What is the Smart Grid Market Size?

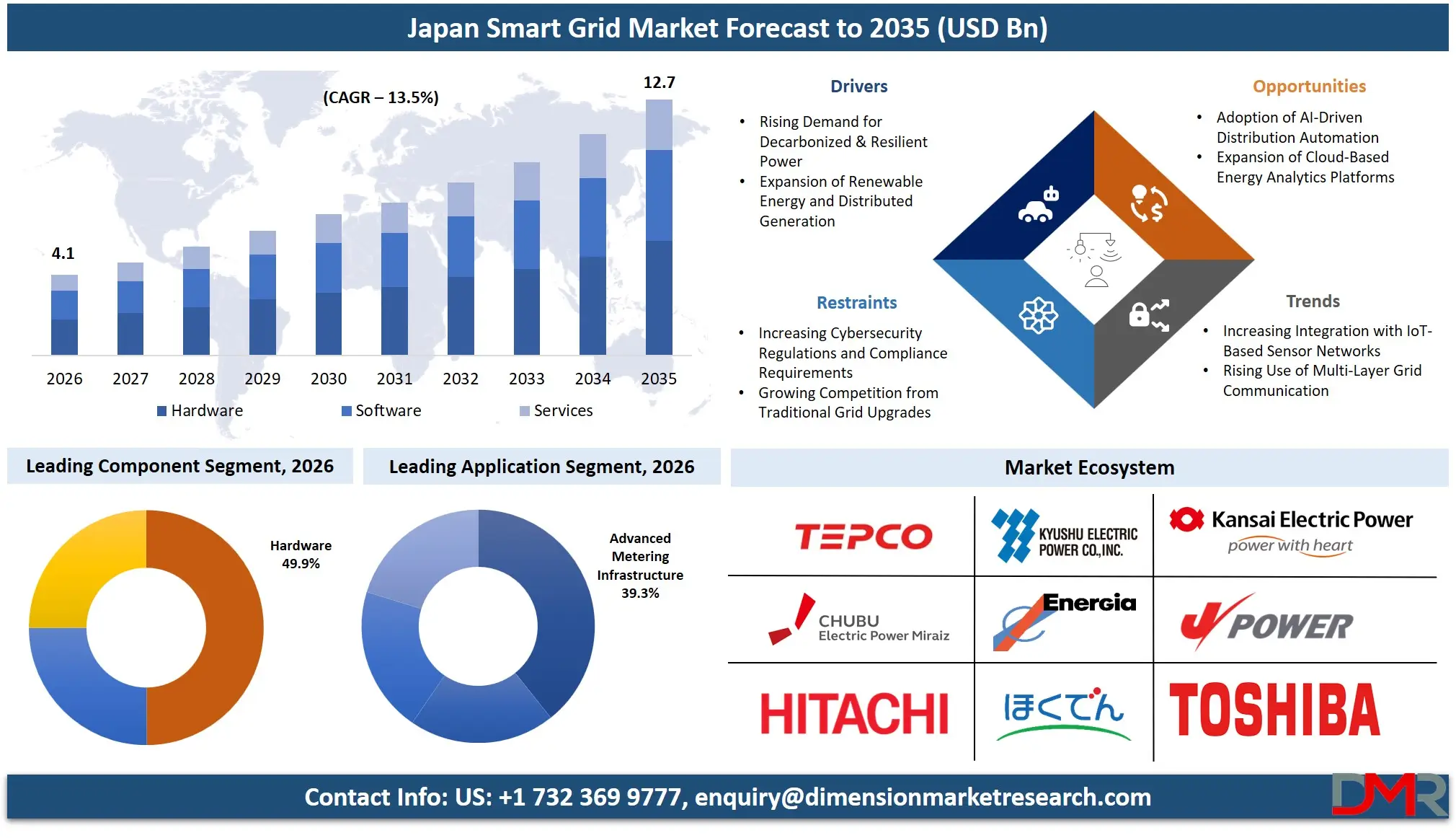

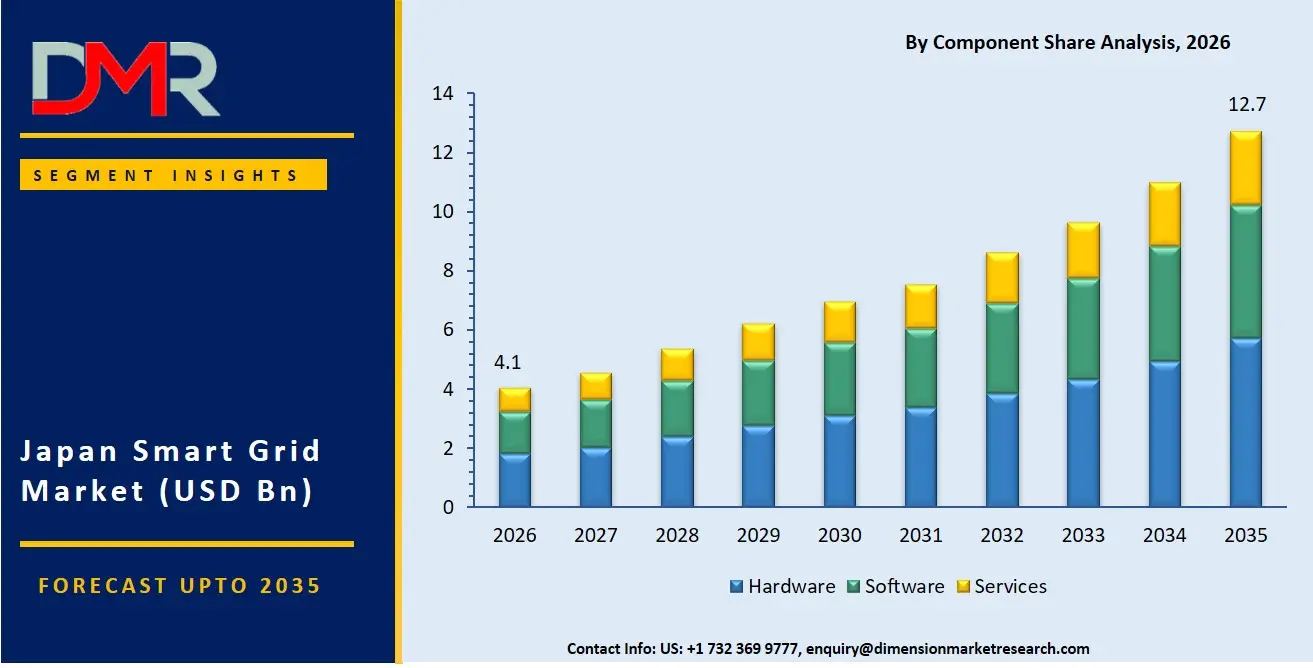

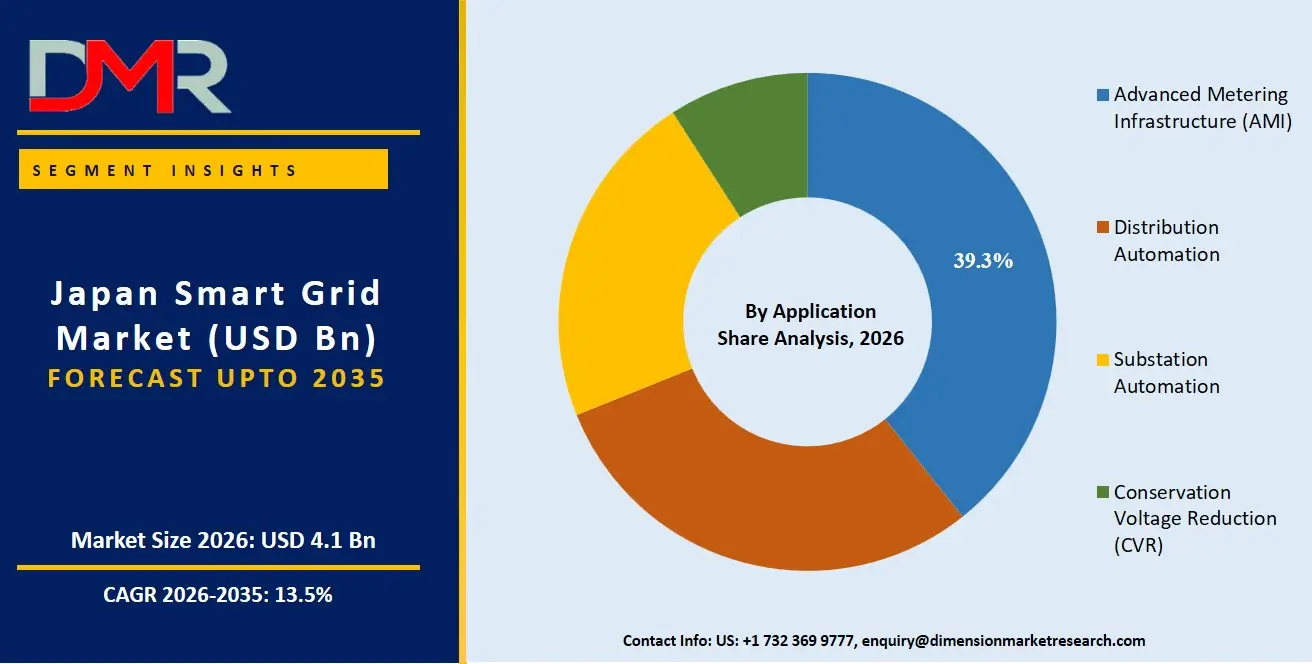

The Japan Smart Grid Market is expected to reach a value of USD 4.1 billion in 2026, and it is further anticipated to reach USD 12.7 billion by 2035, growing at a CAGR of 13.5% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The smart grid market has been showing consistent growth due to Japan's rising dependence on resilient, decarbonized, and decentralized energy systems for effective, secure, and scalable power distribution. This includes several grid platforms and expert services that help utilities and grid operators deploy intelligent solutions for residential, commercial, and industrial purposes. There has been a rising need for professional services owing to the requirements for implementing advanced metering infrastructure, securing operational continuity against supply disruptions, and delivering high-performance grid automation systems to customers. Utility operators have emerged as the largest consumer segment for smart grid services, with hardware components being the most popular choice due to their wide availability and reliability, while there has been rapid growth in software platforms and analytics services.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Key Takeaways

- Market Size & Forecast: The Japan Hydrogen FCV market is forecasted to be valued at USD 4.1 billion in 2026, growing incrementally to USD 12.7 billion by 2035, due to the joint efforts of energy strategy deployment on the part of enterprises as well as the obligatory deployment of zero-emission and resilient power technologies.

- Growth Rate & Outlook: Japan market is expected to grow at 13.5% CAGR, propelled by the urgent need to mitigate emerging renewable energy intermittency vulnerabilities, alongside increasing challenges in orchestrating multi-directional power flows from residential solar, commercial buildings, and industrial facilities.

- Primary Growth Drivers: Major driving factors comprise the transition from traditional centralized power grids towards modern intelligent distribution systems, the necessity to deploy secure and robust communication networks, as well as the implementation of grid management APIs necessitating unique platform & services expertise.

- Key Market Trends: Major trends encompass the introduction of AI-driven substation automation through commercial channels, usage of machine learning within wide area networks for demand forecasting and preventing power waste, and increased focus on cybersecurity amidst rising consumer safety considerations of regulators.

- By Component Analysis: The hardware segment is projected to dominate the Japan Smart Grid Market due to high demand for scalable metering and sensing platforms by utility operators, with capabilities like real-time monitoring, fault detection, and remote control, which offer daily operations, regional balancing, and real-time performance monitoring activities within grid management.

- By Network Architecture Analysis: The Wide Area Network (WAN) segment is projected to dominate the Japan Smart Grid Market due to its high bandwidth, reliability, capability for long-distance communication, and use in distribution automation, substation automation, and conservation voltage reduction for metropolitan areas, industrial zones, and government infrastructure.

- By Application Analysis: The Advanced Metering Infrastructure (AMI) segment is anticipated to dominate in the Japan Smart Grid Market as utility operators adopt systems that are scalable, flexible, efficient, accessible for real-time billing, provide AI-based consumption analytics, telematics integration, business continuity, and grid operations at a higher resolution.

What is the Smart Grid?

A Smart Grid is about the unique set of platforms and expertise involved in operating intelligent, digitally-enabled power networks. These grids, unlike conventional power systems, pertain to "the how and where" of high-reliability, real-time energy management. It entails having a Grid Platform to provide the means through which electricity is monitored and controlled for optimal distribution, and Services to help integrate utility management, manage demand response costs, and optimize load balancing. As companies take charge of their decarbonization commitments, it is important to have services that ensure that grids will be operated successfully while maintaining cost and safety measures.

Use Cases

- Utility Grid Resilience: Electric utilities employ Smart Grid Services for the installation of distribution automation solutions that include real-time fault detection and outage notifications to avoid supply interruptions and increase operational trust.

- Hospital Power Reliability: Hospital networks rely on Smart Grid Platforms for deploying uninterruptible power supply integration, ensuring stable, zero-outage operation, and maintaining compliance with regional health and safety mandates.

- Public Infrastructure Services: Municipal authorities incorporate substation automation APIs in order to push voltage schedules and grid adherence notifications to central control centers in real-time.

- Industrial Demand Response: Manufacturing organizations leverage energy analytics platforms in a cloud-based telematics suite to initiate geo-targeted load shedding during peak energy pricing seasons.

How AI is Transforming the Smart Grid Market?

AI is revolutionizing the smart grid industry through increased demand forecasting and predictive maintenance capabilities. The analytics platform suite includes AI-based systems that detect consumption anomalies and grid inefficiencies in order to resolve them instantaneously, thereby preventing any financial losses and operational damage. In addition, the AI-driven functions of distribution management services help organizations assess load behavior, determine optimal voltage schedules, and customize their outage planning. AI forms an essential part of governance and customer trust initiatives. Professional services involve intelligent agents that monitor compliance and keep grid maintenance logs free of any non-compliant entries while ensuring that all operations comply with regulations and the stringent cybersecurity protocols in Japan.

Market Dynamics

Key Drivers in the Japan Smart Grid Market

Rising Demand for Decarbonized & Resilient Power

AI is revolutionizing the smart grid industry through increased demand forecasting and predictive maintenance capabilities. The analytics platform suite includes AI-based systems that detect consumption anomalies and grid inefficiencies in order to resolve them instantaneously, thereby preventing any financial losses and operational damage. In addition, the AI-driven functions of distribution management services help organizations assess load behavior, determine optimal voltage schedules, and customize their outage planning. AI forms an essential part of governance and customer trust initiatives. Professional services involve intelligent agents that monitor compliance and keep grid maintenance logs free of any non-compliant entries while ensuring that all operations comply with regulations and the stringent cybersecurity protocols in Japan.

Expansion of Renewable Energy and Distributed Generation

The rapid development of renewable energy integration in Japan creates high demands in the power sector in various fields such as residential solar, commercial storage, industrial microgrids, and community energy management. Companies today use smart grid solutions to achieve critical goals related to carbon neutrality, load optimization, asset tracking, and regulatory compliance. With increased use of distributed energy resources by many utility operators, grid owners have become more interested in adopting an automated distribution management system that can handle large data volumes effectively. In addition, there is a growing need for predictable demand response experiences for grid managers, which increases the adoption rate of smart grid platforms.

Restraints in the Japan Smart Grid Market

Increasing Cybersecurity Regulations and Compliance Requirements

The increasingly stringent grid cybersecurity regulations and data protection legislations in Japan have brought about difficulties for the smart grid vendors as well as utility operators. The regulatory bodies are tightening their grip on the control of grid communication deployments, the acquisition and management of data consents from local communities, and encryption measures in order to minimize risks related to cyber intrusions. Enterprises are expected to adhere to the highly stringent operational requirements, making their deployments more complicated and costly. The violation of such rules subjects a utility operator using smart grids to heavy fines, delivery delays, and reputational harm.

Growing Competition from Traditional Grid Upgrades

Growth in the usage of conventional power infrastructure with limited digitalization is impacting the future growth of smart grids within Japan. Traditional systems are preferred over intelligent grids for certain rural applications since they offer lower upfront costs and reduced communication complexity for remote area purposes. Some utility operators have also begun using legacy SCADA systems as part of their daily operations, relying less on cloud-based campaigns. The use of conventional systems also offers simpler maintenance solutions without advanced analytics. Traditional smart grid services are under growing pressure from competing legacy infrastructure investments.

Growth Opportunities in the Japan Smart Grid Market

Adoption of AI-Driven Distribution Automation

There exist many growth opportunities in the smart grid market in Japan through the increasing implementation of distribution automation systems. These intelligent solutions allow utility operators to engage in real-time, fault-tolerant power distribution other than using standard manual switching. Higher reliability, rapid fault isolation, and lower total cost of ownership are some features that may be implemented by grid operators in decarbonizing their networks. Energy providers based in Japan are starting to consider implementing distribution automation as an alternative for effective green grid management. With improved communication infrastructure by telecom suppliers and improved sensor durability, many transmission organizations will spend much money on advanced grid automation systems.

Expansion of Cloud-Based Energy Analytics Platforms

Integration of cloud computing in grid analytics platforms is bringing about great prospects for smart grid providers in Japan. Many utility operators are now using cloud-based analytics technology that automates demand response processes in order to offer predictive maintenance support to grid managers. AI can help organizations understand consumption behavior, customize voltage schedules, and determine when the best time is for preventive maintenance in order to maximize operational uptime and cost savings. The increasing use of machine learning analytics, intelligent automation, and predictive diagnostics in different sectors such as residential, commercial, and industrial operations is driving demand for innovative analytics technology.

Trends in the Japan Smart Grid Market

Increasing Integration with IoT-Based Sensor Networks

Increasingly, Japanese utility operators are adopting IoT-based sensor networks by integrating smart grid services that help improve scalability and fault automation. IoT telemetry allows organizations to easily integrate grid device APIs into their outage management systems, workforce management solutions, and maintenance processes without having to invest heavily in their existing IT infrastructure. The advantages associated with IoT telemetry include real-time asset management, power quality analytics, and multi-site engagement options. Due to the growing adoption of digital transformation approaches in addition to remote grid management processes, the use of IoT telemetry has been steadily increasing. The adoption of IoT telemetry as an alternative to more expensive on-premise grid solutions has continued to gain popularity in Japan.

Rising Use of Multi-Layer Grid Communication

Multi-layer approaches are being incorporated by Japanese utility firms in order to facilitate their grid operations using a combination of WAN, NAN, HAN, and AI-based load balancing. Companies are focusing on creating an integrated grid experience that ensures consistency in the quality of power delivery through different communication modes. Smart grid solutions continue to be an integral part of these multi-layer approaches owing to their real-time visibility and rapid fault response. Companies from sectors such as residential energy management, industrial power procurement, and municipal services have been incorporating smart grids into their digital utility management solutions.

Research Scope and Analysis

The Japan Smart Grid Market is segmented by component, network architecture, application, and end user. The market supports residential energy management, commercial demand response, industrial automation, and government infrastructure across individual consumers, utility operators, public authorities, and energy companies through cloud-based and on-premise grid management solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Component Analysis

Hardware components are expected to lead the Japan Smart Grid Market in 2026 with a projected market share of 49.9% as a result of utility operators' growing preference for scalable metering and sensing platforms. Japanese utilities have developed a preference for smart meters, sensors, and PLCs for performing such functions as consumption tracking, outage detection, and real-time voltage control. Software solutions are likely to occupy the second place with a 24.2% share due to the rising trend in favor of AI-driven analytics and grid optimization across distribution networks. Services, though currently at a 17.1% share, is expected to grow steadily as a consequence of increased knowledge about system integration and ongoing maintenance requirements, particularly for grid modernization projects in Tokyo, Osaka, and Nagoya.

By Network Architecture Analysis

Wide Area Network (WAN) is projected to dominate the Japan Smart Grid Market in 2026, with an estimated share of 45.3%, owing to its widespread adoption in distribution automation, substation automation, and transmission network monitoring. Japanese grid operators and energy aggregators favor WAN because it provides reliable long-distance communication along with high bandwidth and low latency. Neighborhood Area Network (NAN) follows, driven by increasing smart meter concentration in residential clusters and localized demand response programs targeting regional utilities. Home Area Network (HAN) is primarily used by residential prosumers with rooftop solar systems and home energy management systems. Low Power Wide Area Network (LPWAN) is growing rapidly due to increased sensor deployments for grid-edge monitoring and distributed energy resource aggregation in rural and semi-urban areas with limited existing infrastructure.

By Application Analysis

Advanced Metering Infrastructure (AMI) is set to dominate the Japan Smart Grid Market in 2026 with a projected share of 39.3%, thanks to its high deployment penetration, government-backed rollout programs, and low complexity for end-users. AMI solutions enable real-time billing, remote disconnect capabilities, and granular consumption analytics that do not necessitate additional hardware investment. Distribution Automation will experience robust growth in the coming years because of heightened utility preference for fault detection and service restoration reliability. Smart grid network management systems, affordability of intelligent field devices, and knowledge about self-healing grid benefits have spurred distribution automation adoption among regional power companies. Substation Automation is growing rapidly as transmission operators modernize legacy infrastructure. Conservation Voltage Reduction (CVR) holds 9.6% share, primarily deployed in densely populated prefectures to reduce peak demand and improve energy efficiency.

By End User Analysis

The Industrial segment is projected to continue dominating in the Smart Grid Market of Japan, with an expected market share of 46.9% in 2026, owing to robust energy intensity targets and demand response participation, as well as heavy reliance on real-time power quality and load management solutions. Businesses in the Industrial segment are increasingly adopting smart grid technologies due to the benefits offered by such systems, including lower electricity costs, predictable production scheduling, and regulatory compliance with energy efficiency mandates. The Commercial segment is expected to experience the fastest growth, thanks to the increasing deployment of building energy management systems, smart HVAC controls, and lighting automation funded by green building incentives. Other significant end users include Residential with home energy management systems and time-of-use optimization, and Government, providing smart streetlighting and public infrastructure grid modernization as part of municipal decarbonization initiatives.

The Japan Smart Grid Market Report is segmented based on the following:

By Component

- Hardware

- Smart Meters (AMI Meters)

- Sensors

- Programmable Logic Controllers (PLCs)

- Networking Devices

- Grid Infrastructure Equipment

- Software

- Advanced Metering Infrastructure (AMI) Software

- Smart Grid Distribution Management Systems (DMS)

- Smart Grid Network Management Systems

- Substation Automation Systems

- Energy Analytics & Forecasting Platforms

- Services

- Consulting

- System Integration & Deployment

- Support & Maintenance

By Network Architecture

- Home Area Network

- Neighborhood Area Network

- Wide Area Network

- Low Power Wide Area Network

By Application

- Advanced Metering Infrastructure (AMI)

- Distribution Automation

- Substation Automation

- Conservation Voltage Reduction (CVR)

By End User

- Residential

- Commercial

- Industrial

- Government

Competitive Landscape

The dynamics of competition in the Japan Smart Grid marketplace have developed to become increasingly dynamic, with a wide range of multinational technology providers, Japanese grid infrastructure aggregators, and analytics platform players specializing in various niche grid management functions. The essential ingredient for success is found in deep-seated strategic partnerships with renewable energy developers and utility operators in Japan, which open up high-quality supply chains and allow premium grid maintenance services to be sold alongside one another. Market consolidation trends are moving rapidly ahead, with established players in the world of industrial automation and energy providers taking on acquisitions of specialized analytics platform providers to leverage their AI forecasting functionalities. Proprietary intellectual property rights, with AI-based predictive maintenance algorithms and load optimization engines, hold increasing importance compared to just competitive hardware pricing and communication networks.

Some of the prominent players in the Japan Smart Grid Market are:

- Tokyo Electric Power Company Holdings, Inc.

- The Kansai Electric Power Co., Inc.

- Chubu Electric Power Co., Inc.

- Kyushu Electric Power Co., Inc.

- The Chugoku Electric Power Co., Inc.

- The Hokkaido Electric Power Co., Inc.

- Electric Power Development Co., Ltd. (J-POWER)

- Hitachi, Ltd.

- Mitsubishi Electric Corporation

- Toshiba Energy Systems & Solutions Corporation

- Fujitsu Limited

- NEC Corporation

- Panasonic Holdings Corporation

- Fuji Electric Co., Ltd.

- Yokogawa Electric Corporation

- Sumitomo Electric Industries, Ltd.

- OMRON Corporation

- Mitsubishi Heavy Industries, Ltd.

- NTT DATA Corporation

- Siemens AG

- Other Key Players

Recent Developments

- May 2026: Siemens AG announced the next evolution of its Gridscale X platform, introducing AI-powered agentic transmission planning and a unified digital grid management foundation enabling utilities to operate closer to technical limits and integrate third-party applications for grid optimization.

- January 2026: Tokyo Electric Power Company Holdings, Incorporated (TEPCO) announced a major restructuring move involving the sale of up to 26 billion shares in affiliate Kandenko, aiming to raise capital for grid investment, financial stabilization, and expansion into green and digital transformation projects.

- October 2025: Hitachi, Ltd. signed a Memorandum of Understanding with the United States Department of Commerce to advance grid modernization and electrification initiatives, strengthening cross-border investment in modern power grid infrastructure driven by rising electricity demand from AI data centers.

- April 2025: Mitsubishi Electric Corporation announced the rollout of its next-generation energy management and grid control solutions, enhancing real-time monitoring, renewable energy integration, and AI-driven demand-supply balancing capabilities for utility-scale smart grid operations in Japan.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 4.1 Bn |

| Forecast Value (2035) |

USD 12.7 Bn |

| CAGR (2026–2035) |

13.5% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Component, By Network Architecture, By Application, By End User |

| Country Coverage |

Japan |

Frequently Asked Questions

How big is the Japan Smart Grid Market?

▾ The Japan Smart Grid Market is poised to be valued at USD 4.1 billion in 2026 and is projected to reach USD 12.7 billion by 2035, driven by the universal need for secure, scalable, and reliable digital customer communications.

What is the CAGR of the Japan Smart Grid Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 13.5% from 2026 to 2035, reflecting the maturing nature of the SMS market and the accelerating complexity of multi-channel, interactive engagement strategies.

What factors are driving the growth of the Japan Smart Grid Market?

▾ Key drivers include the decarbonization imperative for carbon reduction, the need to modernize legacy power grid systems, the management complexity of multi-directional renewable energy orchestration, and the surge in demand for distribution automation amid evolving grid resilience laws.

What are the major trends in the Japan Smart Grid Market?

▾ Major trends include the integration of AI into demand forecasting and predictive maintenance, the rise of substation automation on commercial channels, the demand for vertical-specific analytics solutions, and the focus on secure, cyber-resilient grid communication practices.

Who are the key players in the Japan Smart Grid Market?

▾ Key players include Toshiba Energy Systems, Hitachi, Ltd., Tokyo Electric Power Company Holdings, Inc., Mitsubishi Electric, and Fuji Electric Co., Ltd., alongside Japanese utility infrastructure leaders such as Kansai Electric Power Co., Inc., and many more.

How is the Japan Smart Grid Market segmented?

▾ The market is segmented by vehicle type, fuel cell technology, operating range, and end user.