Market Overview

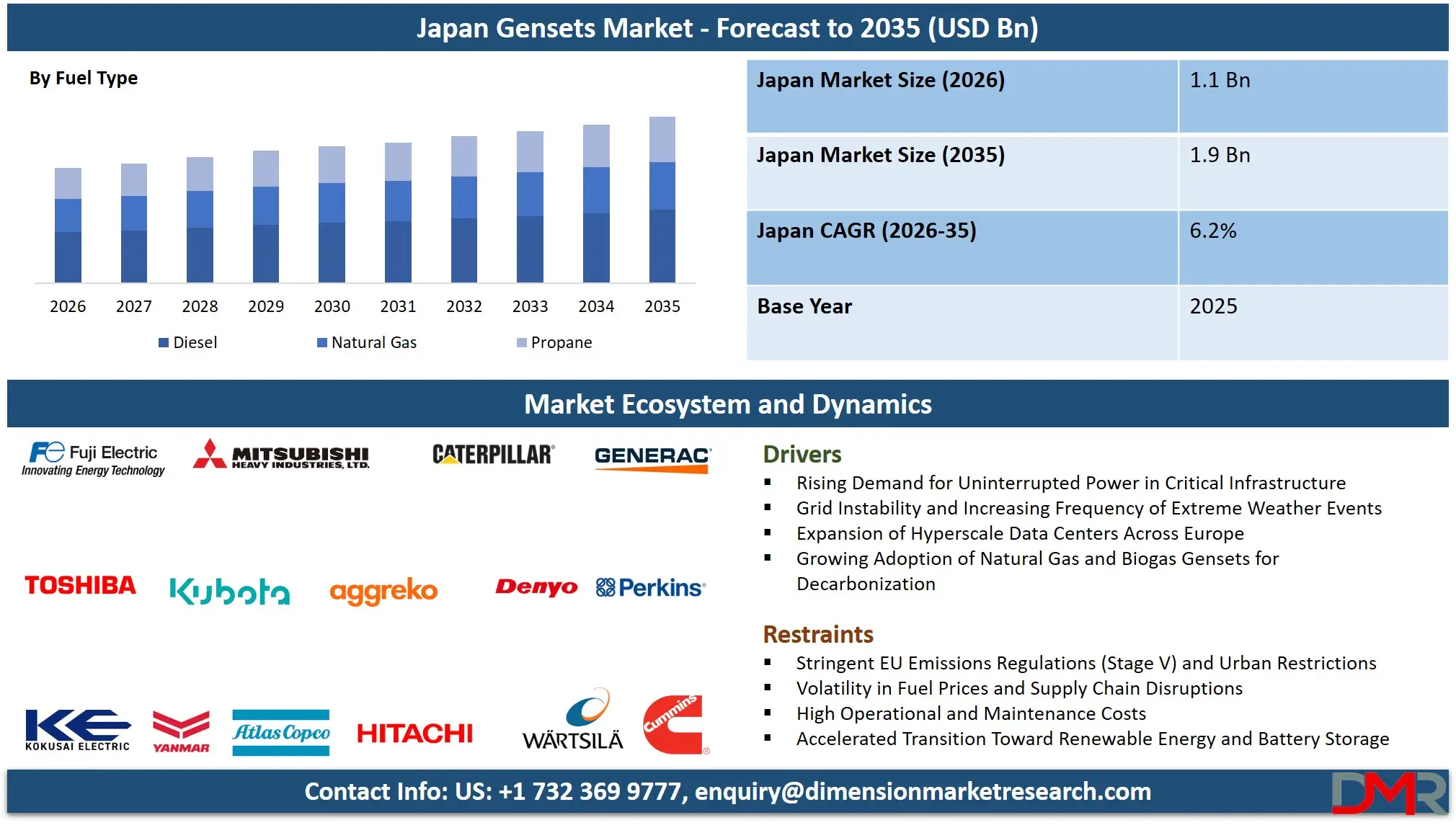

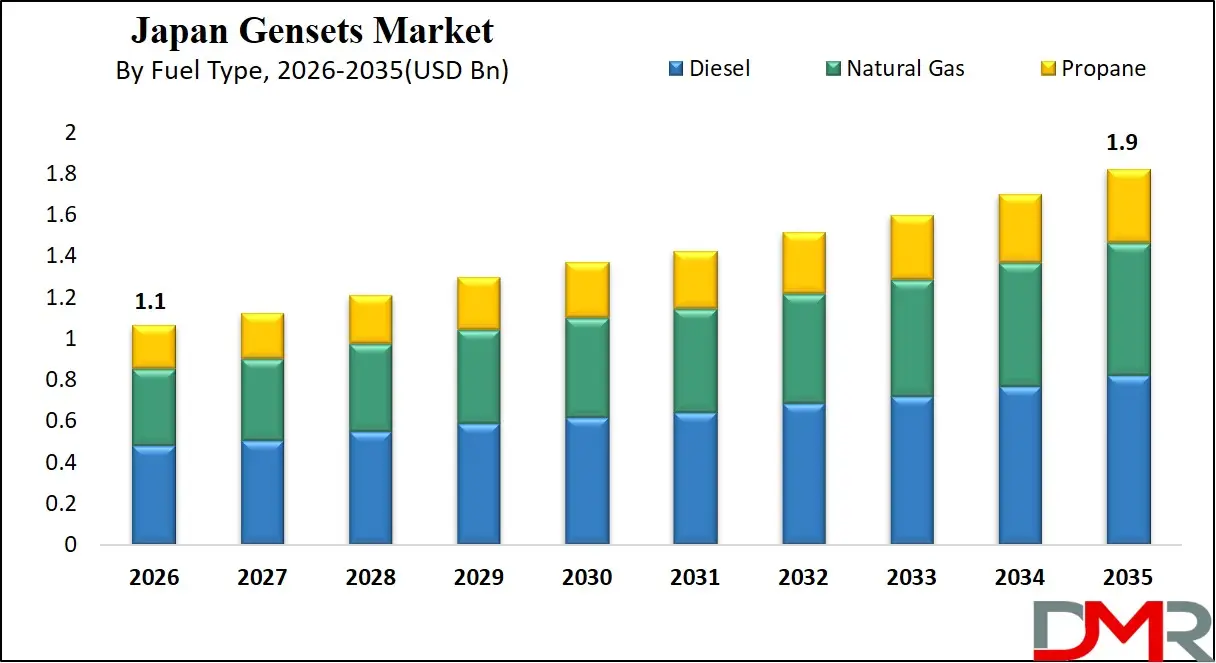

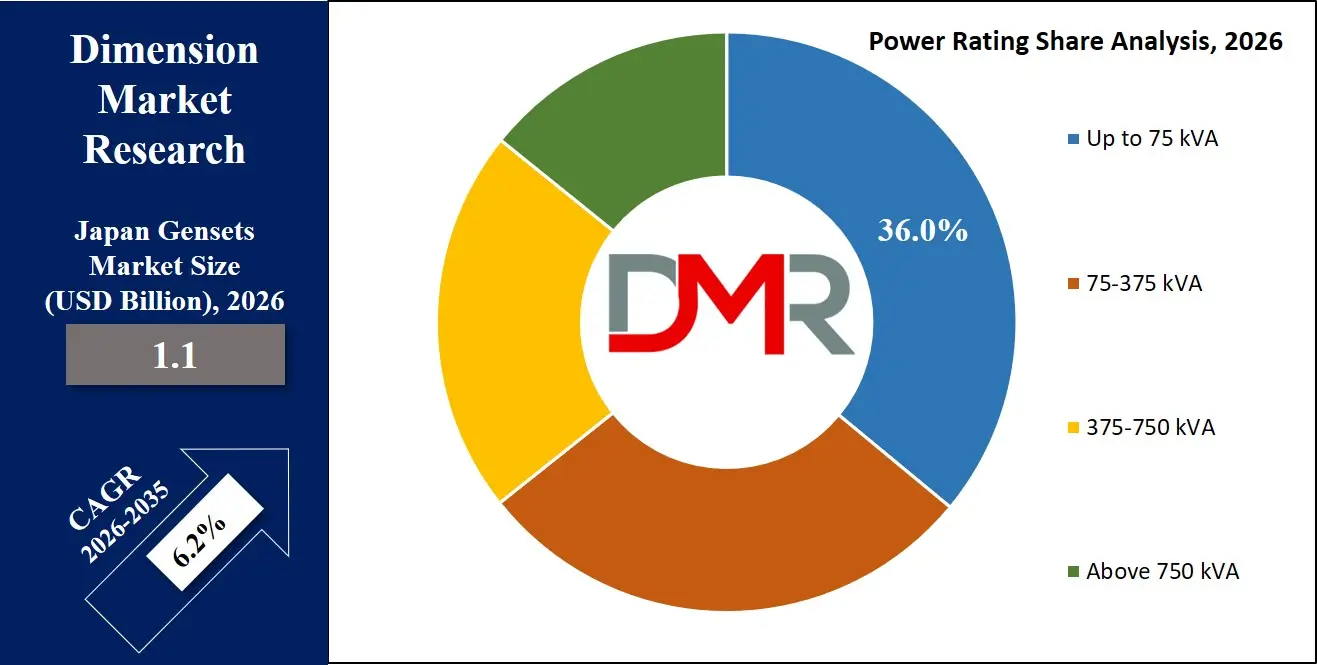

The Japan gensets market is projected to reach USD 1.1 billion in 2026 and is anticipated to grow to USD 1.9 billion by 2035, at a CAGR of 6.2% for the forecasted period reflecting sustained growth driven by increasing electricity demand, aging grid infrastructure, and the rising need for reliable backup power solutions across critical sectors.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Japan Gensets Market is expected to witness stable and technology-driven growth through 2035, supported by the country’s unique energy landscape, high exposure to natural disasters, and strong emphasis on reliability and precision engineering. Unlike regions where genset demand is primarily driven by inadequate grid infrastructure, Japan represents a highly developed electricity market where gensets are deployed as critical resilience assets within a sophisticated and tightly managed energy system.

Japan’s vulnerability to earthquakes, tsunamis, and typhoons has significantly shaped its approach to energy security. Power disruptions, even if temporary, can have widespread economic and social consequences in densely populated urban centers such as Tokyo, Osaka, and Yokohama. As a result, gensets are deeply integrated into disaster preparedness strategies across residential complexes, commercial buildings, public infrastructure, and industrial facilities. Backup power systems are considered essential rather than optional, especially in critical sectors such as healthcare, emergency services, and telecommunications.

The country’s energy mix has undergone notable changes over the past decade, with increased diversification across renewable energy, liquefied natural gas, and other alternative sources. This transition has introduced both opportunities and challenges. While renewable energy adoption is increasing, the intermittent nature of solar and wind power requires reliable backup solutions. Gensets, particularly those powered by natural gas and hybrid configurations, are increasingly being utilized to stabilize power supply and support grid flexibility.

Japan is also recognized globally for its leadership in advanced technologies, and this extends to the genset market. Manufacturers in the country prioritize compact design, energy efficiency, low noise levels, and high reliability. These features are particularly important in urban environments where space constraints and environmental considerations are significant. As a result, Japan has seen strong demand for small to mid-capacity gensets that can deliver efficient performance without compromising on environmental standards.

Another distinguishing factor is Japan’s commitment to hydrogen as a future energy source. The country is actively investing in hydrogen infrastructure and fuel cell technologies, which is influencing the development of next-generation gensets. Hydrogen-powered and dual-fuel systems are being explored as viable alternatives to conventional diesel and gas gensets, aligning with Japan’s long-term decarbonization objectives.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Industrial demand remains a key pillar of the market. Japan’s manufacturing sector, known for its precision and automation, relies heavily on uninterrupted power supply to maintain production efficiency. Even minor power fluctuations can disrupt operations and lead to significant financial losses. Consequently, gensets are widely deployed as standby systems in factories, ensuring continuity and protecting sensitive equipment.

The expansion of digital infrastructure is another important driver. With the increasing adoption of cloud computing, artificial intelligence, and data-driven services, Japan is witnessing steady growth in data center capacity. These facilities require highly reliable backup power systems, creating demand for advanced gensets with high operational efficiency and redundancy capabilities.

In addition, Japan’s aging infrastructure presents challenges for the power grid, particularly in rural and remote areas. This has led to increased adoption of gensets for both backup and primary power applications. Government initiatives aimed at enhancing infrastructure resilience and disaster preparedness further support market growth.

Japan Gensets Market: Key Takeaways

- Steady Japan Market Growth Outlook: The Japan Gensets Market is expected to be valued at USD 1.1 billion in 2026 and is projected to reach USD 1.9 billion by 2035, showcasing steady expansion supported by rising power demand and grid unreliability.

- Moderate CAGR Driven by Industrialization: The market is expected to grow at a CAGR of 6.2% from 2026 to 2035, fueled by increasing infrastructure projects, urbanization, and a growing focus on energy security across industries.

- Diesel Fuel Dominance: Diesel gensets projected to remain dominant in Japan due to unmatched reliability, high power output, and widespread fuel availability, especially for critical infrastructure. However, stricter emission norms are accelerating innovation in cleaner diesel, bi-fuel, and hybrid-compatible technologies.

- Mid-Range Power Leadership: Mid-range gensets up to 75 kVA lead the market, driven by demand from commercial buildings and urban infrastructure. Strict building regulations, compact design needs, and integration with energy management systems further strengthen this segment’s dominance.

- Standby Application Supremacy: Standby power applications dominate Japan’s gensets market due to disaster preparedness requirements. Critical sectors like healthcare, transport, telecom, and finance rely heavily on gensets to ensure uninterrupted operations during frequent natural disasters and grid disruptions.

- Diverse End-User Demand: Manufacturing, healthcare, telecom, and data centers drive genset demand in Japan, each requiring reliable backup power. Rapid digitalization, aging population, and semiconductor growth further expand demand, making data centers the fastest-growing end-user segment.

Impact of Iran Conflict on Japan Gensets Market

- Heightened Concerns Over Energy Supply Stability: Japan's heavy dependence on imported energy makes it highly vulnerable to geopolitical tensions in the Middle East, driving increased investment in backup power systems to ensure energy security and business continuity.

- Increase in Fuel Import Costs: Rising global fuel prices resulting from the Iran conflict directly elevate operational costs for diesel gensets, prompting Japanese end-users to prioritize fuel-efficient models and explore alternative fuel technologies.

- Acceleration of Energy Diversification Efforts: The conflict reinforces Japan's urgency to reduce external energy dependence, accelerating government and private sector investments in renewable energy, hydrogen, and natural gas genset alternatives.

Japan Gensets Market: Use Cases

- Emergency Backup in Urban Infrastructure: Gensets are installed in residential towers, office buildings, and commercial complexes across Japanese cities to provide seamless emergency power during grid outages and natural disasters.

- Disaster Response and Recovery Operations: Portable gensets serve as critical assets for emergency services, powering evacuation centers, medical facilities, and communication networks during earthquakes, typhoons, and other natural calamities.

- Industrial Standby Applications: Manufacturing facilities across Japan's automotive, electronics, and pharmaceutical sectors deploy gensets to prevent costly production stoppages and protect sensitive automated equipment from power disruptions.

- Power Supply for Remote and Island Regions: Gensets provide essential primary and backup power for Japan's numerous remote islands and mountainous communities where grid infrastructure is limited or vulnerable to weather-related disruptions.

- Data Center Backup Systems: High-reliability gensets with extended runtime capabilities form the final layer of defense for Japan's expanding data center infrastructure, ensuring uninterrupted digital services.

Japan Gensets Market: Stats & Facts

Ministry of Economy, Trade and Industry (METI) / Government of Japan

- Japan’s total electricity generation reached about 1,003 TWh in 2023.

- The country generated around 1,008 TWh of electricity in 2022.

- Renewable energy accounted for 22.7% of electricity generation in 2022.

- Japan targets 36%–38% renewable energy share by 2030.

- The government aims for 40%–50% renewable electricity share by 2040.

- Nuclear energy is targeted to contribute 20%–22% of electricity by 2030.

- Japan plans to increase electricity demand to 1.35–1.5 trillion kWh by 2050.

- Electricity demand is expected to grow by 35%–50% by 2050 due to AI and semiconductor industries.

World Nuclear Association / Energy Agencies

- Japan imports around 90% of its total energy requirements.

- Natural gas accounts for about 33% of electricity generation (≈331 TWh).

- Coal contributes around 28% of electricity generation (≈284 TWh).

- Solar power contributes approximately 10% of electricity generation.

- Hydropower accounts for around 8% of electricity generation.

- Nuclear contributes around 8% of electricity generation.

- Wind power contributes about 1% of electricity generation.

- Bioenergy (biofuels and waste) contributes around 6% of electricity generation.

Japan Meteorological Agency (JMA) / Cabinet Office Disaster Management

- Japan experiences over 1,500 earthquakes annually, increasing demand for backup power systems.

- Power outages impacted infrastructure in around 70% of major disasters between 2018–2023.

Tokyo Electric Power Company (TEPCO) / Power Utilities

- Japan records approximately 0.06 power outages per customer annually, among the lowest globally.

- Average outage duration is around 6 minutes per year.

- Power distribution losses are about 4.2%.

- Peak electricity demand reaches approximately 160 million kW.

Japan External Trade Organization (JETRO) / Government-backed Insights

- Renewable energy usage in data centers increased from 14% in 2020 to over 28% in 2023.

- The government targets around 36% renewable usage in data centers by 2025.

Japan Gensets Market: Market Dynamic

Driving Factors in the Japan Gensets Market

High Exposure to Natural Disasters

Japan experiences approximately 1,500 earthquakes annually, along with regular typhoons, tsunamis, and volcanic activity, creating an unwavering demand for reliable backup power systems across all sectors. The 2011 Great East Japan Earthquake fundamentally reshaped national attitudes toward energy resilience, establishing gensets as essential infrastructure rather than optional equipment. Government regulations mandate emergency power systems in hospitals, schools, public buildings, and large commercial facilities. Residential adoption has also grown significantly, with homeowners investing in portable and standby gensets for family safety. This constant threat environment ensures sustained market demand regardless of broader economic conditions.

Advanced Industrial and Technological Base

Japan's position as a global leader in manufacturing, electronics, automotive production, and precision engineering creates sophisticated demand for high-performance gensets capable of protecting sensitive automated equipment and maintaining just-in-time production schedules. The country's extensive industrial parks, semiconductor fabrication plants, pharmaceutical facilities, and research institutions require backup power systems with rapid response times, precise voltage regulation, and seamless integration with existing electrical infrastructure. This technologically sophisticated user base drives continuous innovation in genset design, emissions control, and digital monitoring capabilities.

Restraints in the Japan Gensets Market

High Cost of Advanced Systems

Technologically advanced gensets equipped with Stage V-compliant engines, advanced emissions control systems, noise reduction technologies, and sophisticated remote monitoring capabilities command significant price premiums that limit adoption in price-sensitive segments. Small businesses, residential users, and agricultural operations often face budget constraints that make comprehensive backup power solutions financially challenging. The upfront capital expenditure required for high-quality Japanese-made units can be substantially higher than lower-cost imports, creating market segmentation where cost-conscious buyers may compromise on features or reliability.

Dependence on Imported Fuels

Japan imports approximately 90% of its energy requirements, including virtually all crude oil and natural gas used for genset fuel, creating inherent vulnerability to global energy market fluctuations and geopolitical tensions. The Iran conflict, Middle East instability, and supply chain disruptions directly impact diesel and natural gas prices, affecting both operational costs for end-users and the economic viability of extended genset runtime during prolonged outages. This dependence also raises national security considerations that influence energy policy and encourage alternative fuel development.

Opportunities in the Japan Gensets Market

Development of Hydrogen-Powered Gensets

Japan's national hydrogen strategy, backed by substantial government investment and corporate commitment from companies like Yanmar, Kawasaki, and Mitsubishi, positions the country as a global leader in hydrogen combustion and fuel cell technologies for power generation. The government has established ambitious hydrogen adoption targets ahead of the 2030 and 2050 decarbonization timelines, creating favorable policy environments and funding mechanisms for demonstration projects. Hydrogen gensets offer zero-emission operation while maintaining the rapid response characteristics essential for backup applications, presenting significant growth potential as infrastructure develops.

Integration with Smart Energy Systems

Japan's sophisticated grid infrastructure and widespread adoption of smart building technologies enable seamless integration of gensets with renewable energy systems, battery storage, and intelligent energy management platforms. This integration creates opportunities for advanced microgrid solutions that optimize power sources based on real-time conditions, cost considerations, and environmental priorities. Urban development projects increasingly incorporate hybrid energy systems where gensets work in concert with solar panels and storage to provide resilience while minimizing environmental impact.

Trends in the Japan Gensets Market

Shift Toward Silent and Compact Gensets

Urban densification across Japanese metropolitan areas, combined with stringent noise ordinances in residential and commercial districts, is driving significant innovation in silent and compact genset designs. Manufacturers are developing units with advanced soundproofing enclosures, variable-speed operation that reduces noise during low-load conditions, and reduced physical footprints suitable for rooftop installations, underground parking facilities, and space-constrained urban properties. These space-efficient solutions enable backup power deployment in locations where traditional gensets would be impractical or prohibited.

Growth of Hybrid Energy Solutions

The integration of gensets with renewable energy sources, battery storage systems, and intelligent controls is becoming increasingly prevalent across Japanese applications. Hybrid configurations allow gensets to operate at optimal efficiency levels rather than idling during low demand, reducing fuel consumption, emissions, and maintenance requirements while extending equipment life. This approach is particularly attractive for remote island communities, commercial facilities with solar installations, and industrial sites seeking to balance resilience with sustainability objectives. Government incentives and corporate ESG commitments further accelerate hybrid adoption.

Japan Gensets Market: Research Scope and Analysis

By Fuel Type Analysis

Diesel gensets continue to serve as the backbone of Japan's backup power infrastructure, maintaining a dominant market position driven by their proven reliability, high power density, and extensive service networks across the country. The diesel segment's strength is reinforced by Japan's mature fuel distribution infrastructure, with diesel readily available even in remote island communities and mountainous regions. Critical facilities such as hospitals, data centers, telecommunications towers, and government buildings overwhelmingly specify diesel gensets for their instantaneous response characteristics, ability to handle large load blocks, and extended runtime capabilities essential during prolonged grid outages following major earthquakes or typhoons. The existing installed base of diesel units across Japan represents a substantial replacement and maintenance-driven market, with many units reaching end-of-life after decades of service in disaster-prone environments. However, this segment faces increasing pressure from tightening emissions regulations, with Japanese environmental standards pushing manufacturers toward cleaner diesel technologies incorporating advanced after-treatment systems, improved combustion efficiency, and reduced particulate emissions. Manufacturers are responding with Stage V-equivalent engines that maintain performance while reducing environmental impact. Additionally, the diesel segment is seeing innovation in bi-fuel capabilities, allowing units to operate on a mixture of diesel and natural gas or hydrogen, providing a transitional pathway for users seeking to reduce carbon footprints without sacrificing reliability. The segment's future will be shaped by the balance between diesel's unparalleled reliability advantages and Japan's accelerating decarbonization commitments.

By Power Rating Analysis

Mid-range gensets, typically spanning the upto 75 kVA power band, constitute the largest and most versatile segment of Japan's gensets market, serving as the backbone of urban and commercial backup power infrastructure across the nation's densely populated metropolitan areas. This power range is ideally suited for the diverse requirements of office buildings, retail complexes, educational institutions, small to medium manufacturing facilities, and municipal government buildings that form the core of Japan's urban landscape. The segment benefits from consistent replacement cycles driven by Japan's strict building codes and fire safety regulations, which mandate periodic equipment testing and replacement schedules for emergency power systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Japanese building standards require comprehensive backup power coverage for buildings exceeding certain size or occupancy thresholds, creating a stable, regulation-driven market that remains resilient across economic cycles. Manufacturers serving this segment focus on delivering space-efficient designs suitable for constrained urban installations, with compact footprints, low-noise enclosures, and rooftop or basement installation capabilities essential in land-scarce Japanese cities. The mid-range segment has also seen significant innovation in emissions control technology, with manufacturers introducing Stage V-equivalent engines that meet Japan's increasingly stringent environmental standards while maintaining the reliability and response characteristics demanded by commercial users. Integration capabilities with building energy management systems and remote monitoring platforms have become increasingly important, allowing facility managers to maintain visibility and control over backup power assets.

By Application Analysis

Standby power is projected to dominate Japan's gensets market, reflecting the nation's acute awareness of power vulnerability following decades of earthquake, typhoon, and tsunami experiences that have fundamentally embedded disaster preparedness into the national consciousness. Japan's regulatory framework mandates standby power systems across a comprehensive range of facilities, with requirements varying by building type, occupancy, and criticality of function, but collectively creating a vast and stable market for backup gensets. Hospitals, emergency medical facilities, and long-term care centers face the most stringent requirements, with regulations specifying minimum runtime capabilities, automatic transfer switching, and regular testing protocols to ensure operational readiness. The healthcare sector's standby power requirements have only intensified as Japan's population ages and the demand for continuous medical services grows. Financial institutions, including banks, securities exchanges, and payment processing centers, maintain sophisticated standby power systems to ensure uninterrupted transaction processing and data integrity. Transportation infrastructure, including the Shinkansen bullet train network, regional rail systems, airports, and seaports, relies on standby gensets to maintain safety systems, signaling, lighting, and passenger services during grid disruptions. The telecommunications sector's standby power requirements have expanded with the rollout of 5G infrastructure, which demands backup coverage across a distributed network of towers and base stations. Commercial buildings, retail complexes, and residential towers increasingly incorporate standby gensets as both regulatory compliance measures and market differentiators, with backup power recognized as a valuable amenity. The digitalization of the Japanese economy has expanded the definition of critical infrastructure, with small and medium enterprises increasingly recognizing the business continuity value of standby protection.

By End-User Analysis

Key end-users across Japan's gensets market include manufacturing, healthcare, telecommunications, data centers, and residential sectors, each with distinct requirements and purchasing drivers that shape market dynamics. The manufacturing sector stands as a foundational end-user, reflecting Japan's status as a global industrial powerhouse with concentrations of automotive, electronics, semiconductor, chemical, pharmaceutical, and precision manufacturing facilities across regions including Aichi, Kanagawa, Osaka, and Fukuoka. Japanese manufacturers face unique challenges including aging grid infrastructure in industrial zones, the need for production continuity in just-in-time manufacturing environments, and increasing exposure to electricity price volatility. The automotive sector, anchored by global manufacturers and extensive supply chains, maintains particularly stringent backup power requirements to protect automated assembly lines and maintain quality control. The semiconductor industry, with fabs requiring continuous operation to maintain cleanroom conditions and prevent wafer loss, demands the highest levels of power reliability.

Healthcare facilities represent an indispensable end-user segment, with Japan's extensive network of hospitals, clinics, and long-term care facilities requiring comprehensive backup power coverage to maintain life-support equipment, operating rooms, emergency services, and temperature-sensitive medications during outages. The aging Japanese population has increased demand for healthcare services and consequently expanded the scope of facilities requiring reliable backup power. The telecommunications sector, undergoing 5G infrastructure expansion across urban and rural areas, represents a growing market for distributed backup solutions, particularly for remote towers and network nodes requiring compact, reliable power systems. The data center segment has emerged as the most demanding and fastest-growing end-user category, driven by Japan's position as a regional digital infrastructure hub, with major facilities concentrated in Tokyo, Osaka, and emerging markets across the country. Residential adoption continues to grow, driven by disaster awareness, government subsidies for residential energy storage and backup systems, and the increasing affordability of compact genset solutions.

The Japan Gensets Market Report is segmented on the basis of the following:

By Fuel Type

- Diesel

- Natural Gas

- Propane

By Power Rating

- Up to 75 kVA

- 75-375 kVA

- 375-750 kVA

- Above 750 kVA

By Application

- Standby Power

- Peak Shaving

- Prime/Continuous Power

By End-User

- Construction

- Manufacturing

- Telecom

- Healthcare

- Retail

- Data Centers

- Others

Impact of Artificial Intelligence in the Japan Gensets Market

- AI-Powered Disaster Resilience Optimization: Japan's frequent seismic events and typhoons demand rapid power restoration. AI systems analyze historical disaster patterns, real-time weather data, and grid vulnerability assessments to pre-position maintenance resources and automatically initiate backup protocols before outages occur, minimizing disruption to critical infrastructure.

- Autonomous Load Forecasting and Dispatch: Machine learning algorithms predict electricity demand fluctuations with high accuracy across Japan's diverse regions, from Tokyo's commercial districts to remote island communities. AI autonomously dispatches genset resources, balancing multiple units to operate at optimal efficiency while reducing fuel consumption and emissions.

- Real-Time Condition-Based Monitoring for Remote Islands: Japan's 14,000 islands face unique power reliability challenges. AI-enabled monitoring systems continuously assess genset health across dispersed island installations, automatically prioritizing maintenance alerts based on criticality and enabling centralized management of distributed power assets from mainland operations centers.

- Emissions Compliance Optimization: Japanese environmental regulations demand stringent emissions control. AI algorithms dynamically adjust combustion parameters, after-treatment systems, and operating schedules to maintain compliance while maximizing performance, helping operators navigate complex regulatory requirements across different prefectures and urban zones.

- Smart Grid Integration for Distributed Energy Resources: Japan's push toward decentralized energy systems requires sophisticated coordination. AI serves as the orchestration layer, seamlessly integrating gensets with solar installations, battery storage, and utility grid interfaces to create resilient hybrid systems that support Japan's energy transition goals.

Japan Gensets Market: Competitive Landscape

The Japan gensets market competitive landscape is characterized by a moderately fragmented yet technology-driven structure, where both domestic and international players compete across industrial, commercial, and backup power segments. Leading companies such as Mitsubishi Heavy Industries, Yanmar Co., Ltd., Honda Motor Co., Ltd., and Denyo Co., Ltd. dominate the domestic landscape, while global players like Cummins Inc. and Caterpillar Inc. maintain a strong presence through advanced product offerings and distribution networks. Together, major players account for a significant share of the market, reflecting a semi-consolidated structure.

Competition is primarily driven by technological innovation, product efficiency, pricing strategies, and compliance with stringent emission regulations. Companies are heavily investing in research and development to introduce low-emission, hybrid, and gas-based gensets, aligning with Japan’s decarbonization goals. The integration of IoT-enabled monitoring, predictive maintenance, and smart control systems has become a key differentiator, enabling improved performance, reduced downtime, and enhanced operational efficiency.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Domestic manufacturers benefit from strong local supply chains, established customer relationships, and deep understanding of regulatory frameworks. In contrast, international players leverage advanced engineering expertise, global service networks, and economies of scale to compete effectively. Strategic collaborations, localized production, and after-sales service expansion are widely adopted to strengthen market positioning.

Additionally, the competitive intensity is increasing due to the growing adoption of renewable energy and battery storage solutions, which challenge traditional diesel gensets. As a result, companies are increasingly focusing on hybrid power solutions, alternative fuels, and digital integration to maintain competitiveness and capture emerging opportunities in Japan’s evolving energy landscape.

Some of the prominent players in the Japan Gensets Market are:

- Caterpillar Japan LLC

- Cummins Japan Inc.

- Mitsubishi Heavy Industries, Ltd.

- Yanmar Holdings Co., Ltd.

- Kubota Corporation

- Denyo Co., Ltd.

- Kokusai Electric Co., Ltd.

- Fuji Electric Co., Ltd.

- Hitachi, Ltd.

- Toshiba Corporation

- Kawasaki Heavy Industries, Ltd.

- Isuzu Motors Limited

- Hino Motors, Ltd.

- Perkins Engines Company (Japan operations)

- Volvo Penta Japan

- Wärtsilä Japan Ltd.

- Generac Japan

- AKSA Power Generation Japan

- Atlas Copco Japan

- Aggreko Japan Ltd.

- Other Key Players

Recent Developments in the Japan Gensets Market

- February 2026: JERA Co., Inc. confirmed progress on offshore wind projects in Akita and Aomori, increasing renewable penetration and driving demand for backup gensets to ensure grid stability.

- February 2026: QatarEnergy signed a 27-year LNG supply agreement with JERA Co., Inc., supporting gas-based power generation and cleaner genset applications.

- December 2025: The Government of Japan approved ¥210 billion clean energy investment subsidies under its GX strategy, boosting demand for gensets in data centers and industrial backup applications.

- June 2025: Hino Motors and Mitsubishi Fuso Truck and Bus Corporation merged to form Archion Corporation, strengthening engine technologies relevant to gensets.

- March 2025: JERA Co., Inc. and EDF Trading merged their Japan power trading operations to enhance efficiency in electricity supply and backup power systems.

- December 2024: Kansai Electric Power Company acquired a 49% stake in a major offshore wind project in Europe, supporting renewable expansion and indirectly increasing genset demand for backup power.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 1.1 Bn |

| Forecast Value (2035) |

USD 1.9 Bn |

| CAGR (2026–2035) |

6.2% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Fuel Type (Diesel, Natural Gas, Propane), By Power Rating (Up to 75 kVA, 75-375 kVA, 375-750 kVA, Above 750 kVA), By Application (Standby Power, Peak Shaving, Prime/Continuous Power), By End-User (Construction, Manufacturing, Telecom, Healthcare, Retail, Data Centers, Others) |

| Country Coverage |

Japan |

| Prominent Players |

Denyo Co., Ltd., Yanmar Holdings Co., Ltd., Mitsubishi Heavy Industries, Ltd., Kubota Corporation, Cummins Japan Inc., Caterpillar Japan LLC, Kokusai Electric Co., Ltd., Fuji Electric Co., Ltd., Hitachi, Ltd., Toshiba Corporation, Kawasaki Heavy Industries, Ltd., Isuzu Motors Limited, Hino Motors, Ltd., Perkins Engines Company, Volvo Penta Japan, Wärtsilä Japan Ltd., Generac Japan, AKSA Power Generation Japan, Atlas Copco Japan, and Aggreko Japan Ltd., and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Japan Gensets Market?

▾ The Japan Gensets Market size is estimated to have a value of USD 1.1 billion in 2026 and is expected to reach USD 1.9 billion by the end of 2035.

What is the growth rate in the Japan Gensets Market?

▾ The market is growing at a CAGR of 6.2 percent over the forecasted period of 2026-2035.

Who are the key players in the Japan Gensets Market?

▾ Some of the major key players in the Japan Gensets Market are Caterpillar Inc., Cummins Inc., Generac Holdings Inc., Kohler Co., Mitsubishi Heavy Industries, Ltd., Yanmar, Rolls-Royce plc, and many others.