Market Overview

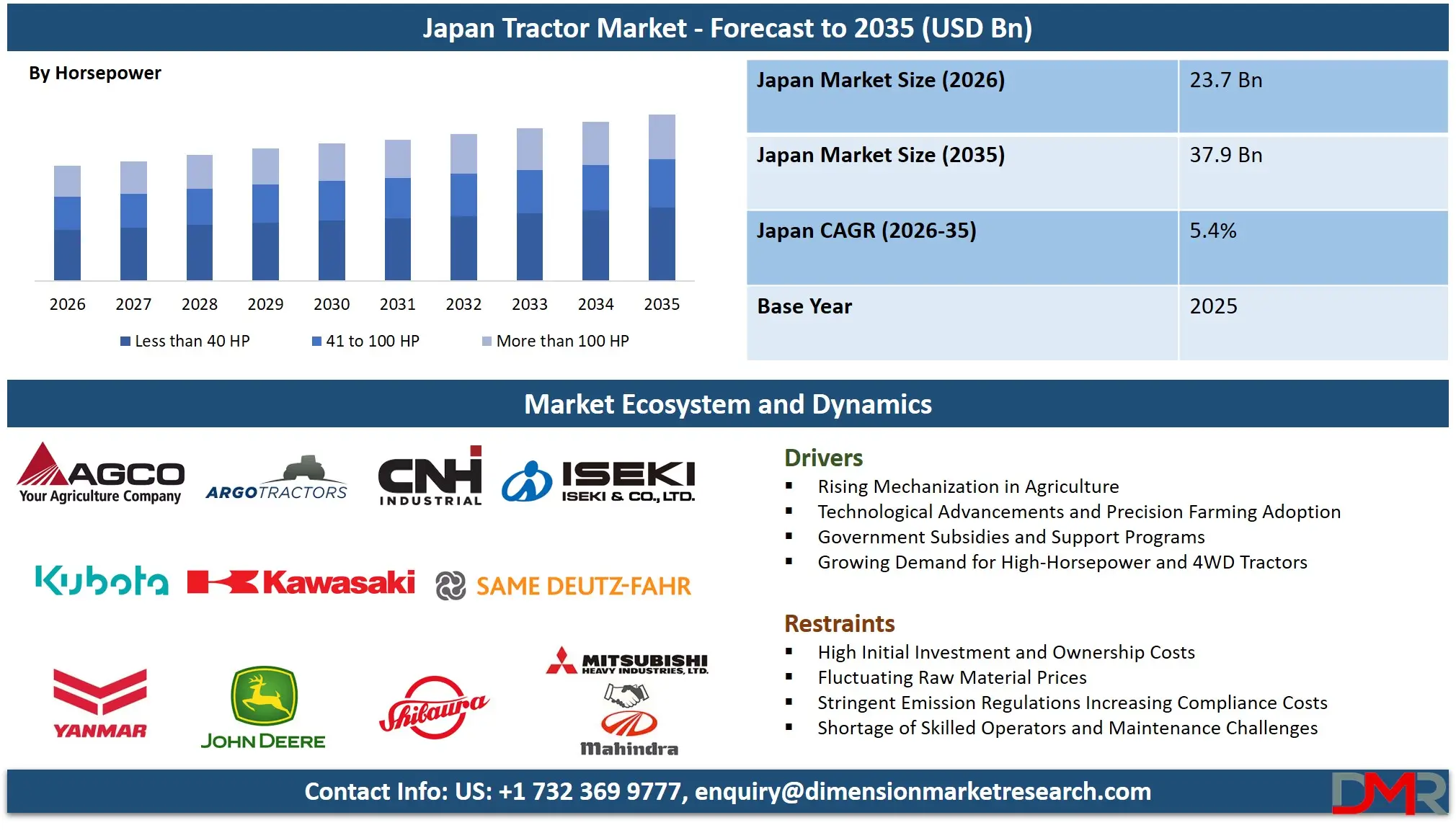

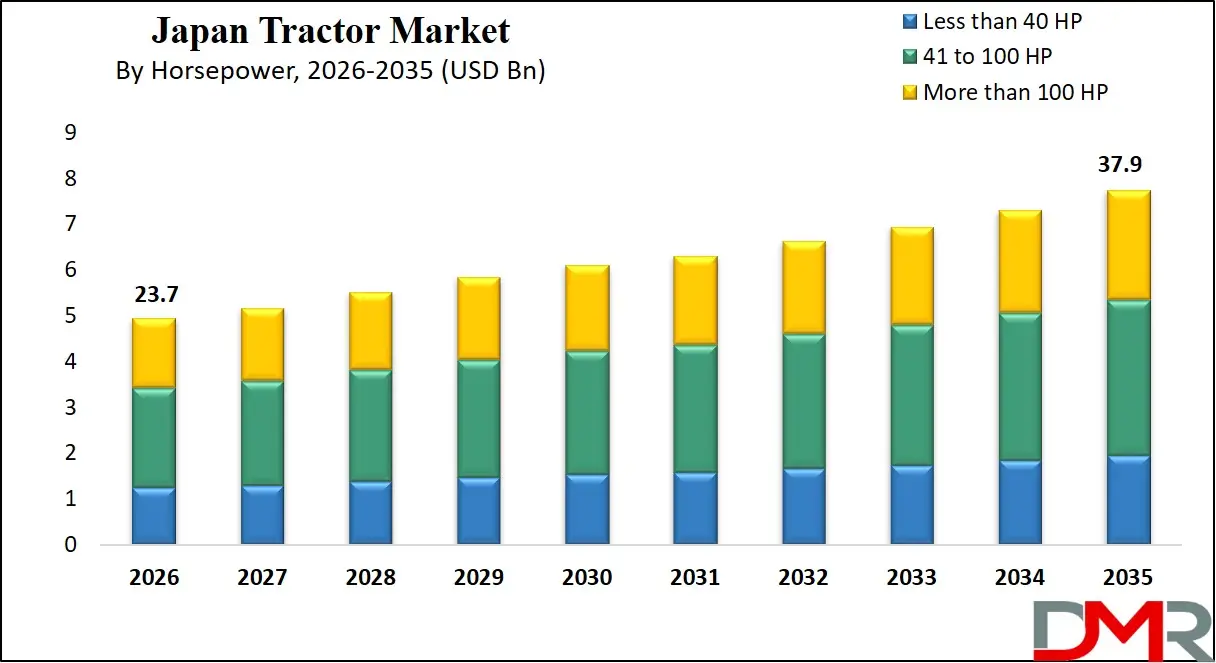

The Japan Tractor Market is projected to be valued at USD 4.9 billion by 2026 and is expected to grow at a modest compound annual growth rate (CAGR) of 5.1% through 2035, reaching a market value of USD 7.7 billion. This growth trajectory is underpinned by the critical need to maintain food security and agricultural productivity in the face of a rapidly aging farming workforce. The market is driven by the adoption of labor-saving technologies, including autonomous tractors and smart farming solutions, which are essential for the survival of Japan's small-scale, part-time farming sector. Government initiatives promoting smart agriculture, coupled with the consolidation of farmland into larger, more efficient units, are key factors sustaining demand for new machinery.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Japanese tractor market is a technologically advanced but mature market, characterized by a high penetration of compact and medium-horsepower machines suited to the country's small, irregularly shaped paddy fields and upland farms. The national imperative to boost agricultural efficiency with fewer workers is accelerating the shift towards ICT-enabled machinery, including GPS-guided tractors and robots. This focus on innovation ensures that Japan remains a leading market for cutting-edge agricultural technology, despite overall volume stagnation.

Trends within the market show a decisive move towards "Smart Agriculture." There is strong adoption of tractors equipped with auto-steering, variable-rate technology, and farm management software. The government's strategic push to reduce the average age of farmers and attract new entrants is creating demand for user-friendly, automated machinery. Furthermore, the market is seeing a rise in specialized machinery for Japan's unique agricultural products, such as rice, vegetables, and fruits, with a focus on precision and reduced soil compaction.

Opportunities in the Japan tractor market are centered on technological solutions for labor scarcity. The development and commercialization of autonomous or "driverless" tractors represent a significant growth area. There is also potential in the aftermarket for retrofit kits that can add smart capabilities to existing machinery. Manufacturers are also exploring the use of robotics and AI for specialized tasks like fruit picking and weeding, which are currently highly labor-intensive. The government's strong financial backing for smart agriculture pilots creates a fertile ground for innovation and early adoption.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Restraints facing the sector include the persistent trend of farmland abandonment and a declining number of commercial farming households, which structurally caps the total available market. The high cost of advanced smart tractors can be prohibitive for part-time farmers, despite subsidies. Additionally, the topographical challenges of Japanese agriculture with many fields on terraces or in mountainous areas limit the applicability of large, high-horsepower machinery. Despite these challenges, the essential role of mechanization in sustaining Japan's food production system ensures a stable, albeit slowly growing, market focused on high-value, technologically advanced equipment.

Japan Tractor Market: Key Takeaways

- The Market Size Insights: The Japan Tractor Market size is estimated to have a value of USD 4.9 billion in 2026 and is expected to reach USD 7.7 billion by the end of 2035.

- The Market Growth Rate Insights: The market is growing at a CAGR of 5.1 percent over the forecasted period of 2026-2035.

- Smart Agriculture Mandate: Leading players like Kubota, Yanmar, and Iseki are at the forefront of developing and deploying autonomous tractors and ICT-based smart farming solutions, driven by government policy and severe labor shortages.

- Focus on Automation: Companies are heavily investing in robotics and AI to create tractors and implements that can perform tasks like tilling, transplanting, and weeding with minimal human intervention.

- Compact Tractor Dominance: The market is dominated by compact and mid-sized tractors (particularly under 40 HP and 41-100 HP), which are ideally suited for Japan's small-scale paddy fields and mixed farming operations.

- Government-Led Innovation: Initiatives like the "Smart Agriculture" project by MAFF are providing subsidies and test fields, accelerating the real-world adoption of connected and autonomous machinery.

- Sustainability Through Efficiency: The focus is on developing fuel-efficient engines and electric/hybrid compact tractors to reduce the carbon footprint of agriculture and meet environmental targets.

- After-Sales & Service Networks: Given the technological complexity of new machinery, robust dealer networks and after-sales support are critical competitive differentiators for brands like Kubota and Yanmar.

- Autonomous Solutions: Deere & Company (through its acquisition of Blue River Technology) and local players are pioneering smaller-scale autonomous solutions tailored for row crops and specialty agriculture in the Japanese context.

- Strategic Partnerships: Collaborations, such as Kubota's work with NTT Group on utilizing 5G for farm management and Yanmar's partnerships with AI startups, are crucial for integrating digital technologies into agricultural machinery.

Japan Tractor Market: Use Cases

- Paddy Rice Farming: Tractors are essential for primary tillage, puddling, and leveling in paddy fields, often working in tandem with specialized transplanters and combine harvesters in Japan's most dominant agricultural sector.

- Upland and Vegetable Farming: In regions dedicated to vegetables, potatoes, and wheat, tractors are used for plowing, rotary tilling, bed shaping, and as a power source for various planting and harvesting attachments.

- Orchards and Fruit Production: Specialized narrow tractors are employed in orchards for mowing, spraying, and light hauling, navigating the tight spaces between fruit trees in apple, citrus, and persimmon farms.

- Livestock and Dairy Operations: On Hokkaido's large-scale dairy farms, tractors are crucial for forage harvesting, baling, feed mixing and distribution, and manure management.

- Public Works and Landscaping: Compact tractors with front loaders and mowers are widely used by municipal governments for park maintenance, roadside verge trimming, and by landscaping companies for grounds upkeep.

Japan Tractor Market: Stats & Facts

Ministry of Agriculture, Forestry and Fisheries (MAFF) - Census of Agriculture and Forestry

- There were approximately 1.03 million commercial farming households in Japan in 2023.

- The total area of cultivated land was approximately 4.3 million hectares in 2023.

- The average area of cultivated land per agricultural sales entity was about 7.5 hectares, but this varies dramatically, with Hokkaido averaging over 25 hectares and other prefectures under 2 hectares.

- The value of gross agricultural output was approximately JPY 8.9 trillion (approx. USD 60 billion) in 2023.

- The census shows a continued trend of farmland consolidation, with larger, more efficient farms (e.g., organizational entities) accounting for a growing share of production.

- Approximately 70% of farm operators are 65 years or older, highlighting the critical labor shortage.

- Machinery inventory data shows a high stock of 4WD compact tractors (under 30 HP), predominantly used in paddy farming.

MAFF - Smart Agriculture Related Surveys

- MAFF's 2023 survey on smart agriculture indicated that over 50% of large-scale farms and farming corporations have introduced at least one form of smart agricultural machinery (e.g., auto-steer tractors, drones).

- The adoption rate of GPS-guided auto-steer tractors has been growing steadily, particularly in Hokkaido and among large-scale paddy farmers in other regions.

- The number of "farmer's market" online platforms for direct sales of agricultural products continues to increase, reflecting the trend of internet use for marketing.

MAFF / Statistics Bureau

- The agricultural workforce was approximately 1.16 million in 2023, a decline of 4.2% from the previous year.

- The average age of farmers actively engaged in farming as their main occupation is 68.4 years old.

- MAFF's statistics on farm management costs show that machinery expenses (depreciation, fuel, repairs) consistently rank among the top production costs for both crop and livestock farms.

National Agriculture and Food Research Organization (NARO) / Academic Research

- NARO is a key driver in developing and disseminating robotics and AI for agriculture, including the "robot tractor" and "smart feeding system" projects.

- Research indicates that auto-steer tractors can reduce work time by up to 20% in certain farming operations, a critical factor in addressing labor shortages.

- Studies highlight the importance of data standardization and connectivity for the widespread adoption of smart farming, a key challenge and focus area for the industry.

The US Tractor Market: Market Dynamic

Driving Factors in the Japan Tractor Market

Critical Labor Shortage and Aging Demographics

The most powerful driver in the Japan tractor market is the existential challenge posed by a shrinking and aging agricultural workforce. With the average age of farmers nearing 70 and few young entrants, there is an urgent, government-backed need to replace manual labor with machinery. This is not just about comfort, but about the very survival of domestic food production. Tractors are no longer just tools for tillage; they are the primary solution for maintaining farming operations with a fraction of the workforce. This has created immense demand for machinery that is not only powerful but also highly automated and easy to operate. The driverless or autonomous tractor, once a futuristic concept, is now a practical necessity being actively developed and deployed to perform tasks like plowing and pesticide spraying without a human in the cab. This demographic pressure ensures a steady demand for new, technologically advanced tractors that offer the highest level of labor substitution.

Government Policy and "Smart Agriculture" Promotion

Proactive government policy is a major catalyst for tractor market dynamics. The Ministry of Agriculture, Forestry and Fisheries (MAFF) has made "Smart Agriculture" a core pillar of its strategy to revitalize the sector. Through substantial subsidies, grants, and demonstration projects, the government actively encourages farmers to adopt ICT-enabled machinery, including tractors with auto-steering, variable-rate fertilization, and farm management information systems. These subsidies significantly lower the high initial cost of advanced machinery, making them accessible to a wider range of farmers and farming corporations. Furthermore, policies aimed at consolidating farmland into larger, more efficient units are creating a class of professional farmers who are more inclined to invest in high-performance, capital-intensive equipment. This policy-driven ecosystem de-risks innovation for manufacturers and accelerates the replacement of older, less efficient tractors with new, smart models.

Restraints in the Japan Tractor Market

Market Maturity and Shrinking Farmland Base

A fundamental restraint on the Japan tractor market is its maturity and the underlying structural decline in agriculture itself. The total area of cultivated land has been gradually shrinking for decades due to urbanization and farmland abandonment. The number of commercial farming households is also in a long-term decline. This means the total available market for new tractors is essentially static or slowly contracting in terms of unit sales. Growth is therefore driven by value selling more expensive, technologically advanced machines rather than by an increase in the number of customers. This mature market environment leads to intense competition among the dominant domestic players (Kubota, Yanmar, Iseki) for replacement sales and market share, making volume growth challenging. The focus shifts to increasing the value per unit and expanding into after-sales services and solutions.

High Cost of Advanced Technology and Small Farm Economics

While the need for automation is high, the cost of smart tractors equipped with GPS, sensors, and robotic controls remains a significant barrier. Despite government subsidies, the upfront investment can be prohibitive for the majority of part-time farmers who operate on small plots and have limited income from agriculture. The economic viability of purchasing a multi-million-yen autonomous tractor for a farm of less than one hectare is questionable, even with subsidies. This creates a two-tier market: larger, corporate farms aggressively adopt new technology, while smaller, family farms rely on older, paid-off machinery or shared equipment cooperatives. Bridging this gap is a key challenge, and it points to a market where growth is heavily concentrated in the professional farming segment, leaving a long tail of small-scale operators with low demand for new, high-tech tractors.

Opportunities in the Japan Tractor Market

Robotics and Autonomous Solutions

The most significant growth opportunity lies in the field of agricultural robotics and fully autonomous tractors. As the government actively promotes the "smart agriculture" revolution, there is a first-mover advantage for companies that can deliver reliable, safe, and cost-effective autonomous solutions. This goes beyond simple auto-steer to include unmanned tractors that can perform a sequence of operations (tilling, planting) with remote monitoring. The opportunity is not only in selling the tractor itself but also in providing the software, sensors, and service contracts that make autonomy work. Given Japan's leadership in robotics and its pressing labor needs, the market is primed for a transition towards a future where farms are managed by a combination of robots and a small number of skilled human supervisors, creating a new, high-value segment within the tractor industry.

Electrification and Sustainable Machinery

While still in its early stages, the development of electric and hybrid compact tractors presents a promising opportunity. Aligning with Japan's carbon neutrality goals and the need for quieter, vibration-free operation (especially beneficial in greenhouses or residential areas), electric tractors offer a new frontier. They appeal to a new generation of farmers and to municipalities for public works. The lower maintenance costs and instant torque characteristics of electric motors are also attractive for specific applications. Companies investing in R&D for battery technology and charging infrastructure for agricultural settings are positioning themselves for the long-term transition away from diesel. This segment offers a chance to re-invigorate the product lineup and attract environmentally conscious buyers, including government entities.

Trends in the Japan Tractor Market

The Rise of "Smart" and Connected Tractors

The dominant trend is the rapid integration of digital technology into tractors. This includes factory-fitted GPS auto-steer systems, which are becoming standard on new mid-to-large-sized models. Tractors are evolving into connected data hubs, collecting information on soil conditions, crop health, and work efficiency. This data is transmitted to cloud-based platforms, allowing farmers to manage their entire operation from a tablet or smartphone. The tractor is no longer a standalone machine but a central component of a digital farm management system. This trend is being driven by large-scale farmers seeking to optimize every input and process, and it is reshaping the entire value proposition of a new tractor from a piece of iron to a sophisticated piece of information technology.

Dominance of Compact and Mid-Sized 4WD Tractors

Given the topographical and structural realities of Japanese agriculture, the market is overwhelmingly characterized by compact (under 40 HP) and mid-sized (41-100 HP) 4WD tractors. Four-wheel drive is essential for traction in wet paddy fields and on sloping terrain. The smaller size allows for maneuverability in narrow farm roads and small, irregular fields. This segment is the lifeblood of the market, serving the vast majority of rice, vegetable, and mixed-crop farms. While there is a niche for larger tractors on Hokkaido, the mainstream market focuses on versatility, compactness, and power-to-weight ratio. Trends within this space include improving operator comfort (cabs with air conditioning), enhancing fuel efficiency, and making smart features like auto-steer available on these smaller, more affordable models.

Japan Tractor Market: Research Scope and Analysis

By Horsepower Analysis

The Less than 40 HP segment is projected to maintain its dominance in the Japan tractor market in terms of unit sales, a direct reflection of the nation's farm structure. These compact tractors are the workhorses of Japan's countless small-scale paddy fields, vegetable plots, and hillside orchards. Their small size and maneuverability are indispensable for navigating narrow farm roads, tight field corners, and the small, irregular plots that characterize agriculture outside of Hokkaido. They are affordable for part-time farmers and are versatile enough for a range of tasks from tilling to mowing. The 41 to 100 HP segment holds significant value share, serving the needs of larger, consolidated farms, particularly in Hokkaido's expansive grain and dairy operations, as well as large-scale paddy cooperatives on the main island. These tractors offer the power needed for deeper tillage and for operating larger implements, improving efficiency for professional farmers. The More than 100 HP segment is a specialized niche, largely confined to the vast fields of Hokkaido and large-scale ranches, where high horsepower is essential for primary tillage and heavy forage work. While critical for those specific applications, its overall volume share remains limited.

By Driveline Analysis

The 4WD tractor segment is anticipated to dominate the Japan market. This is not a matter of preference but of necessity. The primary agricultural landscape in Japan consists of wet rice paddies that require four-wheel drive to prevent the tractor from getting stuck during puddling and tillage. Furthermore, many upland fields and orchards are located on slopes or terraces where 4WD is essential for stability and traction. Japanese farmers universally recognize 4WD as a prerequisite for safe and effective fieldwork. The 2WD tractor segment has become a minor player, largely confined to specific, niche applications such as well-drained upland farms on flat land, or for very specific tasks like road maintenance and light landscaping where the cost saving of 2WD might be a factor. The performance benefits and operational safety of 4WD in Japan's challenging conditions make it the standard for virtually all new tractor sales, from the smallest 20HP models to the largest 100HP+ machines.

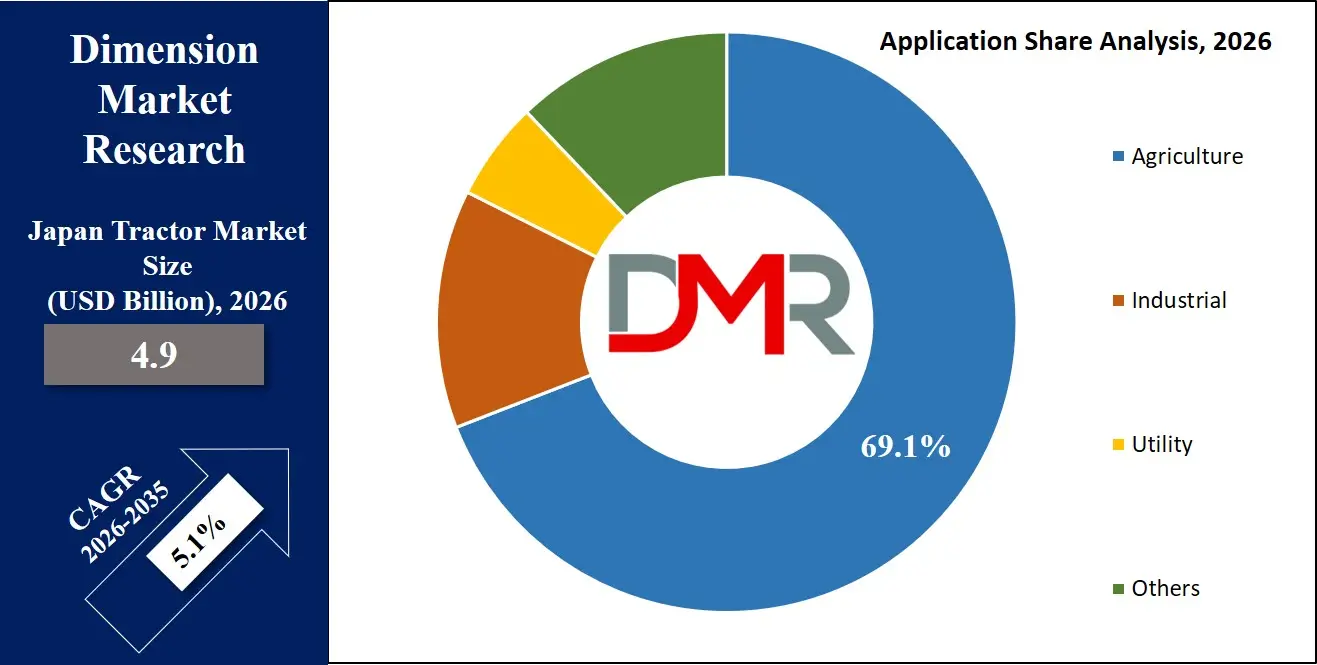

By Application Analysis

Agriculture is projected to stand as the dominant application for tractors in Japan, accounting for the vast majority of revenue in 2026. Within this, rice paddy farming is the single most important sub-application, as rice is the staple crop and occupies a significant portion of arable land. Tractors are fundamental to the entire rice cultivation cycle, from primary tillage to land leveling. Beyond rice, upland farming (vegetables, wheat, soybeans, potatoes) and livestock/dairy (forage production) are key agricultural applications that drive demand for tractors and a wide array of implements.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Utility and Industrial segments are secondary but notable. Compact tractors are frequently used by construction companies for site preparation and by municipal governments for parks and public works maintenance. The "Others" category, including forestry and golf course maintenance, provides a stable but small niche market. However, the primary economic engine for the tractor market remains firmly rooted in the diverse needs of Japan's agricultural sector.

Japan Tractor Market Report is segmented on the basis of the following:

By Horsepower

- Less than 40 HP

- 41 to 100 HP

- More than 100 HP

By Driveline

By Application

- Agriculture

- Industrial

- Utility

- Others

Impact of Artificial Intelligence in Japan Tractor Market

- Autonomous/Unmanned Operation: AI is the brain behind "robot tractors," enabling them to navigate fields, avoid obstacles, and perform tasks like plowing and spraying without a human operator, directly addressing Japan's severe labor shortage.

- Precision Agriculture for Small Fields: AI algorithms analyze data from drones and satellites to create ultra-precise application maps, allowing even small, irregular fields to benefit from variable-rate application of fertilizers and pesticides, maximizing yield on limited land.

- Weed and Pest Recognition: AI-powered cameras on tractors can identify specific weeds or pest damage in real-time, enabling targeted spot-spraying rather than blanket application, reducing chemical use and costs, a key goal for sustainable agriculture.

- Skill Assistance for Inexperienced Farmers: AI systems can learn from expert farmers and provide real-time guidance to novices on optimal operating speeds, implement settings, and navigation lines, helping to transfer tacit knowledge and lower the barrier to entry for new farmers.

- Yield Prediction and Harvest Optimization: By integrating with sensors and harvesters, AI can analyze data during harvest to predict yields with high accuracy and optimize the harvesting process for quality and efficiency, improving farm management decisions.

Japan Tractor Market: Competitive Landscape

The Japan tractor market is a distinctive and consolidated landscape, overwhelmingly dominated by powerful domestic manufacturers. Kubota, Yanmar, and Iseki form the "Big Three" that have historically shaped the market and command the vast majority of sales, particularly in the core compact and mid-sized tractor segments. Their strength lies in their deep understanding of the local market, extensive and trusted dealer networks, and continuous innovation in technologies suited to Japan's unique farming needs. Global giants like John Deere and AGCO (Massey Ferguson, Fendt) are present, primarily competing in the higher-horsepower segment in Hokkaido and for large-scale livestock farms, offering specialized machinery for those applications. Mitsubishi Mahindra Agricultural Machinery Co., Ltd., a joint venture, also holds a notable position.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Competition is fierce, but it revolves less around price and more around technological leadership, reliability, and the comprehensiveness of the "solution" offered. With the market shifting towards smart agriculture, the battleground has moved to who can best integrate AI, robotics, and data platforms into their machinery. Companies are heavily investing in R&D to launch the most advanced autonomous tractors and farm management systems. Strategic alliances are becoming crucial, as seen with Kubota's collaborations with telecom giants like NTT to leverage 5G for remote monitoring.

After-sales service, parts availability, and strong relationships with local agricultural cooperatives (JA) and dealers are critical for maintaining customer loyalty. As the number of farmers declines, the competition is for the loyalty of the remaining, often larger, professional farming entities. The market is expected to remain highly concentrated, with domestic leaders using their technological prowess and market knowledge to fend off international competitors and maintain their dominant positions.

Some of the prominent players in Japan Tractor Market are:

- Kubota Corporation

- Yanmar Holdings Co., Ltd.

- Iseki & Co., Ltd.

- Mitsubishi Mahindra Agricultural Machinery Co., Ltd.

- IHI Shibaura Machinery Corporation

- AGCO Corporation

- CNH Industrial N.V.

- Deere & Company

- Mahindra & Mahindra Ltd.

- Kawasaki Heavy Industries, Ltd.

- IHI Agri-Tech Corporation

- Cornes AG Corporation

- CLAAS KGaA mbH

- LS Mtron Ltd.

- Kioti (Daedong Corporation)

- SDF Group (Same Deutz-Fahr)

- Argo Tractors S.p.A.

- Escorts Kubota Limited

- TYM Corporation

- Fendt (AGCO Group)

- Other Key Players

Recent Developments in Japan Tractor Market

- March 2026: Kubota Corporation announced a strategy to strengthen its global agricultural machinery business by expanding tractor exports and distribution networks across Asia and other emerging markets. The company is focusing on strengthening smart farming technologies and improving supply chain efficiency to support global demand for compact and mid-size tractors.

- September 2025: Kubota Corporation showcased the world’s first hydrogen fuel-cell powered autonomous tractor at Expo 2025 Osaka, Kansai. The concept tractor integrates hydrogen energy technology, autonomous navigation systems, and smart farming software to support carbon-neutral agriculture.

- July 2025: Kubota Corporation acquired a precision agriculture technology startup to strengthen its digital farming ecosystem. The acquisition focuses on integrating AI-based farm management systems with tractors and agricultural machinery to enhance productivity and automation.

- June 2025: Yanmar Co., Ltd. introduced a GPS-guided and AI-enabled automated tractor designed to improve precision farming operations. The tractor allows semi-autonomous field operations, helping address Japan’s agricultural labor shortage and increasing farming efficiency.

- April 2025: Mitsubishi Agricultural Machinery Co., Ltd. launched a hybrid-powered tractor aimed at reducing fuel consumption and emissions. The development aligns with Japan’s environmental policies, promoting low-carbon and sustainable agricultural machinery.

- June 2024: Iseki & Co., Ltd. developed a 123-horsepower unmanned tractor capable of remote monitoring and autonomous field operations. The tractor is targeted at large farms in regions such as Hokkaido where labor shortages have accelerated demand for automated farming equipment.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 4.9 Bn |

| Forecast Value (2035) |

USD 7.7 Bn |

| CAGR (2026–2035) |

5.1% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Horsepower (Less than 40 HP, 41 to 100 HP, and More than 100 HP), By Driveline (2WD, and 4WD), By Application (Agriculture, Industrial, Utility, and Others) |

| Country Coverage |

Japan |

| Prominent Players |

Kubota Corporation, Yanmar Holdings Co., Ltd., Iseki & Co., Ltd., Mitsubishi Mahindra Agricultural Machinery Co., Ltd., IHI Shibaura Machinery Corporation, AGCO Corporation, CNH Industrial N.V., Deere & Company, Mahindra & Mahindra Ltd., Kawasaki Heavy Industries Ltd., IHI Agri-Tech Corporation, Cornes AG Corporation, CLAAS KGaA mbH, LS Mtron Ltd., Daedong Corporation (KIOTI), SDF Group (Same Deutz-Fahr), Argo Tractors S.p.A., Escorts Kubota Limited, TYM Corporation, Fendt (AGCO Group), and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is Japan Tractor Market?

▾ Japan Tractor Market size is estimated to have a value of USD 4.9 billion in 2026 and is expected to reach USD 7.7 billion by the end of 2035.

What is the growth rate in Japan Tractor Market in 2026?

▾ The market is growing at a CAGR of 5.1 percent over the forecasted period of 2026.

Who are the key players in Japan Tractor Market?

▾ Some of the major key players in Japan Tractor Market are John Deere, CNH Industrial (Case IH, New Holland), AGCO Corporation (Massey Ferguson, Fendt, Challenger), Kubota Tractor Corporation, Mahindra USA, CLAAS, Yanmar America, and many others.