What is the Japan In Vitro Diagnostics (IVD) Market Size?

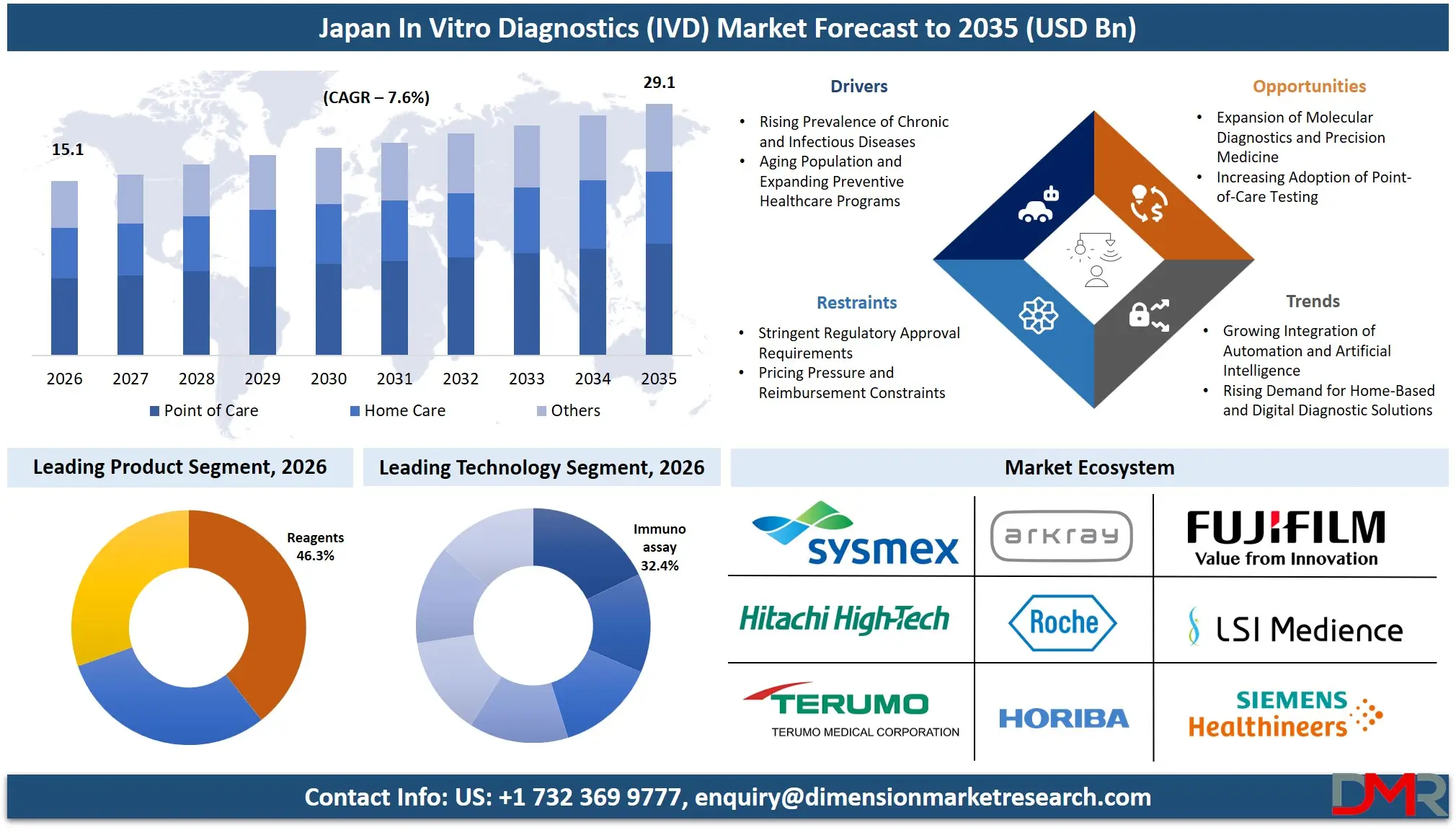

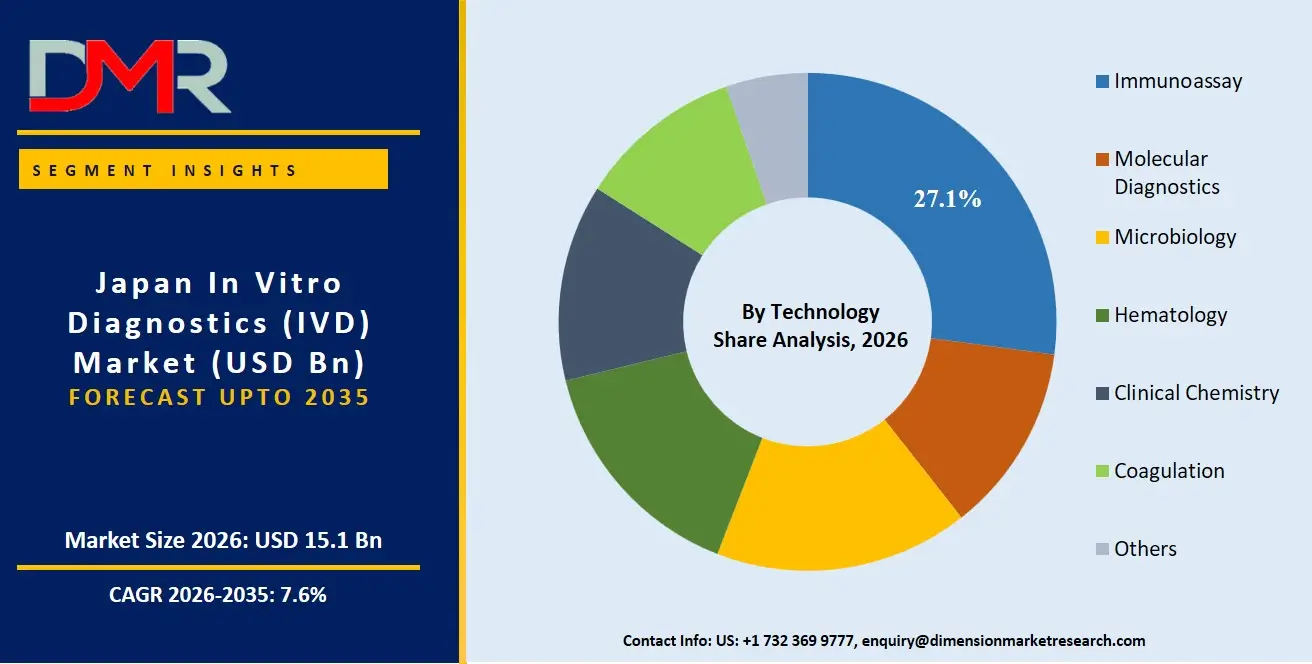

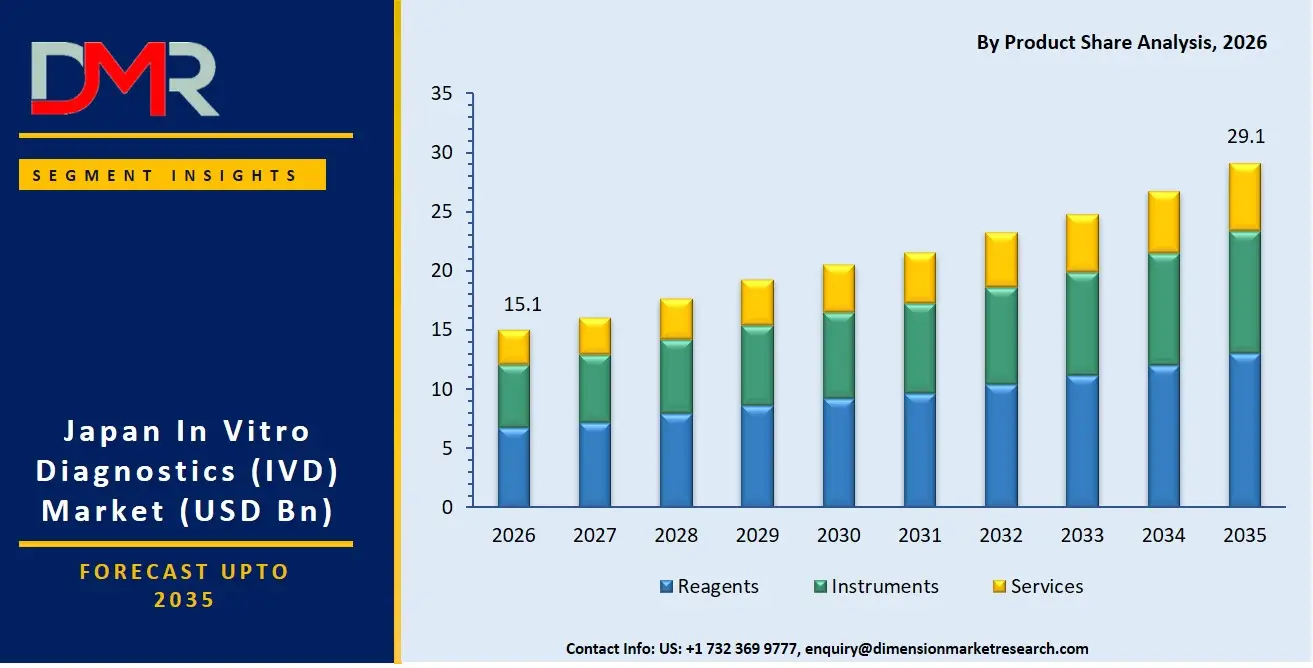

The Japan In Vitro Diagnostics (IVD) Market is expected to reach a value of USD 15.1 billion in 2026, and it is further anticipated to reach USD 29.1 billion by 2035, growing at a CAGR of 7.6% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The IVD market in Japan is experiencing robust expansion, driven by the country's universal healthcare coverage, a super-aging society, and its position as a pioneer in diagnostic technology innovation. The market encompasses a wide array of products and services used to analyze biological specimens, ranging from routine clinical chemistry reagents to advanced molecular diagnostics and next-generation sequencing platforms. The escalating need for early disease detection, personalized medicine, and efficient management of chronic conditions is catalyzing demand across hospital laboratories, independent reference labs, and point-of-care settings. The integration of artificial intelligence and digital pathology is further revolutionizing diagnostic accuracy and workflow efficiency.

Key Takeaways

- Market Size & Forecast: The Japanese IVD market, valued at USD 15.1 billion in 2026, is projected to surge to USD 29.1 billion by 2035. This growth is fueled by high laboratory testing volumes and the rapid adoption of automated, high-throughput systems.

- Growth Rate & Outlook: The market will register a steady CAGR of 7.6%, attributed to the clinical urgency stemming from an aging demographic, the proliferation of decentralized testing, and continuous advancements in biomarker discovery.

- Primary Growth Drivers: Critical growth drivers include the high prevalence of age-related cancers and cardiovascular ailments, government-backed initiatives for infectious disease surveillance, and the shift toward precision oncology with companion diagnostics.

- Key Market Trends: Dominant trends involve the decentralization of care through sophisticated point-of-care devices, the application of liquid biopsy for non-invasive cancer genomic profiling, and the integration of AI-driven algorithms into laboratory automation and imaging systems.

- By Technology Analysis: Immunoassay technology dominates the routine testing landscape due to its established role in detecting a wide spectrum of biomarkers for cancer, cardiac, and infectious diseases, while molecular diagnostics is the fastest-growing segment, driven by PCR and NGS for pathogen identification and genetic analysis.

- By Application Analysis: The infectious disease testing application maintains a commanding market share, reinforced by ongoing respiratory disease monitoring post-pandemic, alongside significant growth in oncology testing for early tumor marker detection and therapy selection.

What is the In Vitro Diagnostics (IVD)?

In vitro diagnostics refers to medical devices and consumables that perform tests on samples taken from the human body such as blood, urine, or tissue to provide critical information for disease screening, diagnosis, prognosis, and treatment monitoring. Unlike imaging or invasive procedures, IVDs function outside the body in vitro (in glass). This field ranges from simple self-test kits used in home care settings to complex genomic sequencers in reference laboratories. In Japan, IVDs are integral to the healthcare continuum, enabling clinical decision-making from primary care clinics to specialized university hospital centers.

Use Cases

- Management of Lifestyle-Related Diseases: Public and private hospitals utilize enzymatic assay reagents on automated clinical chemistry analyzers to perform liver function tests and lipid profiles for the systematic management of metabolic syndrome, a key focus of Japan's national health program.

- Cancer Genomic Profiling: Reference laboratories deploy NGS systems to conduct comprehensive genetic cancer testing on non-small cell lung carcinoma biopsy samples, identifying actionable mutations like EGFR to match patients with approved tyrosine kinase inhibitor therapies.

- Point-of-Care Glycemic Control: Home healthcare providers and outpatient clinics depend on portable blood glucose monitoring devices and HbA1c testing cartridges to enable real-time glycemic control in the vast Japanese diabetic patient population.

- Preventative Infectious Disease Screening: Independent diagnostic laboratories employ high-sensitivity chemiluminescence immunoassays for viral testing, screening donated blood for Hepatitis B, Hepatitis C, and HIV to maintain Japan's safe blood supply chain.

How AI is Transforming the In Vitro Diagnostics (IVD) Market?

The impact of AI on the Japanese IVD market is revolutionizing digital pathology, predictive quality control, and clinical decision support. Machine learning algorithms are now embedded in laboratory automation systems to perform automated urine sediment analysis and flag abnormal leukocyte differentials from complete blood count (CBC) data, reducing manual review time in high-throughput hematology workflows. AI-driven bioinformatics pipelines are essential for interpreting the massive datasets generated by NGS, rapidly aligning genomic variants against clinical databases to generate oncologist-friendly reports. Furthermore, predictive algorithms analyze real-time data from calibrators and controls to anticipate reagent lot failures and system malfunctions before they impact patient results, ensuring uninterrupted diagnostic service in mega-hospital laboratories.

Market Dynamics

Key Drivers in the Japan In Vitro Diagnostics (IVD) Market

Rising Prevalence of Chronic and Infectious Diseases

Japan's growing burden of chronic diseases such as diabetes, cardiovascular disorders, cancer, and kidney disease, along with continued monitoring of infectious diseases, is significantly increasing demand for in vitro diagnostics. Early disease detection has become a healthcare priority to improve treatment outcomes and reduce long-term medical costs. Healthcare providers are expanding routine diagnostic screening programs, while hospitals and laboratories continue investing in advanced testing technologies. The country's aging population further increases diagnostic testing volumes. These factors collectively strengthen the adoption of molecular diagnostics, immunoassays, and clinical chemistry solutions, making disease prevalence a major driver of Japan's IVD market growth.

Aging Population and Expanding Preventive Healthcare Programs

Japan has one of the world's oldest populations, creating sustained demand for diagnostic testing associated with age-related diseases and routine health monitoring. Government initiatives promoting preventive healthcare encourage regular screenings for cancer, cardiovascular diseases, diabetes, and metabolic disorders. Increasing awareness regarding early diagnosis and personalized treatment also supports higher testing frequency across healthcare facilities. Hospitals, diagnostic laboratories, and clinics continue expanding diagnostic capabilities to meet rising patient demand. The combination of demographic changes, preventive healthcare policies, and increasing life expectancy continues driving long-term growth in Japan's in vitro diagnostics market.

Restraints in the Japan In Vitro Diagnostics (IVD) Market

Stringent Regulatory Approval Requirements

Japan maintains rigorous regulatory standards for approving in vitro diagnostic products to ensure safety, quality, and clinical effectiveness. Manufacturers must complete extensive validation, documentation, and compliance procedures before introducing new diagnostic technologies into the market. These lengthy approval timelines may delay product commercialization and increase development costs. International manufacturers also face additional regulatory adaptation requirements when entering Japan. Although strict regulations enhance patient safety and diagnostic reliability, they may slow innovation adoption and limit rapid market expansion, particularly for emerging molecular diagnostic technologies and advanced testing platforms.

Pricing Pressure and Reimbursement Constraints

Government-controlled healthcare reimbursement policies and periodic revisions to diagnostic reimbursement rates create pricing pressure for IVD manufacturers operating in Japan. Healthcare providers increasingly seek cost-effective diagnostic solutions while maintaining high-quality clinical outcomes. Reduced reimbursement rates can affect profit margins and discourage rapid adoption of premium diagnostic technologies. Diagnostic companies must continuously improve operational efficiency and demonstrate strong clinical value to remain competitive. Balancing affordability with technological innovation remains a significant challenge, limiting revenue growth despite increasing demand for advanced diagnostic testing throughout Japan's healthcare system.

Growth Opportunities in the Japan In Vitro Diagnostics (IVD) Market

Expansion of Molecular Diagnostics and Precision Medicine

Growing adoption of precision medicine creates substantial opportunities for molecular diagnostics across Japan. Healthcare providers increasingly utilize genetic testing, companion diagnostics, and biomarker analysis to support personalized treatment decisions, particularly for oncology and rare diseases. Advances in PCR, next-generation sequencing, and genomic technologies continue improving diagnostic accuracy and clinical outcomes. Government support for genomic medicine and precision healthcare further encourages investment in advanced molecular diagnostic platforms. As personalized healthcare becomes increasingly integrated into clinical practice, molecular diagnostics present strong long-term growth opportunities for Japan's in vitro diagnostics market.

Increasing Adoption of Point-of-Care Testing

Point-of-care diagnostics present significant opportunities by enabling rapid disease detection outside traditional laboratory environments. Hospitals, outpatient clinics, emergency departments, pharmacies, and home healthcare settings increasingly utilize portable diagnostic devices to accelerate clinical decision-making. Technological advancements improve testing accuracy, connectivity, and ease of use while reducing turnaround times. Rising demand for decentralized healthcare, remote patient monitoring, and chronic disease management further supports market expansion. Growing investment in portable diagnostic technologies creates substantial opportunities for manufacturers developing innovative point-of-care testing solutions across Japan's healthcare sector.

Trends in the Japan In Vitro Diagnostics (IVD) Market

Growing Integration of Automation and Artificial Intelligence

Automation and artificial intelligence are transforming diagnostic laboratories across Japan by improving workflow efficiency, reducing manual errors, and increasing testing capacity. Laboratories increasingly deploy automated analyzers, robotic sample handling systems, and AI-powered diagnostic software to enhance operational performance. Digital pathology, intelligent image analysis, and predictive analytics further improve diagnostic accuracy and clinical decision-making. Healthcare providers continue investing in laboratory automation to address workforce shortages and rising testing demand. This growing integration of digital technologies represents a major trend shaping the future development of Japan's in vitro diagnostics market.

Rising Demand for Home-Based and Digital Diagnostic Solutions

Consumer preference for convenient healthcare services is increasing demand for home-based diagnostic testing and digital health integration. Self-testing kits, connected diagnostic devices, and remote patient monitoring solutions enable individuals to manage chronic diseases and routine health assessments from home. Advances in telemedicine and digital healthcare platforms further support remote diagnostics and physician consultation. Aging demographics, increasing healthcare accessibility, and technological innovation continue accelerating adoption of home-based testing solutions. This shift toward decentralized and digitally connected diagnostics represents one of the most important emerging trends in Japan's in vitro diagnostics market.

Research Scope and Analysis

The Japan In Vitro Diagnostics (IVD) market is segmented by product, technology, test location, application, and end user. It includes reagents, instruments, services, immunoassays, molecular diagnostics, microbiology, hematology, clinical chemistry, coagulation, point-of-care testing, infectious disease, oncology, diabetes, laboratories, hospitals, home care, and other healthcare settings, supporting comprehensive diagnostic services.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Product Analysis

Reagents is projected to dominate the Japan In Vitro Diagnostics (IVD) market because they are consumed repeatedly during every diagnostic procedure, creating continuous demand across hospitals, diagnostic laboratories, and research institutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Unlike instruments, which are purchased periodically, reagents require frequent replenishment for routine clinical testing, molecular diagnostics, immunoassays, and clinical chemistry applications. Japan's aging population, increasing chronic disease burden, and expanding preventive healthcare programs further drive testing volumes. Technological advancements in assay development and high-throughput laboratory automation also increase reagent utilization. Consequently, recurring consumption, broad clinical application, and stable replacement demand make reagents the dominant product segment in Japan's IVD market.

By Technology Analysis

Immunoassay is anticipated to dominate the technology segment owing to its extensive use in routine clinical diagnostics, disease screening, therapeutic monitoring, and preventive healthcare. Japanese hospitals and laboratories rely heavily on immunoassays for detecting infectious diseases, cardiac biomarkers, hormones, tumor markers, and autoimmune disorders with high sensitivity and efficiency. Automated immunoassay analyzers support rapid processing of large testing volumes while maintaining diagnostic accuracy. Rising demand for early disease detection, an aging population, and expanding health screening programs continue strengthening this segment. Its versatility across multiple medical specialties ensures immunoassay remains the leading diagnostic technology within Japan's IVD market.

By Test Location Analysis

Point-of-care testing is poised to dominate the test location segment because it provides rapid diagnostic results directly at hospitals, clinics, emergency departments, and outpatient facilities. Healthcare providers increasingly adopt point-of-care diagnostics to support immediate clinical decision-making, improve patient outcomes, and reduce laboratory turnaround times. The growing prevalence of chronic diseases, infectious disease surveillance, and demand for decentralized healthcare services further accelerate adoption. Technological improvements have enhanced the accuracy, portability, and ease of use of point-of-care diagnostic devices. These advantages make point-of-care testing the dominant testing location across Japan's evolving healthcare and diagnostic ecosystem.

By Application Analysis

Infectious disease testing is expected to dominate the application segment due to continuous demand for diagnosing respiratory infections, hepatitis, influenza, tuberculosis, HIV, and emerging viral diseases. Japan maintains extensive public health surveillance programs and routine infectious disease screening across hospitals, laboratories, and healthcare facilities. Increased awareness regarding early diagnosis, infection prevention, and outbreak preparedness has strengthened testing volumes nationwide. Molecular diagnostics and immunoassays further improve the speed and accuracy of infectious disease detection. Combined with strong government support for disease surveillance and preventive healthcare, infectious disease diagnostics continue accounting for the largest application share in Japan's IVD market.

By End User Analysis

Laboratories is projected to dominate the end-user segment because they perform the majority of routine, specialized, and high-volume diagnostic testing across Japan. Independent diagnostic laboratories and reference laboratories possess advanced automation systems, skilled personnel, and sophisticated analytical capabilities that enable efficient processing of diverse diagnostic tests. Hospitals frequently outsource specialized testing to these laboratories to improve efficiency and reduce operational costs. Rising demand for preventive health checkups, chronic disease monitoring, and precision medicine continues increasing laboratory testing volumes. Their central role in delivering accurate, standardized, and cost-effective diagnostic services ensures laboratories remain the dominant end-user segment in Japan's IVD market.

The Japan In Vitro Diagnostics (IVD) Market Report is segmented on the basis of the following:

By Product

- Reagents

- Assay Kits

- Calibrators & Controls

- Antibodies

- Enzymes & Buffers

- Other Reagents

- Instruments

- Analyzers

- PCR Systems

- Sequencing Systems

- Point-of-Care Devices

- Laboratory Automation Systems

- Services

- Installation & Maintenance

- Calibration Services

- Validation & Quality Assurance

- Training & Technical Support

By Technology

- Immunoassay

- ELISA

- Chemiluminescence Immunoassay (CLIA)

- Fluorescence Immunoassay (FIA)

- Rapid Immunoassays

- Molecular Diagnostics

- PCR

- Next-Generation Sequencing (NGS)

- In Situ Hybridization (ISH)

- Microarray

- Microbiology

- Bacterial Testing

- Viral Testing

- Fungal Testing

- Parasitology

- Hematology

- Complete Blood Count (CBC)

- Hemostasis Testing

- Blood Cell Analysis

- Clinical Chemistry

- Electrolyte Testing

- Liver Function Tests

- Kidney Function Tests

- Lipid Profile

- Coagulation

- Prothrombin Time (PT)

- Activated Partial Thromboplastin Time (aPTT)

- D-Dimer Testing

- Fibrinogen Testing

- Others

By Test Location

- Point of Care

- Home Care

- Others

By Application

- Infectious Disease

- COVID-19

- Influenza

- Tuberculosis

- Hepatitis

- HIV

- Diabetes

- Blood Glucose Monitoring

- HbA1c Testing

- Oncology

- Tumor Marker Testing

- Companion Diagnostics

- Genetic Cancer Testing

- Nephrology

- Kidney Function Testing

- Urinalysis

- Cardiology

- Cardiac Biomarker Testing

- Lipid Profile Testing

- Drug Testing

- Drugs of Abuse Testing

- Therapeutic Drug Monitoring

- Autoimmune Disease

- ANA Testing

- Rheumatoid Arthritis Testing

- Autoantibody Testing

- Others

By End User

- Laboratories

- Independent Diagnostic Laboratories

- Reference Laboratories

- Hospitals

- Public Hospitals

- Private Hospitals

- Home Care

- Self-Testing

- Home Healthcare Providers

- Others

Competitive Landscape

The competitive landscape of the Japan IVD market is dominated by a strategic duopoly of global in-vitro diagnostic titans and deeply entrenched Japanese conglomerates, alongside a vibrant tier of specialized biotechnology firms. Core competitive differentiation has shifted from pure reagent sales to providing integrated ecosystem solutions that encompass high-throughput instruments, AI-powered middleware, and comprehensive laboratory management services. Strategic alliances between Japanese pharmaceutical companies and diagnostic manufacturers are critical for co-developing companion diagnostics that secure the regulatory approval and NHI reimbursement for high-value oncology biologics. Domestic companies leverage their expansive direct sales forces and service networks, which provide rapid installation, maintenance, and calibration services to hospital laboratories, a critical advantage when ensuring minimal downtime in 24/7 automated testing lines. Intellectual property in biomarker discovery, proprietary signal amplification technologies for ultrasensitive CLIA, and advanced liquid biopsy NGS panel bioinformatics are key differentiators in the high-growth molecular diagnostics segment.

Some of the prominent players in the Japan In Vitro Diagnostics (IVD) Market are:

- Sysmex Corporation

- Fujifilm Holdings Corporation

- Terumo Corporation

- Hitachi High-Tech Corporation

- ARKRAY, Inc.

- HORIBA, Ltd.

- LSI Medience Corporation

- BML, Inc.

- Roche Diagnostics K.K.

- Abbott Japan LLC

- Siemens Healthineers Japan

- Danaher Corporation

- QIAGEN N.V.

- bioMérieux SA

- Becton, Dickinson and Company

- Thermo Fisher Scientific Inc.

- Agilent Technologies, Inc.

- Bio-Rad Laboratories, Inc.

- Werfen S.A.

- Sekisui Medical Co., Ltd.

- Other Key Players

Recent Developments

- March 2026: Fujirebio obtained CE marking for its fully automated Lumipulse® G NfL Blood assay, expanding its neurodegenerative disease diagnostics portfolio with advanced blood-based biomarker testing for clinical laboratories.

- February 2026: Fujirebio and Sysmex Corporation entered a global sales collaboration for dementia testing, expanding the availability of automated immunoassay systems and neurological biomarker assays across international clinical laboratory markets.

- January 2026: Sysmex Corporation announced a new medium-term growth strategy focused on expanding laboratory automation, precision diagnostics, digital healthcare, and advanced in vitro diagnostic technologies to strengthen its leadership in clinical diagnostics.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 15.1 Bn |

| Forecast Value (2035) |

USD 29.1 Bn |

| CAGR (2026–2035) |

7.6% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Product, By Technology, By Test Location, By Application, By End User |

| Regional Coverage |

Japan |

Frequently Asked Questions

How big is the Japan In Vitro Diagnostics (IVD) Market?

▾ The Japan IVD market is poised to be valued at USD 15.1 billion in 2026 and is projected to reach USD 29.1 billion by 2035, driven by the systemic testing needs of a hyper-aging population and the clinical transition toward high-sensitivity, personalized diagnostic algorithms.

What is the CAGR of the Japan IVD Market from 2026 to 2035?

▾ The market is expected to grow at a steady CAGR of 7.6% from 2026 to 2035, reflecting the dual dynamics of stable high-volume routine testing and premium-priced growth in next-generation sequencing and companion diagnostics.

What factors are driving the growth of the Japan IVD Market?

▾ Key drivers include Japan’s mandatory universal health screening programs, the rapid clinical adoption of digital molecular pathology and liquid biopsy, and regulatory harmonization that accelerates companion diagnostic approval alongside targeted pharmaceuticals.

What are the major trends in the Japan IVD Market?

▾ Major trends include the migration from tissue-based to blood-based genomic testing for cancer, the integration of AI across automated hematology and microbiology workflows, and the expansion of community-based POC testing to reduce hospital admission burdens.

Who are the key players in the Japan IVD Market?

▾ Key players in the Japan IVD Market include Sysmex Corporation, Roche Diagnostics, Abbott Japan, Siemens Healthineers, H.U. Group Holdings, Fujirebio, and Thermo Fisher Scientific, who drive innovation through continuous reagent development, integrated instrument placement, and comprehensive laboratory IT solutions.

How is the Japan IVD Market segmented?

▾ The market is segmented by Product, Technology, Test Location, Application, and End User.