What is the Industrial Water Treatment Chemicals Market Size?

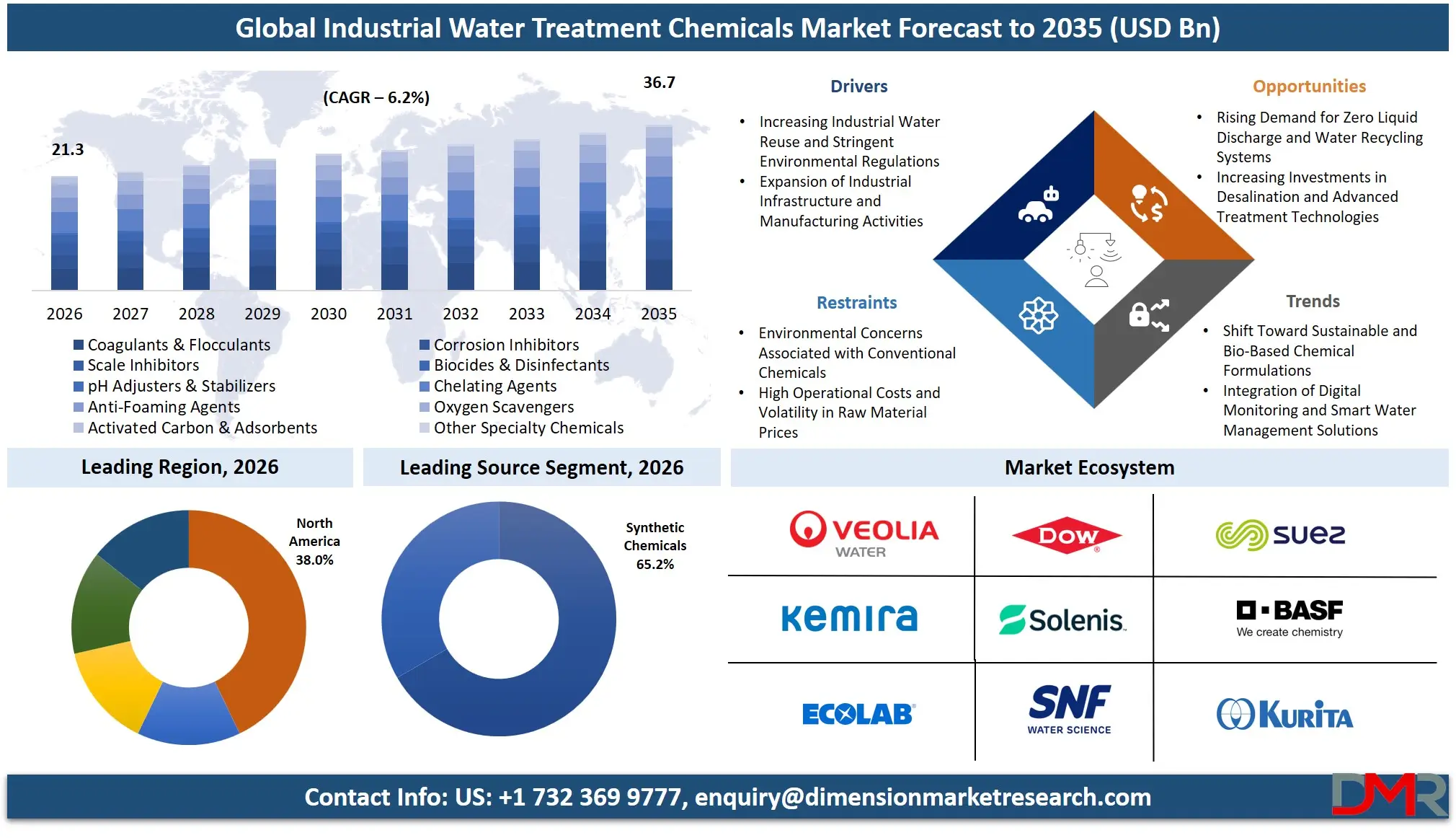

The Global Industrial Water Treatment Chemicals Market is expected to reach a value of USD 21.3 billion in 2026, and it is further anticipated to reach USD 36.7 billion by 2035, growing at a CAGR of 6.2% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market is experiencing consistent growth due to increased pressure on companies to maximize efficiency of water utilization, comply with tight emission standards, and ensure durability of vital equipment and machinery. The market includes coagulants & flocculants, corrosion & scale inhibitors, biocides, pH regulators, and other types of specialty chemicals that help industrial plants perform treatment of process water, cooling water, boiler water, and wastewater. Increasing demand for zero liquid discharge (ZLD) systems, water reuse & recycle projects, and complexities related to varying quality of raw water have increased the need for effective chemical products. Industries like power generation, oil & gas, and chemicals & petrochemicals are major end-users, as they rely on high-quality water and water treatment technology to avoid problems with scaling, fouling, and microbially induced corrosion. Water-stressed areas are speeding up implementation of premium specialty chemicals.

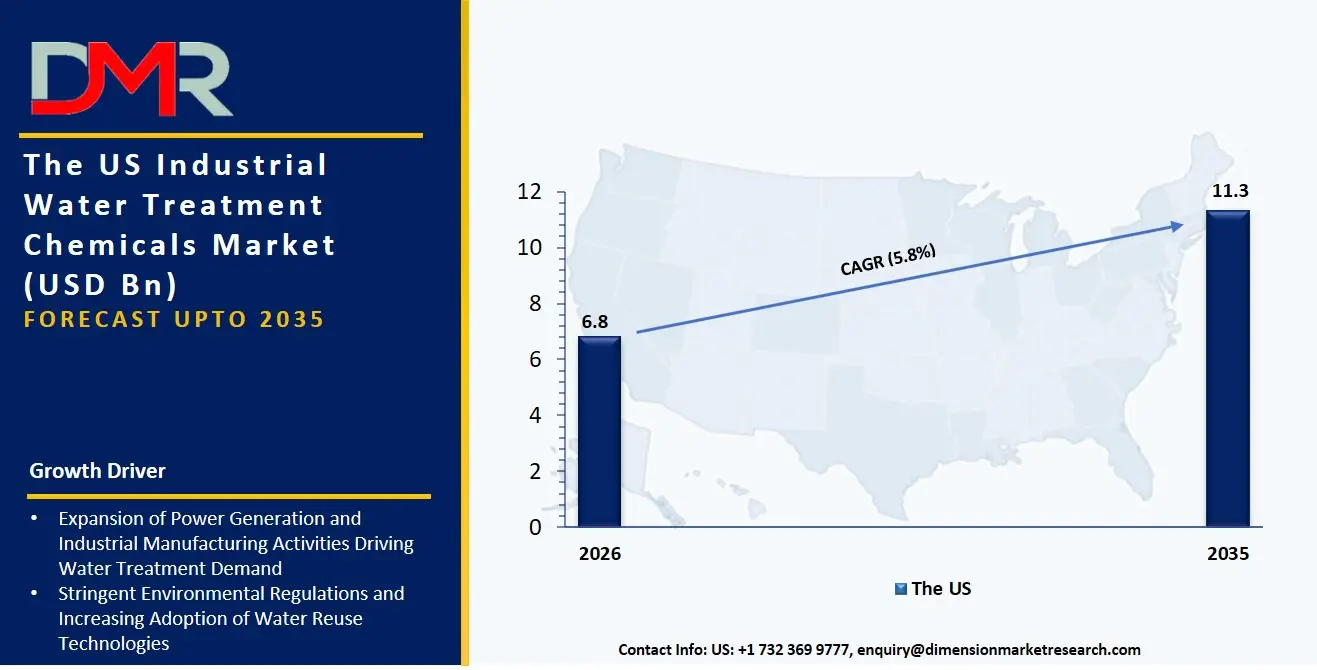

The US Industrial Water Treatment Chemicals Market

The US Industrial Water Treatment Chemicals Market is projected to reach USD 6.8 billion in 2026, growing at a CAGR of 5.8% to reach USD 11.3 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The United States remains a technologically progressive market with significant modernization of existing municipal and industrial water infrastructure and a well-enforced regulatory regime through the EPA. The US market has traditionally been one that features high demand for non-oxidizing biocides and polymer scale inhibitors owing to the need to achieve the highest possible cycles of concentration in cooling towers, with minimal biological growth and corrosion under deposits. The production of large volumes of produced water through shale oil & gas extraction activities is now necessitating the use of high-performance coagulants and flocculants for treatment of the challenging water stream for either deep-well injection or reuse applications.

The Europe Industrial Water Treatment Chemicals Market

The Europe Industrial Water Treatment Chemicals Market is estimated to be valued at USD 6.1 billion in 2026 and is further anticipated to reach USD 10.2 billion by 2035 at a CAGR of 5.9%. Regulatory environment factors such as the Industrial Emissions Directive (IED) and stricy REACH compliance rules for chemicals affect the European market and fuel the need for bio-based and easily biodegradable water treatment chemicals. Growth in reuse and recycling water treatment applications is observed in the region where the food & beverages and textile segments in Germany, France, and Italy work towards minimizing their water footprint by treating highly concentrated organic wastes. Furthermore, pan-European sustainability programs are pushing the limits for chemical manufacturers to invent phosphorus-free scale inhibitors and green chelating agents.

The Japan Industrial Water Treatment Chemicals Market

The Japan Industrial Water Treatment Chemicals Market is projected to be valued at USD 2.2 billion in 2026. It is further expected to witness robust growth, holding USD 3.6 billion in 2035 at a CAGR of 5.6%. The Japanese market stands out with its emphasis on highly purified process water treatment due to the needs of the advanced semiconductor and electronics manufacturing industry. High purity chelating agents, specialized organic coagulants such as PolyDADMAC, and non-oxidizing biocides make up a considerable percentage of expenditures as conglomerates move into smaller chip technologies where any trace of impurity may seriously affect production efficiency. The demand for high integration of the chemical service companies' technical expertise becomes crucial to facilitate the transition from old steel and automotive facilities to the new automated systems for chemical feed.

Key Takeaways

- Market Size & Forecast: According to projections, the Global Industrial Water Treatment Chemicals market size will rise to USD 21.3 billion in 2026 and grow further to USD 36.7 billion by 2035, driven by the increasing water scarcity, as well as by the implementation of the mandatory quality requirements for wastewater discharged from heavy industries.

- Growth Rate & Outlook: The compound annual growth rate for the global market size is predicted to reach 6.2% due to the urgent need for replacing chlorine-based biocides with less harmful chemicals and increasing complexity of preventing scaling during high-stress industrial operations.

- Primary Growth Drivers: These include water reuse and recycling initiatives in order to cut down the consumption of freshwater, the use of corrosion inhibitors to increase the operational life of capital-intensive machinery in the oil and gas industry, and advanced cooling water treatment to avoid Legionella outbreaks.

- Key Market Trends: They include an increased demand for bio-based and "green" specialty chemicals that help companies reach their sustainability goals, the implementation of the digital dosing and control system in order to automatically correct problems with performance within chemical feed systems, and switching from liquid water to solid chemical formulation.

- By Source Analysis: Synthetic chemicals are expected to hold major market volume owing to their effectiveness and economy of use, but biobased chemicals are the fastest-growing sub-segment driven by corporate mandate of ESG toward renewable source material and improved aquatic toxicity profile.

- By End User Industry Analysis: The most profitable end user industries include Power Generation and Oil & Gas because of the large quantity of water treated. Nevertheless, the most precise industry is Semiconductor & Electronics owing to the high purity chemicals necessary for manufacturing the wafers, while Food & Beverage is highly regulated concerning the cooling water treatment according to the FDA requirements.

- Regional Leadership: North America is poised to dominate this market with 38.0% of the market share in 2026 due to the presence of a large number of heavy industries, tight regulations, and investments in unconventional oil & gas water management systems.

What is the Industrial Water Treatment Chemicals?

Industrial Water Treatment Chemicals include the specific chemicals supplied by water treatment firms, chemical suppliers, and custom blenders that are used to condition the source water and treat industrial wastewater. Unlike physical treatment processes, such as filtration or separation, these chemicals deal with the chemistry of the water system. This includes using Coagulants & Flocculants to precipitate and separate out suspended solids from the water, Corrosion and Scale Inhibitors to prevent corrosion and scaling of metal pipes and heat exchangers, Biocides & Disinfectants to kill biological growths, and pH Modifiers to balance the chemical environment. As industries strive for zero liquid discharge, professional chemical management services are required to cope with the complex chemical reactions in water circuits.

Use Cases

- Produced Water Recycling in Oil & Gas: The unconventional producers utilize chemical service providers to provide customized reverse emulsions breaker and organic coagulant for TDS-rich produced water treatment which is recycled in hydraulic fracturing process to minimize the requirement for fresh water and the volume of deep well disposal.

- Legionella Control in Hospitals' Cooling Towers: The healthcare sector employs non-oxidizing biocides along with oxidizing biocides and a monitoring system to manage Legionella pneumophila in their cooling towers according to ASHRAE 188 guidelines without causing any corrosive damage to the chiller loop.

- Membrane Protection in Municipal Desalination: Municipal water departments use phosphonate-based scale inhibition products and membrane cleaners to prevent the formation of calcium carbonate and sulfate scales on RO membranes at desalination plants and keep membrane efficiency intact in drought areas.

- Boiler Feedwater Conditioning in Power Generation: Thermal power stations apply catalyzed oxygen scavengers and pH-adjusting amines to remove oxygen from feedwater for high-pressure steam boiler operation to prevent carbonic acid corrosion.

How AI is Transforming the Industrial Water Treatment Chemicals Market?

The revolution of AI is transforming the industrial water treatment chemicals market by shifting its paradigm from scheduled to predictive chemical feed. In the case of cooling water treatment, AI-based sentinels will be analyzing the ORP signals and flow information to dynamically control the biocides dosing according to real-time microbial growth and thus reduce unnecessary use of chemicals and prevent biofouling incidents. In addition, AI-based process modeling for scale inhibitor dosage makes it possible for chemical companies to accurately predict the scaling indices and control antiscalant injection volume based on changes in the makeup water composition without any human involvement.

The processes of chemical selection and supply chain operations are also becoming AI-driven. With regards to specialty chemical distribution, intelligent procurement tools constantly track water characteristics within the fleet of industrial facilities and identify cost inefficiencies and future chemical demands to optimize truckload delivery and chemical storage. Furthermore, AI-based generative technology complements chemical formulation by conducting simulations of novel biodegradable chelating agents with optimal binding energy with metal ions to evaluate their performance before any wet lab experiments.

Market Dynamics

Key Drivers in the Global Industrial Water Treatment Chemicals Market

Increasing Industrial Water Reuse and Stringent Environmental Regulations

Increased concerns about water shortage and stringent discharge regulations have made it necessary for industries to use advanced technologies for water treatment. Industries like power production, oil and gas, chemicals, and food processing are investing extensively in water treatment chemicals to comply with regulations as well as reuse water. Increased government regulations in terms of wastewater management in both developing and developed nations are increasing the need for coagulants, corrosion inhibitors, and biocides.

Expansion of Industrial Infrastructure and Manufacturing Activities

Industrialization and the production of more products are resulting in the growing need for reliable water treatment systems. Increasing investments in the energy sector, mining, pharmaceuticals, and the manufacturing of semiconductors require proper water treatment to increase efficiency and avoid machine breakdowns. Industrial treatment chemicals aid in preventing scale, corrosion, and biological fouling, leading to increased efficiency and reduced maintenance costs. Growth in industries, especially in the Asia Pacific and the Middle East region, has been creating demand for such chemicals.

Restraints in the Global Industrial Water Treatment Chemicals Market

Environmental Concerns Associated with Conventional Chemicals

Most traditional chemical water treatments are composed of substances which can be potentially harmful to both the environment and public health if released without appropriate precautions. Growing awareness about phosphates, poisonous biocides, and toxic wastes has resulted in more stringent regulations on chemical formulations and their release into the environment, thereby adding to the cost of production for chemical makers. In addition, environmental issues are also prompting some end-users to reduce their use of chemicals.

High Operational Costs and Volatility in Raw Material Prices

The water treatment chemicals industry is faced with problems resulting from variable pricing of petrochemicals and specialty chemicals raw materials used in the production process. Energy cost fluctuations, disruptions in the supply chain, and geo-political instability impact the cost of production and the profit margin. Besides, there are high costs of implementation and maintenance of chemical dosing systems and monitoring. Small and medium size enterprises face financial limitations that prevent them from implementing such advanced programs.

Growth Opportunities in the Global Industrial Water Treatment Chemicals Market

Rising Demand for Zero Liquid Discharge and Water Recycling Systems

Sustainability in water management is opening up new avenues for chemicals utilized in water recycling and zero liquid discharge processes. There has been an increasing adoption of recycling technologies among industries to minimize freshwater intake and adhere to regulation. This has triggered high demand for antiscalants, coagulants, membrane chemicals, and other specialized chemicals. Geographies facing water scarcity, especially in the Asia-Pacific and Middle East regions, are making massive investments in recycling technologies, which will favor growth in the market.

Increasing Investments in Desalination and Advanced Treatment Technologies

Scarcity of fresh water and increasing demands in industries have increased the construction of desalination plants and membrane treatment systems. Special chemicals are needed in these plants for fouling inhibition, cleaning, and protection from corrosion, which creates huge business opportunities for the producers. Fast expansion of the production of desalination plants in countries like Saudi Arabia, the United Arab Emirates, and China is contributing positively towards the development of high-end products.

Trends in the Global Industrial Water Treatment Chemicals Market

Shift Toward Sustainable and Bio-Based Chemical Formulations

More industrial consumers are now using green treatment chemicals for the treatment process in order to be environmentally friendly and meet sustainability goals. Companies have started making green treatment chemicals that are biodegradable, phosphate-free, and organic and help in providing proper treatment without any dangerous by-products. More companies have started focusing on being environmentally responsible, which has helped in this process becoming more common.

Integration of Digital Monitoring and Smart Water Management Solutions

The implementation of technology and intelligent systems in the water treatment industry is revolutionizing the way industrial water treatment systems function. Sensors and advanced automation systems, together with predictive analytics, make it possible to monitor water quality and optimize chemical dosing. They improve process efficiency, eliminate waste, and cut costs. Industrial organizations are gradually adopting IoT-based systems in conjunction with water treatment programs. As a result, it has led to a change in the market, with increased demand for tailor-made chemicals solutions.

Research Scope and Analysis

The Global Industrial Water Treatment Chemicals Market is segmented by product type, source, application, distribution channel, and end-user industry. Coagulants, flocculants, and biocides dominate due to wastewater demand. Synthetic chemicals lead supply, while wastewater treatment is the key application. Power generation, oil & gas, and chemicals are major end users.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

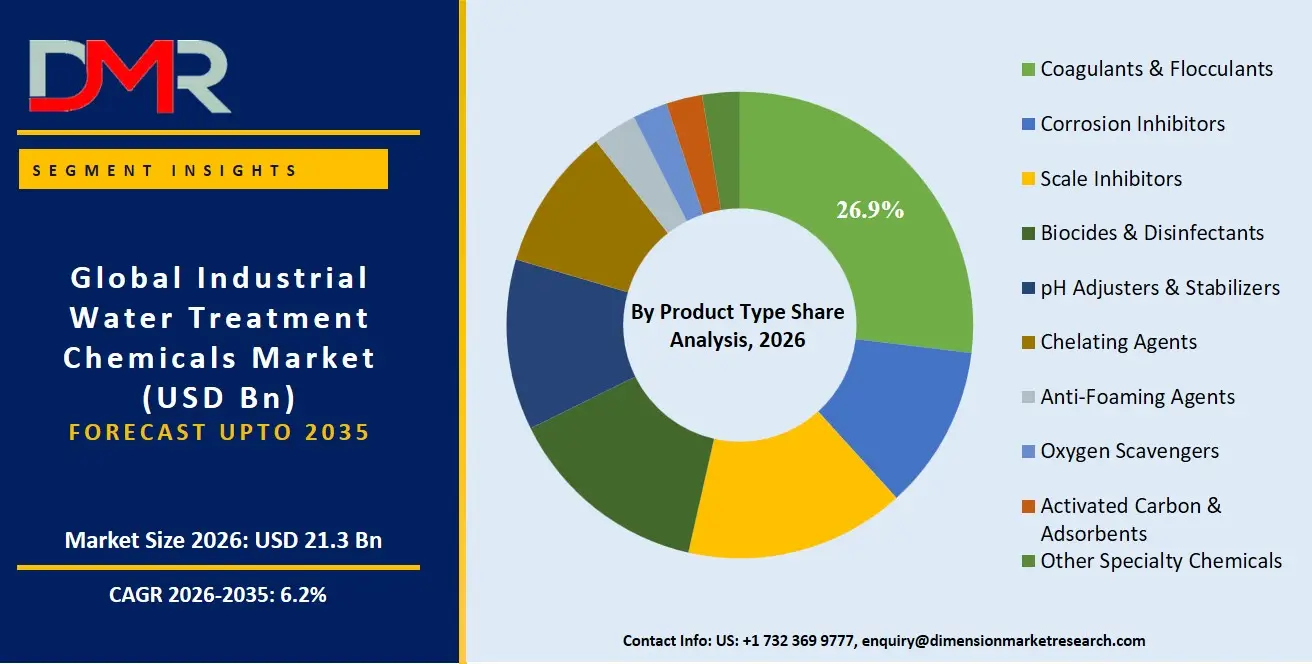

By Product Type Analysis

Coagulants & flocculants is poised to dominate the global industrial water treatment chemicals market because they are indispensable in removing suspended solids, organic matter, and turbidity from industrial water and wastewater streams. These chemicals are extensively used across municipal utilities, power generation, mining, food processing, and chemical manufacturing industries, making them the largest product category. Their broad applicability in clarification, sludge dewatering, and pretreatment processes ensures consistent demand. Increasing regulations regarding wastewater discharge and growing investments in water reuse infrastructure have further strengthened adoption. Inorganic coagulants and polymeric flocculants remain cost-effective and efficient solutions, enabling the segment to maintain its leading position among industrial water treatment chemical products.

By Source Analysis

Synthetic chemicals are projected to dominate the market owing to their superior performance, customization capability, and widespread availability. Industries prefer synthetic formulations because they provide reliable scale control, corrosion protection, microbial management, and process optimization under varying operating conditions. Synthetic products are extensively used in cooling towers, boilers, desalination plants, and wastewater treatment facilities due to their high effectiveness and relatively lower cost. Their long-established manufacturing ecosystem and compatibility with diverse industrial applications contribute to extensive market penetration. Although bio-based alternatives are gaining interest because of sustainability concerns, synthetic chemicals continue to account for the largest market share owing to proven efficiency and broader acceptance across heavy industrial sectors.

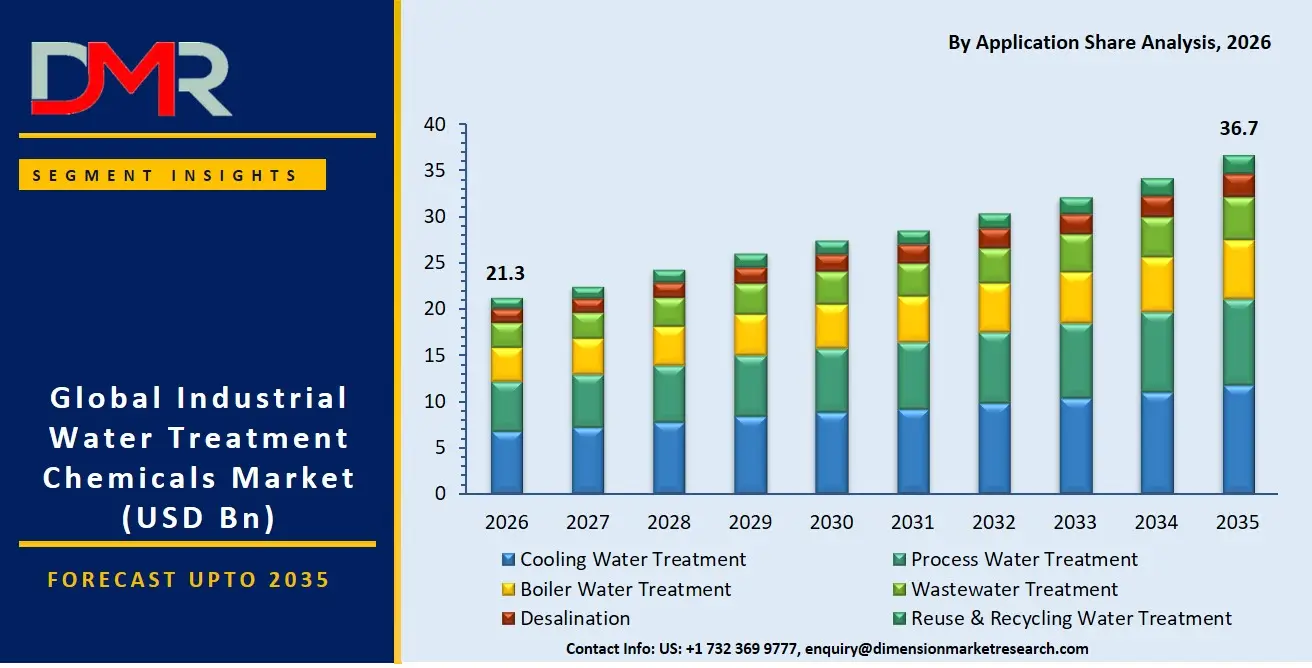

By Application Analysis

Cooling water treatment is anticipated to represent the leading application segment due to its widespread requirement across industries operating heat exchangers and recirculating cooling systems. Power generation facilities, petrochemical plants, mining operations, and manufacturing units depend on efficient cooling systems to maintain equipment performance and reduce downtime.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Chemicals used in cooling water systems prevent microbial contamination, corrosion, and mineral deposition, thereby enhancing operational reliability and extending asset life. Increasing demand for energy-efficient industrial operations and stricter water conservation standards are accelerating adoption. Continuous water circulation and the need for regular chemical replenishment result in significant chemical consumption, enabling cooling water treatment applications to account for the largest market share.

By Distribution Channel Analysis

Direct sales is poised to dominate the industrial water treatment chemicals market because industrial consumers generally require customized solutions, technical support, and long-term service agreements. Major manufacturers prefer direct relationships with large customers such as power plants, oil and gas companies, chemical producers, and municipal utilities to provide application-specific formulations and after-sales services. Direct sales channels facilitate regular monitoring, performance optimization, and efficient supply chain management. Industrial buyers often enter into long-term procurement contracts that ensure product consistency and reliable deliveries. The complexity of water treatment requirements and the importance of technical expertise make direct sales the preferred distribution model, allowing this segment to maintain the largest market share.

By End User Industry Analysis

Power generation is anticipated to dominate the end-user industry segment because thermal and nuclear power plants consume enormous quantities of water for cooling, steam generation, and equipment operation. Efficient water treatment is essential to prevent corrosion, scale buildup, and biological contamination that can reduce plant efficiency and damage critical infrastructure. Continuous chemical dosing requirements in boilers and cooling towers result in substantial consumption of treatment chemicals. Increasing electricity demand worldwide and expansion of power generation capacities further support market growth. Strict regulations governing water quality and wastewater discharge also compel utilities to adopt advanced treatment programs, enabling the power generation sector to maintain its dominant position in the global market.

The Global Industrial Water Treatment Chemicals Market Report is segmented on the basis of the following:

By Product Type

- Coagulants & Flocculants

- Organic Coagulants

- Inorganic Coagulants

- Aluminum Sulfate

- Polyaluminum Chloride

- Ferric Chloride

- Other Inorganic Coagulants

- Flocculants

- Anionic Flocculants

- Cationic Flocculants

- Non-Ionic Flocculants

- Amphoteric Flocculants

- Corrosion Inhibitors

- Organic Corrosion Inhibitors

- Inorganic Corrosion Inhibitors

- Scale Inhibitors

- Phosphonate-Based Scale Inhibitors

- Polymer-Based Scale Inhibitors

- Silicate-Based Scale Inhibitors

- Biocides & Disinfectants

- Oxidizing Biocides

- Non-Oxidizing Biocides

- pH Adjusters & Stabilizers

- Chelating Agents

- EDTA-Based Chelating Agents

- Phosphonate Chelating Agents

- Anti-Foaming Agents

- Oxygen Scavengers

- Activated Carbon & Adsorbents

- Other Specialty Chemicals

By Source

- Synthetic Chemicals

- Bio-Based Chemicals

By Application

- Cooling Water Treatment

- Process Water Treatment

- Boiler Water Treatment

- Wastewater Treatment

- Desalination

- Reuse & Recycling Water Treatment

By Distribution Channel

- Direct Sales

- Distributors & Dealers

- Online Sales

By End User Industry

- Power Generation

- Oil & Gas

- Chemical & Petrochemical

- Mining & Metals

- Food & Beverage

- Pulp & Paper

- Pharmaceuticals

- Textiles

- Semiconductor & Electronics

- Automotive Manufacturing

- Municipal Utilities

- Other Industrial Sectors

Regional Analysis

Leading Region by Market Share

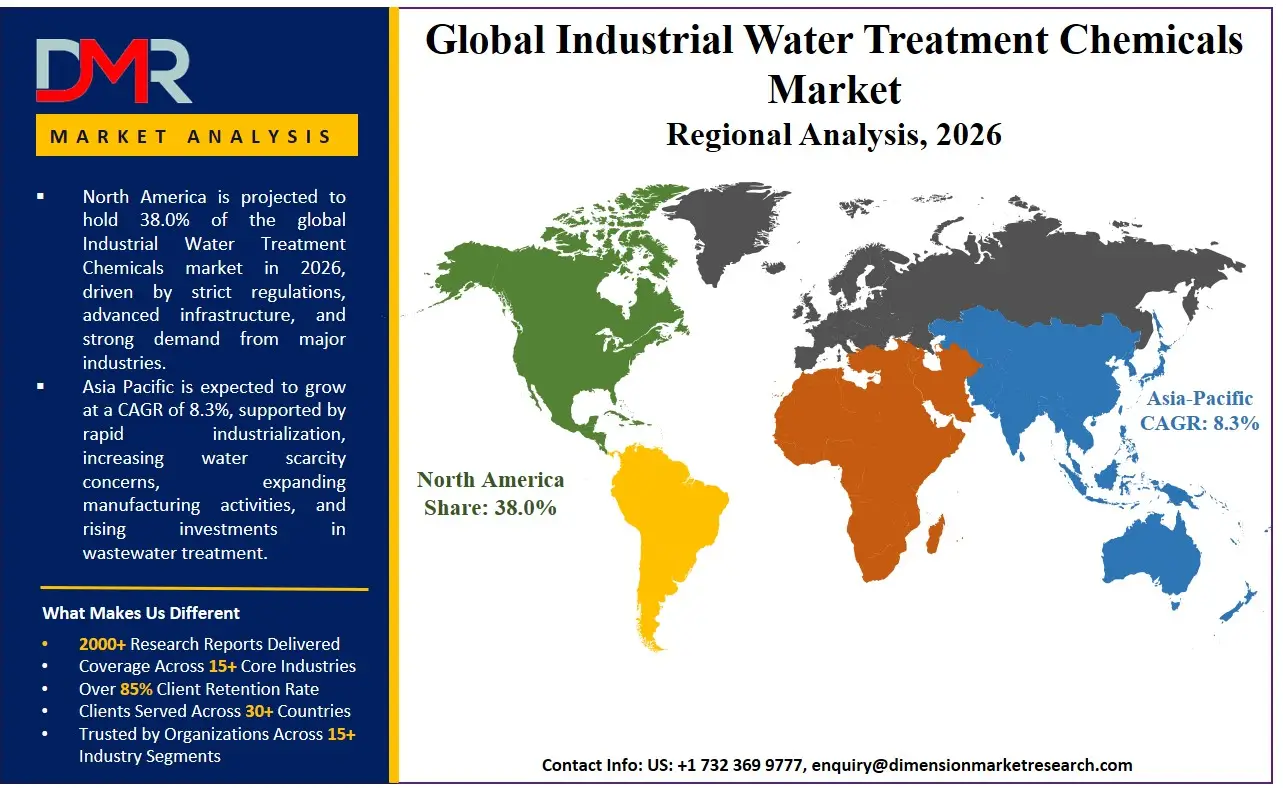

North America is poised to dominate the global industrial water treatment chemicals market, holding a projected 38.0% of the market share by 2026. The United States commands this position due to the sheer scale of its industrial base and the unmatched rigor of its environmental enforcement. The region has an established ecosystem of global chemical manufacturers, specialized water management companies, and a deep pool of field service engineers. Industrial investment in the circular economy, advanced produced water recycling, and the replacement of aging combined sewer systems contributes to the continued demand for high-efficiency polymer coagulants for municipal utilities, alongside sophisticated membrane antiscalants and non-oxidizing biocides for the oil & gas and chemical sectors. Moreover, a strong cost-and-risk management culture perpetuates the outsourcing of water treatment to performance-based chemical service providers.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding industrial water treatment chemicals market, driven by rapid industrialization and severe water quality crises across India, China, and Southeast Asia. The fast-paced growth of coal-fired power generation and heavy manufacturing, coupled with the catastrophic depletion of freshwater resources, is compelling governments and industrial conglomerates to enforce strict zero liquid discharge mandates. This structural shift drives massive demand for precipitated silica antiscalants, high-temperature boiler chemicals, and sludge dewatering flocculants. There is also a severe gap in local technical expertise, necessitating the import of specialty chemicals and direct sales technical support from global chemical firms to design, monitor, and optimize treatment programs for the burgeoning chemical & petrochemical parks in the region.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global industrial water treatment chemicals market has become highly dynamic, featuring a heterogeneous array of multinational chemical conglomerates, specialized regional blenders, and innovative green chemistry start-ups. The key to success will be deep strategic alliances with major EPC contractors and end-users in the power generation and oil & gas sectors, as these relationships provide long-term contracts and operational field data. The movement towards market consolidation is rapidly progressing, with large chemical companies acquiring niche formulators specializing in reverse osmosis (RO) membrane chemicals and cooling water automation software to capture the growing water reuse & recycling segment. Proprietary polymer dispersion technologies and digitized chemical feed automation are becoming a more important basis of competitive differentiation than just commodity price arbitrage or simple bulk chemical delivery.

Some of the prominent players in the Global Industrial Water Treatment Chemicals Market are:

- Ecolab Inc.

- Veolia Water Technologies

- Kurita Water Industries Ltd.

- Solenis LLC

- Kemira Oyj

- SNF Group

- BASF SE

- Dow Inc.

- SUEZ Water Technologies & Solutions

- Buckman Laboratories International Inc.

- Baker Hughes Company

- Nouryon

- Arkema S.A.

- LANXESS AG

- Thermax Limited

- DuPont de Nemours, Inc.

- ChemTreat, Inc.

- Accepta Ltd.

- Italmatch Chemicals S.p.A.

- BWA Water Additives

- Other Key Players

Recent Developments

- January 2026: BASF SE announced a major expansion of its bio-based flocculant production capacity at its European site, an initiative to assist clients in Mining & Metals and Pulp & Paper to achieve their carbon neutrality goals through high-performance, renewable-source chemistries for water recycling and sludge dewatering.

- November 2025: Kurita Water Industries strengthened its collaboration with major semiconductor manufacturers in Japan and introduced a specific practice around ultra-high-purity chelating agents and particle removers, aimed at supporting 2-nanometer chip fabs in maintaining defect-free process water treatment.

- October 2025: Ecolab acquired a data center water optimization firm to further its Nalco Water division's capabilities in non-phosphorus corrosion inhibitors and real-time analytics, supporting the complex water scarcity and cooling water treatment requirements of hyperscale and colocation data centers globally.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 21.3 Bn |

| Forecast Value (2035) |

USD 36.7 Bn |

| CAGR (2026–2035) |

6.2% |

| The US Market Size (2026) |

USD 6.8 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Product Type, By Source, By Application, By Distribution Channel, and By End User Industry |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Industrial Water Treatment Chemicals Market?

▾ The Global Industrial Water Treatment Chemicals market is poised to be valued at USD 21.3 billion in 2026 and is projected to reach USD 36.7 billion by 2035, driven by the universal need for water conservation, process optimization, and stringent discharge compliance across all heavy industries.

What is the CAGR of the Global Industrial Water Treatment Chemicals Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 6.2% from 2026 to 2035, reflecting the tightening complexity of environmental regulations and the persistent requirement for chemical solutions that maintain asset integrity in water-scarce, high-cycle operations.

What factors are driving the growth of the Global Industrial Water Treatment Chemicals Market?

▾ Key drivers include stringent phosphorus and heavy metal discharge limits, the imperative to maximize cooling tower cycles of concentration, the management of complex industrial wastewater streams for reuse, and the surge in demand for bio-based and biodegradable specialty chemicals amid corporate ESG mandates.

Which region held the largest share of the Industrial Water Treatment Chemicals Market in 2026?

▾ North America is poised to hold a 38.0% market share in 2026, driven by a mature energy and industrial sector, rigorous EPA regulation, and substantial investment in produced water management and municipal infrastructure rehabilitation.

Which region is expected to grow the fastest in the Industrial Water Treatment Chemicals Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid industrial expansion in China and India, where coagulants and flocculants for wastewater treatment and boiler chemicals for power generation are critical for supporting economic growth without catastrophic ecological degradation.

What are the major trends in the Global Industrial Water Treatment Chemicals Market?

▾ Major trends include the shift from phosphonate to polymer-based scale inhibitors, the rise of solid-form chemistries for safety and sustainability, the integration of AI-driven chemical dosing automation, and the demand for high-purity chemistries in semiconductor & electronics manufacturing.

Who are the key players in the Global Industrial Water Treatment Chemicals Market?

▾ Key players include water management giants like Ecolab (Nalco Water), Solenis, and Kurita, as well as global chemical manufacturers like BASF, Dow, and Kemira, alongside specialized formulators like SNF Group and ChemTreat.

How is the Global Industrial Water Treatment Chemicals Market segmented?

▾ The market is segmented by Product Type, Source, Application, Distribution Channel, and End User Industry.