What is the Global Neuromorphic Chip Market Size?

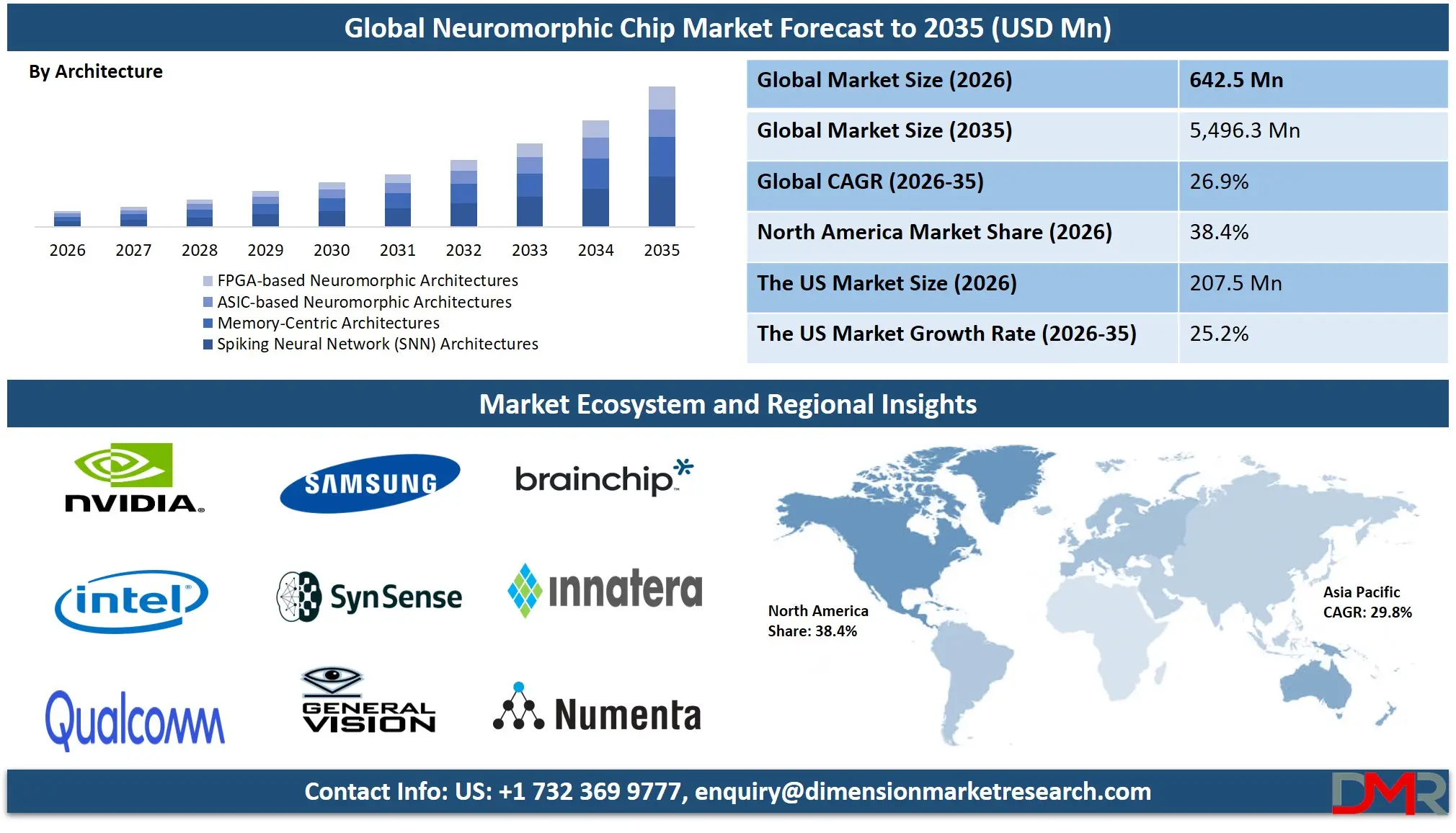

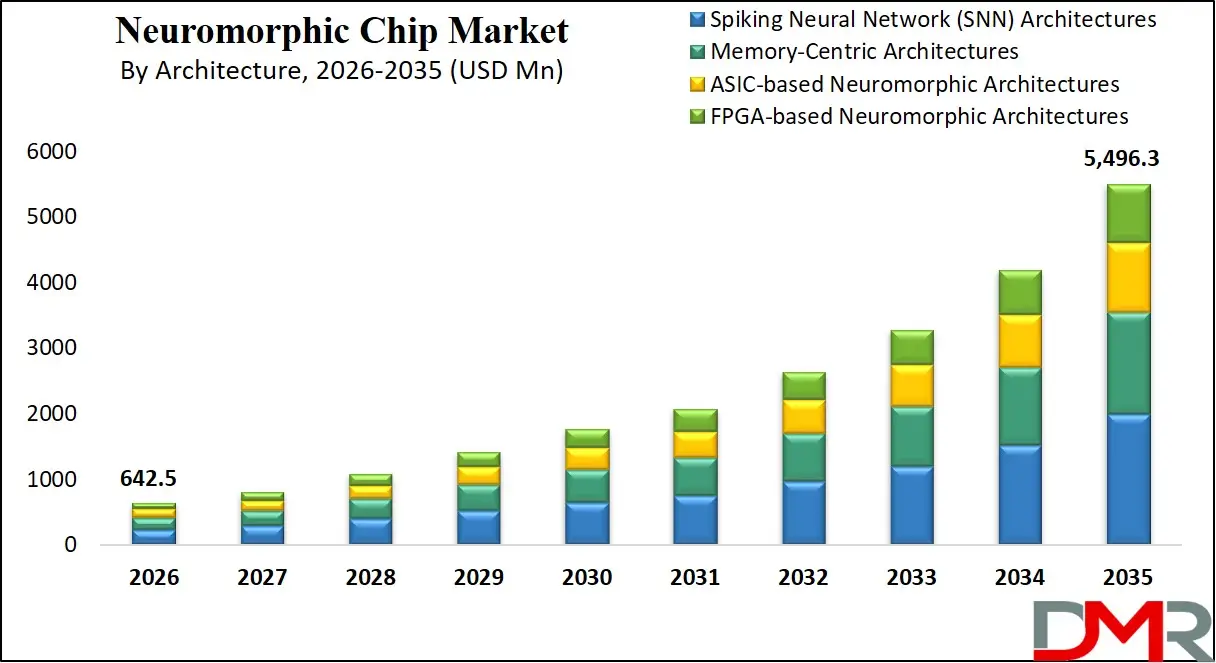

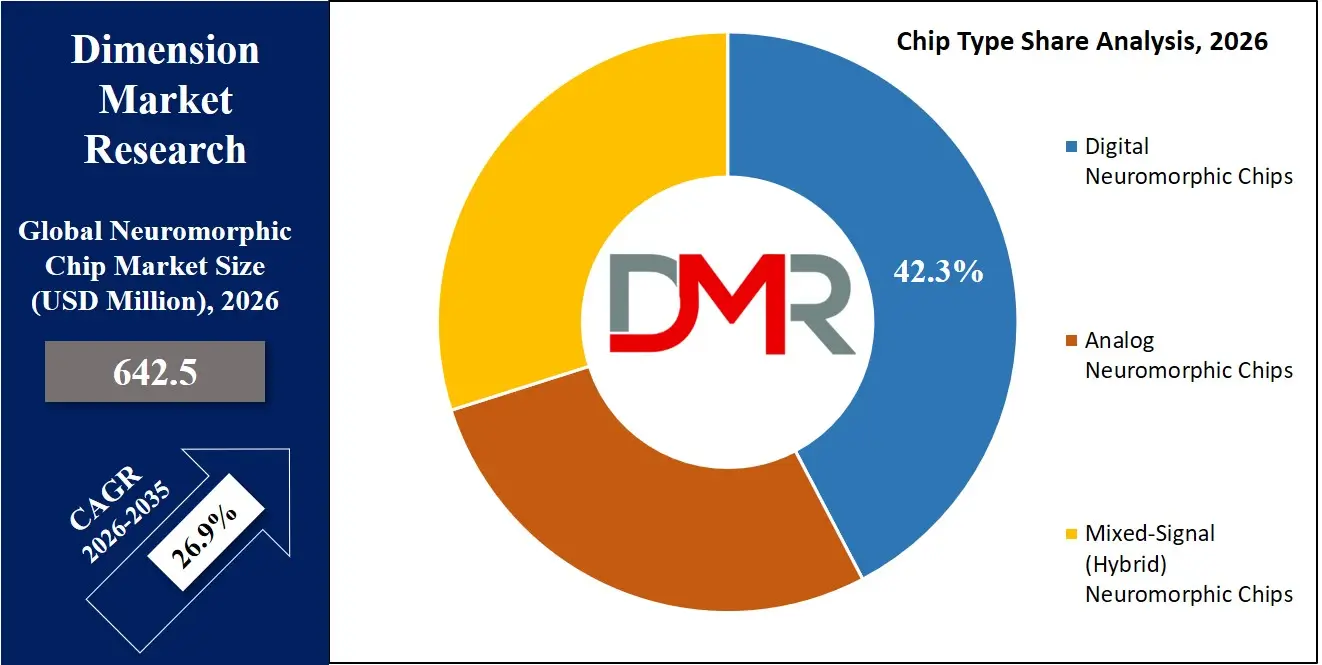

The Global Neuromorphic Chip Market size in 2026 is estimated at USD 642.5 million and grow at a compound annual growth rate (CAGR) of 26.9% to reach a value of USD 5,496.3 million by 2035, owing to the developments in brain-inspired computing, spike-based learning algorithms, event-driven processing, and ultra-low-power neural inference engines.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Neuromorphic Chip Market has been growing at an incremental rate, given the increasing utilization of spiking neural networks, national security mandates of autonomous AI at the edge, and the necessity to invest in both government and commercial capital of brain-like compute infrastructure in data centers and on edge devices worldwide. It also covers such new technologies as real-time event-based vision processing, asynchronous spike routing fabrics, and automated synaptic pruning used in neuromorphic deployment projects.

Modernization is a significant investment that cloud providers, AI startups, and defense contractors are pursuing to allow efficient memory-bandwidth decoupling, reduce the risk of compute underutilization, and increase model inference speed per watt. The move towards automation, predictive scaling of neuromorphic core utilization, and smart workload splitting (training on GPU + inference on neuromorphic) is increasing adoption. Moreover, the need to operationalize national AI strategies and the importance of sustainable brain-like compute are driving digital changes in AI infrastructure, and neuromorphic chips have become an essential part of the future intelligent economy on a global scale.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Neuromorphic Chip Market

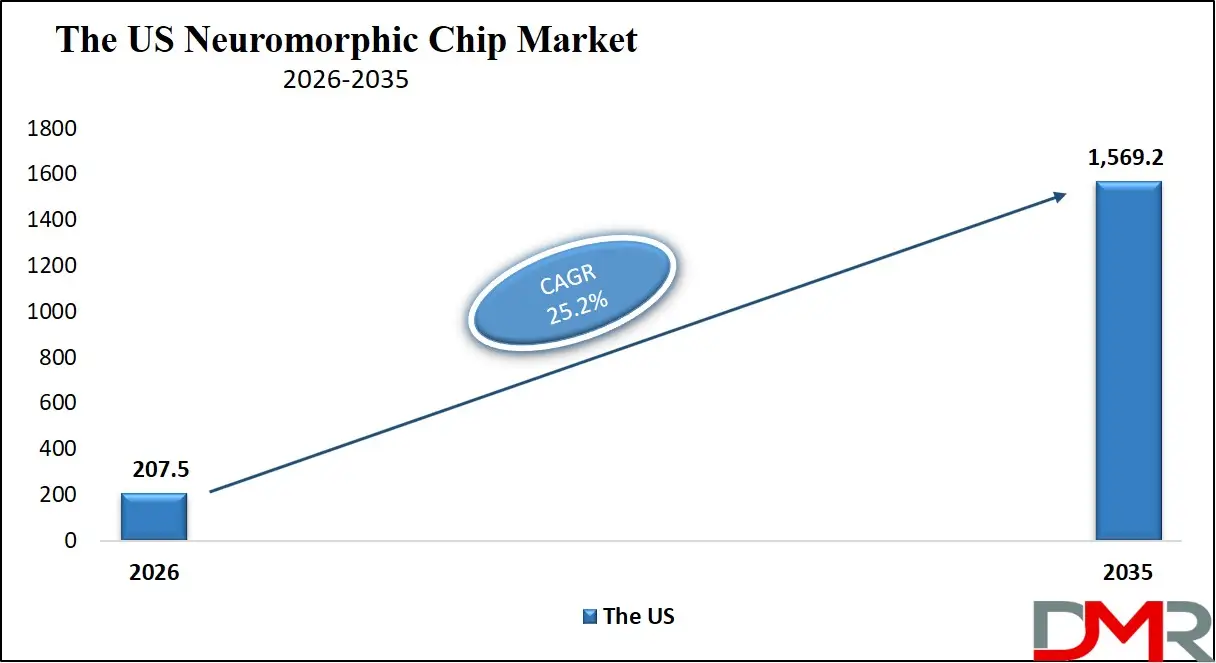

The US Neuromorphic Chip Market is estimated to grow to USD 207.5 million in 2026 with a compound annual growth rate of 25.2% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

In the US, the neuromorphic chip market is motivated by commercial cloud providers (e.g., AWS, Google, Microsoft), national security (e.g., AI-enabled surveillance systems, DARPA's SyNAPSE program), and the necessity of moving beyond general-purpose GPU reliance with more specialized, ultra-low-power solutions. Increasing investment is underway in autonomous event-based workload scheduling, predictive life models of synaptic core wear-out using telemetry, and real-time chip thermal monitoring for spike-timing anomalies. Federal funding programs, including the CHIPS Act and the National AI Initiative, encourage adoption. The edge computing and data center segments dominate, and digital engineering tools enhance the performance of neuromorphic design and simulation. Key players are focusing on chip reusability and supply chain partnerships to raise compute density and energy reliability. The regulatory frameworks that promote AI safety and verifiable model assurance also facilitate the adoption of digital chip health monitoring, and the need to have real-time spike data and automated failover response further determines the growth of markets.

Europe Neuromorphic Chip Market

The Europe Neuromorphic Chip Market is estimated to be valued at USD 134.9 million in 2026, witnessing growth at a CAGR of 26.1%, during the forecast period.

Europe has a mature neuromorphic chip market, and this has a significant influence on the regulatory requirements and regional policies such as the EU AI Act, the European Chips Act, and national sovereignty programs (e.g., France's neuromorphic research infrastructure and Germany's Human Brain Project spin-offs). Countries are also striving for smart neuromorphic modularization to harmonize commercial and institutional workload requirements and interoperability of the cross-border supply chain. Advanced manufacturing, like memristor-based 3D integration and silicon photonics for spike transmission, and high-reliability inference accelerators with in-built life-prediction algorithms, drives innovation. Public-private partnerships and harmonization of neuromorphic compute standards facilitate adoption. Technologies like real-time power capping and smart contract-based telemetry sharing are commonly practiced as research-centric programs, and Europe is a frontrunner in terms of the digital transformation of energy-efficient and specialized neuromorphic chips.

Japan Neuromorphic Chip Market

The Japan Neuromorphic Chip Market is projected to be valued at USD 51.4 million in 2026, progressing at a CAGR of 28.7%, during the period spanning from 2026 to 2035.

Japan boasts a mature neuromorphic chip market supported by high-performance processor design (Fujitsu's Digital Annealer), memory-logic integration technology, and a wide network of robotics AI innovations. Automation, precision, and mission integrity are the priorities in the country and are achieved by spike-based thermal wear prediction models and predictive power management systems for neuromorphic assets. Growth is stimulated by government actions under the AI Strategy 2025 and constant investment in edge AI infrastructure. The high volume of robotics systems, autonomous vehicles, and factory automation requires efficient neuromorphic chips for real-time event-based inference. The difficulties are high validation costs for new chip architectures and integration with legacy systems, yet the prospects are in exporting developed edge and cloud neuromorphic technologies to Asian and Pacific markets.

Key Takeaways

- Market Size & Forecast: The Global Neuromorphic Chip Market is estimated to be valued at USD 642.5 million in 2026 and is expected to grow to USD 5,496.3 million by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 26.9% in the forecast period.

- Primary Growth Drivers: Technological progress in spiking neural networks and event-driven edge inference, regulatory requirements for AI energy efficiency, and commercial data center deployment of brain-like computing are some of the key drivers of growth in the market.

- Key Market Trends: The use of event-based workload scheduling, real-time spike timing optimization, and transition to cloud-based neuromorphic telemetry and fleet management systems are some of the primary market trends.

- By Chip Type: The digital neuromorphic chips segment is anticipated to get the majority share of the Neuromorphic Chip market in 2026.

- By Architecture: The Spiking Neural Network (SNN) architectures segment is expected to get the largest revenue share in 2026 in the Neuromorphic Chip market.

- By Application: The image & video recognition segment is expected to get the largest revenue share in 2026 in the Neuromorphic Chip market.

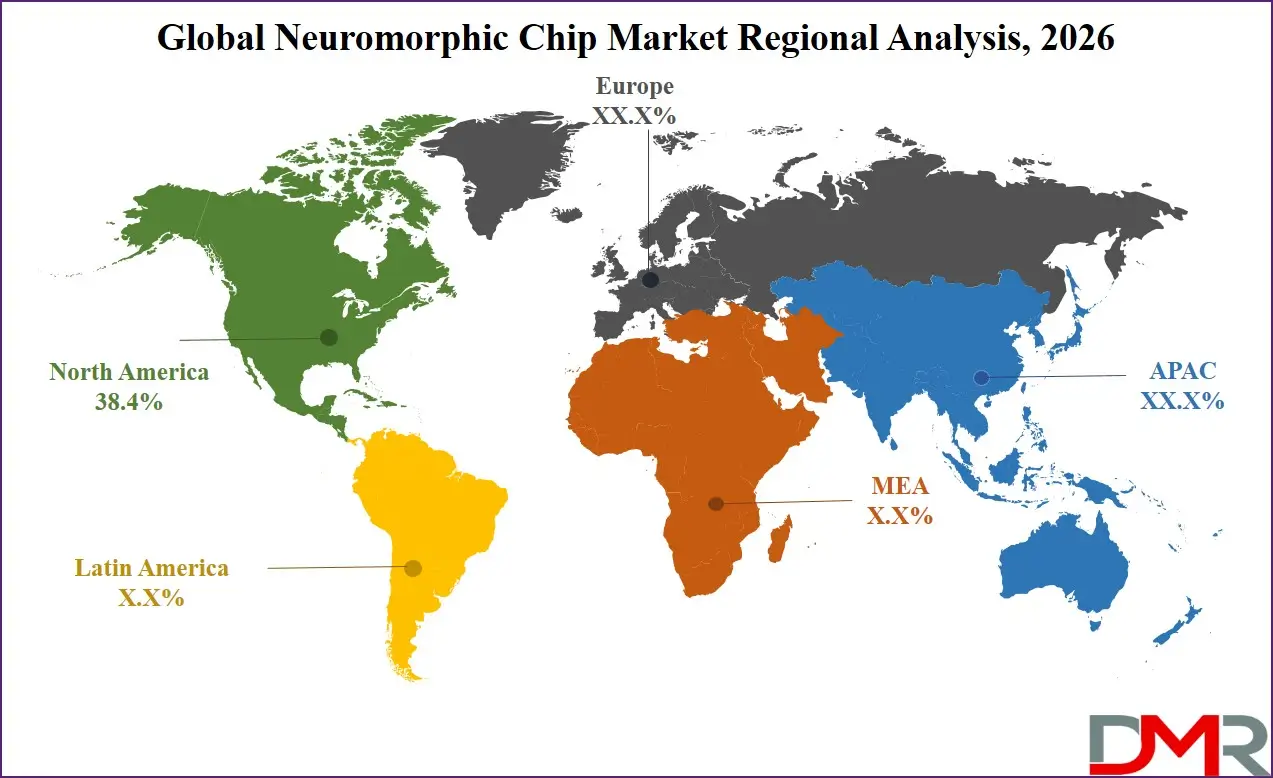

- Regional Leadership: North America is predicted to dominate the market with an estimated 38.4% share in 2026, with high defense AI spend and edge AI investment.

What is a Neuromorphic Chip?

A neuromorphic chip is a specialized processor that mimics the neuro-biological architecture of the human brain to accelerate artificial intelligence workloads including event-based vision, real-time sensory processing, continuous learning, and spiking neural network inference. It employs parallel event-driven compute architectures, synaptic arrays, and asynchronous spike routing to provide high throughput and extreme energy efficiency. The contemporary systems have real-time telemetry, memristor-based multi-die packaging, and AI-assisted power management to ensure transparency, efficiency, and reliability. These neuromorphic chips are capable of supporting efficient model deployment, sustainable brain-like compute operations, and help direct the funds of commercial and government and research stakeholders towards scalable, long-period AI infrastructure. They also facilitate accountability by making sure that accelerator performance data is quantified, tracked, and in line with global AI sustainability objectives.

Use Cases

- Event-Based Vision & Sensory Processing: Neuromorphic chips support real-time object detection, optical flow analysis, and audio event detection with microsecond latency, reducing power consumption by orders of magnitude compared to conventional GPUs.

- Thermal & Power Life Prediction Modeling (Reliability Risk): Mission information, including cumulative spike hours or synaptic cycling, is modeled to provide redundancy margins and continue operation without failure to maintain operational stability over the long term and investor trust.

- Continuous Learning Edge AI: Edge computing deployments are employing digital and mixed-signal neuromorphic accelerators to perform on-device adaptation, few-shot learning, and anomaly detection with quantifiable and proven energy efficiency.

- Autonomous Systems & Government Programs: More efficient edge neuromorphic chips contribute to the success of autonomous vehicles, defense drones, and smart sensors, facilitate national AI adoption, contribute to deployment reliability, and help implement policies, such as the AI compute governance policy and energy efficiency policy.

How AI Is Transforming the Global Neuromorphic Chip Market

Artificial intelligence is transforming neuromorphic chips by enabling predictive modeling of spike-timing behavior, automatic identification of anomalies in synaptic current data, and real-time optimization of voltage-frequency scaling per core. Telemetry and environmental data can be analysed with AI algorithms to determine any degradation or performance drift and scale-optimise mission results. This saves time, is verifiable and cheaper than manual data analysis.

Moreover, AI enhances mission assurance through offering adaptive event-based compute scheduling, anticipating thermal threats to synaptic arrays, and intelligent prioritization of neuromorphic core health monitoring. It is also involved in reducing the cost of baseline testing and ongoing performance tracking, allowing data center operators to reduce the cost and physical footprint of on-prem test campaigns and improve the reliability of neuromorphic workloads and their financial returns.

Market Dynamics

Key Drivers of the Global Neuromorphic Chip Market

Rapid developments in Spiking Neural Networks and Edge Inference

The market is being pushed by a fast uptake of event-driven AI, high-efficiency synaptic processing units, memristor-based packaging, and real-time telemetry analytics. These technologies will allow monitoring of the health of neuromorphic cores in real-time, identify performance anomalies early, predict end-of-life, and simplify the process of ground verification. Consequently, operational uptime and inference efficiency are highly enhanced as well as minimizing expenses of manual telemetry analysis. The growth of spiking neural network models like Loihi and Tianjic, in particular, is also accelerating the need for intelligent neuromorphic chips as edge operators are more inclined towards automation and workload optimization based on spike data.

Growing Focus on AI Regulation and Sustainable Compute

The world is becoming more and more involved in policies of AI energy efficiency, with governments and international bodies proposing compute efficiency policies, like the EU AI Act's sustainability provisions and the US Executive Order on AI. These structures are driving a high demand for efficient neuromorphic chips that can be used to perform ultra-low-power inference and continuous learning. In parallel, global initiatives such as the UN ITU AI for Good are encouraging the adoption of brain-inspired chip architectures. The increasing calls on transparency in AI compute usage and carbon footprint are also enhancing the necessity of verifiable and energy-efficient neuromorphic chips in both commercial and government edge data centers.

Restraints in the Global Neuromorphic Chip Market

High Costs of Design and Advanced Packaging

Neuromorphic chips are costly and time-consuming to develop, requiring extensive validation in thermal environments, testing of synaptic reliability, and long-term endurance analysis of emerging components. Additionally, regulatory restrictions and export controls on advanced semiconductor technologies further increase development complexity and cost. These factors create barriers for new entrants, extend deployment timelines, and increase upfront capital requirements.

Limited Standardization Across Neuromorphic Architectures

The industry continues to rely on multiple neuromorphic architectures, including digital, analog, mixed-signal, and emerging memristor-based systems. However, the lack of standardized software interfaces beyond platforms like Lava, Nengo, and PyNN remains a key challenge. Neuromorphic systems lack universal plug-and-play standards compared to traditional CPU or GPU ecosystems, making integration complex and limiting interoperability of spiking neural network models.

Growth Opportunities in the Global Neuromorphic Chip Market

Expansion of Emerging AI Programs

Developing AI markets such as Brazil, Indonesia, Nigeria, the UAE, and Vietnam are investing in AI infrastructure and advanced edge computing capabilities. These regions present strong growth potential due to increasing demand for energy-efficient automation, event-based vision, and sensory processing applications. With limited legacy infrastructure, they provide opportunities for deployment of modern neuromorphic technologies optimized for edge environments.

Rising Demand for Edge Neuromorphic Inference

The increased requirement of advanced neuromorphic chips is being generated by the growth of edge computing, autonomous systems, and real-time event-based AI applications. These technologies play a vital role in smart cameras, industrial robots, and autonomous vehicles. With the rising importance of sub-millisecond latency as a major industry concern, edge neuromorphic inference capabilities are likely to be fundamental to future AI infrastructure.

Global Neuromorphic Chip Market Trends

Event-Driven Workload Monitoring and Predictive Analytics

Neuromorphic chips are being monitored and spike-timing anomalies detected in real time and synaptic component wear predicted using on-chip learning. The use of digital twin models and machine learning algorithms is enhancing compute scheduling, system lifespan, and deployment reliability. This shift is transforming neuromorphic management from manual telemetry review to fully automated, continuously optimized system monitoring.

Cloud-Based Telemetry and Fleet Management Systems

Cloud computing and digital twin technologies are taking the centre stage in the operations of neuromorphic clusters. These platforms enable real-time storage and analysis of spike performance data, centralized fleet management, as well as remote monitoring of neuromorphic chip health. Cloud-based systems enhance transparency, lower on-prem infrastructure expenses, and quicker responses to workload changes across edge nodes, as experienced by operators of large neuromorphic fleets.

Research Scope and Analysis

By Chip Type Analysis

The digital neuromorphic chips segment is expected to remain the largest in 2026, accounting for about 42.3% of the global neuromorphic chip market, driven by its dominant use in large-scale SNN deployment, high-precision spike computation, and flexibility across diverse event-driven frameworks where deterministic timing and software ecosystem maturity are essential.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Meanwhile, the mixed-signal (hybrid) neuromorphic chips segment is witnessing strong growth, driven by rising demand for ultra-power-efficient inference in edge devices, sensor fusion, and custom workloads where analog efficiency and digital programmability are critical. Adoption is further supported by AI-based power capping, real-time efficiency diagnostics, and modular chiplet configurations that integrate multiple neuromorphic core types for improved workload flexibility and endurance.

By Architecture Analysis

The Spiking Neural Network (SNN) architectures segment is expected to dominate with approximately 52.7% market share in the year 2026, owing to its critical role in hosting event-driven computation, low-latency inference, and brain-like learning operations. Commercial and government buyers are shifting to higher-performance SNN designs in order to have greater throughput-per-watt and improve energy efficiency. SNN solutions are adaptable, making it easy to deploy and integrate with event-based sensors. ASIC-based neuromorphic architectures can still be used, though, in places where deterministic spike routing is required (e.g., aerospace, defense). The multi-architecture usage with SNN and memory-centric accelerators simultaneously has the quickest development, and the neuromorphic portfolios are more flexible to different latency classes and workload contexts.

By Deployment Mode Analysis

The edge deployment segment is expected to dominate with approximately 68.4% market share in 2026, driven by the critical need for ultra-low-latency, power-constrained inference in autonomous vehicles, industrial IoT, and defense drones. Neuromorphic chips excel at edge scenarios due to their event-driven nature, consuming microwatts of power while delivering millisecond response times. The cloud/data center deployment segment, while smaller, is witnessing steady growth, driven by large-scale SNN simulation, neuroscience research, and training of complex spiking models where high-density compute clusters are required. The fusion of edge and cloud deployment models, with federated learning across neuromorphic nodes, has the fastest development.

By Core Technology Analysis

The CMOS-based neuromorphic chips segment is expected to hold the largest share in 2026, accounting for approximately 61.3% of the market, driven by manufacturing maturity, high yield, and seamless integration with existing semiconductor supply chains. Meanwhile, the memristor-based neuromorphic chips segment is witnessing the fastest growth, driven by the ability to emulate synaptic plasticity (STDP) directly in hardware, enabling true in-memory computing and extreme density. The quantum-inspired neuromorphic chips segment, while nascent, is emerging in specialized defense and scientific computing applications with significant long-term potential.

By Component Analysis

The processors (NPUs, SNN chips) segment is expected to dominate in 2026, accounting for approximately 55.6% share, driven by the central role of spiking processing cores in executing event-based neural computations. The memory units (SRAM, DRAM, memristors) segment forms the second-largest category, as neuromorphic architectures heavily rely on co-located memory and compute. The interconnects & communication interfaces segment is growing rapidly, driven by the need for high-bandwidth, low-latency spike exchange across chips. The software & development tools segment, while smaller in revenue, is critical for ecosystem growth, including SNN simulators and event-based data processing pipelines.

By Application Analysis

The image & video recognition segment is predicted to have the highest share of around 32.5% in 2026, hosting mixed-signal and digital neuromorphic chips for real-time event-based vision, object tracking, and anomaly detection. The robotics & autonomous systems segment enables low-latency navigation and path planning. The signal processing segment is witnessing strong growth for radar, LiDAR, and audio event detection. The fastest growing area is natural language processing for always-on voice wake-up and keyword spotting. The fusion of neuromorphic function integration and workload scheduling is generating smarter AI infrastructure markets.

By End-User Industry Analysis

The IT & Telecom segment represents the largest industry vertical in 2026, accounting for approximately 26.8% share, driven by edge computing deployments and 5G/6G network optimization. Consumer Electronics forms the second-largest segment, utilizing neuromorphic chips for smartphones, smart speakers, and wearables, where ultra-low power is critical. The Automotive & Transportation sector is a key high-growth segment for ADAS and autonomous driving. The fastest-growing area is Aerospace & Defense for surveillance drones, electronic warfare, and satellite-based Earth observation. Healthcare and Industrial & Manufacturing are emerging for patient monitoring and predictive maintenance.

The Global Neuromorphic Chip Market Report is segmented based on the following:

By Chip Type

- Digital Neuromorphic Chips

- Analog Neuromorphic Chips

- Mixed-Signal (Hybrid) Neuromorphic Chips

By Architecture

- Spiking Neural Network (SNN) Architectures

- Memory-Centric Architectures

- ASIC-based Neuromorphic Architectures

- FPGA-based Neuromorphic Architectures

By Deployment Mode

- Edge Deployment

- Cloud / Data Center Deployment

By Core Technology

- CMOS-based Neuromorphic Chips

- Memristor-based Neuromorphic Chips

- Quantum-inspired Neuromorphic Chips

By Component

- Processors (NPUs, SNN Chips)

- Memory Units (SRAM, DRAM, Memristors)

- Interconnects & Communication Interfaces

- Software & Development Tools

- Others

By Application

- Image & Video Recognition

- Signal Processing

- Data Mining & Pattern Recognition

- Robotics & Autonomous Systems

- Natural Language Processing

- Others

By End-User Industry

- Consumer Electronics

- Automotive & Transportation

- Healthcare & Medical Devices

- Aerospace & Defense

- Industrial & Manufacturing

- IT & Telecommunications

- Others

Regional Analysis

Leading Region in the Neuromorphic Chip Market

It is projected that North America will take the lead in the global neuromorphic chip market (by value), covering a market share of about 38.4% in the year 2026. The region's dominance is driven by strong defense AI workload cadence (US-based DARPA programs), high neuromorphic chip prices relative to other regions, a mature supply chain for advanced memristor-based packaging and high-bandwidth memory, and the presence of key chip designers and research labs. The widespread adoption of advanced digital and mixed-signal neuromorphic chips for event-based vision, defense AI missions, and government AI programs further strengthens North America's leading position in the market. Additionally, continuous investments in AI-enabled chip health monitoring and memristor manufacturing capabilities are further reinforcing regional technological leadership.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Region in the Neuromorphic Chip Market

Asia-Pacific is the fastest-growing region, supported by strong AI deployment targets (China, India, Japan), increasing semiconductor sovereignty initiatives, rising investments in domestic neuromorphic capabilities, and growing adoption of edge inference systems. The region benefits from well-established manufacturing capacity, increasing commercial participation, and alignment with national AI roadmaps. Countries across the region are actively deploying neuromorphic chips to enhance inference efficiency-per-watt and strengthen digital infrastructure. Growing emphasis on neuromorphic R&D and structured chip development further accelerates market expansion in the region. Moreover, increasing government support and commercial AI commitments are expected to sustain high growth momentum.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The neuromorphic chip market is very competitive, with innovation and strategic alliances being the order of the day. In order to achieve a competitive advantage, companies and research labs are oriented towards the creation of new advanced chip architectures (e.g., memristor-based, quantum-inspired, event-driven), AI-powered chip telemetry, and digital twin-enabled health monitoring platforms. There are high barriers to entry because of capital-intensive fabrication infrastructure, technical neuromorphic design know-how, and the need for software ecosystem maturity and supply chain certifications.

Strategic approaches in the market to increase market presence include partnerships with edge device manufacturers, mergers between chip designers and system integrators, and long-term neuromorphic supply contracts with defense and robotics operators. Moreover, research and development in advanced memristor packaging and event-based software frameworks are important factors in staying competitive and meeting the changing needs of the AI industry.

Some of the prominent players in the Global Neuromorphic Chip Market are:

- Intel Corporation

- International Business Machines Corporation (IBM)

- Samsung Electronics Co., Ltd.

- Qualcomm Incorporated

- BrainChip Holdings Ltd.

- SynSense AG

- Innatera Nanosystems B.V.

- Prophesee S.A.

- GrAI Matter Labs SAS

- General Vision, Inc.

- Applied Brain Research, Inc.

- Knowm Inc.

- Numenta, Inc.

- SK hynix Inc.

- Micron Technology, Inc.

- NXP Semiconductors N.V.

- Analog Devices, Inc.

- Sony Group Corporation

- HRL Laboratories, LLC

- CEA-Leti

- Other Key Players

Recent Developments

- April 2026: Intel Corporation continued expansion of its neuromorphic ecosystem with the Hala Point system, capable of simulating over 1 million neurons, supporting applications in robotics and adaptive AI systems.

- March 2026: Innatera Nanosystems B.V. partnered with Synopsys to adopt advanced simulation technologies for scaling its brain-inspired Pulsar processors, accelerating development of ultra-low-power neuromorphic chips for wearables and IoT devices.

- January 2026: BrainChip Holdings Ltd., SynSense AG, and GrAI Matter Labs SAS advanced toward commercial production, marking a transition of neuromorphic computing from research prototypes to revenue-generating deployments.

- January 2026: SK hynix Inc. and Micron Technology, Inc. expanded development of advanced memory architectures to support neuromorphic workloads, particularly for edge AI and autonomous systems.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 642.5 Mn |

| Forecast Value (2035) |

USD 5,496.3 Mn |

| CAGR (2026–2035) |

26.9% |

| The US Market Size (2026) |

USD 207.5 Mn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Chip Type (Digital Neuromorphic Chips, Analog Neuromorphic Chips, Mixed-Signal Neuromorphic Chips), By Architecture (Spiking Neural Network Architectures, Memory-Centric Architectures, ASIC-based Neuromorphic Architectures, FPGA-based Neuromorphic Architectures), By Deployment Mode (Edge Deployment, Cloud/Data Center Deployment), By Core Technology (CMOS-based Neuromorphic Chips, Memristor-based Neuromorphic Chips, Quantum-inspired Neuromorphic Chips), By Component (Processors, Memory Units, Interconnects & Communication Interfaces, Software & Development Tools, Others), By Application (Image & Video Recognition, Signal Processing, Data Mining & Pattern Recognition, Robotics & Autonomous Systems, Natural Language Processing, Others), By End-User Industry (Consumer Electronics, Automotive & Transportation, Healthcare & Medical Devices, Aerospace & Defense, Industrial & Manufacturing, IT & Telecommunications, Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Neuromorphic Chip Market?

▾ The Global Neuromorphic Chip Market size is estimated to have a value of USD 642.5 million in 2026 and is expected to reach USD 5,496.3 million by the end of 2035.

What is the CAGR of the Global Neuromorphic Chip Market from 2026 to 2035?

▾ The market is growing at a CAGR of 26.9% over the forecasted period.

What factors are driving the growth of the Global Neuromorphic Chip Market?

▾ Technological advancements in spiking neural networks and event-driven edge inference, regulatory mandates for AI energy efficiency, and government funding for national brain-like compute infrastructure are the factors driving the growth of the neuromorphic chip market, globally.

What are the major trends in the Global Neuromorphic Chip Market?

▾ Adoption of event-driven workload scheduling and real-time spike-timing monitoring, and a shift toward cloud-based neuromorphic telemetry and fleet management platforms are the major trends in the market.

Which region held the largest share of the Global Neuromorphic Chip Market in 2026?

▾ North America is expected to account for the largest market share in 2026, with a share of about 38.4%.

Which region is expected to grow the fastest in the Global Neuromorphic Chip Market?

▾ Asia Pacific is the fastest-growing region in the market during the forecast period.

Who are the key players in the Global Neuromorphic Chip Market?

▾ Some of the major key players in the Global Neuromorphic Chip Market are Intel Corporation, IBM Corporation, BrainChip Holdings Ltd., SynSense AG, GrAI Matter Labs, Innatera B.V., and many others.

How is the Global Neuromorphic Chip Market segmented?

▾ The market is segmented by chip type, architecture, deployment mode, core technology, component, application, and end-user industry.