What is the Global Liquid Biopsy Market Size?

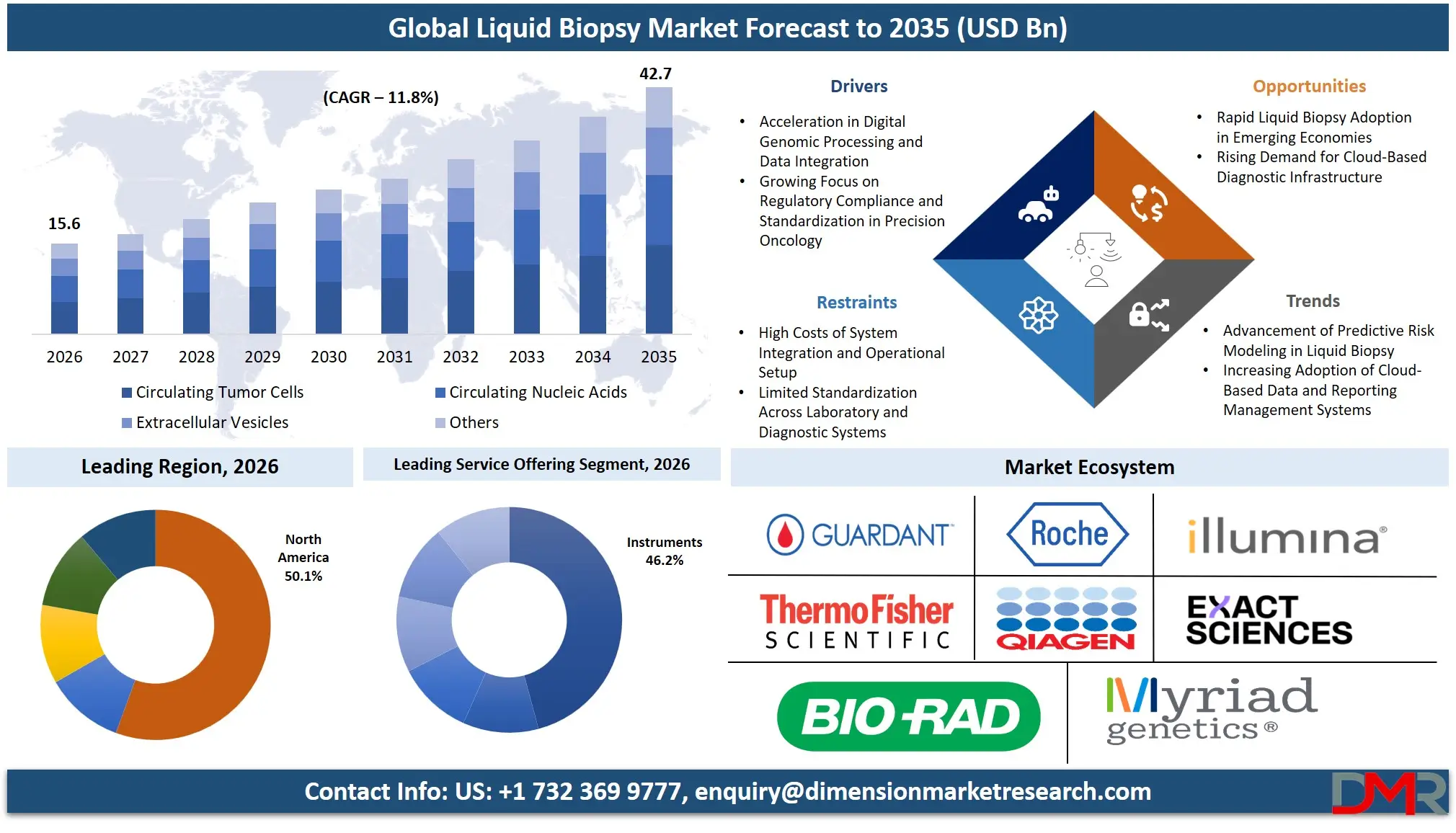

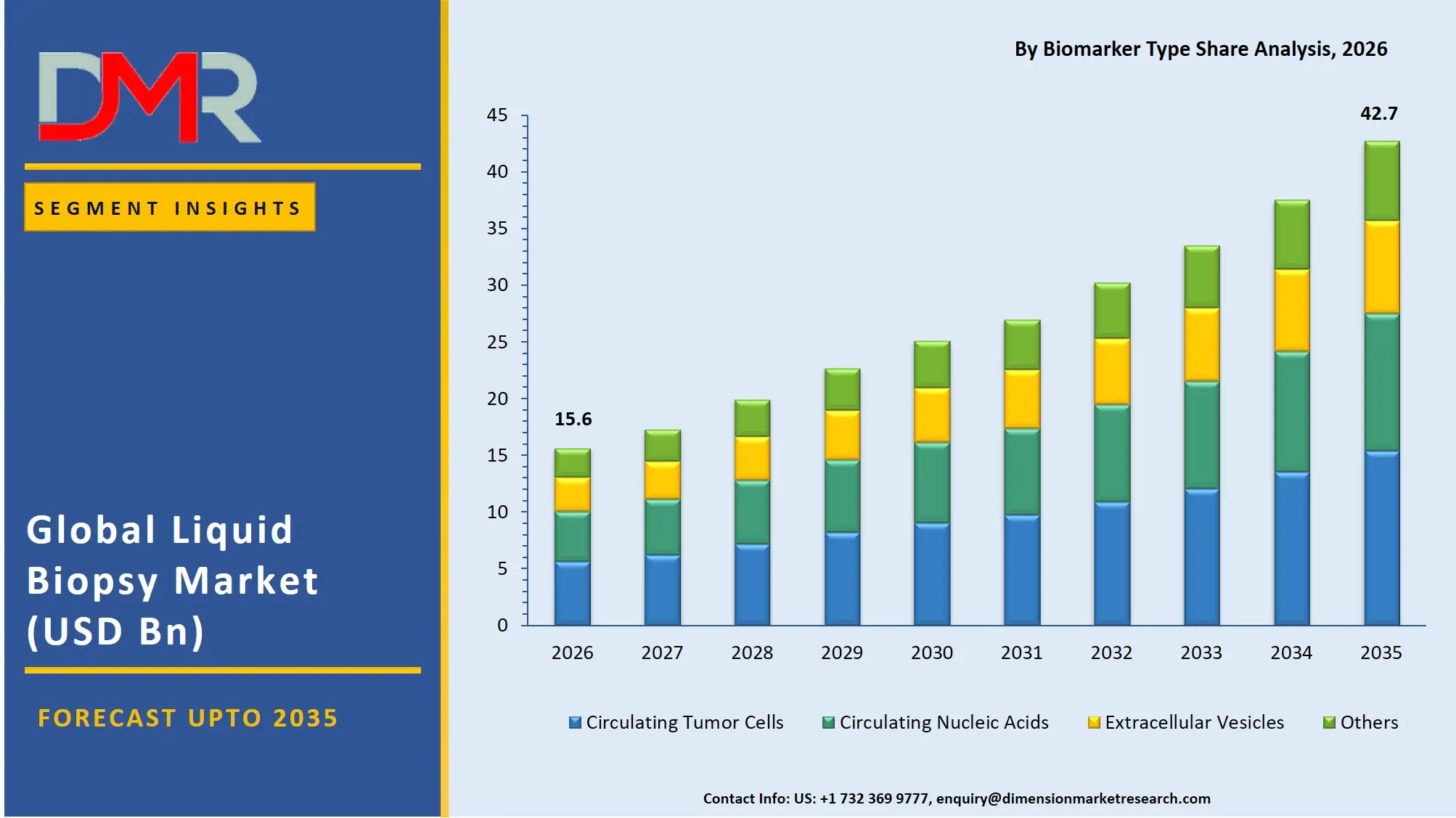

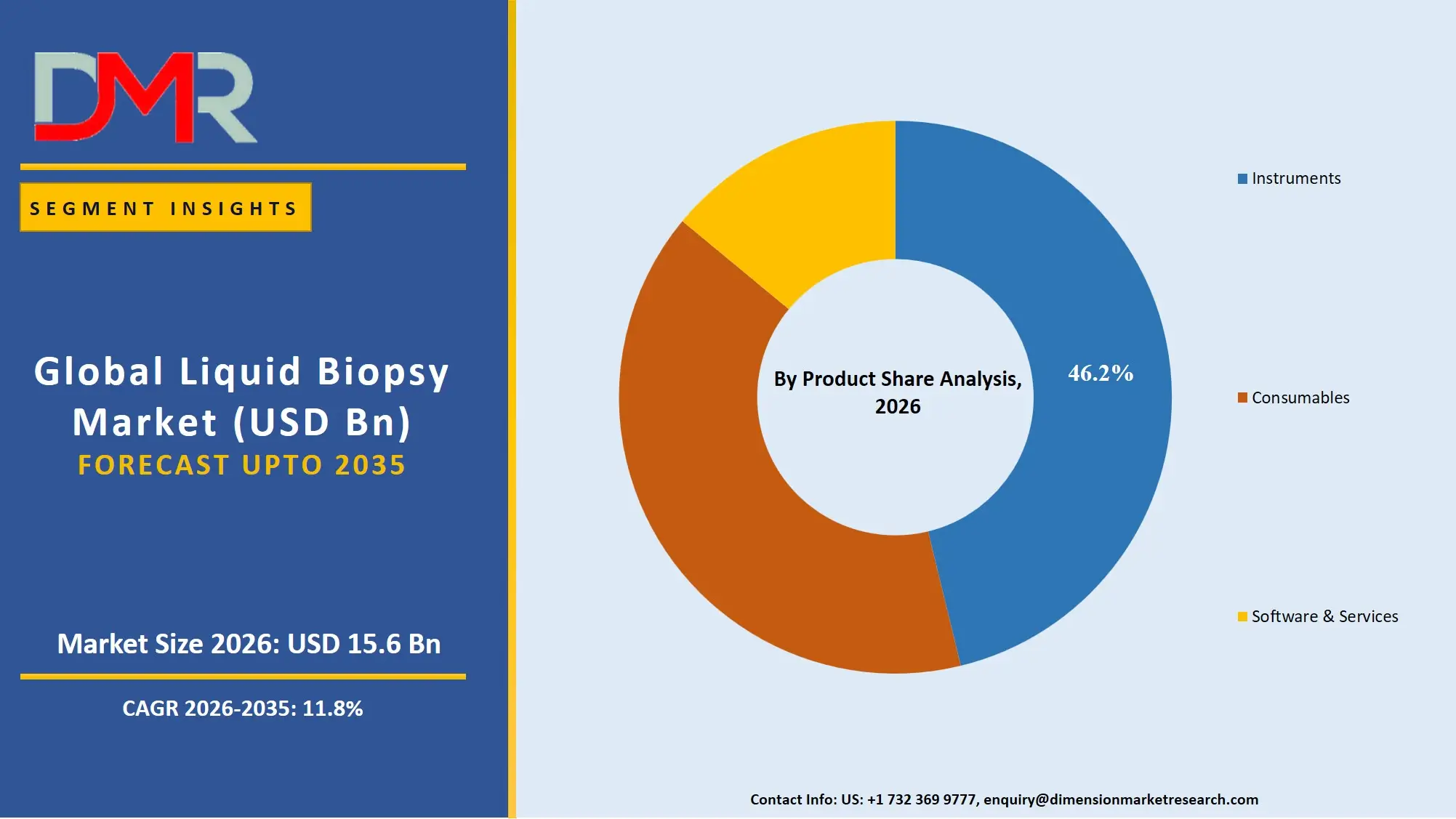

The Global Liquid Biopsy Market size is estimated at USD 15.6 billion in 2026 and is projected to reach USD 42.7 billion by 2035, exhibiting a CAGR of 11.8% during the forecast period, driven by the rising use of artificial intelligence in genomic data interpretation, automation of liquid biopsy workflows, and integrated cancer management in precision oncology.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The global liquid biopsy market is growing due to an increase in machine learning for ctDNA detection and analysis, increased approvals, decreasing the chances of having a false negative result at the early stage of cancer detection, faster processing of getting approved for molecular diagnostics, and increased investment in automation of liquid biopsy usage.

Some other reasons for expansion in this market are technological innovations in real-time genomic analysis, cancer risk prediction, automated bioinformatics processing, and high-throughput digital platforms, along with better data integration standards. The digital revolution in oncology and diagnostic service companies has been helpful in speeding up test processing and making cancer healthcare management easier. This includes treatment response tracking research. In addition, national policies focusing on precision medicine and early cancer detection have ensured sustainable research in liquid biopsy diagnostics.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

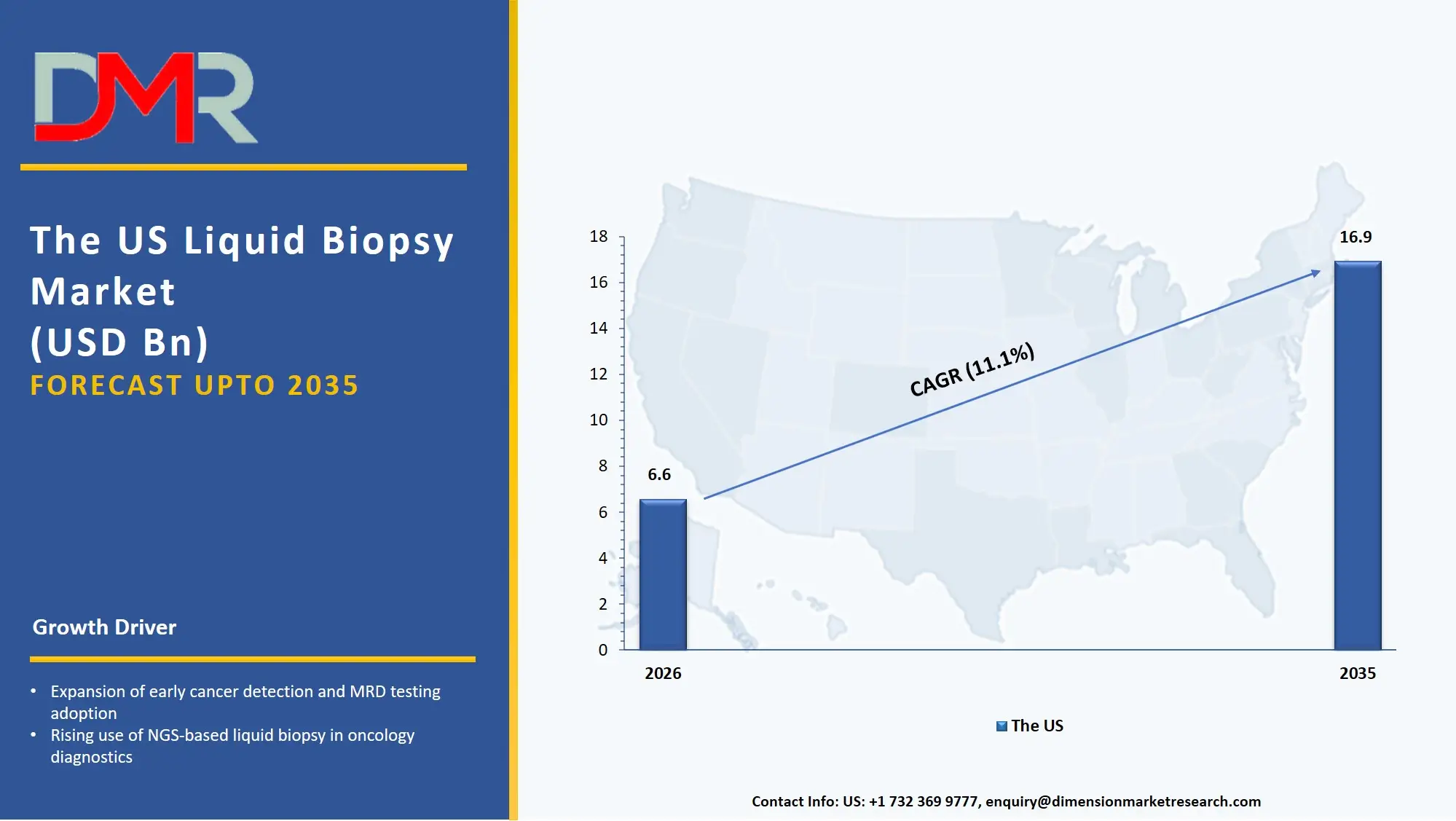

The US Liquid Biopsy Market

The US Liquid Biopsy Market is estimated to grow to USD 6.6 billion in 2026 with a compound annual growth rate of 11.1% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US market is shaped by major federal and state-level initiatives promoting precision oncology, cancer diagnostic affordability programs supported by the American Cancer Society, and NIH-led early detection research initiatives. These programs encourage the use of AI-driven genomic analysis, real-time clinical data integration, and predictive diagnostic software. Automated liquid biopsy platforms are being rapidly adopted, and the US continues to invest in better data sharing between oncology centers, molecular diagnostic record systems, and reliable AI tools for liquid biopsy. Service providers are also influenced by laws like the CLIA framework for advanced diagnostics and national digital health strategies to offer services that ensure data security, compliance, and smooth integration across oncology clinics and patient portals.

Europe Liquid Biopsy Market

The Europe Liquid Biopsy Market is estimated to be valued at USD 4.1 billion in 2026, witnessing growth at a CAGR of 10.6%, during the forecast period.

Europe's liquid biopsy market is mature, shaped by EU-wide policies such as Europe's Beating Cancer Plan, the European Horizon Europe research program and national policies to support digital molecular diagnostics (e.g., France's national genomic medicine plans and Germany's Precision Oncology Strategy 2030). Countries are also making diagnostic processes more modular to align clinical and patient demands and enable the sharing of genomic data across national borders. The market grows due to new tools like software for real-time mutation validation and scoring systems for therapy selection. Use is facilitated by public-private collaborations and data standards. Diagnostic providers have access to technologies such as cloud computing and encryption, and Europe is at the forefront of the digitisation of safe and efficient liquid biopsy operations.

Japan Liquid Biopsy Market

The Japan Liquid Biopsy Market is projected to be valued at USD 848.0 million in 2026, progressing at a CAGR of 12.8%, during the period spanning from 2026 to 2035.

Japan's liquid biopsy market is well developed, with high-quality digital genomic platforms, integrated molecular management systems, and a wide array of AI-powered cancer risk analysis software tools. National focus on automation, efficiency and process integrity is delivered via predictive oncology models and smart diagnostic management. Growth opportunities are aided by government measures under the Society 5.0 program by Japan's Ministry of Economy, Trade and Industry (METI), and continued investment in digital cancer diagnostics. Oncology R&D, industrial cancer analysis for mutation-specific condition development and clinical liquid biopsy all need effective AI to keep pace with data analysis. Higher costs for validating new automation systems and integrating them with legacy laboratory systems are significant, but there are opportunities for the export of Japanese liquid biopsy technologies to the Asian and Pacific markets.

Key Takeaways

- Market Size & Forecast: The Global Liquid Biopsy Market is estimated to be valued at USD 15.6 billion in 2026 and is expected to grow to USD 42.7 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 11.8% in the forecast period.

- Primary Growth Drivers: The availability of new genomic processing technologies that use machine learning, the need to accelerate cancer therapy reimbursement and improve success rates of cancer treatments, and more government investment in national oncology infrastructure are key growth drivers.

- Key Market Trends: The predictive profiling of cancer mutation risks, real-time genomic data processing and the shift to cloud-based liquid biopsy and diagnostic management platforms are key market trends.

- By Product: Instruments are expected to occupy the largest revenue share in 2026 in the global liquid biopsy market.

- By Biomarker Type: Circulating Nucleic Acids (ctDNA, cfDNA, RNA) are expected to occupy the largest revenue share in 2026 in the liquid biopsy market.

- By End User: Hospitals & Laboratories is estimated to take the lead in 2026 with the largest share in the liquid biopsy market.

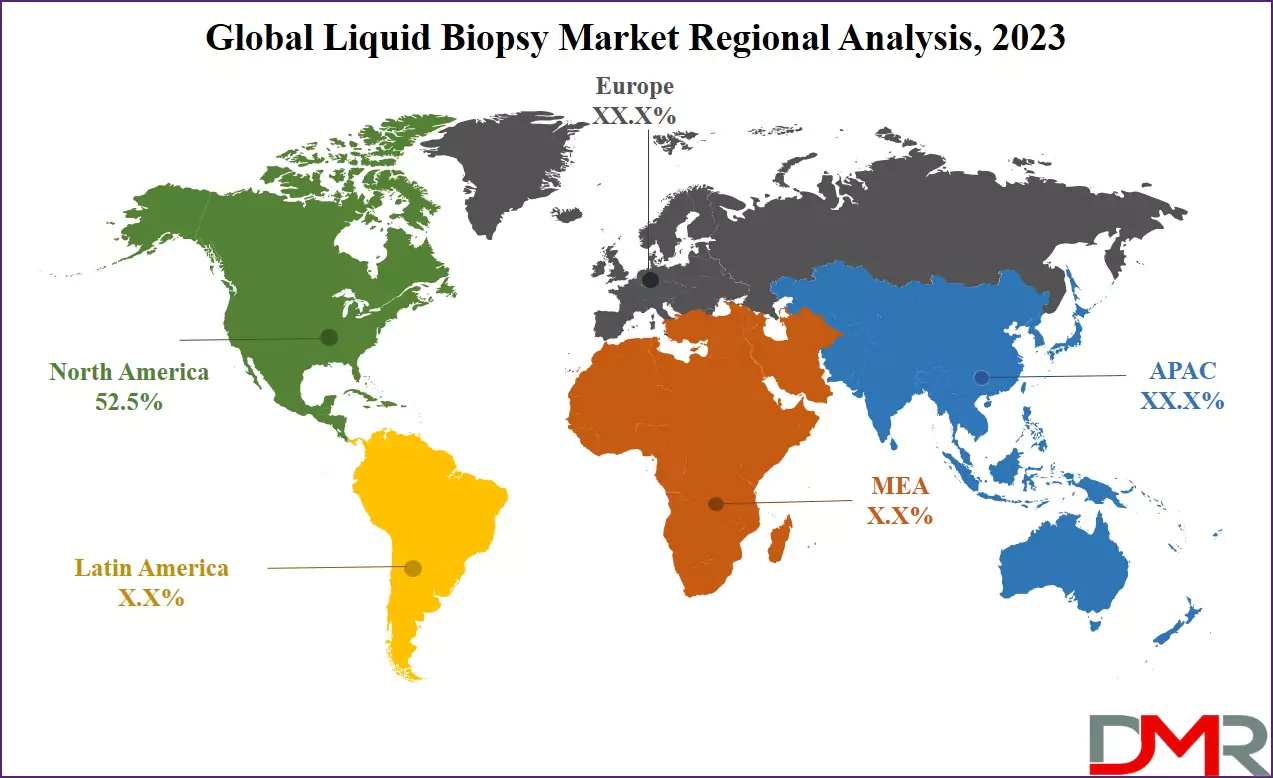

- Regional Leadership: North America is estimated to take the lead in 2026 with 50.1% share in the liquid biopsy market, owing to significant investment in precision oncology and diagnostic technologies.

What is Liquid Biopsy?

Liquid biopsy is a noninvasive test used for detecting, monitoring, and managing cancer using biomarkers in liquid samples like blood or other body fluids. The test uses sophisticated technology, including next-generation sequencing, digital polymerase chain reaction, and bioinformatics. Liquid biopsy can be used for the detection of circulating tumor cells, circulating nucleic acids, and extracellular vesicles. It finds wide application in improving cancer treatment, supporting precision medicine, facilitating early cancer screening, and achieving personalized management of cancer.

Use Cases

- Early Cancer Screening for High-Risk Populations: Liquid biopsy is capable of identifying early cancers such as lung, breast, and colorectal cancer through a simple blood draw, compared to weeks or months of diagnostic time using traditional tissue biopsy and follow-ups of imaging.

- Therapy Selection & Resistance Monitoring: Longitudinal data of tumor mutations, such as EGFR or KRAS, or BRCA mutations are modeled to comprehend clonal evolution to guide the choice of targeted therapy and identify acquired resistance.

- Treatment Monitoring & Minimal Residual Disease (MRD): MRD detection (post-surgery or chemotherapy) is processed via digital platforms and machine learning in clinical and laboratory settings.

- Population Health & Government Programs: Faster liquid biopsy supports oncology innovation and development of rare cancer treatments; government programs by use of smart monitoring of genomic data supports national cancer strategies and helps to adopt standards of care.

How AI Is Transforming the Global Liquid Biopsy Market?

Artificial intelligence is being applied more and more often to liquid biopsy to enhance genomic forecasting, identify false positive trends, and automatically identify anomalies in sequencing data. It also facilitates quicker variant validation as it allows processing of digital submissions on a large scale. Genomic records and electronic health records are easier to analyze and assist diagnostic providers to detect sequencing errors, minimize false calls, and enhance the overall accuracy of reports. This has resulted in test processing being cost effective, quicker and more efficient than the traditional manual review method.

AI is also strengthening diagnostic workflows by improving risk assessment and enabling more accurate test structuring. It helps providers anticipate testing volumes, identify potential processing delays, and monitor the performance of laboratory networks more effectively. In addition, automation of routine quality checks and performance monitoring is reducing operational workload, lowering administrative costs, and improving overall efficiency. This is contributing to better financial performance and more stable diagnostic operations across the liquid biopsy value chain.

Market Dynamics

Key Drivers of the Global Liquid Biopsy Market

Acceleration in Digital Genomic Processing and Data Integration

The market is growing with the rise of digital tools to validate and process genomic data, better management of molecular data, and closer integration of electronic medical records and diagnostic systems. Oncology practice management platforms provide real-time data that allows monitoring the testing workflow, allowing to identify discrepancies early, and checking patient records much faster. This has enhanced efficiency in operations and minimized the human factor as well as the administrative expenses. Simultaneously, demand for more automated diagnostic operations is being facilitated by increased activity in predictive analytics for the assessment of cancer risks, as clinical practice is further digitalizing fundamental laboratory and reporting operations.

Growing Focus on Regulatory Compliance and Standardization in Precision Oncology

There is increasing emphasis on transparency, data accuracy, and compliance within the liquid biopsy ecosystem. Regulatory frameworks such as the IVDR in Europe and diagnostic modernization initiatives in key markets are encouraging improved data handling practices and more structured diagnostic processes. These advancements are underpinning the need to have systems that can offer consistent monitoring of test results and standardized reporting. Concurrently, an active process of enhancing the interoperability of genomic data and curbing reporting inconsistencies is strengthening the necessity of more effective diagnostic administration systems in both governmental and private care providers.

Restraints in the Global Liquid Biopsy Market

High Costs of System Integration and Operational Setup

The deployment of liquid biopsy platforms remains cost-intensive, requiring significant investment in NGS infrastructure, bioinformatics integration, testing, and alignment with clinical workflows. In addition, compliance with data privacy regulations such as GDPR and HIPAA adds to implementation complexity. These factors increase upfront costs and can limit adoption, particularly among smaller diagnostic labs and new market entrants.

Limited Standardization Across Laboratory and Diagnostic Systems

There is still fragmentation in the market in terms of data formats and test processing protocols. Although there are areas that have implemented organized laboratory management systems, numerous diagnostic providers continue to work in both digital and manual systems. Lack of standards causes interoperability between clinicians and diagnostic providers to be constrained and results in inefficiencies in test processing and system integration.

Growth Opportunities in the Global Liquid Biopsy Market

Rapid Liquid Biopsy Adoption in Emerging Economies

Emerging economies such as Brazil, Indonesia, Nigeria, the UAE, and Vietnam are gradually developing their oncology diagnostic and liquid biopsy ecosystems. These regions have long-term growth prospects, with more cancer awareness, and with more people becoming more aware of early cancer detection and gradually digitalizing clinical care. These markets have few legacy diagnostic systems and can be exploited with new, technology-driven testing systems to be scaled up.

Rising Demand for Cloud-Based Diagnostic Infrastructure

The transition to remote oncology care, distributed diagnostic networks, and real-time reporting is creating the uptake of cloud-based diagnostic systems. These systems facilitate centralized data access, enhanced coordination of clinical providers and diagnostic labs, and expedited test administration. Cloud-based deployment is increasingly becoming a trend among contemporary liquid biopsy providers as operational efficiency becomes one of the competitive factors.

Global Liquid Biopsy Market Trends

Advancement of Predictive Risk Modeling in Liquid Biopsy

The liquid biopsy platforms are gradually integrating data-driven technology to determine mutation trends and enhance accuracy in early detection. These systems enable the diagnostic providers to evaluate their testing behavior better, simplify the management of their patient datasets, and improve their overall performance in terms of the portfolio. The move is slowly turning the industry more proactive and data-driven in diagnostic management as opposed to being purely reactive in test management.

Increasing Adoption of Cloud-Based Data and Reporting Management Systems

The use of cloud infrastructure is currently emerging as a fundamental part of present-day liquid biopsy functionality. The systems facilitate real-time genomic analysis, centralized test administration, and enhanced network coordination among the oncologists. Cloud-based platforms are enhancing the efficiency and responsiveness of diagnostic providers that operate in various regions by eliminating the need to depend on physical infrastructure and facilitating scalable operations.

Research Scope and Analysis

The global Liquid Biopsy Market enables non-invasive cancer detection and monitoring through analysis of biomarkers in bodily fluids. It is segmented by product, biomarker type, technology, sample type, application, clinical application, and end user, driven by NGS adoption, ctDNA testing, precision oncology growth, and rising demand from healthcare and pharma sectors.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Product Analysis

The Instruments segment is predicted to hold the largest share of about 46.2% of the worldwide liquid biopsy market in 2026. This will be attributed to the high capital investment in next-generation sequencing platforms, digital PCR, and automated nucleic acid extraction systems used in both clinical laboratories and research institutes. Growth in this category will also be stimulated by the ongoing innovations, the need for high throughput sequencing systems, and automation through robotics. The fast growth of the Consumables category is being fuelled by frequent orders of kits, reagents, and sequencing flow cells required for routine testing and population screening. There is also rapid growth in the Software & Services category due to the increasing need for bioinformatics services and cloud genomics services.

By Biomarker Type Analysis

The Circulating Nucleic Acids (ctDNA, cfDNA, RNA) segment is expected to account for 64.7% share in 2026, due to higher clinical validation, mutation-specific targeting, and greater clinical adoption compared to other biomarkers. The segment is also driven by growing adoption of comprehensive therapy selection and monitoring plans, and integrated testing options to increase value for oncologists in clinical and research applications. It's also the fastest-growing segment in the liquid biopsy market, due to the rapid uptake of fully integrated genomic workflows and laboratory infrastructure. Circulating Tumor Cells (CTCs) are the second-largest segment, followed by Extracellular Vesicles and Others (including tumor-educated platelets and proteins).

By Technology Analysis

The Blood-based segment is expected to hold the largest share in 2026, accounting for approximately 78.3% of the market, owing to its minimally invasive nature, high concentration of circulating biomarkers, and established clinical workflows for blood collection and processing. Blood-based liquid biopsy is widely adopted for early cancer screening, therapy selection, and treatment monitoring across multiple cancer types. The Urine-based segment is gaining traction, particularly for urological cancers such as bladder and prostate cancer, benefiting from non-invasive sample collection and the ability to detect ctDNA and exosomes. The Saliva & Other Body Fluids segment is emerging, supported by research into oral cancers and the convenience of saliva collection for certain applications.

By Sample Type Analysis

The Cloud-based segment is the largest sample type category in 2026, accounting for 52.3% share, driven by digital adoption, remote data access, and the ease of integrating genomic data via secure platforms. Cloud-based solutions enable real-time data sharing between oncologists, laboratories, and researchers, facilitating faster clinical decision-making. On-premise solutions are the second-largest segment, used by large hospital networks and reference laboratories requiring full data control, enhanced security, and compliance with institutional data governance policies. The fastest-growing area is Hybrid platforms, where institutions combine cloud flexibility with on-premise security for complex, multi-site or high-volume genomic testing.

By Application Analysis

The Lung Cancer segment is expected to dominate the market in 2026, accounting for approximately 31.5% share, driven by high incidence rates, the availability of multiple targeted therapies (EGFR, ALK, ROS1, KRAS G12C), and established clinical guidelines recommending liquid biopsy for therapy selection and resistance monitoring. The Breast Cancer segment is the second-largest, supported by the need for monitoring HER2, ESR1 mutations, and other genomic alterations in metastatic settings. The Colorectal Cancer segment follows, with strong adoption for RAS/BRAF mutation detection and recurrence monitoring. Prostate Cancer, Other Cancers (including melanoma, ovarian, pancreatic, and liver cancers), and Non-oncology Applications (such as prenatal testing, transplant monitoring, and infectious disease detection) are also growing segments.

By Clinical Application Analysis

The Therapy Selection segment is expected to account for the largest share in 2026, with approximately 38.6% of the market, driven by the need for comprehensive genomic profiling to match patients with targeted therapies and immunotherapies. Liquid biopsy enables non-invasive identification of actionable mutations, particularly when tissue biopsy is insufficient or inaccessible. Treatment Monitoring is the second-largest segment, as serial liquid biopsy allows real-time assessment of treatment response and early detection of resistance mutations. Early Cancer Screening is the fastest-growing segment, supported by large-scale clinical studies (e.g., PATHFINDER, NHS-Galleri) demonstrating the utility of multi-cancer early detection (MCED) tests in asymptomatic populations. Recurrence Monitoring (including minimal residual disease detection) is also a critical application, enabling early intervention and improved survival outcomes.

By End User Analysis

The Hospitals & Laboratories segment is expected to dominate with around 67.8% market share in 2026, driven by greater testing volume, faster turnaround times, and broader patient access compared to specialty clinics. Hospital-based labs support customized diagnostic workflows because they can offer multiple testing tiers for screening, therapy selection, and monitoring, delivering fast results while keeping data within integrated health systems. The Academic & Research Institutes segment is the second-largest, playing a crucial role in biomarker discovery, assay validation, and translational research. The Specialty Clinics segment, including oncology clinics and reference laboratories, is growing steadily, supported by outsourcing trends and the increasing complexity of genomic testing requiring specialized infrastructure.

The Global Liquid Biopsy Market Report is segmented based on the following:

By Product

- Instruments

- Consumables

- Software & Services

By Biomarker Type

- Circulating Tumor Cells (CTCs)

- Circulating Nucleic Acids (ctDNA, cfDNA, RNA)

- Extracellular Vesicles

- Others

By Technology

- Blood-based

- Urine-based

- Saliva & Other Body Fluids

By Sample Type

- Cloud-based

- On-premise

- Hybrid

By Application

- Lung Cancer

- Breast Cancer

- Colorectal Cancer

- Prostate Cancer

- Other Cancers

- Non-oncology Applications

By Clinical Application

- Early Cancer Screening

- Therapy Selection

- Treatment Monitoring

- Recurrence Monitoring

By End User

- Hospitals & Laboratories

- Specialty Clinics

- Academic & Research Institutes

Regional Analysis

Leading Region in the Liquid Biopsy Market

It is projected that North America will take the lead in the global liquid biopsy market (by value), covering a market share of about 50.1% in the year 2026. The region's dominance is driven by strong oncology diagnostic spending funded by private and public sources, higher average test prices relative to other regions, a mature digital diagnostic supply chain for advanced data sharing, and the presence of major liquid biopsy providers and oncology networks. The widespread adoption of advanced genomic processing and automation for early screening, therapy selection, and treatment monitoring further strengthens North America's leading position. Additionally, ongoing investments in AI-powered genomic monitoring and system interoperability further reinforce the region's technology leadership.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Region in the Liquid Biopsy Market

Asia-Pacific is the fastest-growing region, supported by strong digital diagnostic infrastructure targets in China, India, and Japan, increasing cancer incidence and awareness initiatives, rising investments in local liquid biopsy capabilities, and growing adoption of automated genomic analysis systems. The region benefits from a well-established digital health infrastructure for diagnostic products, increasing commercial activity, and alignment with national cancer control roadmaps. Countries across the region are actively deploying liquid biopsy platforms to improve testing efficiency and strengthen oncology infrastructure. Growing emphasis on precision oncology R&D and structured data development further accelerates market expansion. Moreover, increasing government support and commercial diagnostic commitments are expected to sustain high growth momentum.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The liquid biopsy market is highly competitive, with innovation and strategic alliances shaping the competitive environment. To gain an advantage, companies and diagnostic providers are focused on developing better digital platforms (such as AI-powered genomic engines, automated bioinformatics systems, and cloud-based platforms for data management), AI-powered data analysis, and digital platform-based test monitoring. There are high barriers to entry due to the large capital needed for regulatory approval (FDA, CE-IVD), specialized bioinformatics expertise, and the need for mature software ecosystems and regulatory compliance.

Strategic approaches to increase market presence include partnerships with oncology centers and research hospitals, mergers between diagnostic providers and technology developers, and long-term support contracts with patients and cancer centers. Additionally, research and development in data-sharing standards and scalable software architectures are important for staying competitive and meeting the changing needs of the liquid biopsy community.

Some of the prominent players in the Global Liquid Biopsy Market are:

- Guardant Health, Inc.

- F. Hoffmann-La Roche Ltd.

- Illumina, Inc.

- Thermo Fisher Scientific Inc.

- QIAGEN N.V.

- Bio-Rad Laboratories, Inc.

- Exact Sciences Corporation

- Natera, Inc.

- Myriad Genetics, Inc.

- GRAIL, LLC

- Freenome Holdings, Inc.

- ANGLE plc

- Epigenomics AG

- Oncimmune Holdings plc

- Biocept, Inc.

- Menarini Silicon Biosystems S.p.A.

- Lucence Health Inc.

- MDxHealth SA

- Agena Bioscience, Inc.

- Epic Sciences, Inc.

- Other Key Players

Recent Developments

- April 2026: Guardant Health, Inc. announced a multi-year strategic collaboration with Nuvalent, Inc. to advance companion diagnostics and support the commercialization of targeted oncology therapies using its tissue and liquid biopsy platform, reinforcing its role in precision oncology drug development and biomarker-driven clinical trials.

- February 2026: Illumina, Inc. expanded adoption of its next-generation sequencing (NGS) platforms for liquid biopsy through new clinical partnerships and workflow integrations, strengthening its role as a key enabling provider for ctDNA-based and multi-cancer early detection testing in oncology research and diagnostics.

- January 2026: F. Hoffmann-La Roche Ltd. advanced its liquid biopsy portfolio through continued expansion of Foundation Medicine–driven genomic profiling solutions, strengthening its companion diagnostics ecosystem for targeted oncology therapies and reinforcing integration of comprehensive genomic testing in clinical decision-making.

- January 2026: Exact Sciences Corporation expanded its oncology testing pipeline, including continued commercialization and adoption of its MRD and early cancer detection solutions, strengthening its position in non-invasive colorectal and multi-cancer screening supported by increasing clinical uptake of liquid biopsy-based diagnostics.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 15.6 Bn |

| Forecast Value (2035) |

USD 42.7 Bn |

| CAGR (2026–2035) |

11.8% |

| The US Market Size (2026) |

USD 6.6 Bn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Product, By Biomarker Type, By Technology, By Sample Type, By Application, By Clinical Application, By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Liquid Biopsy Market?

▾ The Global Liquid Biopsy Market size is estimated to have a value of USD 15.6 billion in 2026 and is expected to reach USD 42.7 billion by the end of 2035.

Which region held the largest share of the Global Liquid Biopsy Market in 2026?

▾ North America is expected to account for the largest market share in 2026, with a share of about 50.1%.

Who are the key players in the Global Liquid Biopsy Market?

▾ Some of the major key players in the Global Liquid Biopsy Market are Guardant Health, Inc., Exact Sciences Corporation, Natera, Inc., F. Hoffmann-La Roche Ltd., Thermo Fisher Scientific, Illumina, QIAGEN N.V., and many others.

What is the CAGR of the Global Liquid Biopsy Market from 2026 to 2035?

▾ The market is growing at a CAGR of 11.8% over the forecasted period.

What factors are driving the growth of the Global Liquid Biopsy Market?

▾ The market is driven by advances in machine learning-based genomic processing, regulatory pressure to speed up cancer diagnostics and reduce errors, and increased government investment in national oncology infrastructure.

What are the major trends in the Global Liquid Biopsy Market?

▾ The key market trends include the adoption of predictive cancer mutation risk tracking and real-time genomic data analysis, along with a growing shift toward cloud-based diagnostic platforms and data-enabled test management systems.

Which region is expected to grow the fastest in the Global Liquid Biopsy Market?

▾ Asia Pacific is the fastest-growing region in the market during the forecast period.

How is the Global Liquid Biopsy Market segmented?

▾ The market is segmented by product, biomarker type, technology, sample type, application, clinical application, and end user.