What is the Japan Photovoltaic Market Size?

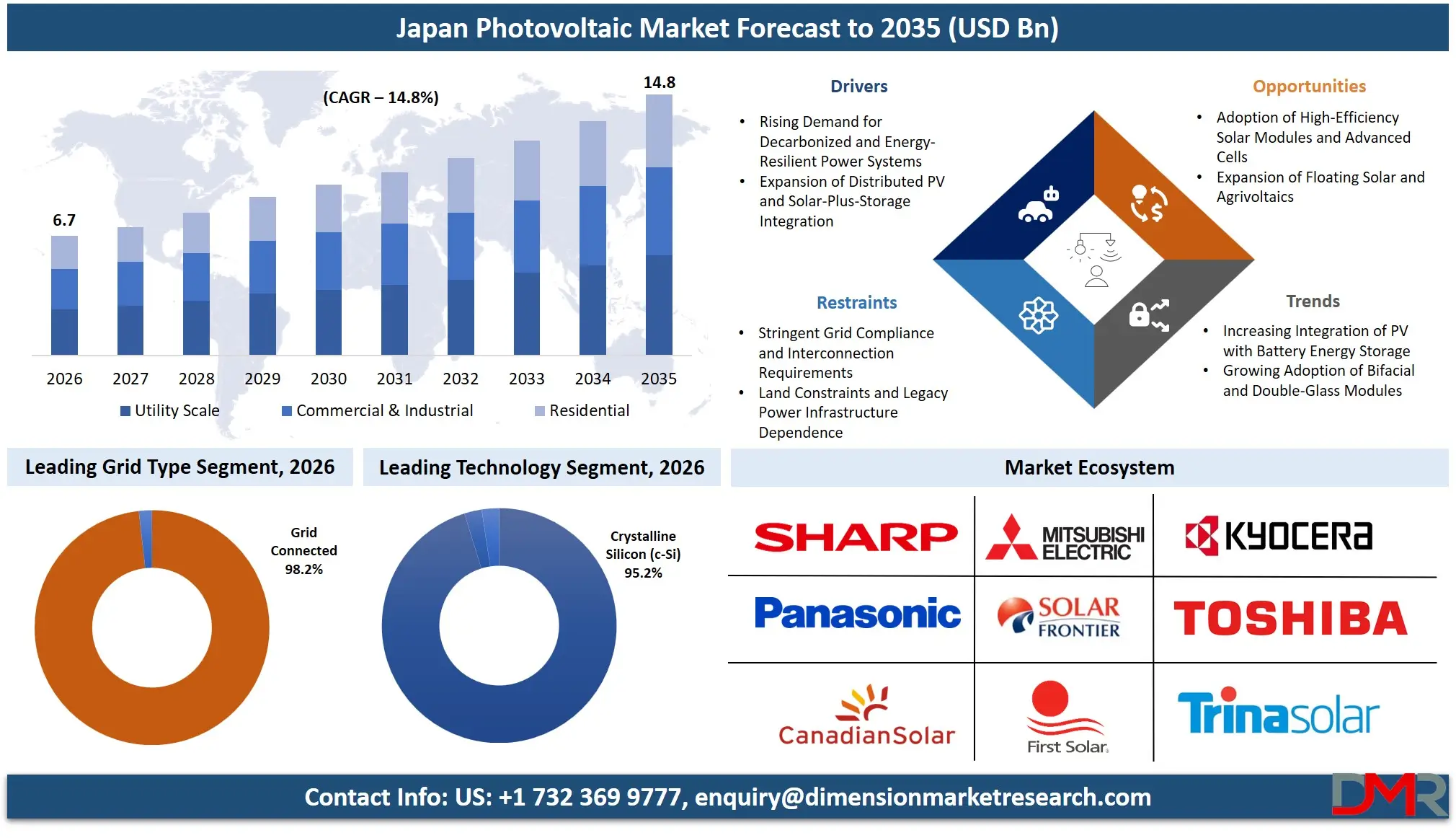

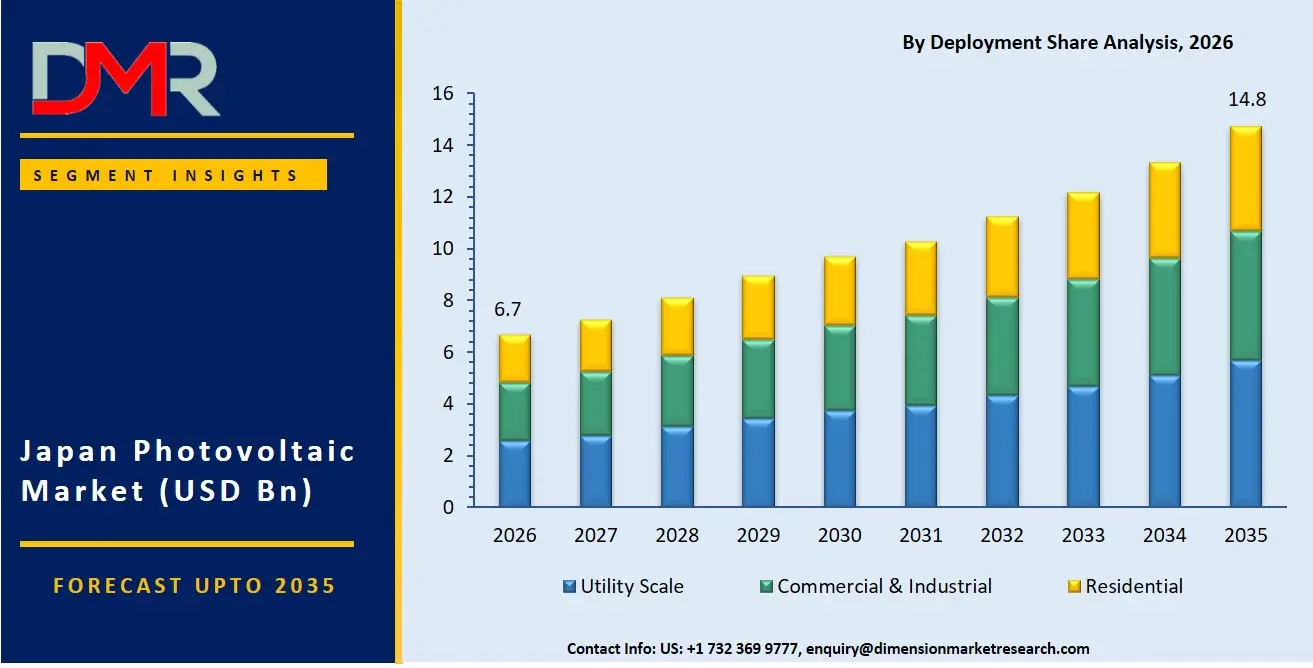

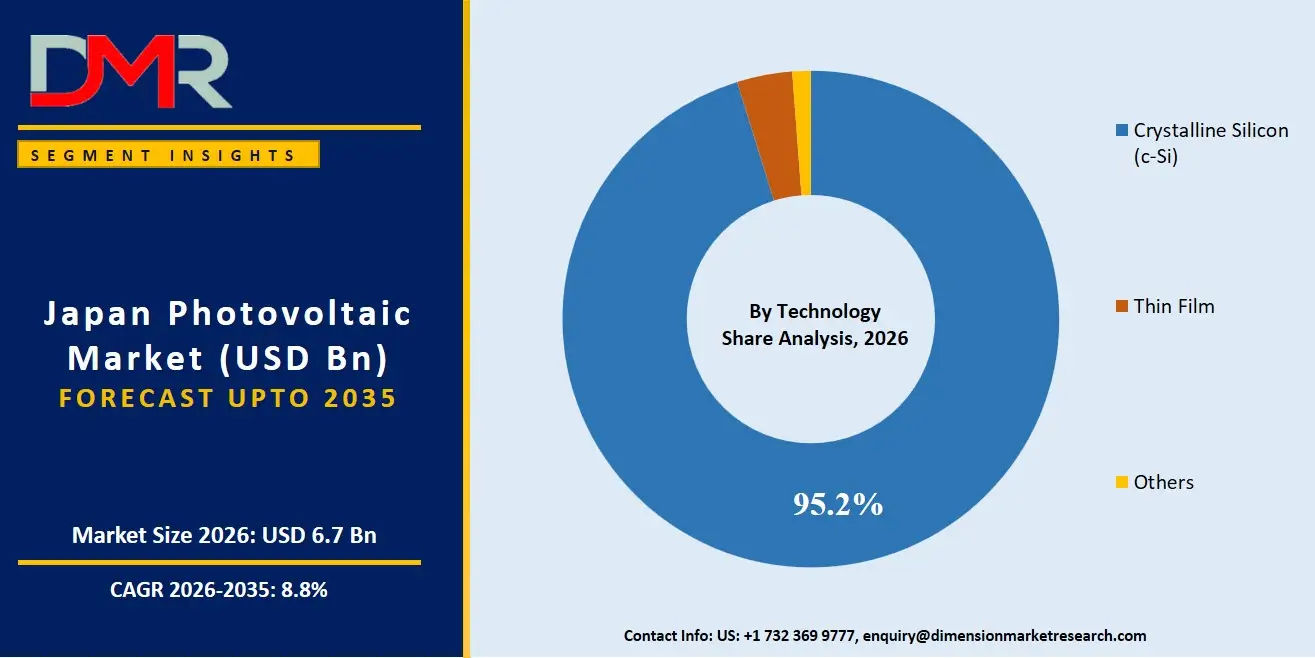

The Japan Photovoltaic (iPaaS) Market is expected to reach a value of USD 6.7 billion in 2026, and it is further anticipated to reach USD 14.8 billion by 2035, growing at a CAGR of 8.8% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Photovoltaic industry has exhibited steady growth because of the increasing need in Japan to adopt durable, decarbonized, and decentralized systems for efficient, secure, and scalable power generation. Some of the PV generating platforms include utility-scale solar plants, rooftop solar plants, and floating PV platforms, which enable firms, businesses, and homeowners to produce sustainable power. High efficiency solar panels and high performance inverters have been needed for reasons including enabling the use of distributed power, ensuring energy independence from energy disruptions, and producing high efficiency power production, among others. Utilities have been established as the leading consumer of PV electricity, where the most common type of solar panel used is that made of crystalline silicon because of its efficiency.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Key Takeaways

- Market Size & Forecast: The Japan Photovoltaic market is forecasted to be valued at USD 6.7 billion in 2026, growing incrementally to USD 14.8 billion by 2035, due to the joint efforts of energy strategy deployment on the part of enterprises as well as the obligatory deployment of zero-emission and resilient power technologies.

- Growth Rate & Outlook: Japan market is expected to grow at 8.8% CAGR, propelled by the urgent need to mitigate emerging renewable energy intermittency vulnerabilities, alongside increasing challenges in orchestrating multi-directional power flows from residential PV, commercial buildings, and industrial facilities.

- Primary Growth Drivers: Major driving factors comprise the transition from traditional centralized power grids towards modern intelligent distribution systems, the necessity to deploy secure and robust energy storage for solar assets, as well as the implementation of renewable energy targets necessitating unique module and inverter expertise.

- Key Market Trends: Major trends encompass the introduction of high-efficiency heterojunction (HJT) and back-contact (IBC) cells, usage of floating solar PV on reservoirs to circumvent land constraints, increased focus on agrivoltaics, and growing integration of lithium-ion battery storage with solar farms.

- By Technology Analysis: The Crystalline Silicon (c-Si) segment is projected to dominate the Japan Photovoltaic Market due to strong demand for high-efficiency and reliable generation systems. Thin Film remains limited to niche applications such as building-integrated PV (BIPV), while Others (perovskite cells) are gaining R&D focus with government backing.

- By Grid Type Analysis: The Grid Connected segment is projected to dominate the market overwhelmingly, accounting for the majority of installed capacity, owing to Japan's comprehensive grid infrastructure, feed-in-premium (FiP) scheme, and widespread utility-scale and rooftop integration.

- By Deployment Analysis: The Commercial & Industrial (C&I) segment is anticipated to lead or closely rival Utility Scale in the Japan Photovoltaic Market due to growing corporate renewable procurement, rooftop installations on factories and warehouses, and attractive economics for self-consumption.

What is Photovoltaic?

Photovoltaics (PV) is the term used to describe the process of converting the sun's energy into electricity through photovoltaic cells using semiconductors to directly generate the electricity. Most PV systems consist of solar panels, inverters, mounting systems, and other balance of system components, all of which combine to generate power suitable for use in residential buildings, commercial firms, industries, and utilities. The modern PV systems have been enhanced with state-of-the-art monitoring systems, energy storage systems, and grid tie-in systems.

Use Cases

- Utility-Scale Solar Generation: Electric companies and IPPs use utility-scale PV plants with multiple inverters to generate clean energy that is connected to the transmission system, helping achieve Japan's renewable energy goals by replacing fossil fuels.

- Rooftop Solar for Households: Residential homeowners install solar panels on their rooftops, usually coupled with storage batteries, as an effective measure to lower energy costs, promote energy consumption, and serve as emergency power when a typhoon or an earthquake occurs.

- Solar + Storage for Factories: Factories install ground-based or rooftop-based PV systems integrated with lithium-ion battery systems to cut down peak-time demands, guarantee uninterrupted production, and support the company's environmental goals.

- Floating Solar on Reservoirs: Municipalities and utility companies utilize floating PV systems at agricultural ponds or dam lakes, producing clean electricity without using valuable land and cutting down water evaporation.

- Agrivoltaics: Farmers utilize solar panels for generating electricity above crops while simultaneously growing crops under the solar panels installed above the land.

How AI is Transforming the Photovoltaic Market?

In the photovoltaic industry, artificial intelligence is driving innovation by optimizing solar irradiance prediction, predicting maintenance needs, and improving operations management. Satellite images and weather reports are utilized by AI technologies to anticipate cloud cover and solar radiation. For PV plants of substantial capacity, anomaly detection technologies that make use of artificial intelligence algorithms can recognize problems in the modules' performance, thus scheduling preventive maintenance actions to increase yield. Regarding the inverters' operation, AI technologies can maximize the performance of MPPT and grid synchronization functions. In order for batteries to be incorporated into the PV plant, algorithms based on AI technologies can optimize their dispatch according to electricity prices and consumption patterns.

Market Dynamics

Key Drivers in the Japan Photovoltaic Market

Rising Demand for Decarbonized and Energy-Resilient Power Systems

The increasing need to meet Net Zero targets (by 2050), to ensure the resilience of infrastructure from natural catastrophes, and decreasing dependency on foreign fossil fuels are pushing Japanese utility companies, corporations, and residential clients towards adopting PV technologies. In the wake of the nuclear disaster at Fukushima, there has been an emphasis on developing decentralized and resilient power sources in Japan. Instead of the Feed-in Tariff (FiT) mechanism, a new FiP mechanism has been implemented in which the market forces determine solar power generation. The increase in the cost of electricity caused by increased fuel prices is making solar power more affordable for individuals and companies.

Expansion of Distributed PV and Solar-Plus-Storage Integration

The number of cases where regulations were concerned about grid impact assessment, output control (curtailment) orders, and the ability to supply reactive power has increased. With such rigorous adherence to regulations, PV power plants are increasingly expensive, difficult to set up, and time-consuming. This applies to regions like Hokkaido and Kyushu where curtailment was common before. There is a need for the owner of the PV power plants to make sure that they have proper grid interconnection facilities and that their operation involves remote monitoring and conformity with output control orders. Failure to adhere to these rules will result in some penalties.

Restraints in the Japan Photovoltaic Market

Stringent Grid Compliance and Interconnection Requirements

The rigid grid interconnection protocols and grid stability rules in Japan have been posing certain operational difficulties for PV project developers, EPC contractors, and utility firms. A new trend of increased regulation has emerged in relation to grid impact evaluation, output curtailment orders, and the ability to provide reactive power with the goal of reducing grid instability, voltage, and frequency risks. The strict adherence to the regulations will make it more expensive and complicated for PV power plants to be constructed especially in Hokkaido and Kyushu, where a lot of output curtailments have been experienced. It is important that the operator of the PV power plant takes all the necessary precautions, including having the appropriate grid connection and remote monitoring systems, as well as adhering to output curtailment instructions.

Land Constraints and Legacy Power Infrastructure Dependence

The barriers that are currently holding back the growth of solar PV development in Japan include the shortage of land as well as the need for existing power networks. The utility-scale ground-mounted solar projects have been encountering various difficulties in terms of identifying lands, securing environmental permits, and overcoming grid capacity constraints, among other challenges. Grid capacity constraints and energy curtailments due to congested regions have been slowing down these kinds of projects. Rural areas rely on conventional power systems owing to their lower costs and easier technological applications than those associated with renewable energy systems. Reliance on old power systems has hindered the adoption of distributed solar photovoltaic and energy management systems in rural regions.

Growth Opportunities in the Japan Photovoltaic Market

Adoption of High-Efficiency Solar Modules and Advanced Cells

Potential areas for growth have become evident in the form of the introduction of high-efficiency crystalline silicon modules in Japan. This innovation in the industry includes such high-efficiency modules as HJT, TOPCon, and IBC cells that enable owners of solar systems to produce more electricity per square meter, which is important since Japan faces challenges regarding limited availability of land. High-efficiency modules provide improvements not only in terms of reliability of renewable energy and balance-of-system costs per watt but also enable savings in installation costs per watt. Given that technology continues to evolve, residential and business users will increasingly turn their attention toward purchasing high-power modules.

Expansion of Floating Solar and Agrivoltaics

The use of Floating solar PV (FPV) has been increasingly recognized in Japan as an alternative means of overcoming the problem of limited land availability. In this regard, FPV installation on agricultural ponds, reservoirs, and dam lakes is gradually being accepted as a means of providing renewable energy production in a way that does not require the use of agricultural and residential land. The use of high-end anchoring and mooring technologies is assisting firms in stabilizing their systems amidst the challenges posed by typhoons and flooding. Additionally, floating solar panels have been found to decrease water evaporation and algae formation. Likewise, agrivoltaics involves installing solar panels above crops to generate power alongside crop production.

Trends in the Japan Photovoltaic Market

Increasing Integration of PV with Battery Energy Storage

Utility firms, businesses, and homes in Japan are increasingly choosing integrated PV and battery systems for ensuring efficient energy production and energy reliability from renewables. It is now increasingly common for companies to participate in designing integrated energy management systems using solar energy, lithium-ion energy storage battery, and smart technology. These integrated energy systems play a significant role in energy load balancing, backup energy, disaster resilience, and managing peak load in case of a grid disturbance. Factors like electricity price fluctuations, energy security concerns, and the need for cutting carbon emissions have contributed to the growing interest in using PV systems with battery energy storage in Japan. Apart from these factors, improved battery technology and lower prices have helped make the system more practical.

Growing Adoption of Bifacial and Double-Glass Modules

Japanese PV project developers are increasingly embracing the use of bifacial modules to capture power on the front and back sides of the modules. This type of module harnesses reflected light off the ground, water surfaces (for floating PV) or roof surface, thereby boosting the power generation by 5 to 25 percent without much increase in cost. Bifacial double glass modules have better resilience against moisture, salt erosion (particularly critical to coastal Japan) and potential induced degradation (PID). Adoption of bifacial and double glass modules is growing particularly fast in utility-scale or floating PV projects with high albedo.

Research Scope and Analysis

The Japan Photovoltaic Market is segmented by technology, grid type, deployment, installation type, component, application, and end use industry. The market supports residential energy management, commercial demand response, industrial automation, and government infrastructure across individual consumers, utility operators, public authorities, and energy companies through various PV generation and storage solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Technology Analysis

Crystalline Silicon (c-Si) modules are expected to lead the Japan Photovoltaic Market in 2026 with a projected market share of 95.2% as a result of utility operators' and residential consumers' growing preference for high-efficiency, reliable, and cost-effective solar cells. Japanese developers have developed a preference for monocrystalline PERC, TOPCon, and HJT modules for performing functions such as maximizing generation per limited rooftop or land area. Thin Film solutions (CIGS, CdTe) are likely to occupy a minor share due to lower efficiency, though they retain niche applications in building-integrated PV (BIPV) and flexible modules. The Others segment, including emerging perovskite PV cells, is gaining R&D attention with government backing, with pilot projects underway for building-integrated and tandem cell applications.

By Grid Type Analysis

Grid Connected systems are projected to dominate the Japan Photovoltaic Market in 2026, with an estimated share of 98.2%, owing to near-universal grid access, the Feed-in Premium (FiP) scheme, and widespread utility-scale and rooftop integration. Japanese grid operators and energy aggregators favor grid-connected PV because it allows surplus electricity to be sold to utilities, provides grid support services, and maximizes system economics. Off-Grid systems follow a very small share, driven by PV-plus-storage installations in remote islands (Ogasawara Islands, remote parts of Hokkaido) and mountain huts, as well as specialized applications such as telecommunications towers and agricultural water pumping.

By Deployment Analysis

Utility Scale is projected to hold a strong but not dominant share of the Japan Photovoltaic Market in 2026 with a projected share of 38.5%, due to ongoing mega-solar projects on abandoned farmland and reclaimed land. However, land constraints and curtailment risks have slowed new utility-scale development. Commercial & Industrial (C&I) will experience robust growth, driven by corporate renewable energy procurement, rooftop installations on factories, warehouses, and office buildings, and attractive economics for self-consumption. Residential deployment continues steadily at 26.0% share, supported by government-backed incentives and rising electricity prices, with many households adding battery storage to increase self-consumption.

By Installation Type Analysis

Rooftop PV is projected to dominate the Japan Photovoltaic Market in 2026 with a share of 54.0%, thanks to high deployment penetration on residential homes, commercial buildings, and industrial facilities, along with government-backed incentives and low complexity for end-users. Rooftop solutions enable self-consumption, surplus electricity sales, and real-time monitoring. Ground-Mounted PV will hold a substantial share of 38.0%, due to utility preference for large-scale generation on abandoned farmland, particularly across Kyushu, Tohoku, and Hokkaido regions, though facing increasing land competition and permitting hurdles. Floating Solar is emerging as a high-growth niche, leveraging Japan's numerous agricultural and hydroelectric reservoirs to circumvent land constraints, especially in Chiba, Hyogo, and Gifu prefectures.

By Component Analysis

Modules are projected to continue dominating the Photovoltaic Market of Japan, with an expected market share of 55.0% in 2026, owing to robust energy generation targets and falling module prices, as well as heavy reliance on module efficiency to maximize limited installation space. Businesses and households are increasingly adopting high-efficiency monocrystalline panels (TOPCon, HJT, IBC) due to lower electricity costs, predictable production scheduling, and regulatory compliance. Inverters are segment is gaining traction owing to the increasing deployment of string inverters for residential and C&I systems and central inverters for utility-scale, with smart hybrid inverters gaining traction for solar-plus-storage. Balance of System (BoS), including cabling, combiner boxes, protection devices, and monitoring hardware.

By Application Analysis

Electric Generation is projected to dominate the Japan Photovoltaic Market in 2026 with an expected market share of 88.0%, owing to robust energy generation targets, the Feed-in Premium scheme, and widespread adoption of PV for household, commercial, industrial, and utility electricity production. Charging Systems represent the fastest-growing application, driven by increasing deployment of EV charging infrastructure integrated with PV generation, particularly in urban and highway rest areas. Lighting applications (streetlights, park lighting, agricultural lighting) and others (water pumping, desalination, remote telecommunications) segment hold the remaining share.

By End Use Industry Analysis

Power Utilities are projected to lead the Japan Photovoltaic Market in 2026 with an expected share of 40.0%, driven by utility-scale solar farms and IPP projects feeding into the grid. Commercial Buildings follow at 24.0% share, with building owners adopting PV for energy cost reduction, carbon neutrality targets, and compliance with building energy efficiency mandates. Residential Buildings maintain steady demand through rooftop programs, with many households adding storage. Industrial Facilities are experiencing rapid growth as manufacturers seek to lower electricity costs, ensure backup power, and meet corporate decarbonization goals. Others (agriculture, public infrastructure, transportation) hold the remaining share, including agrivoltaics and floating solar on public reservoirs.

The Japan Photovoltaic Market Report is segmented based on the following:

By Technology

- Crystalline Silicon (c-Si)

- Thin Film

- Others

By Grid Type

By Deployment

- Utility Scale

- Commercial & Industrial

- Residential

By Installation Type

- Ground Mounted

- Rooftop

- Floating Solar

By Component

- Modules

- Inverters

- Balance of System (BoS)

- Mounting Structures & Trackers

By Application

- Electric Generation

- Lighting

- Charging Systems

- Others

By End Use Industry

- Power Utilities

- Commercial Buildings

- Residential Buildings

- Industrial Facilities

- Others

Competitive Landscape

The dynamics of competition in the Japan Photovoltaic marketplace have developed to become increasingly dynamic, with a wide range of multinational PV manufacturers, Japanese trading houses, and renewable energy developers specializing in various module technologies, inverter systems, and EPC services. The essential ingredient for success is found in deep-seated strategic partnerships with landholders, utility operators, and EPC contractors in Japan, which open up high-quality project pipelines and allow integrated PV solutions and O&M services to be offered alongside one another. Market consolidation trends are moving rapidly ahead, with established players in renewable energy, power infrastructure, and energy storage taking on acquisitions of specialized PV technology providers to strengthen their module efficiency and battery integration capabilities. Proprietary intellectual property rights, including advanced cell architectures (HJT, TOPCon, IBC), module manufacturing techniques, and smart inverter technologies, hold increasing importance compared to just competitive hardware pricing.

Some of the prominent players in the Japan Photovoltaic Market are:

- Sharp Corporation

- Kyocera Corporation

- Panasonic Holdings Corporation

- Mitsubishi Electric Corporation

- Toshiba Energy Systems & Solutions Corporation

- Solar Frontier K.K.

- Canadian Solar Inc.

- Trina Solar Co., Ltd.

- JinkoSolar Holding Co., Ltd.

- JA Solar Technology Co., Ltd.

- LONGi Green Energy Technology Co., Ltd.

- Hanwha Solutions Corporation

- First Solar, Inc.

- OMRON Corporation

- Eurus Energy Holdings Corporation

- RENOVA, Inc.

- Shizen Energy Inc.

- West Holdings Corporation

- Nihon Techno Co., Ltd.

- Sekisui Chemical Co., Ltd.

- Other Key Players

Recent Developments

- June 2026: JinkoSolar Holding Co., Ltd., Trina Solar Co., Ltd., LONGi Green Energy Technology Co., Ltd., and JA Solar Technology Co., Ltd. accelerated investments in energy storage systems, expanding battery manufacturing capacities and integrated solar-plus-storage offerings to address growing renewable energy demand in key markets, including Japan.

- March 2026: RENOVA, Inc. announced the development of the Kikugawa Nishimura Battery Storage Project in Shizuoka Prefecture with an expected capacity of 90 MW / 270 MWh and secured approximately JPY 6 billion in project financing, supporting grid stability and the integration of renewable energy assets in Japan's power system.

- February 2026: Canadian Solar Inc. announced the delivery of its first grid-connected battery energy storage system (BESS) in Japan through its e-STORAGE business. Located in Sapporo, Hokkaido, the project has a rated output of 2 MW and an energy capacity of 8.25 MWh, supporting grid flexibility and renewable energy integration in the Japanese power market.

- November 2025: First Solar, Inc. announced plans to establish a new 3.7 GW solar module manufacturing facility, increasing its total U.S. manufacturing capacity to more than 14 GW by 2026. The expansion strengthens the company's global thin-film solar module supply capabilities amid growing international demand for utility-scale photovoltaic projects.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 6.7 Bn |

| Forecast Value (2035) |

USD 14.8 Bn |

| CAGR (2026–2035) |

8.8% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Technology, By Grid Type, By Deployment, By Installation Type, By Component, By Application, By End Use Industry |

| Country Coverage |

Japan |

Frequently Asked Questions

How big is the Japan Photovoltaic Market?

▾ The Japan Photovoltaic Market is poised to reach USD 6.7 billion in 2026 and USD 14.8 billion by 2035.

What is the CAGR of the Japan Photovoltaic Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 8.8% from 2026 to 2035, reflecting the maturing nature of the PV market and the accelerating deployment of solar-plus-storage, rooftop systems, and floating solar.

What factors are driving the growth of the Japan Photovoltaic Market?

▾ Key drivers include the decarbonization imperative (Net Zero 2050), the need to enhance energy security following fossil fuel price volatility, the Feed-in Premium (FiP) scheme, rising retail electricity prices, corporate renewable energy procurement, and falling costs of solar modules and batteries.

What are the major trends in the Japan Photovoltaic Market?

▾ Major trends include the adoption of high-efficiency modules (HJT, TOPCon, IBC), the integration of lithium-ion battery storage with solar, the expansion of floating solar PV on reservoirs, the growth of agrivoltaics (solar sharing), and the development of perovskite tandem cells.

Who are the key players in the Japan Photovoltaic Market?

▾ Key players include Sharp Corporation, Kyocera Corporation, Panasonic Holdings Corporation, Toshiba Energy Systems & Solutions Corporation, along with international module suppliers such as LONGi, JinkoSolar, and Trina Solar, and Japanese developers such as RENOVA and West Holdings.

How is the Japan Photovoltaic Market segmented?

▾ The market is segmented by technology, grid type, deployment, installation type, component, application, and end use industry.