Market Overview

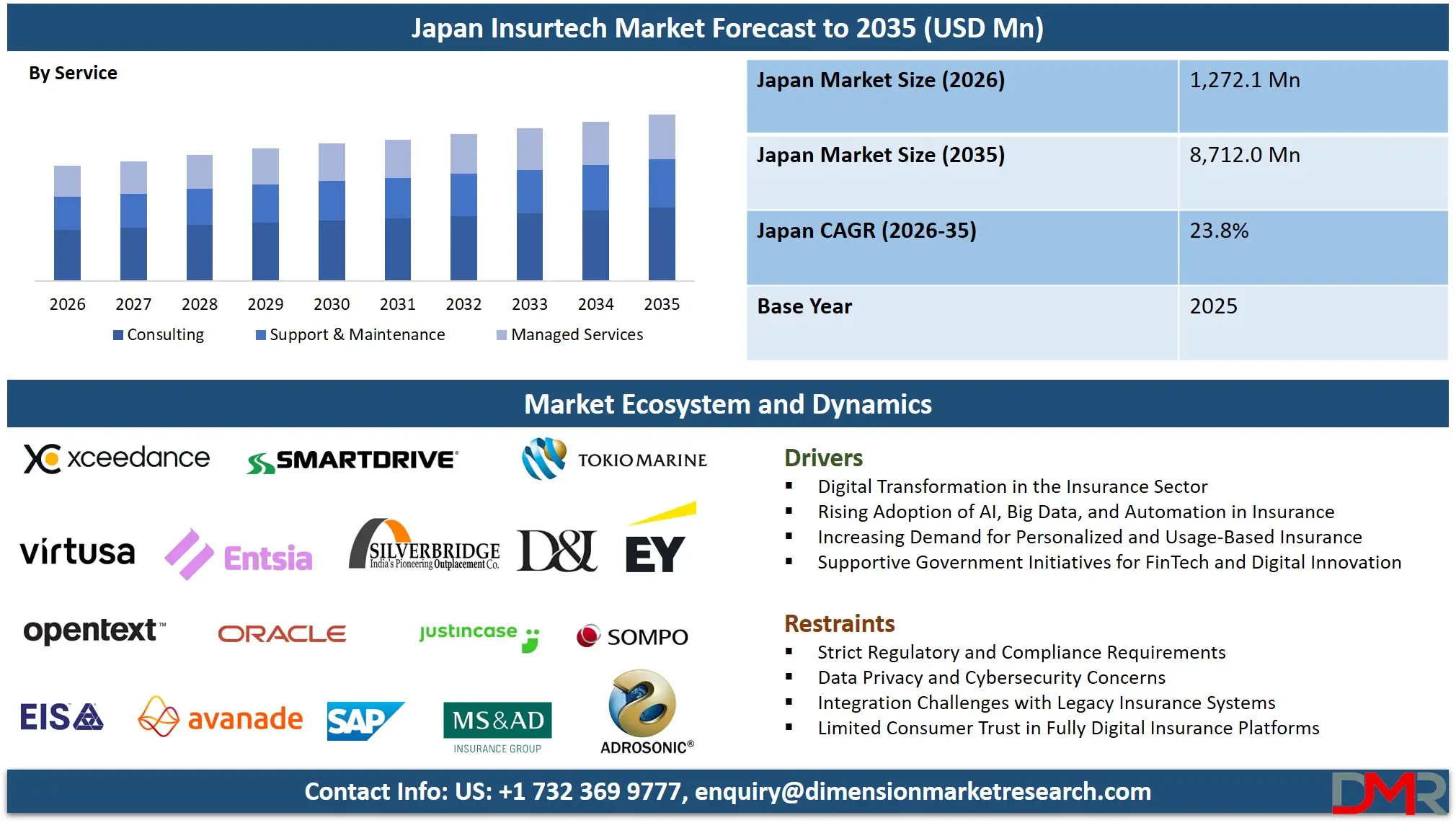

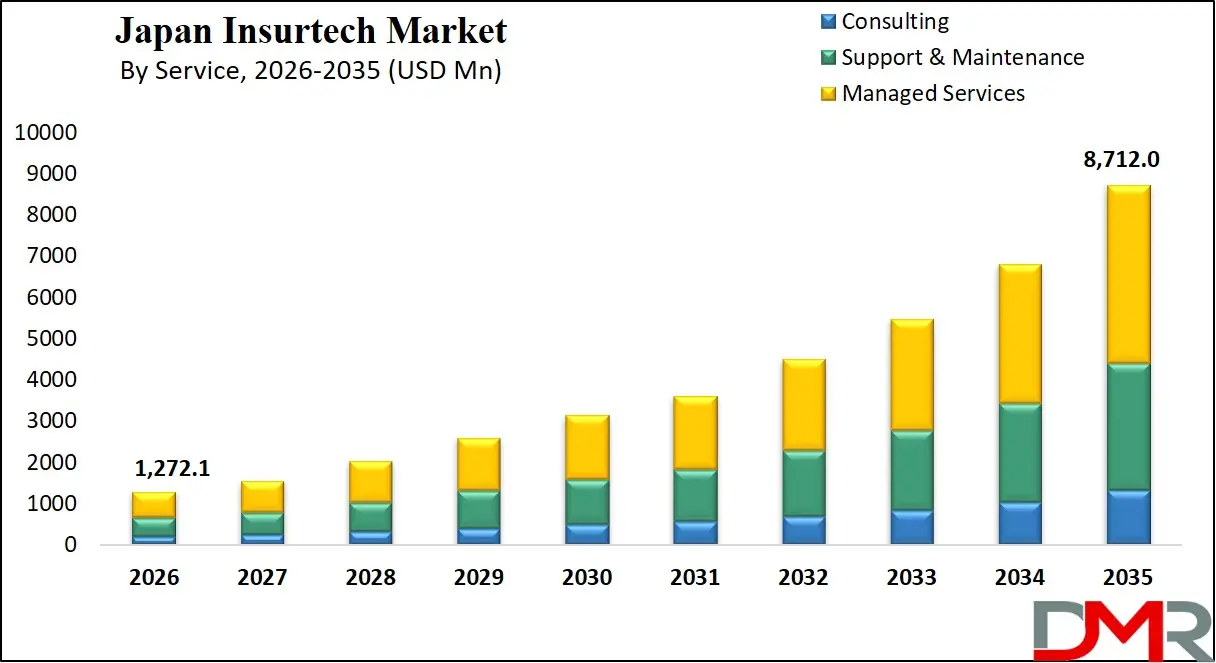

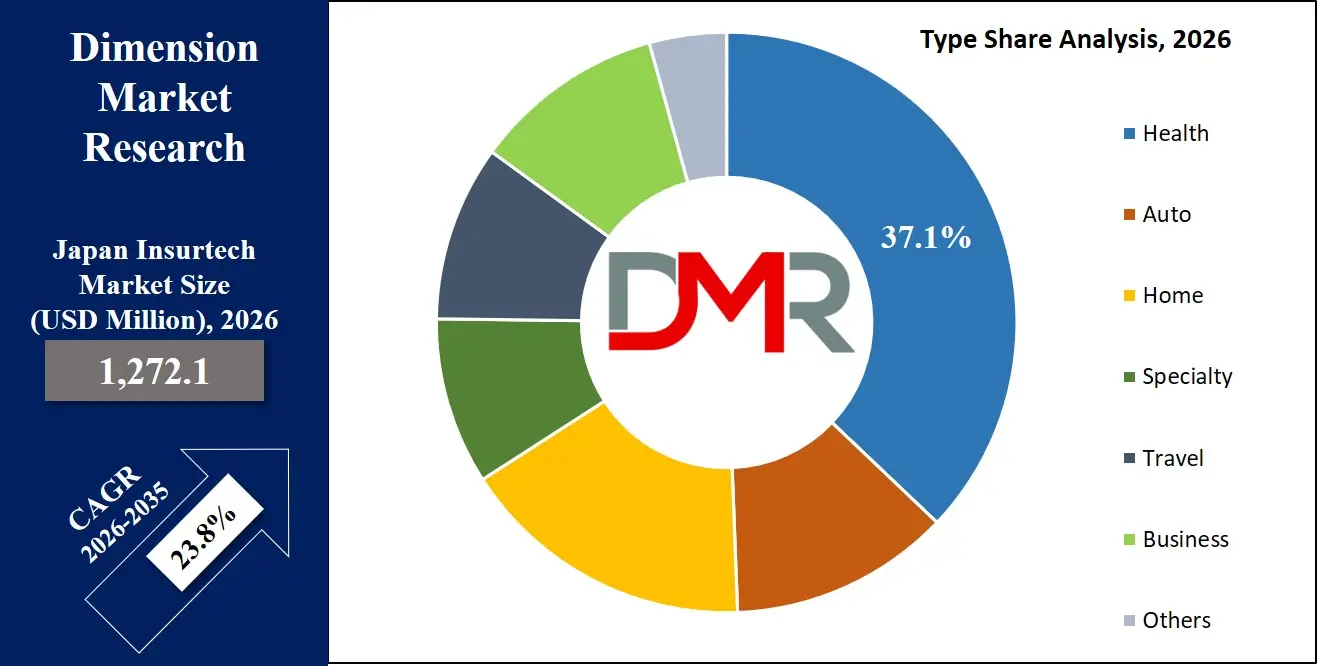

The Japan Insurtech market size is expected to reach a value of USD 1,272.1 million in 2026, and it is further anticipated to reach a market value of USD 8,712.0 million by 2035 at a CAGR of 23.8%.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The insurtech market is an increasingly vital part of Japan's financial and technological ecosystem, driven by a confluence of factors including a rapidly aging society, frequent natural disasters, and a government-led push for digital transformation (DX). As one of the world's largest insurance markets, Japan presents a unique landscape where traditional giants are actively partnering with and investing in technology-driven startups to modernize legacy systems, enhance customer experience, and develop new, data-driven products. The sector covers a wide range of activities, from digital-first insurance carriers and on-demand coverage platforms to AI-powered claims processing and IoT-enabled risk prevention services, all aimed at increasing efficiency and meeting the evolving needs of modern consumers and businesses.

Over the last few years, the insurtech market of Japan has witnessed a strategic transition from simple digitization to deep-seated technological integration. Advanced technologies like AI, IoT, and blockchain are being deployed to move beyond basic policy administration, enabling usage-based insurance (UBI), automating complex underwriting processes, and fighting fraud with greater accuracy. The government's "Society 5.0" initiative, which promotes the use of cyber-physical systems to solve social challenges, has created a fertile ground for insurtech solutions that address issues like healthcare accessibility for the elderly and rapid disaster response and claims settlement.

Key trends currently evident within the insurtech arena in Japan include the rise of embedded insurance, where coverage is integrated seamlessly into the purchase of another product or service (like travel insurance with a flight ticket or device insurance with an electronics purchase). Furthermore, the application of telematics in auto insurance, using IoT devices to monitor driving behavior, is gaining traction, offering personalized premiums and promoting safer driving. In the health sector, wearable devices and digital therapeutics are being integrated with insurance policies to incentivize preventive care and healthy lifestyles. The market is also seeing a significant shift toward "Platform as a Service" (PaaS) models, enabling traditional insurers to launch new products faster and more efficiently.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market is consequently witnessing huge opportunities on the back of the Financial Services Agency's (FSA) proactive stance on regulatory reform, encouraging innovation through initiatives like the "Regulatory Sandbox" system. This allows for the testing of new technologies and business models in a controlled environment. The sheer volume of data available from a tech-savvy population and advanced industrial base provides a rich resource for developing sophisticated AI and machine learning models for risk assessment and pricing. Furthermore, the increasing frequency and severity of natural disasters (typhoons, floods, earthquakes) is accelerating the demand for parametric insurance solutions that leverage IoT and big data for rapid, automated payouts based on pre-defined triggers.

Impact of Iran Conflict on the Japan Insurtech Market

- Increased Demand for Cyber Insurance and Digital Risk Solutions: The Iran conflict has heightened fears of cyber warfare and digital attacks targeting financial institutions and businesses. As organizations strengthen cyber resilience, insurtech platforms offering AI-based cyber risk assessment, underwriting automation, and real-time monitoring are witnessing increased demand globally.

- Rising Demand for Advanced Risk Analytics Platforms: Geopolitical tensions are forcing insurers to reassess underwriting models and geopolitical risk exposure. Insurtech solutions using predictive analytics, AI, and big data for risk modeling are gaining importance as insurers evaluate war-related risks, supply chain disruptions, and global economic instability.

- Increase in Insurance Premiums and Digital Claims Management: War-related disruptions in shipping, energy infrastructure, and global trade have increased insurance premiums and risk coverage complexity. Insurtech platforms that automate claims processing, pricing models, and policy management help insurers manage rising claims volumes and operational costs efficiently.

- Short-Term Slowdown in Technology Investments: Rising oil prices and global economic uncertainty from the conflict can reduce discretionary IT and technology spending by enterprises. This may slow short-term investments in new insurtech platforms and digital transformation initiatives across insurance companies and financial institutions.

- Expansion of Political Risk and Specialized Insurance Products: The conflict is increasing global concern about war, terrorism, and geopolitical instability. As a result, insurers are developing specialized insurance products such as political risk, cyber risk, and supply-chain protection, creating new opportunities for insurtech firms to innovate digital underwriting solutions.

Japan Insurtech Market: Key Takeaways

- Market Value: The Japan Insurtech Market size is estimated to have a value of USD 1,272.1 million in 2026 and is expected to reach USD 8,712.0 million by the end of 2035.

- By Type Segment Analysis: Health insurance is anticipated to dominate this segment in this market as it will hold 37.1% of market share in 2026, driven by an aging population and digital health integration.

- By Technology Segment Analysis: Cloud Computing is projected to dominate the technology segment in the Japan Insurtech Market, providing the scalable foundation for all other digital solutions in 2026.

- By Service Segment Analysis: Managed Services is anticipated to dominate the service segment as insurers seek external expertise to run complex, modern IT infrastructure.

- By End-User Segment Analysis: The BFSI (Banking, Financial Services, and Insurance) sector, specifically the insurers themselves, is projected to dominate the end-user segment in the Japan insurtech market in 2026.

- Key Players: Some of the major key players in the Japan Insurtech Market are Tokio Marine Holdings, Sompo Holdings, MS&AD Insurance Group, JustInCase, SmartDrive, D&I, and many others.

- Market Growth Rate: The market is growing at a CAGR of 23.8 percent over the forecasted period.

Japan Insurtech Market: Use Cases

- Usage-Based Auto Insurance (UBI): Telematics devices or smartphone apps monitor driving behavior (speed, braking, time of day) to calculate premiums based on actual risk, rewarding safe drivers with lower rates.

- Parametric Insurance for Natural Disasters: After a major typhoon or earthquake, policyholders with parametric flood or business interruption insurance receive automatic, pre-defined payouts triggered by verifiable data (e.g., wind speed, seismic intensity), bypassing traditional claims adjustment.

- Digital Health Engagement: Insurers partner with fitness app and wearable device companies to offer premium discounts or rewards points for meeting daily step goals, tracking sleep, or maintaining healthy blood pressure levels, encouraging preventive care.

- AI-Powered Claims Processing: An AI-powered system analyzes photos of a damaged car or property, assesses the damage, cross-references the policy, and approves and processes the claim payment in near real-time, drastically reducing turnaround time.

Japan Insurtech Market: Stats & Facts

Financial Services Agency (FSA), Japan

- The Financial Services Agency approved 12 new insurtech-related licenses in 2023 under its fintech innovation and regulatory sandbox framework.

- Japan introduced a new Risk-Based Capital (RBC) regulatory framework for insurers in 2023, replacing the previous solvency margin system.

- The minimum solvency margin ratio required for Japanese insurers is 150% under FSA regulations.

- The average solvency ratio of Japanese life insurers exceeded 220% in 2022, indicating strong capital adequacy in the sector.

- Amendments to the Insurance Business Law introduced ESG disclosure requirements for insurance companies in 2022.

Life Insurance Association of Japan (LIAJ)

- Individual life insurance policies in force in Japan exceeded 112 million in 2023.

- Life insurance premiums accounted for about 72% of Japan's total insurance premiums in 2023.

- Life insurance new business annual premium equivalent totaled approximately USD 25.8 billion in 2022.

- Group life insurance premiums reached about USD 84.7 billion in fiscal year 2022.

- Approximately 89.8% of Japanese households own at least one life insurance policy.

General Insurance Association of Japan (GIAJ)

- Automobile insurance premiums totaled approximately USD 39.3 billion in fiscal year 2022.

- Fire insurance policies in force exceeded 55 million in Japan in 2023.

- The average claim amount for compulsory automobile liability insurance was about USD 3,050 per claim in 2022.

Ministry of Finance, Japan

- The total assets of Japan's insurance industry reached approximately USD 2.9 trillion in 2022.

- Foreign investments by Japanese life insurers totaled about USD 705 billion in 2023.

- Life insurers hold roughly 38% of their investment portfolios in domestic government bonds.

Bank of Japan (BOJ)

- Insurance density in Japan exceeded USD 10,150 per capita in 2021, among the highest globally.

- Japan's general insurance industry ranks among the top five largest globally by gross written premiums.

Japan Insurtech Market: Market Dynamics

Driving Factors in Japan Insurtech Market

"Society 5.0" and Regulatory Support

Japan's national strategic vision, Society 5.0, which aims to solve social problems by integrating cyber and physical spaces, is a powerful growth driver. It actively promotes the use of AI, IoT, and big data in all sectors, including finance and insurance. This is complemented by the Financial Services Agency's (FSA) proactive approach to fostering innovation through regulatory sandboxes and streamlined approval processes for digital-first business models. This supportive environment encourages both startups and established players to invest heavily in insurtech.

Addressing the Challenges of a Super-Aged Society

Japan's rapidly aging population creates a massive and urgent need for more efficient and sustainable healthcare and long-term care insurance solutions. Insurtech offers the tools to meet this challenge. Telemedicine integration, AI-driven analysis of health records for personalized care plans, wearable devices for remote monitoring of the elderly, and platforms that simplify claims for long-term care insurance are all in high demand. This demographic imperative is a non-negotiable driver of innovation and investment in the health insurtech space.

Restraints in Japan Insurtech Market

Legacy System Integration Complexity

The Japanese insurance market is dominated by long-established companies with deeply embedded legacy IT systems. These systems are often complex, costly to maintain, and not designed for the open, API-driven architecture of modern insurtech. Integrating new, agile solutions with these older systems is a major technical and financial hurdle, often slowing down digital transformation initiatives and increasing project risk.

Data Privacy and Regulatory Compliance

Japan has stringent regulations governing the use of personal data, particularly the Act on the Protection of Personal Information (APPI). For insurtech companies, especially those handling sensitive health and location data, navigating these compliance requirements is complex and costly. Ensuring that new AI models, data-sharing agreements, and IoT devices are fully compliant with APPI and FSA guidelines can significantly extend development timelines and create a barrier to entry for smaller, less experienced players.

Opportunities in Japan Insurtech Market

AI-Driven Personalized and Predictive Underwriting

The vast amounts of data available in Japan present an excellent opportunity for using AI and machine learning to move from generalized risk pools to highly personalized underwriting. By analyzing data from wearables, medical records, driving behavior, and even lifestyle choices, insurers can offer hyper-personalized premiums that accurately reflect an individual's risk profile. This also opens the door for predictive risk prevention services, where insurers can proactively warn a driver about a high-risk route or suggest a health check-up, fundamentally changing the relationship from payer to partner.

Expansion of Cyber Insurance and Services

With increasing digitalization across all sectors of the Japanese economy, the threat of cyber-attacks is a top concern for businesses of all sizes. This creates a significant growth opportunity for cyber insurance. The opportunity extends beyond just providing a payout; insurtech solutions can integrate proactive security tools, continuous network monitoring, and incident response services as part of the policy. This value-added, managed services approach to cyber risk is a highly attractive proposition for SMEs, which make up a vast portion of Japan's economy.

Trends in Japan Insurtech Market

Embedded Insurance Ecosystems

The insurtech sector in Japan is seeing a strong trend toward embedded insurance, where coverage is seamlessly integrated into non-insurance platforms. This is driven by the need for frictionless customer experiences. For example, travel insurance is offered at the moment of booking a flight on an airline app, or warranty insurance for a new home appliance is added during the online checkout process at a major retailer like Rakuten. This trend leverages APIs and cloud computing to make insurance an invisible but valuable part of everyday transactions, significantly expanding distribution channels beyond traditional agents.

Platformization of Core Insurance Systems

Traditional Japanese insurance giants are moving away from rigid, monolithic legacy systems toward open, flexible platforms. They are adopting cloud-native, API-first architectures that allow them to "compose" new insurance products by plugging in different microservices for pricing, underwriting, and claims. This "platformization" enables them to partner more easily with nimble insurtech startups, launch new products in weeks instead of months, and adapt quickly to changing market demands, moving toward a truly agile operational model.

Japan Insurtech Market: Research Scope and Analysis

By Type Analysis

Health is projected to dominate the type segment in this market as it will hold 37.1% of market share in 2026. The dominance of Health insurance in the type segment of the Japan Insurtech Market is primarily due to the nation's super-aged society and the government's focus on preventive care and healthcare cost containment. Japan has one of the oldest populations in the world, creating immense pressure on the public health system and a strong demand for supplementary private health insurance. Insurtech is transforming this space by enabling a shift from reactive treatment to proactive wellness management. Startups and established carriers are leveraging data from wearable devices and health apps to offer "Health Promotion" insurance policies. These policies reward policyholders with points or premium discounts for engaging in healthy behaviors, such as walking more, undergoing preventive health screenings, or using digital therapeutics for conditions like hypertension or diabetes.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The technology allows for granular risk assessment and personalized pricing models based on real-time health data, moving beyond traditional age and medical history questionnaires. Furthermore, insurtech solutions are streamlining the notoriously complex claims process for medical expenses, using AI to automate form processing and verification, thereby improving customer satisfaction and reducing administrative overhead for insurers. The COVID-19 pandemic further accelerated this trend, boosting the adoption of telemedicine and digital health services, which are now being seamlessly integrated into insurance offerings. As the population continues to age and the government encourages individuals to take more responsibility for their health, technology-enabled health insurance products will continue to lead the market.

By Technology Analysis

Cloud Computing is projected to dominate the technology segment of the insurtech market in Japan, serving as the essential foundational layer for all other technological innovations. The strategic reliance on cloud infrastructure is driven by its scalability, cost-efficiency, and ability to support the agility required in the modern insurance landscape. Legacy on-premise systems are ill-equipped to handle the massive data flows from IoT devices, the computational demands of machine learning algorithms, or the need for rapid API integrations with partners. Cloud platforms provide the elastic computing power and storage necessary to run these advanced applications.

The dominance of cloud computing is further cemented by the "cloud-first" policies emerging in many large enterprises and the availability of sophisticated, secure cloud services from global providers like AWS, Microsoft Azure, and Google Cloud, which have all made significant investments in Japan. For insurtech startups, the cloud is a non-negotiable enabler, allowing them to launch and scale without massive upfront capital expenditure on IT infrastructure. For incumbents, migrating core systems to the cloud is the first and most critical step in their digital transformation journey. It enables them to break free from vendor lock-in, modernize their application portfolios, and adopt a composable business architecture. Initiatives from the Japanese government to promote the use of cloud services for critical infrastructure, with enhanced security and compliance certifications, are also allaying concerns and encouraging wider adoption. As the bedrock upon which AI, IoT, and blockchain applications are built, cloud computing's position as the dominant technology is unassailable and fundamental to the market's growth.

By Service Analysis

The managed services segment is expected to dominate the service segment in the Japan Insurtech Market. This dominance is driven by a critical shortage of specialized IT talent and the increasing complexity of modern, cloud-based, and AI-driven insurance platforms. Japanese insurers, both large and small, face immense challenges in recruiting and retaining professionals with deep expertise in rapidly evolving fields like data science, cybersecurity, and cloud architecture. Outsourcing the day-to-day management, monitoring, and optimization of these complex systems to specialized third-party providers offers a compelling solution.

Managed services allow insurance companies to focus on their core business—underwriting, product development, and customer relationships—while leaving the technical heavy lifting to experts. This is particularly attractive for tasks like ensuring 24/7 security monitoring and compliance with FSA regulations, managing and tuning AI models for peak performance, and maintaining complex cloud infrastructures. For many mid-tier and smaller insurers, the cost of building an in-house team capable of managing these functions is prohibitive. Furthermore, as insurers move towards a "platform" model, they are effectively treating their technology stack as a product that needs constant professional oversight. The rise of "Insurance-as-a-Service" platforms, where a vendor provides a complete, managed technology stack, is a perfect example of this trend. By providing operational efficiency, enhanced security, and access to top-tier expertise, managed services have become the preferred model for navigating the technological complexities of the modern insurtech landscape in Japan.

By End-User Analysis

The BFSI (Banking, Financial Services, and Insurance) end-user segment anticipated to dominate the Japan insurtech market. While this may seem self-evident, the nature of this dominance is evolving. The primary end-users are the insurance carriers themselves—the large, established firms like Tokio Marine, Sompo, and MS&AD, as well as a growing number of digital-native insurers. These companies are the primary consumers of insurtech solutions, investing heavily to modernize their operations, enhance their product offerings, and improve customer experience. They are the ones purchasing and integrating cloud platforms, AI-powered underwriting tools, and IoT data analytics services. Their immense scale and financial resources make them the most significant market force, driving demand for enterprise-grade solutions.

However, the definition of "end-user" in insurtech is broadening. It now also includes other entities within the BFSI umbrella, such as regional banks that are beginning to partner with insurtechs to offer insurance products to their customer base, and non-bank financial firms looking to diversify into embedded insurance offerings. The dominance of BFSI is reinforced by the sector's acute need for the specific solutions that insurtech provides: more accurate risk modeling for a volatile climate, automated efficiency to counteract the pressures of a shrinking workforce, and personalized products to engage a digitally-savvy customer base. As the core engine of the entire insurance ecosystem, the BFSI sector, and specifically its insurance arm, will remain the dominant end-user, continuously fueling demand for technological innovation.

Japan Insurtech Market Report is segmented on the basis of the following:

By Type

- Health

- Auto

- Home

- Specialty

- Travel

- Business

- Others

By Technology

- Blockchain

- Cloud Computing

- IoT

- Machine Learning

- Robo Advisory

- Others

By Service

- Consulting

- Support & Maintenance

- Managed Services

By End User

- BFSI

- Automotive

- Manufacturing

- Transportation

- Government

- Health

- Retail

- Others

Impact of Artificial Intelligence in Japan Insurtech Market

- Hyper-Personalized Products: AI analyzes individual lifestyle and health data to create "segment-of-one" insurance policies, moving from standardized coverage to dynamic, personalized plans that reflect real-time personal risk profiles.

- Exponential Efficiency Gains: By automating underwriting, claims processing, and fraud detection, AI drastically reduces processing times from days to minutes and cuts operational costs, directly addressing Japan's labor shortages.

- Augmented Human Workforce: AI acts as a "co-pilot" for agents, providing data-driven insights for sales and customer service. This boosts conversion rates and allows humans to focus on complex consultations and empathy-driven tasks.

- Legacy System Modernization: AI is a catalyst for overhauling Japan's outdated "2025 IT legacy" systems. It helps decode old code and accelerates the migration to flexible cloud infrastructures, making insurers more agile and innovative.

- New Regulatory & Ethical Frameworks: The rise of AI-driven decisions has prompted Japan's FSA to demand "explainable AI" (XAI). This pushes insurers to adopt transparent algorithms to ensure fairness, data privacy, and maintain consumer trust.

Japan Insurtech Market: Competitive Landscape

The competitive landscape in the Japan Insurtech Market is a dynamic mix of global insurance behemoths, nimble local startups, and major technology firms. The market is characterized by a high degree of collaboration, as traditional insurers (the incumbents) increasingly rely on partnerships, investments, and acquisitions to access the agility and technological expertise of insurtech companies. The leading players leverage Japan's digital transformation initiatives by aligning their offerings with the FSA's regulatory framework and the specific societal needs, such as elderly care and disaster resilience. Major global technology consultancies and cloud providers like Accenture, IBM, and Oracle are also key players, providing the infrastructure and integration services necessary for digital overhaul.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Mergers, acquisitions, and strategic investments (CVC) are common strategies, allowing incumbents to quickly absorb new capabilities. For instance, a large insurer might acquire a startup with a leading AI claims platform or invest in a digital health venture. Partnerships are also prevalent, with technology companies teaming up with insurers to co-develop new data-driven products. While the large incumbents dominate in terms of scale and customer base, innovation in niches like on-demand insurance, pet insurance, and micro-insurance separates the new entrants and allows them to grow. With strong governmental support for fintech and insurtech innovation, the market presents opportunities for both established global players and disruptive local startups, ensuring an intensely competitive and rapidly evolving landscape.

Some of the prominent players in the Japan Insurtech Market are:

- Tokio Marine Holdings

- Sompo Holdings

- MS&AD Insurance Group

- JustInCase

- SmartDrive

- D&I

- Oracle

- EY

- SAP

- SilverBridge

- OpenText

- Avanade

- Entsia

- ADROSONIC

- EIS

- MIC Global

- Asseco

- Virtusa

- Xceedance

- Mendix

- Other Key Players

Recent Developments in Japan Insurtech Market

- October 2025: Sompo Holdings launched a new AI-powered platform for predicting and mitigating the risk of business interruption from typhoons. The platform uses machine learning to analyze weather data and a company's supply chain vulnerabilities, providing actionable recommendations days in advance.

- September 2025: Tokio Marine & Nichido Fire Insurance Co. entered a strategic partnership with a leading Japanese smart-home device manufacturer to integrate IoT sensors into home insurance policies. The collaboration focuses on preventing water leaks and fire damage through real-time monitoring and automated shut-off systems.

- August 2025: The Japanese government, through the FSA, announced an expansion of its regulatory sandbox to specifically focus on "Web3 and Insurance," allowing for the live testing of parametric insurance products using smart contracts on blockchain networks.

- November 2024: MS&AD Insurance Group Holdings made a significant investment in a US-based startup specializing in generative AI for underwriting. The partnership aims to develop a Japanese-language model to automate the analysis of complex commercial risk submissions.

- July 2024: JustInCase, a leading Japanese insurtech startup, unveiled a new cloud-based platform for "micro-duration" insurance, enabling partners like ride-sharing and delivery apps to offer coverage for single trips or tasks, leveraging real-time data APIs.

- April 2024: SmartDrive, a telematics company, expanded its partnership with a major regional auto insurer to launch a full-fledged usage-based insurance (UBI) product that relies entirely on smartphone sensor data, eliminating the need for a separate plug-in device.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 1,272.1 Mn |

| Forecast Value (2035) |

USD 8,712.0 Mn |

| CAGR (2026–2035) |

23.8% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Country Coverage |

Japan |

| Segments Covered |

By Type (Health, Auto, Home, Specialty, Travel, Business, and Others), By Technology (Blockchain, Cloud Computing, IoT, Machine Learning, Robo Advisory, and Others), By Service (Consulting, Support & Maintenance, and Managed Services), By End User (BFSI, Automotive, Manufacturing, Transportation, Government, Health, Retail, and Others) |

| Prominent Players |

Tokio Marine Holdings, Sompo Holdings, MS&AD Insurance Group, JustInCase, SmartDrive, D&I, Oracle, EY, SAP, SilverBridge, OpenText, Avanade, Entsia, ADROSONIC, EIS, MIC Global, Asseco, Virtusa, Xceedance, Mendix, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Japan Insurtech Market?

▾ The Japan Insurtech Market size is estimated to have a value of USD 1,272.1 million in 2026 and is expected to reach USD 8,712.0 million by the end of 2035.

Who are the key players in the Japan Insurtech Market?

▾ Some of the major key players in the Japan Insurtech Market are Tokio Marine Holdings, Sompo Holdings, MS&AD Insurance Group, JustInCase, SmartDrive, D&I, and many others.

What is the growth rate in the Japan Insurtech Market?

▾ The market is growing at a CAGR of 23.8 percent over the forecasted period.