Market Overview

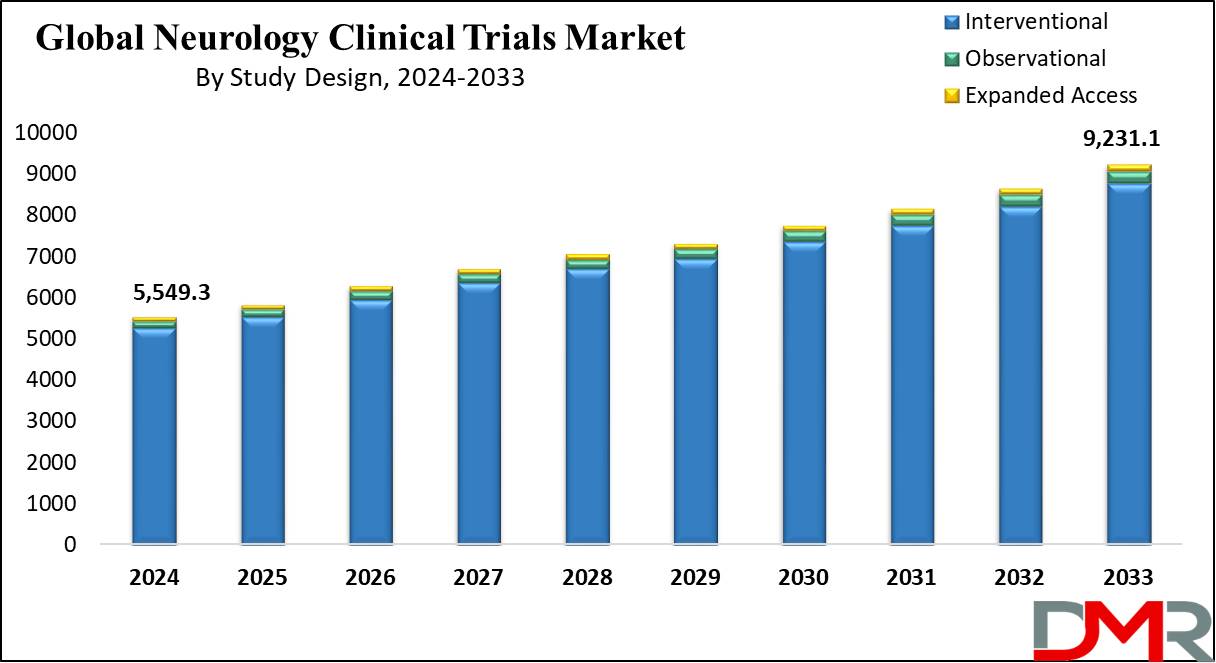

The Global Neurology Clinical Trials Market size is projected to be valued at USD 5,549.3 million in 2024 and is further expected to grow significantly during the forecast period (2024-2032) at a CAGR of 5.8% and reach USD 9,231.2 million by 2033. This growth trend reflects broader developments in neuroscience drug development and rising demand for advanced neurological treatment solutions.

The increasing burden of neurological disorders, including Alzheimer's disease, Parkinson's disease, and Huntington's disease, has driven the phenomenal growth of neurological clinical trials across the world. Increasing investments in neurological studies and trials from both private and public sectors contributed to further market growth. Growing demand for higher therapies and innovative neurological treatments is driving the expansion of clinical studies, further supporting the evolving neurological therapeutics market.

The emergence of Phase II clinical trials as the leading segment in the estimation period is mainly attributed to these trial phases being material in the testing of the efficacy and safety of new medications, particularly for complex diseases in the CNS. Furthermore, interventional study design has emerged as a dominant segment in the market, owing to an appreciable percentage of neurology clinical trials adopting this approach as one of the best methods for research studies on neurological patients to assess the therapeutic effects on them.

The CROs are valued in conducting these studies, therefore increasing trial efficiency and success rates. Other various technological changes, such as the integration of AI in neurology clinical trials, are viewed to further transform data collection and analysis processes, which would drive market share upwards. Considering the burden of neurological disorders said to increase worldwide, the neurology clinical trials market will still likely grow to reflect the increased need for breakthroughs and innovations regarding therapeutic interventions, especially as CNS clinical research expands across multiple regions.

The growing prevalence of neurological disorders worldwide has attracted significant investment from sponsors and stakeholders, leading to increased funding for neurological clinical trials. In March 2022, researchers from Brown University, New York University, and the University of Rochester received USD 16.0 million from the NIH to support Alzheimer’s disease research. Similar funding initiatives are anticipated to further boost market growth.

Additionally, the aging global population is a key factor contributing to the rising incidence of neurological diseases. According to the WHO, the population aged 60 and above reached 1.4 billion in 2020 and is projected to grow to 2.1 billion by 2050. Age-related neurological conditions, including Alzheimer’s disease, stroke, and Parkinson’s disease, are becoming increasingly prevalent. As of 2019, Alzheimer’s disease affected over 50 million people globally, while Parkinson’s disease impacted approximately 10 million individuals worldwide.

The US Neurology Clinical Trials Market

The

U.S. neurology clinical trials market is anticipated to reach a valuation of

USD 2,244.8 million in 2024, which is further poised to attain a valuation of

USD 3,618.9 million by the end of 2033. Thus, the US is amongst the top nations for neurology clinical trials, because the USA concentrates on neurological research and has a great many diseases, including Alzheimer ’s disease, Parkinson’s disease, and Huntington’s disease.

Contract research organizations for clinical trial outsourcing is the emerging market model in the United States, which has been developed to fast-track clinical trials. These Contract Research Organizations offer high incremental services of trial management like patient recruitment and data analysis which are spectacular in adding to the success of trials.

The integration of next-generation technologies in conducting a clinical trial in the U.S.

Artificial intelligence and machine learning-really changed the face of the conduct of such trials: improved data collection, patient characterization and control, and trial results.

A few Phase II disease control trials for testing treatments for neurological disorders also indicate the increasing importance of disease control trials in the U.S., which would probably be on the rise to meet the growing need for novel therapies or interventions in neurological disorders. The market growth in the U.S. is backed up by some government programs and increased funding of neurology clinical trials. Subsequently, raising the rate of neurological disorders further would ensure that the United States remains the leading country in the global neurology clinical trials market throughout the forecast timeframe.

Key Takeaways

- Global Market Value: The global neurology clinical trials market size is estimated to have a value of USD 5,549.3 million in 2024 and is expected to reach USD 9,231.1 million by the end of 2033.

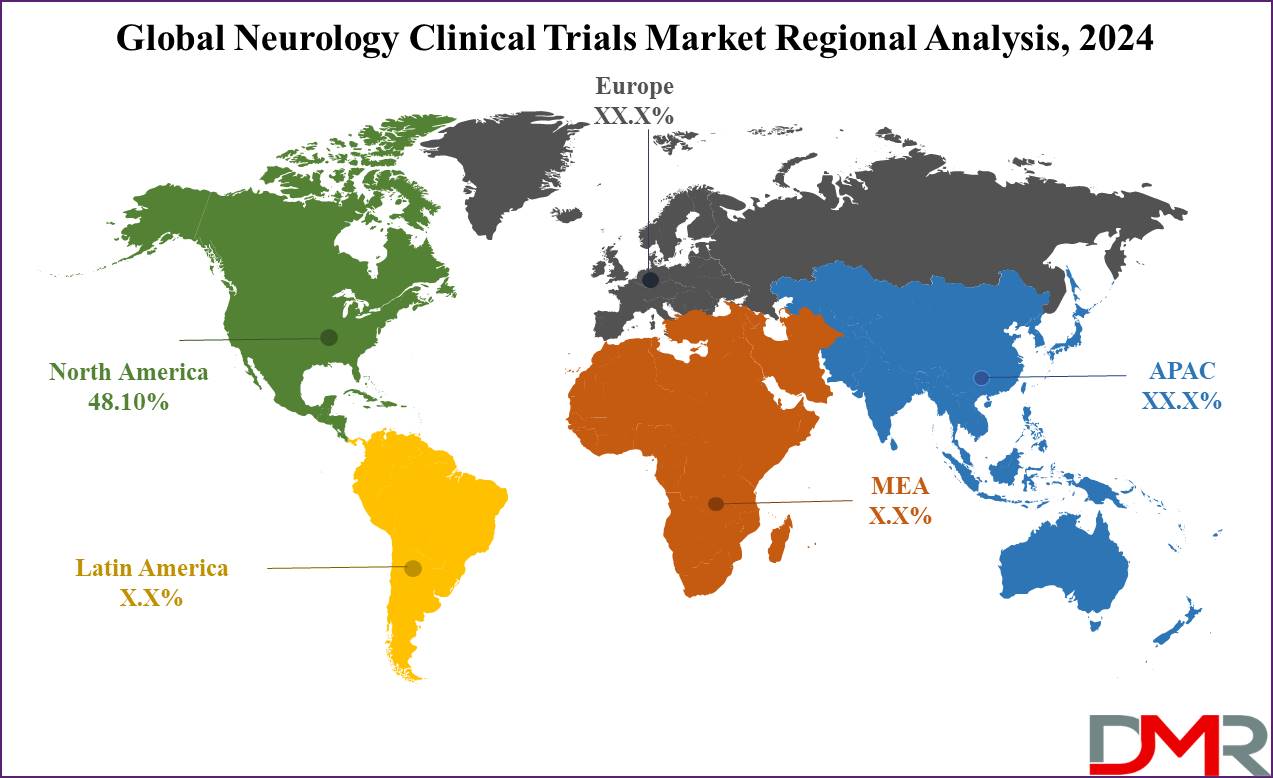

- Regional Analysis: North America is expected to be the largest market share for the global neurology clinical trials market with a share of about 48.10% in 2024.

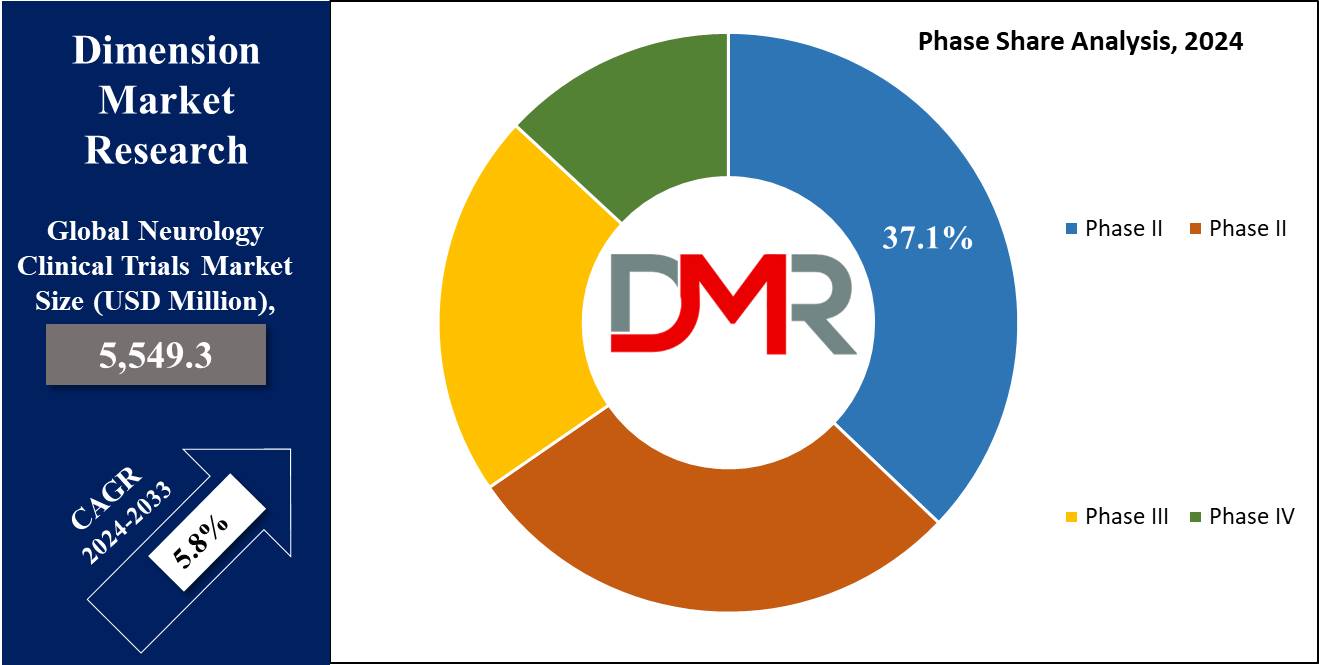

- By Phase Segment Analysis: Phase II clinical trials are expected to dominate the phase segment in this market as it holds 37.1% of market share in 2024.

- By Study Design Segment Analysis: The interventional study design are projected to dominate this market with 94.9% of market share in 2024.

- Key Players: Some of the major key players in the global neurology clinical trials market are Novartis, Covance, Med pace, Charles River Laboratories, and many others.

- Global Growth Rate: The market is growing at a CAGR of 5.8 percent over the forecasted period.

- The US Market Value: The US market size is estimated to have a value of USD 2,244.8 million in 2024 and is expected to reach USD 3,618.9 million by the end of 2033.

Use Cases

- Alzheimer’s Disease: Neurology clinical trials for new treatments seek to prevent further deterioration in cognitive function by attacking amyloid plaques or tau proteins.

- Parkinson’s Disease: Current clinical trials pursue gene therapies that decrease the generation of alpha-synuclein in order to slow the disease progression and enhance motor function.

- Huntington’s Disease: Therapies for relapsing-remitting multiple sclerosis involve the testing of new drugs that may lower the rate of relapses and slow down the disease’s course.

- Multiple Sclerosis (MS): In particular, investigations are made towards the gene-silencing therapies that help to reduce the levels of mutant protein that cause the disease progression in affected persons.

Market Dynamic

Trends

Rise in Neurological Diseases

Expansion of neurological disorders including Alzheimer’s disease, Parkinson’s disease, and Huntington’s disease has been primarily responsible for raising demand for neurology clinical trials. Since the global population is aging, the incidence of neurological disorders associated with aging is growing; therefore, it also boosts demand for treatments.

This good trend enhances the funding for clinical trials, especially those attached to Phase II and III which determine the responsiveness of treatments to various diseases as well as their safety.

Integration of Advanced Technologies

Advanced technologies, AI, and

machine learning combined with biomarkers are among the latest moves in neurological clinical trials, and they are the game-changers in the landscape. These technologies allow for more precise patient recruitment, enhance data analysis, and bring better trial outcomes by defining earlier signs of disease progression. Algorithms from AI and machine learning predict patient responses to treatments in the course of neurology clinical trials.

Growth Drivers

Increased Government Funding

Majorly, neurological research has been a major beneficiary of heavy funding by governments across the world. Indeed, neurology clinical trials have received huge funding. Consequently, large-scale investments are being made to accelerate the development of therapies for neurological diseases due to their emergence as one of the major burdens on public health.

The U.S. National Institutes of Health increased neurology research funding in particular for neurological alarm conditions such as Alzheimer's disease and Parkinson's disease to boost activity for trials.

Rising Investment by Pharmaceutical Companies

Pharmaceutical firms are investing significantly in new treatments for neurological disorders; therefore, propelling the market in neurology clinical trials. Because of the increasing frequency of these disorders and their high unmet medical needs for effective treatments, pharmaceutical businesses are increasing their clinical trials, this will include gene therapies or even biologics.

This appears even more obvious in the two main types of trials known as Phase II and Phase III trials whereby potential treatments are tried out to determine the extent of their efficiency.

Growth Opportunities

Emerging Markets

New opportunities in the geographical regions of Asia-Pacific and Latin America have a high potential to offer large growth opportunities in the neurology clinical trials market. Hence, geographically these regions are experiencing an increase in neurological diseases due to factors like an aging population and improved lifestyles thus offering a window of opportunity for new interventions.

Also, low operational costs and a large patient pool retain the importance of these regions in clinical trials and thereby offer vast opportunities for the expansion of pharmaceutical research facilities.

Precision Medicine in Neurology

The recent emerging concept of precision medicines has today merely started expanding new opportunities in neurology clinical trials. Precision medicine might choose to direct its attention toward a certain individual patient, about their DNA makeup, diet, and history of exposure to certain toxins. This, however, remains inapplicable in neurology because the genetic and environmental differences in neurologic diseases such as Alzheimer’s and Parkinson’s are different from those of simplex diseases. Customized management methodologies created during phase II and phase III of clinical trials.

Restraints

High Cost of Clinical Trials

Several factors have a deterring effect on the growth of the neurology clinical trials market. That includes long study duration, complex trial design, and usage of advanced technologies; all these raise the operational cost in neurology trials. Patient recruitment for a trial in neurology, especially for rare neurological conditions, is an expensive and time-consuming task, adding to hindrance in the growth of this market.

Stringent Regulatory Requirements

Stringent regulatory requirements of health authorities centering around the FDA and the EMA are in force in the neurology clinical trials market. These regulations have a contributory role in the assurance of the safety and efficacy of new treatments. However, they also have some impending consequences on the trial process.

The intricateness of neurological disorders further adds to the regulatory burden, and besides efficacy, clinical trials also need to establish long-term safety, especially in neurodegenerative conditions such as Alzheimer's and Parkinson's.

Research Scope and Analysis

By Phase

Phase II clinical trials are expected to dominate the phase segment in the neurology clinical trials market as it holds 37.1% of the market share in 2024. This is mainly because Phase II has a crucial function in the drug development and therapeutic assessment process. In the Phase II trials, researchers study the efficacy, dosage, and safety of new treatments for various neurological diseases including Alzheimer's disease, Parkinson's disease, and Huntington's disease.

These trials are designed to provide early insights into a drug's therapeutic potential, a factor considered crucial in trials involving the CNS since the patient population often presents difficult outcomes. One major reason Phase II clinical trials have dominated the landscape of clinical trials involves their bridging capability from very early, small-scale preclinical testing to larger Phase III studies.

All the same, the Phase II program identifies the best regimens that merit further development and testing in Phase III. This is a very important phase in protocol refinement, hence reducing the possibility of failure in succeeding phases.

Another reason contributing to the leading position of Phase II trials within the neurology clinical trials market pertains to the growing demand for personalized medicine in neurological diseases. Quite often, Phase II trials involve the approach in a more targeted manner, such as in the conditions of Huntington's disease and Multiple Sclerosis, whereby novel treatments are assessed regarding their ability to treat specific genetic or molecular pathways.

Further, accelerating growth of phase II clinical trials is made possible by the increase in R&D investments in neurological research and the development of CNS drugs, which continue to be indispensable parts of the neurological research clinical trial process.

By Study Design

The interventional study design is anticipated to dominate the neurology clinical trials market with 94.9% the of market share in 2024. The interventional study design, because it assesses the direct implications of therapeutic interventions on patient outcomes. Moreover, this interventional study will allow for the active manipulation of treatment variables and observing resultant effects on neurological conditions in the neurology clinical trials industry where precision in testing treatment efficacy is essential.

The main reason for such a predominance of interventional studies is that they provide more reliable and definitive data concerning treatment efficacy. While in observational studies, researchers only observe the outcomes, interventional trials are a real test of treatments that provide more complete answers to the question of how therapies can change disease progression in conditions like Multiple Sclerosis or Parkinson's disease. This is an approach that has become particularly important in neurological clinical trials, given the fact that treatments targeted at CNS disorders are quite complex.

Moreover, interventional studies bear importance in the processes of drug approval. For instance, regulatory agencies, such as the FDA, give maximum priority to interventional

clinical trials, mainly Phase II and Phase III trials, because these are specifically designed to meet the stringently set criteria for efficacy and safety. Hence, the outcomes from these very studies directly inspire the regulatory decisions, giving more importance to their status.

Last but not least, biomarkers and neuroimaging advanced technologies are being increasingly adopted in interventional studies, hence strengthening their capability to provide critical insights into neurological diseases, hence solidifying their leading position in the study design segment of the global neurology clinical trials market.

By Indication

Huntington's disease is the leading indication in the neurology clinical trials market, primarily owing to the fact of critical unmet medical needs associated with this inherited neurodegenerative disease. The strong demand may be attributed to the fact that the structure of the disease is complex and progressive; the need for clinical trials to identify therapies that are effective in slowing or halting the progress of the disease is immense.

It is the disease-modifying treatments that have sparked further research efforts, making Huntington's disease at the forefront of neurology clinical trials. The rise of gene therapies and other novel treatments geared at the root of genetic mutations behind the disease are among the major reasons for dominance in the clinically tried case of Huntington's disease.

More specifically, gene therapies aimed at lowering or disabling the expression of mutant protein, a core component in Huntington's disease pathogenesis, have emerged in Phase II clinical trials. These are very promising, with great potential to produce breakthrough treatments, and have resulted in an increased surge in trial activity for the condition.

Besides, Huntington's disease is much in the attention spotlight of the research community and pharmaceutical companies because it represents a genetic malady, which allows for early diagnosis and realization of some treatment strategies. Clinical trials for this indication often involve well-defined patient populations, making it easier to conduct both Phase II and Phase III trials. Growth in the neurology clinical trials market for Huntington's disease reflects the rising interest in addressing this devastating disorder that leaves unmet needs for the patients.

The Global Neurology Clinical Trials Market Report is segmented on the basis of the following

By Phase

- Phase I

- Phase II

- Phase III

- Phase IV

By Study Design

- Interventional

- Observational

- Expanded access

By Indication

- Epilepsy

- Parkinson’s Disease

- Huntington’s Disease

- Stroke

- Traumatic brain Injury (TBI)

- Amyotrophic Lateral Sclerosis (ALS)

- Muscle regeneration

- Other Indications

How Does Artificial Intelligence Contribute To Improve Neurology Clinical Trials Market ?

- Patient Recruitment & Enrollment – AI identifies suitable candidates by analyzing medical records, reducing recruitment time and improving trial efficiency.

- Predictive Analytics for Trial Success – AI forecasts trial outcomes based on historical data, helping researchers refine study designs.

- Automated Data Collection & Analysis – AI processes large datasets from brain scans, genetic profiles, and biomarkers to improve accuracy.

- Remote Monitoring & Wearable Integration – AI-powered devices track neurological symptoms in real time, reducing the need for frequent clinic visits.

- Enhanced Drug Discovery & Development – AI accelerates drug candidate selection by analyzing biological data and predicting effectiveness.

- Personalized Treatment Approaches – AI tailors treatments based on patient-specific data, improving trial outcomes and therapy efficacy.

- Risk Detection & Management – AI identifies potential safety concerns early, allowing for proactive intervention in trials.

- Automated Trial Documentation & Compliance – AI ensures regulatory compliance by streamlining data documentation and reducing human errors.

Regional Analysis

North America is projected to dominate the neurology clinical trials market as it will hold

48.10% of the market share in 2024. The pivotal factors that have made North America the leader in the neurology clinical trials market include high investment in neurological research and development by the public and private sectors. The U.S., particularly, has historically dominated the world in the field of clinical trials of neurological disorders, with many major research projects receiving huge funding from organizations like the National Institutes of Health.

These investments are targeted at therapies for diseases like Alzheimer's, Parkinson's, and Multiple Sclerosis, the most prevalent in the region. The presence within the region of a large number of major pharmaceutical companies and biotechnology firms fuels North America's dominance even more. Companies like Pfizer, Biogen, and Roche, along with CROs such as IQVIA and Parexel, are deeply into the development and testing of new therapies for neurological diseases. Particularly, these organizations have been conducting more than hundreds of Phase II and Phase III trials for complex disorders like amyotrophic lateral sclerosis and Huntington's disease.

Besides, North America is the unmistakable leader, due to a very robust regulatory environment, taken care of by agencies like the FDA. The FDA has set high standards for neurology clinical trials, ensuring the safety of the patients and the effectiveness of such treatments. Admittedly, this sets very tight regulations, but they instill confidence in clinical research and hence also attract local and international investment in the field.

Also, advanced health infrastructure in the region, along with higher penetration of the latest technologies, including artificial intelligence and biomarkers, facilitates the process of trials, which further cements the position of North America in the neurology clinical trials market.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

Neurology clinical trials is an immensely competitive market, wherein a few key players dominate the market and have been responsible for promoting innovation in neurological research. The major companies operating in this market are Pfizer Inc., Biogen Inc., Roche Holding AG, AstraZeneca plc, Novartis AG, and Eli Lilly and Company. These companies make heavy investments in the development of new therapies for neurological disorders targeting the diseases of Alzheimer's, Parkinson's, Huntington's, and Multiple Sclerosis.

With a strong pipeline targeting neurodegenerative disorders, Pfizer continues to lead the market, along with Biogen. Other than recent breakthroughs in amyloid-targeting therapies, Biogen has been at the forefront of neurology trials; as such, research up until now in Alzheimer's disease and MS places the company at the leading edge. Roche is making fairly serious strides in neurology clinical trials, most especially in Huntington's disease, where gene-silencing therapy is at Phase II trials and shows promise.

The outsourcing of neurology trials to contract research organizations, such as IQVIA and Parexel, is also being increasingly done, with trial management, patient recruitment, and the analysis of data being outsourced. The role of CROs in improving trial efficiency, especially for Phase II and Phase III trials, is very critical. The use of advanced technologies like AI and biomarkers by these companies will contribute to further optimizing the results of such trials and thus shorten the trial duration accordingly.

Some of the prominent players in the Global Neurology Clinical Trials Market are

Recent Development

- October 2024: Biogen announced promising Phase II results for its gene therapy targeting Huntington’s disease. The trial showed a significant reduction in mutant huntingtin protein levels, which is a key marker of disease progression.

- September 2024: Pfizer initiated a large-scale Phase III clinical trial focused on a new treatment for Alzheimer’s disease. The therapy targets amyloid plaques, which are believed to play a critical role in the progression of Alzheimer's.

- August 2024: Roche began patient enrollment for its Phase II trial of a gene-silencing therapy for Parkinson’s disease. The therapy aims to reduce the production of alpha-synuclein, a protein associated with Parkinson's progression.

- July 2024: IQVIA entered into a partnership with Novartis to launch an AI-powered platform designed to streamline neurology clinical trials. The platform focuses on improving patient recruitment, particularly for rare neurological diseases where finding eligible candidates can be challenging.

- June 2024: AstraZeneca completed its Phase II trial for a novel therapy targeting Multiple Sclerosis (MS). The therapy demonstrated a significant reduction in relapse rates among patients with relapsing-remitting MS, a form of the disease that causes recurring flare-ups.

- May 2024: Eli Lilly and Company received FDA approval to proceed with a Phase II clinical trial for its monoclonal antibody treatment targeting frontal temporal dementia (FTD), a lesser-known but highly debilitating neurological disease.

- April 2024: GlaxoSmithKline (GSK) announced the successful completion of a Phase I trial for a novel Parkinson’s disease treatment, which focuses on enhancing mitochondrial function to slow disease progression.

Report Details

|

Report Characteristics

|

| Market Size (2024) |

USD 5,549.3 Mn |

| Forecast Value (2033) |

USD 9,231.1 Mn |

| CAGR (2024-2033) |

5.8% |

| Historical Data |

2018 – 2023 |

| The US Market Size (2024) |

USD 2,244.8 Mn |

| Forecast Data |

2025 – 2033 |

| Base Year |

2023 |

| Estimate Year |

2024 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Phase (Phase I, Phase II, Phase III, and Phase IV), By Study Design (Interventional, Observational, and Expanded Access), By Indication (Epilepsy, Parkinson’s Disease, Huntington’s Disease, Stroke, Traumatic brain Injury (TBI), Amyotrophic Lateral Sclerosis (ALS), Muscle regeneration, Other Indications) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia- Pacific– China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Novartis, Covance, Med pace, Charles River Laboratories, Syneous Health, Icon Plc., GlaxoSmithKline, Aurora healthcare, Biogen, IQVIA, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

The Global Neurology Clinical Trials Market size is estimated to have a value of USD 5,549.3 million in 2024 and is expected to reach USD 9,231.1 million by the end of 2033.

North America is expected to be the largest market share for the Global Neurology Clinical Trials Market with a share of about 48.10% in 2024.

Some of the major key players in the Global Neurology Clinical Trials Market are Novartis, Covance, Med pace, Charles River Laboratories, and many others.

The market is growing at a CAGR of 5.8 percent over the forecasted period.

The US Market size is estimated to have a value of USD 2,244.8 million in 2024 and is expected to reach USD 3,618.9 million by the end of 2033.