What is the Japan Computer Vision Market Size?

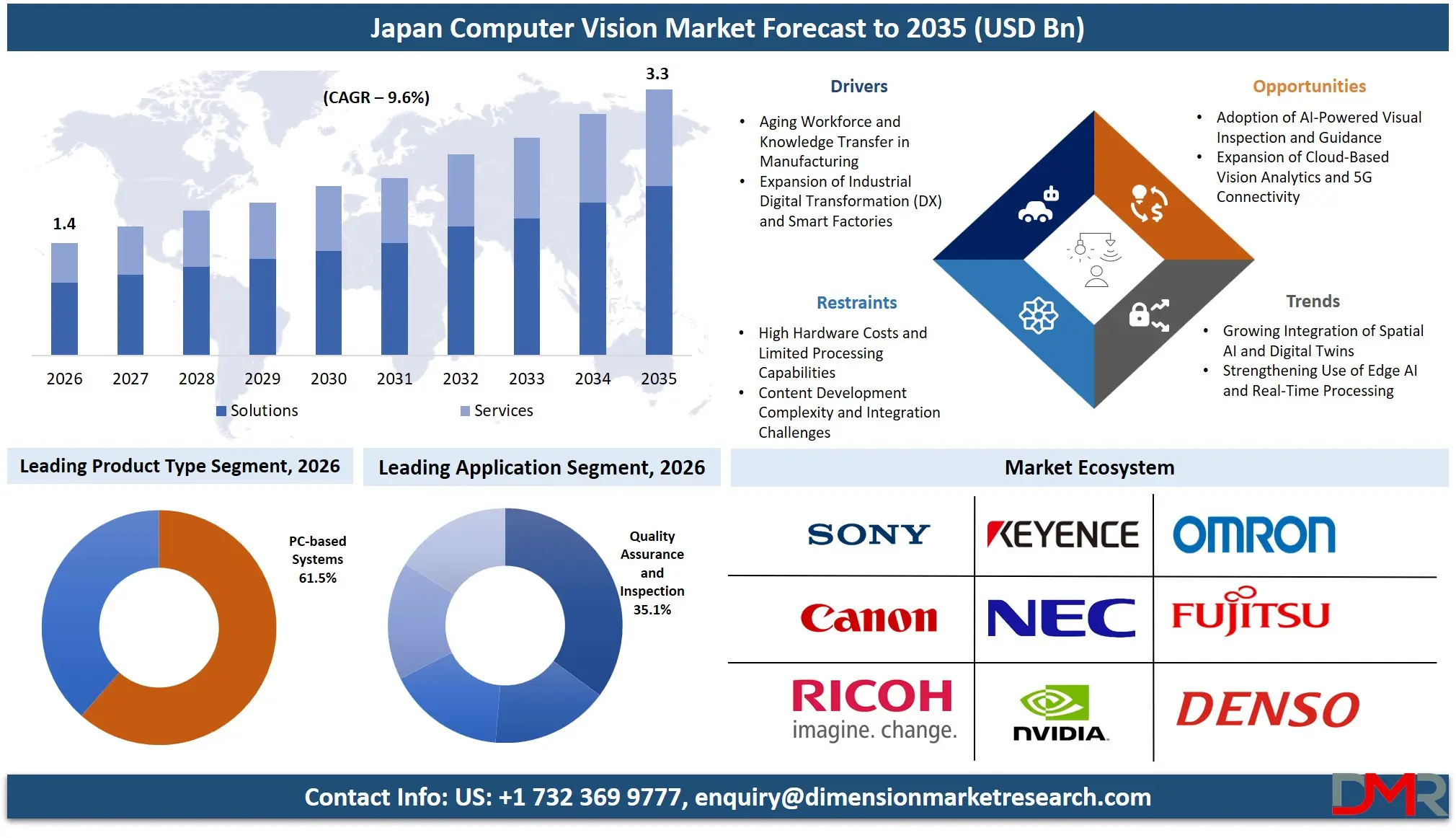

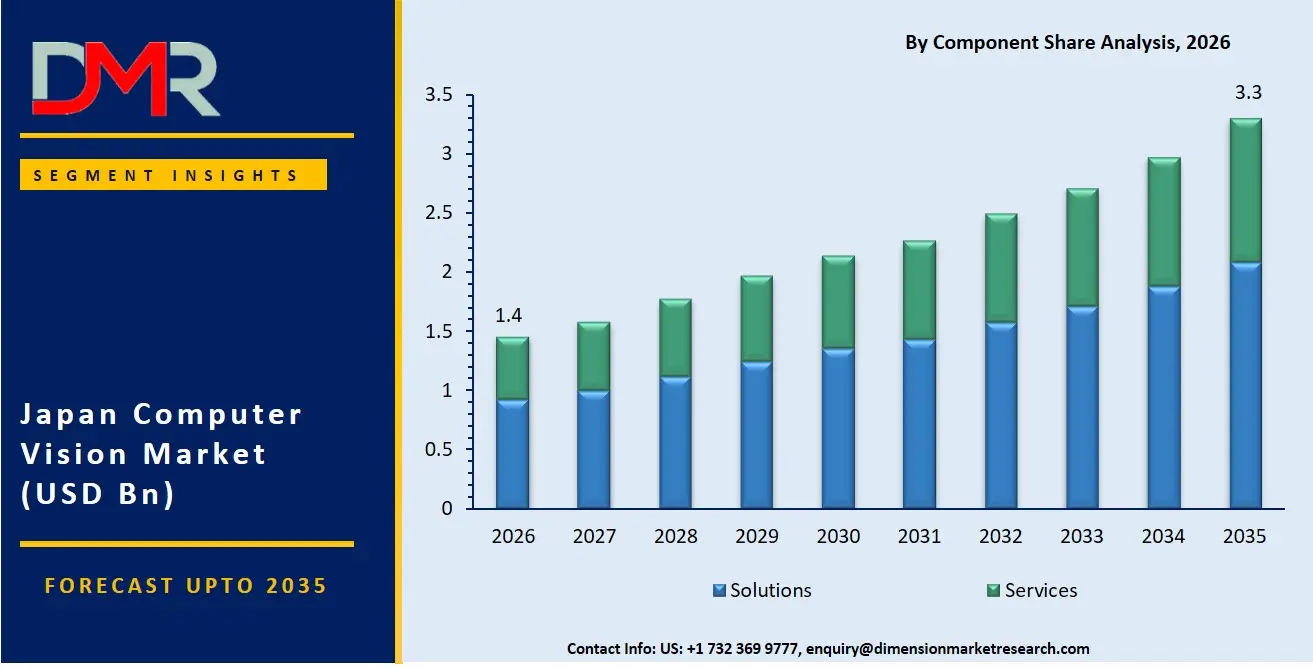

The Japan Computer Vision Market size is expected to reach USD 1.4 billion in 2026 and is likely to grow to USD 3.3 billion by 2035, progressing at a CAGR of 9.6% during the forecast period. The computer vision market has been showing consistent growth due to Japan's rising dependence on AI-driven visual processing solutions that extract meaningful information from digital images and video streams for real-time analysis and automation.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

This includes several solution components, software platforms, and professional services that help enterprises deploy computer vision for commercial and industrial purposes. There has been a rising need for custom vision analytics development owing to the requirements for implementing advanced deep learning algorithms, securing operational continuity in manufacturing, and delivering high-performance real-time object detection systems to industrial customers. Large enterprises have emerged as the largest enterprise size segment for computer vision services, with smart camera-based systems being the most popular product type due to their widespread factory automation penetration, while there has been rapid growth in edge-based vision analytics and cloud-based model training services.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Key Takeaways

- Market Size & Forecast: The Japan Computer Vision market is forecasted to be valued at USD 1.4 billion in 2026, growing incrementally to USD 3.3 billion by 2035, due to the joint efforts of digital transformation deployment on the part of enterprises as well as the adoption of deep learning-powered inspection technologies.

- Growth Rate & Outlook: Japan market is expected to grow at 9.6% CAGR, propelled by the urgent need to mitigate emerging workforce aging vulnerabilities in industrial quality control, alongside increasing challenges in transferring tacit knowledge from retiring skilled inspectors to new employees across manufacturing floors, electronics cleanrooms, and logistics centers.

- Primary Growth Drivers: Major driving factors comprise the transition from traditional manual visual inspection toward modern AI-driven vision systems, the necessity to deploy real-time defect detection for factory automation, as well as the adoption of AI-powered object recognition and 3D mapping for industrial and retail applications.

- Key Market Trends: Major trends encompass the introduction of AI-driven visual inspection through 5G networks, usage of edge-based real-time processing within industrial environments for asset tracking and workflow optimization, and increased focus on compact, high-resolution smart camera systems amidst rising enterprise quality considerations.

- By Component Analysis: The solutions segment is projected to dominate the Japanese computer vision market due to high demand for AI-powered inspection software, deep learning models, and image processing algorithms by enterprise users, with capabilities like real-time defect detection, spatial recognition, and automated visual logging, which offer daily operations, quality control, and real-time performance monitoring activities within digital workflow management.

- By Product Type Analysis: The PC-based Systems segment is projected to hold the largest share of the Japan Computer Vision Market in 2026 at around 61.5%, driven by strong adoption in semiconductor, automotive, and multi-camera industrial inspection applications, while Smart Camera-based Systems continue to grow due to their compact design and ease of deployment in factory inspection and tracking use cases.

- By End-User Industry Analysis: The Manufacturing, Electronics & Semiconductors segment is anticipated to dominate in the Japan Computer Vision Market as Japanese factories adopt systems that are scalable, flexible, and efficient for wafer inspection, component placement verification, and quality assurance, addressing the aging workforce and knowledge retention challenges unique to Japan.

What are Computer Visions?

Computer vision is a field of artificial intelligence that enables machines to interpret and make decisions based on visual data from the world, including images, videos, and real-time camera feeds. In contrast to traditional image processing, computer vision creates value by enabling automated decision-making using deep learning models, while traditional processing relies on rule-based algorithms. Computer vision technologies require convolutional neural networks, object detection algorithms, semantic segmentation, and sensor fusion for aligning visual insights with physical inspection points. The most important parts include smart camera-based systems such as industrial vision sensors and AI cameras, PC-based systems with powerful GPUs for complex vision tasks, and expert services for custom model development, vision system integration, and maintenance.

Use Cases

- Industrial Quality Assurance: Manufacturing companies use AI-powered smart camera systems for real-time defect detection and dimensional measurement, providing instant pass/fail decisions and minimizing costly rework across Japan's precision electronics factories.

- Hospital Surgical Guidance: Hospitals use PC-based vision systems to analyze real-time endoscopic video for tumor localization and vessel navigation, assisting surgeons with AI-enhanced overlays in line with health and safety regulations within Japan.

- Retail Shelf Analytics: Retail stores make use of smart camera-based systems to monitor shelf stock levels, analyze customer traffic patterns, and detect planogram compliance, decreasing out-of-stock incidents and improving sales conversion ratios.

- Automotive Driver Monitoring: Automobile firms use in-cabin vision systems to detect driver drowsiness, distraction, and gaze direction, issuing alerts while keeping drivers' eyes fixed on the road amidst dense traffic on urban highways.

How AI is Transforming the Computer Vision Market?

AI is revolutionizing the computer vision industry through improved object recognition, scene understanding, and predictive analytics capabilities. The computer vision software suite includes AI-based systems that detect product defects, track worker movements, and recognize physical anomalies in order to flag quality issues instantaneously, thereby preventing production discontinuities. In addition, the AI-driven functions of vision platforms help organizations assess operator behavior, determine optimal inspection thresholds, and customize their training modules. AI forms an essential part of quality governance initiatives. Professional services involve intelligent agents that monitor vision session logs and keep model calibration data free of any non-compliant entries while ensuring that all visualizations comply with safety regulations and the stringent quality standards in Japan.

Market Dynamics

Key Drivers in the Japan Computer Vision Market

Aging Workforce and Knowledge Transfer in Manufacturing

Manufacturing industries in Japan are witnessing a severe shortage of skilled visual inspectors owing to the demographic problem and retiring technicians. The issue is tackled using computer vision technology as it offers the ability to capture expert inspection knowledge and provide automated pass/fail decisions to young or unskilled quality control staff. Smart camera systems facilitate real-time defect classification based on models trained on retired experts' historical judgments, enabling on-the-ground personnel involved in inspection processes to operate with high accuracy. Toyota, Hitachi, and Mitsubishi Electric use computer vision technology to preserve inspection knowledge and cut down the time required for inspector training by 40%. It has been seen that AI-assisted visual inspection minimizes errors in highly sensitive electronics production. Since Japanese companies are known for maintaining strict quality standards, such technology is being quickly embraced by many automotive, electronics, and semiconductor industries.

Expansion of Industrial Digital Transformation (DX) and Smart Factories

Computer vision and the creation of smart factories through industrial DX represent one of the major drivers of market growth in the computer vision space in Japan. In today's world, computer vision becomes an integral part of Industry 4.0 systems that allow smart cameras, AI vision servers, and vision workstations to interact with IoT sensors, digital twins, and MES systems to provide real-time defect visualization and process automation. The use of computer vision technology can prove to be advantageous particularly in the context of the need for zero-defect processes and real-time quality control in the factories in Japan. In addition, due to government support through METI in the form of subsidies for DX projects, companies tend to choose vision-based inspection solutions as compared to manual quality management systems.

Restraints in the Japan Computer Vision Market

High Hardware Costs and Limited Processing Capabilities

Japan is one of the highly developed computer vision markets, however, high costs associated with the development and deployment of high-quality AI-powered smart camera systems (costing more than USD 5,000 for each high-end unit) limit SME penetration into the market. Most SMEs find it unprofitable to invest in such high-priced vision devices due to the relatively limited onboard processing power for complex deep learning models as well as high integration complexity. These factors make it hard for computer vision vendors to gain entry into the wide SME sector in Japan, which represents more than 99% of total enterprises in the country. Other devices experience issues with lighting sensitivity and environmental robustness, making them unsuitable for certain industrial conditions.

Content Development Complexity and Integration Challenges

Creation of customized computer vision models tailored to a specific defect detection workflow or application, be it in semiconductor manufacturing, healthcare imaging, or for logistics sorting, involves specific expertise in deep learning, image annotation, and model optimization. Many firms in Japan do not have in-house capabilities for developing vision solutions, thus making them dependent on expensive outsourced help. The integration of vision solutions into existing ERP, MES, or legacy quality systems entails technical complexities and delays. Moreover, there being no standardized vision ecosystem, models trained for one smart camera platform may not run on other devices from different vendors.

Growth Opportunities in the Japan Computer Vision Market

Adoption of AI-Powered Visual Inspection and Guidance

The inspection and guidance process enabled via the application of AI-based computer vision technologies can be considered as a promising growth driver for the Japan computer vision market. The emergence of enterprise-level implementations of intelligent systems enabling the remote visual support of workers by experts in the execution of challenging activities like defect classification and assembly verification with the help of smart cameras or PC-based systems shows the trend towards efficient and cost-effective knowledge transmission. As for Japan, its specific labor market and distribution of industrial facilities makes it even more relevant to implement vision-based remote inspection. Besides, innovations in the field of artificial intelligence and real-time object detection allow achieving error correction and workflow validation autonomously.

Expansion of Cloud-Based Vision Analytics and 5G Connectivity

Cloud-based vision analytics platforms present one of the future areas of opportunities within the computer vision industry in Japan. The modern devices such as smart camera systems, PC-based vision servers, and edge AI cameras have been connected to cloud-based systems capable of delivering real-time model updates, persisting historical defect data, and continuous algorithm retraining. This approach helps to decrease the demand for processing performed by the device, improve model accuracy over time, and enables shared vision intelligence among multiple factory lines. Connection to edge computing devices via Japan's 5G network can provide sub-10 milliseconds of latency for critical industrial operations requiring real-time visual guidance. The ability to integrate smoothly with the current cloud ecosystem is highly valued by Japanese enterprises, making the cloud-based vision ecosystem particularly relevant for industrial users.

Trends in the Japan Computer Vision Market

Growing Integration of Spatial AI and Digital Twins

The introduction of technologies such as spatial AI and digital twin are essential and are some of the key elements behind the growth of the computer vision market in Japan. Companies have been utilizing vision systems in order to synchronize their digital twin information with actual machinery, where, through the smart cameras, the maintenance workers are able to view component status, temperatures, and vibration indicators overlaid on live video feeds. Through simultaneous localization and mapping (SLAM) technology integrated with vision, persistent AI annotations that stick to actual physical locations have helped increase efficiency when dealing with industrial equipment. In Japan, due to advanced manufacturing processes and technology utilization by engineers, the adoption of spatial AI in the enterprise computer vision market has accelerated.

Strengthening Use of Edge AI and Real-Time Processing

A significant trend within the computer vision market in Japan is the growing demand for edge-based vision solutions. Nowadays, companies prefer a solution where AI inference can be performed directly on the camera device without sending data to a central server. With on-device deep learning acceleration, users are able to achieve sub-millisecond defect detection, a function vital when conducting high-speed production line reviews, surgical procedure assistance, and real-time security monitoring. Major players in vision platforms are taking advantage of edge AI technology in order to help their enterprise clients implement real-time visual inspection without incurring network latency or cloud bandwidth costs. The trend is highly dominant within the Japanese computer vision market due to the preference for low-latency, high-reliability operation amongst Japanese industrial enterprises.

Research Scope and Analysis

The Japan Computer Vision Market is segmented by component, product type, application, and end-user industry. The market supports industrial quality control, commercial visual analytics, enterprise inspection training, and public sector visual monitoring across manufacturing, electronics & semiconductors, healthcare, retail, and automotive through cloud-based and on-premise vision deployment models.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Component Analysis

Solutions are expected to lead the Japan Computer Vision Market in 2026 with a projected market share of 63.1% as a result of enterprises' growing preference for high-performance deep learning models, image processing algorithms, and AI-driven analytics. Japanese enterprises have developed a preference for smart camera-based systems and PC-based vision workstations for performing such functions as quality inspection, positioning guidance, and real-time measurement. Services are likely to occupy the second position due to the rising trend in favor of custom vision model development and ongoing integration support, particularly for digital transformation projects in Tokyo, Osaka, and Nagoya.

By Product Type Analysis

PC-based Systems (high-performance GPU servers and workstations) are projected to dominate the Japan Computer Vision Market in 2026, with an estimated share of 61.5%, driven by complex multi-camera applications requiring heavy deep learning inference for semiconductor wafer inspection, medical imaging, and 3D interactive modelling. Smart Camera-based Systems (integrated AI cameras and vision sensors) follow, owing to their all-in-one design, ease of deployment, and low entry cost for assembly line defect detection, automated optical inspection, and enterprise barcode reading. The dominance of PC-based systems is further reinforced by Japan's strong semiconductor and automotive manufacturing base, where high-precision, compute-intensive inspection workflows remain essential. However, smart camera adoption continues to expand steadily as manufacturers seek compact and cost-efficient vision solutions for scalable factory automation deployments.

By Application Analysis

Quality Assurance and Inspection is expected to lead with 35.1% share in 2026, driven by strong demand for zero-defect manufacturing across the automotive, electronics, and semiconductor industries. Enterprises prefer vision-based automated optical inspection for real-time defect detection, dimensional measurement, and surface flaw analysis. Demand is concentrated in major industrial hubs such as Tokyo, Osaka, and Nagoya, where advanced manufacturing supports adoption. Positioning and Guidance follows, supported by logistics centers seeking vision-guided robotics and automated guided vehicles. Measurement and identification are used for barcode reading, OCR, and precise dimensional gauging. Predictive Maintenance leverages thermal and visual anomaly detection. 3D Visualization and Interactive 3D Modelling are primarily for digital twin synchronization and medical surgical planning.

By End-User Industry Analysis

Manufacturing, Electronics & Semiconductors is set to dominate the Japan Computer Vision Market in 2026 with a projected share of 38.0%, thanks to its high deployment penetration, government-backed DX subsidy programs, and the urgent need to address the aging skilled workforce. Computer vision enables real-time wafer inspection, component placement verification, and granular production analytics that do not necessitate additional hardware investment beyond existing smart cameras. Automotive will experience robust growth due to heightened preference for driver monitoring systems, in-line part inspection, and quality control unique to Japan. Healthcare is driven by vision adoption for medical imaging analysis and surgical navigation across major university hospitals. Transportation & Logistics benefits from automated package sorting and barcode reading. Retail & E-commerce leverages shelf analytics and customer behavior tracking. Security & Surveillance grows steadily as urban safety initiatives adopt AI-based facial and anomaly detection.

The Japan Computer Vision Market Report is segmented based on the following:

By Component

By Product Type

- Smart Camera-based Systems

- PC-based Systems

By Application

- Quality Assurance and Inspection

- Positioning and Guidance

- Measurement and Identification

- Predictive Maintenance

- 3D Visualization and Interactive 3D Modelling

By End-User Industry

- Automotive

- Manufacturing, Electronics & Semiconductors

- Healthcare

- Transportation & Logistics

- Retail & E-commerce

- Security & Surveillance

- Others

Competitive Landscape

The dynamics of competition in the Japan Computer Vision marketplace have developed to become increasingly dynamic, with a range of global AI vision platform providers and specialized Japanese computer vision software companies focusing on deep learning, edge inference engines, and real-time object tracking. The essential ingredient for success is found in deep-seated strategic partnerships with industrial manufacturers, semiconductor fabs, and telecom carriers in Japan, which strengthen go-to-market capabilities and enable enterprise vision services to be delivered alongside core hardware. Market consolidation trends are moving ahead, with established Japanese electronics companies partnering with or acquiring specialized AI vision and deep learning startups to enhance their vision device functionality. Proprietary intellectual property rights, particularly AI-based real-time inference engines and cross-platform vision frameworks, hold increasing importance compared to camera hardware pricing and standalone device performance.

Some of the prominent players in the Japan Computer Vision Market are:

- Sony Group Corporation

- Keyence Corporation

- OMRON Corporation

- Canon Inc.

- NEC Corporation

- Fujitsu Limited

- Hitachi, Ltd.

- Panasonic Holdings Corporation

- Ricoh Company, Ltd.

- DENSO CORPORATION

- Preferred Networks, Inc.

- Japan Computer Vision Corp.

- Morpho, Inc.

- Cognex Corporation

- Basler AG

- Teledyne Technologies Incorporated

- Intel Corporation

- NVIDIA Corporation

- MVTec Software GmbH

- SICK AG

- Other Key Players

Recent Developments

- March 2026: Sony Group Corporation announced the release of the IMX908 4K CMOS image sensor for security cameras through its semiconductor business, featuring industry-leading 1.45 μm LOFIC pixels and enhanced high-dynamic-range imaging capabilities. The new sensor is designed to improve image recognition accuracy for AI-powered computer vision applications in surveillance, smart infrastructure, and security systems.

- March 2026: Preferred Networks, Inc. partnered with Internet Initiative Japan Inc. and Japan Advanced Institute of Science and Technology to deploy direct liquid-cooled, high-density AI servers in a modular data center, supporting the development of next-generation AI infrastructure for advanced vision AI, autonomous systems, and large-scale machine learning workloads.

- March 2026: NVIDIA Corporation introduced new Cosmos world models, Isaac simulation frameworks, and Isaac GR00T foundation models to accelerate physical AI and robotics deployments. The technologies enhance machine perception, visual reasoning, and autonomous decision-making capabilities across industrial automation, robotics, and computer vision applications.

- June 2025: Cognex Corporation announced the full launch of OneVision, a cloud-based platform for AI-powered machine vision, designed to help manufacturers build, train, and scale industrial vision applications more efficiently. The platform addresses key barriers to AI adoption in manufacturing by simplifying model development, deployment, and lifecycle management for machine vision systems.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 1.4 Bn |

| Forecast Value (2035) |

USD 3.3 Bn |

| CAGR (2026–2035) |

9.6% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Component, By Product Type, By Application, By End-User Industry |

| Country Coverage |

Japan |

Frequently Asked Questions

How big is the Japan Computer Vision Market?

▾ The Japan Computer Vision Market is poised to be valued at USD 1.4 billion in 2026 and is projected to reach USD 3.3 billion by 2035.

What is the CAGR of the Japan Computer Vision Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 9.6% from 2026 to 2035, supported by industrial digital transformation, 5G-enabled real-time visual inspection, and consistent enterprise replacement cycles.

What factors are driving the growth of the Japan Computer Vision Market?

▾ Growth is driven by the aging workforce and knowledge transfer needs in manufacturing, rising demand for AI-based visual quality control, expansion of smart factory initiatives, and government DX subsidies. Japan's strong industrial base and preference for high-precision technology also support enterprise-driven market expansion.

What are the major trends in the Japan Computer Vision Market?

▾ Key trends include spatial AI with digital twins, edge-based real-time inference, AI-powered visual inspection, and expansion of 5G-connected cloud vision analytics. Enterprises prefer seamless integration across smart camera systems, PC-based vision workstations, and edge AI devices.

Who are the key players in the Japan Computer Vision Market?

▾ Key players include Sony Group Corporation, Keyence Corporation, OMRON Corporation, Canon Inc., NEC Corporation, Fujitsu Limited, Ricoh Company, Ltd., and many more.

How is the Japan Computer Vision Market segmented?

▾ The market is segmented by component, product type, application, and end-user industry.