What is the Japan Quantum Computing Market Size?

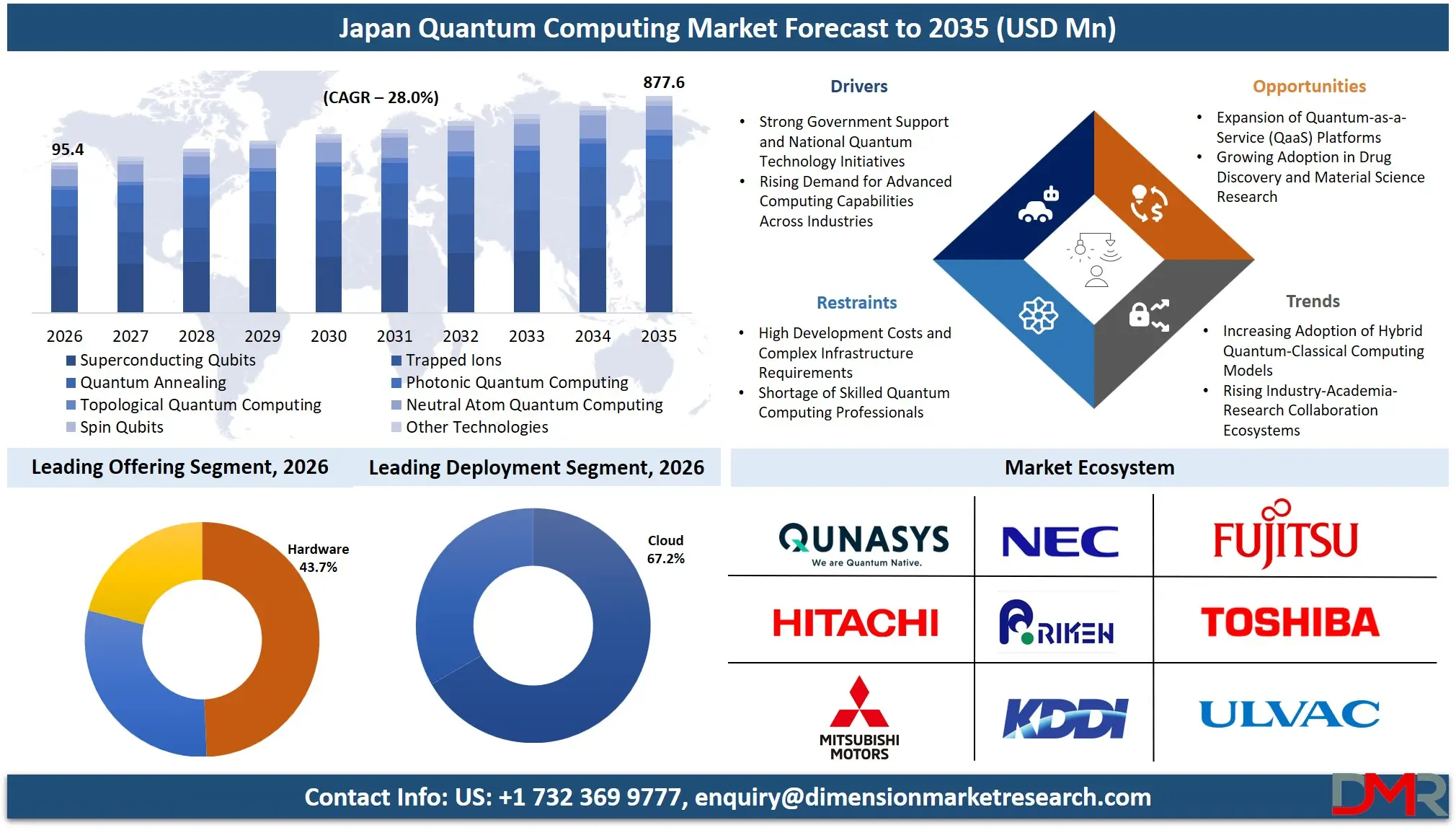

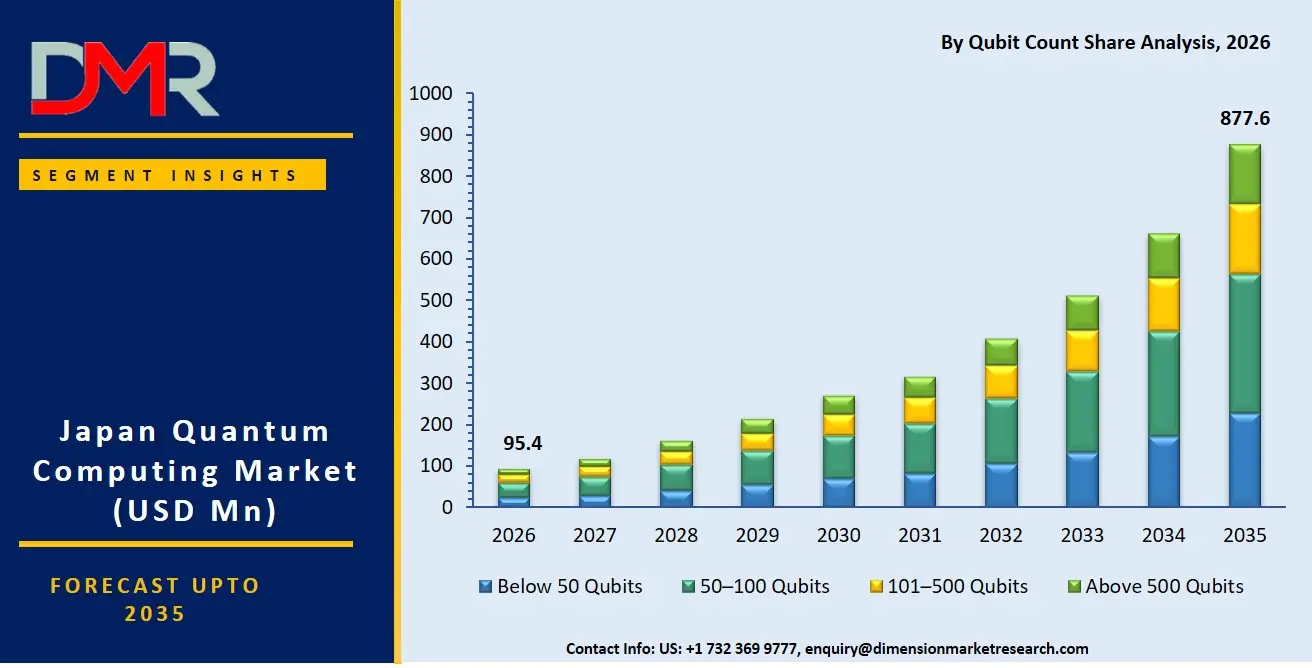

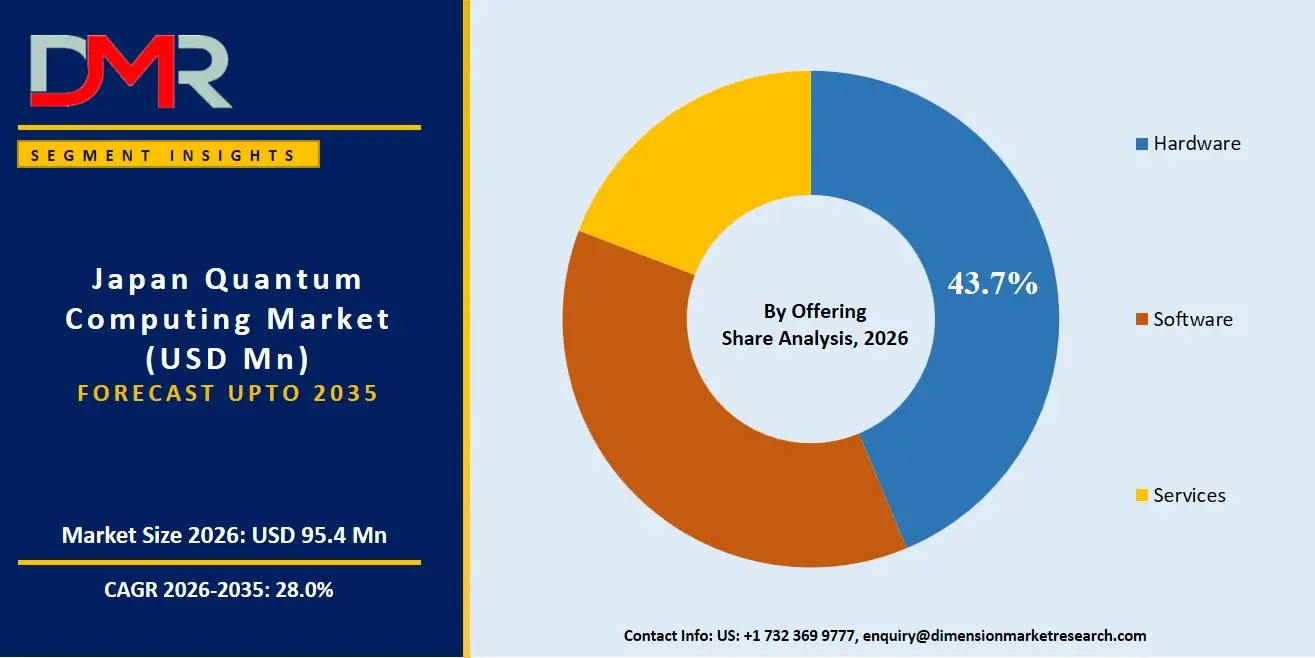

The Japan Quantum Computing Market is expected to reach a valuation of USD 95.4 million in 2026, and is further anticipated to surge to USD 877.6 million by 2035, growing at a staggering CAGR of 28.0% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Japan quantum computing market is experiencing accelerated momentum as the nation confronts its "2025 Digital Cliff" and a critical shortage of computational power to solve complex societal challenges. This emergent market encompasses a rich ecosystem of quantum processors, cryogenic control systems, specialized algorithms, and consultative services designed to help research consortia and enterprises harness quantum mechanical phenomena like superposition and entanglement.

The escalating necessity to model novel materials for next-generation batteries, optimize logistics for an aging population, and develop quantum-resistant cryptographic protocols is fueling the demand for specialized quantum hardware, error mitigation middleware, and full-stack quantum-as-a-service (QaaS) platforms. Early adopters are concentrated in academic-led government moonshot programs, with superconducting and trapped-ion modalities remaining the most pursued due to their relative coherence maturity. The automotive, materials science, and financial services industries are key players as they seek quantum advantage in simulations, Monte Carlo analyses, and combinatorial optimization that are intractable for classical high-performance computing (HPC) systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Key Takeaways

- Market Size and Forecast: The forecast market value for Japan quantum computing market is set to be USD 95.4 million in 2026, growing exponentially to USD 877.6 million in 2035, powered by the twin forces of R&D roadmap initiatives by governments and the urgent requirement to discover novel functional materials using physics-based simulations.

- Growth Rate & Outlook: Market growth at a CAGR of 28.0% is forecast from 2026 to 2035, due to the severe shortage of in-house quantum information scientists and rising complications involved in managing qubit coherence, gate fidelity, and hybrid integration of classical HPC and NISQ processors.

- Primary Growth Drivers: Important factors that influence market growth include the national necessity to go past the barriers posed by Moore's Law, developing Quantum Algorithms for practical quantum advantage in drug discovery, and integrating quantum computers with classical supercomputers such as Fugaku.

- Key Market Trends: Major trends include the rise of industry-specific quantum applications (e.g., quantum chemistry for carbon capture, quantum Monte Carlo for derivatives pricing), the use of AI-powered error mitigation within Middleware to auto-correct decoherence issues, and the shift toward Quantum-Safe Cryptography consulting as government bodies prioritize post-quantum data sovereignty.

- By Qubit Count Analysis: 50–100 Qubit processors are expected to dominate commercial experimentation due to their balance of computational power and manageable error rates. Professional services are increasingly required to build seamless hybrid classical-quantum workflows that connect on-premise supercomputing resources with cloud-based quantum backends.

- By End-User Industry Analysis: Academic & Research Institutions and Healthcare & Pharmaceuticals are the most active verticals due to government grants and the pursuit of in-silico molecular docking. Automotive and Logistics & Transportation are the fastest-growing sectors as the electrification of vehicles and supply chain fragility demand robust Quantum Optimization and materials simulation.

What is Quantum Computing?

Quantum computing is an advanced computing technology that uses the principles of quantum mechanics to process information. Unlike classical computers, which use bits that exist as either 0 or 1, quantum computers use quantum bits, or qubits, which can exist in multiple states simultaneously through a property known as superposition. Quantum computers also leverage entanglement and interference to perform complex calculations more efficiently than traditional systems. This enables them to solve certain optimization, simulation, cryptography, and machine learning problems that are difficult or impossible for classical computers to handle within a practical timeframe. Although still in the early stages of development, quantum computing has the potential to transform industries such as healthcare, finance, logistics, energy, materials science, and cybersecurity through unprecedented computational capabilities.

Use Cases

- EV Battery Material Simulation: Automotive and chemical conglomerates hire Simulation Software and Quantum Chemistry algorithm developers to model molecular interactions for solid-state electrolytes, accelerating the discovery of higher-density battery materials beyond the capabilities of classical Density Functional Theory (DFT).

- Quantum-Safe Migration in BFSI: Megabanks use Consulting Services and Quantum Programming Platforms to catalog their cryptographic assets and deploy hybrid classical-quantum algorithms, ensuring transactional integrity against future "Harvest Now, Decrypt Later" threats.

- Sovereign Quantum AI Hub Navigation: Government agencies employ Integration & Deployment services to architect private cloud-based quantum testbeds that comply with stringent data localization laws, ensuring sensitive citizen data is processed via domestic quantum processors rather than foreign backends.

- Photonics-Fueled Drug Discovery: Pharmaceutical firms use QaaS platforms to run protein folding simulations on photonic quantum computers, integrating the results with classical molecular dynamics pipelines to identify viable drug targets with unmatched energy efficiency.

How AI is Transforming the Quantum Computing Market?

AI technologies have transformed the sector of quantum professional services by significantly improving not only hardware calibration but also applications development. Firstly, with regard to Software and Middleware, AI-enabled error correction software translates quantum circuits into machine code, actively suppressing decoherence and crosstalk between qubits, thereby increasing the effective number of gates in NISQ devices. Secondly, AI functionalities in Quantum Programming Platforms help scientists steer their hybrid workflows and apply classical machine learning to train the optimal quantum circuit (ansatz) and route through qubits that ensure the highest accuracy of gates.

Furthermore, Governance and Algorithms Development are also becoming increasingly dependent on AI innovations. In particular, in terms of Consulting Services, intelligent agents provide continuous benchmarking and validation of annealer and gate model processor outcomes, detecting possible errors related to the noise bias, calibration deviations, and logical inconsistencies of algorithms in accordance with fidelity benchmarks. In addition, AI-powered assistants are supporting Quantum Algorithms discovery by modeling abstract Hamiltonian equations and generating novel variational quantum circuits, providing visualization of computational topology prior to running qubits.

Market Dynamics

Key Drivers in the Japan Quantum Computing Market

Strong Government Support and National Quantum Strategy

The quantum computing market of Japan is greatly influenced by the favorable policies adopted by the Japanese government and its technology vision for many years to come. The Japanese government recognizes quantum technology as a key area of focus that can strengthen its competitiveness, independence, and economy. Significant amounts of money are invested by the Japanese government through various programs and initiatives in quantum hardware, software, and talent. Universities and national laboratories are getting government grants in order to make their quantum research and innovations successful. Government-driven cooperation between academia, industries, and other organizations is playing an important role in developing a vibrant quantum ecosystem.

Rising Demand for Advanced Computing in Industrial Sectors

Growing requirement of computing solutions in different industries has facilitated quantum computing adoption in Japan. The traditional computers have several restrictions in the resolution of extremely complicated computational problems based on optimization, simulation, and other data-related problems. Different industries like automotive, manufacturing, pharmaceutical, finance, and logistics are exploring the possibilities of adopting quantum computing solutions to derive competitive benefits from better problem solving. The key focus areas in quantum computing technology include material development, supply chain optimization, risk analysis, and enhancement of AI systems among others. Organizations are constantly searching for advanced computing solutions amid the growing digitization trend, and thus, quantum computing solutions find relevance in this regard.

Restraints in the Japan Quantum Computing Market

High Development Costs and Infrastructure Requirements

The cost implication of manufacturing and maintaining quantum computer technology is one of the significant constraints affecting the Japanese quantum computing industry. Quantum computers require the use of quantum processors, cryogenic coolers, high-level control electronics, among others. These elements make quantum computer development and maintenance expensive for both technology manufacturers and research organizations. Furthermore, the constant costs involved in creating and sustaining a quantum environment make it challenging for small firms to participate in the market due to their inability to incur the costs. Thus, the cost implication poses challenges to the growth of the Japanese quantum computing industry.

Limited Availability of Skilled Quantum Workforce

The availability of skilled quantum computing experts is one of the critical problems impeding the growth of the market in Japan. Skills related to quantum computing include quantum physics, mathematics, computer science, engineering, and algorithms. Nevertheless, there is still a limited number of experts in comparison with the rising demands on the market. Companies often experience difficulty attracting researchers, programmers, hardware specialists, and quantum experts that can develop complex quantum technologies. In addition, quantum computing involves complicated technical issues that may prolong the period for training personnel. Despite the fact that there are programs aimed at educating skilled specialists, they do not seem sufficient.

Growth Opportunities in the Japan Quantum Computing Market

Expansion of Quantum-as-a-Service (QaaS) Platforms

The rising trend in the usage of Quantum-as-a-Service (QaaS) is seen as a major business opportunity for the Japanese quantum computing market. With the help of QaaS, firms have an easier way to gain access to quantum computing via the cloud without having to invest in costly hardware. QaaS provides firms, startups, universities, and research institutes with a more affordable route to exploring quantum computing. As businesses become more involved in digital transformation projects, quantum computing on a cloud service becomes a much easier option to consider. The providers get to grow their clientele and penetrate the market more easily.

Growing Applications in Drug Discovery and Material Science

The prospects of quantum computing are huge in areas such as drug discovery and material science which are strategically vital for Japan. The conventional computing system often lacks the capability to simulate the interactions between molecules and complex chemical reactions. Quantum computing holds the promise of better accuracy in simulation that can help to discover new drugs and innovative materials, including energy-efficient compounds. In order to innovate, there is a growing focus of the robust pharmaceutical and chemical industries and advanced manufacturing companies of Japan towards research collaboration related to quantum computing. If successfully implemented, the use of quantum computing in these scientific domains could lead to fast discovery of new products.

Trends in the Japan Quantum Computing Market

Increasing Adoption of Hybrid Quantum-Classical Computing

One of the key trends emerging within the Japanese quantum computing market is the increasing implementation of hybrid computing models. Instead of replacing existing computing solutions, firms are beginning to combine quantum computing with their existing classical high-performance computing systems. The adoption of hybrid computing allows firms to leverage quantum computing technology for specialized computations while making use of classical technology for general-purpose computing tasks. This approach addresses many of the issues related to quantum computing that currently exist, such as error and scaling problems. Hybrid computing solutions for various purposes, including optimization, simulation, machine learning, and industrial research, are being investigated by firms in Japan.

Rising Collaboration Between Industry, Academia, and Research Institutes

Collaboration between industry players, academic institutions, and research bodies is emerging as a major trend in Japan's quantum computing space. Given the complexities of quantum computing, collaboration has become an essential element to foster growth and share knowledge. Collaborations have helped speed up developments in quantum hardware, software, algorithms, and applications. Universities play the role of conducting basic research while enterprises help in commercializing quantum computing technology by providing relevant use cases. Government agencies have played their part by supporting such collaborations. Collaboration can be seen as an approach to mitigate risks, accelerate developments, and enhance competitiveness. Increasing instances of quantum computing collaborations in Japan will continue to be an important trend in the years to come.

Research Scope and Analysis

The Japan Quantum Computing Market is segmented by offering into hardware, software and services, by deployment into on-premises and cloud, by qubit count, technology and application. The market is further categorized by end-user industry, including academic and research institutions, aerospace and defense, BFSI, healthcare, energy, chemicals, logistics and government organizations.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Offering Analysis

Hardware is projected to be the dominant offering type for the Japan quantum computing market since quantum computers rely heavily on physical assets such as processors, cryogenic infrastructure, control electronics, and quantum chips. Large investments made by government bodies, universities, and firms are mainly focused on improving the hardware aspect to ensure better qubit stability, scaling capabilities, and computing power. The established semiconductor fabrication facilities in Japan and its electronics prowess make a conducive environment for hardware advancements. Organizations will have to focus on developing robust quantum processors as they attempt to achieve quantum advantage. Hardware also forms the basis for software and services ecosystems to thrive. The large capital required for the procurement of hardware drives substantial market revenue, making hardware the dominant offering segment in the Japan quantum computing market.

By Deployment Analysis

Cloud deployment is anticipated to lead in the Japanese quantum computing market owing to its capability of offering affordable access to quantum services without the need for organizations to make investments in costly infrastructure. Most businesses, universities, and research centers lack the necessary funds and capabilities to implement quantum computers within their premises. Cloud computing enables organizations to test quantum algorithms and applications using subscription services. Moreover, cloud computing provides the advantage of constant updates of quantum processors by service providers. The rising demand for Quantum as a Service (QaaS) and partnership among technology vendors and Japanese companies also contributes significantly to the leading role played by cloud deployment.

By Qubit Count Analysis

The 50–100 qubits segment is poised to dominate because it represents the most commercially viable balance between computational capability and system reliability. Quantum systems within this range are sufficiently advanced to support meaningful research, optimization studies, and proof-of-concept commercial applications while maintaining manageable error rates. Many organizations in Japan use these systems for experimentation in finance, manufacturing, logistics, and material science. While lower-qubit systems are mainly used for education and training, higher-qubit systems remain limited in availability and face greater technical challenges. The 50–100 qubit category therefore serves as the practical sweet spot for organizations seeking real-world quantum experience. This balance of accessibility, performance, and affordability makes it the leading qubit-count segment in Japan's developing quantum computing ecosystem.

By Technology Analysis

Superconducting qubits is expected to dominate the technology segment due to their relative technological maturity, scalability potential, and strong global industry support. This architecture has received substantial investment from major technology companies and research organizations, resulting in significant improvements in qubit performance and coherence times. Japan's advanced electronics and semiconductor industries align well with the manufacturing requirements of superconducting quantum systems. The technology benefits from an established research ecosystem and a growing body of commercial and academic expertise. Furthermore, most currently available commercial quantum computers utilize superconducting architectures, making them more accessible to Japanese organizations. Continuous advancements in error correction, processor connectivity, and system scalability further strengthen the position of superconducting qubits as the dominant technology segment within Japan's quantum computing market.

By Application Analysis

Optimization is poised to dominate the application segment because it offers some of the earliest and most practical commercial use cases for quantum computing. Japanese industries such as manufacturing, logistics, transportation, finance, and supply chain management face increasingly complex optimization challenges involving resource allocation, scheduling, routing, and operational efficiency. Quantum computing has the potential to solve these problems significantly faster than conventional computing approaches. As a result, organizations are actively exploring optimization-focused quantum applications to achieve measurable business value. Compared with other applications that remain largely experimental, optimization delivers more immediate opportunities for commercial deployment. Strong industry demand, clear return-on-investment potential, and widespread applicability across multiple sectors contribute to optimization's leading position within Japan's quantum computing market.

By End-User Industry Analysis

Academic and research institutions is projected to dominate the end-user segment because quantum computing remains in a relatively early stage of commercialization, with much of the activity concentrated in research and technology development. Universities, national laboratories, and research organizations across Japan are heavily involved in advancing quantum hardware, software, algorithms, and applications. These institutions receive significant government funding and often collaborate with private-sector companies to accelerate innovation. Research institutions also play a critical role in workforce development by training future quantum scientists and engineers. Since many commercial applications are still under development, academic users account for a substantial share of quantum system utilization. Their leadership in experimentation, innovation, and technology validation makes this the dominant end-user segment in Japan.

The Japan Quantum Computing Market Report is segmented on the basis of the following:

By Offering

- Hardware

- Quantum Processors

- Quantum Chips

- Cryogenic Systems

- Control Electronics

- Quantum Sensors

- Software

- Quantum Algorithms

- Quantum Programming Platforms

- Simulation Software

- Middleware

- Services

- Consulting Services

- Integration & Deployment

- Training & Support

- Quantum-as-a-Service (QaaS)

By Deployment

By Qubit Count

- Below 50 Qubits

- 50–100 Qubits

- 101–500 Qubits

- Above 500 Qubits

By Technology

- Superconducting Qubits

- Trapped Ions

- Quantum Annealing

- Photonic Quantum Computing

- Topological Quantum Computing

- Neutral Atom Quantum Computing

- Spin Qubits

- Other Technologies

By Application

- Optimization

- Machine Learning & Artificial Intelligence

- Simulation & Modeling

- Cybersecurity & Cryptography

- Drug Discovery & Development

- Financial Modeling

- Supply Chain & Logistics Optimization

- Weather Forecasting

- Material Science Research

- Energy Grid Optimization

- Others

By End-User Industry

- Academic & Research Institutions

- Aerospace & Defense

- Banking, Financial Services and Insurance (BFSI)

- Healthcare & Pharmaceuticals

- Energy & Power

- Chemicals

- Logistics & Transportation

- Government Organizations

Competitive Landscape

The competitive environment of the Japan quantum computing market has become a deeply strategic ecosystem, involving a unique tapestry of domestic hardware pioneers, global public-cloud hyperscalers, and specialized university-originated software startups. Success relies heavily on deep integration into Japan's government-funded quantum moonshot programs, as these consortia open the necessary proof-of-concept opportunities and facilitate co-development with flagship research institutes like RIKEN and AIST. The movement towards vertical integration is progressing rapidly, with traditional electronics manufacturers acquiring quantum software and control electronics startups to build full-stack solutions. Proprietary intellectual property, including novel qubit coupling architectures, cryogenic CMOS controllers, and industry-specific algorithmic blueprints, is becoming a more critical basis of competitive differentiation than merely offering generic cloud access to foreign backends.

Some of the prominent players in the Japan Quantum Computing Market are:

- Fujitsu Limited

- NEC Corporation

- Hitachi Ltd.

- Mitsubishi Group

- RIKEN (Research Institute)

- Toshiba Corporation

- Rakuten Group Inc.

- KDDI Corporation

- ULVAC Inc.

- Blueqat Inc.

- QunaSys Inc.

- Quemix Inc.

- QuEL Inc.

- Qubitcore

- Quantum Biosystems

- LQUOM (formerly QWAVE Dynamics)

- OptQC

- Jij Inc.

- Anritsu Corporation

- AIST (National Institute of Advanced Industrial Science and Technology)

- Other Key Players

Recent Developments

- June 2026: Fujitsu and RIKEN announced the successful deployment of a domestically fabricated 64-qubit superconducting processor, specifically engineered for hybrid HPC-quantum workloads to accelerate Material Science Research, integrated directly with the Fugaku supercomputer.

- March 2026: Toshiba launched a specialized Quantum-as-a-Service (QaaS) trial focused on Financial Modeling, providing access to its in-house Simulated Bifurcation Machine technology to solve high-frequency portfolio optimization problems for major Japanese BFSI institutions.

- October 2025: NEC expanded its quantum network integration services, establishing a dedicated Consulting practice for Government Organizations to secure metropolitan fiber-optic networks with Quantum Key Distribution (QKD) protocols, ensuring resilience against future decryption attacks.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 95.4 Mn |

| Forecast Value (2035) |

USD 877.6 Mn |

| CAGR (2026–2035) |

28.0% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Offering, By Deployment, By Qubit Count, By Technology, By Application, By End-User Industry |

| Country Coverage |

Japan |

Frequently Asked Questions

How big is the Japan Quantum Computing Market?

▾ The Japan Quantum Computing market is poised to be valued at USD 95.4 million in 2026 and is projected to reach USD 877.6 million by 2035, driven by the universal need for specialized skills in qubit fabrication, error correction middleware, and hybrid classical-quantum integration.

What is the CAGR of the Japan Quantum Computing Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 28.0% from 2026 to 2035, reflecting the accelerating scaling of qubit counts and the persistent shortage of internal quantum engineering talent.

What factors are driving the growth of the Japan Quantum Computing Market?

▾ Key drivers include the national quantum talent gap, the imperative to simulate novel materials for energy transition, the management complexity of NISQ devices, and the surge in demand for quantum-safe cryptographic migration amid evolving data sovereignty laws.

What are the major trends in the Japan Quantum Computing Market?

▾ Major trends include the integration of Generative AI into quantum circuit design, the rise of Green Quantum benchmarking, the demand for industry-specific solution blueprints, and the focus on Quantum Error Suppression within complex superconducting environments.

Who are the key players in the Japan Quantum Computing Market?

▾ Key players include domestic hardware giants like Fujitsu, NEC, and Toshiba, as well as the quantum divisions of global cloud providers like IBM Japan, AWS Japan, and specialized quantum software startups like QunaSys and blueqat.

How is the Japan Quantum Computing Market segmented?

▾ The market is segmented by Offering, Deployment, Qubit Count, Technology, Application, and End-User Industry.