What is the Japan Carbon Credit Market Size?

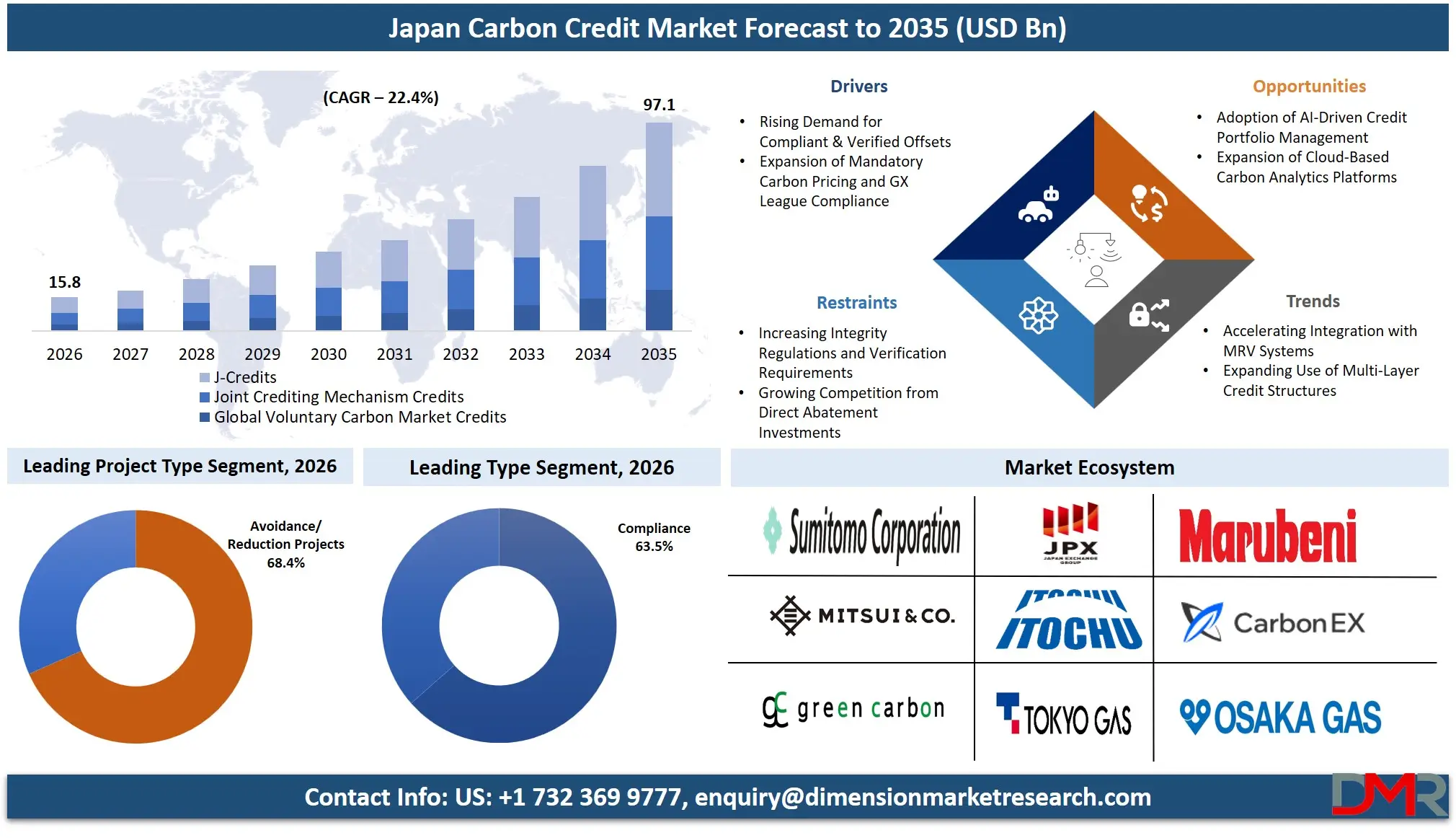

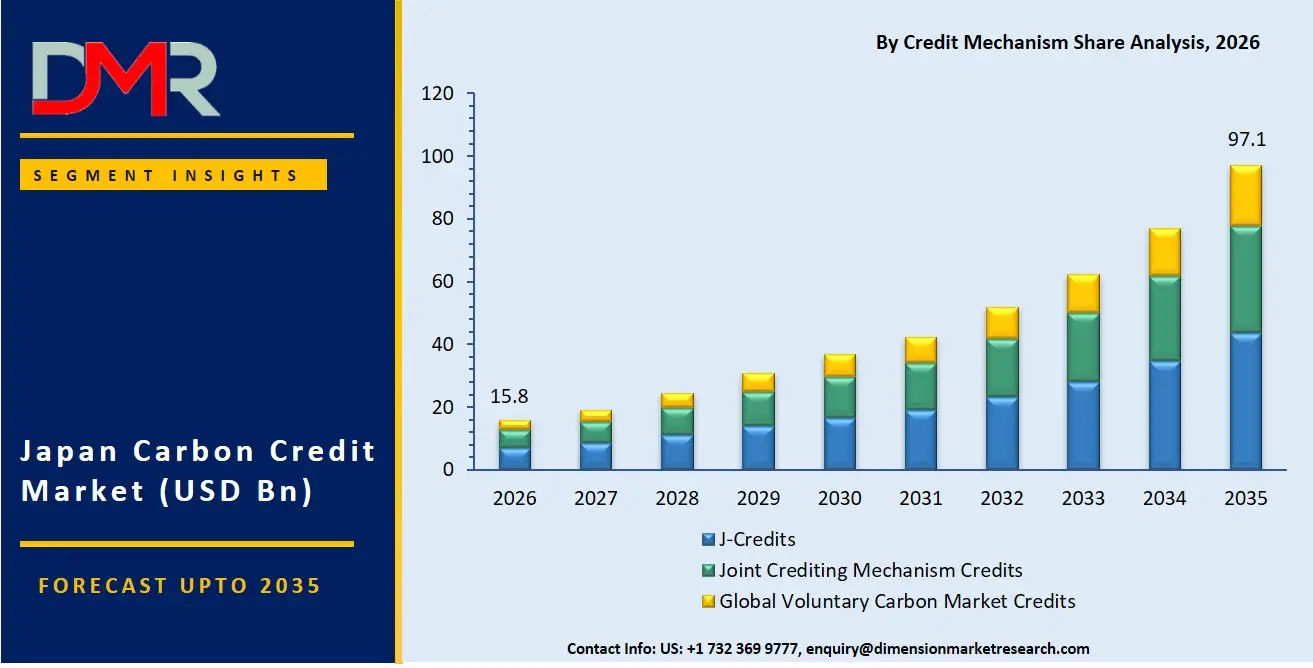

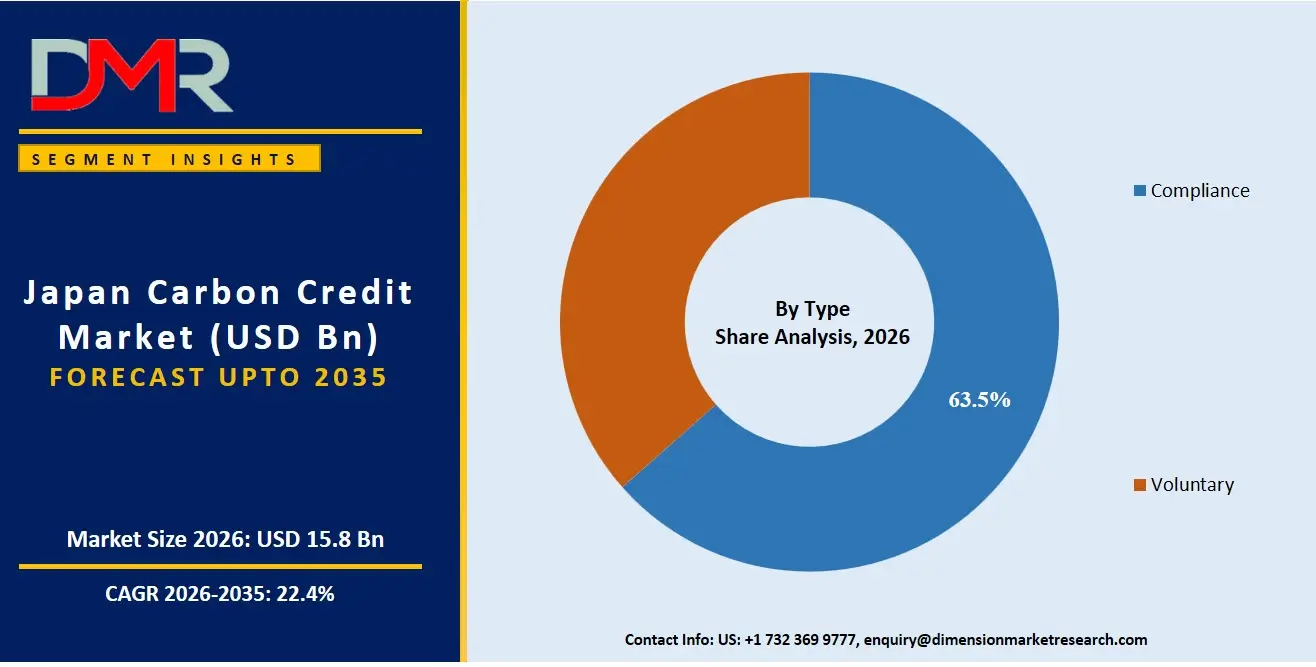

The Japan Carbon Credit Market is expected to reach a value of USD 15.8 billion in 2026, and it is further anticipated to reach USD 97.1 billion by 2035, growing at a CAGR of 22.4% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The carbon credit market has been showing consistent growth due to Japan's rising dependence on resilient, decarbonized, and decentralized offset mechanisms for effective, secure, and scalable emissions management. This includes several credit platforms and expert services that help industrial emitters and local governments deploy carbon-neutral solutions for power, manufacturing, and transport purposes. There has been a rising need for professional advisory services owing to the requirements for implementing verified emission reduction accounting, securing operational continuity against carbon pricing volatility, and delivering high-performance offset portfolio management to clients. Heavy industrial emitters have emerged as the largest consumer segment for carbon credit services, with J-Credits being the most popular choice due to their government backing and local credibility, while there has been rapid growth in global VCM credits and JCM project-based credits.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Key Takeaways

- Market Size & Forecast: The Japan Carbon Credit market is forecasted to be valued at USD 15.8 billion in 2026, growing incrementally to USD 97.1 billion by 2035, due to the joint efforts of energy strategy deployment on the part of enterprises as well as the obligatory deployment of zero-emission and compliant offset technologies.

- Growth Rate & Outlook: Japan market is expected to grow at 22.4% CAGR, propelled by the urgent need to mitigate emerging compliance deadline vulnerabilities, alongside increasing challenges in orchestrating cross-sectoral credit flows from industrial facilities, commercial buildings, and transportation networks.

- Primary Growth Drivers: Major driving factors comprise the transition from voluntary carbon neutrality goals towards mandatory compliance mechanisms under the GX League, the necessity to deploy secure and robust MRV (Monitoring, Reporting, Verification) systems, as well as the implementation of carbon accounting APIs necessitating unique platform & services expertise.

- Key Market Trends: Major trends encompass the introduction of AI-driven emission forecasting through commercial channels, usage of machine learning within industrial networks for supply chain decarbonization and preventing carbon leakage, and increased focus on credit integrity amidst rising regulatory scrutiny of compliance buyers.

- By Type Analysis: The Compliance segment is projected to dominate the Japan Carbon Credit Market due to mandatory emissions reduction obligations imposed on large industrial emitters, power utilities, and manufacturing facilities, with capabilities like regulatory audit trails, government-backed verification, and penalty avoidance, which offer daily operations, regional compliance, and real-time performance monitoring activities within carbon management.

- By Credit Mechanism Analysis: The J-Credits segment is projected to dominate the Japan Carbon Credit Market due to its high credibility, government endorsement, capability for domestic offsetting, and use in energy efficiency, renewable energy, and waste management for metropolitan areas, industrial zones, and government infrastructure.

- By End-Use Industry Analysis: The Power & Utilities segment is anticipated to dominate in the Japan Carbon Credit Market as grid operators comply with mandatory carbon pricing rules and utilize credits that are scalable, flexible, efficient, accessible for real-time compliance, provide AI-based consumption analytics, renewable integration, business continuity, and emissions management at a higher resolution.

What are Carbon Credits?

A Carbon Credit is about the unique set of platforms and expertise involved in operating tradable, verified emissions offsets. These credits, unlike conventional pollution permits, pertain to "the how and where" of high-integrity, real-time carbon management. It entails having a Credit Platform to provide the means through which emissions are monitored and retired for optimal decarbonization, and Services to help integrate compliance management, manage offset procurement costs, and optimize portfolio balancing. As companies face mandatory decarbonization commitments under Japanese law, it is important to have services that ensure that credits will be transacted successfully while maintaining cost and integrity measures.

Use Cases

- Utility Compliance: Electric utilities employ Carbon Credit Services for the acquisition of Compliance credits that include real-time retirement and audit trail notifications to avoid regulatory penalties and increase operational trust.

- Manufacturing Decarbonization: Industrial networks rely on Carbon Credit Platforms for deploying verified emission reduction integration, ensuring stable, net-zero operation, and maintaining compliance with regional carbon pricing mandates under the Tokyo Cap-and-Trade program.

- Public Infrastructure Offsets: Municipal authorities incorporate JCM credit APIs in order to push offset schedules and carbon adherence notifications to central emissions registries in real-time.

- Aviation Demand Response: Airline organizations leverage carbon analytics platforms in a cloud-based telematics suite to initiate geo-targeted credit procurement during peak carbon pricing seasons.

How AI is Transforming the Carbon Credit Market?

AI is revolutionizing the carbon credit industry through increased supply/demand forecasting and credit integrity verification capabilities. The analytics platform suite includes AI-based systems that detect retirement anomalies and portfolio inefficiencies in order to resolve them instantaneously, thereby preventing any financial losses and operational damage. In addition, the AI-driven functions of credit management services help organizations assess offset behavior, determine optimal retirement schedules, and customize their procurement planning. AI forms an essential part of governance and regulatory trust initiatives. Professional services involve intelligent agents that monitor compliance and keep carbon credit registries free of any non-compliant entries while ensuring that all operations comply with regulations and the stringent carbon integrity protocols in Japan.

Market Dynamics

Key Drivers in the Japan Carbon Credit Market

Rising Demand for Compliant & Verified Offsets

There is an observable increase in the demand for verified carbon credits within the Japan carbon market due to the importance that companies attach to regulation compliance and ESG standards. Carbon credits have become an integral component in the overall decarbonization strategies of firms, especially those working in industries that consume huge amounts of energy. Companies are now paying close attention to credit quality, traceability, and emissions reduction accuracy. Internal company management has also been bolstered to mitigate potential reputation risks. As a result, structured credit management and procurement planning are becoming more important across industrial buyers, supporting steady market expansion and improving overall confidence in verified carbon offset instruments.

Expansion of Mandatory Carbon Pricing and GX League Compliance

Japan's carbon credit market is experiencing significant momentum in the wake of the progressive adoption of mandatory carbon price schemes and the development of GX League towards its evolution into GX-ETS. Various sectors including power generation, manufacturing, real estate, and transport are now under pressure to monitor their emissions and implement systematic strategies to decarbonize their operations. The move towards mandatory carbon pricing and emissions trading is motivating companies to trade carbon credits as flexible mechanisms to achieve their compliance obligations amidst cost concerns. The increased adoption of a regulated carbon market is also helping corporates plan better for the future. Carbon credits have become a crucial part of Japan’s overall decarbonization strategy.

Restraints in the Japan Carbon Credit Market

Increasing Integrity Regulations and Verification Requirements

The Japan carbon credits market is increasingly becoming burdened by tightening regulations that require verifications. There are strict verification systems meant to ensure that there is proper issuance of carbon credits, no double issuance of credits, and also to create transparency in the carbon market. Although this improves the credibility of the carbon market, it becomes very costly in terms of compliance for carbon credit issuers. Buyers must undergo various processes of verifying carbon credits as well. Companies have to undergo rigorous documentation and process procedures to facilitate compliance, thereby making it very expensive in some cases and causing delays for small firms that cannot afford to do so.

Growing Competition from Direct Abatement Investments

One of the main factors affecting the Japan carbon credit market is the rising preference for direct mitigation efforts over the buying of carbon credits. Several industrial giants have been putting money into renewable energy sources, electrification technology, and process efficiencies that help lower emissions directly. Direct mitigation initiatives are seen as more cost-efficient in the long run and have better synergy with the company's sustainability policy. As a consequence, the use of carbon credits may diminish in specific industries, where emissions can be lowered via direct means. Large manufacturing and energy-consuming firms have proven to be particularly susceptible to this trend.

Growth Opportunities in the Japan Carbon Credit Market

Adoption of AI-Driven Credit Portfolio Management

With growing intricacy in carbon compliance rules in Japan, there are more chances for credit portfolio management systems to get enhanced. More and more firms are moving to adopt advanced technologies that provide insight into the process of buying, retiring, and reducing costs related to carbon credits. The systems allow companies to make smart business moves through studying the history of previous actions and predicting the future demand for credits. In light of growing sophistication of corporate sustainability reports, firms want their carbon credit management process to be efficient and streamlined, especially when it comes to several kinds of credits – namely J-Credits, JCM credits, and voluntary offsets.

Expansion of Cloud-Based Carbon Analytics Platforms

Another opportunity that has emerged in Japan’s carbon credit market space is cloud-based carbon analytics platforms. These platforms help organizations to keep track of their emissions information, comply with regulatory requirements, and facilitate credit acquisition within an integrated framework. Such platforms are being adopted by energy, manufacturing, and logistics companies due to their benefits for accurate reporting and meeting the demands of ESG reporting requirements. As a result of increasing focus on digital transformation within corporate sustainability management efforts, organizations are adopting this solution at a fast pace. Also, due to enhanced integration capabilities and monitoring functionalities, organizations are able to make more efficient and precise decisions about carbon offsets.

Trends in the Japan Carbon Credit Market

Accelerating Integration with MRV Systems

Integration of monitoring, reporting, and verification (MRV) technology into carbon credit schemes is gaining popularity in the Japanese carbon credit market. The use of digital MRV technology by industries ensures that the data recorded is accurate and reliable. Carbon emissions can be tracked in real time, and this facilitates regulatory compliance by industries. The integration of MRV technology also increases transparency when it comes to carbon credits generation and application in the industry. The increasing demand for standardized reporting procedures and automation due to expanding decarbonization activities by firms calls for MRV technology. This is more so in emission-intensive sectors.

Expanding Use of Multi-Layer Credit Structures

Japanese companies are increasingly employing multi-level carbon credit schemes that involve J-Credits, JCM credits, and voluntary international carbon credits. Such a strategy allows corporations to consider both cost effectiveness, credit availability, and their quality when dealing with various compliance issues. The adoption of different sources of carbon credits is beneficial since it gives a company the chance to balance emissions on different levels in terms of geography and supply chain management. In addition, it allows organizations to consider both domestic regulations and global carbon footprint targets. Overall, a hybrid credit scheme becomes a frequent choice in the developing carbon trading market environment.

Research Scope and Analysis

The Japan Carbon Credit Market is segmented by type, credit mechanism, project type, trading platform, and end-use industry. The market supports industrial compliance, corporate voluntary commitments, aviation offsetting, and municipal decarbonization across individual buyers, industrial emitters, public authorities, and energy companies through cloud-based and on-premise credit management solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Type Analysis

Compliance credits are expected to lead the Japan Carbon Credit Market in 2026 with a projected market share of 63.5%, as a result of mandatory emissions trading schemes under the GX League, the Tokyo Cap-and-Trade Program, and Saitama Target Setting System. Japanese power utilities, steel manufacturers, and chemical producers have developed a strong preference for Compliance credits for performing such critical functions as regulatory obligation fulfillment, penalty avoidance, and auditable retirement tracking that meets government standards. The compliance segment benefits directly from Japan's legally binding carbon reduction targets under the Paris Agreement and the country's commitment to achieve carbon neutrality by 2050, which forces large emitters to procure verified offsets or face substantial financial penalties. Furthermore, the expansion of the GX League's emissions trading framework has brought hundreds of additional industrial facilities under mandatory carbon pricing, creating consistent and predictable demand for compliance-grade credits. These credits are issued through government-approved mechanisms such as the J-Credit Scheme, ensuring that each credit represents a real, additional, and permanently verified emission reduction.

By Credit Mechanism Analysis

J-Credits are projected to dominate the Japan Carbon Credit Market in 2026 with an estimated share of 51.6%, owing to their widespread adoption in energy efficiency, renewable energy, and waste management projects across all 47 prefectures of Japan. Japanese industrial buyers and energy aggregators strongly favor J-Credits because they provide government-backed integrity along with domestic additionality and low reputational risk, making them the safest choice for compliance buyers who cannot afford any questions about credit quality or verification standards. The J-Credit Scheme, jointly operated by Japan's Ministry of Economy, Trade and Industry (METI), Ministry of the Environment (MOE), and Ministry of Agriculture, Forestry and Fisheries (MAFF), offers a streamlined registration and issuance process that reduces transaction costs and administrative burdens for project developers. Credits generated under this mechanism cover a wide range of project types, including solar and wind power generation, biomass energy utilization, energy efficiency improvements in factories and buildings, waste heat recovery, and forestry management activities that enhance carbon sequestration.

By Project Type Analysis

Avoidance/Reduction Projects are expected to lead the Japan Carbon Credit Market in 2026 with a projected market share of 68.4%, owing to their lower cost, faster implementation, and widespread availability across renewable energy, energy efficiency, fuel switching, and waste management applications throughout Japan. Japanese industrial buyers and utilities strongly prefer avoidance credits for near-term compliance obligations under the GX League and Tokyo Cap-and-Trade programs because these credits can be generated relatively quickly and cost-effectively compared to removal projects that require longer timeframes and more complex verification protocols. Renewable energy projects, including solar, wind, biomass, and small-scale hydro, constitute the largest source of avoidance credits in Japan, benefiting from the country's aggressive renewable feed-in tariff programs and the gradual reopening of nuclear power plants. Energy efficiency projects in commercial buildings, industrial facilities, and residential housing also generate substantial volumes of avoidance credits by reducing electricity consumption and associated emissions from fossil fuel-based generation. Fuel switching projects that replace coal or heavy oil with natural gas, biomass, or hydrogen further contribute to the avoidance category.

By Trading Platform Analysis

The Over-The-Counter (OTC) segment is projected to continue dominating the Carbon Credit Market of Japan with an expected market share of 71.4% in 2026, owing to bilateral contract flexibility, customized delivery terms, and direct relationships between project developers and corporate buyers that have been cultivated over many years of market participation. Businesses in the OTC segment are increasingly adopting carbon credit procurement through bilateral agreements because of the significant benefits offered by such systems, including lower transaction costs compared to exchange trading, predictable pricing through long-term offtake contracts, and direct regulatory compliance with integrity mandates that require buyers to verify project details and credit quality before purchase. OTC transactions allow buyers and sellers to negotiate specific contract terms including credit vintage, project type, delivery schedule, and price adjustment mechanisms that are simply not available on standardized exchange platforms. Large corporate buyers in Japan, particularly electric power companies, steel manufacturers, and trading houses, prefer OTC deals because they can secure large volumes of credits from specific projects that align with their sustainability strategies.

By End-Use Industry Analysis

Power & Utilities is set to dominate the Japan Carbon Credit Market in 2026 with a projected share of 34.2%, thanks to its high emission intensity, mandatory compliance obligations under the GX League emissions trading framework, and relatively low abatement cost curve compared to other industrial sectors. Power & Utilities companies enable real-time compliance monitoring, portfolio balancing across multiple generating assets, and granular offset analytics that do not necessitate additional infrastructure investment beyond existing environmental management systems. Japan's ten regional electric power companies, including Tokyo Electric Power Company (TEPCO), Kansai Electric Power Company (KEPCO), and Chubu Electric Power Company, collectively operate hundreds of fossil fuel-fired power plants that generate significant carbon dioxide emissions requiring offset procurement under mandatory carbon pricing mechanisms. These utilities face increasing pressure from both regulators and shareholders to demonstrate measurable progress toward decarbonization while maintaining reliable and affordable electricity supply to residential, commercial, and industrial customers across their service territories. Many power companies have established dedicated carbon credit procurement teams and portfolio management systems to optimize their credit purchasing strategies.

The Japan Carbon Credit Market Report is segmented based on the following:

By Type

By Credit Mechanism

- J-Credits

- Joint Crediting Mechanism (JCM) Credits

- Global Voluntary Carbon Market (VCM) Credits

By Project Type

- Avoidance/Reduction Projects

- Removal/Sequestration Projects

- Nature-based Projects

- Technology-based Projects

By Trading Platform

- Exchange-Traded

- Over-The-Counter (OTC)

By End-Use Industry

- Power & Utilities

- Manufacturing & Industrial

- Aviation

- Automotive & Transportation

- Buildings & Construction

- Agriculture & Forestry

- Waste Management

- Others

Competitive Landscape

The dynamics of competition in the Japan Carbon Credit marketplace have developed to become increasingly dynamic, with a wide range of multinational credit providers, Japanese carbon aggregators, and analytics platform players specializing in various niche credit management functions. The essential ingredient for success is found in deep-seated strategic partnerships with renewable energy developers and industrial emitters in Japan, which open up high-quality credit supply chains and allow premium credit retirement services to be sold alongside one another. Market consolidation trends are moving rapidly ahead, with established players in the world of industrial decarbonization and energy providers taking on acquisitions of specialized analytics platform providers to leverage their AI forecasting functionalities. Proprietary intellectual property rights, with AI-based price prediction algorithms and portfolio optimization engines, hold increasing importance compared to just competitive credit pricing and registry access.

Some of the prominent players in the Japan Carbon Credit Market are:

- Japan Exchange Group, Inc.

- Tokyo Stock Exchange, Inc.

- Sumitomo Corporation

- Marubeni Corporation

- Mitsui & Co., Ltd.

- Mitsubishi Corporation

- Itochu Corporation

- Mizuho Bank, Ltd.

- MUFG Bank, Ltd.

- Sumitomo Mitsui Banking Corporation

- Daiwa Securities Group Inc.

- ENEOS Holdings, Inc.

- JERA Co., Inc.

- Tokyo Gas Co., Ltd.

- Chubu Electric Power Co., Inc.

- Osaka Gas Co., Ltd.

- Nippon Steel Corporation

- Green Carbon, Inc.

- Bywill Inc.

- Carbon EX Co., Ltd.

- Other Key Players

Recent Developments

- April 2026: Green Carbon, Inc. announced the complete sell-out of approximately 65,000 tCO₂e of J-Credits generated through its rice cultivation methane reduction projects in Japan, reflecting rising corporate demand for high-traceability domestic agricultural carbon credits under the J-Credit Scheme.

- April 2026: Japan Exchange Group, Inc. advanced the implementation of Japan’s mandatory GX-ETS phase, supporting carbon allowance trading infrastructure for companies representing nearly 60% of the country’s emissions, reinforcing the expansion of the domestic carbon market ecosystem.

- February 2026: Tokyo Stock Exchange, Inc. reported a significant increase in carbon credit trading activity as major Japanese emitters accelerated purchases ahead of the mandatory GX-ETS compliance phase, strengthening Japan’s transition toward a nationwide emissions trading framework.

- August 2025: Sumitomo Corporation expanded its decarbonization and carbon credit trading initiatives through investments in nature-based carbon removal and GX-related emissions management projects, strengthening its position in Japan’s growing voluntary carbon market ecosystem.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 15.8 Bn |

| Forecast Value (2035) |

USD 97.1 Bn |

| CAGR (2026–2035) |

22.4% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Type, By Credit Mechanism, By Project Type, By Trading Platform, By End-Use Industry |

| Country Coverage |

Japan |

Frequently Asked Questions

How big is the Japan Carbon Credit Market?

▾ The Japan Carbon Credit Market is poised to be valued at USD 15.8 billion in 2026 and is projected to reach USD 97.1 billion by 2035, driven by the universal need for secure, scalable, and reliable digital carbon retirement solutions.

What is the CAGR of the Japan Carbon Credit Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 22.4% from 2026 to 2035, reflecting the maturing nature of the carbon market and the accelerating complexity of multi-channel, interactive offset strategies.

What factors are driving the growth of the Japan Carbon Credit Market?

▾ Key drivers include the decarbonization imperative for carbon reduction, the need to integrate voluntary and compliance mechanisms, the management complexity of multi-jurisdictional credit procurement, and the surge in demand for credit portfolio management amid evolving carbon pricing laws under the GX League.

What are the major trends in the Japan Carbon Credit Market?

▾ Major trends include the integration of AI into credit demand forecasting and integrity verification, the rise of J-Credit and JCM project registrations, the demand for vertical-specific analytics solutions, and the focus on secure, fraud-resilient credit retirement practices.

Who are the key players in the Japan Carbon Credit Market?

▾ Key players include Japan Exchange Group, Inc., Carbon EX Co., Ltd., Mitsui & Co., Ltd., Mitsubishi Corporation, Itochu Corporation, Mizuho Bank, Ltd., and many more.

How is the Japan Carbon Credit Market segmented?

▾ The market is segmented by type, credit mechanism, project type, trading platform, and end-use industry.