available market data.

- Siemens Healthineers achieved My Green Lab ACT Ecolabel certification for more than 150 reagents running on Atellica analyzers in July 2025, becoming the first IVD manufacturer to earn this distinction. As reported by Siemens Healthineers.

Market Size and Forecast

The Global Immunochemistry Instruments and Reagents Market size is estimated at USD 29.8 Billion in 2026 from USD 27.3 Billion in 2026, and is projected to reach USD 64.4 Billion by 2035, exhibiting a CAGR of 8.9% during the forecast period.

Historical performance confirms consistent base business expansion across the market's largest operators. Roche's Core Lab segment grew steadily in 2023 to 2024 even as COVID-19-related revenues normalized. Bio-Rad's Clinical Diagnostics segment maintained positive currency-neutral growth across both years. These patterns confirm that demand is broad-based and not dependent on any single product cycle, which underpins the reliability of the 2026 to 2035 growth trajectory.

An upside scenario exists if compact analyzer adoption in mid-sized laboratories accelerates faster than projected. The autoimmune diagnostics segment also represents an underutilized reagent opportunity; wider adoption of newly cleared autoimmune panels would accelerate reagent pull-through beyond current forecast assumptions.

A downside scenario emerges if high capital costs slow instrument placements across Asia Pacific and Latin America. Currency headwinds can compress reported revenue even when underlying test volumes hold firm, as DiaSorin's 9M 2025 results showed with only 3% reported growth versus 5% at constant exchange rates. If pricing instability persists in import-dependent markets, volume growth could lag the 8.9% CAGR base case during the 2026 to 2028 window.

Market Dynamics

Integrated Platform Adoption and Expanded Biomarker Menus Drive Laboratory Revenue Growth

Consolidation of clinical chemistry and immunoassay testing onto single automated platforms directly reduces laboratory operating costs and testing turnaround time. Labs choosing integrated systems lower their capital footprint while increasing throughput per workstation. This architecture has moved from experimental to commercially cleared, making platform integration a standard expectation among buyers rather than a premium feature.

Cardiac biomarker menu expansion is building a stronger commercial case for immunoassay platform investment. Each newly cleared assay increases billable test volume per instrument, improving return on capital for laboratories and strengthening reagent pull-through for manufacturers. Blood-screening immunoassay demand is simultaneously widening the addressable market. Blood banks and public health laboratories running newly cleared infectious disease tests must procure compatible reagents on an ongoing basis, creating a durable, non-discretionary demand base that insulates revenue against economic cycles.

High Platform Costs and Prolonged Regulatory Timelines Constrain Expansion in Price-Sensitive Markets

Automated immunoassay analyzers carry substantial capital costs that exceed budget thresholds for smaller and emerging-market laboratories. This structural barrier prevents instrument penetration in geographies where diagnostic infrastructure investment remains limited, leaving a significant installed-base gap. Manufacturers unable to offer financing models or lower-cost platform tiers risk ceding these markets to simpler, lower-throughput testing alternatives.

Regulatory timelines compound the cost barrier by extending time-to-market for new assays. FDA 510(k) clearance cycles mean clinical need and regulatory approval are rarely synchronized. Each month of clearance delay represents foregone reagent revenue and delayed market access, which disproportionately affects smaller manufacturers with thinner pipelines. Manufacturers that treat regulatory affairs as a core commercial function rather than a post-development compliance step will compress approval cycles and reach the market ahead of competitors.

India Manufacturing Scale-Up and Compact Analyzer Deployment Open New Revenue Pools

Local manufacturing presence is reshaping supply chain economics in high-growth geographies. Producing reagents in-country eliminates import duties and logistics costs that would otherwise compress competitive pricing in price-sensitive environments. Mid-sized laboratories represent a segment historically underserved by high-throughput platform manufacturers. Compact analyzers lower the entry cost for lab operators while maintaining the manufacturer's reagent revenue model, capturing accounts that were previously outside the addressable market for large-lab-focused incumbents.

Autoimmune disease diagnostics represent a high-value reagent category with underpenetrated testing rates globally. Manufacturers with cleared, validated autoimmune panels will capture a growing share of specialty reagent procurement budgets from both hospitals and reference laboratories. As autoimmune disease prevalence sustains clinical attention, this application area offers both volume growth and premium per-test pricing that outperforms routine panel economics.

Market Trends

Platform Integration, Full Lab Automation, and Novel Biomarker Launches Reshape Competitive Structure

Consolidation of clinical chemistry and immunoassay testing onto single workstations is moving from product differentiator to table-stakes requirement. Buyers now expect hardware, software, and decision-support capability in a single platform purchase. CLIA is cementing its position as the dominant immunoassay modality for infectious disease screening, holding a 36.9% technology share in 2026. Manufacturers that lead in CLIA reagent breadth, not just instrument throughput, will control the most defensible share of high-volume screening revenue. Novel biomarker discovery is generating a new reagent category outside routine testing cycles, where early movers who secure cleared assays in specialty categories capture premium pricing and first-mover loyalty from reference laboratories before the category becomes commoditized.

Research Scope and Analysis

The market is driven by reagent-led recurring revenue, with CLIA technology and infectious disease applications dominating usage. Diagnostic laboratories lead end-use demand, while routine testing ensures stable volume. Instruments enable long-term reagent consumption, creating a structured ecosystem of recurring procurement and high-margin specialty testing growth.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Product Analysis

Reagents and Kits lead the segment with a 67.2% share, reflecting the razor-and-blade commercial model where every installed analyzer requires a continuous supply of matched reagents. This creates non-discretionary, repeat procurement that compounds over the instrument's operational life. Manufacturers with large installed bases effectively lock in multi-year reagent revenue regardless of new instrument sales cycles.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Instruments represent the capital investment layer that enables the entire reagent revenue stream downstream. Instrument placements are subject to budget cycles, procurement committees, and regulatory clearance timelines, making this sub-segment more volatile than reagents. Manufacturers that prioritize rapid instrument penetration in underpenetrated mid-sized lab segments build the foundation for compounding reagent revenue over the life of each placement.

By Technology Analysis

CLIA (Chemiluminescent Immunoassay) leads the segment with a 36.9% share, supported by high analytical sensitivity and full automation compatibility. CLIA's dominance is reinforced by active regulatory validation momentum, with multiple high-volume infectious disease assays cleared on CLIA platforms in 2024 and 2025. Labs adopting CLIA benefit from throughput performance that supports both high-volume routine screening and expanding specialty menus on the same platform.

ELISA remains widely deployed in research settings and lower-throughput diagnostic environments where capital constraints limit access to fully automated CLIA systems. Its lower instrument cost makes it the default entry point for smaller laboratories and academic research institutes, but manual processing steps create throughput limitations that push high-volume labs toward automated alternatives as test volumes scale. Fluorescence Immunoassay is gaining clinical relevance in autoimmune and specialty biomarker panels where detection precision is prioritized over throughput. RIA represents a legacy modality with a declining but active installed base, primarily in endocrinology and research applications; regulatory restrictions on radioactive materials are accelerating substitution toward CLIA and fluorescence platforms in most clinical settings.

By Application Analysis

Infectious Diseases holds the dominant position with a 35.0% share. Blood bank screening mandates and public health surveillance programs generate non-discretionary, high-frequency test orders that sustain reagent volume regardless of disease prevalence cycles. This application's revenue leadership is structural, anchored by regulatory requirements rather than discretionary clinical ordering patterns.

Oncology is a structurally expanding application area, driven by the clinical shift toward biomarker-guided treatment decisions in cancer care. As precision oncology protocols become standard of care in high-income markets, reagent utilization per oncology patient increases. Endocrinology generates high-frequency, repeat-order reagent demand because hormonal disorders require ongoing monitoring; thyroid, fertility, and cortisol panels are ordered routinely across primary care and specialist settings. Cardiology is a high-value area where biomarker immunoassays are ordered under time-critical clinical conditions, generating multiple repeat assay orders across a hospital stay and making it a premium-priced driver of reagent revenue. Autoimmune Diseases represent the highest-growth application category within the specialty diagnostics tier; autoimmune panels typically require a broader reagent menu per patient than infectious disease screening, resulting in higher per-patient reagent revenue and stronger gross margin contribution for manufacturers with cleared portfolios.

By End-Use Analysis

Diagnostic Laboratories hold the dominant position with a 47.5% share. Centralized reference laboratories operate at throughput levels that justify investment in high-capacity automated immunoassay analyzers, which generate the highest per-site reagent consumption volumes. Their purchasing scale gives them negotiating leverage on reagent contracts, but their volume commitment also makes them the most commercially valuable accounts for platform manufacturers.

Hospitals represent the second-largest end-use category, combining high-urgency stat testing with routine panel processing. Hospital laboratories are primary adopters of integrated clinical chemistry and immunoassay platforms because consolidation reduces the number of instruments required per lab footprint. Academic and Research Institutes serve as a critical testing ground for novel biomarker assays before clinical deployment; research institute adoption signals which assay categories are likely to transition into routine clinical use within two to five years, making this segment a leading indicator of future commercial reagent volume. Blood Banks operate under mandatory regulatory testing protocols that create predictable, non-negotiable reagent demand for every donated blood unit screened.

By Test Type Analysis

Routine Testing holds a 71.6% share, covering thyroid function, fertility hormones, infectious disease screening, and cardiac markers ordered on a scheduled, recurring basis. This recurring order pattern creates predictable reagent consumption that manufacturers can model and contract against, making routine testing the most commercially stable segment in the market.

Specialized Testing captures the remaining share and carries structurally higher per-test pricing than routine panels, reflecting the lower manufacturing volumes and advanced detection requirements of specialty reagents. Autoimmune panels, novel biomarker kits, and reference laboratory-exclusive assays fall into this category. Manufacturers actively building specialized testing portfolios are capturing premium pricing and differentiating beyond commoditized routine reagent lines, which strengthens overall margin contribution per installed instrument.

Key Market Segments

By Product

- Reagents and Kits

- Instruments

By Technology

- CLIA

- ELISA

- Fluorescence Immunoassay

- RIA

By Application

- Infectious Diseases

- Oncology

- Endocrinology

- Cardiology

- Autoimmune Diseases

By End-Use

- Diagnostic Laboratories

- Hospitals

- Academic and Research Institutes

- Blood Banks

By Test Type

- Routine Testing

- Specialized Testing

Regional Analysis

North America holds a dominant position with a 42.0% share, valued at USD 11.4 Billion in 2026. The US alone accounts for USD 10.1 Billion, supported by a dense network of centralized diagnostic laboratories, mandatory blood-screening programs, and a high volume of FDA-cleared immunoassay menu expansions in 2024 and 2025. The US regulatory framework, while demanding, validates product quality and gives cleared assays commercial credibility that accelerates hospital and lab adoption.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Asia Pacific is the highest-priority expansion geography for manufacturers, with India representing the most clearly quantified opportunity in the region. Europe is a mature but active immunochemistry market driven by CE-mark product launches that expand the clinical reagent menu across member states; the transition from the prior EU IVD Directive to the more stringent IVDR framework has extended review timelines and increased clinical evidence requirements, raising barriers for smaller manufacturers. Latin America represents an underpenetrated market where currency volatility and import-dependent reagent supply chains create pricing instability that constrains the pace of platform upgrades in both private and public sector laboratories. The Middle East and Africa present a bifurcated structure where GCC countries are active buyers of high-throughput platforms and premium reagent portfolios, while Sub-Saharan Africa faces infrastructure and budget constraints that limit adoption to essential infectious disease screening.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Competitive Landscape

The Immunochemistry Instruments and Reagents Market operates as a moderately consolidated oligopoly at the top tier, where five to six global manufacturers collectively control the majority of high-throughput analyzer placements and the recurring reagent contracts they generate. Competitive battles are fought primarily at the instrument placement and contract renewal stages rather than on reagent price alone. The largest revenue positions belong to manufacturers with the broadest cleared assay menus and the deepest installed bases in centralized diagnostic laboratories.

Mid-tier manufacturers are differentiating through platform specialization and segment targeting. One major manufacturer identified a structural gap left by high-throughput platform leaders and launched a compact integrated analyzer targeting small- and mid-sized laboratories in Q2 2024. Sustainability is also emerging as a competitive differentiator; becoming the first IVD manufacturer to earn My Green Lab ACT Ecolabel certification for over 150 reagents in July 2025 illustrates how environmental credentials are becoming a procurement differentiator alongside throughput and menu breadth. Manufacturers that combine menu breadth, platform integration, geographic manufacturing presence, and sustainability credentials will build more durable market positions than those competing on instrument throughput or reagent price alone.

Company Profiles

Roche Diagnostics anchors its competitive position through the depth of its Elecsys immunoassay platform and the breadth of its cleared assay menu. Its strategy compounds throughput leadership with continuous product refresh cycles, as demonstrated by high-throughput analyzer launches in CE-mark countries during 2024 and new specialty assay categories entering the cleared menu in 2025. Roche's scale in the Core Lab segment creates a self-reinforcing advantage where greater installed base drives higher reagent volumes, which funds continued assay development, which sustains menu breadth leadership over competitors.

Abbott Laboratories strengthens its immunoassay portfolio through biomarker platform partnerships that extend clinical utility beyond its proprietary assay pipeline. Its approach of leveraging partner expertise to expand the Alinity i menu rapidly reduces R&D costs while accelerating the commercial value of each instrument placement. Danaher Corporation operates through Beckman Coulter with an active regulatory pipeline execution strategy; its business model emphasizes post-placement reagent and service revenue, meaning each cleared assay and new analyzer placement compounds its long-term revenue base. Siemens Healthineers is executing a dual strategy targeting mid-sized laboratory expansion while advancing full automation and predictive analytics in high-capacity settings, and has established a sustainability leadership position as the first IVD manufacturer to earn My Green Lab ACT Ecolabel certification for its reagent portfolio.

Key Players

- Roche Diagnostics

- Abbott Laboratories

- Danaher Corporation

- Siemens Healthineers

- Thermo Fisher Scientific

- Bio-Rad Laboratories

- Sysmex Corporation

- Ortho Clinical Diagnostics (QuidelOrtho)

- Agilent Technologies

- Revvity (PerkinElmer)

- DiaSorin

- bioMerieux

- Mindray

- Randox Laboratories

- Snibe Co., Ltd.

Supply Chain and Value Chain Analysis

The Immunochemistry Instruments and Reagents supply chain begins with raw material suppliers providing monoclonal antibodies, enzyme substrates, chemiluminescent compounds, and calibrator proteins. These inputs flow to reagent manufacturers and instrument component suppliers who produce finished kits and analyzer hardware. Control over upstream antibody supply is a significant competitive lever, as disruptions at this stage directly constrain reagent production capacity. Maximum value in the chain is created at the reagent manufacturing and assay development stage; proprietary assay formulations, validated calibration matrices, and cleared quality controls carry the highest intellectual property content and the strongest pricing power.

Buyers in this market hold moderate-to-low short-term switching power once a platform is installed, because reagent compatibility is instrument-specific and revalidating assays on a competing platform carries time and regulatory cost. Manufacturers that place instruments under multi-year reagent supply contracts effectively lock in downstream revenue, which is why instrument placement strategy is the primary determinant of long-term supply chain control. Large diagnostic laboratories with the highest test volumes negotiate directly with manufacturers, while smaller hospitals and regional labs typically procure through distributors, requiring manufacturers to maintain parallel commercial strategies for both channel types simultaneously.

Regulatory Landscape

The market operates under in vitro diagnostic regulatory frameworks that vary by geography but share a common requirement: analytical performance validation before commercial launch. In the United States, the FDA 510(k) clearance pathway governs most immunoassay analyzer and reagent submissions, requiring manufacturers to demonstrate substantial equivalence to a predicate device. The FDA De Novo authorization pathway is becoming commercially relevant as manufacturers introduce first-of-kind assays; De Novo clearance is more resource-intensive than 510(k), but it establishes the cleared product as a future predicate, giving the innovator a structural regulatory advantage over later entrants targeting the same clinical application.

CE marking under the EU In Vitro Diagnostic Regulation governs market access across European member states. The transition from the prior EU IVD Directive to the more stringent IVDR framework has extended review timelines and increased clinical evidence requirements, raising barriers for smaller manufacturers seeking European market access. Sustainability compliance is emerging as a regulatory-adjacent procurement requirement; as hospital and public sector procurement policies incorporate environmental performance criteria, manufacturers without documented sustainability compliance risk exclusion from tender processes in key European and North American markets, creating a de facto non-regulatory barrier with similar commercial consequences.

Investment and White Space Analysis

Current investment flows concentrate on three areas: integrated platform development, geographic manufacturing expansion in India, and specialty assay pipeline build-out in autoimmune and cardiology categories. The largest players are reinvesting margin gains into product and platform development rather than returning all capital to shareholders, signaling sustained R&D intensity at the top of the competitive hierarchy. India represents the clearest white space opportunity with quantified scale; reagents alone account for over 91% of the country's immunochemistry market value, and local manufacturing capability is the primary lever for competing on price in that environment.

The mid-sized laboratory segment represents underserved white space in established markets. New entrants or regional manufacturers capable of deploying compact, cost-effective systems into this segment can accumulate installed base and recurring reagent revenue without competing head-to-head against large-lab-focused incumbents. Autoimmune disease diagnostics remain underpenetrated relative to clinical need; manufacturers that build and clear autoimmune reagent portfolios now will establish clinical reference laboratory relationships before this application area becomes crowded. Players that combine geographic manufacturing localization with specialty assay menu expansion will compound two distinct revenue advantages within the same investment cycle.

Recent Developments

- May 4, 2026, DiaSorin announced the appointment of Gabriele Allegri as President of its Immuno Division, strengthening executive leadership of its immunodiagnostics business unit.

- February 24, 2026, DiaSorin and QIAGEN. Product launch. Introduced the next-generation LIAISON QuantiFERON-TB Gold Plus II assay for the U.S. market, expanding tuberculosis diagnostics on the LIAISON immunoassay platform.

- January 29, 2026, DiaSorin. Regulatory clearance. Received FDA De Novo authorization for the first fully automated laboratory test for Hepatitis Delta Virus on the LIAISON XL immunoassay platform, establishing a new predicate for future HDV testing submissions.

- November 18, 2025, DiaSorin and QIAGEN. Product launch. Unveiled the next-generation LIAISON QuantiFERON-TB Gold Plus II assay across all CE-mark countries, delivering productivity gains and faster results for tuberculosis screening programs.

- September 19, 2025, DiaSorin launched the LIAISON TSH-R Ab immunodiagnostic assay for Graves' Disease diagnosis across all CE-mark countries, expanding its autoimmune disease testing menu.

- September 8, 2025, DiaSorin presented new clinical evidence on the MeMed BV host-response immunoassay at ACEP 2025, supporting emergency medicine clinical decisions on the LIAISON platform in acute care settings.

- July 24, 2025, Siemens Healthineers announced that more than 150 reagents running on Atellica analyzers received My Green Lab ACT Ecolabel certification, becoming the first IVD manufacturer to earn this distinction.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 27.3 Billion |

| Market Value (2026) |

USD 29.8 Billion |

| Forecast Revenue (2035) |

USD 64.4 Billion |

| CAGR (2026–2035) |

8.9% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020 – 2024 |

| Forecast Period |

2026 – 2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Product (Reagents and Kits, Instruments), By Technology (CLIA, ELISA, Fluorescence Immunoassay, RIA), By Application (Infectious Diseases, Oncology, Endocrinology, Cardiology, Autoimmune Diseases), By End-Use (Diagnostic Laboratories, Hospitals, Academic and Research Institutes, Blood Banks), By Test Type (Routine Testing, Specialized Testing) |

| Regional Analysis |

North America – US and Canada; Europe – Germany, France, The UK, Spain, Italy, and Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, and Rest of APAC; Latin America – Brazil, Mexico, and Rest of Latin America; Middle East & Africa – GCC, South Africa, and Rest of MEA |

| Competitive Landscape |

Roche Diagnostics, Abbott Laboratories, Danaher Corporation, Siemens Healthineers, Thermo Fisher Scientific, Bio-Rad Laboratories, Sysmex Corporation, Ortho Clinical Diagnostics (QuidelOrtho), Agilent Technologies, Revvity (PerkinElmer), DiaSorin, bioMérieux, Mindray, Randox Laboratories, Snibe Co., Ltd. |

| Customization Scope |

Customization for segments and region or country level will be provided. Additional customization can be done based on requirements. |

| Purchase Options |

Three license options: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |

Frequently Asked Questions

What is the current size of the global Immunochemistry Instruments and Reagents Market?

▾ The global Immunochemistry Instruments and Reagents Market is valued at USD 27.3 Billion in 2025. North America holds the largest regional share at 42.0%, equivalent to USD 11.4 Billion, with the US alone accounting for USD 10.1 Billion.

What is the forecast growth rate through 2035?

▾ The market is forecast to reach USD 64.4 Billion by 2035, growing at a CAGR of 8.9% over the 2026 to 2035 period. The US market is projected to reach USD 20.4 Billion by 2035 at a slightly lower CAGR of 7.9%, reflecting its more mature starting base.

Which segment holds the largest revenue share?

▾ Reagents and Kits lead the By Product segment with a 67.2% revenue share in 2026. Every installed analyzer generates ongoing reagent procurement, making this the most commercially stable and predictable revenue stream in the market.

Which technology segment leads and why?

▾ CLIA holds the leading technology share at 36.9%. Its combination of high analytical sensitivity, full automation compatibility, and an expanding cleared assay menu positions it as the technology with the strongest near-term commercial momentum across both routine screening and specialty testing applications.

Which region offers the strongest expansion opportunity?

▾ Asia Pacific, and India specifically, offers the most clearly quantified expansion opportunity. Reagents represent over 91% of India's immunochemistry market value, and local manufacturing capability is the primary lever for competing on price in that environment.

What is the biggest challenge facing market participants?

▾ The two most significant structural challenges are the high capital cost of automated immunoassay platforms, which limits instrument penetration in emerging-market and smaller-laboratory settings, and prolonged regulatory approval timelines that delay commercialization of new assays and represent foregone reagent revenue during the review period.