Market Overview

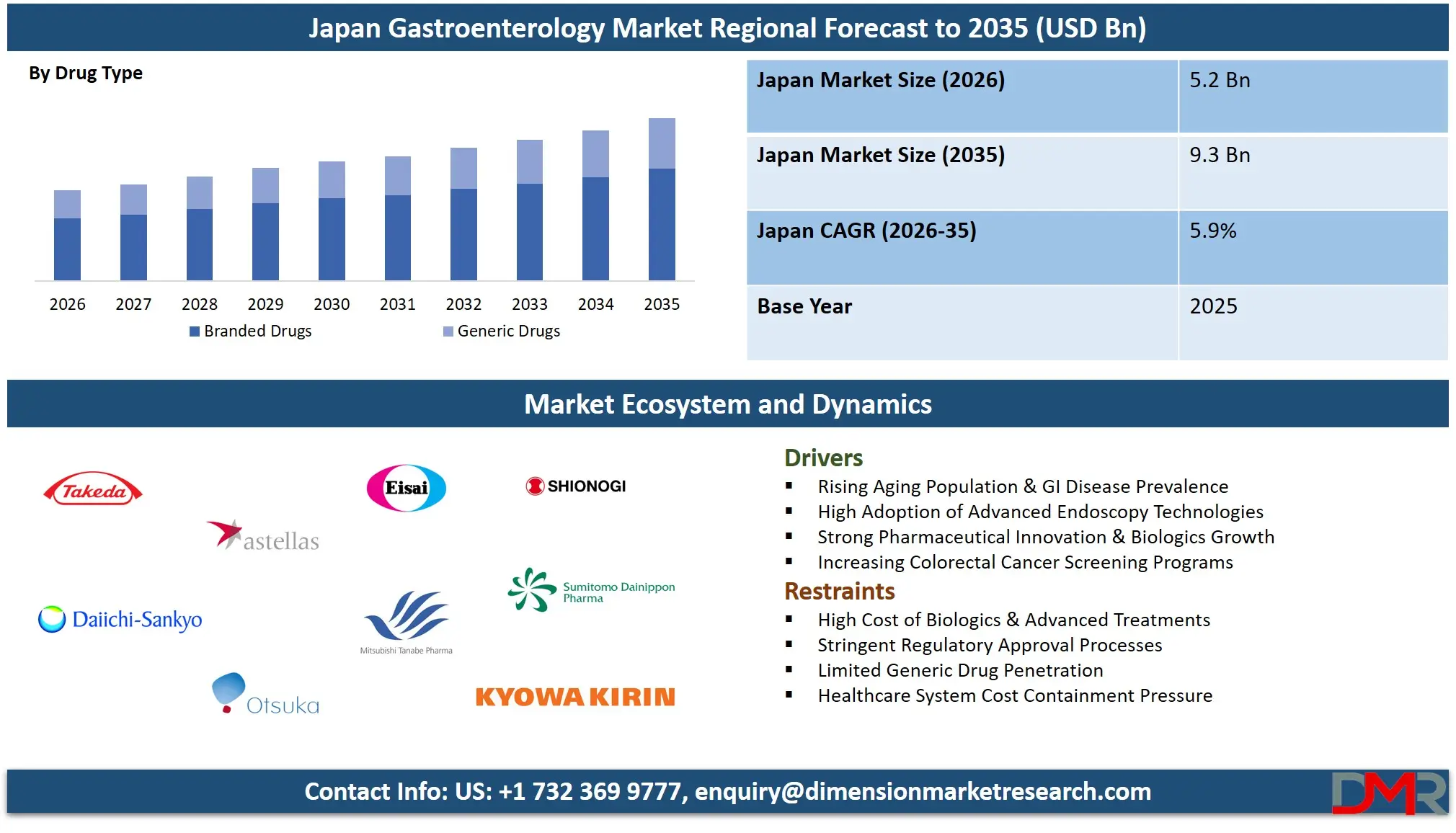

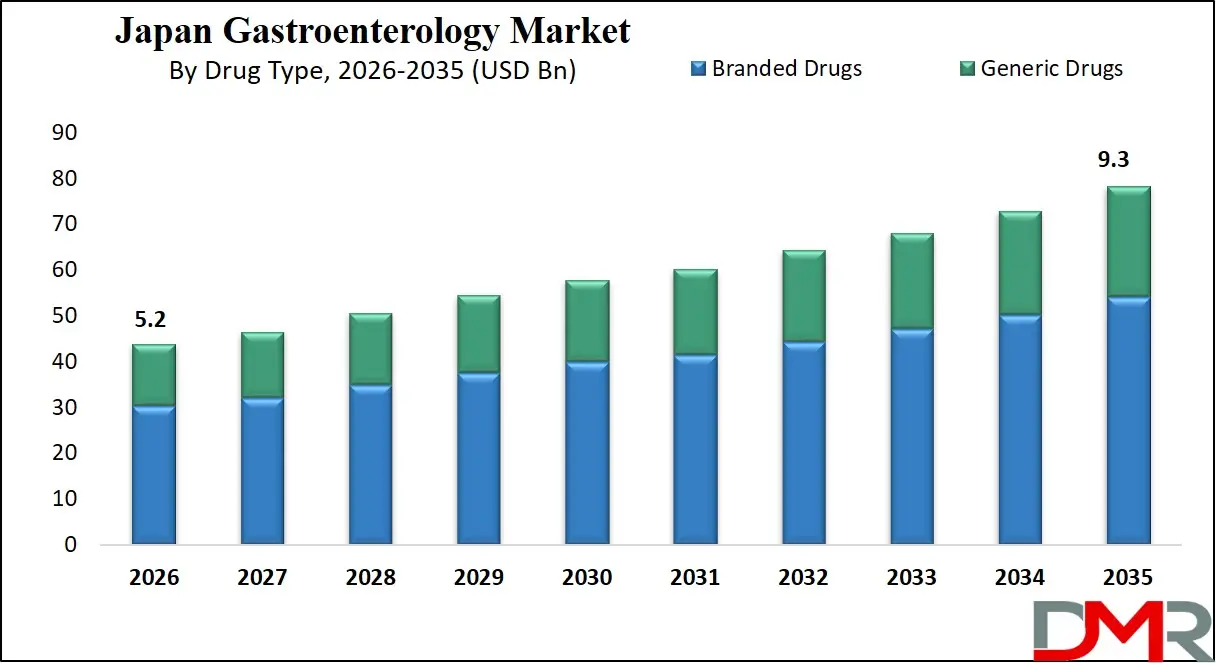

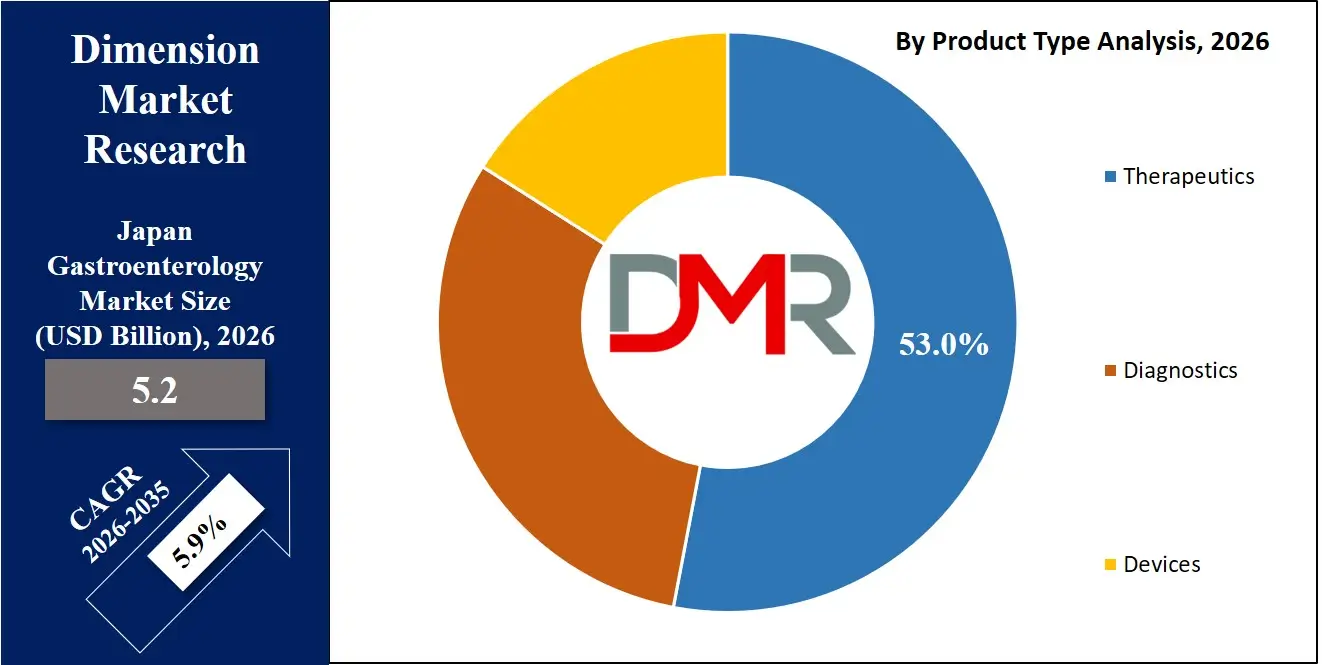

The Japan gastroenterology market is estimated to be valued at USD 5.2 billion in 2026 and is projected to reach USD 9.3 billion by 2035, growing at a CAGR of 5.9%, driven by increasing prevalence of gastrointestinal disorders, rising demand for endoscopic procedures, growth in biologics, and expanding diagnostic technologies.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Gastroenterology is a specialized branch of Medicine focused on the study, diagnosis, and treatment of disorders affecting the digestive system, including the esophagus, stomach, intestines, liver, pancreas, and gallbladder. It encompasses a wide range of conditions such as acid reflux, inflammatory bowel diseases, functional gastrointestinal disorders, liver diseases, and gastrointestinal cancers. The field integrates clinical evaluation with advanced diagnostic techniques like endoscopy, imaging, and laboratory testing to enable early detection and effective disease management. Gastroenterology also involves therapeutic interventions using pharmacological treatments, minimally invasive procedures, and surgical support, with a growing emphasis on personalized medicine, biologics, and preventive care strategies to improve patient outcomes and quality of life.

The Japan gastroenterology market reflects a mature and technologically advanced healthcare landscape characterized by strong demand for gastrointestinal therapeutics, diagnostic procedures, and medical devices. The market is driven by a rapidly aging population, increasing incidence of digestive disorders, and widespread adoption of screening programs for colorectal cancer and other chronic conditions. Japan’s healthcare system emphasizes early diagnosis and precision treatment, leading to high utilization of endoscopic procedures, imaging technologies, and innovative drug therapies. In addition, the presence of leading domestic pharmaceutical companies and continuous research and development activities contribute to the expansion of advanced treatment options across inflammatory bowel disease, gastroesophageal reflux, and liver-related conditions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Furthermore, the market benefits from robust healthcare infrastructure, high healthcare expenditure, and strong regulatory support for innovative therapies, including biologics and targeted treatments. The integration of digital health solutions, artificial intelligence in diagnostics, and improved patient access through hospitals and specialized clinics are enhancing the efficiency of gastrointestinal care delivery. At the same time, evolving lifestyle patterns, dietary changes, and increasing awareness about digestive health are influencing demand dynamics. The Japan gastroenterology market is expected to witness steady growth, supported by technological advancements, rising clinical research activities, and continuous improvements in disease management and treatment accessibility.

Japan Gastroenterology Market: Key Takeaways

- Strong Market Growth Outlook: The market is projected to grow from USD 5.2 billion in 2026 to USD 9.3 billion by 2035, reflecting steady expansion driven by rising GI disease burden.

- Therapeutics Segment Dominance: Therapeutics hold the largest share at 53.0% in 2026, supported by increasing use of biologics, biosimilars, and small molecule drugs.

- High Preference for Oral Medications: Oral drugs dominate with 62.0% market share, indicating strong patient compliance and widespread use in chronic GI disease management.

- Branded Drugs Lead the Market: Branded drugs account for 69.0% share, highlighting Japan’s strong inclination toward innovative and high quality pharmaceutical treatments.

- GERD as a Key Application Area: GERD leads the application segment with 27.0% share, driven by high prevalence and long term treatment demand across the aging population.

Japan Gastroenterology Market: Use Cases

- Colorectal Cancer Screening and Early Diagnosis: High adoption of endoscopy, colonoscopy, and diagnostic imaging supports early detection of gastrointestinal cancers, improving patient outcomes.

- Chronic GI Disease Management: Biologics, small molecules, and GI therapeutics are widely used for managing IBD, IBS, and GERD with a focus on long term care.

- Advanced Endoscopic Procedures: Minimally invasive endoscopic techniques are used for diagnosis and treatment, driving demand for gastroenterology devices and imaging systems.

- Liver Disease and Hepatic Care: Rising liver disorders increase demand for diagnostics, antiviral therapies, and specialized hepatology treatments.

Impact of US-Iran Conflict in the Japan Gastroenterology Market

- Enhanced Diagnostic Accuracy: AI integration with endoscopy and imaging enables real-time detection of polyps, early-stage colorectal cancer, and mucosal lesions, reducing missed diagnoses and improving clinical outcomes.

- Personalized Treatment and Monitoring: Predictive analytics and machine learning support tailored therapy for IBD, liver disorders, and other chronic GI conditions, optimizing biologic and targeted drug use.

- Improved Healthcare Efficiency: AI-powered platforms enhance workflow, telemedicine, and remote monitoring, increasing patient engagement, early screening, and continuity of care across hospitals and clinics.

Japan Gastroenterology Market: Stats & Facts

- Ministry of Health, Labour and Welfare (MHLW) / Government-backed Research

- In 2023, Japan had 316,900 patients with ulcerative colitis

- In 2023, there were 95,700 patients with Crohn’s disease

- IBD cases in Japan increased by ~40% over 8 years (2015–2023)

- Ulcerative colitis cases rose from ~220,000 in 2015 to 316,900 in 2023

- Crohn’s disease cases increased from ~71,000 in 2015 to 95,700 in 2023

- National Cancer Center Japan / e-Stat Government Data

- Digestive organ cancers remain among the most common cancer categories in Japan (2024)

- Colorectal cancer is the most prevalent cancer type in Japan (latest data)

- Over 50,000 deaths annually are attributed to colorectal cancer

- Colorectal cancer ranks among the top causes of cancer mortality in Japan

- Japan reports high incidence rates across esophageal, gastric, liver, and pancreatic cancers

- Survival outcomes are improving due to early detection and screening programs (2024)

- National Database of Health Insurance Claims (Government Data)

- Hospitalization rates for hemorrhagic gastric ulcers declined from 41.5 to 27.9 per 100,000

- Colonic diverticular bleeding increased from 15.1 to 34.0 per 100,000

- Ischemic colitis cases rose from 20.8 to 34.9 per 100,000

- Lower GI bleeding cases have surpassed upper GI bleeding cases since 2017 trends

- GI bleeding remains a major cause of hospital admissions in Japan

- National Cancer & Clinical Research Programs (Japan Government-linked)

- Around 800 GI cancer patients were treated annually in a national center (2023)

- Over 78 Phase I clinical trials for GI oncology were ongoing in 2023

- Around 69 Phase II/III trials were conducted for GI treatments

- Additional 11 investigator-initiated GI clinical trials were active

Japan Gastroenterology Market: Market Dynamic

Driving Factors in the Japan Gastroenterology Market

Rising Burden of Gastrointestinal and Lifestyle-Related Disorders

The increasing prevalence of gastrointestinal diseases such as GERD, inflammatory bowel disease, and colorectal cancer is a major growth driver in Japan. Aging population dynamics, changing dietary patterns, and sedentary lifestyles are contributing to higher incidence rates. This is driving demand for GI therapeutics, proton pump inhibitors, biologics, and advanced diagnostic procedures including endoscopy and imaging technologies.

Strong Adoption of Advanced Diagnostic and Endoscopic Technologies

Japan’s healthcare system is highly advanced, with widespread use of endoscopic procedures, capsule endoscopy, and AI-enabled diagnostic imaging. Hospitals and specialized clinics are investing in minimally invasive technologies to improve early disease detection and treatment efficiency. This supports increased utilization of gastroenterology devices, biopsy tools, and precision diagnostics.

Restraints in the Japan Gastroenterology Market

High Cost of Biologics and Advanced GI Treatments

The cost associated with biologics, targeted therapies, and advanced endoscopic procedures remains high, limiting accessibility for certain patient groups. Despite insurance coverage, pricing pressure and reimbursement constraints impact the widespread adoption of innovative gastrointestinal therapeutics.

Stringent Regulatory and Approval Framework

Japan’s regulatory environment requires rigorous clinical validation and approval processes for new drugs and medical devices. This can delay the commercialization of novel GI therapeutics, biosimilars, and diagnostic technologies, affecting market entry timelines and innovation cycles.

Opportunities in the Japan Gastroenterology Market

Expansion of Biologics and Biosimilars Market

The growing demand for targeted treatment in inflammatory bowel disease and other chronic GI conditions is creating opportunities for biologics and biosimilars. Pharmaceutical companies are focusing on developing cost-effective alternatives, enhancing treatment accessibility and expanding the gastroenterology therapeutics market.

Integration of Digital Health and AI in Gastroenterology

The adoption of artificial intelligence in endoscopy, predictive analytics, and digital diagnostics presents significant growth potential. AI-assisted detection of gastrointestinal abnormalities and telemedicine platforms are improving diagnostic accuracy, patient monitoring, and overall healthcare delivery efficiency.

Trends in the Japan Gastroenterology Market

Shift toward Minimally Invasive and Precision Treatments

There is a growing trend toward minimally invasive procedures such as endoscopic mucosal resection and robotic-assisted interventions. Precision medicine approaches, including targeted biologics and personalized GI therapeutics, are gaining traction in disease management.

Increasing Focus on Preventive Healthcare and Screening Programs

Government-led initiatives and awareness campaigns are promoting early screening for colorectal cancer and other digestive disorders. This trend is boosting demand for diagnostic imaging, lab testing, and routine endoscopic examinations, strengthening the overall gastroenterology market in Japan.

Japan Gastroenterology Market: Research Scope and Analysis

By Product Type Analysis

Therapeutics are expected to dominate the product type segment in the Japan gastroenterology market, accounting for around 53.0% of the total market share in 2026, primarily driven by the rising prevalence of chronic gastrointestinal disorders such as GERD, inflammatory bowel disease, and colorectal cancer. The strong demand for advanced treatment options, including biologics, biosimilars, and small molecule drugs, is supporting segment growth as healthcare providers increasingly focus on long term disease management and symptom control. In addition, Japan’s well established pharmaceutical industry and high adoption of innovative GI therapeutics, including targeted therapies and proton pump inhibitors, are further strengthening this segment, supported by favorable reimbursement frameworks and continuous clinical advancements.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

At the same time, the diagnostics segment plays a crucial role in the overall market, driven by Japan’s strong emphasis on early disease detection and preventive healthcare. High utilization of endoscopic procedures such as colonoscopy and upper GI endoscopy, along with advanced imaging systems and laboratory testing, is contributing to steady growth in this segment. The integration of AI based diagnostic tools and minimally invasive screening techniques is enhancing accuracy and efficiency, particularly in the detection of gastrointestinal cancers and liver diseases. Increasing awareness, national screening programs, and rising demand for precision diagnostics are further supporting the expansion of the diagnostics segment within the Japan gastroenterology market.

By Route of Administration Analysis

Oral medications are anticipated to dominate the route of administration segment in the Japan gastroenterology market, capturing around 62.0% of the total market share in 2026, primarily due to their convenience, cost effectiveness, and high patient compliance in long term treatment. These formulations are widely used for managing common gastrointestinal conditions such as GERD, irritable bowel syndrome, and mild to moderate inflammatory bowel disease, with strong demand for proton pump inhibitors, antacids, and other GI therapeutics. The availability of a broad range of branded and generic oral drugs, along with established prescribing practices and easy accessibility through retail and online pharmacies, further supports the dominance of this segment across the country.

Injectables, on the other hand, represent a significant and growing segment, particularly in the treatment of severe and chronic gastrointestinal disorders such as advanced inflammatory bowel disease and certain gastrointestinal cancers. This segment is driven by the increasing use of biologics and targeted therapies that require parenteral administration for higher efficacy and faster therapeutic response. Hospitals and specialty care centers are the primary settings for injectable treatments, supported by advanced healthcare infrastructure and specialist supervision. Although injectables have lower patient convenience compared to oral medications, their effectiveness in complex cases and rising adoption of innovative biologic therapies are contributing to steady growth within this segment.

By Drug Type Analysis

Branded drugs are anticipated to dominate the drug type segment in the Japan gastroenterology market, capturing around 69.0% of the total market share in 2026, primarily due to the strong presence of innovative pharmaceutical companies and continuous development of advanced GI therapeutics. The preference for branded medications is supported by high trust among healthcare professionals, proven clinical efficacy, and availability of novel biologics and targeted therapies for conditions such as inflammatory bowel disease, colorectal cancer, and liver disorders. In addition, Japan’s regulatory environment and focus on quality standards further encourage the adoption of branded drugs, especially in hospital based treatments and specialty care settings where precision and reliability are critical.

Generic drugs, while holding a comparatively smaller share, are gaining traction due to increasing cost containment measures and government initiatives to promote affordable healthcare. These drugs are widely used for common gastrointestinal conditions such as GERD and mild digestive disorders, offering cost effective alternatives to branded medications. The expansion of generic drug penetration is supported by rising awareness, improved quality perception, and efforts to reduce overall healthcare expenditure. Although generics face competition from established branded therapies, their growing availability and pricing advantage are expected to gradually strengthen their role in the Japan gastroenterology market.

By Application Analysis

Gastroesophageal reflux disease is anticipated to dominate the application segment in the Japan gastroenterology market, capturing around 27.0% of the total market share in 2026, driven by its high prevalence across the adult and aging population. Changing dietary habits, increasing stress levels, and sedentary lifestyles are contributing to a growing patient pool requiring long term management. This has led to strong demand for proton pump inhibitors, antacids, and other GI therapeutics, along with frequent use of diagnostic procedures such as upper GI endoscopy for accurate assessment. The chronic nature of the condition and high recurrence rates further support sustained treatment demand, making GERD a key revenue generating segment.

Inflammatory bowel disease represents a significant and steadily growing segment within the market, supported by increasing diagnosis rates and rising awareness of chronic gastrointestinal conditions. The management of IBD, including Crohn’s disease and ulcerative colitis, relies heavily on advanced therapeutics such as biologics, immunosuppressants, and targeted drug therapies, which are contributing to higher treatment costs and market expansion. In addition, the need for continuous monitoring through endoscopy, imaging, and laboratory testing is driving demand for diagnostic services. Although the patient population is smaller compared to GERD, the complexity of treatment and shift toward personalized medicine are strengthening the importance of the IBD segment in Japan.

By End-User Analysis

Hospitals are anticipated to dominate the end user segment in the Japan gastroenterology market, capturing around 47.0% of the total market share in 2026, primarily due to their comprehensive infrastructure and ability to manage complex gastrointestinal conditions. Hospitals serve as primary centers for advanced endoscopic procedures, surgical interventions, and administration of biologics and injectable therapies, particularly for severe cases such as colorectal cancer, inflammatory bowel disease, and liver disorders. The presence of skilled specialists, access to advanced diagnostic imaging, and availability of integrated treatment pathways further strengthen their dominance. In addition, strong reimbursement systems and high patient preference for hospital based care in Japan contribute to sustained demand within this segment.

Diagnostic centers, while holding a smaller share, play a vital role in the early detection and monitoring of gastrointestinal diseases. These facilities are increasingly equipped with advanced diagnostic technologies such as endoscopy systems, imaging modalities, and laboratory testing services, enabling efficient and accurate disease identification. Growing emphasis on preventive healthcare and routine screening programs, particularly for colorectal cancer and other digestive disorders, is driving patient visits to diagnostic centers. Their cost effectiveness, faster service delivery, and accessibility make them an important component of the gastroenterology care ecosystem, supporting overall market growth in Japan.

The Japan Gastroenterology Market Report is segmented on the basis of the following:

By Product Type

- Therapeutics

- Biologics

- Biosimilars

- Small Molecules

- Diagnostics

- Endoscopic Procedures

- Imaging

- Lab Tests

- Devices

- Biopsy Tools

- Surgical Instruments

By Route of Administration

- Injectables

- Oral Medications

- Others

By Drug Type

- Branded Drugs

- Generic Drugs

By Application

- Inflammatory Bowel Disease (IBD)

- Gastroesophageal Reflux Disease (GERD)

- Irritable Bowel Syndrome (IBS)

- Colorectal Cancer

- Liver Disorders

By End-User

- Hospitals

- Diagnostic Centers

- Retail Pharmacies

- Online Pharmacies

Impact of Artificial Intelligence in the Japan Gastroenterology Market

Artificial intelligence is significantly transforming the Japan gastroenterology market by enhancing the accuracy and efficiency of diagnostic procedures. AI powered systems are increasingly integrated with endoscopy and imaging technologies to assist in the real time detection of abnormalities such as polyps, early stage colorectal cancer, and mucosal lesions. These solutions use advanced algorithms and machine learning to analyze high resolution images, reducing the risk of missed diagnoses and improving clinical outcomes. In Japan, where early detection and preventive healthcare are highly prioritized, the adoption of AI assisted endoscopy is supporting higher screening efficiency, better workflow optimization, and improved decision making for gastroenterologists.

Beyond diagnostics, AI is also influencing treatment planning and patient management across the gastroenterology landscape. Predictive analytics and data driven tools are being used to assess disease progression, personalize treatment strategies, and optimize the use of biologics and targeted therapies for conditions such as inflammatory bowel disease and liver disorders. AI enabled platforms are further supporting telemedicine, remote monitoring, and digital health integration, improving patient engagement and continuity of care. As Japan continues to invest in healthcare innovation and smart technologies, the role of artificial intelligence is expected to expand, driving advancements in precision medicine and overall gastrointestinal care delivery.

Japan Gastroenterology Market: Competitive Landscape

The competitive landscape of the Japan gastroenterology market is moderately fragmented, characterized by the presence of both domestic and global players competing across therapeutics, diagnostics, and medical devices. Companies are primarily focused on innovation, including the development of biologics, advanced endoscopic systems, and AI enabled diagnostic solutions to strengthen their market position.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Strategic initiatives such as product launches, regulatory approvals, research and development investments, and expansion of distribution networks are commonly adopted to gain a competitive edge. Additionally, the market is witnessing increasing emphasis on minimally invasive technologies, precision medicine, and preventive healthcare solutions, while strong regulatory standards and high quality requirements further intensify competition and drive continuous technological advancement.

Some of the prominent players in the Japan Gastroenterology Market are:

- Takeda Pharmaceutical Company

- Astellas Pharma

- Daiichi Sankyo Company

- Otsuka Pharmaceutical

- Eisai Co., Ltd.

- Mitsubishi Tanabe Pharma

- Shionogi & Co., Ltd.

- Kyowa Kirin

- Sumitomo Pharma

- Ono Pharmaceutical

- Zeria Pharmaceutical

- Chugai Pharmaceutical

- EA Pharma

- Asahi Kasei Pharma

- Alfresa Pharma

- Hisamitsu Pharmaceutical

- Santen Pharmaceutical

- Nippon Kayaku

- Meiji Seika Pharma

- Kissei Pharmaceutical

- Other Key Players

Recent Developments in the Japan Gastroenterology Market

- March 2026: Everest Medicines announced the commercial launch of VELSIPITY for ulcerative colitis, expanding access to advanced gastroenterology therapeutics in Asia.

- January 2026: RaQualia Pharma completed its merger agreement with TMRC, strengthening its pharmaceutical pipeline and R&D capabilities in specialty therapeutic areas including gastrointestinal disorders.

- January 2025: Johnson and Johnson announced a major acquisition of Intra Cellular Therapies to expand its specialty drug portfolio and innovation capabilities.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 5.2 Bn |

| Forecast Value (2035) |

USD 9.3 Bn |

| CAGR (2026–2035) |

5.9% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product Type (Therapeutics, Diagnostics, Devices), By Route of Administration (Injectables, Oral Medications, Others), By Drug Type (Branded Drugs, Generic Drugs), By Application (Inflammatory Bowel Disease, Gastroesophageal Reflux Disease, Irritable Bowel Syndrome, Colorectal Cancer, Liver Disorders), By End-User (Hospitals, Diagnostic Centers, Retail Pharmacies, Online Pharmacies) |

| Country Coverage |

Japan |

| Prominent Players |

Takeda Pharmaceutical Company, Astellas Pharma, Daiichi Sankyo Company, Otsuka Pharmaceutical, Eisai Co., Ltd., Mitsubishi Tanabe Pharma, Shionogi & Co., Ltd., Kyowa Kirin, Sumitomo Pharma, Ono Pharmaceutical, Zeria Pharmaceutical, Chugai Pharmaceutical, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Japan Gastroenterology Market?

▾ The Japan Gastroenterology Market size is estimated to have a value of USD 5.2 billion in 2026 and is expected to reach USD 9.3 billion by the end of 2035.

What is the growth rate in the Japan Gastroenterology Market in 2026?

▾ The market is growing at a CAGR of 5.9% over the forecasted period of 2026.

Who are the key players in the Japan Gastroenterology Market?

▾ Some of the major key players in the Japan Gastroenterology Market are Takeda Pharmaceutical Company, Astellas Pharma, Daiichi Sankyo Company, Otsuka Pharmaceutical, Eisai Co., Ltd., Mitsubishi Tanabe Pharma, Shionogi & Co., Ltd., Kyowa Kirin, Sumitomo Pharma, Ono Pharmaceutical, Zeria Pharmaceutical, Chugai Pharmaceutical, and many others.