What is the Chronic Disease Management Market Size?

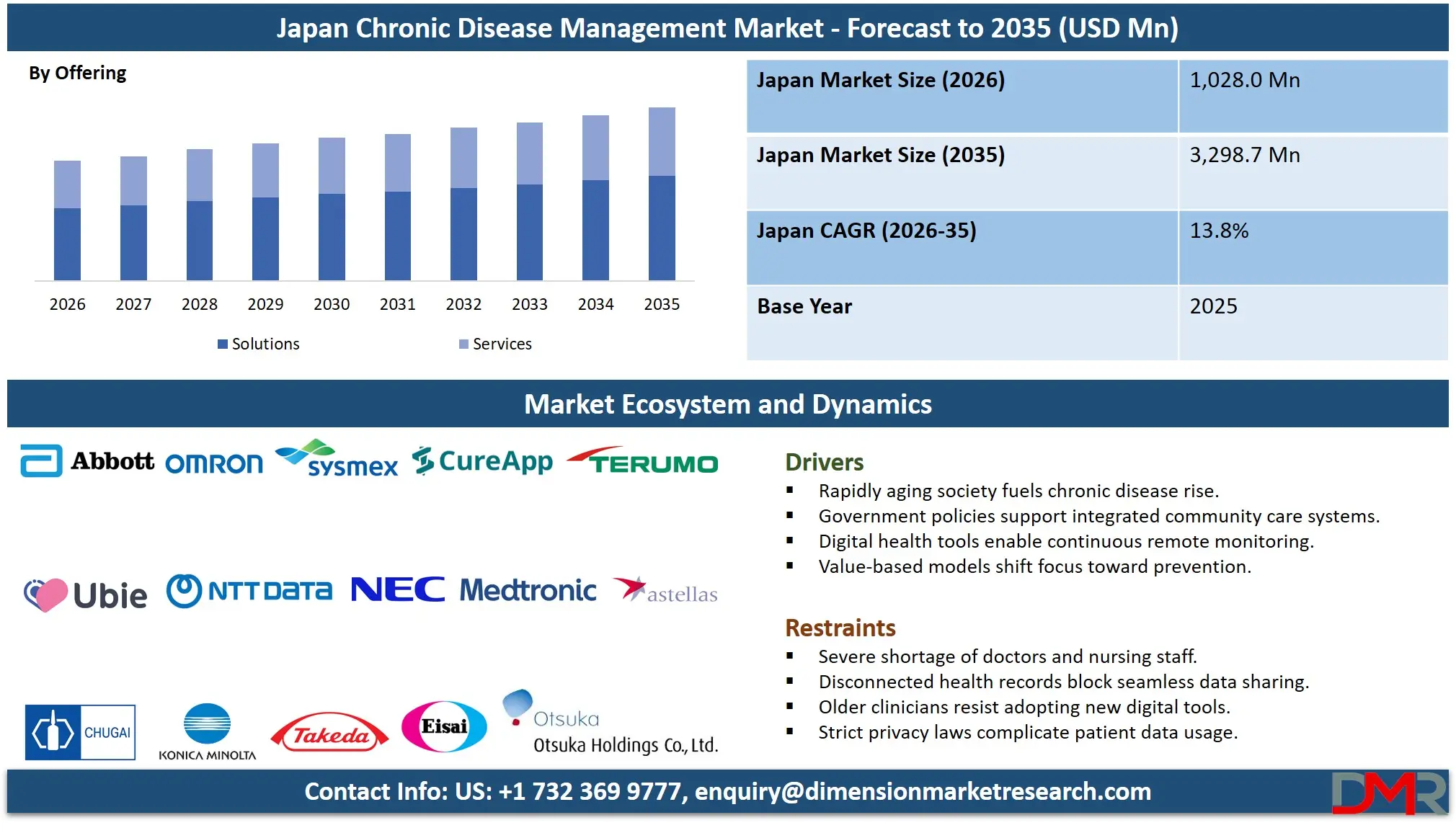

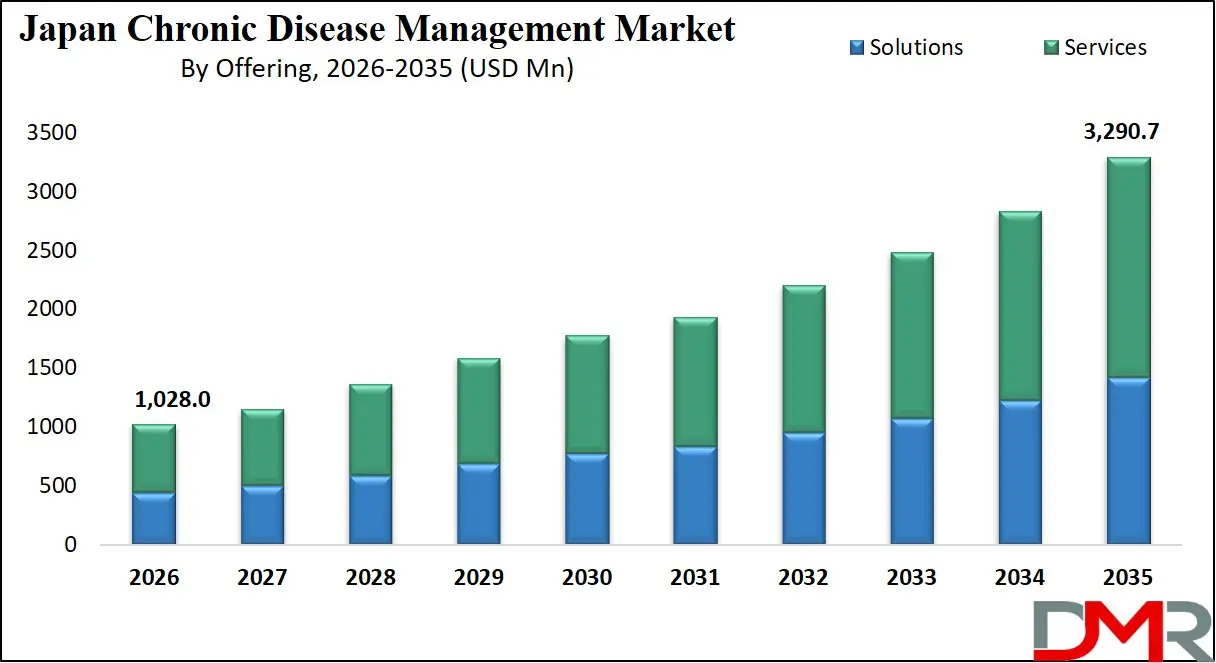

The Japan Chronic Disease Management market is expected to reach a value of USD 1,028.0 million in 2026, and it is further anticipated to reach USD 3,290.7 million by 2035, growing at a CAGR of 13.8% during the forecast period. The Chronic Disease Management in Japan entails the incorporation of digital health systems, remote care monitoring systems, and value-based care coordination in managing the aging population in Japan, which constitutes almost 30.0% of the entire population. The accelerating phenomenon of super-aging, together with the shrinking labor force, has exerted tremendous structural strain on the national healthcare system, which is pushing the industry toward vigorous policy changes in favor of preventive care, hospital-at-home care, and the digitalization of medical records.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The main innovation hubs to develop AI-based diagnostics and IoT-enabled elder care technologies are Tokyo, Osaka-Kansai, and the Fukuoka startup ecosystem. The market ecosystem comprises large Japanese electronic conglomerates that have shifted their focus to MedTech, highly focused HealthTech startups, university research clusters in hospitals, and the national health insurance system (NHI), the major payer and regulator.

Additionally, the Long-term Care Insurance (LTCI) reforms at the Ministry of Health, Labour and Welfare and the Vision of a Digital Garden City Nation are obligating regional providers to implement advanced care management systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Key Takeaways

- Market Size & Forecast: Japan Chronic Disease Management market is projected to reach USD 1,028.0 million by 2026 and expand dramatically to USD 3,290.7 million by 2035, fueled by the dual drivers of generative AI commercialization and heightened national security concerns regarding synthetic media.

- Growth Rate & Outlook: Market growth is expected at a CAGR of 13.8%, due to the sharp rise in lifestyle-related diseases among the working-age population (shakai hoken) and the reimbursement expansion for online medical consultations and remote monitoring under the national fee schedule.

- Primary Growth Drivers: The driving forces include the 2024-26 medical fee revisions which permanently increased reimbursement for telehealth and RPM. The proliferation of "Family Pharmacy" networks requiring digital medication adherence tracking, and the corporate mandate for Kenko Keiei (Health and Productivity Management) forcing large enterprises to invest in employee wellness platforms.

- Key Market Trends: Among the main market trends are the integration of RPM data into the Karte (Electronic Medical Record) workflow, the application of AI for early detection of frailty and sarcopenia, the expansion of Special Zones for Telemedicine (Kekkaku Tokku), and the convergence of CDM software with the government's My Number (MynaPortal) health record infrastructure.

- By Offering Analysis: Solutions will prevail in offering segment with high demand of disease specific software particularly in diabetes and heart failure management. Home healthcare providers are quickly adopting Remote Patient Monitoring platforms, and employer-sponsored health plans are increasingly adopting outsourced disease management services.

- By Deployment Type Analysis: Cloud-based solutions lead due to strict data security guidelines and the need for seamless data sharing across medical institutions. Hybrid models remain important for large hospitals managing sensitive data, ensuring compliance with local regulations while maintaining operational flexibility.

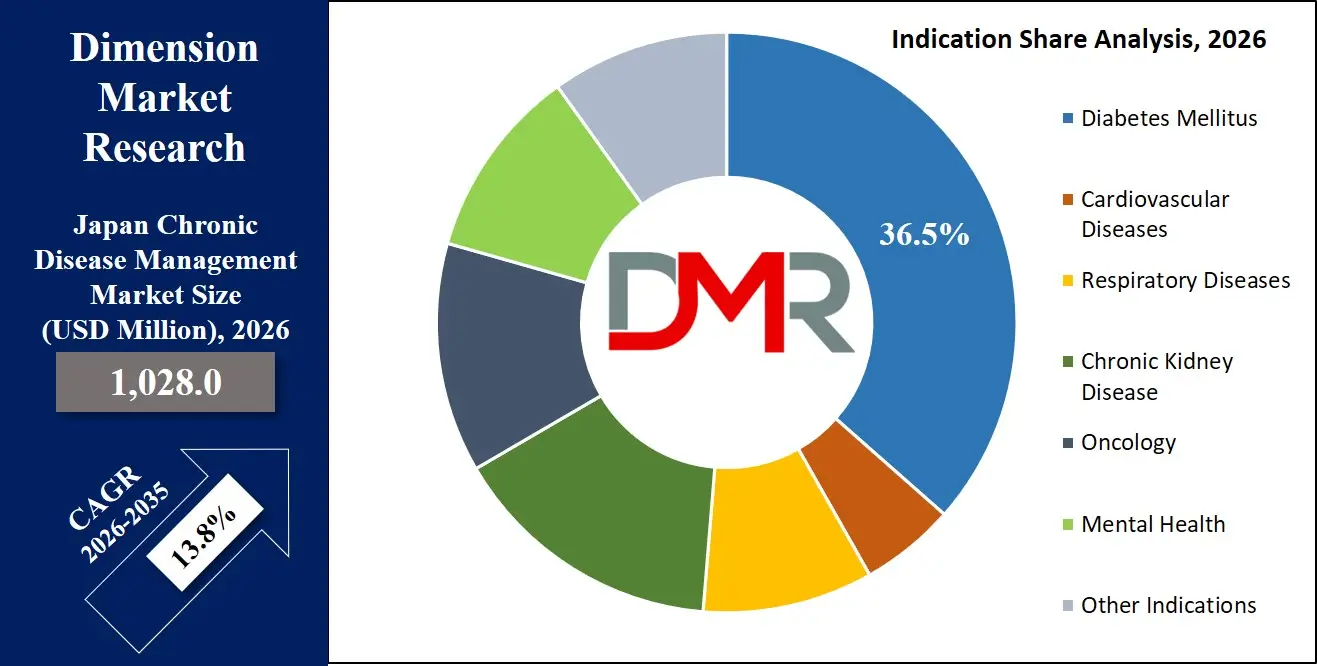

- By Indication Analysis: Diabetes Mellitus is poised to be the largest segment since nationwide screening programs will entail continuous monitoring. The most rapidly growing segment with increasing cases in the elderly is cardiovascular diseases, which is mostly heart failure.

What is the Chronic Disease Management?

Chronic Disease Management (CDM) is a model of healthcare delivery that is systematic and coordinated and is meant to be used in people with long-term diseases, like diabetes, heart failure, COPD, or high blood pressure. Instead of treating acute care in episodic, acute care, CDM focuses on continuous, proactive monitoring and educating patients to avoid complications and hospitalization. It combines clinical guidelines, self-management devices, remote monitoring devices, and multidisciplinary care teams to maximize the quality of life and health outcomes. The aim is to empower the patients with lifestyle change support and medication adherence monitoring and give clinicians information-driven insights. CDM helps reduce the cost burden on the healthcare system by filling the gap between face-to-face visits with online touchpoints and analytics to enhance longitudinal care among aging and vulnerable groups, thereby lowering the total cost burden of healthcare systems.

Use Cases

- Corporate Health & Productivity Management: Japanese trading companies (Sogo Shosha) and manufacturers use diabetes and mental health management systems to meet METIs Kenko Keiei standards, minimizing presenters due to hypertension and metabolic syndrome.

- Municipal Elderly Care & Frailty Prevention: Municipal governments use Remote Patient Monitoring (RPM) systems designed to access the vital and activity rate of elderly living alone in rural depopulated regions combined with the Kaigo Yobo (Long-Term Care Prevention) services.

- Pharmacy-Linked Adherence Tracking: Family pharmacists (Kakaritsuke Yakuzaishi) manage polypharmacy in the elderly by using mobile apps that allow them to keep track of medication adherence to medication reviews that patients must comply with under the new dispensing fee systems.

- Cancer Survivorship & CAR-T Follow-up: Specialty cancer centers are developing at National Cancer Center hospitals to address the issue of adverse events after discharge and long-term follow-up of patients receiving advanced immunotherapy.

Market Dynamics

Key Drivers of the Japan Chronic Disease Management Market

Reimbursement Reform and the Digital Shift

The biannual updates of medical fees by the MHLW (Shinryo Houshu Kaitei) have decisively altered incentives towards outpatient and digital care. The introduction of permanent increases in fees on "Medical Information and Communication Technology" and Remote Management Fees on the hypertension and diabetes have made it economically effective to invest in software by the clinics. The 2024 revision specifically covered remote monitoring of heart failure patients who have implantable devices and provided a direct stream of revenue to cardiologists who implement CHF platforms.

Structural Aging and Workforce Shortage

Japan is experiencing a serious shortage of physicians in the regions and a declining number of home care workers. The government is requiring the employment of technology as a substitute to labour with more than 30 percent of the population aged above 65 and predicted shortage of 570,000 care workers by the year 2040. CDM platforms with AI-based risk stratification can assist visiting nurses in prioritizing high-acuity patients, which can be used to supplement the limited human labor force.

Market Challenges / Restraints in the Japan Chronic Disease Management Market

Legacy IT Fragmentation and Data Interoperability

Although the rates of EMR adoption are high in Japan, they have been associated with notoriously siloed and vendor-locked systems. It has been slow to integrate with the national MynaPortal because of the complex privacy regulations and because of the disposition of large EMR vendors such as Fujitsu, NEC and Sysmex to easily open APIs. A CDM vendor can only do custom engineering on a hospital with a HOPE/EGMAIN system to a local clinic with a MediBrow system; this is a complex and expensive endeavor in terms of time, which prevents scalability.

The "Monthly Visit" Culture

The Japanese culture of visiting the clinic regularly and in person every month due to stable chronic conditions is a cultural and economic obstacle to pure digital RPM. The touch and the personal interaction of the doctor with patients tend to bring a psychological reassurance (Ishin Denshin). The best telehealth platforms are thus most readily adopted in the market through hybrid models in which face-to-face visits are extended to either bi-monthly or quarterly with the supplement of data instead of complete virtual replacement.

Growth Opportunities in the Japan Chronic Disease Management Market

Integration with Next-Generation Karte and PHR

There is a huge untapped market among software vendors capable of writing seamless integration connectors (FHIR-based APIs) to the leading Japanese EMR ecosystems. The Next-Generation Medical Infrastructure Law advocated by the government generates the requirement of analytics platforms, capable of anonymizing and using real-world information (RWD) in hospital records. Secondary revenue stream RWD aggregators that also serve as CDM platforms to Pharma and MedTech companies command a large share.

Specialist-Driven Chronic Care in Retail Settings

With the liberalization of restrictions on the outside dispensing system, clinics in drugstore chains (ex: Welcia, Matsumoto Kiyoshi) are turning into the main points of contact with lifestyle diseases. CDMs that are customized to the requirements of these "Health Support Pharmacies" to handle walk-in cholesterol and glucose checks offer a high-growth channel of distribution that is different than the hospital-centric model.

Trends in the Japan Chronic Disease Management Market

The Rise of Ninchisho (Dementia) Digital Management

Although diabetes and CVD are the most common, the fastest-growing niche is the use of digital tools in managing Alzheimer's and other forms of dementia. Early detection and community support are required in the Orange Plan national strategy on dementia. Digital cognitive assessment tools and GPS-linked wearables to prevent wandering are also being integrated into CDM platforms and are reimbursable by Long-Term Care Insurance.

Pharma-Driven Beyond-the-Pill Services

Japanese pharmaceutical giants are transforming their sales of pure drugs into integrated services of disease management. As an illustration, firms that sell SGLT2 inhibitors to treat diabetes and CKD are collaborating with startups to provide branded RPM applications to enhance medication compliance and gather real-world evidence to negotiate NHI prices.

Research Scope and Analysis

By Offering Analysis

Solutions are predicted to lead the offering segment due to the increase in the demand of disease-specific software including diabetes management and chronic heart failure (CHF) platforms. These solutions conform to outpatient management fee structures supported by the government, and thus, it is imperative to providers. The most rapid growth can be observed in Remote Patient Monitoring (RPM) platforms, especially when it comes to the home healthcare agencies that are trying to streamline the workforce and lower labor expenses. In the meantime, services, particularly disease management programs provided by outside healthcare professionals, are taking off with large employer sponsored health plans. The programs are aimed at enhancing preventive health outcomes, promoting better employee health screening outcomes, and finally lowering insurance premiums and long-term health care spending.

By Deployment Type Analysis

The cloud-based deployment models is poised to dominate the market as there is a high requirement of strict regulations regarding the security of medical data and the demand of interoperability among healthcare facilities. These solutions facilitate easy data exchanges and sharing of data between clinics within medical corporations, improving care coordination and efficiency. Nevertheless, the hybrid deployment models remain relevant, particularly in large national universities hospitals and sophisticated treatment facilities. Such organizations frequently have access to very sensitive information, such as genomic and oncology databases, which are required to be stored on-premise, in accordance with strict local data protection laws. Hybrid models are therefore a compromise, providing the scalability of cloud systems with the flexibility and control of on-premises infrastructure.

By Indication Analysis

Diabetes Mellitus is poised to be a major indication segment, mainly because of the national screening programs that demand continuous monitoring and follow up treatment of millions of individuals every year. This spurred long-term need in digital management solutions and patient engagement tools. The cardiovascular diseases, and especially heart failure are the most rapidly increasing segment since Japan is aging with greater cardiac risks.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

With the introduction of reimbursement policies to finance remote cardiac monitoring, there is an enhanced growth in the adoption of CHF platforms to minimize hospital readmissions. Chronic Kidney Disease (CKD) is also becoming a focal point of concern, with the economic cost of dialysis-based therapies being high, and the focus on preventative nephrology care interventions and preemptive intervention approaches.

By Technology

Wearables and connected devices form the backbone of digital health ecosystems, especially in aging societies like Japan, where device comfort and discreet design are prioritized to encourage long-term usage. The technologies allow real-time monitoring of crucial health indicators. Predictive analytics with Artificial Intelligence (AI) and Machine Learning (ML) serve as important points of difference between solution providers. High-tech systems that can predict frailty, stroke risk, or disease development with the help of the national health databases have great clinical importance. As well, mobile apps and SMS-enabled platforms are essential tools of engagement, especially among younger insured groups, to provide lifestyle tips, medicine reminders, and preventive care reminders, which can facilitate behavior change and better health results.

By End User

Healthcare providers, particularly ambulatory care centers and small clinics, represent the largest user base due to Japan's decentralized and clinic-focused primary care system. These centers depend on online systems greatly to handle patient volumes effectively and provide care around the clock. Payers such as the national health insurance societies and government insurance systems are key players in market dynamics as they influence care models and reimbursement policies. The market of the private insurers is still relatively niche, with the supplementary health insurance and corporate wellness programs. At the same time, pharmaceutical and medical technology firms are becoming strategic partners, combining digital health tools with treatments to improve treatment outcomes, increase patient adherence, and innovate value-based care delivery.

Japan Chronic Disease Management Market Report is segmented based on the following:

By Offering

- Solutions

- Disease-Specific Software

- Diabetes Management Platforms

- CHF/CVD Platforms

- COPD Platforms

- Remote Patient Monitoring (RPM) Platforms

- Telehealth / Teleconsultation Platforms

- Analytics & Population-Health Platforms

- Clinical Decision Support

- Risk Stratification

- Mobile Apps & Patient Engagement Tools (mHealth)

- Integration & EHR Connectors

- Services

- Disease Management Programs

- Remote Monitoring Services

- Consulting & Implementation

- Training & Support

By Deployment Type

- Cloud-based

- On-premises

- Hybrid

By Indication

- Diabetes Mellitus

- Cardiovascular Diseases

- Heart Failure

- Hypertension

- Coronary Artery Disease

- Respiratory Diseases

- Chronic Kidney Disease

- Oncology

- Mental Health

- Depression

- Anxiety

- Chronic Behavioral Health Comorbidity

- Other Indications

By Technology

- Wearables & Connected Devices

- IoT & Sensors

- AI / ML & Predictive Analytics

- Clinical Decision Support

- Mobile Apps & SMS Platforms

By End User

- By Providers

- Ambulatory Care Centers

- Hospitals, Physician Groups & Integrated Delivery Networks

- Home Healthcare Agencies

- Nursing Homes & Assisted Living Facilities

- Diagnostic & Imaging Centers

- Pharmaceutical & Medtech Companies

- By Payer

- Public Payers (Medicare, Medicaid)

- Private Insurers

- Employer-Sponsored Health Plans

Competitive Landscape

The Japan Chronic Disease Management market features a competitive environment comprising domestic electronic health record giants, telecom carriers leveraging IoT networks, and specialized HealthTech ventures. Unlike the US market, global platform giants like Epic or Cerner face significant localization barriers due to Japanese medical fee logic and language.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The most successful players are those with deep partnerships with established Japanese infrastructure providers (Fujitsu, NEC) and those who have navigated the complex Iryo Joho System (Medical Information System) certification process. Mergers between traditional MedTech manufacturers (Omron, Tanita) and software startups are accelerating.

Some of the prominent players in the Chronic Disease Management Market are:

- Omron Healthcare Co., Ltd.

- Otsuka Pharmaceutical Co., Ltd.

- Abbott

- Sysmex

- CureApp

- Terumo

- Kyowa Kirin Co., Ltd.

- Koninklijke Philips N.V.

- Ubie

- NTT Data

- NEC

- Medtronic Japan

- Teladoc Health, Inc.

- Astella

- DarioHealth Corp.

- Biofourmis, Inc.

- Chugai

- Konica Minolta

- Takeda Pharmaceutical Company Limited

- Eisai

- Other Key Players

Recent Developments

- March 2026: The Japan Agency for Medical Research and Development (AMED) announced new grant funding specifically for AI-based systems aimed at predicting Hiesho (cold sensitivity) and managing multi-morbidity in elderly women.

- December 2025: Sompo Holdings expanded its "Nursing Care & Digital" division, acquiring a local RPM startup to integrate real-time sensor data from senior housing facilities directly into its long-term care insurance claim workflows.

- August 2025: The Ministry of Internal Affairs and Communications (MIC) released new guidelines encouraging the use of Local 5G networks in hospitals for secure, high-bandwidth transmission of remote ultrasound and endoscopic images for chronic liver disease management.

- May 2024: Omron Healthcare announced a collaboration with a major university hospital in Tokyo to utilize its VitalSight RPM data to validate the clinical utility of remote cardiac monitoring specifically for Japanese JCS Heart Failure Guidelines.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 1,028.0 Mn |

| Forecast Value (2035) |

USD 3,290.7 Mn |

| CAGR (2026–2035) |

13.8% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Offering (Solutions, Services), By Deployment Type (Cloud-based, On-premises, Hybrid), By Indication (Diabetes Mellitus, Cardiovascular Diseases, Respiratory Diseases, Chronic Kidney Disease, Oncology, Mental Health, Other Indications), By Technology (Wearables & Connected Devices, IoT & Sensors, AI/ML & Predictive Analytics, Clinical Decision Support, Mobile Apps & SMS Platforms), By End User (Providers, Payers) |

| Country Coverage |

Japan |

Frequently Asked Questions

How big is the Japan Chronic Disease Management Market?

▾ Japan’s Chronic Disease Management market is poised to be valued at USD 1,028.0 million in 2026 and is projected to reach USD 3,298.7 million by 2035, driven by aging population, rising chronic disease burden, and digital healthcare adoption.

What is the CAGR of the Japan Chronic Disease Management Market from 2026 to 2035?

▾ The Japan Chronic Disease Management market is expected to grow at a CAGR of 13.8% from 2026 to 2035, reflecting strong expansion due to increased adoption of remote monitoring, digital therapeutics, and value-based care initiatives.

What factors are driving the growth of the Japan Chronic Disease Management Market?

▾ Key growth drivers include Japan’s rapidly aging population, rising prevalence of diabetes and cardiovascular diseases, government healthcare reforms, expansion of remote patient monitoring, and increasing demand for cost-effective, preventive, and continuous care solutions.

What are the major trends in the Japan Chronic Disease Management Market?

▾ Major trends include the adoption of AI-driven predictive analytics, the expansion of wearable health devices, growth of digital therapeutics, the integration of cloud-based healthcare platforms, and increasing collaboration between healthcare providers, insurers, and technology companies.

Who are the key players in the Japan Chronic Disease Management Market?

▾ Key players include Fujitsu Ltd., NEC Corporation, Omron Healthcare, CureApp, Welby Inc., Philips, Medtronic, ResMed, Takeda Pharmaceutical, and Sony, along with emerging digital health startups and healthcare technology solution providers.

How is the Japan Chronic Disease Management Market segmented?

▾ The Japan Chronic Disease Management market is segmented across offering, including solutions and services; deployment type, comprising cloud-based and hybrid models; indication, covering diabetes, cardiovascular diseases, and chronic kidney disease; technology, such as AI, wearables, and mobile platforms; and end users including providers, payers, and life sciences companies.