Market Overview

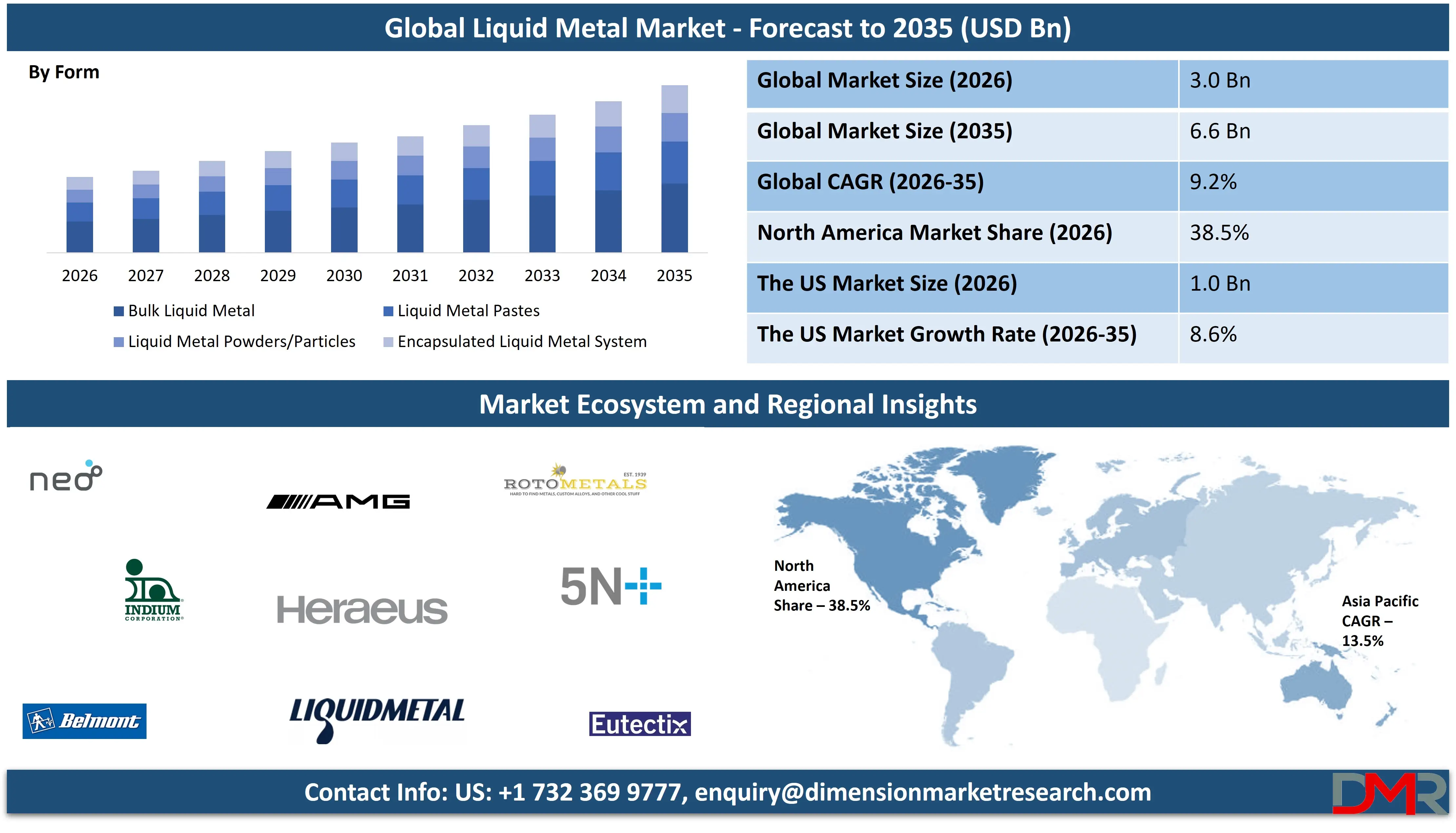

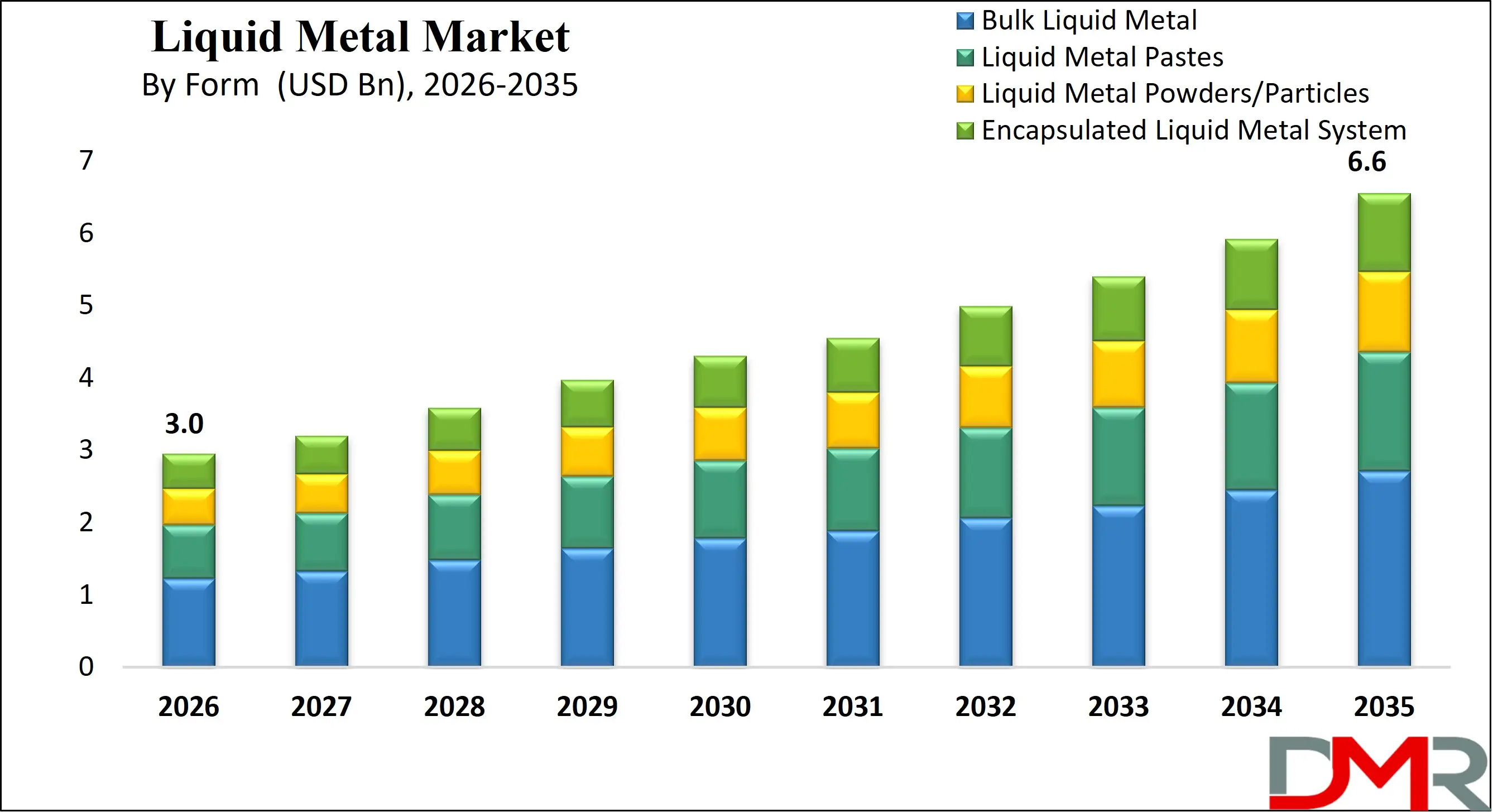

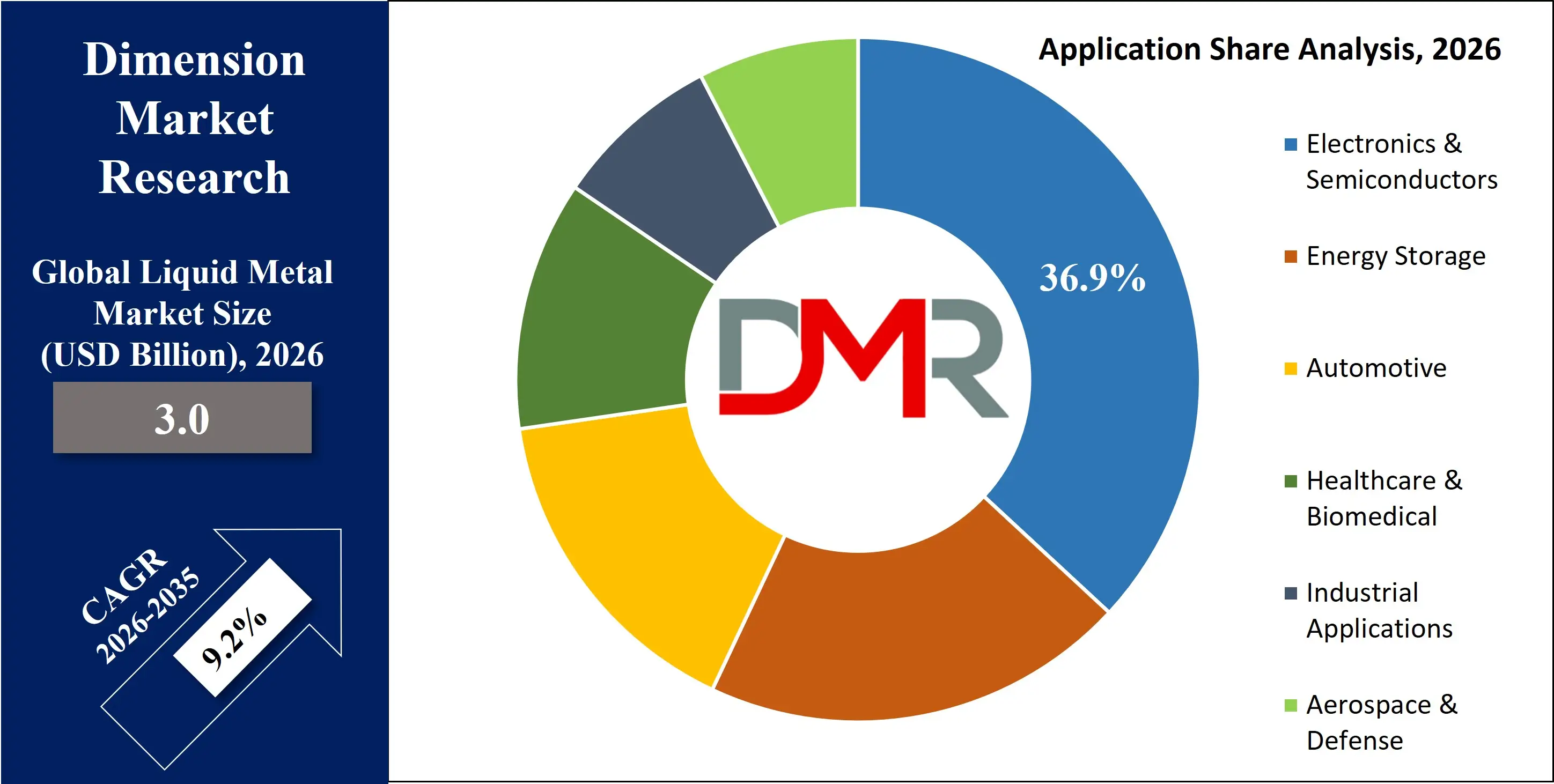

The Global Liquid Metal Market size is projected to reach USD 3.0 billion in 2026 and grow at a compound annual growth rate of 9.2% to reach a value of USD 6.6 billion in 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Liquid metal refers to metals or metal alloys that remain liquid at or near room temperature. These materials are mainly made from gallium, indium, bismuth, and sodium–potassium alloys. Unlike traditional solid metals, liquid metals combine high electrical and thermal conductivity with the ability to flow. This allows them to spread across uneven surfaces and fit into compact or flexible structures. Common types include eutectic gallium–indium (EGaIn), Galinstan, indium-based alloys, and sodium–potassium (NaK) systems. They are available in bulk, as pastes, as powders, or as encapsulated systems. Because of their excellent heat transfer, conductivity, low melting points, and flexibility, they are widely used in electronics, energy storage, automotive, healthcare, aerospace, and industrial applications.

Market growth is mainly driven by increasing demand for better cooling solutions in high-performance computers, electric vehicles, and 5G equipment. As electronic devices become smaller and more powerful, effective heat management becomes more important. The shift toward wearable and flexible devices is also supporting adoption. At the same time, stricter regulations on mercury-based materials are encouraging the use of safer gallium- and indium-based alternatives. The industry is gradually moving from research-focused applications to larger-scale commercial use, especially in semiconductors and grid-level energy storage.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Recent progress includes improved large-scale production of encapsulated liquid metal particles, better integration into flexible circuits, and pilot testing of liquid metal batteries. Companies are forming partnerships with semiconductor and energy firms to speed up commercialization. Ongoing investments in advanced cooling technologies and renewable energy infrastructure are further strengthening market expansion.

The US Liquid Metal Market

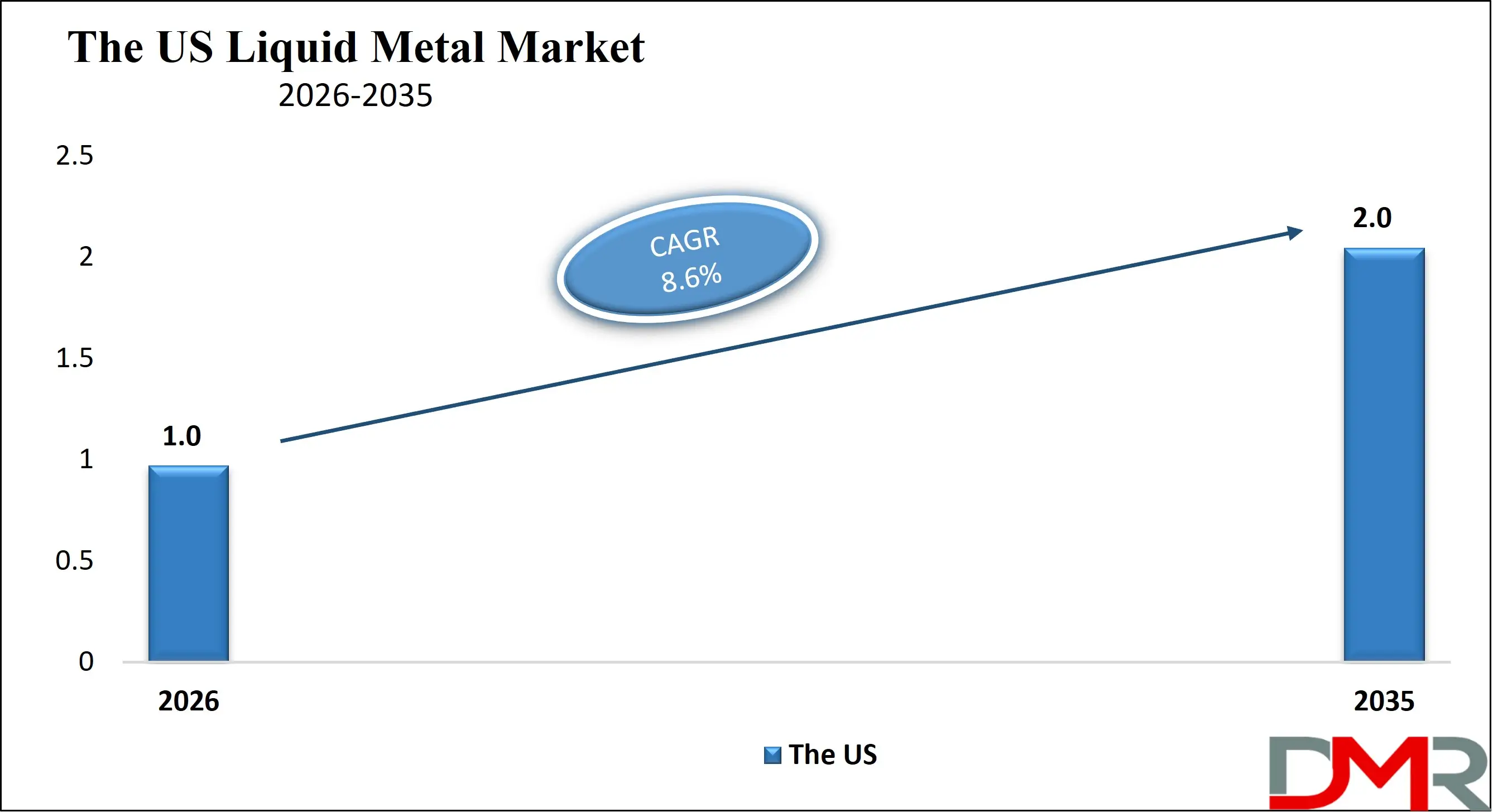

The US Liquid Metal Market size is projected to reach USD 1.0 billion in 2026 at a compound annual growth rate of 8.6% over its forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US represents a technologically advanced and innovation-driven market for liquid metal materials. Strong demand stems from semiconductor manufacturing, electric vehicle production, aerospace engineering, and defense modernization programs. Federal incentives supporting domestic chip fabrication and clean energy storage infrastructure encourage adoption of advanced thermal management and conductive materials. Research institutions and private sector partnerships accelerate product development, particularly in liquid metal batteries and flexible electronics. The presence of established supply chains and high R&D spending strengthens commercialization, while regulatory oversight ensures safer alternatives to mercury-based materials. Market growth is further supported by defense and space exploration investments requiring high-performance cooling systems.

Europe Liquid Metal Market

Europe Liquid Metal Market size is projected to reach USD 750 million in 2026 at a compound annual growth rate of 8.8% over its forecast period.

Europe demonstrates steady expansion driven by sustainability initiatives and advanced manufacturing capabilities. Policies aligned with climate neutrality goals and energy transition strategies encourage adoption of innovative storage technologies, including liquid metal batteries for grid resilience. Automotive electrification across Germany, France, and the Nordic region stimulates demand for efficient thermal management solutions. Strict environmental regulations accelerate the shift away from toxic materials toward gallium- and indium-based alloys. Research funding under regional innovation programs fosters flexible electronics and biomedical applications. The region’s strong aerospace and industrial base also supports specialized cooling and heat-transfer systems, enhancing overall adoption.

Japan Liquid Metal Market

Japan Liquid Metal Market size is projected to reach USD 150 million in 2026 at a compound annual growth rate of 9.0% over its forecast period.

Japan’s market benefits from advanced electronics manufacturing, robotics innovation, and a highly developed automotive industry. Rapid miniaturization of consumer electronics and leadership in semiconductor equipment production create strong demand for precision thermal interface materials. Government initiatives promoting next-generation batteries and renewable integration support research into liquid metal energy storage systems. Urbanization and industrial automation further drive applications in sensors and wearable healthcare devices. However, limited domestic raw material availability poses supply chain challenges, prompting strategic import partnerships. Japan’s emphasis on technological excellence and high-performance materials ensures continued growth across automotive, electronics, and industrial manufacturing sectors.

Liquid Metal Market: Key Takeaways

- Market Growth: The Liquid Metal Market size is expected to grow by USD 3.4 billion, at a CAGR of 9.2%, during the forecasted period of 2027 to 2035.

- By Form: The bulk liquid metal segment is anticipated to get the majority share of the Liquid Metal Market in 2026.

- By Application: The electronic & semiconductors segment is expected to get the largest revenue share in 2026 in the Liquid Metal Market.

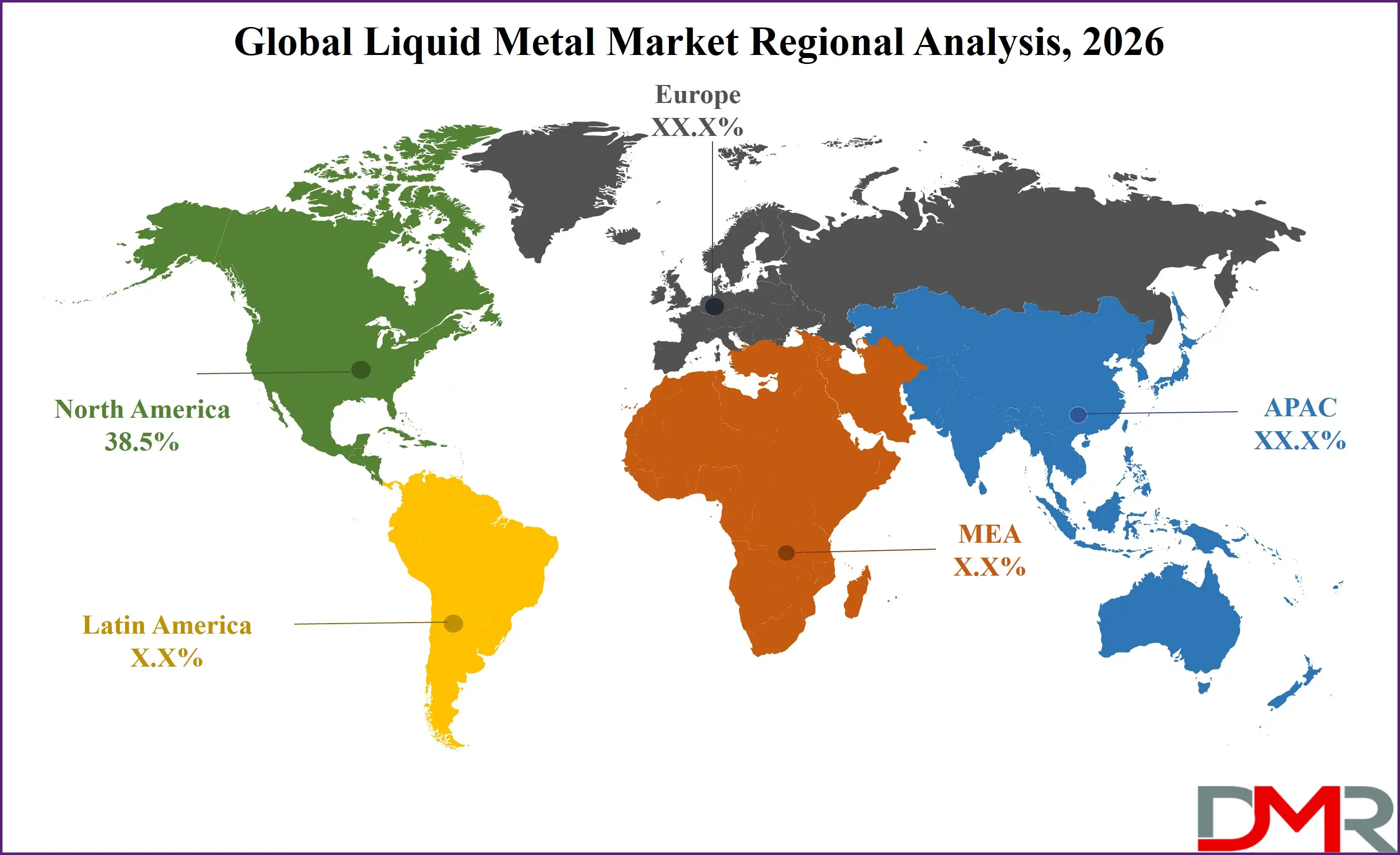

- Regional Insight: North America is expected to hold a 38.5% share of revenue in the Global Liquid Metal Market in 2026.

- Use Cases: Some of the use cases of Liquid Metal include flexible electronics, EV Thermal Management, and more.

Liquid Metal Market: Use Cases

- Thermal Interface Materials: Used in CPUs, GPUs, and EV batteries to enhance heat dissipation and improve performance reliability.

- Flexible Electronics: Enables stretchable circuits and wearable devices due to high conductivity and mechanical adaptability.

- Liquid Metal Batteries: Applied in grid-scale energy storage for renewable energy stabilization and long cycle life.

- Conductive Inks & Printed Circuits: Supports printed electronics for smart packaging and IoT devices.

- EV Thermal Management: Enhances cooling efficiency in electric vehicle battery packs and power electronics.

- Biomedical Devices: Used in soft robotics and wearable health sensors requiring biocompatibility and flexibility.

- Aerospace Cooling Systems: Provides efficient heat transfer in compact and high-performance aerospace components.

Stats & Facts

- The US Department of Energy reported in 2024 that grid-scale battery storage deployment grew by over 100% year-over-year in installed capacity.

- International Energy Agency stated in 2024 that global electricity demand increased by approximately 2.2%.

- European Commission indicated in 2025 that over 40% of electricity generation in the EU came from renewable sources.

- The US Energy Information Administration reported in 2024 that battery storage capacity exceeded 16 GW nationwide.

- Japan Ministry of Economy, Trade and Industry stated in 2024 that EV sales accounted for nearly 3% of total vehicle sales domestically.

- International Renewable Energy Agency reported in 2024 that renewable capacity additions reached 473 GW globally.

Market Dynamic

Driving Factors in the Liquid Metal Market

Rising Demand for Advanced Thermal Management

The expansion of high-performance computing, electric mobility, and compact smart devices is significantly increasing the need for efficient heat dissipation technologies. Liquid metals offer superior thermal conductivity compared to conventional interface materials, making them ideal for densely packed chips and battery modules. As devices become smaller yet more powerful, managing heat effectively becomes critical to prevent failures. Industries are therefore adopting advanced cooling materials to enhance operational reliability, extend product lifespan, and improve overall energy efficiency.

Expansion of Renewable Energy and Storage Infrastructure

The accelerating transition toward renewable energy sources has intensified the demand for reliable and long-duration energy storage systems. Liquid metal batteries provide advantages such as extended cycle life, enhanced safety, and scalability for grid-scale installations. Utilities and governments are increasingly investing in storage solutions to manage intermittency from solar and wind generation. Simultaneously, modernization of power grids and smart infrastructure development is strengthening the need for durable, high-performance storage technologies worldwide.

Restraints in the Liquid Metal Market

High Material and Production Costs

The production of liquid metal materials involves relatively scarce elements such as gallium and indium, which are often obtained as by-products of other mining processes. This dependency contributes to price fluctuations and supply uncertainties. In addition, advanced processing, purification, and encapsulation methods require specialized equipment and technical expertise, increasing manufacturing costs. These economic factors restrict adoption in price-sensitive sectors and limit widespread commercial deployment, particularly in emerging markets.

Supply Chain and Raw Material Constraints

The supply of critical raw materials is concentrated in limited geographic regions, creating geopolitical and logistical vulnerabilities. Disruptions in mining operations, export restrictions, or trade tensions can significantly affect availability and pricing. Limited reserves of rare metals may also constrain long-term scalability. To address these risks, companies are focusing on diversified sourcing, recycling initiatives, and strategic stockpiling to maintain production stability and reduce dependency on single-region suppliers.

Opportunities in the Liquid Metal Market

Growth in Flexible and Wearable Electronics

Rising consumer demand for wearable health monitors, smart textiles, and flexible gadgets is generating strong opportunities for stretchable conductive materials. Liquid metal-based inks and circuits provide excellent flexibility while maintaining high electrical performance. Their ability to withstand repeated bending and deformation makes them ideal for next-generation electronics. As innovation in soft robotics and biomedical sensors accelerates, liquid metals are positioned to become integral components in emerging flexible technology ecosystems.

Defense and Aerospace Modernization

Growing defense budgets and aerospace innovation programs are creating demand for high-performance thermal management materials. Advanced radar systems, avionics, and space equipment require lightweight yet highly conductive cooling solutions. Liquid metals offer efficient heat transfer capabilities under extreme operational conditions. Modernization initiatives focused on compact and energy-efficient systems further support adoption. These sectors present attractive long-term growth potential due to stringent performance requirements and consistent investment in advanced technologies.

Trends in the Liquid Metal Market

Integration with Printed Electronics

The evolution of additive manufacturing and printed electronics is driving the incorporation of liquid metal inks into customizable circuit fabrication. These materials enable rapid prototyping, improved design flexibility, and scalable production of conductive pathways. Manufacturers benefit from reduced material waste and enhanced precision in circuit layouts. As demand for IoT devices and compact smart components grows, integration with printed electronics is becoming a transformative trend in the industry.

Shift Toward Non-Toxic Alternatives

Increasing environmental awareness and regulatory oversight are encouraging industries to move away from hazardous materials such as mercury. Safer gallium-based alloys are gaining preference due to lower toxicity and comparable conductivity. This shift is influencing product design, research priorities, and compliance strategies across sectors. Companies are investing in sustainable material innovation to align with global environmental standards while maintaining performance efficiency in thermal and electrical applications.

Impact of Artificial Intelligence in Liquid Metal Market

- Material Discovery Optimization: AI accelerates alloy composition analysis to enhance conductivity and stability.

- Predictive Thermal Modeling: Machine learning simulates heat transfer performance before product deployment.

- Manufacturing Process Automation: AI-driven robotics improve encapsulation precision and reduce defects.

- Supply Chain Forecasting: Algorithms predict raw material demand and mitigate shortages.

- Battery Performance Analytics: AI monitors charge-discharge cycles to optimize grid storage systems.

- Quality Inspection Systems: Computer vision ensures consistency in liquid metal particle production.

- Design Simulation Tools: AI-based CAD integration enables rapid prototyping of flexible circuits.

- Lifecycle Monitoring: Predictive analytics extend component lifespan through real-time diagnostics.

Research Scope and Analysis

By Metal Type Analysis

Gallium and gallium-based alloys dominate the liquid metal market due to their exceptional thermal and electrical conductivity, low toxicity compared to mercury, and excellent wettability on diverse substrates. Projected to hold 48.6% market share by 2026, this segment benefits strongly from rising demand in semiconductor packaging, EV battery thermal management, and flexible electronics. Alloys such as EGaIn and Galinstan provide stable performance across varying temperatures while maintaining fluidity near room temperature. Increasing environmental restrictions on hazardous materials further encourage the transition toward gallium systems. Continuous R&D investments aimed at improving oxidation resistance, cost optimization, and encapsulation techniques are reinforcing this segment’s long-term leadership and commercial scalability.

Sodium–potassium (NaK) alloys represent the fastest-growing material segment, primarily due to their outstanding heat transfer capabilities and extremely low melting points. These alloys remain liquid at sub-zero temperatures, making them ideal for specialized applications in aerospace cooling systems, nuclear reactors, and advanced industrial heat exchangers. Their high thermal conductivity and stability under extreme conditions position them as a preferred solution for mission-critical systems requiring efficient thermal regulation. Although handling complexity and reactivity require stringent safety measures, technological advancements in containment and system integration are expanding their commercial viability. Growing investments in advanced energy systems are expected to further accelerate adoption of NaK alloys.

By Form Analysis

Bulk liquid metal is anticipated to account for 41.3% of the market share by 2026, driven by widespread usage in direct heat transfer, thermal interface materials, and metallurgical processes. This form is particularly valued in large-scale industrial applications where high-volume conductivity and efficient cooling are required. Its ability to conform to irregular surfaces enhances heat dissipation efficiency in EV battery packs and power electronics. Bulk formats are also easier to integrate into existing infrastructure without complex processing requirements. As industrial automation and high-performance computing expand, demand for reliable and high-capacity thermal solutions continues to reinforce this segment’s leadership position globally.

Encapsulated liquid metal systems are rapidly gaining traction due to improved safety, stability, and compatibility with emerging technologies. Encapsulation techniques prevent oxidation, leakage, and direct exposure, enabling their integration into wearable devices, biomedical sensors, and printed electronics. This form enhances material durability while preserving conductivity and flexibility. Increasing interest in soft robotics and stretchable circuits further supports demand for encapsulated systems. Technological progress in microencapsulation and polymer composites has improved scalability and cost efficiency, making these systems commercially viable. As flexible electronics transition from research prototypes to mainstream products, encapsulated liquid metals are positioned for accelerated expansion.

By Application Analysis

Electronics and semiconductors lead the market with a projected 36.9% share by 2026, supported by the escalating need for advanced thermal management in compact and high-performance devices. Increasing transistor density in AI processors, GPUs, and data center servers generates significant heat, necessitating superior conductive materials. Liquid metals outperform traditional thermal greases in heat dissipation, improving device reliability and lifespan. The rapid evolution of 5G infrastructure and high-frequency components further amplifies adoption. Additionally, miniaturization trends in consumer gadgets require adaptable and high-efficiency materials. Strong investment in chip manufacturing facilities worldwide ensures sustained dominance of this application segment.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Energy storage is the fastest-growing application segment, propelled by grid modernization efforts and renewable energy integration worldwide. Liquid metal batteries offer long operational lifespans, intrinsic safety, and high energy efficiency, making them attractive for grid-scale installations. As solar and wind capacity expands, the need for stable and large-capacity storage solutions increases significantly. Governments and utilities are actively funding pilot projects to enhance storage reliability and reduce dependency on lithium-based technologies. The scalability of liquid metal battery systems, combined with reduced degradation over time, strengthens their potential in supporting decarbonization goals and resilient power infrastructure development.

By End-Use Industry Analysis

Consumer electronics is projected to capture 34.2% of the market share by 2026, driven by growing production of smartphones, laptops, gaming systems, and wearable devices. Continuous advancements in processor speed and battery performance generate higher thermal loads, increasing the need for efficient cooling solutions. Liquid metals enable compact designs without compromising performance, supporting thinner and lighter devices. The rise of augmented reality, virtual reality, and AI-enabled gadgets further intensifies demand for high-conductivity materials. Manufacturers are increasingly adopting advanced thermal interface materials to enhance reliability and user experience, reinforcing this segment’s strong contribution to overall market growth.

The energy and power utilities sector is expanding rapidly as grid operators deploy advanced battery technologies to improve stability and resilience. Liquid metal-based storage systems are particularly suited for large-scale, long-duration applications supporting renewable integration. Utilities are seeking cost-effective and durable alternatives to conventional storage technologies to manage peak loads and intermittency challenges. Infrastructure upgrades and smart grid development initiatives further encourage adoption. Additionally, the ability of liquid metal batteries to operate with minimal degradation over extended cycles reduces long-term operational costs. These advantages are positioning the sector as a key growth avenue within the broader market landscape.

The Liquid Metal Market Report is segmented on the basis of the following

By Material Type

- Gallium & Gallium-Based Alloys

- Eutectic Gallium–Indium (EGaIn)

- Galinstan (Gallium–Indium–Tin)

- Gallium–Indium–Tin Alloys

- Indium-Based Alloys

- Bismuth-Based Alloys

- Sodium–Potassium (NaK) Alloys

- Mercury

By Form

- Bulk Liquid Metal

- Liquid Metal Pastes

- Liquid Metal Powders / Particles

- Encapsulated Liquid Metal Systems

By Application

- Electronics & Semiconductors

- Thermal Interface Materials (TIMs)

- Flexible & Printed Electronics

- Conductive Inks & Circuits

- Energy Storage

- Liquid Metal Batteries

- Grid-Scale Storage Systems

- Automotive

- EV Thermal Management

- Sensors & Electronic Components

- Healthcare & Biomedical

- Wearable Sensors

- Biomedical Devices

- Industrial Applications

- Heat Transfer & Cooling Systems

- Metallurgical Processes

- Aerospace & Defense

- Advanced Cooling Systems

- Specialized Components

By End-Use Industry

- Consumer Electronics

- Automotive & Electric Vehicles

- Energy & Power Utilities

- Healthcare & Medical Devices

- Aerospace & Defense

- Industrial Manufacturing

Regional Analysis

Leading Region in the Liquid Metal Market

North America is projected to account for 38.5% of the global market share by 2026, supported by strong semiconductor manufacturing expansion, EV production growth, and sustained defense investments. Federal incentives promoting domestic chip fabrication and clean energy storage deployment significantly accelerate material adoption. The region benefits from advanced R&D infrastructure, university–industry collaborations, and a mature supply chain ecosystem. High adoption of AI-driven data centers and renewable energy projects further boosts demand for advanced thermal and energy storage solutions. Continuous innovation and supportive regulatory frameworks position North America as the dominant regional contributor to overall market revenue.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest Growing Region in the Liquid Metal Market

Asia-Pacific is witnessing the fastest growth, driven by its dominance in electronics manufacturing, rapid EV adoption, and expanding renewable infrastructure. Countries such as China, Japan, and South Korea are investing heavily in semiconductor fabrication plants and battery innovation programs. Urbanization, industrialization, and supportive government policies aimed at clean energy transition are accelerating market penetration. The region’s strong supply chain networks and cost-competitive manufacturing capabilities further enhance scalability. Growing consumer electronics production and increasing grid storage deployments provide sustained demand momentum. These factors collectively position Asia-Pacific as the most dynamic and rapidly expanding regional market.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The Liquid Metal Market is defined by technology-driven competition, high entry barriers rooted in advanced material science expertise, and strong intellectual property portfolios. Companies compete through continuous R&D to enhance the conductivity, thermal stability, and safety of gallium-, indium-, and sodium-based alloys. Strategic partnerships with semiconductor, EV, and energy storage manufacturers are essential for commercialization and long-term supply agreements. Market participants also expand production capacity and adopt vertical integration to manage raw material volatility and geopolitical risks. Ongoing innovation in alloy formulation and encapsulation technologies remains the primary factor shaping competitive differentiation in the Liquid Metal Market.

Some of the prominent players in the global Liquid Metal are

- Liquidmetal Technologies

- Indium Corporation

- 5N Plus Inc.

- Heraeus Holding GmbH

- AMG Advanced Metallurgical Group

- Neo Performance Materials

- Liquid Metals Group Co., Ltd.

- Sino Santech Materials Technology Co., Ltd.

- Metaliqx Pte Ltd.

- Eutectix LLC

- BMG Metals Inc.

- Dongguan EONTEC Co., Ltd.

- Beijing DREAM Ink Technologies

- Gallinstan Technologies

- Advanced Technology & Materials

- Ningbo Shine Magnetic Materials Co., Ltd.

- Zhuzhou Keneng New Material Co., Ltd.

- Yunnan Germanium Co., Ltd.

- RotoMetals, Inc.

- Belmont Metals

- Other Key Players

Recent Developments

- In December 2025, Mitsubishi Chemical Group (MCG) entered into a strategic partnership with Boston Materials, Inc., a specialist in advanced energy transfer materials. As part of the collaboration, MCG’s U.S.-based corporate venture capital arm, Diamond Edge Ventures, has invested in Boston Materials. The partnership aims to accelerate the development of next-generation thermal management solutions tailored for high-performance computing (HPC) and artificial intelligence (AI) data center applications.

- In July 2025, Liquidmetal Technologies, Inc. (announced that its wholly owned Hong Kong subsidiary, Liquidmetal Asia Holdings Limited, has signed an agreement to establish a joint venture named Hangzhou Feifeng Liquidmetal Co. Ltd. The new entity will build a manufacturing facility in Hangzhou, China, dedicated to producing amorphous alloy products. The venture will be owned 70% by Liquidmetal Asia and 30% by an individual investor, backed by an initial capital investment of USD 6.0 million.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 3.0 Bn |

| Forecast Value (2035) |

USD 6.6 Bn |

| CAGR (2026–2035) |

9.2% |

| The US Market Size (2026) |

USD 1.0 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors, etc. |

| Segments Covered |

By Material Type (Gallium & Gallium-Based Alloys, Indium-Based Alloys, Bismuth-Based Alloys, Sodium–Potassium (NaK) Alloys, Mercury), By Form (Bulk Liquid Metal, Liquid Metal Pastes, Liquid Metal Powders / Particles, Encapsulated Liquid Metal Systems), By Application (Electronics & Semiconductors, Energy Storage, Automotive, Healthcare & Biomedical, Industrial Applications, Aerospace & Defense), By End-Use Industry (Consumer Electronics, Automotive & Electric Vehicles, Energy & Power Utilities, Healthcare & Medical Devices, Aerospace & Defense, Industrial Manufacturing) |

| Regional Coverage |

North America – US, Canada; Europe – Germany, UK, France, Russia, Spain, Italy, Benelux, Nordic, Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, Rest of MEA |

| Prominent Players |

Prominent Players Liquidmetal Technologies, Indium Corporation, 5N Plus Inc., Heraeus Holding GmbH, AMG Advanced Metallurgical Group, Neo Performance Materials, Liquid Metals Group Co., Ltd., Sino Santech Materials Technology Co., Ltd., Metaliqx Pte Ltd., Eutectix LLC, BMG Metals Inc., Dongguan EONTEC Co., Ltd., Beijing DREAM Ink Technologies, Gallinstan Technologies, Advanced Technology & Materials, Ningbo Shine Magnetic Materials Co., Ltd., Zhuzhou Keneng New Material Co., Ltd., Yunnan Germanium Co., Ltd., RotoMetals, Inc., Belmont Metals, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days, and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Liquid Metal Market?

▾ The Global Liquid Metal Market size is expected to reach USD 3.0 billion by 2026 and is projected to reach USD 6.6 billion by the end of 2035.

Which region accounted for the largest Global Liquid Metal Market?

▾ North America is expected to have the largest market share in the Global Liquid Metal Market, with a share of about 38.5% in 2026.

How big is the Liquid Metal Market in the US?

▾ The US Liquid Metal market is expected to reach USD 1.0billion by 2026.

Who are the key players in the Liquid Metal Market?

▾ Some of the major key players in the Global Liquid Metal Market include 5N plus Neo, AMG, and others

What is the growth rate in the Global Liquid Metal Market?

▾ The market is growing at a CAGR of 9.2 percent over the forecasted period.