What is the Japan Distributed Control System Market Size?

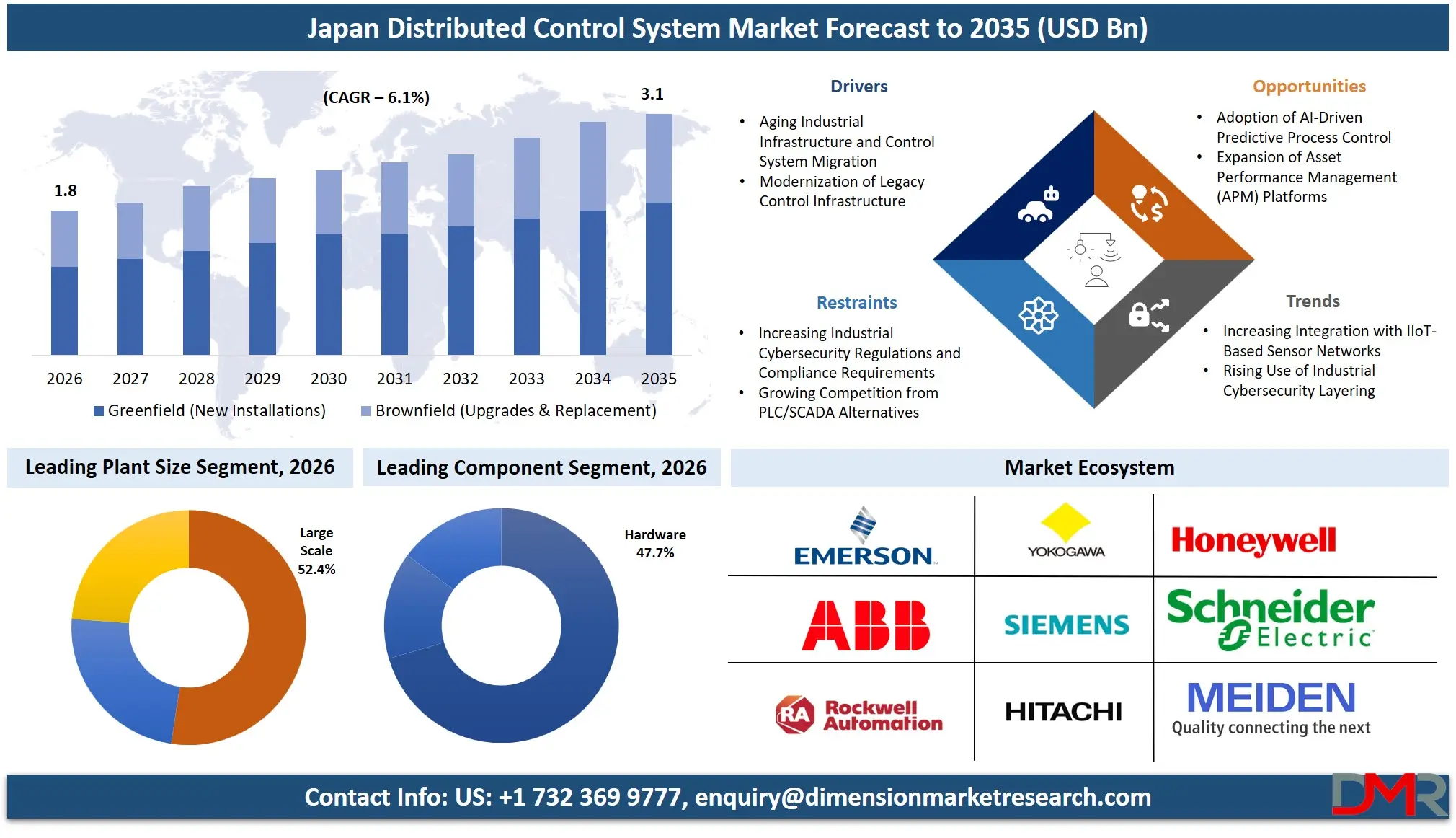

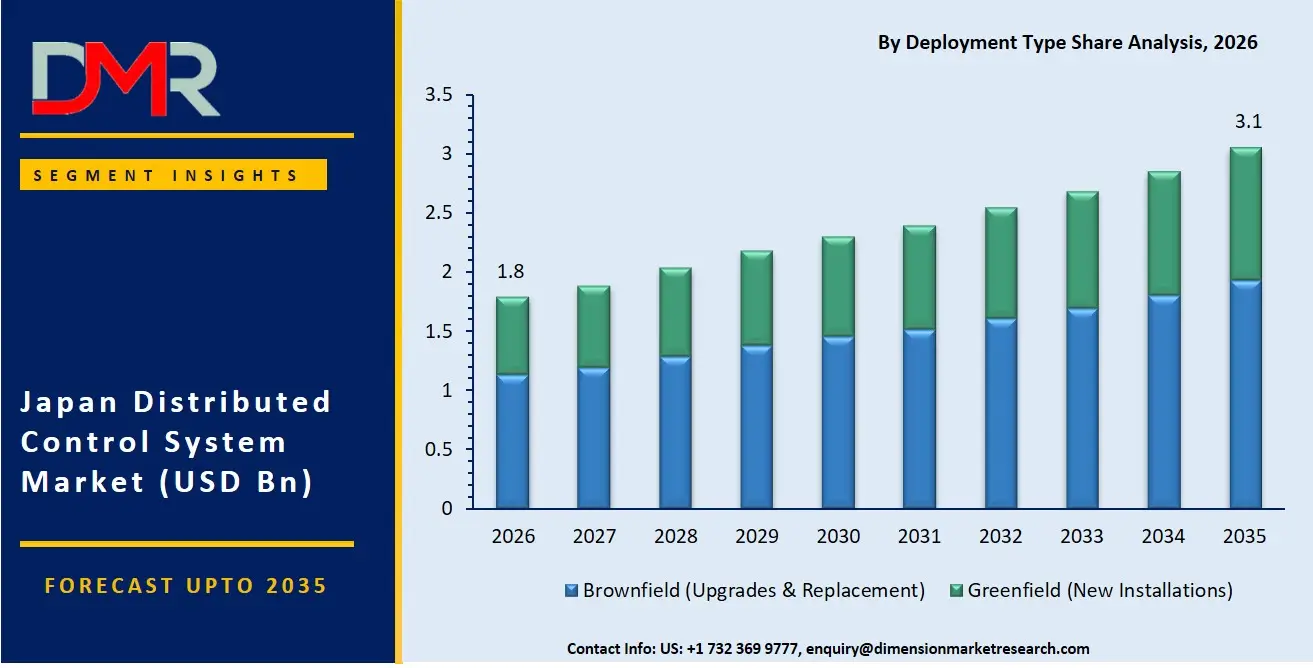

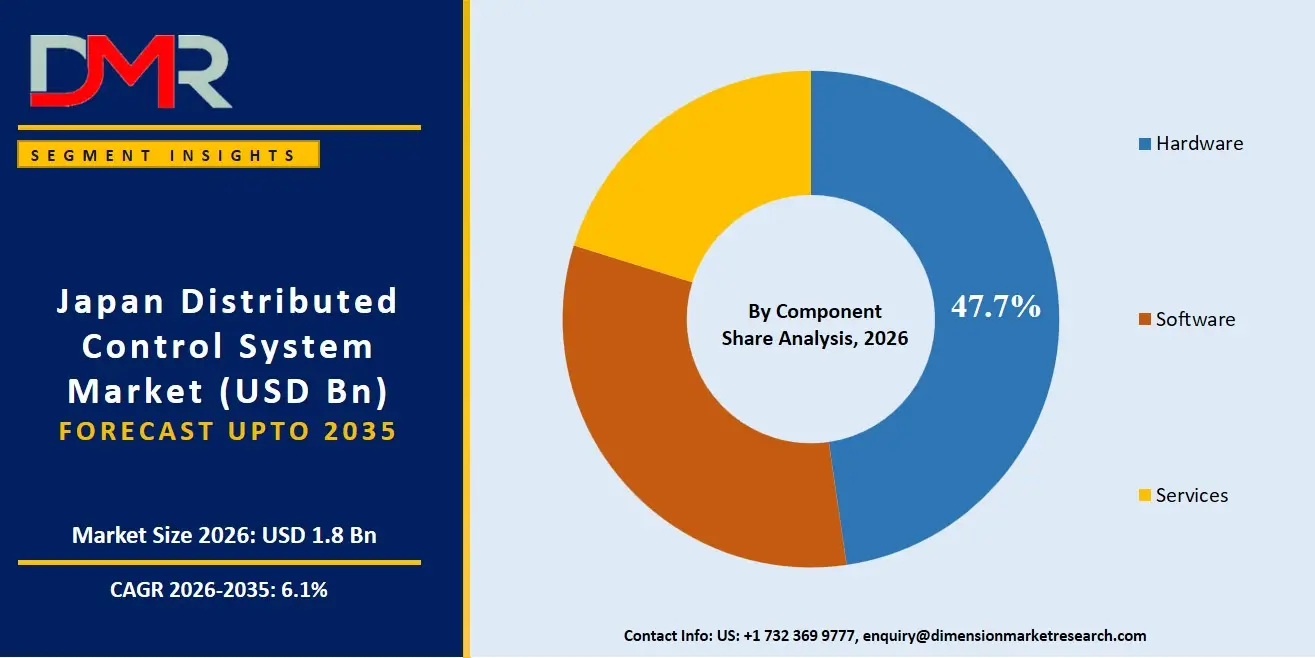

The Japan Distributed Control System (DCS) Market is expected to reach a value of USD 1.8 billion in 2026, and it is further anticipated to reach USD 3.1 billion by 2035, growing at a CAGR of 6.1% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Distributed Control System market has been showing consistent growth due to Japan's rising focus on resilient, decarbonized, and highly automated industrial process control systems for safe, secure, and scalable plant operations. This includes several control platforms and expert services that help plant operators deploy intelligent automation solutions for continuous and batch processing across oil & gas, chemicals, energy & power, pharmaceuticals, and other heavy industries.

There has been a rising need for professional services owing to the requirements for implementing advanced process control (APC), ensuring operational continuity against production disruptions, and delivering high-performance safety instrumented systems to industrial customers. Energy & power plant operators have emerged as a large consumer segment for DCS services, with hardware components being the most popular choice due to their wide availability and proven reliability, while there has been rapid growth in software platforms, APC, and asset performance management services.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Key Takeaways

- Market Size & Forecast: The Japan DCS market is forecasted to be valued at USD 1.8 billion in 2026, growing incrementally to USD 3.1 billion by 2035, due to the joint efforts of industrial automation strategy deployment on the part of enterprises as well as the obligatory deployment of zero-emission and highly reliable process control technologies across Japanese manufacturing and process industries.

- Growth Rate & Outlook: The Japan market is expected to grow at 6.1% CAGR, propelled by the urgent need to modernize aging control infrastructure at Japanese refineries, petrochemical complexes, and thermal power plants, alongside increasing challenges in orchestrating complex continuous and batch production processes with higher efficiency and safety standards.

- Primary Growth Drivers: Major driving factors comprise the transition from legacy pneumatic and analog control systems towards modern intelligent distributed control platforms, the necessity to deploy secure and robust industrial communication networks within process plants, as well as the implementation of plant-wide asset performance management (APM) and APC systems necessitating unique platform and services expertise.

- Key Market Trends: Major trends encompass the introduction of AI-driven predictive process optimization through commercial channels, usage of machine learning within asset performance management for equipment degradation forecasting and preventing unplanned downtime, and increased focus on industrial cybersecurity amidst rising regulatory scrutiny from Japan's METI and NISC.

- By Component Analysis: The hardware segment is projected to dominate the Japan DCS Market due to high demand for scalable controllers, I/O modules, and human-machine interface (HMI) platforms by energy & power and chemical plant operators, with capabilities like real-time process monitoring, fault-tolerant control, and safety system integration, which offer daily operations, plant balancing, and real-time performance monitoring activities within process automation.

- By Deployment Type Analysis: The Brownfield (Upgrades & Replacement) segment is projected to dominate the Japan DCS Market due to aging industrial infrastructure across Japanese refineries, chemical complexes, and power plants dating from the 1970s–1990s, alongside the need to modernize legacy systems with minimal production downtime, especially in major industrial zones of Keihin, Hanshin, and Iyo.

- By System Type Analysis: The Continuous Process Systems segment is anticipated to dominate in the Japan DCS Market as plant operators adopt systems that are scalable, highly available, efficient, provide AI-based process analytics, predictive maintenance integration, operational continuity, and plant-wide control at high resolution across major refineries, petrochemical facilities, and thermal power stations.

What is a Distributed Control System?

A Distributed Control System (DCS) refers to a unique set of control platforms and expertise involved in operating intelligent, digitally-enabled industrial process automation networks. Unlike conventional PLC-based or manual control panels, a DCS pertains to "the how and where" of high-reliability, real-time process management across large-scale continuous and batch operations. It entails having a Control Platform to provide the means through which process variables (temperature, pressure, flow, level) are monitored and controlled for optimal production, and Services to help integrate plant-wide automation, manage process optimization costs, and improve overall equipment effectiveness. As Japanese companies take charge of their decarbonization and operational excellence commitments, it is important to have services that ensure that industrial plants will be operated safely, reliably, and efficiently while maintaining rigorous safety and quality measures.

Use Cases

- Refinery Process Control: Oil & gas companies employ DCS for the installation of distributed automation solutions that include real-time fractionator control, crude unit optimization, and emergency shutdown integration to avoid unsafe conditions and increase operational reliability at refineries in Chiba, Wakayama, and Yamaguchi.

- Thermal & Nuclear Power Plant Operations: Energy operators rely on DCS platforms for deploying boiler-turbine coordination, reactor protection system integration, ensuring stable, zero-unplanned-outage operation, and maintaining compliance with Japan's nuclear regulatory authority (NRA) mandates.

- Pharmaceutical Batch Manufacturing: Pharmaceutical companies incorporate batch recipe management and serialization APIs to push production schedules and quality adherence notifications to central control rooms in real-time, complying with PMDA GMP requirements.

- Water & Wastewater Treatment Automation: Municipal and industrial water treatment facilities leverage advanced process control platforms within a distributed telemetry suite to initiate automated chemical dosing and filter backwash sequences during varying influent conditions.

How AI is Transforming the Distributed Control System Market?

AI is revolutionizing the DCS industry through increased process prediction and predictive maintenance capabilities. The analytics platform suite includes AI-based systems that detect process anomalies and control inefficiencies in order to resolve them instantaneously, thereby preventing any financial losses, safety incidents, and operational damage. In addition, the AI-driven functions of asset performance management services help organizations assess equipment degradation, determine optimal maintenance schedules, and customize their turnaround planning. AI forms an essential part of governance and operational integrity initiatives. Professional services involve intelligent agents that monitor compliance and keep plant maintenance logs free of any non-compliant entries while ensuring that all operations comply with regulations and the stringent industrial cybersecurity protocols in Japan, including guidelines from METI's Cyber Security Management Framework.

Market Dynamics

Key Drivers in the Japan Distributed Control System Market

Aging Industrial Infrastructure and Control System Migration

The average age of DCS installations across Japanese refineries, petrochemical complexes, thermal power plants, and steel mills now exceeds 20–25 years, with many systems dating back to the bubble economy era of the 1980s and early 1990s. These legacy systems face escalating challenges including obsolete spare parts, unsupported operating systems, vendor withdrawal of maintenance contracts, and a shrinking pool of engineers familiar with proprietary legacy platforms. Simultaneously, Japan's aging workforce, often called the "2025 problem" in industrial automation circles, has led to the retirement of veteran plant operators who understood the nuances of older control systems. As a result, plant owners are increasingly compelled to migrate to modern DCS platforms that offer improved reliability, cybersecurity, remote operability, and knowledge preservation through digital workflows. METI and the Ministry of Health, Labour and Welfare have also published guidelines encouraging modernization to prevent safety incidents arising from aging control equipment. This wave of brownfield migration projects, typically executed during scheduled turnarounds, represents a sustained and powerful driver for the Japan DCS market.

Modernization of Legacy Control Infrastructure

The rapid aging of control systems installed during Japan's high-growth era (1970s–1990s) creates high demands in the process industries for migration projects. Companies today use modern DCS solutions to achieve critical goals related to operational continuity, spare parts availability, regulatory compliance, and workforce succession (loss of veteran operators). With the increased complexity of production processes, plant owners have become more interested in adopting an integrated DCS that can handle large I/O counts effectively. In addition, there is a growing need for predictive and prescriptive analytics for plant managers, which increases the adoption rate of modern DCS platforms.

Restraints in the Japan Distributed Control System Market

Increasing Industrial Cybersecurity Regulations and Compliance Requirements

The increasingly stringent industrial cybersecurity regulations and data protection legislation in Japan have brought about difficulties for DCS vendors as well as plant operators. The regulatory bodies, including METI and NISC, are tightening their grip on the control of industrial communication deployments, the acquisition and management of operational data, and encryption measures in order to minimize risks related to cyber intrusions targeting critical infrastructure. Enterprises are expected to adhere to the highly stringent operational requirements, making their deployments more complicated and costly. The violation of such rules subjects a plant operator using DCS to heavy fines, delivery delays, and reputational harm.

Growing Competition from PLC/SCADA Alternatives

Growth in the usage of PLC/SCADA architectures with lower upfront costs is impacting the future growth of traditional DCS within Japan, particularly for smaller or simpler processes. PLC/SCADA systems are preferred over DCS for certain unit-specific applications since they offer lower initial investment and reduced engineering complexity for skid-mounted or standalone processes. Some plant operators have also begun using hybrid control solutions as part of their daily operations, relying less on large-scale DCS for non-critical applications. The use of PLC/SCADA systems also offers simpler maintenance without specialized DCS engineering expertise. Traditional DCS vendors are under growing pressure from competing PLC/SCADA investments.

Growth Opportunities in the Japan Distributed Control System Market

Adoption of AI-Driven Predictive Process Control

There exist many growth opportunities in the DCS market in Japan through the increasing implementation of APC and predictive analytics within DCS platforms. These intelligent solutions allow plant operators to engage in real-time, constraint-based process optimization other than using standard PID control. Higher yield, rapid anomaly detection, and lower total cost of ownership are some features that may be implemented by plant operators in decarbonizing their facilities. Energy and chemical producers based in Japan are starting to consider implementing AI-embedded DCS as an alternative for effective green and efficient plant management. With improved industrial communication infrastructure and improved sensor durability, many industrial organizations will spend significant money on advanced DCS automation and analytics.

Expansion of Asset Performance Management (APM) Platforms

Integration of APM within DCS analytics platforms is bringing about great prospects for DCS providers in Japan. Many plant operators are now using APM technology that automates equipment health monitoring in order to offer predictive maintenance support to plant managers. AI can help organizations understand equipment degradation patterns, customize maintenance schedules, and determine when the best time is for preventive maintenance in order to maximize operational uptime and cost savings. The increasing use of machine learning analytics, intelligent automation, and predictive diagnostics in different sectors such as chemicals, energy & power, and pharmaceuticals is driving demand for innovative APM technology integrated with DCS.

Trends in the Japan Distributed Control System Market

Increasing Integration with IIoT-Based Sensor Networks

Increasingly, Japanese plant operators are adopting Industrial Internet of Things (IIoT)-based sensor networks by integrating DCS services that help improve asset visibility and predictive maintenance. IIoT telemetry allows organizations to easily integrate wireless sensors and device APIs into their asset management systems, operator round solutions, and maintenance processes without having to invest heavily in new control hardware. The advantages associated with IIoT telemetry include real-time asset condition monitoring, vibration analytics, and multi-site equipment health dashboards. Due to the growing adoption of digital transformation approaches in addition to remote plant management processes, the use of IIoT telemetry has been steadily increasing. The adoption of IIoT telemetry as an alternative to more expensive hardwired sensing solutions has continued to gain popularity in Japan.

Rising Use of Industrial Cybersecurity Layering

Multi-layer cybersecurity approaches are being incorporated by Japanese industrial firms in order to protect their DCS environments using a combination of network segmentation, unidirectional gateways, anomaly detection, and secure remote access. Companies are focusing on creating a resilient control system architecture that ensures the integrity and availability of process control through different defense-in-depth layers. DCS solutions continue to be an integral part of these cybersecurity frameworks owing to their critical role in safe operations. Companies from sectors such as energy & power, chemicals, pharmaceuticals, and water treatment have been incorporating DCS into their industrial cybersecurity management programs.

Research Scope and Analysis

The Japan Distributed Control System Market is segmented by component, deployment type, plant size, system type, and end-use industry. The market supports oil & gas refining, chemicals & petrochemicals production, energy & power generation, pharmaceuticals & biotechnology, food & beverages, metals & mining, pulp & paper, water & wastewater treatment, and others across individual plant operators, utility operators, and industrial companies through cloud-connected and on-premise control management solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Component Analysis

Hardware components are expected to lead the Japan DCS Market in 2026 with a projected market share of 47.7% as a result of plant operators' growing preference for scalable control and I/O platforms. Japanese industrial facilities have developed a preference for controllers, I/O modules, power supplies, and HMIs for performing such functions as process variable monitoring, logic execution, alarm management, and safety interlocking. Software solutions are likely to occupy the second place, due to the rising trend in favor of APC, asset performance management, and batch management across production networks. The services segment is expected to grow steadily as a consequence of increased knowledge about system migration, engineering support, and ongoing maintenance requirements, particularly for plant modernization projects in Keihin (Tokyo-Yokohama), Hanshin (Osaka-Kobe), and Iyo (Ehime) industrial belts.

By Deployment Type Analysis

Brownfield (Upgrades & Replacement) is projected to dominate the Japan DCS Market in 2026, with an estimated share of 58.7%, owing to the aging installed base across Japanese refineries, chemical complexes, and thermal power plants built during the post-war economic boom. Plant operators favor brownfield deployment because it minimizes production downtime while delivering reliability improvements and enhanced cybersecurity features. Greenfield (New Installations) follows, driven by new industrial park developments in regions like Hokkaido (semiconductor-related chemicals) and Hiroshima (automotive and materials), as well as greenfield pharmaceutical and LNG receiving terminals requiring state-of-the-art DCS from the outset.

By Plant Size Analysis

Large Scale plants (typically >5,000 I/O points) are set to dominate the Japan DCS Market in 2026 with a projected share of 52.4%, thanks to the concentration of mega-refineries, petrochemical complexes, and utility-scale power generation facilities across Japan's coastal industrial belts. Large facilities require sophisticated DCS capabilities for handling tens of thousands of I/O points, complex interlocking logics, and advanced APC. Medium Scale plants (500–5,000 I/O) will experience robust growth in the coming years because of heightened industrial automation adoption among regional chemical and food manufacturers. Small Scale plants (<500 I/O) hold a smaller share but are growing steadily as specialty chemical plants, small-batch pharmaceutical facilities, and district heating systems modernize their control infrastructure.

By System Type Analysis

Continuous Process Systems are set to dominate the Japan DCS Market in 2026 with a projected share of 65.1%, thanks to their extensive deployment in oil refining, petrochemical production, thermal power generation, LNG receiving terminals, and metals processing, where uninterrupted 24/7 operation and tight regulatory compliance are critical. Batch Process Systems will experience robust growth in the coming years because of heightened preference for flexible, recipe-driven production in pharmaceuticals, specialty chemicals, and food & beverages, where batch traceability, cleaning validation, and compliance with Japan's PMDA and MHLW requirements drive DCS adoption.

By End-Use Industry Analysis

The Energy & Power segment is projected to continue dominating the DCS Market of Japan, with an expected market share of 31.5% in 2026, owing to large-scale installed bases at thermal (coal, LNG, oil) power plants, nuclear facilities, and increasingly at integrated renewable-thermal hybrid plants, as well as heavy reliance on real-time process control, boiler-turbine coordination, and safety system integration. The Chemicals & Petrochemicals segment is also a significant adopter of DCS technologies due to the benefits offered by such systems, including lower production costs, predictable process scheduling, and regulatory compliance with safety mandates from Japan's METI (High Pressure Gas Safety Act, Fire Service Act). Other significant end users include Oil & Gas (upstream, pipeline, and terminal automation), Pharmaceuticals & Biotechnology driven by strict PMDA GMP requirements, Food & Beverages supported by traceability and quality control mandates, Metals & Mining (steel, aluminum, copper), Pulp & Paper (integrated mills), and Water & Wastewater Treatment as part of municipal and industrial infrastructure modernization initiatives.

The Japan Distributed Control System Market Report is segmented based on the following:

By Component

- Hardware

- Software

- Services

By Deployment Type

- Greenfield (New Installations)

- Brownfield (Upgrades & Replacement)

By Plant Size

- Small Scale

- Medium Scale

- Large Scale

By System Type

- Continuous Process Systems

- Batch Process Systems

By End-Use Industry

- Oil & Gas

- Chemicals & Petrochemicals

- Energy & Power

- Pharmaceuticals & Biotechnology

- Food & Beverages

- Metals & Mining

- Pulp & Paper

- Water & Wastewater Treatment

- Others

Competitive Landscape

The dynamics of competition in the Japan DCS marketplace have developed to become increasingly dynamic, with a wide range of global automation majors, specialized Japanese DCS vendors, and system integrators focusing on various process industry verticals. The essential ingredient for success is found in deep-seated strategic partnerships with Japanese engineering, procurement, and construction (EPC) firms and direct relationships with plant operators, which open up high-quality supply chains and allow premium maintenance and migration services to be sold alongside core DCS platforms. Market consolidation trends are moving rapidly ahead, with established players in industrial automation taking on acquisitions of specialized analytics and APC providers to leverage their AI and machine learning capabilities. Proprietary intellectual property rights, with domain-specific process models, safety system know-how, and deep industry application expertise, hold increasing importance compared to just competitive hardware pricing and generic control software. Utility companies such as TEPCO, Kansai Electric, Chubu Electric, and Kyushu Electric are major customers and end-users of DCS, not market competitors in the DCS vendor landscape.

Some of the prominent players in the Japan Distributed Control System Market are:

- Yokogawa Electric Corporation

- Emerson Electric Co.

- Honeywell International Inc.

- ABB Ltd.

- Siemens AG

- Schneider Electric SE

- Rockwell Automation, Inc.

- Hitachi, Ltd.

- Azbil Corporation

- Mitsubishi Electric Corporation

- Toshiba Corporation

- Fuji Electric Co., Ltd.

- Meidensha Corporation

- Mitsubishi Heavy Industries, Ltd.

- Valmet Oyj

- GE Vernova LLC

- Endress+Hauser Group Services AG

- NovaTech Process Solutions, LLC

- Yaskawa Electric Corporation

- Baker Hughes Company

- Other Key Players

Recent Developments

- October 2025: Yokogawa Electric Corporation announced expansion of its OpreX industrial automation portfolio, integrating cloud-based monitoring, AI-driven predictive maintenance, and cybersecurity enhancements to improve lifecycle management of distributed control systems across global process industries.

- October 2025: Siemens AG expanded its strategic partnership with Capgemini to co-develop AI-native solutions for manufacturing operations, product engineering, and industrial automation. The collaboration integrates Siemens' automation and digitalization portfolio with advanced AI capabilities, further strengthening its position in industrial control and automation systems.

- October 2025: Emerson Electric Co. announced expansion of its DeltaV Distributed Control System capabilities with embedded AI-driven operations and edge analytics, enabling autonomous plant control and enhanced predictive maintenance across refining, chemicals, and life sciences industries, strengthening its global process automation leadership.

- September 2025: ABB Ltd. reported advancement of its industrial automation portfolio by integrating AI-assisted engineering for control logic generation into its ABB Ability System 800xA platform, aimed at reducing engineering time and improving operational efficiency in large-scale industrial plants.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 1.8 Bn |

| Forecast Value (2035) |

USD 3.1 Bn |

| CAGR (2026–2035) |

6.1% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Component, By Deployment Type, By Plant Size, By System Type, By End-Use Industry |

| Country Coverage |

Japan |

Frequently Asked Questions

How big is the Japan Distributed Control System Market?

▾ The Japan Distributed Control System Market is poised to be valued at USD 1.8 billion in 2026 and is projected to reach USD 3.1 billion by 2035.

What is the CAGR of the Japan Distributed Control System Market from 2026 to 2035?

▾ The market is projected to grow at a CAGR of around 6.1% from 2026 to 2035, reflecting the maturing nature of the industrial control market and the accelerating complexity of plant-wide, integrated automation strategies.

What factors are driving the growth of the Japan Distributed Control System Market?

▾ Key drivers include the decarbonization imperative for energy efficiency and emissions reduction, the need to modernize legacy control systems installed during the 1970s–1990s, the complexity of managing advanced continuous and batch production processes, and the surge in demand for asset performance management amid evolving industrial safety and cybersecurity regulations.

What are the major trends in the Japan Distributed Control System Market?

▾ Major trends include the integration of AI into predictive process control and asset performance management, the rise of brownfield migration services, the demand for vertical-specific advanced process control solutions, and the focus on secure, cyber-resilient industrial OT practices in compliance with METI guidelines.

Who are the key players in the Japan Distributed Control System Market?

▾ Key players include Yokogawa Electric Corporation, Mitsubishi Electric Corporation, Azbil Corporation, Hitachi, Ltd., Fuji Electric Co., Ltd., Toshiba Energy Systems, alongside global majors such as ABB Ltd., Siemens AG, Emerson Electric Co., and Schneider Electric, and many more.

How is the Japan Distributed Control System Market segmented?

▾ The market is segmented by component, deployment type, plant size, system type, and end-use industry.