Market Overview

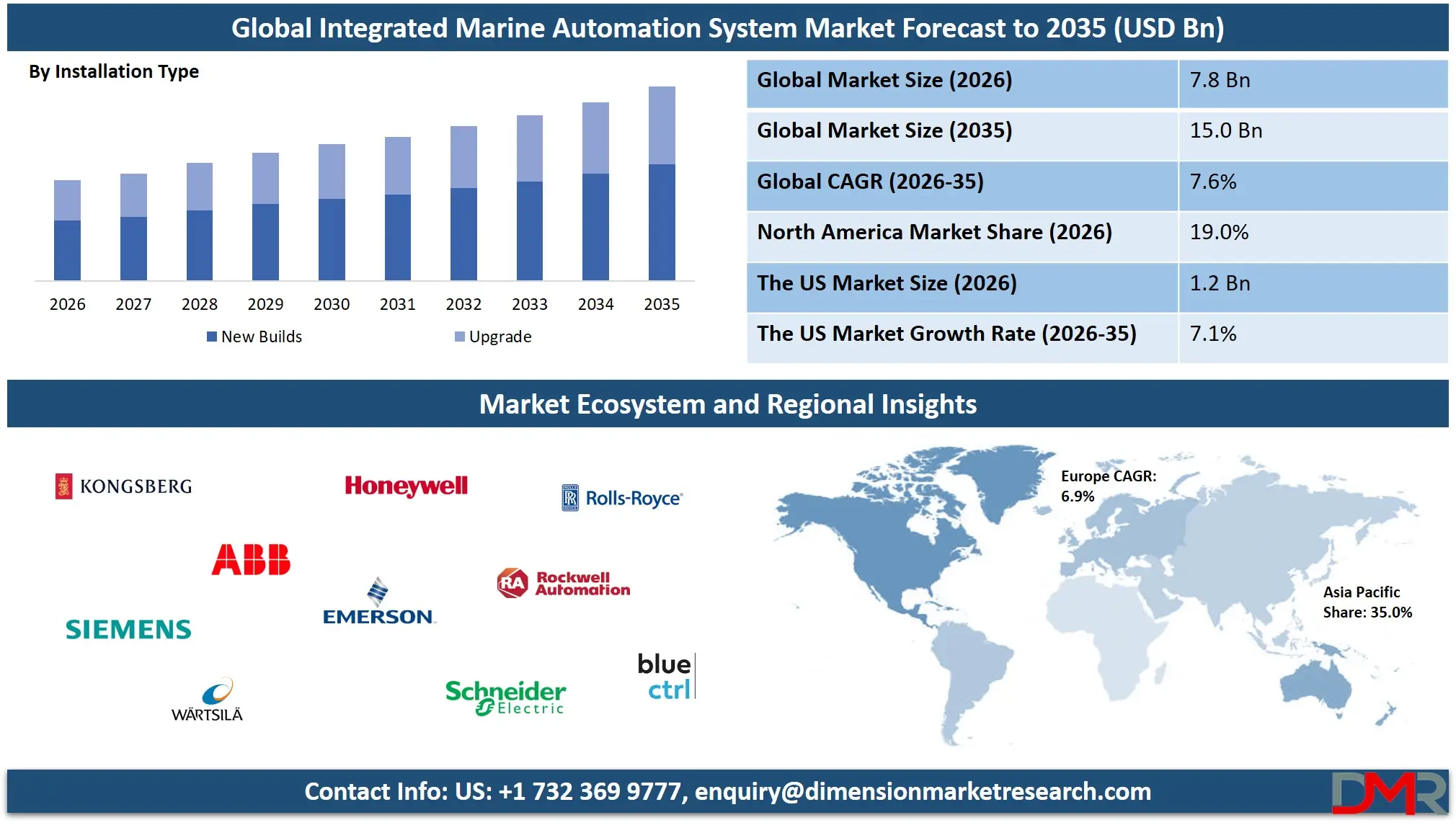

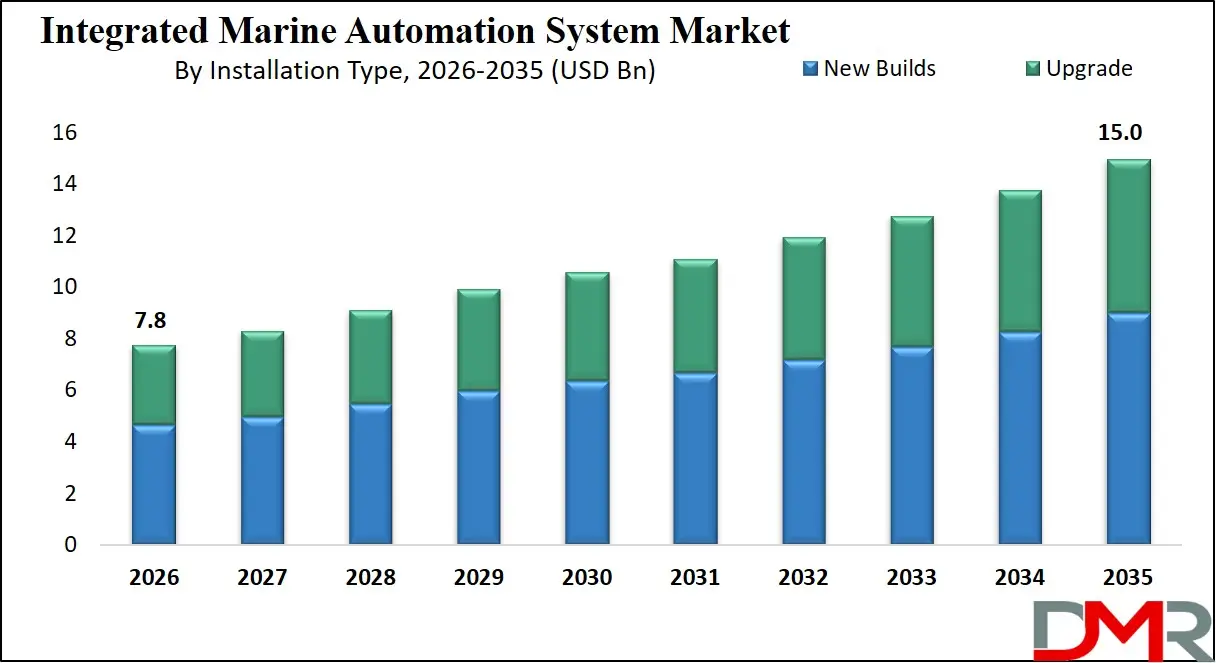

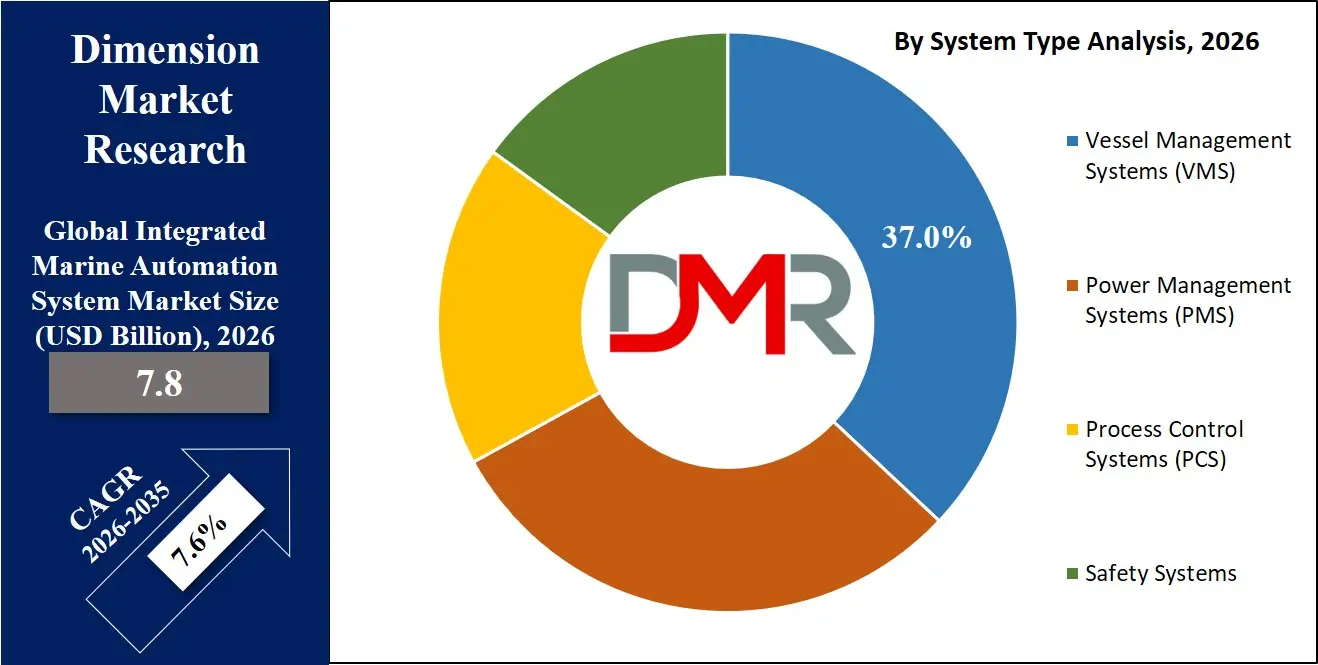

The global Integrated Marine Automation System market is expected to reach USD 7.8 billion in 2026 and expand at a CAGR of 7.6%, driven by increasing adoption of vessel management systems, power optimization solutions, and advanced onboard automation technologies, reaching a projected value of USD 15.0 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

An Integrated Marine Automation System is a comprehensive solution designed to monitor, control, and optimize various onboard operations of a vessel through the seamless integration of hardware, software, and communication networks. It encompasses power management systems, navigation and vessel control modules, safety and alarm systems, and auxiliary equipment, allowing ship operators to enhance efficiency, reduce human error, and ensure regulatory compliance. By connecting multiple subsystems into a single interface, it enables real-time monitoring, predictive maintenance, and energy optimization, supporting both commercial and naval applications. The system's adoption has increased with the growing demand for smart shipping solutions, hybrid propulsion, and digitalized maritime operations that prioritize operational reliability and fuel efficiency.

The global Integrated Marine Automation System market refers to the worldwide industry that develops, manufactures, and deploys these advanced automation solutions for ships, offshore platforms, and naval vessels. It includes a diverse range of components such as sensors, controllers, software platforms, communication networks, and monitoring services that collectively ensure safe and efficient vessel operation. Rising adoption of intelligent ship management, compliance with international maritime regulations, and the shift toward energy-efficient propulsion systems have been key drivers of market growth. Manufacturers and service providers are focusing on delivering fully integrated solutions that combine predictive analytics, remote monitoring, and automation to optimize vessel performance and reduce operational costs.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market also reflects regional variations influenced by shipbuilding capacity, modernization initiatives, and the expansion of global trade networks. Asia-Pacific dominates due to large-scale commercial shipbuilding in countries like China, South Korea, and Japan, while Europe remains a strong market for retrofitting and advanced digital solutions in existing fleets. North America, the Middle East, and emerging regions are witnessing gradual adoption driven by defense modernization, offshore exploration, and port infrastructure enhancements. The growing focus on smart shipping, autonomous navigation, and environmental compliance is further fueling investment in integrated marine automation solutions, making the market highly competitive and innovation-driven.

The US Integrated Marine Automation System Market

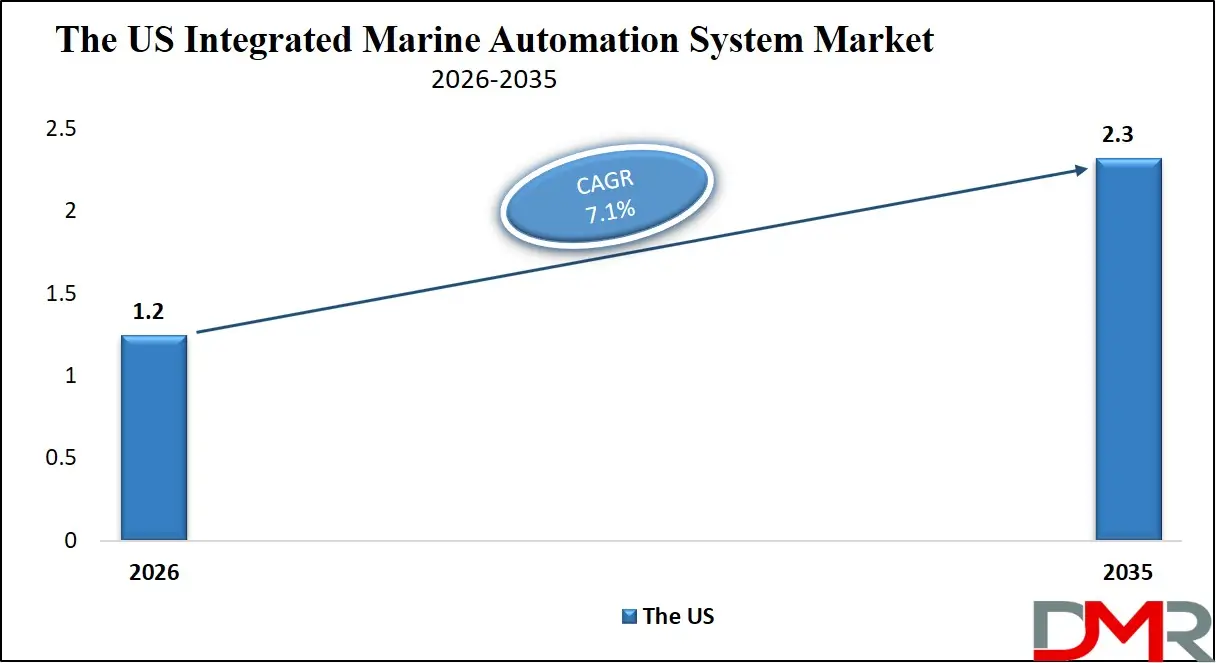

The US Integrated Marine Automation System Market size is expected to reach at USD 1.2 billion in 2026. It is further expected to witness subsequent growth in the upcoming period, holding USD 2.3 billion in 2035 at a CAGR of 7.1%.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Integrated Marine Automation System market is experiencing significant growth driven by modernization of commercial fleets, naval vessels, and offshore support ships. Increasing adoption of energy-efficient propulsion systems, predictive maintenance solutions, and real-time monitoring technologies is fueling demand across US shipping and defense sectors. Integration of vessel management systems, power control modules, and safety solutions enables operators to improve operational efficiency, reduce human error, and comply with strict maritime regulations. Growing investments in smart shipping and digitalization initiatives continue to expand the US market steadily.

Advanced automation solutions in the US focus on optimizing vessel performance, reducing fuel consumption, and improving crew safety. Strong naval modernization programs, offshore exploration projects, and retrofitting of existing vessels are key growth drivers. Companies in the US are offering integrated hardware and software platforms, enabling predictive analytics, remote monitoring, and intelligent alarm systems. Regulatory compliance requirements and the push for sustainable hybrid marine propulsion further support adoption, making the US market competitive and innovation-driven across commercial and defense applications.

The Europe Integrated Marine Automation System Market

The Europe Integrated Marine Automation System market is projected to reach approximately USD 2.3 billion in 2026, reflecting steady growth driven by the modernization and retrofitting of existing commercial and naval fleets. The region's demand is fueled by the need to comply with stringent maritime regulations, improve operational efficiency, and integrate advanced vessel management and power control systems. European operators are increasingly adopting energy-efficient propulsion and automated monitoring solutions to reduce fuel consumption, enhance safety, and optimize fleet performance across cargo, passenger, and defense vessels.

The market's growth in Europe, with a projected CAGR of 6.8%, is supported by strong technological innovation and increasing investments in smart shipping solutions. Companies in the region are focusing on integrating software platforms, predictive maintenance systems, and real-time analytics into marine automation solutions. Additionally, the retrofit segment plays a crucial role as operators upgrade legacy vessels to meet evolving environmental and operational standards. Government initiatives promoting sustainable maritime practices and digitalization in ports and shipping operations are further strengthening the adoption of integrated marine automation systems in Europe.

The Japan Integrated Marine Automation System Market

The Japan Integrated Marine Automation System market for is projected to reach approximately USD 624 million in 2026, driven by the country's strong shipbuilding industry and growing emphasis on advanced vessel automation. The demand is fueled by the adoption of intelligent navigation, power management, and safety systems across commercial shipping, offshore support, and naval vessels. Japanese operators are increasingly implementing energy-efficient propulsion technologies and integrated monitoring solutions to optimize fuel usage, enhance operational efficiency, and comply with stringent maritime regulations.

The market in Japan is expected to grow at a robust CAGR of 8.2%, reflecting rapid technological adoption and innovation in marine automation. Investments in predictive maintenance, digital twin technologies, and real-time vessel analytics are accelerating the deployment of integrated systems. Additionally, government initiatives supporting smart shipping, digitalization of maritime operations, and environmental sustainability are encouraging fleet modernization. These factors collectively position Japan as one of the fastest-growing markets in the global Integrated Marine Automation System landscape.

Global Integrated Marine Automation System Market: Key Takeaways

- Global Market Size & Growth: The market is projected to reach at USD 7.8 billion in 2026, growing at a CAGR of 7.6% to reach USD 15.0 billion by 2035, nearly doubling in value.

- Component Dominance: Hardware holds 62.0% of the market in 2026, emphasizing the importance of sensors, controllers, and monitoring modules over software and services.

- System Type Leadership: Vessel Management Systems (VMS) capture 37.0% of the share, central for navigation, propulsion, and safety operations across fleets.

- End-User Focus: Commercial shipping leads with 74.0% market share, reflecting high adoption for fleet efficiency and regulatory compliance.

- Regional Insights: Asia-Pacific holds 35.0% market share, while Japan grows fastest at 8.2% CAGR, followed by Europe at 6.8%, driven by shipbuilding and automation adoption.

Global Integrated Marine Automation System Market: Use Cases

- Commercial Shipping Fleet Optimization: Integrated automation systems streamline navigation, propulsion, and energy management for commercial vessels. Real-time monitoring and predictive maintenance reduce fuel consumption, lower operational costs, and improve fleet efficiency.

- Naval and Defense Vessel Automation: Automation enhances safety, mission efficiency, and operational readiness on naval vessels. Remote monitoring and control of propulsion, weapons, and safety systems reduce crew workload and ensure compliance with defense standards.

- Offshore Oil and Gas Support: Automation systems manage power, engine performance, and safety alarms on offshore vessels and rigs. Continuous monitoring ensures reliable operations and minimizes downtime in challenging marine environments.

- Port and Harbor Operations: Integrated systems optimize vessel docking, traffic management, and cargo handling in ports. Real-time data and predictive analytics improve turnaround times, operational efficiency, and safety for port authorities.

Global Integrated Marine Automation System Market: Stats & Facts

- UNCTAD – Review of Maritime Transport / Maritime Trade (UN Government Source)

- Global maritime trade reached approximately 12,292 million tons in 2023, rebounding with a 2.4% growth over the previous year.

- Total estimated ton‑miles (distance‑adjusted maritime shipments) reached 62,037 billion in 2023, a 4.2% increase over 2022.

- Average shipping distance per ton continued to expand, rising from 4,675 miles in 2000 to 5,186 miles in 2024.

- Around 80% of the volume of international trade in goods is carried by sea.

- UK Department for Transport – Shipping Fleet Statistics 2025

- Gross tonnage on the UK Ship Register fell to 8.7 million gross tonnes at the end of 2025, down 12% from 2024.

- The UK‑registered trading fleet accounted for 0.4% of the world trading fleet by deadweight tonnage in 2025.

- The UK fleet ranked 31st largest globally by deadweight and 28th by gross tonnage in 2025.

- The number of UK‑registered vessels decreased to 1,034 in 2025, compared to 1,054 in 2024.

- UK Department for Transport – Seafarers in the UK Shipping Industry 2025

- An estimated 24,550 seafarers were active at sea in the UK in 2025, a 2% increase over 2024.

- There were 11,120 certificated officers active at sea in 2025.

- The UK had 10,510 ratings working at sea in 2025.

- 1,380 officer cadets were in training and active at sea in 2025.

- EU Blue Economy Report – Maritime Transport (EU Government Source)

- Around 13 billion tonnes of traded goods were transported by sea globally in 2023, a 2.4% increase over 2022.

- EU ports handled 3.4 billion tonnes of goods in 2023, down 3.9% from the previous year.

- 1.6 billion tonnes of goods were transported via short sea shipping in the EU in 2023, a 5.4% decrease from 2022.

- 386 million passengers embarked/disembarked at EU ports in 2023, a 6.8% increase from 2022.

- Government and Intergovernmental Maritime Workforce & Technology

- The UK recorded a 6% increase in deck ratings working at sea in 2025 vs 2024.

- Ratings, uncertificated officers and certificated officers represented various segments of the UK maritime workforce in 2025.

- National and Sectoral Government Context

- India's maritime sector carries 95% of the nation's trade by volume by sea.

- India plans up to ₹80 lakh crore investment in maritime infrastructure under Vision 2047.

Impact of US-Iran Conflict on the Global Integrated Marine Automation System Market

- Disruption of Strategic Shipping Routes: The conflict has affected vital maritime corridors, especially the Strait of Hormuz, forcing vessels to take longer alternative routes. This has increased transit times and operational costs for global shipping.

- Rise in Freight Costs and Insurance Premiums: Shipowners face higher war-risk insurance premiums and surging freight charges, impacting budgets for vessel operations, upgrades, and adoption of automation systems.

- Delays in Vessel Deployments and Retrofits: Operational disruptions and increased costs can delay both new vessel deployments and retrofitting of existing fleets with integrated marine automation solutions.

- Pressure on Operating Budgets: Elevated fuel prices and operational expenditures reduce available capital for investment in automation technologies, predictive maintenance tools, and energy-efficient systems.

- Indirect Impact on Market Growth: While the war does not directly target automation systems, the resulting supply chain volatility, cost pressures, and strategic rerouting can slow overall market expansion and affect adoption cycles globally.

Global Integrated Marine Automation System Market: Market Dynamic

Driving Factors in the Global Integrated Marine Automation System Market

Adoption of Smart Shipping Solutions

The growing demand for intelligent vessel management, predictive maintenance, and real-time monitoring is driving market growth. Operators are increasingly integrating power management systems, navigation control, and safety modules to enhance operational efficiency, reduce fuel consumption, and ensure compliance with maritime regulations. The push for digitalized marine operations and automation in both commercial and defense sectors is accelerating adoption globally.

Rising Focus on Energy Efficiency and Sustainability

Stringent environmental regulations and rising fuel costs are encouraging shipping companies to adopt energy-efficient automation solutions. Integrated systems that optimize propulsion, engine performance, and power distribution help reduce carbon emissions and operational costs, supporting sustainable maritime operations and compliance with international standards such as IMO regulations.

Restraints in the Global Integrated Marine Automation System Market

High Capital Investment and Implementation Costs

The cost of installing and integrating advanced automation systems, including hardware, software, and monitoring solutions, can be prohibitive for small and mid-sized shipping companies. The requirement for specialized installation and skilled personnel further limits adoption in emerging markets.

Complex Integration and Maintenance Challenges

Integrating multiple onboard subsystems into a seamless automation platform can be technically challenging. Ensuring compatibility among legacy equipment, real-time monitoring systems, and safety modules requires significant technical expertise, which can delay deployment and increase operational risks.

Opportunities in the Global Integrated Marine Automation System Market

Expansion in Retrofit and Modernization Projects

As existing vessels seek upgrades to meet regulatory compliance and enhance efficiency, the retrofit market offers significant opportunities. Adding integrated automation solutions to older fleets enables predictive maintenance, energy optimization, and improved safety without requiring new ship construction.

Growth in Autonomous and Semi-Autonomous Vessels

The development of autonomous and semi-autonomous ships presents a major opportunity for integrated automation systems. Intelligent control, real-time monitoring, and remote operation solutions are essential for these vessels, creating demand for advanced software, sensors, and communication networks in commercial and naval applications.

Trends in the Global Integrated Marine Automation System Market

Integration of IoT and Digital Twin Technologies

Marine automation is increasingly adopting IoT-enabled sensors and digital twin models to provide real-time analytics, predictive maintenance, and performance optimization. These technologies enable operators to monitor multiple subsystems simultaneously and make data-driven operational decisions.

Shift Toward Hybrid and Electric Propulsion Systems

Automation systems are being designed to manage hybrid and electric propulsion, optimizing energy usage and reducing emissions. The integration of power management, battery monitoring, and engine control in hybrid vessels is shaping the future of sustainable shipping and supporting green maritime initiatives.

Global Integrated Marine Automation System Market: Research Scope and Analysis

By Component Analysis

In the global Integrated Marine Automation System market, hardware is expected to dominate the component segment, accounting for approximately 62.0% of the total market share in 2026. This dominance is driven by the essential role of physical devices such as sensors, controllers, actuators, and monitoring modules, which form the backbone of vessel automation. Hardware components are critical for enabling real-time monitoring, engine control, power management, and safety systems on both commercial and naval vessels. The high cost of these devices, combined with their indispensable function in ensuring operational efficiency and compliance with maritime regulations, contributes to their significant share in the market.

Software, on the other hand, represents a growing segment within the component analysis, offering solutions for data analytics, remote monitoring, predictive maintenance, and intelligent vessel management. Software platforms integrate multiple onboard systems, allowing operators to analyze performance, optimize energy consumption, and implement automated decision-making processes. The increasing adoption of digitalization in shipping, the push for smart shipping solutions, and the need for predictive insights to reduce downtime are driving the demand for software solutions. While the market share of software is smaller than hardware, it is expanding rapidly due to the critical role it plays in enhancing the efficiency and intelligence of modern marine automation systems.

By System Type Analysis

In the global Integrated Marine Automation System market, Vessel Management Systems (VMS) are expected to lead the system type segment, capturing approximately 37.0% of the total market share in 2026. VMS play a central role in monitoring and controlling critical vessel operations, including navigation, propulsion, and onboard safety systems. By integrating multiple subsystems into a single interface, VMS enable real-time decision-making, predictive maintenance, and efficient resource management, which helps shipping operators reduce fuel consumption, minimize downtime, and ensure compliance with maritime regulations. The high adoption of VMS in commercial shipping, naval fleets, and offshore vessels drives their dominant position in this segment.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Power Management Systems (PMS) also form a significant part of the system type segment, offering solutions to monitor, control, and optimize energy generation and distribution on vessels. PMS ensures efficient operation of engines, generators, and auxiliary equipment, balancing power loads and reducing fuel consumption. These systems are essential for both conventional and hybrid propulsion vessels, allowing operators to improve energy efficiency, extend equipment life, and maintain operational reliability. The growing emphasis on sustainable shipping and compliance with environmental regulations is further increasing the adoption of PMS across commercial and defense fleets worldwide.

By Installation Type Analysis

In the global Integrated Marine Automation System market, new builds are expected to dominate the installation type segment, capturing approximately 60.0% of the total market share in 2026. This trend is driven by the integration of advanced automation systems during the construction of new vessels, allowing shipbuilders to design ships with fully optimized navigation, power management, and safety systems from the outset. Installing automation solutions during new builds ensures seamless integration of hardware and software, enhances operational efficiency, reduces human error, and supports compliance with international maritime regulations. The demand for technologically advanced vessels in commercial shipping, defense, and offshore operations contributes to the high share of new builds in this segment.

Upgrade or retrofit installations also hold a significant share of the market, as many operators seek to modernize existing vessels with integrated automation systems. Retrofitting allows older ships to incorporate advanced power management, vessel monitoring, and predictive maintenance solutions without requiring complete reconstruction. This approach improves energy efficiency, operational reliability, and safety standards while extending the service life of the vessel. The growing need for regulatory compliance, reduction of operational costs, and adoption of smart shipping technologies is driving the retrofit market, making it an important segment alongside new build installations.

By Automation Level Analysis

In the global Integrated Marine Automation System market, partial automation is expected to dominate the automation level segment, capturing approximately 70.0% of the total market share in 2026. Partial automation systems combine automated controls with human oversight, allowing operators to manage navigation, propulsion, power distribution, and safety systems while retaining manual intervention when necessary. This approach ensures operational reliability, reduces human error, and enhances efficiency on commercial and naval vessels without requiring full autonomous capabilities. The widespread adoption of partial automation is driven by the balance it provides between technological advancement and crew control, making it suitable for most existing fleets.

Remotely-operated systems also represent a growing segment in the automation level category, enabling operators to control vessel functions from onshore or remote locations. These systems integrate sensors, communication networks, and intelligent software to monitor propulsion, engine performance, and safety modules in real time. Remotely-operated automation enhances operational flexibility, allows rapid response to emergencies, and supports specialized operations such as offshore exploration or defense missions. While the market share of remotely-operated systems is smaller than partial automation, their adoption is increasing with the development of autonomous and semi-autonomous vessel technologies.

By End-User Analysis

In the global Integrated Marine Automation System market, commercial shipping is expected to dominate the end-user segment, capturing approximately 74.0% of the total market share in 2026. The high adoption in this sector is driven by the need for efficient vessel management, fuel optimization, and real-time monitoring of propulsion, navigation, and safety systems across cargo, container, and tanker fleets. Integrated automation systems help shipping companies reduce operational costs, enhance fleet performance, and ensure compliance with international maritime regulations. The growing focus on smart shipping, digitalization of fleet operations, and energy-efficient solutions further supports the dominance of commercial shipping in this market.

The defense sector also represents a key end-user segment, deploying integrated marine automation systems on naval and patrol vessels to enhance mission readiness, safety, and operational efficiency. Automation solutions in defense applications manage propulsion, power distribution, onboard safety, and weapons systems while reducing crew workload. Real-time monitoring, predictive maintenance, and remote control capabilities improve response times and operational reliability for defense fleets. Although the market share of defense is smaller than commercial shipping, the adoption of advanced automation technologies is increasing due to naval modernization programs and the need for secure, efficient, and resilient maritime operations.

The Global Integrated Marine Automation System Market Report is segmented on the basis of the following:

By Component

- Hardware

- Software

- Services

By System Type

- Vessel Management Systems (VMS)

- Power Management Systems (PMS)

- Process Control Systems (PCS)

- Safety Systems

By Installation Type

By Automation Level

- Partial Automation

- Remotely-Operated

- Fully Autonomous

By End-User

- Commercial Shipping

- Defense

- Others

Impact of Artificial Intelligence in the Global Integrated Marine Automation System Market

The impact of artificial intelligence in the global Integrated Marine Automation System market is increasingly significant as shipping operators and naval fleets adopt intelligent solutions to enhance vessel efficiency and safety. AI technologies enable real-time data analysis from multiple onboard systems, allowing predictive maintenance, fault detection, and energy optimization. Machine learning algorithms can monitor engine performance, propulsion systems, and power distribution to detect anomalies early, reducing downtime and operational costs.

AI also supports advanced navigation and decision-making, integrating vessel management, environmental monitoring, and safety systems to optimize routes, reduce fuel consumption, and comply with maritime regulations. In defense and offshore applications, AI enhances autonomous and semi-autonomous operations, enabling remote control, threat detection, and operational reliability. The integration of AI with IoT-enabled sensors and digital twin technologies is driving smarter, more efficient marine automation, positioning the market for rapid growth as operators seek advanced predictive and automated solutions.

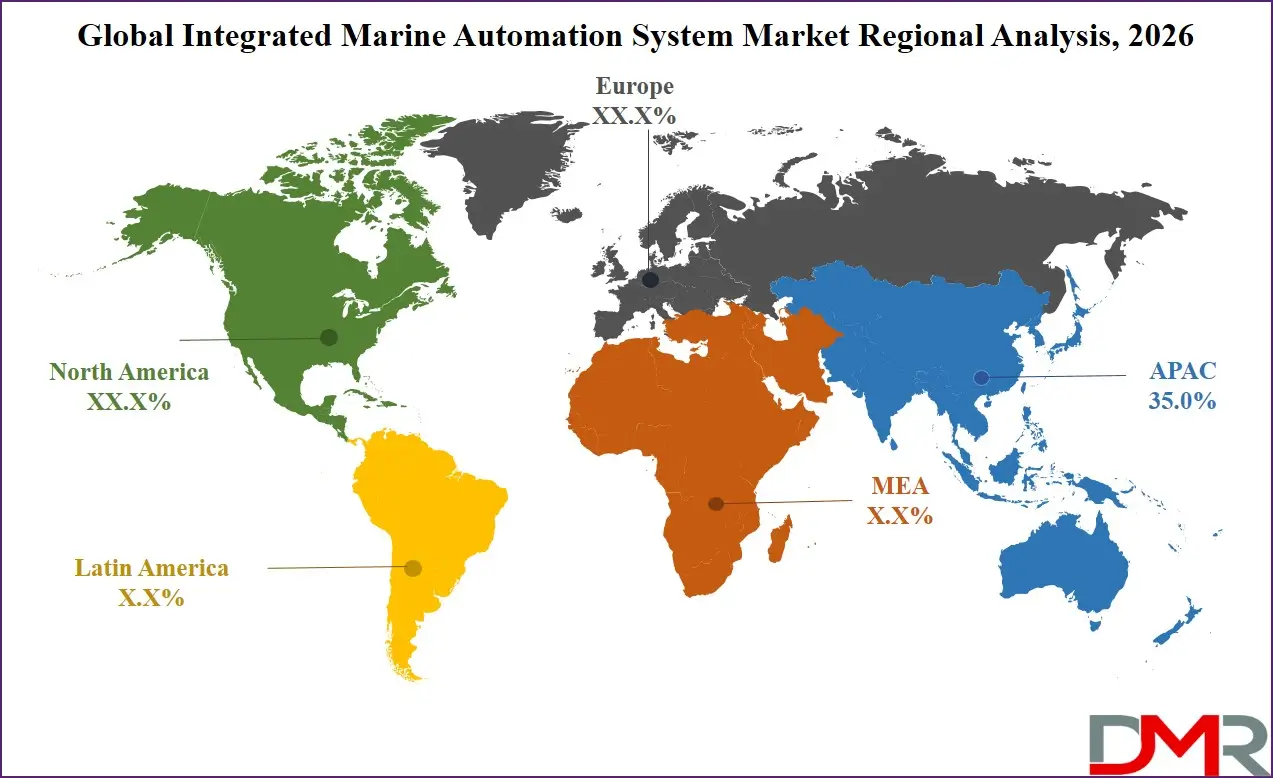

Global Integrated Marine Automation System Market: Regional Analysis

Region with the Largest Revenue Share

In 2026, the Asia-Pacific (APAC) region is expected to account for approximately 35.0% of the Integrated Marine Automation System market, driven by rapid expansion in maritime trade, increasing shipbuilding activities, and strong adoption of advanced navigation and control technologies. Countries such as China, Japan, South Korea, and Singapore are leading contributors due to their well-established shipbuilding industries and growing investments in smart port infrastructure. Additionally, rising demand for fuel-efficient and autonomous vessel operations is further accelerating the deployment of integrated automation systems across commercial and defense marine fleets in the region.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Region with the Highest CAGR

APAC is expected to record the fastest growth due to its rapidly expanding shipbuilding industry and strong maritime trade activity, particularly in countries such as China, South Korea, Japan, and India. The region is witnessing increasing adoption of smart ship technologies, automation-driven navigation systems, and fuel-efficient vessel operations, driven by rising pressure to improve operational efficiency and reduce emissions. Additionally, major investments in port modernization and naval fleet upgrades are accelerating demand for integrated marine automation solutions. Government support for digitalization of maritime infrastructure further strengthens APAC's position as the fastest-growing regional market.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Integrated Marine Automation System Market: Competitive Landscape

The competitive landscape of the global Integrated Marine Automation System market is characterized by intense technological innovation, strategic partnerships, and continuous product enhancements as key players strive to gain market share. Providers are focusing on expanding their solution portfolios through advanced software platforms, real‑time analytics, and integrated hardware systems to meet the rising demand for smart shipping, predictive maintenance, and energy‑efficient operations. Market participants are also investing in research and development to incorporate digital twin, Internet of Things, and artificial intelligence technologies into automation systems, while forming strategic collaborations and service networks to strengthen global reach and support customers across commercial, naval, and offshore segments.

Some of the prominent players in the Global Integrated Marine Automation System Market are:

- Kongsberg Gruppen ASA

- ABB Ltd.

- Siemens AG

- Wärtsilä Corporation

- Honeywell International Inc.

- Emerson Electric Co.

- Rolls‑Royce Holdings plc

- Rockwell Automation Inc.

- Schneider Electric SE

- Blue Ctrl AS

- Høglund AS

- Jason Marine Group

- L3Harris Technologies, Inc.

- Marlink Group

- API Marine ApS

- Fugro

- Hyundai Electric & Energy System Co., Ltd.

- Marine Technologies, LLC

- Northrop Grumman Corporation

- Sea Machines Robotics, Inc.

- Other Key Players

Recent Developments in the Global Integrated Marine Automation System Market

- March 2026: Kraken Robotics agreed to acquire the Covelya Group, a strategic deal to expand its maritime technology capabilities and broaden automation, sensor, and underwater mission solutions across global commercial and defense markets.

- September 2025: Sea Machines Robotics launched six new marine autonomy products, expanding its flagship system line with enhanced hardware variants, high‑level software APIs, a cloud‑based fleet data platform, and a new high‑performance unmanned surface vessel to support advanced onboard automation and defense applications.

- September 2025: Sea Machines unveiled SMLink APIs for its marine autonomy platform, enabling real‑time telemetry streaming and third‑party command integration to improve interoperability with external control and automation systems on vessels.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 7.8 Bn |

| Forecast Value (2035) |

USD 15.0 Bn |

| CAGR (2026–2035) |

7.6% |

| The US Market Size (2026) |

USD 1.2 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Component (Hardware, Software, Services), By System Type (Vessel Management Systems, Power Management Systems, Process Control Systems, Safety Systems), By Installation Type (New Builds, Upgrade), By Automation Level (Partial Automation, Remotely-Operated, Fully Autonomous), and By End-User (Commercial Shipping, Defense, Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Kongsberg Gruppen ASA, ABB Ltd., Siemens AG, Wärtsilä Corporation, Honeywell International Inc., Emerson Electric Co., Rolls-Royce Holdings plc, Rockwell Automation Inc., Schneider Electric SE, Blue Ctrl AS, Høglund AS, Jason Marine Group, L3Harris Technologies, Inc., Marlink Group, API Marine ApS, Fugro, Hyundai Electric & Energy System Co., Ltd., Marine Technologies, LLC, Northrop Grumman Corporation, Sea Machines Robotics, Inc., and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Integrated Marine Automation System Market?

▾ The Global Integrated Marine Automation System Market size is estimated to have a value of USD 7.8 billion in 2026 and is expected to reach USD 15.0 billion by the end of 2035.

What is the growth rate in the Global Integrated Marine Automation System Market in 2026?

▾ The market is growing at a CAGR of 7.6% over the forecasted period of 2026.

What is the size of the US Integrated Marine Automation System Market?

▾ The US Integrated Marine Automation System market is projected to be valued at USD 1.2 billion in 2026. It is expected to witness subsequent growth in the upcoming period as it holds USD 2.3 billion in 2035 at a CAGR of 7.1%.

Which region accounted for the largest Global Integrated Marine Automation System Market?

▾ Asia Pacific is expected to have the largest market share in the Global Integrated Marine Automation System Market with a share of about 35.0% in 2026.

Who are the key players in the Global Integrated Marine Automation System Market?

▾ Some of the major key players in the Global Integrated Marine Automation System Market are Kongsberg Gruppen ASA, ABB Ltd., Siemens AG, Wärtsilä Corporation, Honeywell International Inc., Emerson Electric Co., Rolls-Royce Holdings plc, Rockwell Automation Inc., Schneider Electric SE, Blue Ctrl AS, Høglund AS, Jason Marine Group, and many others.