Market Overview

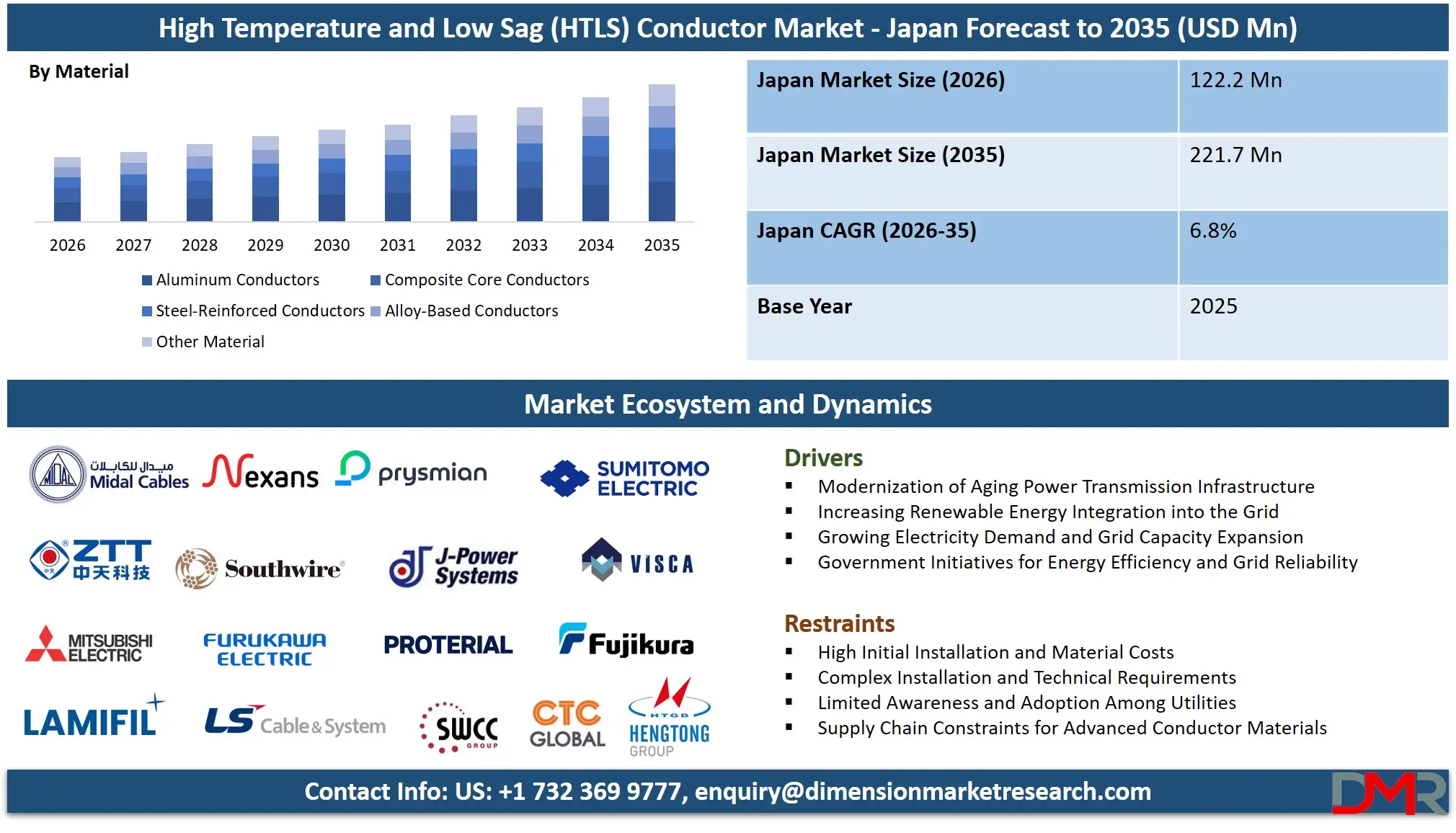

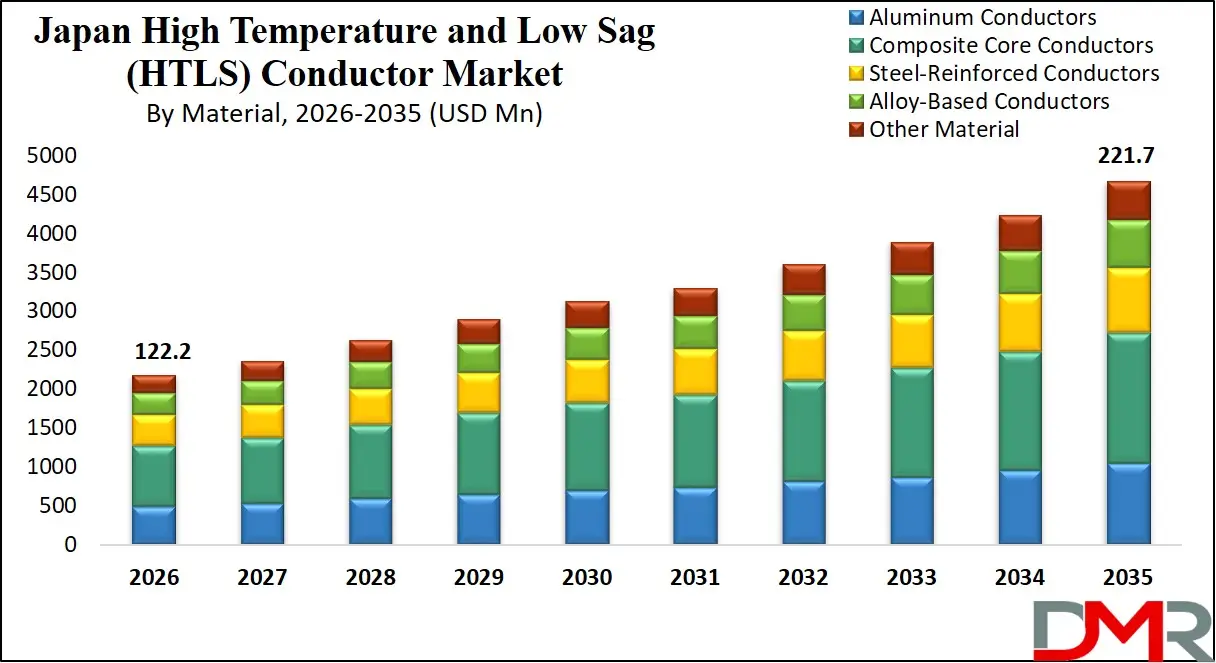

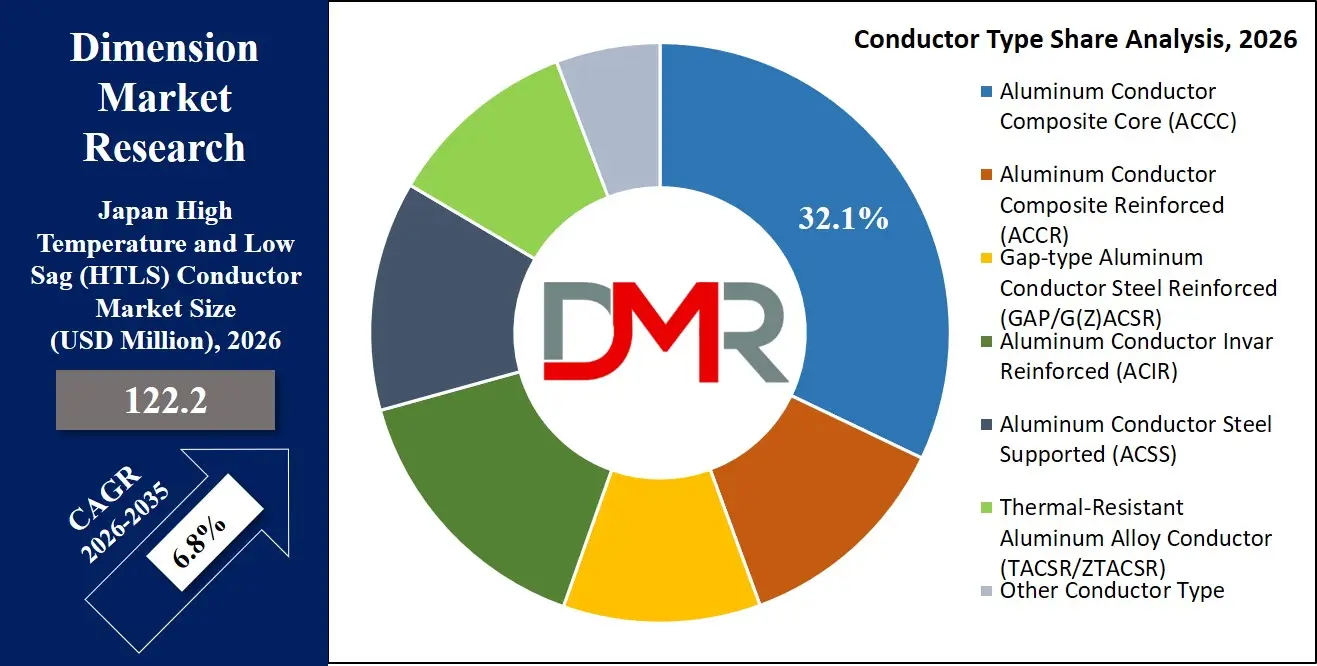

The Japan High Temperature and Low Sag (HTLS) Conductor Market is anticipated to be valued at approximately USD 122.2 million in 2026 and is expected to attain nearly USD 221.7 million by 2035, expanding at a CAGR of about 6.8% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The growth of this market is fundamentally driven by the imperative to modernize Japan's aging power grid, bolster energy security, and integrate renewable energy sources following the national energy policy shifts. The country's transmission network faces unique challenges, including a divided frequency (50Hz/60Hz), a high concentration of renewable energy generation in specific northern and southern regions, and the need for enhanced resilience against natural disasters.

A substantial portion of Japan's transmission infrastructure was constructed during the post-war economic boom, and much of it is now decades old, facing reliability issues and capacity limitations. With land acquisition and new right-of-way development being exceptionally difficult and costly in densely populated Japan, utilities are prioritizing reconductoring existing lines with HTLS technology to increase power transfer capacity without building new towers.

Japan's energy landscape has been transformed since 2011, with a strong push towards renewables, particularly solar and offshore wind. This creates a pressing need to strengthen the grid interconnections between Hokkaido, Tohoku, and Honshu to transmit clean energy to major demand centers like Tokyo and Osaka. HTLS conductors offer a critical solution for upgrading these long-distance transmission corridors.

Government initiatives, such as the Green Growth Strategy and the push for carbon neutrality by 2050, are catalyzing investment in grid infrastructure. The Organization for Cross-regional Coordination of Transmission Operators (OCCTO) plays a key role in planning and mandating transmission upgrades to facilitate renewable energy integration and ensure nationwide grid stability, further driving the adoption of advanced conductor technologies like HTLS.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Despite the positive outlook, the market faces challenges, including the high initial cost of HTLS conductors compared to conventional ACSR, stringent Japanese Industrial Standards (JIS), and the technical complexities of replacing conductors on existing towers in challenging geographical and urban environments.

Nonetheless, ongoing advancements in materials science, composite core technology, and Japanese engineering excellence are expected to solidify the role of HTLS conductors in creating a resilient, high-capacity, and sustainable transmission grid for Japan's future energy needs.

Impact of Iran War on Japan High Temperature and Low Sag (HTLS) Conductor Market

- Increased Raw Material Procurement Costs: Japan is a major importer of raw materials, including aluminum and the carbon fiber used in composite cores. Geopolitical instability in the Middle East can disrupt global supply chains and inflate prices for these commodities, increasing manufacturing costs for domestic and international HTLS suppliers serving the Japanese market.

- Supply Chain Vulnerability: Conflicts in key shipping regions can lead to logistics delays and higher freight costs. This vulnerability is critical for Japan, which relies on stable maritime routes for importing specialized materials like advanced alloys and carbon fiber, potentially impacting project timelines for planned grid upgrades.

- Energy Price Escalation and Manufacturing Impact: As a major energy importer, Japan is highly susceptible to global oil and gas price spikes caused by regional wars. Higher energy costs can increase the expense of domestic manufacturing processes, including aluminum smelting and conductor production, potentially affecting the overall economics of HTLS projects.

- Reinforced Focus on National Energy Security: Geopolitical tensions typically prompt the Japanese government to accelerate efforts to enhance domestic energy independence and grid resilience. This often translates into increased investment in robust transmission infrastructure to ensure a stable power supply, thereby creating long-term, sustained demand for HTLS conductors as a key enabling technology.

Japan High Temperature and Low Sag (HTLS) Conductor Market: Key Takeaways

- Steady Market Growth Trajectory: The Japan HTLS Conductor Market, valued at USD 122.2 million in 2026, is projected to reach USD 221.7 million by 2035, reflecting consistent growth underpinned by the critical need for grid modernization and the integration of variable renewable energy.

- Moderate but Stable CAGR: The market is expected to grow at a CAGR of 6.8% from 2026 to 2035, driven by targeted government policies, OCCTO's grid expansion plans, and the technical necessity of upgrading the nation's aging and frequency-divided transmission network.

- Aluminum Conductor Composite Core (ACCC) to Lead: ACCC is projected to hold a significant market share, as its lightweight, high-strength, and low-sag properties are ideal for increasing capacity on existing rights-of-way in Japan's constrained geography, particularly for long-distance interconnections linking renewable energy zones to major cities.

- Grid Reconductoring/Capacity Upgrade as Key Application: This segment will dominate, driven by the prohibitive cost and difficulty of acquiring new land for transmission corridors in Japan. Reconducting existing lines is the most practical and cost-effective strategy for upgrading the grid to handle increased loads from offshore wind and solar power.

- General Electric Utilities as Primary End-Users: The ten major general electric utilities (e.g., TEPCO, Kansai EPCO, Chubu EPCO) and the Power Development Corporation (J-POWER) are the primary procurers of HTLS conductors, driven by government mandates for renewable integration, grid resilience, and compliance with OCCTO's long-term transmission plans.

- Grid Interconnection Bottlenecks Drive Adoption: The need to alleviate congestion on interconnections between the country's two frequency regions and on lines from Hokkaido/Tohoku to the Tokyo metropolitan area is a powerful driver for HTLS reconductoring, offering a faster solution than building new, expensive transmission corridors.

Japan High Temperature and Low Sag (HTLS) Conductor Market: Use Cases

- Cross-Frequency Interconnection Upgrades: Utilities utilize HTLS conductors to upgrade the capacity of frequency converter stations and the AC lines feeding them, improving the efficiency and volume of power exchange between Japan's 50Hz and 60Hz grids.

- Offshore Wind Farm Grid Connection: Transmission system operators deploy HTLS conductors to reconduct existing onshore lines leading to coastal landing points, enabling them to carry the large amounts of power generated by new offshore wind projects to inland load centers.

- Volcanic and Mountainous Terrain Reconductoring: In regions with challenging geography, such as crossing volcanic zones or mountainous areas, utilities deploy HTLS conductors for their reduced sag and higher strength, allowing for longer spans and reduced tower stress in environmentally sensitive areas.

- Urban Infeed Capacity Enhancement: Utilities in metropolitan areas like Tokyo, Osaka, and Nagoya reconductor transmission lines entering the city with HTLS conductors to meet growing demand and ensure supply reliability without needing to acquire new, unavailable right-of-way.

- Resilience Against Seismic and Weather Events: Following major earthquakes and typhoons, utilities are increasingly specifying HTLS conductors for their superior strength and durability, using them in reconstruction and reinforcement projects to build a more resilient grid capable of withstanding future natural disasters.

Japan High Temperature and Low Sag (HTLS) Conductor Market: Stats & Facts

Ministry of Economy, Trade and Industry (METI)

- Japan's government has set a target for renewable energy to account for 36-38% of the power mix by 2030, necessitating significant grid expansion and upgrades.

- The Grid Reinforcement Plan, formulated by OCCTO under METI's supervision, identifies critical interregional transmission lines requiring capacity enhancement, many of which are prime candidates for HTLS reconductoring.

- METI projects a significant increase in power demand from data centers and semiconductor fabs, placing additional strain on existing urban transmission networks.

Organization for Cross-regional Coordination of Transmission Operators (OCCTO)

- OCCTO has identified the need to increase the interconnection capacity between Eastern and Western Japan (the 50/60Hz boundary) and from the Hokkaido-Tohoku region to Tokyo.

- The organization's master plan includes multiple "trunk transmission line" projects where HTLS conductors are being evaluated and specified to maximize capacity within existing corridors.

- OCCTO reports that interconnection queues for renewable energy projects are growing, particularly for offshore wind in the north, driving the need for rapid transmission solutions like reconductoring.

Federation of Electric Power Companies of Japan (FEPC)

- The 10 major electric power companies manage a vast network of high-voltage transmission lines exceeding 30,000 km.

- A significant percentage of this infrastructure was built in the 1970s and 1980s and is now entering a phase of renewal and capacity upgrading.

- Investment in transmission infrastructure by the major utilities is expected to rise steadily to support the government's 2050 carbon neutrality goal.

New Energy and Industrial Technology Development Organization (NEDO)

- NEDO has funded demonstration projects for advanced HTLS conductors and dynamic line rating systems to validate their performance in Japan's unique climatic and grid conditions.

- Research focuses on developing next-generation conductor materials with even higher heat resistance and lower sag for future ultra-high-voltage lines.

- NEDO's roadmap includes digitalizing grid management, where smart conductors with integrated monitoring will play a key role.

Japan Wind Power Association (JWPA)

- Japan aims to install 10 GW of offshore wind by 2030 and up to 45 GW by 2040, primarily in the waters off Hokkaido, Tohoku, and Kyushu.

- The association highlights that grid capacity is the single biggest bottleneck for offshore wind deployment, making onshore grid upgrades, including HTLS reconductoring, an urgent national priority.

- Successful offshore wind integration depends on the coordinated upgrade of the onshore transmission backbone from northern Japan to the Kanto region.

Institute of Energy Economics, Japan (IEEJ)

- Analysis suggests that reconductoring existing lines with advanced conductors can be significantly more cost-effective and faster than building new transmission lines, especially in land-scarce Japan.

- The IEEJ emphasizes that grid resilience investments, including the use of more robust conductors, are critical given Japan's high exposure to earthquakes, typhoons, and tsunamis.

- Achieving energy security and decarbonization targets will require transmission capacity to grow at a pace never seen before, with HTLS as a core enabling technology.

Japan High Temperature and Low Sag (HTLS) Conductor Market: Market Dynamic

Driving Factors in the Japan High Temperature and Low Sag (HTLS) Conductor Market

Aging Infrastructure and the Need for Renewal

A primary driver is the urgent need to address Japan's aging transmission network. Much of the high-voltage grid was built decades ago and requires renewal to maintain reliability. HTLS conductors offer a unique advantage by not only replacing aged wires but also simultaneously increasing power-carrying capacity. This allows utilities to kill two birds with one stone addressing asset end-of-life concerns while also preparing the grid for future load growth and renewable energy influx without the immense challenge of new tower construction.

Mandates for Renewable Energy Integration

Japan's legally binding commitment to carbon neutrality by 2050 and its 2030 renewable energy target are powerful, policy-driven drivers. The government, through METI and OCCTO, has formulated specific plans to reinforce the grid to accommodate large-scale solar and, critically, offshore wind. This creates a compliance-driven necessity for transmission expansion. HTLS reconductoring of key interties, such as those connecting Hokkaido's potential wind power to Honshu, is not just an operational choice but a required step to meet national energy goals.

Restraints in the Japan High Temperature and Low Sag (HTLS) Conductor Market

High Implementation and Material Costs

The initial procurement and installation cost of HTLS conductors remains significantly higher than that of conventional ACSR conductors. In a utility environment with strict cost controls and regulatory approval processes for capital expenditure, justifying the premium for HTLS can be challenging, particularly for projects not facing immediate capacity constraints. While the life-cycle cost may be lower, the higher upfront investment is a notable restraint.

Stringent Technical Standards and Approval Processes

All transmission equipment in Japan must comply with rigorous Japanese Industrial Standards (JIS) and utility-specific technical specifications. Introducing new HTLS technologies, especially those with composite cores, requires extensive type testing and approval from multiple utilities. This lengthy and costly validation process can slow the adoption of innovative conductor designs compared to markets with more harmonized standards.

Opportunities in the Japan High Temperature and Low Sag (HTLS) Conductor Market

Development of Offshore Wind Grid Connections

The most significant growth opportunity lies in serving the massive offshore wind pipeline. The government's goal of 45 GW by 2040 requires a complete overhaul of the onshore grid in northern Japan. This creates a multi-billion dollar opportunity for HTLS conductors to upgrade the long-distance AC transmission lines that will carry this power south. Targeted reconductoring of these specific, congested corridors is a high-value application with strong political and financial backing.

Disaster Resilience and Grid Hardening

Japan's susceptibility to natural disasters presents a unique opportunity. There is a growing national focus on "grid hardening"making the transmission system more resilient to earthquakes, typhoons, and tsunamis. HTLS conductors, often with stronger cores (like composite or Invar), can be positioned not just as capacity-enhancers but as critical components for building a more robust and reliable grid that can better withstand and rapidly recover from catastrophic events.

Trends in the Japan High Temperature and Low Sag (HTLS) Conductor Market

Adoption of Low-Sag Metal-Based Conductors

While composite cores are gaining ground, there is a strong trend in Japan towards the adoption of metal-based HTLS solutions like Gap-type ACSR (G(Z)ACSR) and Aluminum Conductor Invar Reinforced (ACIR). These conductors offer proven, reliable low-sag performance at high temperatures and can be more readily accepted within existing JIS frameworks and utility engineering practices, providing a lower-risk path to capacity upgrades.

Development of High-Capacity Interconnections

A clear trend is the concentration of HTLS deployment on major inter-regional trunk lines. Projects identified in the OCCTO Grid Reinforcement Plan, such as the Hokkaido-Honshu HVDC link and its associated AC lines, and the 50/60Hz frequency converter stations, are the focal points for investment. This trend moves HTLS adoption from niche applications to the core of national transmission planning, driving volume and establishing standard use cases.

Japan High Temperature and Low Sag (HTLS) Conductor Market: Research Scope and Analysis

By Conductor Type Analysis

The Aluminum Conductor Composite Core (ACCC) segment is projected to lead the Japan HTLS Conductor Market, capturing a significant share in 2026. This leadership is driven by the specific demands of upgrading Japan's long-distance, high-capacity trunk lines, particularly those connecting renewable-rich regions to major load centers. Utilities facing severe constraints on existing rights-of-way require a conductor like ACCC, which offers a step-change in capacity (up to double) with near-zero sag, thanks to its lightweight carbon/glass fiber core. Its superior performance in high-temperature operation (up to 180°C) while maintaining critical ground clearance makes it ideally suited for maximizing the potential of existing tower lines in densely populated or geographically challenging areas.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Japanese market's focus on offshore wind integration, where power from northern islands must be transmitted over long distances, aligns perfectly with ACCC's low-loss, high-capacity characteristics. Transmission planners, under pressure from OCCTO to rapidly increase throughput on key interties, are increasingly specifying composite core solutions for their proven ability to deliver the highest capacity gain per dollar invested in existing infrastructure.

While well-established solutions like Gap-type ACSR (G(Z)ACSR) and Thermal-Resistant Aluminum Alloy Conductor (TACSR/ZTACSR) maintain a strong presence due to their reliability and familiarity within Japanese utilities, ACCC is gaining momentum. As the demand for maximum capacity enhancement intensifies and the track record of composite conductors grows, the ACCC segment is poised to maintain its leading position, supported by ongoing material innovations and successful pilot projects in the Japanese grid.

By Material Analysis

Composite core materials are expected to dominate the material segment in the Japan market, favored for their unmatched strength-to-weight ratio and superior thermal stability. The critical need to increase capacity on existing towers without adding structural load is the primary driver. For upgrades on long-span river crossings or lines in mountainous areas, the lightweight nature of composite cores simplifies installation and reduces stress on aging tower structures, a key advantage in Japan's geography.

Composite core-based conductors provide the highest ampacity increase with the least amount of thermal sag, directly addressing the capacity bottlenecks on trunk lines identified by OCCTO. This allows for a significant boost in power transfer from new offshore wind farms without the need for costly and time-consuming tower reinforcement or replacement. Their resistance to corrosion is also highly valued in Japan's coastal and industrial environments.

Although steel-reinforced and specialized alloy-based conductors (like Invar) remain relevant, particularly for applications where their specific properties are required or where a more incremental upgrade is acceptable, their performance at elevated temperatures is limited compared to composites. As Japan pursues aggressive grid expansion targets to meet its 2030 and 2050 goals, composite core materials are projected to maintain their dominant position due to their superior technical capabilities and long-term economic benefits.

By Voltage Level Analysis

High Voltage (HV) and Extra High Voltage (EHV) transmission applications are anticipated to dominate the voltage level segment in Japan. These voltage levels form the backbone of the inter-regional transmission system, connecting major generation sourcesincluding future offshore wind clustersto the main load centers like Tokyo, Nagoya, and Osaka. The critical lines identified for reinforcement in OCCTO's national plan are predominantly at the 187 kV, 275 kV, and 500 kV levels.

HTLS deployment at these voltages is paramount because it directly addresses the core strategic challenge of interregional power transfer. Upgrading an EHV line with HTLS technology provides a massive increase in bulk power transfer capability, effectively relieving congestion on the nation's most important arteries. These projects are complex and capital-intensive, but they deliver the greatest impact on national grid capacity and renewable integration.

While lower voltage (MV) distribution upgrades occur for local load growth and distributed generation, the HV and EHV segments will continue to lead in terms of market value and strategic importance. The direct link between upgrading these high-voltage networks and achieving national energy policy targets ensures their continued dominance in the HTLS market over the forecast period.

By Application Analysis

Grid reconductoring and capacity upgrade applications are forecasted to overwhelmingly dominate the application segment. This dominance is a direct reflection of Japan's fundamental grid challenge: the need to significantly increase transmission capacity in a country where building new lines is exceptionally difficult, slow, and expensive. Reconducting existing rights-of-way with HTLS conductors is the most viable and practical solution.

Transmission owners like J-POWER and the major utilities are utilizing HTLS reconductoring as the primary tool to execute the OCCTO Grid Reinforcement Plan. By replacing conductors on existing lines, they can achieve the mandated capacity increases on interties like the Hokkaido-Honshu link within a fraction of the time and cost of a new greenfield project. This application directly enables the interconnection of queued renewable projects and strengthens the resilience of the grid backbone.

While new power transmission projects (e.g., for new power plants) and renewable energy grid integration are specific use cases, they are almost always achieved through the overarching application of reconductoring existing lines. As Japan continues its multi-decade effort to build a 21st-century grid atop a 20th-century infrastructure, the reconductoring and capacity upgrade segment will remain the primary driver of HTLS market revenue.

By End-Use Industry Analysis

The electric utilities sector, encompassing the ten general electric utilities and J-POWER, is expected to dominate the end-use segment. These entities own and operate the vast majority of Japan's high-voltage transmission infrastructure and are directly responsible for executing the national grid reinforcement plans mandated by METI and coordinated by OCCTO.

Their procurement of HTLS conductors is driven by a combination of factors: regulatory compliance with renewable integration targets, the need to ensure grid stability and reliability in a liberalizing market, and long-term asset management strategies. As investor-owned utilities with a public service obligation, they are the primary channel through which government policy is translated into tangible infrastructure projects, from Hokkaido to Kyushu.

While independent power producers (IPPs) and renewable energy developers may contribute to demand through generator interconnection facilities, their scale is dwarfed by the major utilities' systematic, multi-year programs to upgrade their core transmission assets. The electric utilities' central role in Japan's power system makes them, and will continue to make them, the largest and most influential end-users in the HTLS conductor market.

Japan High Temperature and Low Sag (HTLS) Conductor Market Report is segmented on the basis of the following:

By Conductor Type

- Aluminum Conductor Composite Core (ACCC)

- Aluminum Conductor Composite Reinforced (ACCR)

- Gap-type Aluminum Conductor Steel Reinforced (GAP/G(Z)ACSR)

- Aluminum Conductor Invar Reinforced (ACIR)

- Aluminum Conductor Steel Supported (ACSS)

- Thermal-Resistant Aluminum Alloy Conductor (TACSR/ZTACSR)

- Other Conductor Type

By Material

- Aluminum Conductors

- Composite Core Conductors

- Steel-Reinforced Conductors

- Alloy-Based Conductors

- Other Material

By Voltage Level

- Low Voltage (LV)

- Medium Voltage (MV)

- High Voltage (HV)

- Extra High Voltage (EHV)

By Application

- Power Transmission

- Power Distribution

- Renewable Energy Grid Integration

- Grid Reconductoring / Capacity Upgrade

- Other Application

By End-Use Industry

- Electric Utilities

- Renewable Energy Integration

- Oil & Gas

- Mining & Metal Processing

- Railways & Transportation

- Other End-Use Industry

Impact of Artificial Intelligence on Japan's High Temperature and Low Sag (HTLS) Conductor Market

- AI-Enhanced Composite Core Engineering: Carbon fiber composite cores, often designed with AI-assisted modeling, provide the high strength and minimal thermal expansion required to maximize capacity on Japan's existing transmission towers without structural reinforcement.

- Advanced Metallurgy for High-Temperature Alloys: Heat-resistant aluminum-zirconium alloys are crucial for HTLS conductors, enabling continuous operation at elevated temperatures (150°C-210°C) to handle peak loads from variable renewable sources without degradation.

- Gap-Type Conductor Technology for Sag Control: This design, where aluminum strands are mechanically and electrically separated from the steel core, allows for independent thermal expansion, ensuring minimal sag at high temperatures, a key feature for retrofitting lines in Japan's dense urban and complex terrain.

- Protective Coating Technologies for Longevity: Advanced coatings are critical for extending the lifespan of conductors in Japan's diverse environments, from coastal salt spray to industrial pollution, reducing long-term maintenance needs.

- AI-Powered Conductor Design and Modeling: Computational modeling and finite element analysis, accelerated by AI, are used to optimize stranding patterns, core geometry, and material combinations for maximum performance and reliability under Japan's specific seismic and weather conditions.

Japan High Temperature and Low Sag (HTLS) Conductor Market: Competitive Landscape

The Japan HTLS Conductor Market is characterized by a mix of dominant domestic wire and cable giants and specialized international technology providers. Japanese heavyweights like Sumitomo Electric Industries, Furukawa Electric, and Fujikura Ltd. leverage their deep engineering expertise, long-standing relationships with domestic utilities, and mastery of materials science to offer a range of HTLS solutions, often based on advanced alloys and Gap-type designs.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

International players, particularly CTC Global with its ACCC conductor, are actively collaborating with Japanese utilities and trading houses to introduce advanced composite core technologies, often targeting the most demanding, high-capacity upgrade projects. These partnerships are crucial for navigating the stringent technical approval processes and established supply chains in Japan.

Traditional full-line manufacturers and specialized suppliers, both domestic and international (like Prysmian and Nexans), compete for project tenders. Meanwhile, materials science companies, including carbon fiber manufacturers like Toray Industries (a Japanese leader), play a vital strategic role in the upstream supply chain for composite core conductors, providing a potential advantage for domestically-integrated solutions.

Some of the prominent players in the Japan High Temperature and Low Sag (HTLS) Conductor Market are:

- Sumitomo Electric Industries, Ltd.

- Furukawa Electric Co., Ltd.

- Fujikura Ltd.

- SWCC Showa Holdings Co., Ltd.

- Hitachi Metals, Ltd. / Proterial, Ltd.

- Mitsubishi Cable Industries, Ltd.

- VISCAS Corporation

- J-POWER Systems Corporation

- CTC Global Corporation

- Prysmian S.p.A.

- Nexans S.A.

- LS Cable & System Ltd.

- Southwire Company, LLC

- Lamifil N.V.

- Hengtong Group

- ZTT International Limited

- Midal Cables Ltd.

- APAR Industries Limited

- Sterlite Power

- Other Key Players

Recent Developments in Japan High Temperature and Low Sag (HTLS) Conductor Market

- March 2025: Sumitomo Electric Industries, Ltd. announced the successful completion of a demonstration project using its new Gap-type ultra-heat-resistant conductor on a transmission line in a mountainous region of Japan, validating its sag performance under heavy load conditions.

- January 2025: Furukawa Electric Co., Ltd. was selected by a major Japanese utility to supply Aluminum Conductor Invar Reinforced (ACIR) for a critical grid upgrade project aimed at increasing transfer capacity from a new offshore wind farm connection point.

- October 2024: CTC Global Corporation expanded its collaboration with a Japanese trading house to promote its ACCC conductor to utilities nationwide, focusing on its application for reconductoring key interties identified in the OCCTO grid reinforcement plan.

- July 2024: Fujikura Ltd. announced the development of a next-generation high-strength, heat-resistant aluminum alloy conductor, leveraging its material science expertise to improve sag characteristics and ampacity for the domestic market.

- April 2024: J-POWER (Electric Power Development Co., Ltd.) began a reconductoring project on a section of its trunk line network using advanced HTLS conductors to enhance grid resilience and prepare for increased power flows from northern Japan.

- February 2024: The New Energy and Industrial Technology Development Organization (NEDO) launched a new research program featuring a consortium of universities and cable manufacturers, including Sumitomo Electric and Furukawa, to develop digital twin technology for monitoring the real-time performance of HTLS conductors.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 122.2 Mn |

| Forecast Value (2035) |

USD 221.7 Mn |

| CAGR (2026–2035) |

6.8% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Conductor Type (Aluminum Conductor Composite Core (ACCC), Aluminum Conductor Composite Reinforced (ACCR), Gap-type Aluminum Conductor Steel Reinforced (GAP/G(Z)ACSR), Aluminum Conductor Invar Reinforced (ACIR), Aluminum Conductor Steel Supported (ACSS), Thermal-Resistant Aluminum Alloy Conductor (TACSR/ZTACSR), Other Conductor Type), By Material (Aluminum Conductors, Composite Core Conductors, Steel-Reinforced Conductors, Alloy-Based Conductors, Other Material), By Voltage Level (Low Voltage (LV), Medium Voltage (MV), High Voltage (HV), Extra High Voltage (EHV)), By Application (Power Transmission, Power Distribution, Renewable Energy Grid Integration, Grid Reconductoring / Capacity Upgrade, Other Application), and By End-Use Industry (Electric Utilities, Renewable Energy Integration, Oil & Gas, Mining & Metal Processing, Railways & Transportation, Other End-Use Industry). |

| Country Coverage |

Japan |

| Prominent Players |

Sumitomo Electric Industries, Ltd., Furukawa Electric Co., Ltd., Fujikura Ltd., SWCC Showa Holdings Co., Ltd., Hitachi Metals, Ltd. / Proterial, Ltd., Mitsubishi Cable Industries, Ltd., VISCAS Corporation, J-POWER Systems Corporation, CTC Global Corporation, Prysmian S.p.A., Nexans S.A., LS Cable & System Ltd., Southwire Company, LLC, Lamifil N.V., Hengtong Group, ZTT International Limited, Midal Cables Ltd., APAR Industries Limited, Sterlite Power, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Japan High Temperature and Low Sag (HTLS) Conductor Market?

▾ The Japan HTLS Conductor Market size is estimated to have a value of USD 122.2 million in 2026 and is expected to reach USD 221.7 million by the end of 2035.

What is the growth rate in the Japan High Temperature and Low Sag (HTLS) Conductor Market?

▾ The market is growing at a CAGR of 6.8 percent over the forecasted period of 2026-2035.

Who are the key players in the Japan High Temperature and Low Sag (HTLS) Conductor Market?

▾ Some of the major key players in the Japan HTLS Conductor Market are Sumitomo Electric Industries, Furukawa Electric, Fujikura Ltd., CTC Global Corporation, J-POWER Systems, Prysmian, and many others.