What is the Japan Agritech Market Size?

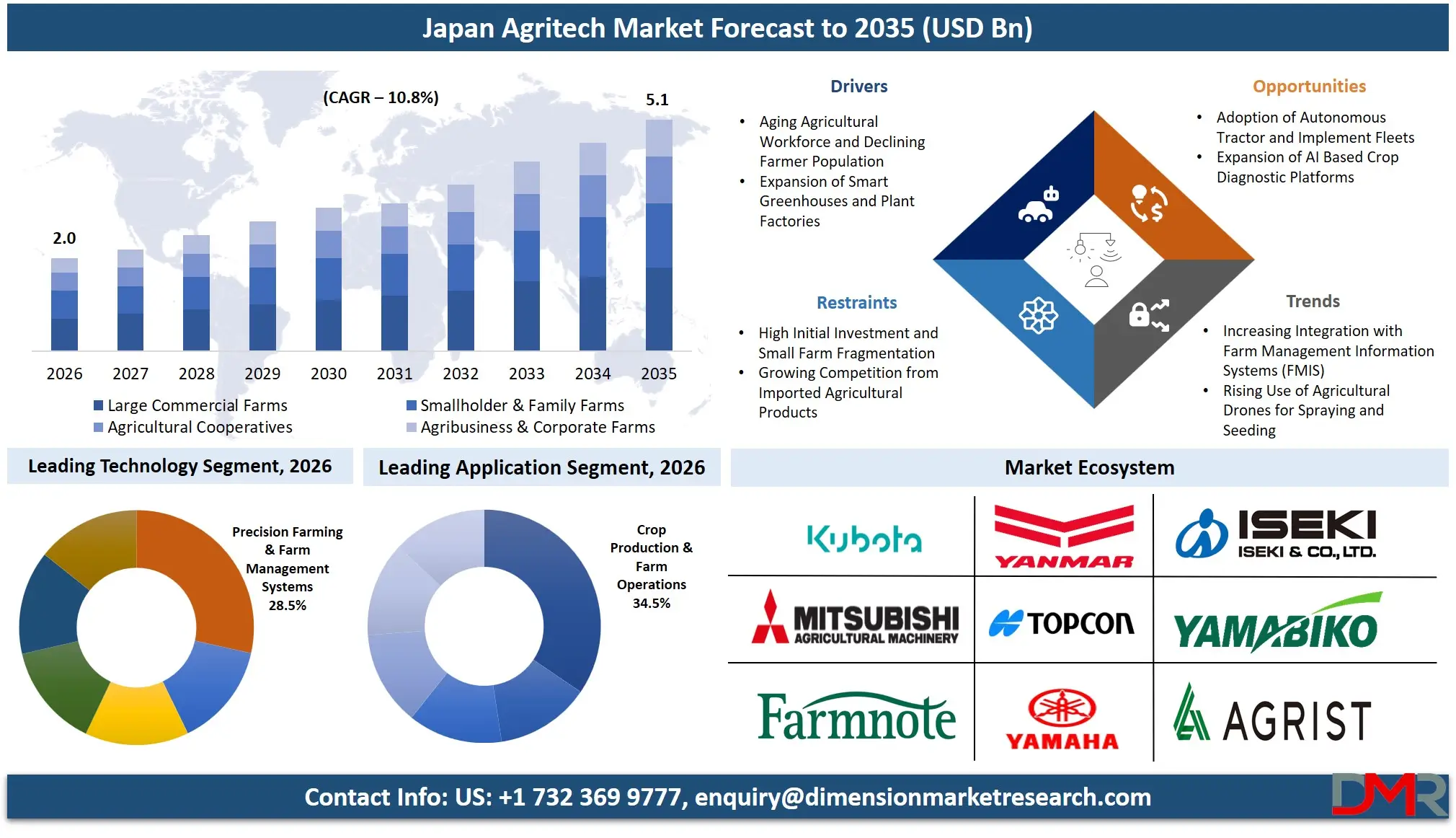

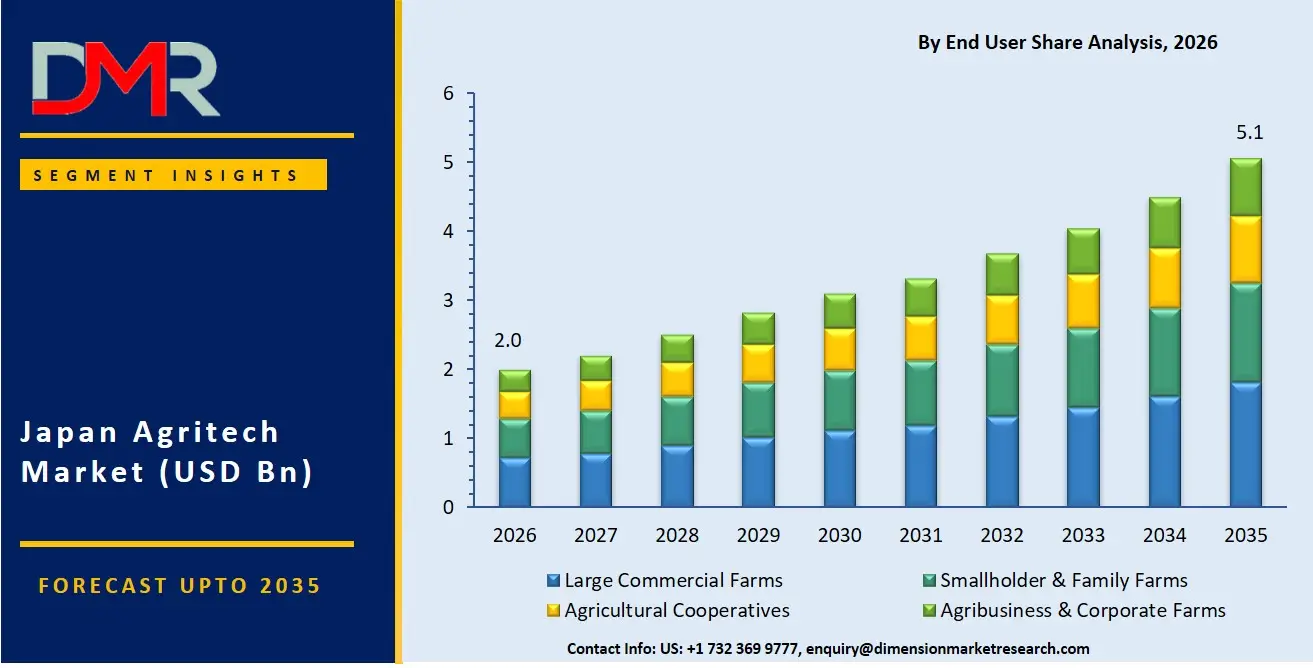

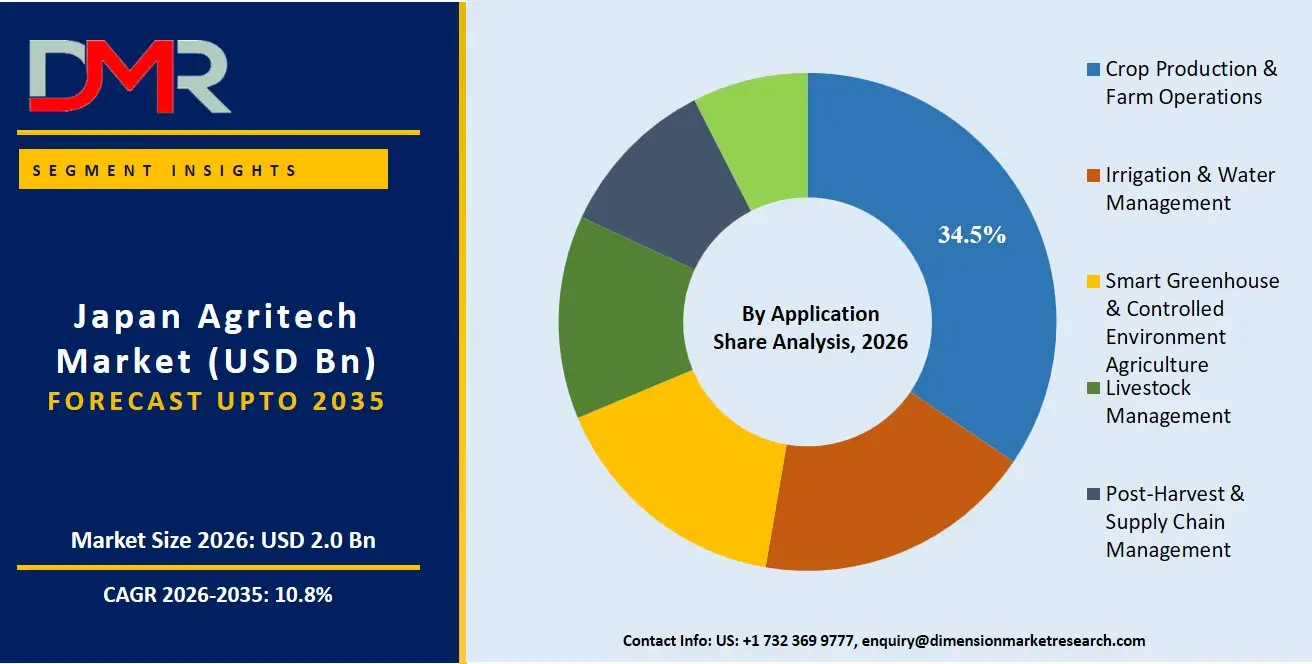

The Japan Agritech Market is expected to reach a value of USD 2.0 billion in 2026, and it is further anticipated to reach USD 5.1 billion by 2035, growing at a CAGR of 10.8% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The agritech industry has been witnessing steady growth owing to Japan's elderly farm owners, reduced farmland, and increasing demand for labor-efficient, data-driven farming systems. These solutions include various digital services and platforms that allow farm operators to utilize intelligent solutions for farming, greenhouse operations, and optimizing logistics. The increase in the need for professional services can be attributed to the need for smart sensor infrastructure, continuity assurance despite labor shortage and adverse climatic conditions, and providing high-efficiency automation technologies to the consumers. Commercial large-scale farms have become the biggest buyer base for agritech technologies, as precision farming platforms are the preferred choice because of their high yield potential, while agriculture robots and analytical AI services have seen rapid adoption.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Key Takeaways

- Market Size & Forecast: The Japan Agritech market is forecasted to be valued at USD 2.0 billion in 2026, growing incrementally to USD 5.1 billion by 2035, due to the government-set productivity targets for rice, vegetables, and fruit, together with the imperative requirement to compensate for retiring farmers through technology-enabled autonomy.

- Growth Rate & Outlook: It is anticipated that the growth rate of the Japan market will be 10.8% CAGR owing to the severe scarcity of skilled agricultural labor (68-years-old average age of farmers) along with the difficulties encountered in managing crop quality and yield in the volatile climate conditions.

- Primary Growth Drivers: The key growth drivers include the change from conventional, skill-oriented, and manual farming to intelligent and data-driven farming system, development and use of efficient farm management information systems (FMIS), and use of robotics for planting, weeding, harvesting, and crop-spraying.

- Key Market Trends: The major trends include the implementation of fully autonomous tractors in agriculture, variable-rate fertilization and monitoring using satellite and drone imagery, and farm-to-fork traceability in the face of strict food safety regulations and quality controls.

- By Technology Analysis: The Precision Farming & Farm Management Systems segment is projected to dominate the Japan Agritech Market in 2026 due to high demand for scalable FMIS platforms by large commercial farms and cooperatives.

- By Application Analysis: The Crop Production & Farm Operations segment is anticipated to dominate in the Japan Agritech Market as farm operators adopt systems for real time planting, fertilizing, and harvesting management.

- By End User Analysis: Large Commercial Farms are projected to continue dominating the Japan Agritech Market in 2026, owing to their ability to invest in high-cost robotics and precision platforms.

What is Agritech?

Agritech refers to the integrated use of digital platforms, sensing devices, robotics, and data analytics to optimize agricultural production, reduce physical labor, and enhance food quality and safety. Unlike traditional farming heavily dependent on manual experience and seasonal intuition, agritech involves "the how and where" of high-precision, real‑time crop management. It entails having a Farm Operating System to provide the means through which soil conditions, weather, crop health, and machinery status are monitored and controlled for optimal yield, and Advisory Services to help integrate supply chain logistics, manage labor costs, and comply with food safety regulations. As Japan's agricultural sector faces a severe decline in the farming workforce, it is critical to have solutions that ensure farms will remain productive and profitable while maintaining food security and environmental compliance.

Use Cases

- Large Scale Rice Farming Automation: Commercial rice cultivation carried out in Niigata and Hokkaido uses automated processes based on autonomous tractors and rice transplanters. The process ensures the preparation of paddies, planting, and harvesting. It has reduced labor demands by 60%, enabling the timely execution of agricultural operations despite limited labor.

- Smart Greenhouse Vegetable Production: IoT technology-based climate controls and AI-driven fertigation processes used for tomato and cucumber production in greenhouses located in Shizuoka and Kumamoto make sure that vegetables are available throughout the year. Moreover, it leads to reduced use of pesticides and earning more money as a result of high quality.

- Orchard Pest and Disease Detection: Drones with multicolor cameras used for monitoring fruits at the apple-growing orchards of Aomori and mandarin-producing orchards of Wakayama provide AI-driven detection services. Thus, one can detect diseases or pest infestations and undertake targeted spraying, leading to 30-40% savings on chemicals.

- Autonomous Weeding in Vegetable Fields: Robotic weeding machines with computer vision capabilities used at Ibaraki and Nagano vegetable farms are capable of recognizing crops from weeds. Thus, it allows avoiding manual weed removal and reduces herbicide utilization.

How AI is Transforming the Agritech Market?

AI is transforming the agritech industry in Japan with advanced yield prediction, automated visual inspection, and predictive crop management techniques. Image recognition technology that utilizes AI technology can be used to inspect pests' effects, nutritional deficiencies, and disease problems on crops by analyzing drone or static camera images, helping farmers to mitigate any losses to crops. AI-based crop growth modeling also makes use of weather forecast models, soil sensors, and yield data to make daily decisions on how to water, fertilize, and harvest. Quality and traceability in agriculture is also being made easier by using artificial intelligence in Japan. The AI is able to classify and inspect produce based on their size, color, and defects within a short period of time. In addition, traceability software is helping farmers stay compliant with Japan's strict labeling and export regulations.

Market Dynamics

Key Drivers in the Japan Agritech Market

Aging Agricultural Workforce and Declining Farmer Population

The average age of Japanese farmers is 68, while the total farm operator population has decreased considerably over the last twenty years. As a result of this problem, Japan needs to urgently adopt robotics, automation, and FMIS to take up these manual labor jobs. Farmers need autonomous tractors, rice planters, autonomous harvesters, and weeders to keep their yields going. In the absence of agricultural technology, there could be an unutilized mass of fertile lands. The Japanese government, through its Strategic Innovation Promotion Project, supports autonomous technologies' trial runs in fields in Hokkaido, Tohoku, and Kyushu.

Expansion of Smart Greenhouses and Plant Factories

Japan has been leading the world in controlled environment agriculture (CEA) technology, growing thousands of plant factories that produce leafy vegetables using LED lights and full-scale hydroponics. Smart greenhouse farming, involving the use of IoT sensors, artificial intelligence for temperature regulation, and robotics for harvests, has led to high demand for agritech platforms. Firms are adopting these technologies to facilitate year-round cultivation, decrease the use of pesticides by 90% and earn premium prices at wholesale urban centers. Consumer tastes for locally sourced pesticide-free fruits and vegetables are driving investments in technology.

Restraints in the Japan Agritech Market

High Initial Investment and Small Farm Fragmentation

Despite the potential benefits associated with such innovations as autonomous tractors (costing around $133,000-$267,000 per unit), smart greenhouses ($333.1-$667.0 per 100 m²), and artificial intelligence analytics, the cost of their purchase is currently too high for small and family farms which constitute a large portion of farmland area in Japan. Small-scale farmers typically operate on a shoestring budget and can neither purchase nor lease innovative farming equipment because of insufficient finances and risk sharing techniques. Besides, there are some government subsidies offered but their acquisition process may be quite difficult.

Growing Competition from Imported Agricultural Products

With an increasing amount of inexpensive agricultural imports coming into Japan from countries like China, Southeast Asia, and the Americas, the pressure is put on farmers within the country to stay profitable in their operations. In some cases, prices of agricultural imports are considerably cheaper than the cost of producing such products inside Japan, even after implementing agritech techniques. Because of such economic conditions, Japanese farmers cannot invest heavily in agritech without having some form of differentiation through quality, safety, or branding.

Growth Opportunities in the Japan Agritech Market

Adoption of Autonomous Tractor and Implement Fleets

There is immense potential in the agritech sector in Japan because of the increasing use of autonomous level 2 and level 3 tractors. The brands such as Kubota, Yanmar, and Iseki have developed autonomous tractors equipped with path planning, obstacle detection, and remote monitoring technology. The intelligent tractor systems enable an operator to control several units at once, which is necessary due to a labor shortage problem. Improved precision and efficiency, reduced fuel use, and lower cost of ownership when compared with manual operations constitute the benefits of using autonomous vehicles. With the enhanced GNSS signals and 5G coverage in rural locations, companies would invest heavily in fleet management systems.

Expansion of AI Based Crop Diagnostic Platforms

Integrating artificial intelligence technologies with drones and satellites has brought a lot of opportunities for agritech startups in Japan. A number of agricultural co-ops are already adopting cloud-based diagnostic systems for automatically detecting pests, nutrients deficiencies, and growth stages of crops. Artificial intelligence allows organizations to detect problematic areas in just a few hours and even predict the effects on the yield. More and more farmers are adopting machine learning technologies for predicting disease outbreaks, optimizing harvest timing, and grading produce.

Trends in the Japan Agritech Market

Increasing Integration with Farm Management Information Systems (FMIS)

More frequently, farmers within Japan are choosing to use cloud-based FMIS solutions that incorporate field mapping, task management, stock management, and vehicle telematics. Using such tools, one can digitize all aspects of farming from planting until harvesting without having to pay high costs for creating tailor-made software. The benefits related to modern FMIS solutions include real-time labor management, input cost management, and documentation for subsidy application purposes and food safety certifications. As a result of the growing popularity of digital transformation practices along with remote farm management, the FMIS trend continues to develop in Hokkaido, Kanto, and Kyushu.

Rising Use of Agricultural Drones for Spraying and Seeding

In recent times, agricultural drone applications have not only been limited to crop scouting but have also seen wide adoption for variable rate spraying of pesticides and fertilizers, as well as direct seeding into rice fields. Japanese firms are now using drones fitted with precise nozzles along with GPS guidance systems to replace the old-fashioned method of backpacks and reduce drift of the chemicals. Firms are concentrating more on integrating both aerial and ground processes, whereby they first perform drone mapping of the area to be sprayed, carry out the spraying process, and then confirm results through post-spraying images.

Research Scope and Analysis

The Japan Agritech Market is segmented by technology, application, and end user. The market supports smallholder production, large commercial farming, agricultural cooperatives, and corporate agribusiness through cloud‑based and on‑premise farm management, automation, and analytics solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Technology Analysis

Precision Farming & Farm Management Systems are expected to lead the Japan Agritech Market in 2026 with a projected market share of 28.5% as a result of agricultural cooperatives' and large farms' growing preference for integrated FMIS platforms. Japanese operators have developed a preference for variable-rate application maps, growth stage monitoring, and work record digitization for performing functions such as input optimization, yield forecasting, and compliance reporting. Agricultural Robotics & Automation is the fastest-growing major segment due to the critical labor shortage across grain, vegetable, and fruit production. IoT & Smart Farming Devices hold a stable share as an enabling layer for sensing and connectivity, while AI-based analytics and drone solutions are gradually gaining traction across large commercial farms. Agricultural Biotechnology & Inputs remains meaningful but not dominant in a technology-focused agritech market.

By Application Analysis

Crop Production & Farm Operations is set to dominate the Japan Agritech Market in 2026 with a projected share of 34.5%, thanks to its high deployment penetration across rice, wheat, soybean, vegetable, and fruit farming, government-backed digitalization programs, and clear return on investment through yield increase and labor reduction. Irrigation & Water Management follows as the second-largest segment, reflecting the importance of water efficiency in Japan's rice paddies and high-value crops. Smart Greenhouse & Controlled Environment Agriculture is gaining share due to the expansion of plant factories and premium vegetable production. Livestock Management, Post-Harvest & Supply Chain Management, and Agricultural Trade & Distribution Platforms account for the remainder, with marketplace platforms remaining comparatively smaller than production-focused applications.

By End User Analysis

Large Commercial Farms are projected to continue dominating the Japan Agritech Market, with an expected market share of 40.8% in 2026, owing to their larger scale, better access to capital, and ability to deploy robotics and full-farm FMIS. Smallholder & Family Farms remain numerous but contribute less revenue per farm. Agricultural Cooperatives maintain a substantial share because they play a critical role in facilitating technology access across Japan's fragmented farming landscape, aggregating smallholder output, and providing shared machinery and advisory services to member farms. Agribusiness & Corporate Farms are gradually expanding the adoption of advanced digital agriculture.

The Japan Agritech Market Report is segmented based on the following:

By Technology

- Precision Farming & Farm Management Systems

- Agricultural Robotics & Automation

- IoT & Smart Farming Devices

- Unmanned Aerial Vehicles

- Artificial Intelligence & Data Analytics

- Agricultural Biotechnology & Inputs

By Application

- Crop Production & Farm Operations

- Irrigation & Water Management

- Livestock Management

- Smart Greenhouse & Controlled Environment Agriculture

- Post-Harvest & Supply Chain Management

- Agricultural Trade & Distribution Platforms

By End User

- Large Commercial Farms

- Smallholder & Family Farms

- Agricultural Cooperatives

- Agribusiness & Corporate Farms

Competitive Landscape

The dynamics of competition in the Japan Agritech marketplace have developed to become increasingly dynamic, with a strong presence of domestic agricultural machinery giants, specialized robotics startups, FMIS software providers, and telecommunications companies entering the smart farming space. The essential ingredient for success is found in deep‑seated strategic partnerships with agricultural cooperatives and prefectural extension services, which open up distribution channels and allow premium training and maintenance services to be sold alongside hardware. Market consolidation trends are moving rapidly ahead, with established players in the tractor industry taking on acquisitions of AI analytics and drone startups to integrate their crop intelligence functionalities. Proprietary intellectual property rights, with AI‑based autonomous navigation algorithms, computer vision for selective harvesting, and disease detection models, hold increasing importance compared to just competitive hardware pricing and brand reputation.

Some of the prominent players in the Japan Agritech Market are:

- Kubota Corporation

- Yanmar Holdings Co., Ltd.

- Iseki & Co., Ltd.

- Yamaha Motor Co., Ltd.

- Mitsubishi Mahindra Agricultural Machinery Co., Ltd.

- Yamabiko Corporation

- Topcon Corporation

- OPTiM Corporation

- AGRIST Co., Ltd.

- Nileworks Inc.

- Inaho Co., Ltd.

- Spread Co., Ltd.

- TOWING Co., Ltd.

- Farmnote Holdings, Inc.

- Sakata Seed Corporation

- Kumiai Chemical Industry Co., Ltd.

- Nihon Nohyaku Co., Ltd.

- Hokko Chemical Industry Co., Ltd.

- Mitsui Chemicals, Inc.

- OAT Agrio Co., Ltd.

- Other Key Players

Recent Developments

- April 2026: Kubota Corporation announced its investment in U.S.-based agritech startup Agtonomy to accelerate development of autonomous farming platforms for specialty crops. The collaboration focuses on AI-driven automation systems and smart machinery integration to address labor shortages and improve precision farming efficiency in fruit, vegetable, and nut cultivation.

- February 2026: OPTiM Corporation launched its nationwide Drone Shading and Heat-Reduction Coating DX Service for agricultural greenhouses and livestock facilities, enabling automated drone-based environmental control using a digital platform for workflow, mapping, and operations management across Japan.

- November 2025: Yanmar Holdings Co., Ltd. entered a clean-energy agriculture partnership with JERA, SMBC Group, and SMFL to develop regional decarbonized farming models integrating renewable energy and agricultural production. The initiative aims to support Japan's rural revitalization and build sustainable agriculture-energy ecosystems.

- July 2025: Topcon Corporation expanded its precision agriculture portfolio with the launch of the UC7 Plus boom height control system, enhancing automated spray control and input efficiency for large-scale farming operations through advanced sensing and positioning technologies.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 2.0 Bn |

| Forecast Value (2035) |

USD 5.1 Bn |

| CAGR (2026–2035) |

10.8% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Technology, By Application, By End User |

| Country Coverage |

Japan |

Frequently Asked Questions

How big is the Japan Agritech Market?

▾ The Japan Agritech Market is poised to be valued at USD 2.0 billion in 2026 and is projected to reach USD 5.1 billion by 2035.

What is the CAGR of the Japan Agritech Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 10.8% from 2026 to 2035, reflecting the accelerating adoption of autonomous machinery, FMIS platforms, and AI diagnostics across Japanese agriculture.

What factors are driving the growth of the Japan Agritech Market?

▾ Key drivers include the severe aging and decline of the farming population, rising labor costs, government subsidies for smart agriculture, expansion of high-value greenhouse and plant factory production, and increasing food safety and traceability requirements for export markets.

What are the major trends in the Japan Agritech Market?

▾ Major trends include the integration of AI into yield forecasting and disease detection, the rise of autonomous tractor fleets and harvesting robots, the proliferation of drone-based spraying and seeding, and the focus on farm-to-fork traceability using blockchain and AI.

Who are the key players in the Japan Agritech Market?

▾ Key players include Kubota Corporation, Yanmar Holdings Co., Ltd., Iseki & Co., Ltd., Topcon Corporation, OPTiM Corporation, Farmnote Holdings, Inc., AGRIST Co., Ltd., NTT DATA Corporation, alongside other major machinery, robotics, and IT firms, and many more.

How is the Japan Agritech Market segmented?

▾ The market is segmented by technology, application, and end user.