Market Overview

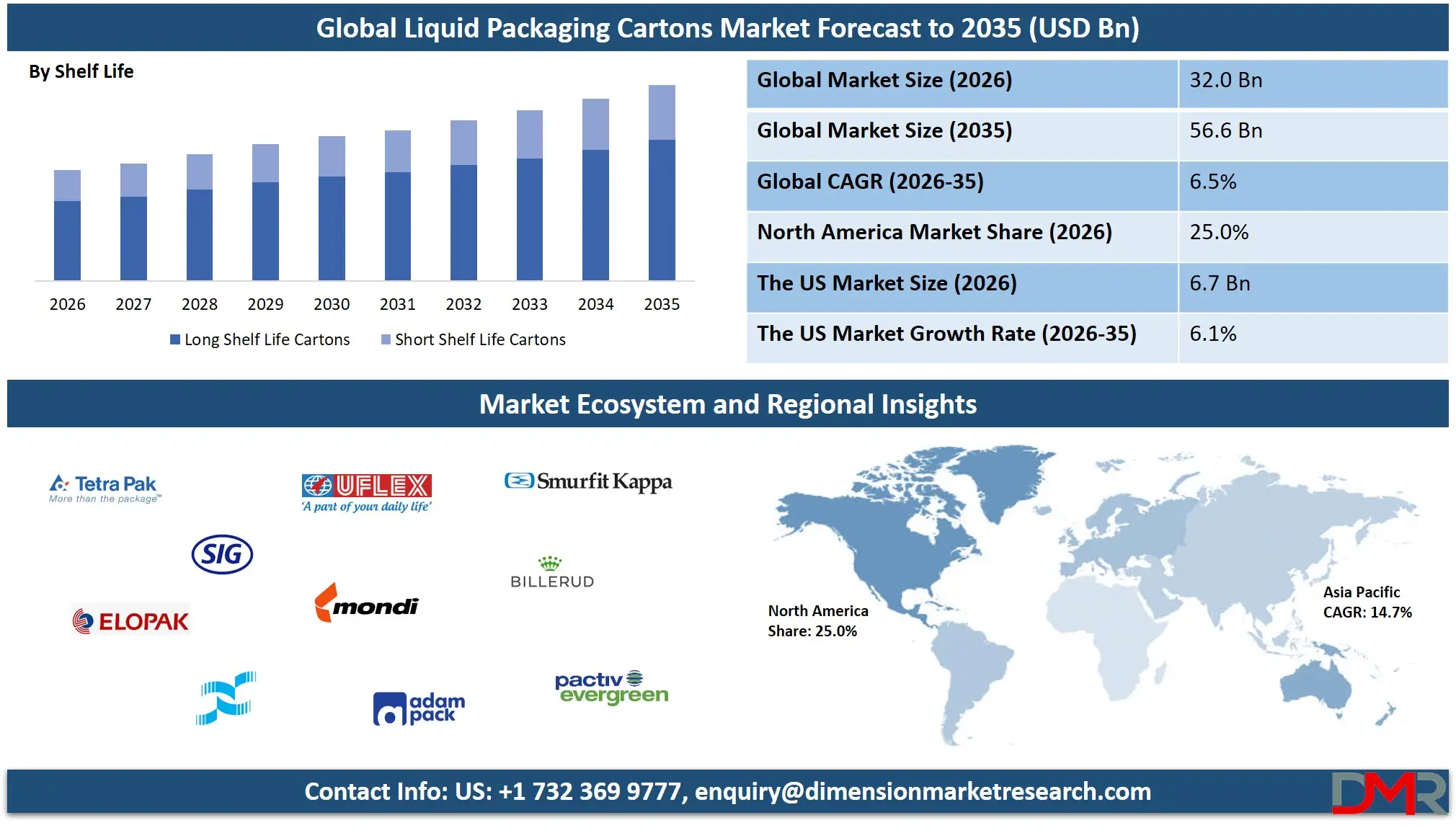

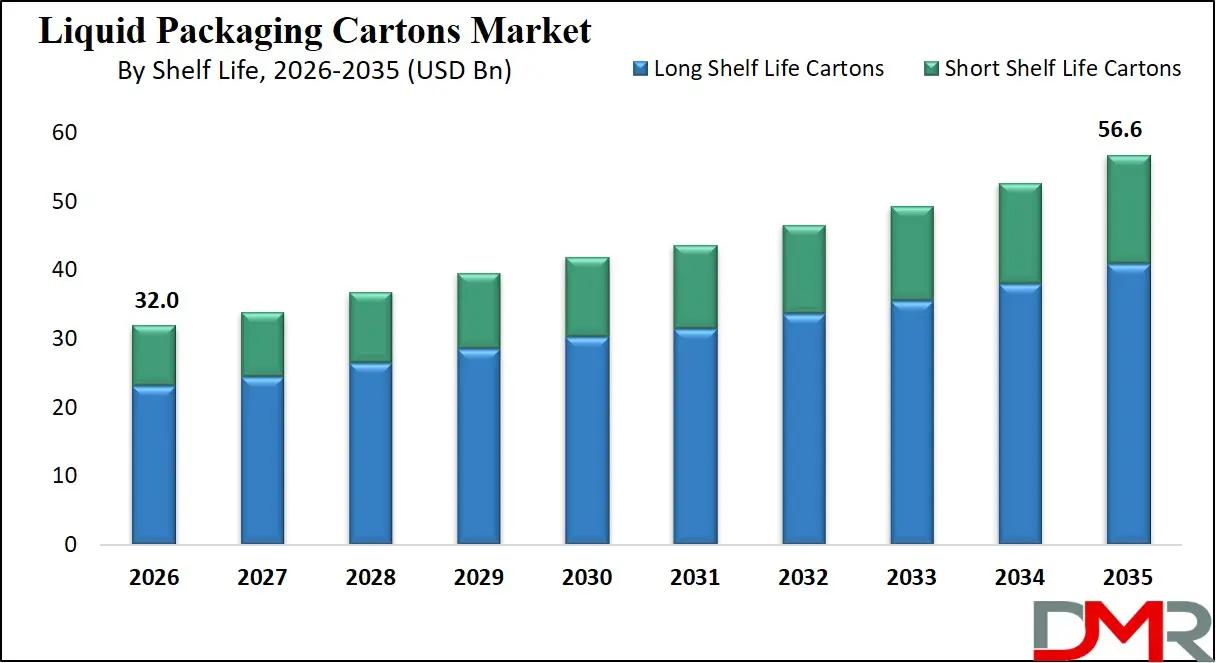

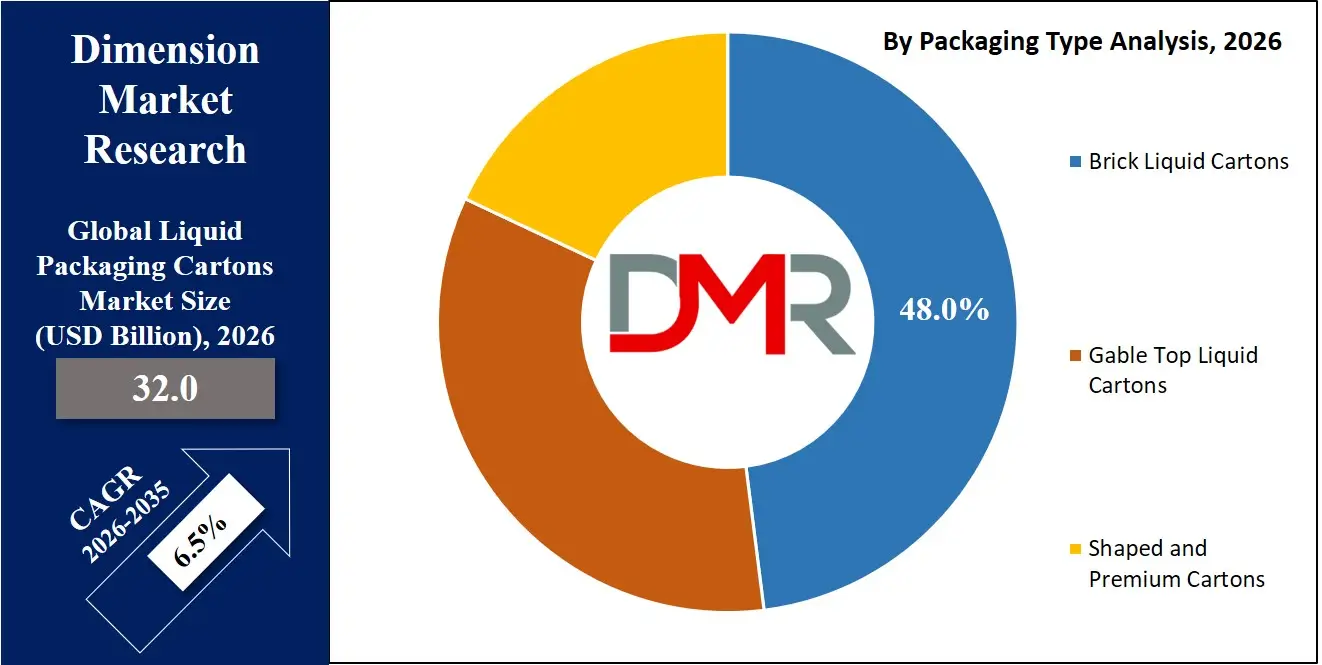

The Global Liquid Packaging Cartons Market is expected to be valued at USD 32.0 billion in 2026 and is projected to grow at a CAGR of 6.5% through 2035, reaching approximately USD 56.6 billion, driven by rising demand for aseptic cartons, dairy packaging solutions, and sustainable beverage packaging formats worldwide.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Liquid packaging cartons are fiber based composite containers specifically designed for storing and transporting liquid products such as milk, fruit juices, plant based beverages, soups, and other fluid foods. These cartons are typically manufactured using multilayer paperboard structures combined with polymer coatings and, in aseptic formats, thin aluminum barriers to protect contents from light, oxygen, and microbial contamination. They are engineered to maintain product freshness, extend shelf life, and ensure safe distribution across long supply chains. Liquid cartons are widely used in the food and beverage industry due to their lightweight structure, stackability, printability for branding, and compatibility with high speed filling lines. Their recyclability and increasing use of renewable materials further enhance their role in sustainable packaging solutions.

The global Liquid Packaging Cartons Market represents the worldwide industry involved in the production, distribution, and sale of carton based liquid packaging systems across dairy, beverage, and liquid food sectors. This market includes aseptic cartons, gable top cartons, and shaped packaging formats used in both refrigerated and ambient distribution channels. Growth is driven by rising consumption of packaged milk, ready to drink beverages, and long shelf life products, particularly in emerging economies. Expansion of modern retail infrastructure, improvements in cold chain logistics, and increasing demand for convenient and portion sized packaging formats continue to strengthen market penetration across both developed and developing regions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

From an industry perspective, the global market is influenced by technological advancements in aseptic processing, material innovation in paperboard packaging, and regulatory emphasis on sustainable and recyclable materials. Manufacturers are investing in bio based polymers, renewable fiber sourcing, and lightweight carton designs to reduce carbon footprint and improve environmental performance. Competitive dynamics are shaped by large multinational packaging solution providers, regional converters, and integrated filling technology companies. As consumer preference shifts toward eco-friendly beverage packaging and safe food containment solutions, the market is expected to maintain steady growth supported by dairy consumption trends, plant based drink adoption, and expansion of the global packaged beverage industry.

The US Liquid Packaging Cartons Market

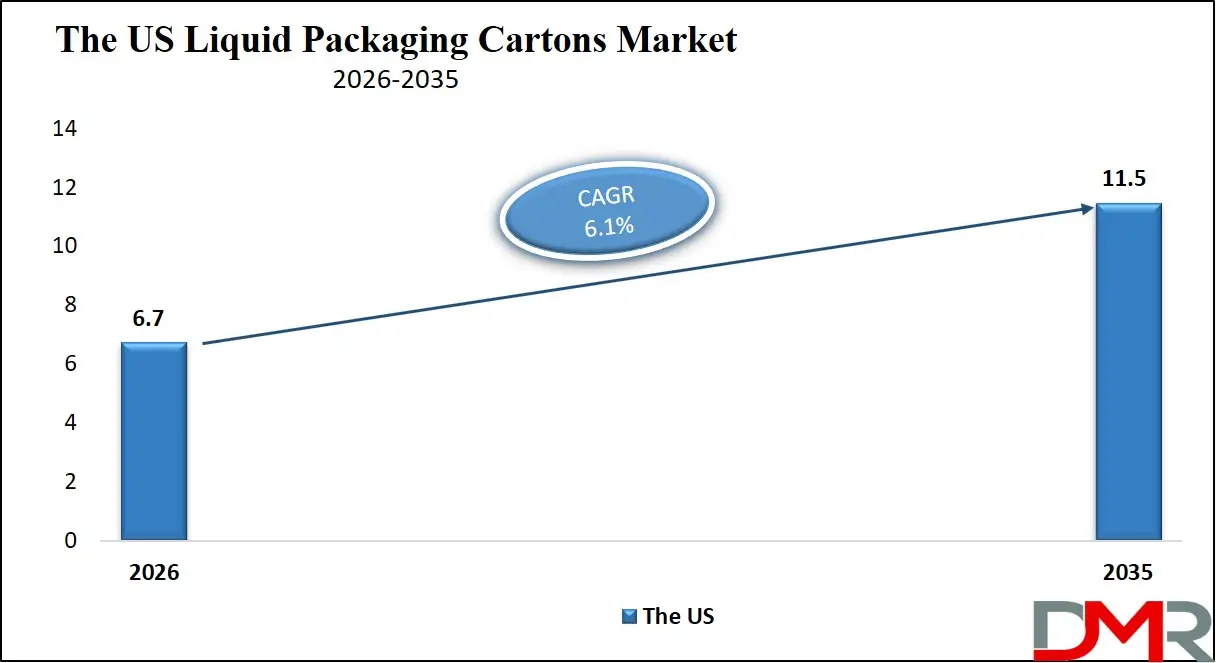

The U.S. Liquid Packaging Cartons Market size is expected to reach at USD 6.7 billion in 2026. It is further expected to witness subsequent growth in the upcoming period, holding USD 11.5 billion in 2035 at a CAGR of 6.1%.

The US Liquid Packaging Cartons Market represents a mature yet steadily expanding segment of the broader food and beverage packaging industry, supported by strong consumption of dairy products, plant based beverages, and ready to drink formulations. Demand is largely driven by the widespread use of gable top cartons for fresh milk and aseptic cartons for long shelf life beverages. Growing consumer preference for sustainable packaging, recyclable paperboard materials, and reduced plastic usage is accelerating the shift toward fiber based liquid packaging solutions across retail and foodservice channels.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Market growth in the United States is further supported by advanced filling technology, well established cold chain infrastructure, and strong presence of leading carton manufacturers and packaging solution providers. Increasing adoption of shelf stable milk, functional beverages, and nutritionally fortified drinks continues to expand aseptic carton utilization. Regulatory focus on environmental compliance and extended producer responsibility programs is encouraging innovation in bio based polymers and renewable fiber sourcing. As private label dairy and beverage brands expand, liquid carton packaging remains a preferred format for safety, convenience, and branding flexibility.

The Europe Liquid Packaging Cartons Market

The Europe liquid packaging cartons market is projected to reach approximately USD 9.0 billion in 2026, expanding at a CAGR of 6.2% during the forecast period. Growth is supported by strong demand for aseptic beverage packaging, high per capita consumption of dairy products, and increasing adoption of sustainable paperboard cartons across Western and Northern Europe. Countries such as Germany, France, Italy, and the Nordic region have well established recycling infrastructure and strict environmental regulations, which encourage the use of fiber based liquid packaging solutions over rigid plastics.

Market expansion is further driven by rising demand for plant based beverages, functional drinks, and long shelf life milk products that rely on advanced multilayer carton structures for barrier protection and product safety. European beverage brands are actively investing in renewable materials, aluminum free barrier technologies, and lightweight packaging formats to reduce carbon footprint and comply with circular economy policies. Continuous innovation in aseptic processing and digital printing capabilities is also strengthening Europe's position as a technologically advanced and sustainability focused liquid carton packaging market.

The Japan Liquid Packaging Cartons Market

The Japan liquid packaging cartons market is projected to reach approximately USD 1.6 billion in 2026, expanding at a CAGR of 5.0% over the forecast period. Market growth is supported by steady consumption of packaged milk, ready to drink tea, and functional beverages, which are widely distributed through convenience stores and vending channels. Japan's advanced retail infrastructure and strong preference for hygienic, high quality food packaging solutions continue to drive adoption of aseptic cartons and multilayer paperboard packaging formats across dairy and beverage categories.

Additionally, increasing demand for portion controlled packs and premium beverage packaging is contributing to the expansion of carton based liquid packaging in the country. Sustainability initiatives and resource efficiency policies are encouraging manufacturers to focus on recyclable materials, lightweight carton structures, and renewable fiber sourcing. While growth remains moderate compared to emerging Asian markets, technological sophistication, high quality standards, and consistent consumer demand for packaged liquid products position Japan as a stable and innovation driven market within the global liquid packaging cartons industry.

Global Liquid Packaging Cartons Market: Key Takeaways

- Strong Long-Term Growth Outlook: The Global Liquid Packaging Cartons Market is projected to grow from USD 32.0 billion in 2026 to USD 56.6 billion by 2035, driven by rising demand for aseptic, shelf-stable, and sustainable beverage packaging solutions worldwide.

- Dominance of Long Shelf Life Formats: Long shelf life cartons lead the market due to increasing consumption of UHT milk, plant-based drinks, and ready-to-drink beverages requiring advanced barrier protection and ambient distribution.

- Sustainability Driving Innovation: Growing regulatory pressure and consumer preference for eco-friendly packaging are accelerating adoption of renewable fiber, bio-based polymers, aluminum-free barriers, and lightweight carton designs.

- Asia Pacific Leads Market Expansion: Asia Pacific holds the largest revenue share and highest growth rate, supported by expanding dairy consumption, urbanization, and growth in organized retail infrastructure.

- Technology Enhancing Operational Efficiency: Advancements in aseptic filling, digital printing, AI-based quality monitoring, and smart traceability are improving efficiency, product safety, and brand differentiation across the industry.

Global Liquid Packaging Cartons Market: Use Cases

- Dairy Processing and Long Shelf Life Milk Distribution: Liquid packaging cartons play a critical role in global dairy processing by enabling safe storage and transportation of white milk, flavored milk, and lactose free products. Aseptic cartons combined with ultra-high temperature processing allow dairy beverages to remain shelf stable without refrigeration, supporting export oriented supply chains and rural distribution networks. Multilayer paperboard structures protect against light and oxygen exposure, preserving nutritional value and taste. This use case is especially important in emerging markets where cold chain infrastructure is limited and demand for packaged dairy products is rising.

- Fruit Juice and Ready to Drink Beverage Packaging: Carton based liquid packaging is widely used for fruit juice, vegetable juice, and ready to drink tea and coffee products. Aseptic filling technology ensures microbial safety while maintaining flavor integrity and extended shelf life. Brick cartons offer efficient stacking and cost effective logistics for high volume beverage manufacturers. In developed markets, shaped and portion size cartons enhance branding and convenience for on the go consumption. Growing demand for clean label beverages and sustainable packaging materials further strengthens carton adoption in the non-alcoholic beverage segment.

- Plant Based and Functional Beverage Solutions: The rapid growth of plant based beverages such as almond, soy, and oat drinks has significantly expanded demand for aseptic liquid cartons. These products require oxygen and light barrier protection to maintain stability and nutritional performance. Carton packaging supports extended distribution cycles, e commerce channels, and export trade. Manufacturers increasingly prefer renewable paperboard and bio based polymer coatings to align with sustainability goals. Functional beverages fortified with protein, vitamins, and probiotics also rely on carton packaging for safe containment and extended shelf life performance.

- Liquid Food and Nutritional Product Packaging: Liquid packaging cartons are extensively used for soups, broths, stocks, and medical nutrition products. These applications require secure barrier packaging to prevent contamination and maintain product consistency. Aseptic cartons enable ambient storage, reducing refrigeration costs and improving retail shelf efficiency. For clinical nutrition and meal replacement products, cartons provide portion control and tamper evidence features. The growing global demand for convenient meal solutions and packaged liquid foods continues to expand the application scope of carton based liquid packaging systems.

Global Liquid Packaging Cartons Market: Stats & Facts

- India Government / Official Industry Data

- The paper and packaging industry is officially recognized as the fifth largest sector of the Indian economy and continues expanding toward 2025.

- India's paper and paperboard production capacity exceeds 25 million tonnes annually during 2024–25.

- Eurostat (European Commission) – Packaging Waste Data (2023)

- In 2023, the European Union generated 79.7 million tonnes of packaging waste, equivalent to approximately 177.8 kg per person, with 40.4% attributed to paper and cardboard materials.

- In 2023, the EU recorded 35.3 kg of plastic packaging waste per person, of which 14.8 kg was recycled.

- In 2023, the recycling rate for plastic packaging waste in the EU was 42.1%.

Global Liquid Packaging Cartons Market: Market Dynamic

Driving Factors in the Global Liquid Packaging Cartons Market

Rising Demand for Aseptic and Shelf Stable Packaging

Increasing global consumption of shelf stable milk, plant based beverages, and ready to drink products is a major growth driver for the liquid packaging cartons market. Aseptic cartons combined with ultra-high temperature processing allow safe storage without refrigeration, reducing distribution costs and expanding market reach in developing regions. Growth in packaged dairy products and functional beverages has accelerated adoption of multilayer paperboard cartons with advanced barrier protection. Expanding modern retail networks and export oriented beverage trade further strengthen demand for long shelf life liquid packaging solutions.

Shift toward Sustainable and Renewable Packaging Materials

Growing environmental awareness and regulatory pressure to reduce plastic waste are driving the transition toward fiber based packaging formats. Liquid cartons made from renewable paperboard and bio based polymers are increasingly preferred over rigid plastic containers. Brands are investing in recyclable packaging structures and carbon footprint reduction initiatives to meet sustainability targets. Consumer preference for ecofriendly beverage packaging and responsible sourcing practices is influencing procurement decisions across dairy processors and beverage manufacturers, reinforcing the role of sustainable carton packaging systems.

Restraints in the Global Liquid Packaging Cartons Market

High Capital Investment in Aseptic Filling Technology

The adoption of advanced aseptic packaging systems requires significant investment in specialized filling lines, sterilization equipment, and quality control systems. Small and medium sized beverage producers may face financial constraints when transitioning from traditional packaging formats to carton based aseptic solutions. Installation complexity and maintenance costs can limit rapid capacity expansion, particularly in cost sensitive markets. This capital intensive nature of integrated carton packaging and filling technology can act as a barrier to entry for new participants.

Recycling Infrastructure and Material Recovery Challenges

Although liquid cartons are largely recyclable, effective recycling depends on well-established collection and material recovery infrastructure. In several regions, separation of paperboard, polymer layers, and aluminum barriers remains technically challenging and economically demanding. Limited awareness regarding carton recycling processes can reduce recovery rates. Regulatory compliance requirements and extended producer responsibility obligations may increase operational costs for manufacturers, particularly in markets where waste management systems are still developing.

Opportunities in the Global Liquid Packaging Cartons Market

Expansion of Plant Based and Functional Beverage Segments

Rapid growth in plant based milk alternatives, protein enriched drinks, and fortified beverages presents strong opportunities for carton manufacturers. These products require protective barrier packaging to maintain nutritional stability and extended shelf life. Increasing consumer demand for lactose free dairy, immunity boosting beverages, and clean label formulations supports higher adoption of aseptic liquid cartons. Emerging markets in Asia Pacific and Latin America offer significant growth potential as plant based beverage penetration continues to expand.

Innovation in Bio Based and Lightweight Carton Structures

Technological advancements in renewable fiber sourcing, plant based polymer coatings, and lightweight carton design create new growth avenues. Development of aluminum free barrier solutions and fully renewable packaging formats enhances sustainability credentials while reducing material usage. Brands are actively seeking innovative beverage packaging solutions that balance performance, cost efficiency, and environmental responsibility. These innovations can open premium market segments and strengthen competitive positioning for carton packaging providers.

Trends in the Global Liquid Packaging Cartons Market

Increasing Adoption of Resealable and Convenience Packaging

Consumer lifestyles are driving demand for resealable screw caps, portion controlled packs, and on the go beverage formats. Carton manufacturers are integrating ergonomic design features to improve user convenience and product freshness after opening. Family size packs and single serve cartons are gaining popularity across dairy and ready to drink beverage categories. This trend reflects broader shifts toward convenience driven food packaging and enhanced consumer experience in retail environments.

Digital Printing and Smart Packaging Integration

The integration of digital printing technology and smart labeling solutions is transforming carton based liquid packaging. Advanced printing enables high quality branding, limited edition packaging, and faster product launches. Smart packaging features such as traceability codes and authentication markers enhance supply chain transparency and food safety assurance. As beverage brands compete on differentiation and consumer engagement, liquid packaging cartons are evolving beyond containment to become interactive marketing and traceability platforms.

Global Liquid Packaging Cartons Market: Research Scope and Analysis

By Packaging Type Analysis

Brick liquid cartons are anticipated to dominate the packaging type segment, accounting for approximately 48.0% of the total market share in 2026, primarily due to their structural efficiency, cost effectiveness, and compatibility with aseptic filling technology. Their rectangular design enables optimal palletization, improved storage efficiency, and lower transportation costs across long distance supply chains. Brick cartons are widely used for shelf stable milk, fruit juices, plant based beverages, and other long shelf life liquid products because they provide strong barrier protection against light and oxygen. The multilayer paperboard structure combined with aluminum or polymer coatings enhances product safety, extends shelf life, and supports large scale beverage packaging operations globally.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Gable top liquid cartons represent another significant segment within the market, primarily used for refrigerated dairy products and fresh beverages. These cartons are commonly utilized for fresh white milk, flavored milk, cream, and chilled juices due to their convenient pourability and consumer friendly design. Unlike aseptic brick cartons, gable top formats are typically associated with short shelf life applications and depend on cold chain distribution. Their strong presence in North America and parts of Europe reflects mature dairy consumption patterns and established refrigeration infrastructure. Increasing demand for sustainable packaging and recyclable paperboard materials continues to support steady adoption of gable top liquid cartons in the fresh beverage segment.

By Shelf Life Analysis

Long shelf life cartons are anticipated to dominate the shelf life segment, capturing approximately 72.0% of the total market share in 2026, largely due to their compatibility with aseptic packaging technology and ultra-high temperature processing. These cartons allow milk, fruit juices, plant based beverages, and liquid nutritional products to be stored at ambient temperatures without refrigeration, significantly reducing logistics and distribution costs. The multilayer paperboard structure with aluminum or advanced polymer barriers protects against light, oxygen, and microbial contamination, ensuring product safety and extended freshness. Strong demand from emerging economies, expansion of modern retail networks, and increasing preference for shelf stable beverage packaging continue to strengthen the dominance of long shelf life liquid cartons globally.

Short shelf life cartons account for the remaining share of the segment and are primarily used for refrigerated dairy and fresh beverage applications. These cartons are commonly utilized for pasteurized milk, flavored milk, cream, and chilled juices that require cold chain distribution to maintain quality and safety. Gable top cartons are widely associated with this category due to their convenient design and suitability for fresh consumption products. Although this segment faces limitations in regions with underdeveloped refrigeration infrastructure, it remains important in mature markets with strong dairy consumption and established cold storage systems, supporting steady demand within the overall liquid packaging cartons market.

By Material Structure Analysis

Multi-layer paperboard cartons are anticipated to dominate the material structure segment, capturing approximately 86.0% of the total market share in 2026 due to their superior barrier performance, structural strength, and compatibility with aseptic filling systems. These cartons typically consist of layered paperboard combined with polyethylene coatings and, in many cases, thin aluminum foil to provide protection against moisture, oxygen, and light exposure. This structure ensures product integrity for shelf stable milk, fruit juices, plant based beverages, and liquid nutritional products. Their lightweight design, cost efficiency, and ability to support high speed beverage packaging lines make them the preferred material format across global dairy and ready to drink beverage industries.

Bio based and renewable cartons represent a growing segment within the material structure category, driven by increasing emphasis on sustainable packaging and carbon footprint reduction. These cartons incorporate plant based polymers, renewable fiber sourcing, and in some cases aluminum free barrier solutions to enhance recyclability and environmental performance. Beverage brands and dairy processors are increasingly adopting renewable packaging materials to meet regulatory requirements and consumer demand for eco-friendly liquid packaging. Although currently smaller in market share compared to conventional multilayer structures, this segment is gaining momentum as sustainability initiatives and circular economy practices reshape the global beverage packaging landscape.

By Closure Type Analysis

Resealable screw caps are anticipated to dominate the closure type segment, capturing approximately 69.0% of the total market share in 2026 due to their strong consumer convenience and enhanced product preservation capabilities. These closures are widely used in aseptic cartons and large format dairy packaging, allowing multiple use occasions while maintaining freshness and reducing spillage. Resealable caps improve user experience for shelf stable milk, plant based beverages, and ready to drink products by offering controlled pouring and secure reclosure. Their integration with advanced carton packaging systems also supports tamper evidence and extended shelf life performance, making them the preferred closure solution across retail beverage categories.

Non resealable openings account for the remaining share of the segment and are typically used in cost sensitive or single serve liquid packaging applications. These closures are common in smaller portion packs, school milk programs, and institutional distribution where immediate consumption is expected. While they offer lower production costs and simplified manufacturing processes, they provide limited functionality after initial opening. Despite lower convenience compared to screw caps, non resealable carton openings remain relevant in emerging markets and bulk supply chains where affordability and high volume distribution are key purchasing factors within the global liquid packaging cartons market.

By Application Analysis

Dairy products are anticipated to dominate the application segment, capturing approximately 52.0% of the total market share in 2026, driven by high global consumption of white milk, flavored milk, yogurt drinks, and other liquid dairy formulations. Liquid packaging cartons are widely preferred in this segment due to their strong barrier protection, compatibility with aseptic processing, and suitability for both refrigerated and shelf stable distribution. The use of multilayer paperboard cartons ensures product safety, extended freshness, and efficient transportation across long supply chains. Rising demand for lactose free milk, fortified dairy beverages, and value added dairy products continues to strengthen carton penetration within the global dairy packaging industry.

Nonalcoholic beverages represent another significant application within the market, supported by growing consumption of fruit juices, plant based beverages, ready to drink tea, and functional drinks. Aseptic cartons are extensively used to preserve flavor, nutritional content, and shelf life without the need for preservatives. Increasing urbanization, health conscious consumer preferences, and expansion of modern retail channels are driving demand for sustainable beverage packaging formats. Brick cartons and portion size packs are particularly popular in this segment due to their convenience, branding flexibility, and efficient logistics, reinforcing steady growth in carton based packaging for non-alcoholic beverage products.

The Global Liquid Packaging Cartons Market Report is segmented on the basis of the following:

By Packaging Type

- Brick Liquid Cartons

- Aseptic Brick Cartons

- Standard Brick Cartons

- Gable Top Liquid Cartons

- Refrigerator Dairy Cartons

- Refrigerator Beverage Cartons

- Shaped and Premium Cartons

- Slim Cartons

- Curve and Contour Cartons

- Portion Size and On the Go Cartons

By Shelf Life

- Long Shelf Life Cartons

- Short Shelf Life Cartons

By Material Structure

- Multi-Layer Paperboard Cartons

- Aluminum Barrier Structure

- Polymer Barrier Structure

- Bio Based and Renewable Cartons

- Plant Based Polymer Coated Cartons

- Fully Renewable Fiber Cartons

By Closure Type

- Resealable Screw Caps

- Non Resealable Openings

By Application

- Dairy Products

- Non Alcoholic Beverages

- Alcoholic Beverages

- Liquid Food Products

Impact of Artificial Intelligence in the Global Liquid Packaging Cartons Market

The impact of artificial intelligence in the global liquid packaging cartons market is becoming increasingly significant as manufacturers and converters integrate smart technologies to improve operational efficiency, enhance quality control, and drive innovation across the value chain. In production facilities, AI powered vision systems and machine learning algorithms are used to monitor high speed filling lines, detect defects in carton formation, and optimize sealing and closure processes. By analyzing real time data from sensors and equipment, AI enables predictive maintenance that minimizes unplanned downtime and extends the lifecycle of packaging machines. This leads to lower operational costs, improved throughput, and higher overall equipment effectiveness for liquid carton producers.

Beyond manufacturing automation, artificial intelligence is also influencing supply chain optimization and demand forecasting within the liquid packaging cartons market. Advanced analytics models can predict seasonal trends in dairy, beverage, and functional drink consumption, allowing manufacturers to better align production schedules with market demand. AI driven inventory management reduces waste and improves material utilization for multilayer paperboard and polymer components. Additionally, smart packaging initiatives leveraging AI enabled traceability systems are gaining traction, allowing stakeholders to verify product authenticity, monitor cold chain conditions, and enhance end to end transparency. As beverage brands prioritize sustainability, efficiency, and consumer engagement, artificial intelligence technologies will continue to reshape packaging innovation, supply chain resilience, and market competitiveness in the global liquid cartons industry.

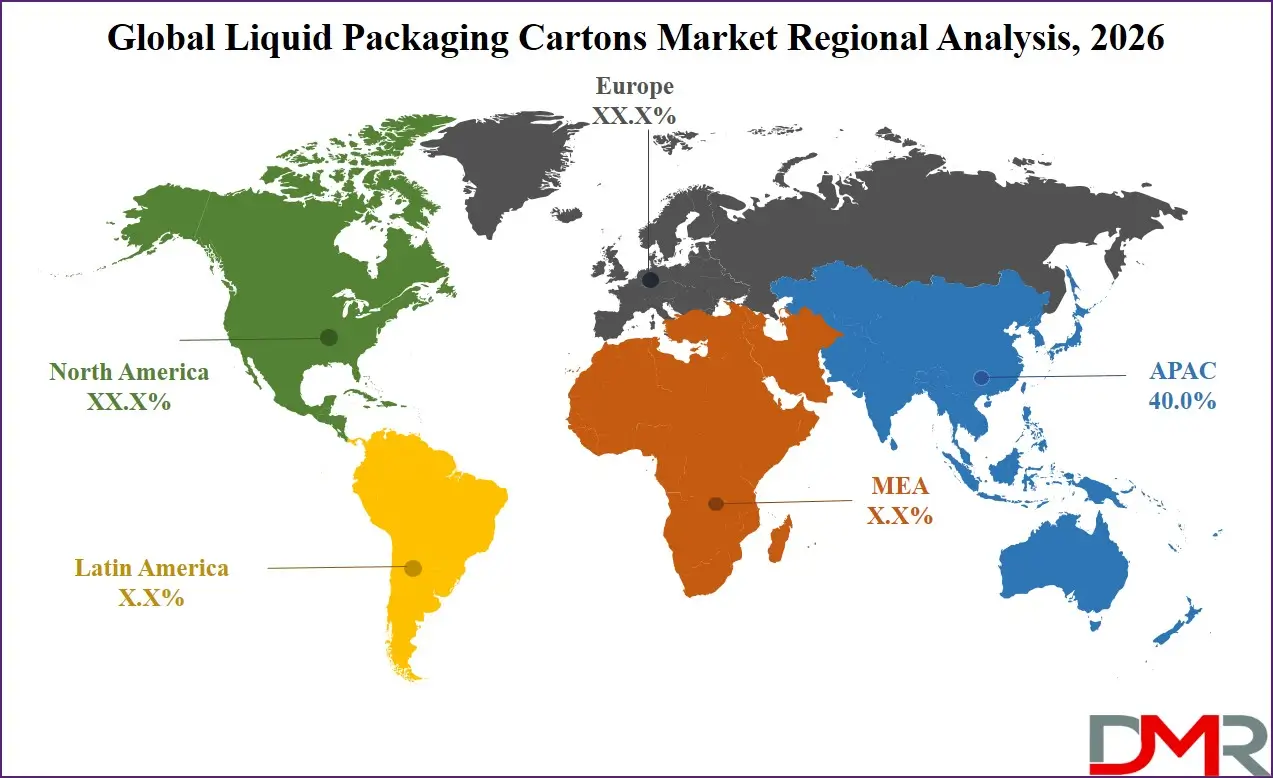

Global Liquid Packaging Cartons Market: Regional Analysis

Region with the Largest Revenue Share

Asia Pacific is anticipated to lead the global Liquid Packaging Cartons Market landscape, accounting for approximately 40.0% of total global market revenue in 2026, driven by strong growth in dairy consumption, rising demand for aseptic beverage packaging, and rapid expansion of modern retail infrastructure across China, India, and Southeast Asia. Increasing urbanization, higher disposable incomes, and growing preference for packaged milk, fruit juices, and plant based beverages are accelerating adoption of multilayer paperboard cartons. In addition, expanding cold chain networks and investment in shelf stable liquid food distribution are reinforcing the region's dominance in the global liquid carton packaging industry.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Region with the Highest CAGR

Asia Pacific is projected to register the highest CAGR in the global Liquid Packaging Cartons Market during the forecast period, driven by expanding dairy production, rising consumption of packaged beverages, and increasing adoption of aseptic packaging solutions in emerging economies such as China and India. Rapid urbanization, growth of organized retail, and improving distribution infrastructure are accelerating demand for shelf stable milk, fruit juices, and plant based drinks. Strong population growth and rising disposable incomes further support sustained expansion, positioning Asia Pacific as the fastest growing regional market globally.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Liquid Packaging Cartons Market: Competitive Landscape

The competitive landscape of the global Liquid Packaging Cartons Market is characterized by intense rivalry among established packaging solution providers and regional converters, focused on technological innovation, capacity expansion, and sustainability initiatives. Key players are investing in advanced aseptic filling systems, renewable material development, and lightweight carton structures to enhance performance and meet stringent environmental regulations. Strategic collaborations with beverage manufacturers and dairy processors are driving custom packaging solutions, while digital printing and smart packaging technologies are being adopted to support brand differentiation. Overall, competition is shaped by efforts to improve operational efficiency, expand geographic presence, and address evolving consumer preferences for eco-friendly and convenient liquid packaging formats.

Some of the prominent players in the Global Liquid Packaging Cartons Market are:

- Tetra Pak International S.A.

- SIG Combibloc Group AG

- Elopak AS

- Nippon Paper Industries Co., Ltd.

- Uflex Limited

- Mondi plc

- Smurfit Kappa Group plc

- Billerud AB

- Adam Pack S.A.

- Pactiv Evergreen Inc.

- Amcor plc

- Greatview Aseptic Packaging Co. Ltd.

- IPI S.r.l.

- Stora Enso Oyj

- WestRock Company

- Heli Packaging Technology Co., Ltd.

- Parksons Packaging Ltd.

- Evergreen Packaging LLC

- TidePak Aseptic Packaging Material Co. Ltd.

- Liqui-Box Corporation

- Other Key Players

Recent Developments in the Global Liquid Packaging Cartons Market

- January 2026: A leading global packaging company launched a paper based barrier aseptic juice carton designed to replace conventional aluminum layers with renewable materials, significantly reducing carbon footprint while maintaining product protection and extended shelf life for beverage applications.

- January 2025: A major liquid carton manufacturer introduced an advanced aseptic milk carton incorporating a high renewable fiber content and paper based barrier structure, aimed at improving recyclability and supporting sustainable dairy packaging initiatives.

- November 2024: A prominent global packaging corporation announced an agreement to acquire a large international packaging and healthcare solutions company in a multi-billion dollar transaction to expand its production capabilities and strengthen its position across beverage and liquid packaging segments.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 32.0 Bn |

| Forecast Value (2035) |

USD 56.6 Bn |

| CAGR (2026–2035) |

6.5% |

| The US Market Size (2026) |

USD 6.7 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Packaging Type (Brick Liquid Cartons, Gable Top Liquid Cartons, Shaped and Premium Cartons), By Shelf Life (Long Shelf Life Cartons, Short Shelf Life Cartons), By Material Structure (Multi-Layer Paperboard Cartons, Bio Based and Renewable Cartons), By Closure Type (Resealable Screw Caps, Non Resealable Openings), By Application (Dairy Products, Non Alcoholic Beverages, Alcoholic Beverages, Liquid Food Products) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Tetra Pak International S.A., SIG Combibloc Group AG, Elopak AS, Nippon Paper Industries Co., Ltd., Uflex Limited, Mondi plc, Smurfit Kappa Group plc, Billerud AB, Adam Pack S.A., Pactiv Evergreen Inc., Amcor plc, Greatview Aseptic Packaging Co. Ltd., IPI S.r.l., Stora Enso Oyj, WestRock Company |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Liquid Packaging Cartons Market?

▾ The Global Liquid Packaging Cartons Market size is estimated to have a value of USD 32.0 billion in 2026 and is expected to reach USD 56.6 billion by the end of 2035.

What is the growth rate in the Global Liquid Packaging Cartons Market in 2026?

▾ The market is growing at a CAGR of 6.5% over the forecasted period of 2026.

What is the size of the US Liquid Packaging Cartons Market?

▾ The US Liquid Packaging Cartons market is projected to be valued at USD 6.7 billion in 2026. It is expected to witness subsequent growth in the upcoming period as it holds USD 11.5 billion in 2035 at a CAGR of 6.1%.

Which region accounted for the largest Global Liquid Packaging Cartons Market?

▾ Asia Pacific is expected to have the largest market share in the Global Liquid Packaging Cartons Market with a share of about 40.0% in 2026.

Who are the key players in the Global Liquid Packaging Cartons Market?

▾ Some of the major key players in the Global Liquid Packaging Cartons Market are Tetra Pak International S.A., SIG Combibloc Group AG, Elopak AS, Nippon Paper Industries Co., Ltd., Uflex Limited, Mondi plc, Smurfit Kappa Group plc, Billerud AB, Adam Pack S.A., Pactiv Evergreen Inc., Amcor plc, Greatview Aseptic Packaging Co. Ltd., IPI S.r.l., Stora Enso Oyj, WestRock Company, Heli Packaging Technology Co., Ltd, and many others.