What is the Neocloud Market Size?

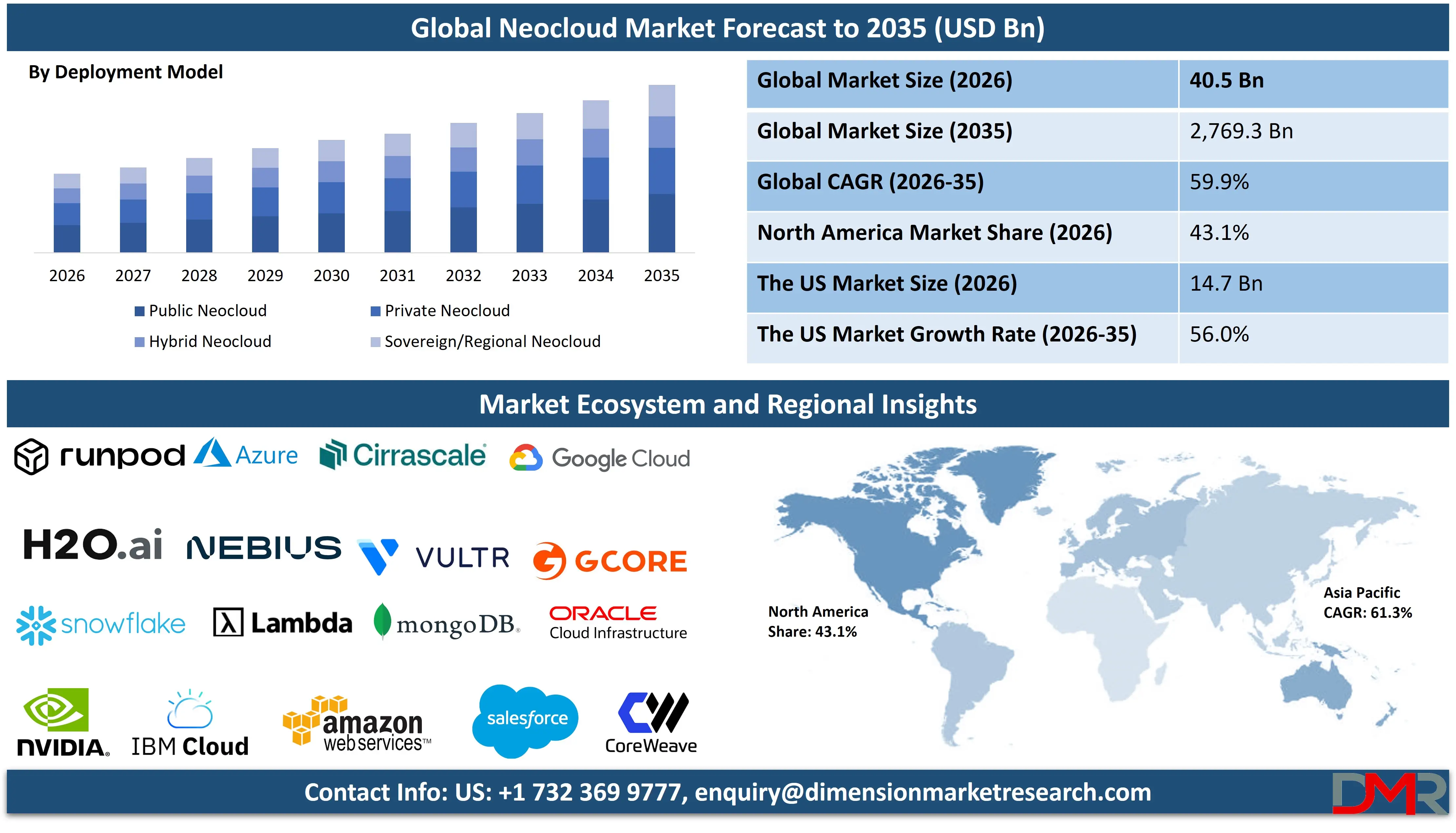

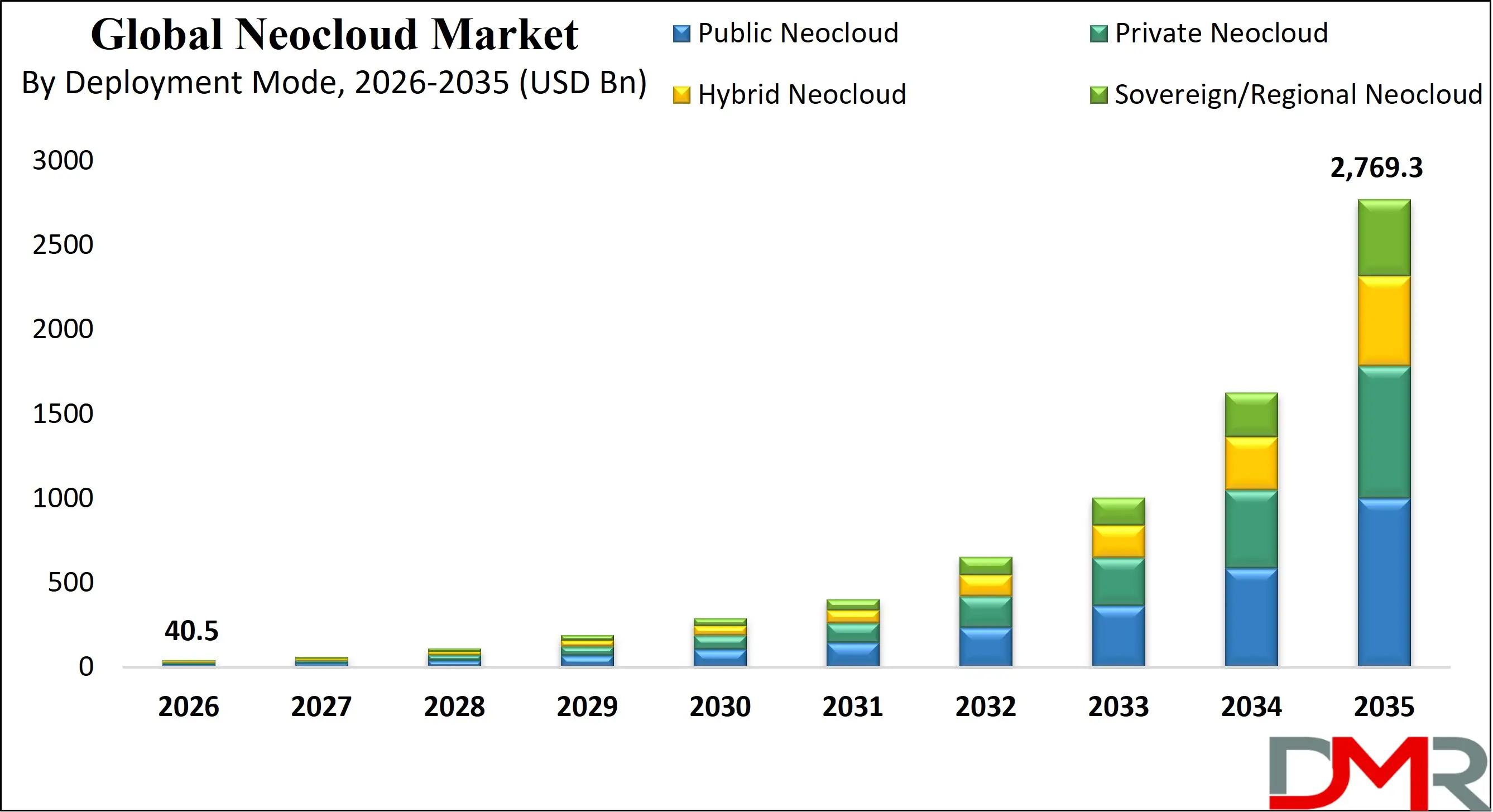

The global neo cloud market is expected to reach a value of USD 40.5 billion in 2026, and it is further anticipated to reach USD 2,769.3 billion by 2035, growing at a CAGR of 59.9% during the forecast period. The neo cloud market is an advanced form of cloud computing, which involves cloud-native application, AI-driven infrastructure, distributed edge, and sovereign cloud infrastructure. It is growing at a fast pace with the growing need of high-performance computing (HPC), AI workloads, real-time data processing as well as scaling digital infrastructure in industries.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Technology centers like Silicon Valley, Western Europe, China and India are becoming global adoption centers with the support of hyperscalers, new neo cloud providers and enterprise digital transformation programs. Its ecosystem has proximal providers of infrastructure, platform development, AI service vendors, and edge computing specialists that provide programmable, flexible, and intelligent cloud environments. The global organizations are moving to neo cloud models to attain higher levels of agility, automation, cost minimization, and regulatory adherence, as well as, accommodate the advanced workloads of generative AI, IoT, and real-time analytics.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Neocloud Market

The US neo cloud market is expected to reach USD 14.7 billion in 2026 which is further projected to grow to USD 801.9 billion by 2035, at a CAGR of 56.0% which indicates high enterprise adoption of the cloud and transformation of cloud by artificial intelligence.

Innovation In the United States, the most innovative in the world in neo clouds, the rapid use of AI-native infrastructure, GPU-as-a-Service (GPUaaS), and cloud-native DevOps frameworks. Companies in the IT, BFSI, healthcare, and manufacturing industries are moving towards neo cloud computing to facilitate high-performance computing, real-time analytics, and scalable hybrid environments.

Major competitors like Amazon Web Services, Microsoft Azure, and Google Cloud also enhance adoption. The robust investments in AI infrastructure, advanced data centers, and edge computing also contribute to growth. Enterprise modernization, demand of generative AI, and the growing requirement of low-latency computing environments are expected to ensure the market grows at a high rate.

Europe Neocloud Market

Europe neo cloud market is expected to reach USD 5.6 billion in 2026 which is further projected to grow to USD 585.9 billion by 2035, at a CAGR of 59.2%. The Europe neo cloud market emerges as a major area of the global ecosystem with the powerful regulation framework and rising demands of sovereign cloud services and data compliance. Although there is a regional differentiation in valuation, Europe is a major player in the global market which is will play major role in this market by the coming decade. Germany, France, and the UK are the European nations that are moving to neo cloud platforms to facilitate AI workloads, hybrid cloud setup, and secure data governance frameworks. Strict GDPR rules promote the growth of the region as it promotes investment in localized cloud infrastructure.

Moreover, companies are also embracing edge and hybrid neo-deployments to maximize the latency and performance of distributed systems. The level of competition is very high, and major players in the world such as Amazon Web Services and Microsoft Azure share the industry with local players. Digital transformation initiatives and increasing need of secure, compliant cloud solutions are expected to drive the growth of the market steadily.

Japan Neocloud Market

The Neocloud market is projected to reach over USD 700.5 million by 2026, at a CAGR of 57.4% for the forecasted period from 2026 to 2035. Japan neo cloud market is within the fast-growing neo cloud market in the Asia-Pacific region, which is currently the fastest expanding neo cloud market in the world.

The Japanese market is fueled by the need to develop AI infrastructure, smart cities, and new technologies in manufacturing. The move towards neo cloud platforms is gaining momentum with enterprises in all industries aiming at utilizing the platform to facilitate real-time data processing, IoT integration, and automation. Government efforts of encouraging digital transformation and data localization are also driving faster adoption. Another area that Japanese companies are using neo cloud is in robotics, autonomous systems as well as high-performance computing applications.

The ecosystem is being reinforced by the availability of global vendors like Google Cloud and Oracle and local innovation. The market is also predicted to expand quickly because of the adoption of AI and the development of edge computing as well as rising investments in enterprise clouds.

Key Takeaways

- Market Size & Forecast: The global neocloud market is projected to reach USD 40.5 billion by 2026 and expand to USD 2,769.3 billion by 2035, driven by rising global cloud adoption.

- Growth Rate & Outlook: Market growth is anticipated to be at a CAGR of 59.9% as a result of digital transformation efforts of companies, dependency on cloud computing services, and the rapid adoption of advanced technologies, particularly those driven by AI.

- Primary Growth Drivers: Growth in this market in accordance of cloud infrastructures will be attributed to the increasing workloads related to AI/ML, edge computing solutions, hybrid clouds, and an increased need for cloud sovereignty.

- Key Market Trends: Some notable trends that shows the high potential of this market include GPU-as-a-Service, cloud-native architecture, edge-cloud fusion, zero trust security approaches, and cloud automation with Infrastructure as Code.

- By Deployment Model Analysis: Hybrid neocloud is projected to dominates this segment wit 35.5% of market share in 2026 as it is prevalent here as companies tend to blend both public scaling and private management capabilities. Companies opt for hybrid clouds to handle their data security issues while utilizing their fast-paced GPU resources from public neocloud vendors.

- By Offering Type Analysis: AI/ML Cloud Platforms are prevalent here as neoclouds are designed for artificial intelligence workloads. The offering type offers integration of AI platforms that help in developing, training, and deploying models effectively to foster innovation and scale.

- By Product Type Analysis: AI/ML training workloads are projected to dominate this segment with 31.5% of market share in 2026 take the lead here since they need highly-intensive GPU resources. Such workloads generate demands for infrastructure, which leads to improvements in artificial intelligence, such as generative AI and prediction systems.

- Regional Leadership: North America is projected to dominate this market with 43.1% of market share by the end of 2026, due to strong hyperscaler presence, while Asia-Pacific is the fastest-growing region, driven by digital economies, cloud-first policies, and increasing government-supported infrastructure investments.

What is the Neocloud?

Neo Cloud (also called Neocloud) can be defined as a newer type of cloud computing environment that is oriented primarily towards supporting applications involving artificial intelligence (AI) and other intensive processes. In contrast to regular cloud platforms, Neo Clouds concentrate solely on providing computing capabilities via GPUs, making them indispensable for AI-related processes. Such cloud computing environments are capable of offering fast computing speeds, scalability, and an efficient computing infrastructure tailored specifically for large-scale operations.

Neo Clouds are typically employed for machine learning and deep learning tasks, conducting scientific calculations, as well as analytics requiring fast computations. As opposed to providing a broad range of services, Neo Clouds concentrate on offering speedy computing capacity.

Use Cases

- AI and Machine Learning Workloads: Businesses leverage GPU-as-a-Service and AI-powered cloud computing solutions that allow fast training of large scale models, as well as real-time inference, resulting in better insight generation and decision-making, along with the ability to utilize artificial intelligence at scale.

- Edge Computing Applications: Neo cloud edge computing services can be used to enable real-time data processing by Internet of Things (IoT) systems, autonomous machines, and smart cities, increasing responsiveness and allowing for quick decisions to be made right where the action takes place.

- DevOps & Automation: Companies can leverage Infrastructure as Code capabilities of neo clouds and implement DevOps and automation strategies, thus automating infrastructure provision and facilitating CI/CD pipelines for faster development, testing, and deployment of applications.

- Hybrid Cloud Deployments: Businesses adopt hybrid cloud approaches, whereby workloads are deployed across multiple locations, including public cloud infrastructure, on-premises systems, and private clouds, which provides flexibility and optimizes performance and cost of operation.

- Data Sovereignty & Compliance: Governments and enterprises utilize sovereign neo cloud technology in order to comply with laws regarding data sovereignty and ensure safe handling of regulated information in accordance with regional regulations.

How AI Is Transforming the Neocloud Market

Artificial intelligence has started revolutionizing the field of neocloud technology by increasing demands for advanced and high-quality infrastructure in the domain. The demands associated with training machine learning algorithms require advanced GPUs, advanced networking and advanced storage capacities, and all of this is leading companies in providing innovative solutions on an ongoing basis. In fact, the companies have started developing data centers that can provide services to enterprises, along with GPU-as-a-service solutions.

Not only this, but artificial intelligence also provides automation of resource allocation, predictive maintenance and advanced workload management capabilities, which ultimately lead to better utilization of resources and efficiency of the cloud infrastructure. Furthermore, in relation to artificial intelligence, cloud service providers have realized their importance for businesses and hence have developed specialized offerings and technologies for meeting the requirements of the users.

Market Dynamics

Key Drivers of the Neocloud Market

Rising Demand for AI and High-Performance Computing

One of the main catalysts of the neocloud market is the rapid adoption of artificial intelligence, machine learning, and advanced analytics. The current AI algorithms demand enormous computing resources, particularly training and real time inference. Neocloud solutions, which have a GPU-intensive architecture and high-speed networking, are required to support such loads effectively. With more companies adopting AI in their business processes, whether through automation or predictive analytics, the need to scale and use high-performance cloud environments is increasing, leading to growth in the market.

Growth of Data-Driven Enterprises

Data is now one of the key resources of organizations to support decision making processes at the strategic level, to enhance the customer experience, and to optimise operations. This move towards data-driven models produces large volumes of structured and unstructured data that have to be processed fast and safely. Neocloud platforms facilitate faster data ingestion, processing as well as storage using optimized architectures. Having the capability to scale resources on-demand enables enterprises to effectively handle variable workloads, and they make them an appealing option to companies needing agility and performance.

Market Challenges / Restraints in the Neocloud Market

High Infrastructure and Operational Costs

The high price of developing and sustaining sophisticated infrastructure is one of the biggest problems in the neocloud market. High-speed interconnects, GPU clusters, and data centers that consume a lot of energy demand a lot of capital. Also, the cost of running the business like electricity, cooling and maintenance increases the financial strain. These can render neocloud services costly to smaller organizations, which may restrict their adoption despite the advantages of performance.

Limited Skilled Workforce

The successful implementation and operation of neoclouds require expert knowledge in fields like AI, cloud architecture and distributed computing. But this highly technical skill of professionals is in short supply worldwide. This skills deficit may slow the implementation process, augment the risks of operations, and decrease the overall performance of the neocloud adoption. Organizations also might experience difficulties in training current employees or recruiting talented employees.

Growth Opportunities in Neocloud Market

Expansion of AI Across Industries

The neocloud market has immense growth prospects as the integration of AI technologies is rapidly growing across various industries, including healthcare, finance, retail, and manufacturing. Computational requirements are unique to each industry, whether it be medical imaging analysis or fraud detection and supply chain optimization. Neocloud providers have a chance to ride on this trend and provide their customers with customized solutions that can meet the needs of a particular industry, consequently increasing their customer base and market coverage.

Emergence of Edge and Distributed Computing

The emergence of edge computing is presenting new possibilities to neocloud platforms to go beyond centralized data centers. Edge-neocloud integration is faster and more efficient in making decisions in real time because it processes data nearer to its origin. It is more essential in such applications as autonomous vehicles, smart cities, and IoT ecosystems. With the increase in the demand of low-latency computing, neocloud providers can create hybrid and distributed solutions to address the changing technological demands.

Trends in the Neocloud Market

Shift Toward GPU-as-a-Service (GPUaaS)

One of the current trends in the neocloud market is the increased popularity of GPU-as-a-Service models. Organizations also do not have to spend on buying hardware at a high price since they can rent the resources of GPUs on-demand and only pay as they use them. This will reduce the entry barriers and will allow both startups and enterprises to get access to high-performance computing. It is also scalable and users are allowed to add or remove resources according to the needs of the workload.

Focus on Sustainability and Energy Efficiency

With the high level of energy consumption in data centres, the sustainability issue has become a major concern to neocloud providers. Firms are investing in energy saving hardware products, superior cooling systems, and renewable energy resources to minimise environmental impact. This is not only because of the regulatory aspects, but also due to the increasing concern of customers with regard to environmental responsibility. Cost savings in the long-run can also be a result of sustainable practices, which makes them a strategic priority of providers.

Research Scope & Analysis

By Offering

The offering segment is projected to dominated by hyperscale cloud providers and AI-first infrastructure firms. Infrastructure-as-a-Service (IaaS) and Platform-as-a-Service (PaaS) are led by companies like Amazon Web Services, Microsoft Azure, and Google Cloud due to their global data center footprint and mature ecosystems. AI/ML cloud platforms are increasingly dominated by NVIDIA Cloud, Google Vertex AI, and AWS SageMaker, driven by demand for AI-native stacks. Cloud software & tooling and developer platforms see strong participation from GitHub, Databricks, and Snowflake. Data platforms are heavily influenced by Snowflake and Databricks due to scalable data lakehouse models. Managed and professional services are led by Accenture and IBM, leveraging enterprise relationships. Overall, dominance is shaped by compute scale, AI capabilities, and integrated service ecosystems.

By Deployment Model

Hybrid neocloud is projected to dominates the deployment model segment as businesses are more inclined towards a balanced platform between public and private cloud environments. With this model, organizations are able to retain sensitive and regulated data on private infrastructure, and use the scalability and high-performance of the GPUs of the public neocloud platforms. It is especially favorable when it comes to AI workloads that involve the dynamic scaling and adaptable allocation of resources across environments. The hybrid configurations are also better equipped to handle disaster recovery, workload portability and compliance needs than the single-cloud configurations. Although edge neocloud is becoming popular with the increase of latency-sensitive applications, such as IoT and autonomous systems, it is an adjunct solution.

By Workload Type

AI/ML training workloads are expected to dominate this segment with the presence of NVIDIA-powered clouds, AWS, and Google Cloud due to their access to high-performance GPUs and specialized AI chips. AI/ML inference workloads are increasingly led by edge-enabled cloud providers and optimized platforms like AWS Inferentia and Google TPU-based services, focusing on cost-efficient real-time processing. High-performance computing (HPC) is dominated by AWS, Microsoft Azure, and specialized providers like IBM and Oracle Cloud, supporting scientific simulations and complex computations. Data analytics and big data processing are led by Databricks, Snowflake, and Google BigQuery due to scalable data processing capabilities. General-purpose workloads continue to be controlled by hyperscalers like AWS and Azure. Overall, dominance is driven by compute power, AI hardware integration, and data processing efficiency.

By Organization Size

Large enterprises are poised to dominate the neocloud market due of their well-developed financial resources and the use of innovative technologies like AI, machine learning, and cloud computing. The infrastructure that is needed by these organizations is highly scalable to accommodate the complexity of workload, global operations, and huge datasets. Neocloud solutions address these requirements by providing high-performance GPU resources, multi-cloud integration, and compliance-ready environments. Security, data governance, and reliability are also important to large enterprises, further motivating them to move to hybrid and private neocloud solutions. Small and medium-sized enterprises (SMEs) are entering the market at an accelerated rate, particularly via more flexible models such as GPU-as-a-Service, but continue to have a lower share in the overall proportion.

By End-User Industry

IT and telecom industry is poised to be the leader in neocloud market since it is both a significant supplier and consumer of neocloud services. These firms are in the vanguard in terms of cloud infrastructure, AI implementation, and high-scale data processing. They use neocloud services to facilitate cloud-native application, network optimization and real-time analytics. Moreover, telecom providers are capitalizing on neocloud features to strengthen 5G networks and edge computing solutions. Although other industries like BFSI and healthcare are fast embracing AI-driven cloud solutions, their application is still increasing relative to IT and telecom. The industry has a fundamental place in facilitating digital infrastructure and innovation, so it is likely to remain a key market force within the neocloud ecosystem.

Neocloud Market Report is segmented based on the following

By Offering

- Infrastructure-as-a-Service (IaaS)

- Platform-as-a-Service (PaaS)

- AI/ML Cloud Platforms (AI Native Cloud Stacks)

- Cloud Software & Tooling

- Developer Platforms

- Data Platforms

- Managed & Professional Services

By Deployment Model

- Public Neocloud

- Private Neocloud

- Hybrid Neocloud

- Sovereign/Regional Neocloud

By Workload Type

- AI/ML Training Workloads

- AI/ML Interference Workloads

- High-Performance Computing (HPC)

- Data Analytics& Big Data Processing

- General-purpose Cloud Workloads

By Organization Size

- Startups & AI-native Companies

- Mid-Market Enterprises

- Large Enterprises

- Research Institutions & Academia

- Government & Defense

By End-User Industry

- BFSI (Banking, Financial Services, Insurance)

- Healthcare & Life Sciences

- Manufacturing

- IT & Telecom

- Media & Entertainment

- Automotive

- Energy & Utilities

- Others

Regional Analysis

Leading Region by Market Share

North America is projected to hold the largest share with 43.1% of market share in the global neocloud market in 2026, driven by the high level of technological infrastructure, the development of artificial intelligence, and the presence of large cloud and artificial intelligence providers like Amazon Web Services, Microsoft Azure, and Google Cloud. The region enjoys great investments in high-performance computer, advanced data centres as well as infrastructure of GPUs. Businesses in all industries are embracing AI-based solutions, creating additional demand on neocloud solutions. Moreover, favorable government policies, good research environments, and incessant innovation also lead to market dominance. The existence of the top AI startups and technology giants, guarantees the continued development and implementation of neocloud solutions, which makes North America the industry leader in revenue and level of technology.

Fastest-Growing Regional Market

Asia-Pacific is posies to be the most significant growth in the neocloud market because of the accelerated digitalization, rising adoption of AI, and the growth of cloud infrastructure in the countries such as China, India, and Japan. The government and companies are spending a lot of money on AI creation, smart cities, and technologies that rely on data and this increases the demand of high-performance cloud solutions. The increasing startup environment and the increasing number of tech-friendly businesses in the region also boost adoption. Also, 5G networks and edge computing enable real-time applications, increasing the use of neocloud. The low cost, a huge user base, and growing awareness of AI potential are making the markets grow quickly, making Asia-Pacific one of the major future locations of innovation and implementation of neoclouds.

Competitive Landscape

The neocloud market is quite competitive and fast-moving because the demand to have AI-oriented infrastructure and high-performance computing is growing. Large cloud providers like Amazon Web Services, Microsoft Azure, and Google Cloud are still leading because of their international infrastructure, large service portfolios, and good relations with enterprises. These firms are also spending a lot of money in the GPU power, AI applications, and expansion of their data centers to stay on top. Meanwhile, they are incorporating high-level AI services into their offerings, which are becoming more enticing to firms interested in end-to-end solutions. The size and financial power enable them to keep on innovating and setting industry standards.

In addition to these giants, there is a new generation of specialized neocloud providers, which only specializes in GPU-intensive workloads and AI infrastructure. Firms such as CoreWeave and Lambda Labs are on the rise with more affordable, high-performance GPU-as-a-service options customized to machine learning and deep learning applications. Flexibility, faster deployment and competitive prices are some of the ways these players distinguish themselves. Startups and mid-sized enterprises often prefer these providers due to their specialization and ability to deliver optimized performance for AI workloads without the complexity of traditional cloud ecosystems.

Some of the prominent players in the Neocloud Market are

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- Oracle Cloud Infrastructure

- IBM Cloud

- Salesforce

- Snowflake

- MongoDB

- CoreWeave

- Lambda

- Cirrascale Cloud Services

- Gcore

- Vultr

- Nebius

- RunPod

- H2O.ai

- Nerdio

- Expedient

- Alibaba Cloud

- NVIDIA

- Other Key Players

Recent Developments

- March 2026: Sharon AI finalized a USD 1.25 billion cloud capacity agreement with ESDS Software Solutions to deploy Nvidia B300 clusters in Australia, significantly boosting the region's high-performance AI infrastructure and catering to the surging demand for localized GPU power.

- March 2026: Nebius raised USD 4.3 billion through convertible notes to scale its global GPU fabric, aiming to challenge traditional hyperscalers by offering specialized, high-density AI infrastructure and expanding its footprint across key European and North American data hubs.

- January 2026: CoreWeave achieved a market capitalization of approximately USD 42 billion following its highly anticipated public listing, solidifying its position as a dominant independent AI cloud provider and reflecting massive investor confidence in the specialized GPU-as-a-Service business model.

- October 2025: Nscale partnered with Aker and OpenAI to launch "Stargate Norway," an ambitious infrastructure project targeting the deployment of 100,000 Nvidia GPUs by 2026 to create one of the world's most powerful and sustainable AI supercomputers.

- January 2025: CoreWeave completed a USD 1.1 billion Series C funding round at a USD 19 billion valuation, led by Coatue Management and Nvidia, to accelerate the global expansion of its specialized data centers designed specifically for large-scale AI workloads.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 40.5 Bn |

| Forecast Value (2035) |

USD 2,768.3 Bn |

| CAGR (2026–2035) |

59.9% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors, etc. |

| Segments Covered |

By Offering (Infrastructure-as-a-Service (IaaS), Platform-as-a-Service (PaaS), AI/ML Cloud Platforms (AI-Native Cloud Stacks), Cloud Software & Tooling, Developer Platforms, Data Platforms, Managed & Professional Services), By Deployment Model (Public Neocloud, Private Neocloud, Hybrid Neocloud, Sovereign/Regional Neocloud), By Workload Type (AI/ML Training Workloads, AI/ML Inference Workloads, High-Performance Computing (HPC), Data Analytics & Big Data Processing, General-Purpose Cloud Workloads), By Organization Size (Startups & AI-Native Companies, Mid-Market Enterprises, Large Enterprises, Research Institutions & Academia, Government & Defense), and By End-User Industry (BFSI, Healthcare & Life Sciences, Manufacturing, IT & Telecom, Media & Entertainment, Automotive, Energy & Utilities, Others) |

| Regional Coverage |

North America – US, Canada; Europe – Germany, UK, France, Russia, Spain, Italy, Benelux, Nordic, Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, Rest of MEA |