What is the Japan Semiconductor Market Size?

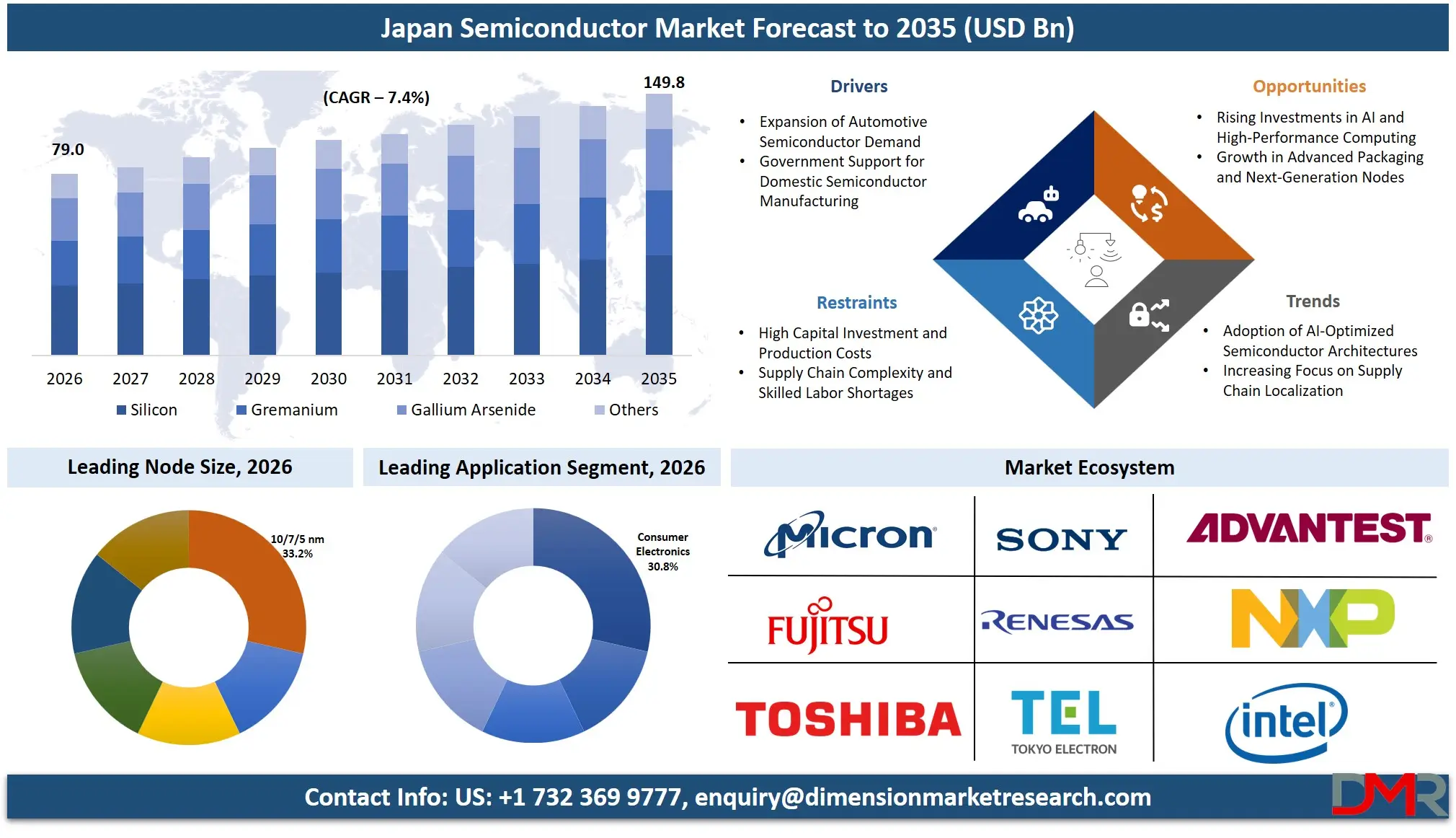

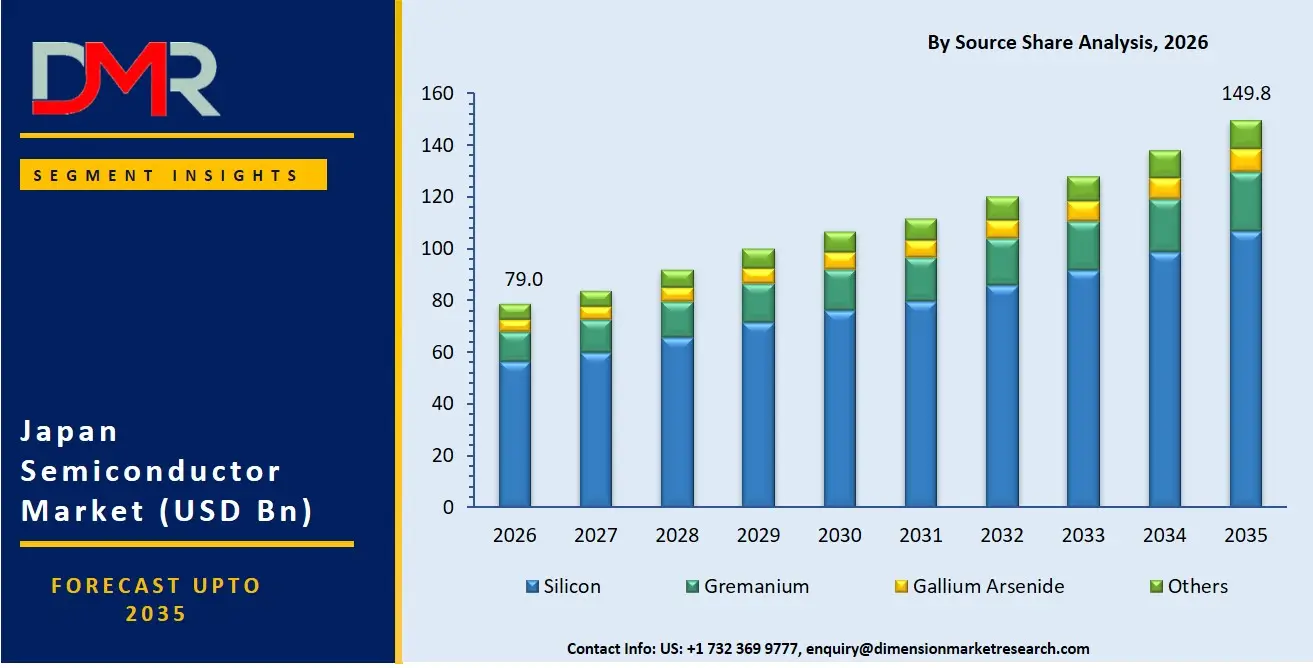

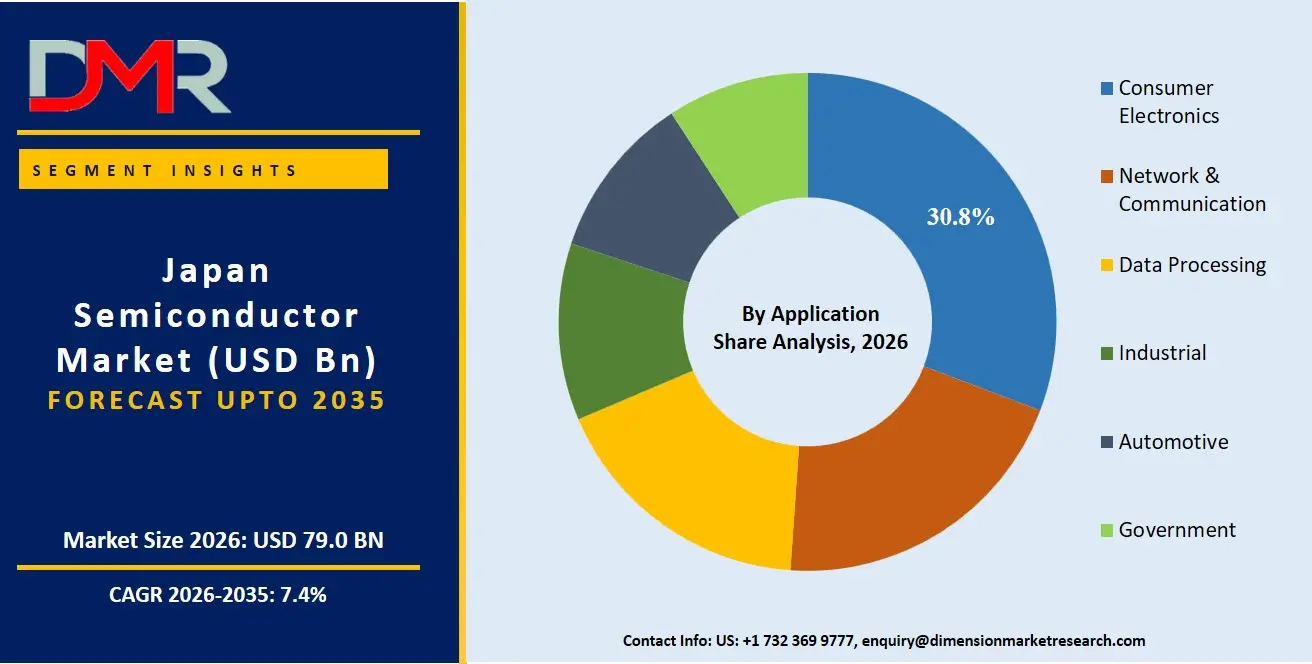

The Japan Semiconductor Market size is expected to be USD 79.0 billion in 2026 and increase at a compound annual growth rate of 7.4% to USD 149.8 billion in 2035 owing to Japan's thriving automotive industry.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Market for Japan Semiconductor refers to the design, production, and delivery of integrated circuits, memory chips, processors, sensors, and power devices for various end-user industries including the automotive industry, consumer electronics, industrial automation, telecommunication, and data processing applications. This market is witnessing growth owing to increased use of AI computing, electric cars, 5G network, and advanced packaging. Government support programs for semiconductor manufacturing and localizing semiconductor supply chain operations are also aiding semiconductor industry growth in Japan.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Key Takeaways

- Market Size & Forecast: The Japan Semiconductor Market size is projected to reach USD 79.0 billion in 2026 and is anticipated to have a value of USD 149.8 billion in 2035.

- Growth Rate & Outlook: The Japan Semiconductor Market size is set to grow at a compound annual growth rate of 7.4% during the forecast period of 2026 to 2035.

- Primary Growth Drivers: Some of the major growth drivers in the market are Semiconductor Needs in Automobiles, and more.

- Key Market Trends: Some of the major trends in the market are AI-Oriented Semiconductor Architecture Adoption, and more.

- By Node Size: 10/7/5 nm segment is anticipated to get the majority share of the Japan Semiconductor Market in 2026.

- By Application: Consumer Electronics is expected to get the largest revenue share in 2026 in the Japan Semiconductor Market.

- By Source: Silicon segment is expected to get the largest revenue share in 2026 in the Japan Semiconductor Market.

What is the Japan Semiconductor?

Semiconductors are electronic parts that manage, process, and store information using integrated circuits, memory chips, sensors, processors, and power semiconductors. The industry serves a wide range of applications in consumer electronics, automotive components, industrial automation, telecoms networks, and artificial intelligence platforms. An increase in demand for fast computers, electric cars, 5G networks, and edge computing systems will further boost the growth of the industry through technological advancements and innovations in the area of manufacturing processes and semiconductor packaging. Investment in local production capacity, resilient supply chains, and next-gen nodes will further enhance industry growth.

Use Cases

- Semiconductor Usage in Automotive Electronics: These semiconductors are vital components of advanced driver assistance systems, battery management systems in electric cars, autonomous driving systems, and infotainment systems integrated in the vehicles. Electrification and an increase in connectivity solutions in the mobility segment is expected to drive the adoption of reliable and energy-efficient automotive semiconductors among Japanese automakers.

- Semiconductor Usage in Consumer Electronics: It involves the application of memory semiconductors, sensors, and processors for smartphone devices, video game consoles, TV, wearable devices, and smart home products. Rising demands for efficient and compact semiconductor-powered devices are likely to motivate these firms to develop better semiconductor design architectures.

- Semiconductor Usage in Industrial Automation: In the current scenario, these semiconductors find extensive use in robotic and automation systems, PLCs, and IoT-enabled industrial applications. The rapid proliferation of smart manufacturing and industry 4.0 trends is increasing the need for semiconductor products that can perform real-time operations.

- Usage of Semiconductors in Data Center & AI Computing: It implies semiconductors used in cloud infrastructures, accelerators for artificial intelligence computing, GPUs, and high-speed networking infrastructure. With rising digitalization and generative AI applications along with massive investments in hyperscale data centers, the demand for semiconductors has been significantly boosted.

How AI Is Transforming the Japan Semiconductor Market

Innovation in semiconductor manufacturing is also being driven through artificial intelligence with the use of predictive maintenance, defect detection, and process optimization in manufacturing processes. Artificial intelligence improves yield management, reduces downtime, and increases efficiencies in semiconductor manufacturing processes. Semiconductor firms are incorporating the application of machine learning in accelerating chip design processes, saving on energy costs, and improving manufacturing accuracy.

The incorporation of AI is also resulting in high demands for processors that can perform intensive computations. Generative artificial intelligence, autonomous systems, and intelligent automation are leading to the development of semiconductors suited to handle these innovations. This innovation is also contributing to smarter factories, automated inspection, and improved supply chain management in the semiconductor industry.

Market Dynamic

Driving Factors in the Japan Semiconductor Market

Semiconductor Needs in Automobiles

There is substantial growth of semiconductor needs owing to Japan's thriving automotive industry. The use of semiconductors in EVs, advanced driver assistance systems, and automotive electronics is increasing rapidly. Vehicles in modern times consist of thousands of semiconductors in the form of sensors, audio visual systems, and battery controllers. Increased focus on connectivity and hybrid technologies has further raised demands for semiconductors.

Restraints in the Japan Semiconductor Market

Expensive Manufacturing Process and Cost of Production

The production of semiconductors requires huge capital costs to support highly sophisticated machinery, equipment, and processes for manufacture. With increased cost of operations, increased energy cost, and cost of raw materials, the cost of producing semiconductors becomes a challenge. The small players in the market have difficulty coping with large-scale semiconductor companies around the world.

Opportunities in the Japan Semiconductor Market

Increased Investments in AI and HPC Technologies

An increased adoption of artificial intelligence, machine learning, and cloud computing technologies creates many opportunities for semiconductor companies to develop advanced semiconductor products. There is currently a growing demand for accelerators for AI, graphics processing units, and high bandwidth memory chips. Japanese semiconductor firms have an opportunity to make use of this market potential.

Trends in the Japan Semiconductor Market

AI-Oriented Semiconductor Architecture Adoption

There is a quick pace of growth in AI-oriented semiconductor architecture development with the aim of providing faster data processing and energy efficiency. The companies are developing neural processing units, edge AI chips, and accelerators to cater to the needs of generative AI.

Research Scope and Analysis

This report covers a broad range of aspects associated with the Japanese semiconductor industry, including type of components, materials used for production, node sizes, applications, verticals, and technological innovations. The report studies the impact of various growth drivers, competitive dynamics, investments, and demand trends related to automotive, consumer electronics, industrial automation, and artificial intelligence computing markets.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Component Analysis

The memory devices are expected to maintain their supremacy position by garnering a market share of around 28.6% in the year 2026 on account of rising demand from the artificial intelligence server, consumer electronics, and high-performance computing end-user industries. The increasing deployment of data-centric technologies, cloud-based systems, and gaming technologies will drive the prominence of DRAM and NAND Flash semiconductors. The logic devices market segment will experience robust growth on account of increased usage in processors, GPUs, and communication systems. The sensor segment is poised to be the fastest growing segment on account of increasing installation in automotive safety systems, industrial automation systems, and IoT technologies.

By Source Analysis

Silicon will hold major market dominance in the coming year 2026 with a forecasted market share of 71.4%, thanks to the widespread application of silicon in the production of integrated circuits, memory chips, processors, and power devices. Semiconducting properties of silicon come at relatively low costs, are scalable, and have good electrical characteristics; thus, they are favored across consumer electronic, automotive, and industrial products. Gallium arsenide is predicted to show rapid growth owing to the rising usage of gallium arsenide semiconductors in various high-frequency communication and 5G network infrastructure equipment and other military applications. Germanium semiconductors find uses in optical and high-speed applications.

By Node Size Analysis

Market share of 10/7/5 nm nodes is expected to be about 33.2% by 2026 driven by an increased demand for advanced processors, AI accelerators, and high-performance mobile chips because these nodes ensure efficient power consumption, high speeds of execution, and higher transistor densities. The 5 nm segment is estimated to have the highest CAGR owing to the growing preference of semiconductor players toward high-performance computing and efficient systems. 32/28 nm and 65 nm nodes will continue meeting requirements of automotive, industrial, and embedded markets where longevity of products is crucial. The progress made in EUV lithography is facilitating the adoption of smaller node technology.

By Application Analysis

The consumer electronics segment is anticipated to have the highest market share of around 30.8% by 2026 on account of high semiconductor usage in mobile phones, gaming consoles, smart devices, and wearable technology. The rise in the number of consumers demanding small and powerful electronic devices is continuing to help drive the growth in this segment. On account of the rising adoption of electric vehicles, self-driving cars, and automated driving assistance systems, the automotive segment is predicted to witness the highest growth rate. The industrial segment is also growing due to automation and the Industry 4.0 initiative.

The Japan Semiconductor Market Report is segmented on the basis of the following:

By Component

- Memory Devices

- Logic Devices

- MPU

- MCU

- Analog IC

- Sensors

- Power Devices

- Discrete Power Devices

- Others

By Source

- Silicon

- Germanium

- Gallium Arsenide

- Others

By Node Size

- 16/14 nm

- 10/7/5 nm

- 32/28 nm

- 65 nm

- 5 nm

- Others

By Application

- Network & Communication

- Data Processing

- Consumer Electronics

- Industrial

- Automotive

- Government

Competitive Landscape

The competition in the Japanese semiconductor industry is intense and is fueled by innovation and technological advancement coupled with robust manufacturing infrastructure and support from the government. Players in the market concentrate their efforts mainly on research and development, advanced node fabrication, and localizing the supply chain. Barriers to entry into the market are high due to the need for large financial investments, the complexities surrounding IP, and the skills required for operations. Manufacturers are becoming more involved in collaborating with other manufacturers internationally, entering joint ventures, and signing up supply contracts.

Some of the prominent players in the Japan Semiconductor are:

- Tokyo Electron Limited

- Renesas Electronics Corporation

- Sony Semiconductor Solutions Corporation

- Kioxia Holdings Corporation

- Rohm Co., Ltd.

- Mitsubishi Electric Corporation

- Toshiba Electronic Devices & Storage Corporation

- Fujitsu Limited

- Advantest Corporation

- Screen Holdings Co., Ltd.

- Disco Corporation

- Sumco Corporation

- Shin-Etsu Chemical Co., Ltd.

- Japan Display Inc.

- Murata Manufacturing Co., Ltd.

- NXP Semiconductors

- Micron Memory

- Intel Corporation

- Qualcomm Incorporated

- Samsung Electronics

- Other Key Players

Recent Developments

- In April 2026, The production and installation of machines for the manufacture of 3-nm chips is anticipated to commence in 2028 at the second foundry facility that TSMC is planning to build in Japan. It has been said that the facility will manufacture up to 15,000 twelve inch wafers in a month. This move by TSMC is a significant upgrade since previously its Japan plans had involved only matured nodes.

- In March 2026, The Tower Semiconductor Company has made known a plan of restructuring the company's Japan business via TPSCo, where the firm will fully own their 300mm Fab 7 facility, while Nuvoton Technology Corporation will fully own their 200mm Fab 5 facility. Both firms have agreed to enter into long-term contracts aimed at ensuring that supply to their existing clients is not interrupted, with the deal set to complete by 2027.

- In November 2025, FUJIFILM Corporation built a new development and evaluation facility at its Shizuoka Factory belonging to the FUJIFILM Electronic Materials. The development will help to improve the company's abilities for evaluating product performance and quality for the development of more efficient semiconductor materials while securing a stable supply due to an increasing demand resulting from artificial intelligence and future semiconductors.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 79.0 Bn |

| Forecast Value (2035) |

USD 149.8 Bn |

| CAGR (2026–2035) |

7.4% |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Component, By Source, By Node Size, By Application |

| Country Coverage |

Japan |

Frequently Asked Questions

How big is the Japan Semiconductor Market?

▾ The Japan Semiconductor Market size is expected to reach USD 79.0 billion by 2026 and is projected to reach USD 149.8 billion by the end of 2035.

What is the CAGR of the Japan Semiconductor Market from 2026 to 2035?

▾ The market is growing at a CAGR of 7.4 percent over the forecasted period.

What factors are driving the growth of the Japan Semiconductor Market?

▾ Semiconductor Needs in Automobiles, and more are the factors driving the growth of the Japan Semiconductor Market.

What are the major trends in the Japan Semiconductor Market?

▾ Growth in Adoption of Hybrid/Multi-Cloud Solutions, and more are some of the major trends in the market.

Who are the key players in the Japan Semiconductor Market?

▾ Some of the key players in the Japan Semiconductor Market include Micron, Sony, Renesas, and more

How is the Japan Semiconductor Market segmented?

▾ The Japan Semiconductor Market is segmented by component, source, node size, application.