What is the Japan Green Steel Market Size?

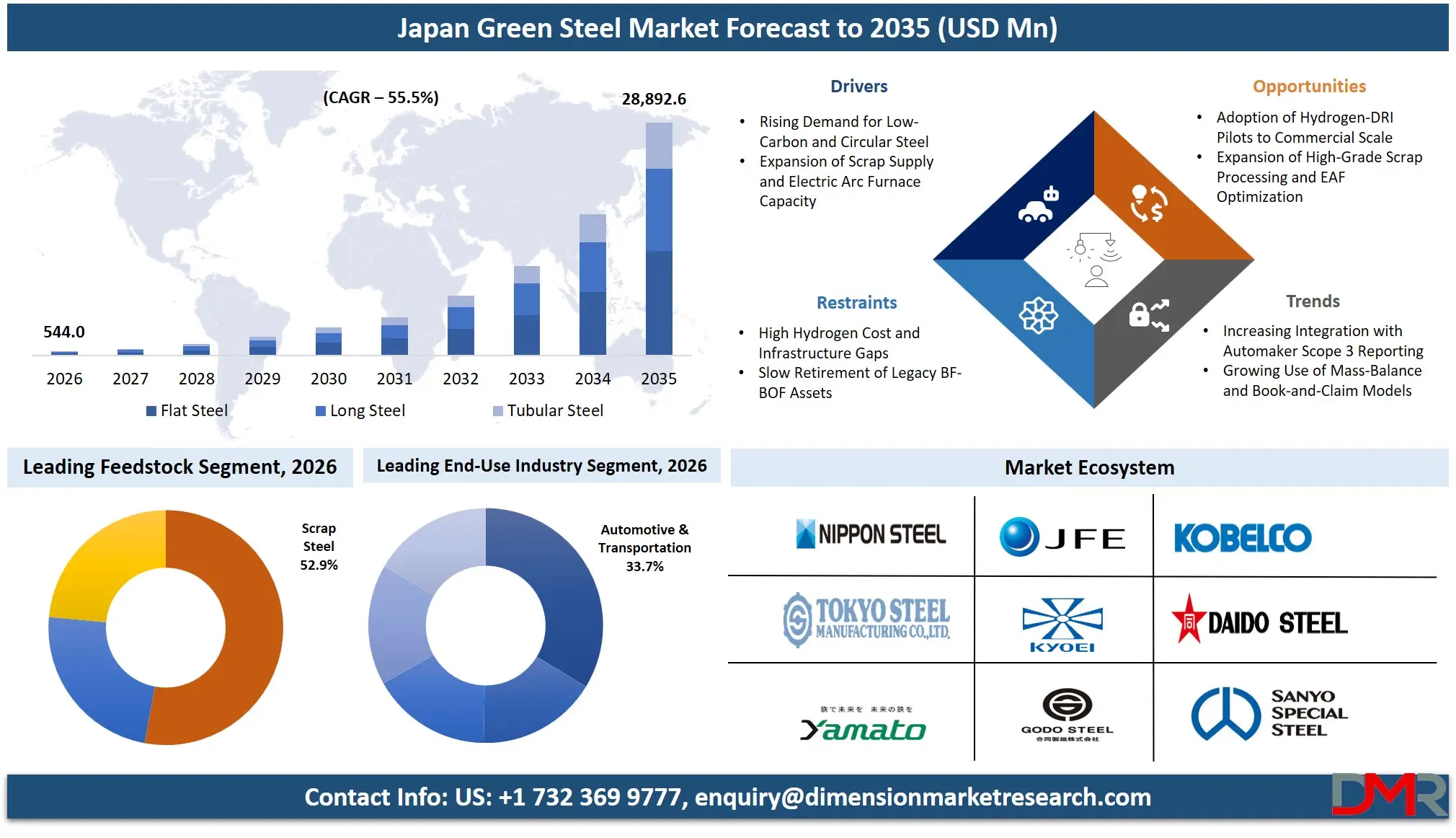

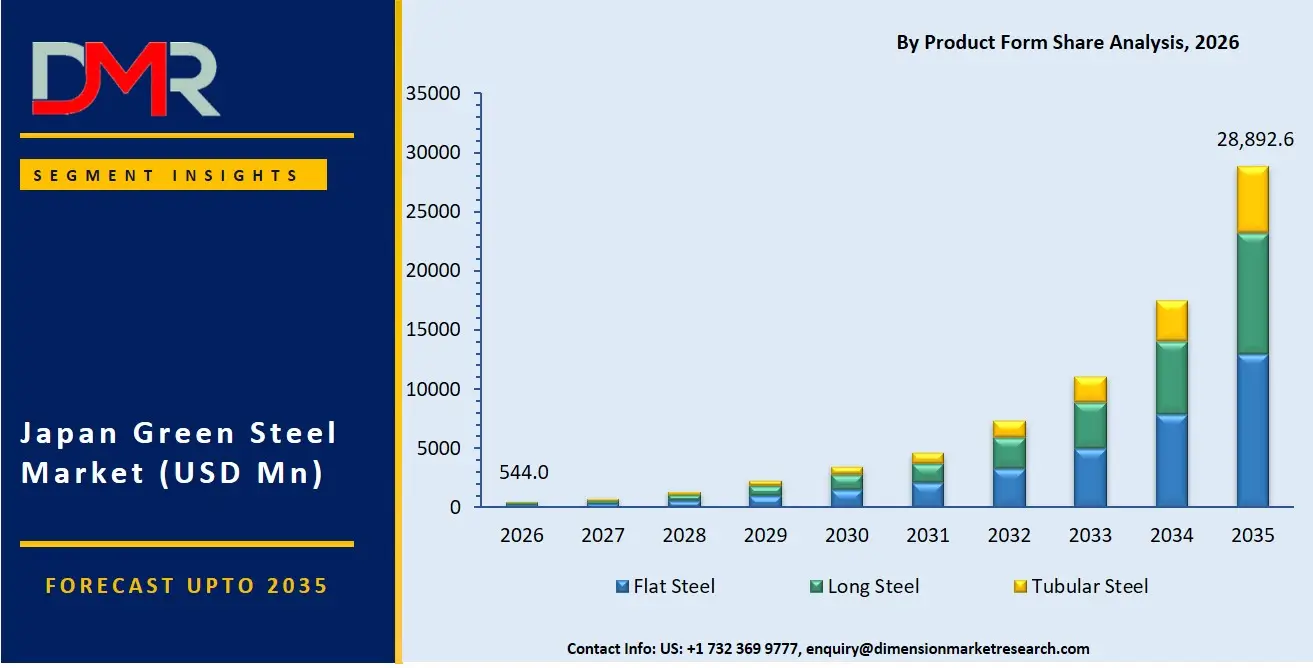

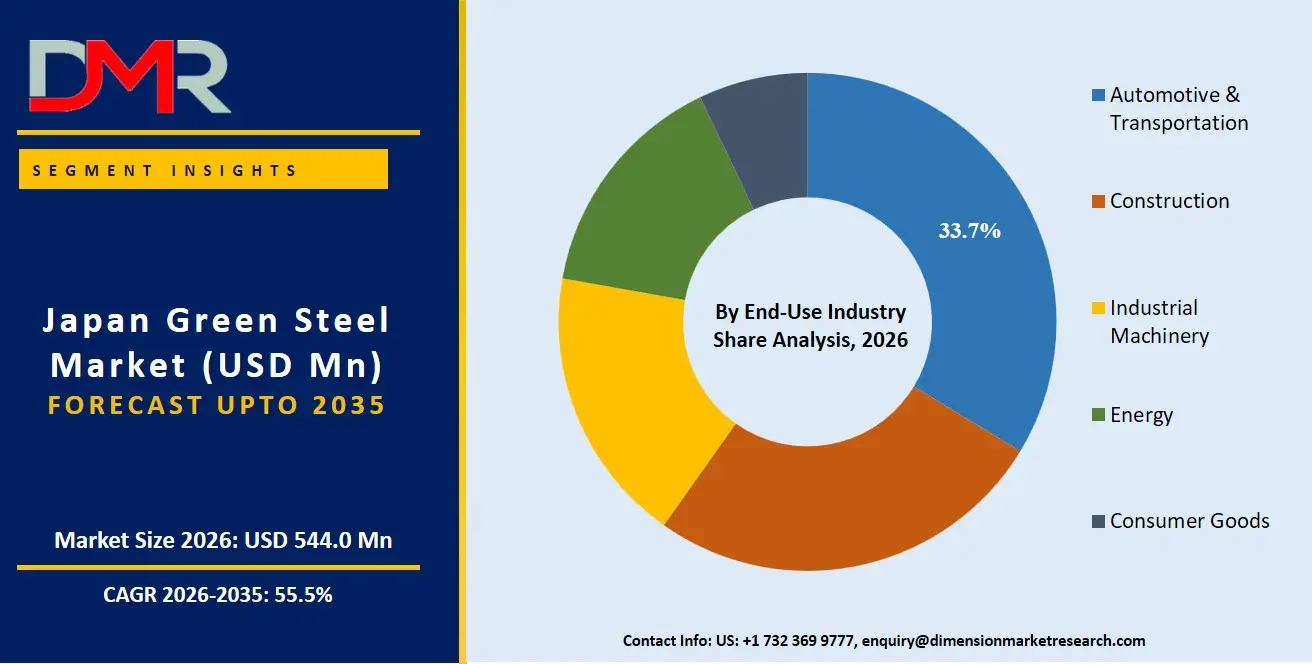

The Japan Green Steel Market is expected to reach a value of USD 544.0 million in 2026, and it is further anticipated to reach USD 28,892.6 million by 2035, growing at a CAGR of 55.5% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The green steel market has been showing consistent growth due to Japan's rising dependence on low-carbon, scrap-based, and hydrogen-ready steelmaking routes for effective, secure, and scalable industrial decarbonization. This includes several production technologies and engineering services that help steelmakers and end-users deploy low-emission solutions for automotive, construction, and machinery applications. There has been a rising need for plant retrofitting and hydrogen supply integration owing to the requirements for implementing electric arc furnaces, securing operational continuity against scrap supply disruptions, and delivering high-performance hydrogen-DRI systems to customers. Automotive manufacturers have emerged as the largest consumer segment for green steel, with Electric Arc Furnace (EAF) production being the most commercially active near-term route, while hydrogen-based DRI remains in pilot-scale demonstration.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Key Takeaways

- Market Size & Forecast: The Japan Green Steel market is forecasted to be valued at USD 544.0 million in 2026, growing incrementally to USD 28,892.6 million by 2035, due to the joint efforts of industrial decarbonization strategy on the part of steel enterprises as well as the obligatory deployment of low-emission and recycled-material production technologies.

- Growth Rate & Outlook: Japan market is expected to grow at 55.5% CAGR, propelled by the urgent need to reduce blast furnace CO₂ intensity, alongside increasing challenges in orchestrating scrap steel collection, automotive take-back loops, and hydrogen supply chain development.

- Primary Growth Drivers: Major driving factors comprise the transition from traditional BF-BOF steelmaking towards modern EAF and hydrogen-DRI production systems, the necessity to secure stable scrap steel supply, as well as the implementation of carbon capture retrofits and hydrogen injection pilots (COURSE50, GREINS).

- Key Market Trends: Major trends encompass the expansion of scrap-based EAF capacity through commercial channels, usage of hydrogen reduction within integrated steelworks for semi-industrial trials, and increased focus on low-carbon certification amidst rising buyer-side scope 3 emission mandates.

- By Production Technology Analysis: The Electric Arc Furnace (EAF) segment is projected to dominate the Japan Green Steel Market due to high demand for scrap-based and renewable-powered steel by automotive and construction buyers, with capabilities like real-time melt monitoring, energy efficiency, and lower capital intensity, which offer daily operations, regional scrap balancing, and batch flexibility within steel plant management.

- By Steel Type Analysis: The Recycled Steel segment is projected to dominate the Japan Green Steel Market due to its established supply chain, cost competitiveness, and use in construction rebar, structural sections, and automotive non-exposed parts for metropolitan infrastructure, general machinery, and consumer goods.

- By End-Use Industry Analysis: The Automotive & Transportation segment is anticipated to dominate in the Japan Green Steel Market as vehicle manufacturers adopt low-CO₂ steel grades (from EAF or hydrogen-DRI) to meet supply chain decarbonization targets, supported by OEM green procurement frameworks and Japan's carbon neutrality goals.

Use Cases

- Automotive Supply Chain Decarbonization: Car manufacturers procure Green Steel (EAF or H-DRI-based) for body-in-white and chassis components to reduce scope 3 emissions, supported by mass-balance certification and supplier CO₂ data exchange.

- Industrial Machinery Production: Machinery producers rely on Green Steel plates and sections for excavators and press frames, ensuring stable mechanical properties while complying with low-carbon procurement mandates.

- Public Infrastructure Projects: Municipal authorities specify low-carbon steel (recycled or hydrogen-based) for bridge girders and port structures under Japan's Green Infrastructure funding programs.

- Energy Industry Applications: Energy infrastructure developers use low-carbon steel tubulars for offshore wind monopiles and hydrogen transport pipelines, requiring both strength and verifiable emission reductions.

What is Green Steel?

Green Steel refers to steel produced with significantly lower CO₂ emissions compared to conventional BF-BOF routes. This involves transitioning from coke-based reduction to hydrogen-based direct reduction (H-DRI), increasing scrap usage in Electric Arc Furnaces (EAF), or retrofitting existing blast furnaces with carbon capture, utilization, and storage (CCUS) or biomass injection. Unlike conventional steel, green steel pertains to "the how and where" of emissions reduction across the value chain. It entails having a Production Technology pathway to provide the means through which carbon intensity is measured and reduced, and Engineering Services to help integrate hydrogen supply, manage scrap logistics, and optimize furnace loading. As companies take charge of their decarbonization commitments, it is important to have verifiable low-emission steel that will be produced successfully while maintaining cost and safety measures.

How AI is Transforming the Green Steel Market?

The implementation of artificial intelligence in the green steel industry is becoming increasingly prominent as an optimization tool for improving the efficiency and stability of scrap-based production through Electric Arc Furnace (EAF). The use of advanced analytics and sensing technologies can help steel producers in the classification of materials as well as in the monitoring and optimization of the production process and its energy consumption. In scrap-based EAF production chains, data-enabled methods assist producers in improving the consistency of scrap charges and detecting material inconsistencies, thus decreasing yield loss and improving product quality. In addition, predictive maintenance is used for the maintenance of critical pieces of equipment like furnaces and rolling mills to prevent unexpected downtimes.

In hydrogen-based green steel production pilots like COURSE50 and GREINS, digital sensing systems have been utilized on a relatively limited basis in monitoring processes and measuring reduction efficiency. However, these applications have been mostly experimental. Overall, AI in the Japan green steel market acts as a supplementary optimization layer to existing metallurgical processes without revolutionizing the production processes entirely.

Market Dynamics

Key Drivers in the Japan Green Steel Market

Rising Demand for Low-Carbon and Circular Steel

Metallurgical innovation is revolutionizing the green steel industry through hydrogen reduction scale-up and scrap quality optimization. The technology portfolio includes hydrogen-DRI pilot plants that detect reduction anomalies and furnace inefficiencies in order to resolve them progressively, thereby preventing energy waste and operational delays. In addition, the EAF process improvements help steelmakers assess scrap chemistry, determine optimal charge mix, and customize power input scheduling. Metallurgical innovation forms an essential part of governance and customer trust initiatives. Engineering services involve process monitoring that tracks compliance and keeps emission logs while ensuring that all operations comply with regulations and the carbon accounting protocols in Japan.

Expansion of Scrap Supply and Electric Arc Furnace Capacity

The rapid development of scrap collection and EAF modernization in Japan creates high demand in the steel sector for secondary raw materials, automotive shredder residue processing, industrial scrap sorting, and demolition recycling. Companies today use green steel production routes to achieve critical goals related to carbon neutrality, material yield optimization, asset tracking, and regulatory compliance. With increased use of EAFs by many steel operators, plant owners have become more interested in adopting automated charge optimization systems that can handle variable scrap quality effectively. In addition, there is a growing need for predictable low-carbon steel supply for buyers, which increases the adoption rate of green steel procurement contracts.

Restraints in the Japan Green Steel Market

High Hydrogen Cost and Infrastructure Gaps

The high cost of green hydrogen and limited pipeline infrastructure in Japan have brought about difficulties for hydrogen-DRI projects as well as steel operators. Energy supply constraints are tightening the feasibility of large-scale hydrogen reduction deployments, the acquisition of hydrogen from domestic electrolysis or imports, and storage measures in order to minimize risks related to supply disruption. Enterprises are expected to secure long-term hydrogen supply agreements, making their project economics more complicated and costly. The current situation subjects a steel operator using hydrogen-DRI to high operating costs, delivery delays, and reputational risk if hydrogen is unavailable.

Slow Retirement of Legacy BF-BOF Assets

Growth in the continued operation of conventional BF-BOF infrastructure with partial decarbonization retrofits is impacting the market share growth of truly low-emission green steel within Japan. Traditional integrated mills are preferred over EAF green steel for certain high-grade automotive applications due to stricter impurity control and established supply relationships. Some steelmakers have also begun using BF-BOF with CCUS as part of their transition strategy, relying less on full hydrogen conversion. The use of conventional integrated routes also offers simpler raw material procurement without advanced scrap sorting.

Growth Opportunities in the Japan Green Steel Market

Adoption of Hydrogen-DRI Pilots to Commercial Scale

There exist many growth opportunities in the green steel market in Japan through the scaling of hydrogen-based direct reduction from pilot to demonstration and eventually commercial plants. These industrial systems allow steel operators to reduce CO₂ intensity by >80% compared to coke-based smelting. Near-zero emission steel, higher product purity, and long-term cost certainty are some features that may be implemented by steelmakers in decarbonizing their product portfolios. Steel producers based in Japan are starting to consider commercializing hydrogen-DRI as an alternative for effective green steel production after 2030. With improved hydrogen infrastructure by energy suppliers (Iwatani, ENEOS) and engineering partners (IHI, JFE Engineering), integrated steelworks will invest significantly in advanced green steel production systems post-2030.

Expansion of High-Grade Scrap Processing and EAF Optimization

Integration of advanced scrap sorting and pre-heating technologies in EAF-based steelmaking is bringing about great prospects for green steel providers in Japan. Many steel operators are now using sensor-based scrap sorting technology that automates charge composition in order to offer impurity reduction support to melt shop managers. Advanced scrap classification can help organizations understand material chemistry, optimize energy input, and determine when the best time is for furnace tapping in order to maximize operational uptime and yield. The increasing use of eddy current separators, X-ray fluorescence sorters, and automated scrap logistics in different sectors such as automotive dismantling, construction demolition, and industrial maintenance is driving demand for higher-quality recycled feedstock.

Trends in the Japan Green Steel Market

Increasing Integration with Automaker Scope 3 Reporting

Increasingly, Japanese steel operators are responding to automaker scope 3 emissions reporting requirements by providing verified low-CO₂ steel certificates. Data exchange allows organizations to easily integrate steel mill emission factors into their product carbon footprint calculations, supply chain management solutions, and sustainability reports without having to invest heavily in bespoke verification. The advantages associated with standardized carbon accounting include real-time emission factor updates, product-level carbon tracking, and multi-buyer alignment options. Due to the growing adoption of supply chain decarbonization approaches in addition to internal emission reduction processes, the use of certified green steel has been steadily increasing. The adoption of low-CO₂ steel as an alternative to conventional BF-BOF material has continued to gain popularity in Japan.

Growing Use of Mass-Balance and Book-and-Claim Models

Mass-balance allocation approaches are being incorporated by Japanese steel firms in order to facilitate their green steel sales using a combination of hydrogen-DRI, EAF, and BF-BOF with CCUS. Companies are focusing on creating an integrated product portfolio that ensures consistency in the quality of steel delivery through different production routes while allowing allocation of low-carbon attributes to specific customer orders. Green steel certificates continue to be an integral part of these attribution approaches owing to their flexibility and rapid market scaling. Companies from sectors such as automotive body manufacturing, industrial machinery fabrication, and construction engineering have been incorporating green steel certificates into their decarbonization management systems.

Research Scope and Analysis

The Japan Green Steel Market is segmented by production technology, steel type, product form, feedstock, end-use industry, and deployment. The market supports automotive decarbonization, construction material procurement, industrial machinery fabrication, and government infrastructure across individual steel consumers, integrated steelworks, EAF mini-mills, and trading companies through physical green steel products and certified low-CO₂ allocations.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Production Technology Analysis

Electric Arc Furnace (EAF) is expected to lead the Japan Green Steel Market in 2026 with a projected market share of 49.9% as a result of steel operators' growing preference for scrap-based and renewable-powered melting. Japanese EAF mills have developed a preference for high-quality scrap and optimized power sourcing for performing functions such as rebar production, section rolling, and flat steel casting. BF-BOF with decarbonization (CCUS, biomass co-injection) is likely to occupy the second place due to the rising retrofitting of existing integrated works to reduce emissions without full asset replacement, particularly for high-grade automotive sheet production. Hydrogen-Based Steelmaking (H-DRI) is expected to grow steadily as a consequence of successful pilot operations (COURSE50, GREINS) leading to semi-commercial deployment post-2030, with first commercial plants expected in the late 2030s. DRI (Direct Reduced Iron) gas-based and coal-based transition routes, along with emerging technologies, comprise the remaining share.

By Steel Type Analysis

Recycled Steel is projected to dominate the Japan Green Steel Market in 2026, with an estimated share of 45.3%, owing to its established supply chain from scrap collection networks, cost competitiveness compared to primary steel, and widespread acceptance in construction rebar, structural sections, and general engineering applications. Japanese construction firms and industrial machinery manufacturers favor recycled steel because it provides verifiable CO₂ reduction along with consistent mechanical properties. Low-Carbon Steel follows, driven by automotive OEM scope 3 emission targets and the need for high-formability grades for body panels. High-Strength Low-Alloy (HSLA) Steel is growing rapidly due to light weighting requirements in automotive and heavy machinery, combining strength with reduced material usage and lower carbon footprint per component.

By Product Form Analysis

Flat Steel is set to dominate the Japan Green Steel Market in 2026 with a projected share of 39.3%, thanks to its high usage in automotive outer panels, appliance bodies, electrical steel applications, and industrial equipment. Flat steel products enable established EAF and BF-BOF decarbonization pathways with minimal property variation and have strong demand from automotive and consumer goods sectors. Long Steel will experience robust growth in the coming years because of construction sector demand for low-carbon rebars, pilings, structural beams, bars, and rods for building and civil engineering projects. Tubular Steel is growing as energy infrastructure developers and construction projects require low-carbon pipes, hollow sections, and line pipe for hydrogen transport and offshore wind applications.

By Feedstock Analysis

Scrap Steel is projected to continue dominating in the Green Steel Market of Japan, with an expected market share of 52.9% in 2026, owing to well-established collection infrastructure, EAF capacity, and the circular economy orientation of Japan's steel sector. Businesses in the scrap-based EAF segment are increasingly adopting advanced sorting technologies due to the benefits offered by such systems, including lower CO₂ intensity, predictable melt chemistry, and regulatory compliance with resource efficiency mandates. Iron Ore remains relevant for BF-BOF and transitional DRI routes, particularly for high-grade automotive sheet where residual elements in scrap must be minimized. Green Hydrogen, though currently a small share, is expected to experience the fastest growth post-2030, thanks to the scaling of hydrogen-DRI pilot projects, government hydrogen subsidies, and import terminal development.

By End-Use Industry Analysis

Automotive & Transportation is projected to dominate the Japan Green Steel Market in 2026, with an estimated share of 33.7%, owing to large-volume consumption of high-strength steel grades and aggressive OEM scope 3 emission reduction targets. Japanese automakers and tier-1 suppliers favor green steel because it provides scope 3 abatement along with formability and strength. Construction follows, driven by increasing green building certifications and public works low-carbon material mandates for residential and commercial buildings. Energy is primarily used by offshore wind and hydrogen pipeline projects requiring low-carbon tubulars. Industrial Machinery is growing due to adoption of recycled-content steel for general fabrication and heavy equipment. Consumer Goods represents a smaller but stable segment, including appliances and electronics enclosures requiring certified low-carbon flat steel.

By Deployment Analysis

Brownfield Retrofit is projected to dominate the Japan Green Steel Market in 2026, with an estimated share of 68.4%, owing to the high capital costs of greenfield construction and the extensive existing integrated steelworks and EAF facilities across Japan requiring decarbonization upgrades. Japanese steelmakers are prioritizing CCUS additions to BF-BOF lines, hydrogen injection pilots at existing works, and EAF modernization at current sites. Greenfield deployment, while smaller in share, is expected to grow for new hydrogen-DRI plants and large-scale EAF scrap-based facilities built on brownfield sites after demolition of older assets, with fully new sites being rare due to land constraints and infrastructure requirements.

The Japan Green Steel Market Report is segmented based on the following:

By Production Technology

- Electric Arc Furnace (EAF)

- Scrap-based

- Renewable-powered

- Hydrogen-Based Steelmaking (H-DRI)

- Green hydrogen

- Hybrid (hydrogen + natural gas)

- DRI (Direct Reduced Iron)

- Gas-based

- Coal-based (transition)

- BF-BOF (with decarbonization)

- Emerging Technologies

By Steel Type

- Recycled Steel

- Low-Carbon Steel

- High-Strength Low-Alloy (HSLA) Steel

By Product Form

- Flat Steel

- Hot rolled

- Cold rolled

- Coated

- Long Steel

- Tubular Steel

By Feedstock

- Scrap Steel

- Iron Ore

- Green Hydrogen

By End-Use Industry

- Construction

- Automotive & Transportation

- Energy

- Industrial Machinery

- Consumer Goods

By Deployment

- Greenfield

- Brownfield Retrofit

Competitive Landscape

The competitive landscape of the Japan Green Steel market is shaped by integrated steelmakers, electric arc furnace (EAF) operators, trading houses, and engineering firms competing across decarbonization pathways such as BF-BOF optimization, scrap-based EAF expansion, and hydrogen-DRI development. Leading producers, including Nippon Steel Corporation, JFE Steel Corporation, and Kobe Steel, Ltd., are pursuing hybrid strategies that combine blast furnace efficiency improvements with long-term investments in hydrogen reduction technologies and EAF capacity additions. EAF-focused players such as Tokyo Steel Manufacturing Co., Ltd. strengthen competitiveness through cost-efficient, scrap-based low-carbon steel production. Strategic partnerships are central, particularly between steelmakers, scrap suppliers, hydrogen energy providers, and automotive OEMs, ensuring raw material security and stable off-take demand for low-carbon steel. Rather than traditional price-based competition, advantage is increasingly driven by process innovation, energy efficiency, and emissions reduction technologies. While large-scale consolidation remains limited, capital allocation is increasingly shifting toward green steel investments, including retrofits, hydrogen pilots, and EAF modernization across Japan's steel ecosystem.

Some of the prominent players in the Japan Green Steel Market are:

- Nippon Steel Corporation

- JFE Steel Corporation

- Kobe Steel, Ltd.

- Tokyo Steel Manufacturing Co., Ltd.

- Daido Steel Co., Ltd.

- Kyoei Steel, Ltd.

- Yamato Kogyo Co., Ltd.

- Toa Steel Co., Ltd.

- Godo Steel, Ltd.

- Osaka Steel Co., Ltd.

- Aichi Steel Corporation

- Sanyo Special Steel Co., Ltd.

- Mitsubishi Steel Mfg. Co., Ltd.

- Topy Industries, Ltd.

- Toyo Kohan Co., Ltd.

- Maruichi Steel Tube Ltd.

- The Japan Steel Works, Ltd.

- IHI Corporation

- JFE Engineering Corporation

- Mitsubishi Materials Corporation

- Other Key Players

Recent Developments

- May 2026: Nippon Steel Corporation announced execution of structural reforms including integration activities with Sanyo Special Steel Co., Ltd. and continued expansion of its GX (Green Transformation) strategy, reinforcing its shift toward low-carbon steel production and overseas decarbonized capacity expansion including U.S. Steel and AM/NS India operations.

- May 2026: JFE Steel Corporation reported continued advancement of its hydrogen-based steelmaking roadmap under the GREINS and COURSE50 frameworks, with consortium-based R&D alongside Nippon Steel, Kobe Steel, and JRCM targeting large-scale CO₂ reduction in blast furnace operations and scaling toward commercialization phases.

- April 2026: Kobe Steel, Ltd. advanced CCS (carbon capture and storage) feasibility work in partnership with Osaka Gas for a large-scale CCS value chain targeting industrial CO₂ reduction in steel production and thermal power applications in Japan's Kansai region.

- March 2026: Tokyo Steel Manufacturing Co., Ltd. announced continued optimization of its electric arc furnace (EAF) operations, including increased procurement of renewable electricity and further reduction of Scope 1 and Scope 2 emissions intensity, reinforcing its position as Japan's lowest-CO₂ primary steel producer and a benchmark for scrap-based green steel production.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 544.0 Mn |

| Forecast Value (2035) |

USD 28,892.6 Mn |

| CAGR (2026–2035) |

55.5% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Production Technology, By Steel Type, By Product Form, By Feedstock, By End-Use Industry, By Deployment |

| Country Coverage |

Japan |

Frequently Asked Questions

How big is the Japan Green Steel Market?

▾ The Japan Green Steel Market is poised to be valued at USD 544.0 million in 2026 and is projected to reach USD 28,892.6 million by 2035, driven by the universal need for secure, scalable, and reliable digital customer communications.

What is the CAGR of the Japan Green Steel Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 55.5% from 2026 to 2035, reflecting the maturing nature of the green steel transition and the accelerating complexity of scrap logistics, hydrogen development, and buyer-side carbon targets.

What factors are driving the growth of the Japan Green Steel Market?

▾ Key drivers include the decarbonization imperative for CO2 reduction, the need to modernize legacy BF-BOF steel plants, the management complexity of scrap steel collection and hydrogen supply, and the surge in demand for EAF and hydrogen-DRI amid evolving carbon neutrality laws and OEM scope 3 requirements.

What are the major trends in the Japan Green Steel Market?

▾ Major trends include the expansion of scrap-based EAF production, the pilot-to-commercial scaling of hydrogen-DRI (COURSE50, GREINS), the retrofitting of BF-BOF with CCUS and biomass, and the focus on low-CO2 certification and mass-balance allocation models.

Who are the key players in the Japan Green Steel Market?

▾ Key players include Nippon Steel Corporation, JFE Steel Corporation, Kobe Steel, Ltd., Tokyo Steel Manufacturing Co., Ltd., and Daido Steel Co., Ltd., and many more.

How is the Japan Green Steel Market segmented?

▾ The market is segmented by production technology, steel type, product form, feedstock, end-use industry, and deployment.