Market Overview

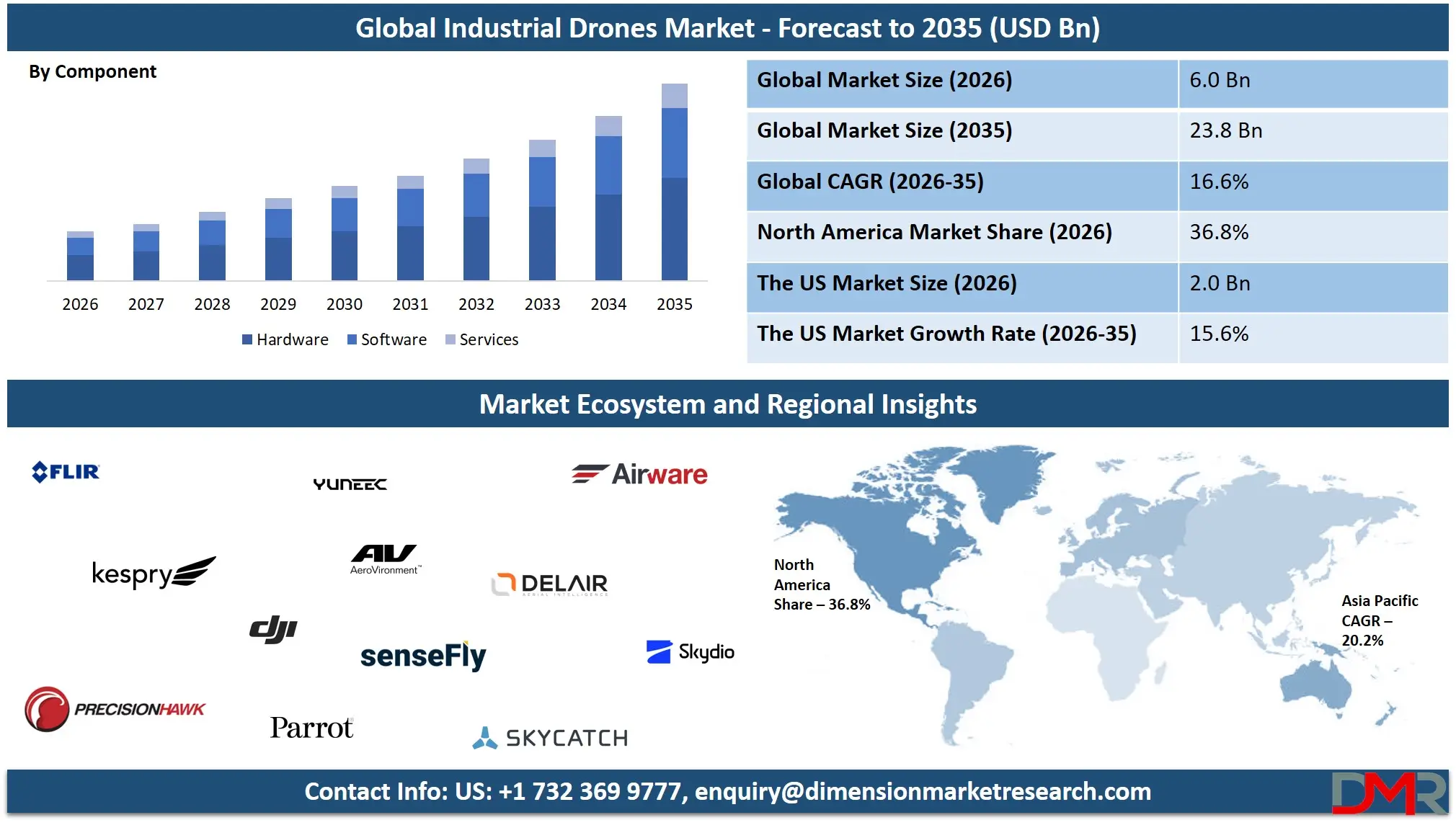

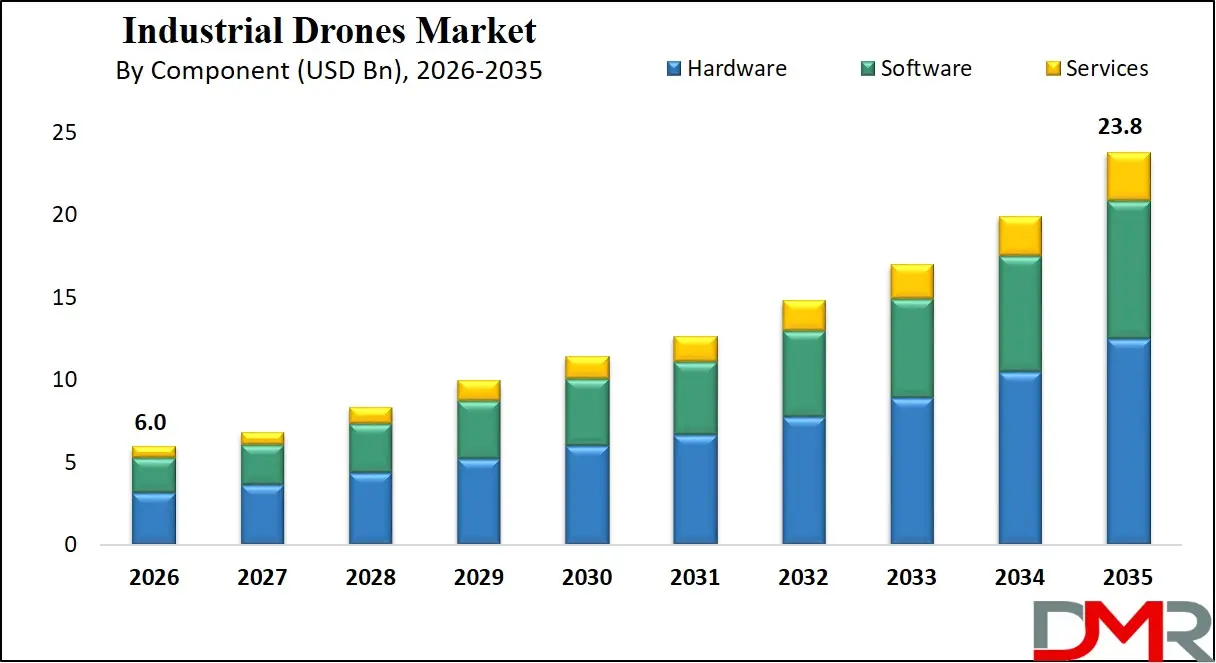

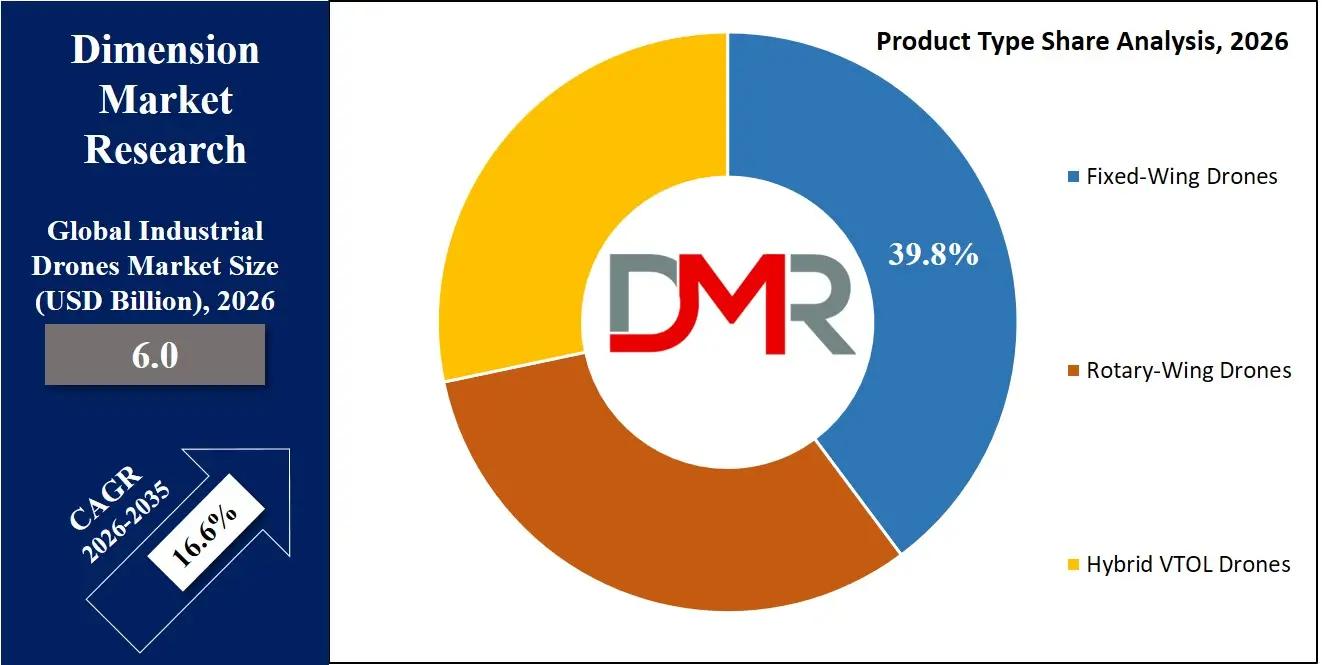

The Global Industrial Drones Market size is projected to reach USD 6.0 billion in 2026 and grow at a compound annual growth rate of 16.6% to reach a value of USD 23.8 billion in 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Industrial drones are unmanned aerial vehicles (UAVs) built specifically for commercial and industrial use across sectors such as agriculture, infrastructure inspection, mining, oil & gas, utilities, logistics, and public safety. They combine robust hardware airframes, propulsion systems, flight controllers, and advanced payloads like LiDAR, thermal, and multispectral sensors with intelligent software for flight planning, analytics, and autonomous navigation. Unlike consumer drones, industrial models are designed for durability, longer range, higher payload capacity, and strict regulatory compliance, making them suitable for demanding enterprise environments.

These drones have become mainly important as industries look for safer, faster, and more cost-effective alternatives to manual inspections and monitoring. As industrial assets become more digital and connected, drones play a key role in collecting real-time data for predictive maintenance and performance optimization. Technologies such as AI and computer vision are turning drones into smart tools that not only capture images but also analyze and interpret data. This shift is driving wider adoption across infrastructure, energy, and agriculture.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Improvements in battery life, hybrid VTOL designs, and cloud-based fleet management platforms are making drone operations more scalable and efficient. Clearer regulations and growing approvals for beyond-visual-line-of-sight (BVLOS) flights are opening up new commercial possibilities. As organizations move from small pilot projects to full-scale deployment, industrial drones are becoming a standard part of modern industrial operations.

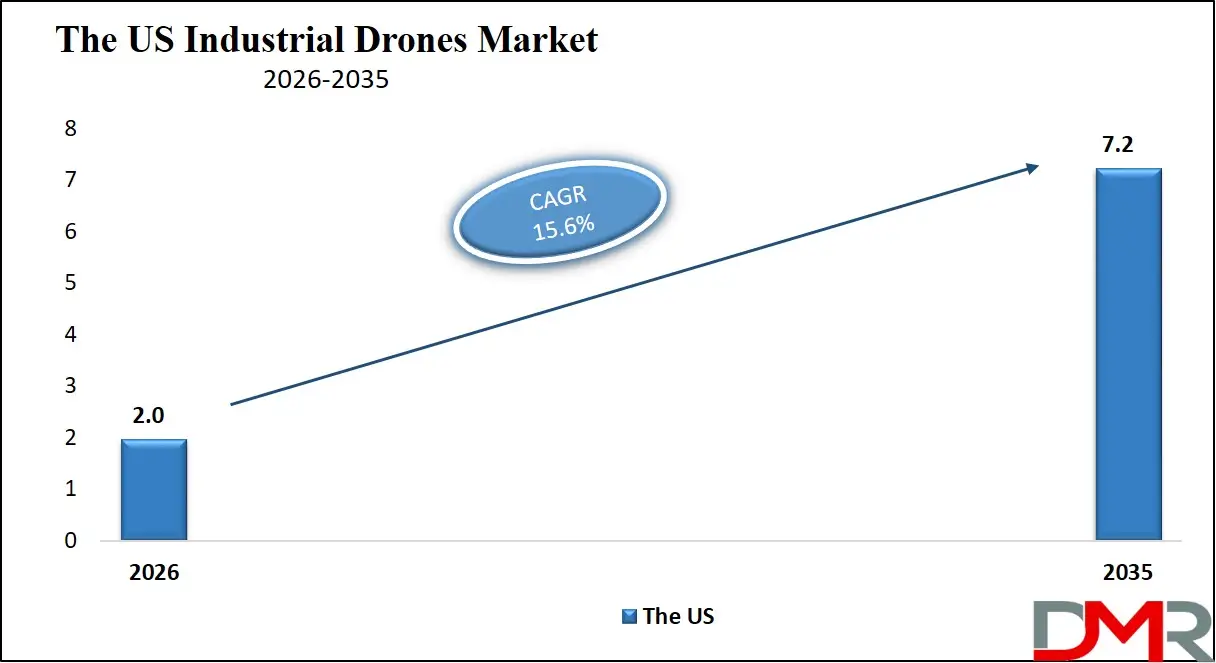

The US Industrial Drones Market

The US Industrial Drones Market size is projected to reach USD 2.0 billion in 2026 at a compound annual growth rate of 15.6% over its forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US represents a technologically advanced and innovation-driven environment for industrial drones. Strong participation from aerospace technology firms, software developers, and defense contractors has strengthened domestic manufacturing and R&D capabilities. Federal Aviation Administration (FAA) frameworks, including Part 107 rules and incremental BVLOS approvals, have facilitated structured commercial expansion. Utilities, oil & gas, and large-scale agriculture are leading adopters, leveraging drones for predictive maintenance and yield optimization. Government infrastructure spending programs and smart city initiatives further stimulate demand. The presence of venture capital investment and startup ecosystems accelerates product innovation, particularly in AI-enabled autonomy and drone-as-a-service (DaaS) models.

Europe Industrial Drones Market

Europe Industrial Drones Market size is projected to reach USD 1.5 billion in 2026 at a compound annual growth rate of 15.9% over its forecast period.

Europe’s market growth is closely tied to regulatory harmonization under the European Union Aviation Safety Agency (EASA) framework. The European Green Deal and sustainability-focused industrial policies are encouraging drone use in renewable energy monitoring, precision agriculture, and environmental compliance tracking. Countries such as Germany, France, and the UK lead adoption in infrastructure inspection and construction digitization. Strong emphasis on data privacy and airspace safety shapes product design and operational protocols. Collaborative cross-border drone corridors and urban air mobility trials are fostering innovation. Industrial digitization initiatives and smart infrastructure upgrades are accelerating deployment across utilities and transportation sectors.

Japan Industrial Drones Market

Japan Industrial Drones Market size is projected to reach USD 300 million in 2026 at a compound annual growth rate of 15.5% over its forecast period.

Japan’s industrial drones landscape is driven by advanced manufacturing, aging workforce challenges, and strong government-backed automation initiatives. The country promotes drone deployment for infrastructure inspection, disaster management, and precision agriculture, particularly in rural regions facing labor shortages. Urban density and frequent natural disasters create strong demand for rapid aerial assessment and resilient monitoring systems. The government’s roadmap for unmanned traffic management (UTM) and autonomous logistics supports commercialization. Japanese firms emphasize compact, high-precision drone systems integrated with robotics and IoT ecosystems. While regulatory caution remains, increasing pilot projects in smart cities and industrial automation are expanding long-term growth opportunities.

Industrial Drones Market: Key Takeaways

- Market Growth: The Industrial Drones Market size is expected to grow by USD 16.9 billion, at a CAGR of 16.6%, during the forecasted period of 2027 to 2035.

- By Service Type: The fixed-wing drone segment is anticipated to get the majority share of the Industrial Drones Market in 2026.

- By Component: The hardware segment is expected to get the largest revenue share in 2026 in the Industrial Drones Market.

- Regional Insight: North America is expected to hold a 36.8% share of revenue in the Global Industrial Drones Market in 2026.

- Use Cases: Some of the use cases of Industrial Drones include precision agriculture, infrastructure inspection, and more.

Industrial Drones Market: Use Cases

- Precision Agriculture: Drones enable crop health monitoring, spraying, and soil analysis through multispectral imaging and automated flight mapping, improving yields and reducing chemical usage.

- Infrastructure Inspection: Industrial drones inspect bridges, roads, and buildings, reducing manual risk while providing high-resolution structural diagnostics.

- Oil & Gas Monitoring: UAVs perform pipeline surveillance and asset inspections in hazardous or remote locations, lowering operational downtime.

- Mining Surveying: Equipped with LiDAR and photogrammetry tools, drones generate topographical maps and conduct volumetric calculations for operational planning.

- Utility Asset Management: Powerline and renewable energy infrastructure inspections enhance reliability and predictive maintenance efficiency.

- Logistics & Delivery: Autonomous drones facilitate last-mile delivery and warehouse inventory tracking in controlled industrial environments.

- Public Safety & Disaster Response: Rapid aerial deployment supports search and rescue, disaster assessment, and emergency coordination.

Stats & Facts

- Federal Aviation Administration reported in 2024 that over 400,000 commercial drones were registered in the United States.

- European Union Aviation Safety Agency stated in 2025 that all EU member states have implemented unified drone operation categories under EASA regulations.

- U.S. Department of Agriculture indicated in 2024 that precision agriculture technologies are deployed across more than 30% of large-scale farms.

- International Energy Agency reported in 2024 that renewable power capacity additions reached over 500 GW globally.

- U.S. Department of Energy noted in 2025 that grid modernization investments exceeded USD 39 billion in federal allocations.

- Japan Ministry of Land, Infrastructure, Transport and Tourism announced in 2024 expanded Level 4 drone operation permissions in designated zones.

- European Commission reported in 2025 that over EUR 1 trillion remains allocated under Green Deal–linked sustainability programs.

- U.S. Bureau of Labor Statistics recorded in 2024 continued labor shortages in construction and utilities sectors exceeding 300,000 positions.

- International Civil Aviation Organization confirmed in 2024 increased global adoption of unmanned traffic management frameworks.

- U.S. Geological Survey highlighted in 2025 expanded use of aerial LiDAR mapping for environmental monitoring programs.

Market Dynamic

Driving Factors in the Industrial Drones Market

Technological Advancements in AI and Sensor Integration

Rapid innovation in AI-driven navigation, computer vision, and high-resolution sensor technologies is significantly enhancing industrial drone capabilities. Advanced LiDAR, hyperspectral imaging, and thermal sensors allow precise data collection for predictive maintenance and asset monitoring. Improvements in battery efficiency and hybrid propulsion systems extend flight endurance, enabling long-range operations. Cloud connectivity and real-time analytics platforms convert aerial data into actionable insights, improving operational efficiency. These advancements reduce operational costs, minimize human risk in hazardous environments, and accelerate enterprise-scale adoption across energy, agriculture, and infrastructure sectors.

Infrastructure Modernization and Automation Demand

Global infrastructure modernization initiatives and industrial automation strategies are boosting demand for aerial inspection and data solutions. Aging bridges, power grids, and oil pipelines require frequent monitoring, and drones provide faster and safer alternatives to manual inspection. Industrial sectors are increasingly adopting digital twins and predictive maintenance systems, where drone-generated data plays a central role. Labor shortages in developed economies further push companies toward automation. As industries seek cost optimization and operational resilience, drone integration becomes a strategic investment rather than an experimental technology.

Restraints in the Industrial Drones Market

Regulatory and Airspace Restrictions

Airspace management regulations, including restrictions on beyond-visual-line-of-sight operations, urban deployment, and cross-border flights, limit full commercial scalability. Certification requirements and compliance procedures can be time-consuming and costly for manufacturers and operators. Variability in regulations across countries adds operational complexity for multinational companies. Delays in airspace integration frameworks may hinder expansion into logistics and urban mobility applications, slowing broader adoption in densely populated regions.

High Initial Capital and Integration Costs

Industrial-grade drones equipped with advanced sensors and autonomous systems involve substantial upfront investment. Integration with enterprise software systems, training personnel, and ensuring cybersecurity compliance increase total ownership costs. Small and medium-sized enterprises may face financial barriers, slowing adoption rates. Maintenance, battery replacement, and software upgrades add recurring costs, influencing procurement decisions and delaying fleet expansion.

Opportunities in the Industrial Drones Market

Expansion of BVLOS and Autonomous Operations

Broader regulatory approvals for BVLOS operations open new commercial opportunities in logistics, infrastructure monitoring, and rural connectivity. Autonomous fleet operations supported by AI-driven traffic management systems can significantly expand operational range and efficiency. As governments refine unmanned traffic systems, enterprises gain scalability advantages, unlocking revenue streams in remote inspections and automated delivery services.

Growth in Renewable Energy and Smart Infrastructure

The expansion of solar farms, wind parks, and smart grid systems presents substantial opportunity for drone-enabled inspection and maintenance services. Renewable energy installations require regular performance monitoring, which drones can deliver efficiently. Integration with IoT-enabled smart infrastructure platforms enhances data-driven asset management, creating long-term service contracts and recurring revenue models.

Trends in the Industrial Drones Market

Shift Toward Drone-as-a-Service (DaaS)

Organizations increasingly prefer subscription-based drone services rather than direct asset ownership. DaaS models reduce capital expenditure while providing access to certified pilots, analytics software, and maintenance support. This model enhances accessibility for SMEs and accelerates market penetration across multiple industries.

Integration with Digital Twins and Cloud Ecosystems

Industrial drones are becoming integral components of digital twin frameworks. Real-time aerial data feeds into cloud-based simulation models, improving predictive analytics and infrastructure lifecycle management. Seamless integration with enterprise resource planning (ERP) and asset management systems strengthens operational intelligence and long-term strategic planning.

Impact of Artificial Intelligence in Industrial Drones Market

- Autonomous Navigation: AI enables obstacle detection and adaptive flight routing for safer and longer missions.

- Computer Vision Analytics: Real-time defect detection improves inspection accuracy in infrastructure and utilities.

- Predictive Maintenance Models: AI-driven analytics forecast equipment failures using drone-collected data.

- Fleet Management Optimization: Intelligent scheduling enhances operational efficiency and reduces downtime.

- Data Processing Automation: Machine learning accelerates image and LiDAR data interpretation.

- Precision Agriculture Insights: AI algorithms assess crop health and recommend targeted interventions.

- Enhanced Safety Systems: Automated emergency landing and collision avoidance systems reduce operational risks.

- Autonomous Delivery Systems: AI supports route optimization and last-mile logistics efficiency.

Research Scope and Analysis

By Product Type Analysis

Fixed-wing drones are expected to account for 39.8% market share in 2026, maintaining a strong position due to their extended flight endurance, higher cruising speeds, and suitability for large-area mapping and surveying applications. These drones are widely used in mining, agriculture, oil & gas pipeline monitoring, and environmental assessment where long-range coverage is critical. Their aerodynamic efficiency enables longer flight times compared to multi-rotor systems, reducing operational interruptions and improving data acquisition efficiency. Integration with LiDAR and hyperspectral imaging enhances their value in geospatial intelligence and volumetric analysis. Government-backed infrastructure modernization programs and the growing need for topographical surveying further support their continued dominance in industrial-scale operations.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Hybrid vertical take-off and landing (VTOL) drones represent the fastest-growing segment due to their ability to combine the endurance of fixed-wing platforms with the hovering flexibility of rotary-wing drones. These systems are increasingly preferred in remote infrastructure inspection and utility monitoring applications where runway access is limited. Advancements in battery density and lightweight composite materials are improving operational performance. Growing adoption in logistics and energy asset monitoring is accelerating deployment. As industries demand operational flexibility and extended coverage, hybrid VTOL platforms are projected to witness significant expansion over the forecast period.

By Payload Capacity Analysis

The 5–10 kg payload category is projected to hold 29.6% market share in 2026, driven by its balance between carrying advanced sensors and maintaining flight efficiency. This capacity range supports LiDAR systems, thermal cameras, and multispectral sensors used in infrastructure inspection, mining, and renewable energy monitoring. Enterprises favor this segment for mid-scale industrial tasks requiring sophisticated data capture without compromising maneuverability. Increasing demand for detailed aerial analytics and industrial compliance monitoring is reinforcing its leadership.

The above 10 kg segment is expanding rapidly, particularly in logistics, heavy industrial inspection, and defense-linked infrastructure monitoring. These drones support high-end payloads including multiple sensors and delivery modules. As battery and propulsion technologies improve, heavier payload drones are becoming more efficient and commercially viable. Their use in long-range BVLOS operations is expected to accelerate growth significantly.

By Component Analysis

Hardware is anticipated to dominate with 52.4% market share in 2026, as industrial drones require durable airframes, propulsion systems, advanced sensors, and high-performance flight controllers. The demand for ruggedized components suitable for harsh environments in mining, oil & gas, and utilities strengthens this segment. Continuous innovation in composite materials and sensor miniaturization enhances performance and reliability, reinforcing hardware’s central role in industrial drone deployment.

Software is the fastest-growing component segment, fueled by AI-driven analytics, cloud integration, and autonomous flight management systems. Industrial users increasingly rely on real-time data processing, predictive analytics, and digital twin integration platforms. Subscription-based software models are accelerating adoption and generating recurring revenue streams.

By Technology Analysis

AI and computer vision technologies are projected to hold 27.9% market share in 2026, reflecting their central role in transforming industrial drones from data-capture devices into intelligent decision-support systems. These technologies enable automated defect detection in bridges, powerlines, pipelines, and construction assets through real-time image processing and deep learning algorithms. Advanced object recognition and anomaly detection significantly reduce manual inspection time while improving accuracy and consistency. AI-powered obstacle avoidance enhances flight safety, particularly in dense urban or industrial environments. Integration with digital twin platforms and predictive maintenance systems further strengthens enterprise adoption. As industries prioritize automation, safety compliance, and operational efficiency, AI and computer vision remain foundational to next-generation industrial drone capabilities.

LiDAR technology is witnessing rapid expansion due to its high-precision terrain modeling, volumetric analysis, and structural mapping capabilities. It plays a crucial role in mining surveys, forestry management, corridor mapping, and infrastructure planning. LiDAR-equipped drones generate highly accurate 3D point clouds, even in low-light or densely vegetated environments, providing advantages over conventional photogrammetry. Integration with fixed-wing and hybrid VTOL platforms enhances coverage efficiency across large geographies. As demand increases for topographical intelligence in renewable energy installations, transportation networks, and smart city development, LiDAR adoption continues to accelerate. Falling sensor costs and miniaturization trends are making the technology more commercially viable, positioning it as a high-growth enabler of advanced geospatial analytics.

By Application Analysis

Infrastructure and construction are expected to account for 21.7% market share in 2026, supported by increasing investments in smart cities, transportation corridors, and urban redevelopment projects. Drones are widely deployed for bridge inspections, high-rise façade assessments, site progress monitoring, and structural integrity analysis. By enabling rapid aerial surveys and 3D modeling, they help construction firms improve project planning and reduce costly delays. Integration with Building Information Modeling (BIM) and digital twin technologies enhances real-time project tracking and asset lifecycle management. Safety improvements are another key driver, as drones minimize the need for workers to access hazardous or elevated locations. As governments continue infrastructure modernization initiatives, this segment is expected to maintain strong and sustained demand.

Agriculture is expanding rapidly due to the global shift toward precision farming and resource optimization. Industrial drones assist in crop health monitoring, multispectral imaging, automated spraying, and soil condition analysis. These capabilities allow farmers to apply fertilizers and pesticides with greater accuracy, reducing input costs and environmental impact. Labor shortages in rural regions and the increasing need to enhance crop yields are accelerating adoption, especially in large-scale farming economies. Integration with AI-based analytics platforms enables predictive yield assessment and disease detection. As climate variability increases and food security concerns grow, agricultural stakeholders are increasingly relying on drone-based intelligence to improve productivity, sustainability, and operational resilience.

By Operation Mode Analysis

Remotely piloted drones are projected to hold 46.3% market share in 2026, largely because regulatory frameworks across major markets continue to emphasize supervised and controlled operations. Enterprises prioritize operational reliability, compliance, and risk mitigation, particularly when operating near critical infrastructure or populated areas. Remotely piloted systems provide greater human oversight, ensuring adherence to safety protocols and airspace restrictions. This mode remains prevalent in utilities, oil & gas, and infrastructure inspection, where manual verification is often required. Training programs and certification standards further support this segment’s leadership. While automation is advancing, supervised operations continue to represent the most commercially established and regulator-approved deployment model.

Fully autonomous drones are the fastest-growing operation mode due to rapid advancements in AI navigation, onboard computing, and unmanned traffic management systems. These drones can execute pre-programmed missions, perform real-time decision-making, and return to base without human intervention. Autonomous systems significantly reduce labor costs and enable scalable fleet operations across geographically dispersed assets. Regulatory progress in beyond-visual-line-of-sight (BVLOS) approvals is further unlocking commercial potential. Industries such as logistics, renewable energy, and large-scale agriculture are increasingly adopting autonomous fleets for continuous monitoring and delivery tasks. As confidence in AI-driven safety systems grows, fully autonomous drones are expected to gain substantial market traction.

By Range Analysis

Medium-range drones are anticipated to capture 38.5% market share in 2026, as they offer an optimal balance between operational endurance and cost efficiency. These drones are particularly suitable for utilities inspection, agricultural monitoring, and infrastructure assessments that require moderate coverage areas. Their manageable operational requirements and compatibility with existing regulatory frameworks make them attractive for enterprise deployment. Medium-range systems often integrate advanced sensors while maintaining portability and flexible deployment capabilities. This versatility supports their widespread adoption across multiple industries, ensuring continued dominance within industrial applications that require routine monitoring and inspection over defined geographic zones.

Long-range drones are expanding quickly, driven by increasing regulatory permissions for BVLOS operations and growing demand for remote asset surveillance. These drones are extensively used in oil & gas pipeline monitoring, environmental surveillance, border security, and large-scale renewable energy asset inspections. Extended endurance and advanced communication systems enable coverage of vast and inaccessible terrains. Technological improvements in battery efficiency and hybrid propulsion systems are enhancing mission duration and reliability. As industries expand into remote regions and prioritize continuous asset monitoring, long-range drones are becoming critical tools for operational efficiency and risk management.

By End User Analysis

Utilities are expected to command 24.1% market share in 2026, driven by rising demand for powerline inspections, renewable asset monitoring, and grid modernization initiatives. Drones significantly improve inspection speed and accuracy while reducing operational downtime and worker safety risks. Thermal imaging and AI-based defect detection enable predictive maintenance of substations, transmission lines, and wind turbines. Increasing integration with smart grid infrastructure strengthens data-driven asset management strategies. As energy systems become more decentralized and renewable-focused, utility companies are scaling drone deployments to enhance resilience, improve outage response times, and maintain regulatory compliance.

Transportation and logistics represent the fastest-growing end-user segment, fueled by rapid e-commerce expansion and the pursuit of automated supply chain solutions. Industrial drones are being deployed for last-mile delivery trials, warehouse inventory monitoring, and yard management operations. Autonomous navigation systems and route optimization software are improving delivery efficiency and reducing operational costs. Governments and private operators are piloting drone corridors and urban air mobility frameworks to support commercial scaling. As logistics networks prioritize speed, transparency, and automation, drone integration is becoming a strategic enabler of next-generation distribution ecosystems.

The Industrial Drones Market Report is segmented on the basis of the following:

By Product Type

- Fixed-Wing Drones

- Rotary-Wing Drones

- Multi-rotor

- Quadcopter

- Hexacopter

- Octocopter

- Hybrid VTOL Drones

By Payload Capacity

- Up to 2 kg

- 2–5 kg

- 5–10 kg

- Above 10 kg

By Component

- Hardware

- Airframe

- Propulsion System

- Flight Control System

- Payload

- Cameras

- LiDAR

- Thermal Sensors

- Multispectral & Hyperspectral Sensors

- Software

- Flight Planning & Navigation

- Data Processing & Analytics

- AI & Autonomous Control

- Services

- Integration & Deployment

- Maintenance & Repair

- Training & Support

By Technology

- GPS/GNSS Navigation

- AI & Computer Vision

- LiDAR

- Thermal Imaging

- Hyperspectral Imaging

By Application

- Agriculture

- Crop Monitoring

- Spraying & Seeding

- Infrastructure & Construction

- Site Monitoring

- Structural Inspection

- Oil & Gas

- Pipeline Inspection

- Asset Monitoring

- Mining

- Surveying

- Volume Calculation

- Utilities

- Powerline Inspection

- Renewable Asset Monitoring

- Logistics

- Last-Mile Delivery

- Inventory Management

- Public Safety

- Search & Rescue

- Disaster Assessment

- Environmental Monitoring

- Wildlife Monitoring

- Land & Water Assessment

By Operation Mode

- Remotely Piloted

- Semi-Autonomous

- Fully Autonomous

By Range

- Short Range

- Medium Range

- Long Range

By End-User Industry

- Agriculture

- Construction & Infrastructure

- Oil & Gas

- Mining

- Utilities

- Transportation & Logistics

- Public Safety

Regional Analysis

Leading Region in the Industrial Drones Market

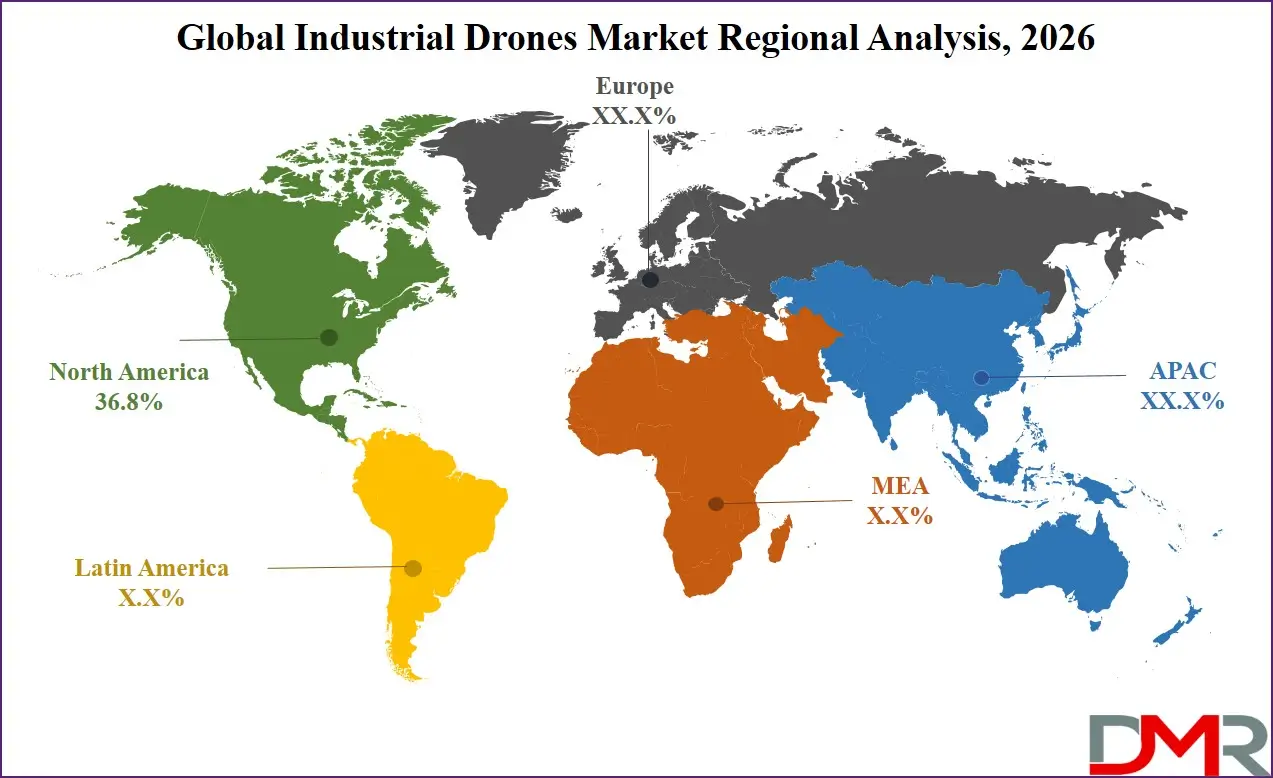

North America is projected to lead with 36.8% market share in 2026, supported by advanced regulatory structures, strong aerospace manufacturing capabilities, and widespread enterprise adoption. The region benefits from well-established R&D ecosystems and significant venture capital funding, accelerating innovation in AI-enabled autonomy and sensor integration. Federal investments in infrastructure modernization and grid resilience programs create sustained demand across utilities and construction sectors. The presence of structured FAA regulatory pathways, including expanding BVLOS permissions and drone corridor initiatives, further strengthens commercial scalability. High adoption in oil & gas, agriculture, and public safety applications reinforces North America’s dominant and technologically advanced market position.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest Growing Region in the Industrial Drones Market

Asia-Pacific is witnessing the fastest growth due to rapid industrialization, infrastructure expansion, and smart city initiatives across major economies such as China, Japan, South Korea, and India. Governments are actively promoting automation, renewable energy deployment, and digital infrastructure development, all of which increase demand for aerial monitoring solutions. Agricultural modernization programs and rural labor shortages are accelerating precision farming adoption. Expanding logistics networks and e-commerce ecosystems further support drone deployment in warehouse automation and delivery services. Regulatory advancements and investment in unmanned traffic management systems are strengthening the region’s long-term growth trajectory, positioning Asia-Pacific as a key expansion hub for industrial drone manufacturers and service providers.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The industrial drones market is characterized by technological innovation, strategic partnerships, and increasing vertical integration. Companies focus on enhancing AI capabilities, sensor performance, and flight endurance to differentiate offerings. Strategic collaborations with software providers and infrastructure firms strengthen ecosystem positioning. Entry barriers include regulatory certification, capital-intensive R&D, and airspace compliance requirements. Many players are shifting toward service-based models to ensure recurring revenue streams. Continuous investment in autonomous navigation, cybersecurity, and cloud integration remains central to maintaining competitive advantage in an evolving industrial automation environment.

Some of the prominent players in the global Industrial Drones are:

- DJI

- Parrot SA

- AeroVironment

- Skydio

- Yuneec

- senseFly

- Delair

- PrecisionHawk

- Kespry

- Terra Drone Corporation

- Autel Robotics

- 3D Robotics

- Insitu (Boeing)

- FLIR/Teledyne FLIR

- Intel Corporation

- Aeryon Labs

- Skycatch

- Airware

- Microdrones

- Percepto

- Other Key Players

Recent Developments

- In February 2026, Corvus Robotics has introduced Corvus One for Cold Chain, an autonomous aerial inventory system designed to operate in freezer environments reaching minus 20°F. Built on the existing Corvus One platform, the solution enables continuous, fully autonomous drone operations in highly challenging cold storage conditions. The system required major engineering enhancements, including redesigned thermal management, advanced sensing capabilities, improved flight stability, and strengthened onboard perception to maintain operational accuracy despite frost buildup, glare, airflow disruptions, and extreme temperature fluctuations common in industrial freezer facilities.

- In February 2026, Electro Optic Systems (EOS) has formed a strategic partnership with ROKETSAN to pursue integrated defence capabilities across selected markets, with the agreement announced at the World Defense Show. EOS contributes counter-drone technologies, including kinetic and high-energy laser systems, highlighted by its 100-kilowatt-class laser export contract with the Netherlands and a conditional agreement in the Republic of Korea. ROKETSAN brings expertise in defence platforms, systems integration, sensors, command-and-control technologies, and directed energy solutions, strengthening the joint ability to deliver advanced integrated defence capabilities.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 6.0 Bn |

| Forecast Value (2035) |

USD 23.8 Bn |

| CAGR (2026–2035) |

16.6% |

| The US Market Size (2026) |

USD 2.0 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product Type (Fixed-Wing Drones, Rotary-Wing Drones, Hybrid VTOL Drones), By Payload Capacity (Up to 2 kg, 2–5 kg, 5–10 kg, Above 10 kg), By Component (Hardware, Software, Services), By Technology (GPS/GNSS Navigation, AI & Computer Vision, LiDAR, Thermal Imaging, Hyperspectral Imaging), By Application (Agriculture, Infrastructure & Construction, Oil & Gas, Mining, Utilities, Logistics, Public Safety, Environmental Monitoring), By Operation Mode (Remotely Piloted, Semi-Autonomous, Fully Autonomous), By Range (Short Range, Medium Range, Long Range), By End-User Industry (Agriculture, Construction & Infrastructure, Oil & Gas, Mining, Utilities, Transportation & Logistics, Public Safety) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

DJI, Parrot SA, AeroVironment, Skydio, Yuneec, senseFly, Delair, PrecisionHawk, Kespry, Terra Drone Corporation, Autel Robotics, 3D Robotics, Insitu (Boeing), FLIR/Teledyne FLIR, Intel Corporation, Aeryon Labs, Skycatch, Airware, Microdrones, Percepto, and Other Key Players |

Frequently Asked Questions

How big is the Global Industrial Drones Market?

▾ The Global Industrial Drones Market size is expected to reach USD 6.0 billion by 2026 and is projected to reach USD 23.8 billion by the end of 2035.

Which region accounted for the largest Global Industrial Drones Market?

▾ North America is expected to have the largest market share in the Global Industrial Drones Market, with a share of about 36.8% in 2026.

How big is the Industrial Drones Market in the US?

▾ The US Industrial Drones market is expected to reach USD 2.0 billion by 2026.

Who are the key players in the Industrial Drones Market?

▾ Some of the major key players in the Global Industrial Drones Market include DJI, Parrot, Kespry, and others.

What is the growth rate in the Global Industrial Drones Market?

▾ The market is growing at a CAGR of 16.6 percent over the forecasted period.