What is the Third-Party Food Chemistry Labs Market Size?

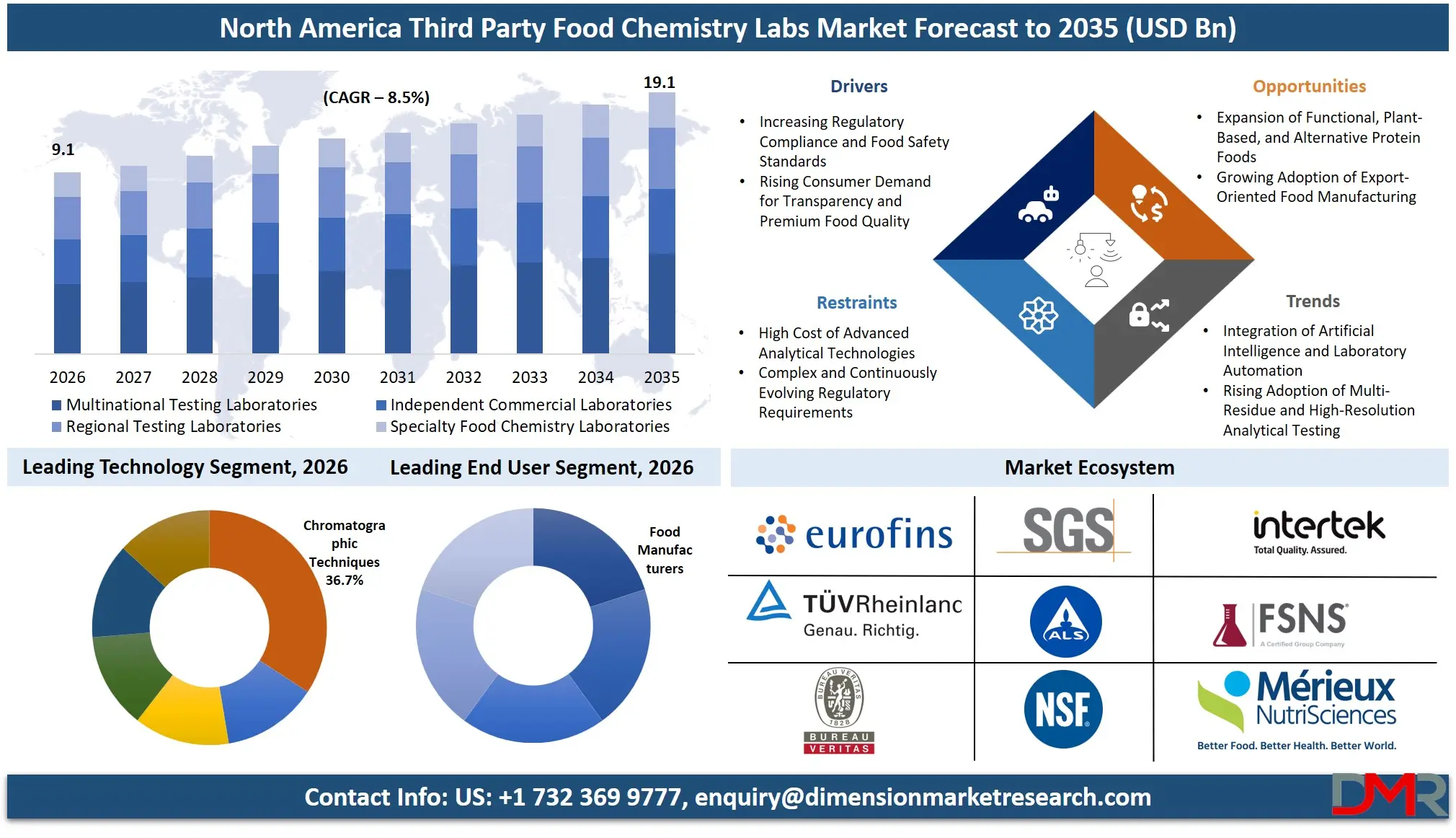

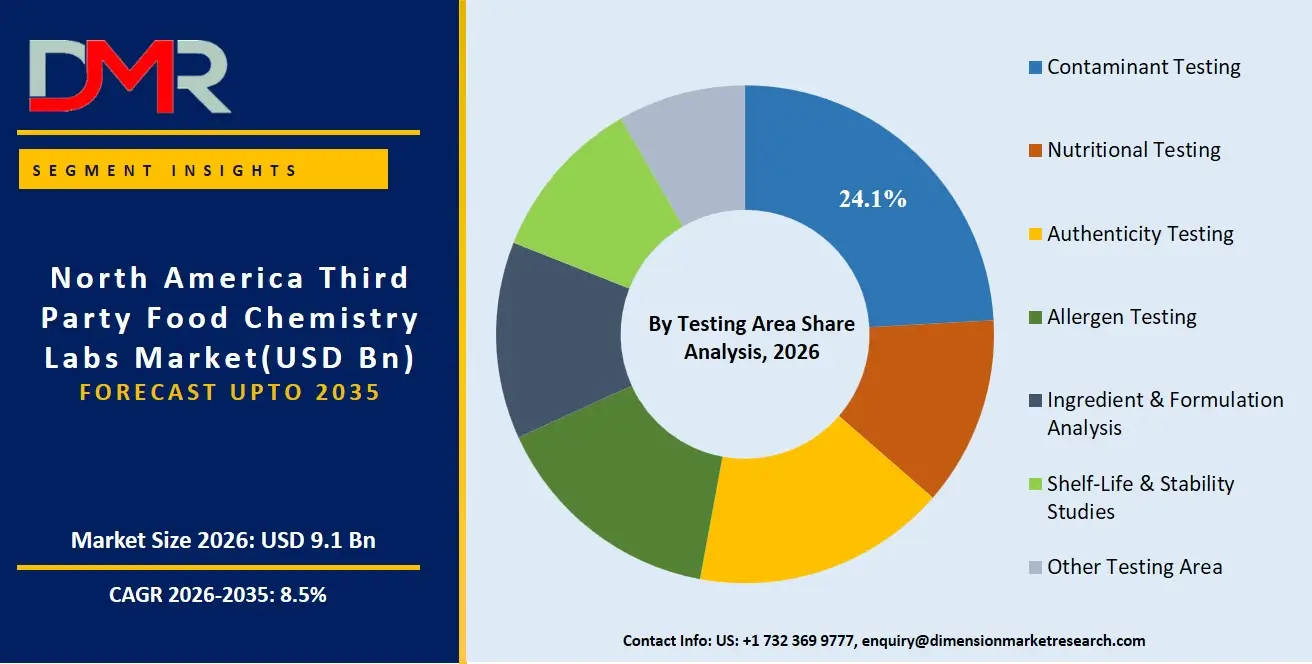

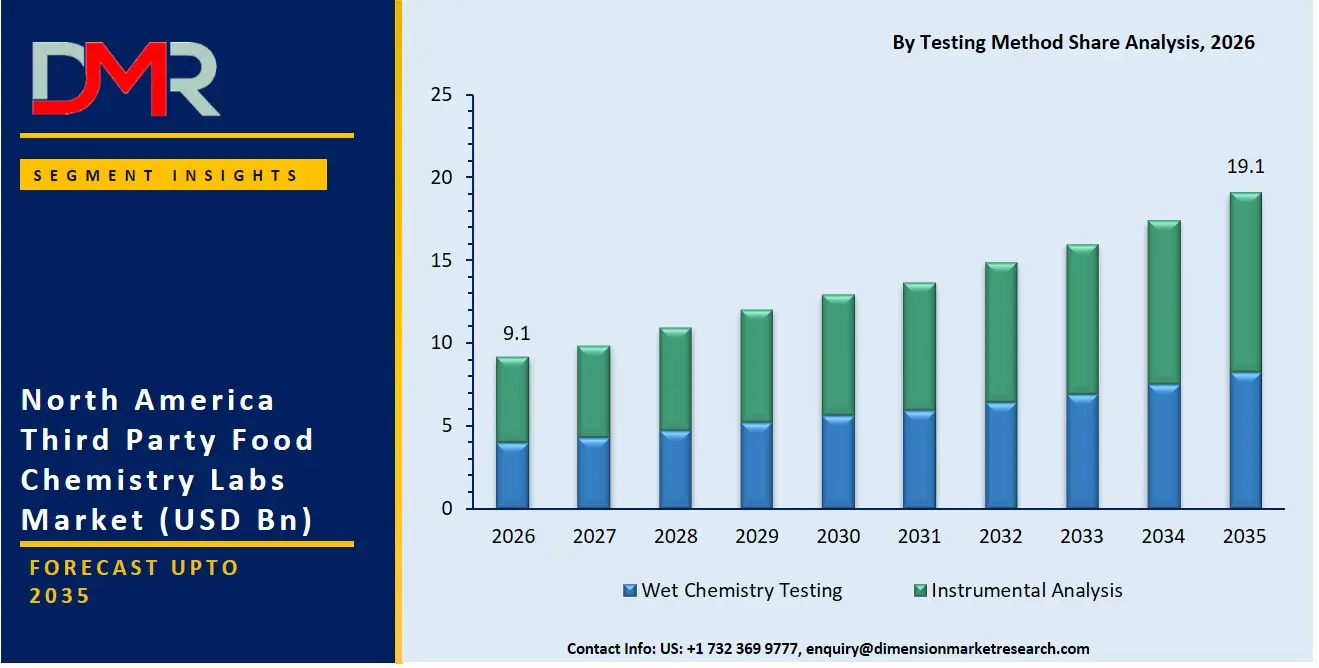

The North America Third Party Food Chemistry Labs Market is expected to reach a value of USD 9.1 billion in 2026, and it is further anticipated to reach USD 19.1 billion by 2035, growing at a CAGR of 8.5% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The third-party food chemistry testing market in North America has experienced robust growth, driven by an increasingly complex food supply chain and a heightened consumer focus on safety and transparency. This market consists of independent laboratories that provide essential analytical services, from contaminant detection to nutritional verification, for a wide array of food products. The escalating demand for comprehensive testing to meet stringent regulatory standards like the FDA's Food Safety Modernization Act (FSMA), coupled with the rise in food fraud and adulteration incidents, has made third-party validation a critical component of the food industry. Laboratories equipped with advanced chromatographic and spectroscopic instrumentation are the major service providers in this sector, offering the specialized expertise that many food manufacturers and retailers lack in-house.

Key Takeaways

- Market Size & Forecast: Based on forecasts, the North American market for third-party food chemistry labs is poised to attain a value of USD 9.1 billion by 2026, expanding substantially to USD 19.1 billion by 2035, fueled by the mandatory shift toward preventative safety controls and the growing "clean label" consumer movement.

- Growth Rate & Outlook: The market is projected to register a CAGR of 8.5%, attributed to key growth factors such as the increasing incidence of foodborne illnesses and recalls, the complexity of global food supply chains, and the rapid innovation in plant-based and functional food categories requiring novel analytical methods.

- Primary Growth Drivers: Crucial growth drivers include the stringent implementation of FSMA rules around preventive controls and foreign supplier verification, soaring consumer demand for verified non-GMO and organic claims, and the biotechnology boom in alternative proteins necessitating precise ingredient and formulation analysis.

- Key Market Trends: Major trends are centered on the adoption of AI-enabled data analysis for rapid contaminant screening, the shift toward automated laboratory platforms to handle high sample volumes, and a surge in demand for authenticity testing to combat sophisticated food fraud in high-value products like oils, honey, and dietary supplements.

- By Testing Area Analysis: The contaminant testing segment dominates the North American market, driven by mandatory regulatory monitoring for heavy metals, pesticide residues, and mycotoxins. Allergen testing is a rapidly growing sub-segment, spurred by the prevalence of undeclared allergens as a leading cause of food recalls.

- By Technology Analysis: The market for instrumental analysis is projected to be led by chromatographic techniques like HPLC/UHPLC and GC, which form the gold standard for quantifying pesticide residues, veterinary drugs, and fatty acid profiles. Spectroscopic methods like ICP-MS are experiencing rapid growth for ultra-trace heavy metals analysis.

What is the Third-Party Food Chemistry Labs?

Third-party food chemistry testing refers to the independent analysis of food products and ingredients by an ISO/IEC 17025-accredited laboratory that has no direct affiliation with the manufacturer, retailer, or supplier. This independent oversight provides an objective, legally defensible assessment of a product's safety, quality, and authenticity. The process involves advanced analytical chemistry techniques, from mass spectrometry for detecting low-level contaminants to molecular testing for species identification. Unlike internal quality control, third-party labs offer specialized expertise, high-throughput automated platforms, and a scientific seal of approval that is vital for regulatory clearance, export certification, and building consumer trust in a brand's label claims, especially in the context of complex global supply chains.

Use Cases

- Allergen Cross-Contamination Verification: A baked goods manufacturer employs a third-party lab to perform ELISA-based allergen testing on in-process samples after a production line changeover, ensuring that a "gluten-free" product is free from gluten cross-contamination below the 20 ppm regulatory threshold before it reaches the retail shelf.

- Authenticity Testing of Imported Oils: An olive oil importer partners with a specialty laboratory that uses NMR and GC-FID spectrometry to verify geographic origin and detect economic adulteration with cheaper vegetable oils, a critical step for product classification and avoiding tariff violations upon U.S. entry.

- Shelf-Life Validation for Plant-Based Meats: A food technology startup launching a new refrigerated plant-based burger utilizes a contract research organization (CRO) lab to conduct accelerated and real-time shelf-life studies, analyzing lipid oxidation and moisture migration to scientifically establish a safe and optimal "best by" date.

- Regulatory Compliance for Exporters: A seafood exporter from Canada to the U.S. sends finished product samples to a multinational testing lab for heavy metals and veterinary drug residue testing, generating the certificate of analysis required by FDA's foreign supplier verification programs for seamless customs clearance.

How AI is Transforming the Third Party Food Chemistry Labs Market?

The impact of AI on the North American food chemistry testing market is revolutionizing operational speed, data integrity, and predictive capabilities. AI-enabled data analysis tools are processing the vast amounts of complex data generated by modern instruments like time-of-flight mass spectrometers and orbitrap analyzers, exponentially accelerating the identification of unknown contaminants and adulterants beyond the scope of traditional targeted methods.

Furthermore, AI is pivotal in optimizing laboratory efficiency and sample triage. Machine learning algorithms on automated laboratory platforms flag anomalous chromatographic peaks for chemist review, drastically reducing manual data interrogation time. Beyond the lab bench, AI-driven predictive analytics are being used to forecast supply chain risks, modeling historical testing data with environmental factors to predict future aflatoxin contamination hotspots in grain crops, allowing food manufacturers to make smarter, proactive sourcing and testing decisions.

Market Dynamics

Key Drivers in the North America Third Party Food Chemistry Labs Market

Increasing Regulatory Compliance and Food Safety Standards

Stringent food safety regulations across North America continue to drive demand for third-party food chemistry laboratories. Agencies such as the U.S. FDA, USDA, Health Canada, and CFIA require manufacturers to comply with rigorous standards governing contaminants, additives, nutritional labeling, allergens, and chemical residues. Food companies increasingly rely on independent laboratories to ensure objective testing, regulatory compliance, and product certification before commercialization. Growing cross-border food trade further necessitates internationally recognized testing services that comply with multiple regulatory frameworks. Third-party laboratories also assist manufacturers during inspections, audits, recalls, and certification processes, making outsourced chemistry testing an indispensable component of modern food quality assurance systems throughout the region.

Rising Consumer Demand for Transparency and Premium Food Quality

North American consumers increasingly expect detailed nutritional information, ingredient transparency, clean-label products, and verified claims regarding organic, non-GMO, and sustainable food production. Food manufacturers therefore require advanced chemical analysis to validate product composition, detect adulteration, confirm authenticity, and substantiate marketing claims. Third-party laboratories provide unbiased verification that enhances consumer confidence while protecting brand reputation. Growing demand for premium functional foods, plant-based products, infant nutrition, dietary supplements, and specialty beverages further increases testing complexity. Independent laboratories equipped with sophisticated analytical technologies help manufacturers meet evolving consumer expectations, maintain product consistency, and reduce the risk of misleading labeling or regulatory penalties.

Restraints in the North America Third Party Food Chemistry Labs Market

High Cost of Advanced Analytical Technologies

Establishing and operating modern food chemistry laboratories requires significant capital investment in sophisticated analytical instruments such as LC-MS/MS, GC-MS, ICP-MS, HPLC, NMR, and advanced spectroscopy systems. Continuous calibration, maintenance, accreditation, skilled personnel, and software validation substantially increase operating expenses. Smaller laboratories often struggle to keep pace with rapidly evolving analytical requirements and regulatory expectations. These financial barriers may limit market expansion and reduce competitiveness among regional laboratories. Food manufacturers with substantial internal laboratory capabilities may also perform routine testing in-house, decreasing outsourcing demand for certain standardized analyses while intensifying pricing pressure within the third-party laboratory industry.

Complex and Continuously Evolving Regulatory Requirements

Food regulations frequently change in response to emerging contaminants, evolving scientific evidence, new labeling requirements, and international trade standards. Third-party laboratories must continually update testing methodologies, obtain additional certifications, retrain technical personnel, and validate analytical procedures to remain compliant. Variations between U.S., Canadian, and international regulatory frameworks further complicate laboratory operations. Constant regulatory evolution increases administrative workload and operational costs while extending method development timelines. Laboratories unable to rapidly adapt risk losing accreditation or customer confidence. Maintaining harmonized compliance across multiple food categories and jurisdictions remains a significant operational challenge for independent chemistry testing providers.

Growth Opportunities in the North America Third Party Food Chemistry Labs Market

Expansion of Functional, Plant-Based, and Alternative Protein Foods

Rapid commercialization of functional foods, plant-based alternatives, cultivated proteins, precision fermentation ingredients, and nutraceutical products creates substantial demand for specialized chemical analysis. These innovative products require comprehensive nutritional profiling, stability testing, contaminant screening, bioactive compound quantification, allergen verification, and authenticity assessment before market introduction. Third-party laboratories capable of developing customized analytical methods are well positioned to capture this expanding market. Continuous product innovation by food manufacturers also increases demand for formulation support, shelf-life validation, regulatory consulting, and advanced ingredient characterization, creating long-term business opportunities for laboratories offering specialized food chemistry expertise across North America.

Growing Adoption of Export-Oriented Food Manufacturing

North American food manufacturers are increasingly expanding exports to Europe, Asia-Pacific, Latin America, and the Middle East, requiring compliance with diverse international food safety regulations. Independent food chemistry laboratories play a vital role in generating globally accepted analytical reports, validating export documentation, and supporting certification for destination-specific regulatory requirements. Rising international trade agreements and premium food exports create sustained demand for accredited third-party testing services. Laboratories offering multi-country regulatory expertise, internationally recognized accreditations, customized export compliance testing, and rapid turnaround services can strengthen their competitive position while supporting manufacturers seeking access to global food markets.

Trends in the North America Third Party Food Chemistry Labs Market

Integration of Artificial Intelligence and Laboratory Automation

Third-party food chemistry laboratories are increasingly implementing artificial intelligence, laboratory information management systems (LIMS), robotic sample preparation, automated reporting, and predictive data analytics to improve operational efficiency. Automation minimizes human error, enhances testing consistency, shortens turnaround times, and increases laboratory throughput. AI-assisted analytical interpretation also supports anomaly detection, trend analysis, and quality control optimization. Digital integration enables clients to monitor testing progress through cloud-based platforms while improving regulatory documentation and audit readiness. These technological advancements allow laboratories to manage growing sample volumes without compromising analytical accuracy or compliance with accreditation requirements.

Rising Adoption of Multi-Residue and High-Resolution Analytical Testing

Food manufacturers increasingly prefer comprehensive analytical solutions capable of simultaneously detecting hundreds of contaminants, pesticide residues, veterinary drugs, processing chemicals, heavy metals, and emerging pollutants within a single workflow. Consequently, third-party laboratories are expanding the use of high-resolution mass spectrometry, advanced chromatography, metabolomics, and multi-residue screening techniques. These technologies improve analytical sensitivity, reduce testing time, and support compliance with increasingly stringent regulatory thresholds. Growing emphasis on food authenticity, traceability, ingredient verification, and contaminant surveillance continues to accelerate investments in next-generation analytical platforms, enabling laboratories to deliver broader, faster, and more precise testing services.

Research Scope and Analysis

The North America Third Party Food Chemistry Labs Market is segmented by Testing Area, Testing Method, Food Category, Technology, Sample Type, Laboratory Type, and End User. The market encompasses comprehensive analytical services ranging from contaminant and nutritional testing to advanced instrumental analysis, serving diverse food industries through accredited laboratories that support regulatory compliance, food safety, quality assurance, and product authenticity.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Testing Area Analysis

Contaminant Testing is poised to represent the leading testing area because food manufacturers must continuously monitor products for chemical contaminants that could threaten consumer health and regulatory compliance. Heavy metals, pesticide residues, mycotoxins, veterinary drug residues, and processing contaminants remain major concerns across agricultural and processed food products. Increasing government inspections, stricter maximum residue limits, and expanding international trade requirements continue driving outsourced analytical testing. Third-party laboratories equipped with advanced instrumentation provide reliable, accredited results that help manufacturers minimize recall risks, protect brand reputation, and maintain market access. Consequently, contaminant testing consistently generates the highest testing volumes across North American food chemistry laboratories.

By Testing Method Analysis

Instrumental Analysis is projected to hold the largest share because modern food safety regulations require highly sensitive, accurate, and reproducible analytical techniques capable of detecting contaminants at trace levels. Technologies such as chromatography, mass spectrometry, spectroscopy, ICP-MS, and NMR provide superior analytical precision compared with conventional wet chemistry methods.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Third-party laboratories increasingly invest in these platforms to support contaminant detection, authenticity verification, nutritional analysis, and regulatory compliance. Instrumental methods also offer higher throughput, automation, and multi-residue testing capabilities, enabling laboratories to process large sample volumes efficiently. Their broad application across virtually every food category makes Instrumental Analysis the dominant testing methodology throughout North America.

By Food Category Analysis

Ready-to-Eat & Processed Foods is expected to dominate due to their extensive production volumes, complex formulations, and strict regulatory oversight. These products require comprehensive testing for preservatives, additives, contaminants, allergens, nutritional content, shelf-life stability, and packaging interactions before commercialization. Increasing consumer demand for convenience foods, frozen meals, packaged snacks, and prepared foods has significantly expanded testing requirements. Manufacturers also conduct frequent batch verification to ensure product consistency and labeling accuracy. Since processed foods incorporate multiple ingredients sourced from diverse suppliers, third-party laboratories perform extensive chemical analyses throughout product development and commercial production, making this category the largest contributor to laboratory testing demand.

By Technology Analysis

Chromatographic Techniques is poised to account for the largest market share because they serve as the foundation of modern food chemistry analysis. High-performance liquid chromatography (HPLC), ultra-high-performance liquid chromatography (UHPLC), and gas chromatography (GC) are extensively used for contaminant detection, additive quantification, nutritional profiling, flavor analysis, and authenticity verification. These techniques deliver exceptional analytical sensitivity, selectivity, and reproducibility while supporting regulatory compliance across multiple food applications. When combined with mass spectrometry, chromatography enables comprehensive multi-residue analysis within a single workflow. Their versatility across virtually all food matrices ensures chromatographic techniques remain the preferred technology platform among North America's third-party food chemistry laboratories.

By Sample Type Analysis

Finished Food Products is expected to dominate sample testing because regulatory compliance and commercial product release depend on verifying final product quality before market distribution. Manufacturers routinely submit finished products for nutritional verification, contaminant screening, allergen analysis, labeling validation, preservative quantification, and shelf-life confirmation. Retailers, exporters, and regulatory authorities also prioritize finished product testing to ensure consumer safety and legal compliance. Independent laboratories provide unbiased verification that supports product certification, customer confidence, and recall prevention. Since every commercially distributed food product requires final quality validation, finished food products consistently generate the highest sample volumes for third-party food chemistry laboratories across North America.

By Laboratory Type Analysis

Multinational Testing Laboratories is projected to dominate the market owing to their extensive laboratory networks, advanced analytical infrastructure, internationally recognized accreditations, and comprehensive service portfolios. These organizations support multinational food manufacturers with standardized testing protocols across multiple countries while maintaining compliance with regional and international regulatory frameworks. Their significant investments in automation, high-end instrumentation, digital laboratory management systems, and research capabilities enable faster turnaround times and broader analytical coverage. Strong brand recognition, technical expertise, and the ability to manage high sample volumes further strengthen their competitive position, making multinational laboratories the preferred partners for large food and beverage companies throughout North America.

By End User Analysis

Food Manufacturers is poised to represent the dominant end-user segment because they require continuous chemistry testing throughout product development, production, packaging, and commercialization. Routine analytical testing supports regulatory compliance, quality assurance, nutritional labeling, contaminant detection, ingredient verification, shelf-life validation, and export certification. Increasing innovation in processed foods, functional foods, clean-label products, and plant-based formulations has further expanded laboratory testing requirements. Many manufacturers outsource specialized analyses to accredited third-party laboratories to reduce operational costs while accessing advanced analytical expertise. Continuous production cycles and stringent food safety obligations make food manufacturers the largest consumers of third-party food chemistry laboratory services across North America.

The North America Third Party Food Chemistry Labs Market Report is segmented on the basis of the following:

By Testing Area

- Contaminant Testing

- Heavy Metals

- Pesticide Residues

- Veterinary Drug Residues

- Mycotoxins

- Process Contaminants

- Nutritional Testing

- Macronutrients

- Micronutrients

- Calorie Determination

- Authenticity Testing

- Species Identification

- Adulteration Detection

- Geographic Origin Verification

- Non-GMO Verification

- Allergen Testing

- Major Food Allergens

- Cross-Contamination Assessment

- Ingredient & Formulation Analysis

- Shelf-Life & Stability Studies

- Other Testing Area

By Testing Method

- Wet Chemistry Testing

- Moisture Analysis

- Protein Analysis

- Fat Analysis

- Ash & Fiber Analysis

- Instrumental Analysis

- Chromatography

- Gas Chromatography (GC)

- Liquid Chromatography (HPLC/UHPLC)

- Spectroscopy

- FTIR

- UV-Visible Spectroscopy

- ICP-OES/ICP-MS

- Mass Spectrometry

- Atomic Absorption Spectroscopy (AAS)

- Nuclear Magnetic Resonance (NMR)

By Food Category

- Ready-to-Eat & Processed Foods

- Meat & Poultry

- Seafood

- Dairy & Dairy Alternatives

- Bakery & Confectionery

- Beverages

- Fruits & Vegetables

- Cereals & Grains

- Oils & Fats

- Functional Foods & Nutraceuticals

- Plant-Based Foods

- Infant Nutrition

- Pet Food

- Dietary Supplements

By Technology

- Chromatographic Techniques

- Spectroscopic Techniques

- Molecular Testing

- Rapid Testing Technologies

- AI-Enabled Data Analysis

- Automated Laboratory Platforms

By Sample Type

- Finished Food Products

- Raw Materials

- In-Process Samples

- Packaging Contact Materials

- Environmental Samples

- Water Samples

By Laboratory Type

- Multinational Testing Laboratories

- Independent Commercial Laboratories

- Regional Testing Laboratories

- Specialty Food Chemistry Laboratories

By End User

- Food Manufacturers

- Beverage Manufacturers

- Ingredient Suppliers

- Retail & Private Label Brands

- Food Importers & Exporters

- Food Service Companies

- Government & Regulatory Agencies

- Agriculture & Farming Companies

- Contract Research Organizations (CROs)

Competitive Landscape

The North American third-party food chemistry labs market is characterized by intense competition between a few dominant multinational networks, a broad layer of independent commercial labs, and a constellation of high-value specialty labs. The multinational players compete on breadth of service, global supply chain integration, and throughput speed, aggressively investing in automated laboratory platforms and IT systems that provide clients with enterprise-level data portals. Strategic M&A remains the dominant growth tactic for these firms to rapidly acquire new testing specialties and expand their geographic reach into regional markets. In contrast, specialty labs construct a virtually impenetrable competitive moat around their specific areas of expertise, such as authenticity testing or extractables and leachables (E&L) analysis for packaging. For these firms, intellectual property in the form of proprietary sample preparation methodologies and unmatched scientific interpretation constitutes their primary market differentiator over scale or price. The landscape is witnessing increased competition from agile start-ups that are purely AI-native, developing software layers that analyze existing lab data streams to provide predictive supply chain intelligence, positioning themselves as a novel intermediary between the physical lab and the food industry client.

Some of the prominent players in the North America Third Party Food Chemistry Labs Market are:

- Eurofins Scientific

- SGS SA

- Bureau Veritas

- Intertek Group plc

- ALS Limited

- Mérieux NutriSciences

- TÜV SÜD

- TÜV Rheinland

- NSF International

- UL Solutions

- IEH Laboratories & Consulting Group

- Microbac Laboratories

- Food Safety Net Services (FSNS)

- Certified Laboratories, Inc.

- EMSL Analytical, Inc.

- Q Laboratories, Inc.

- Silliker Inc.

- Dairyland Laboratories, Inc.

- Deibel Laboratories

- EAG Laboratories

- Other Key Players

Recent Developments

- February 2026: Eurofins Scientific expanded its North American food chemistry testing capabilities by introducing advanced multi-residue analytical services using high-resolution mass spectrometry, enabling faster detection of contaminants, pesticides, and emerging food safety risks.

- November 2025: SGS strengthened its food testing network across North America by upgrading laboratory automation and digital Laboratory Information Management Systems (LIMS), improving sample throughput, traceability, and turnaround times for food chemistry analyses.

- August 2025: Mérieux NutriSciences launched enhanced authenticity and adulteration testing services for plant-based foods and functional ingredients in North America, addressing growing demand for clean-label verification and regulatory compliance.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 9.1 Bn |

| Forecast Value (2035) |

USD 19.1 Bn |

| CAGR (2026–2035) |

8.5% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Testing Area, By Testing Method, By Food Category, By Technology, By Sample Type, By Laboratory Type, and By End User |

| Regional Coverage |

North America – The US and Canada |

Frequently Asked Questions

How big is the North America Third Party Food Chemistry Labs Market?

▾ The market is positioned to be valued at USD 9.1 billion in 2026 and is projected to reach USD 19.1 billion by 2035, driven by the universal need for objective food safety verification and scientific substantiation of label claims in a highly litigious and regulated market.

What is the CAGR of the North America Third Party Food Chemistry Labs Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 8.5% from 2026 to 2035, reflecting the accelerating outsourcing trend among food companies and the continuous introduction of complex, novel food products requiring specialized analytical chemistry expertise.

What factors are driving the growth of the North America Third Party Food Chemistry Labs Market?

▾ Key drivers include the mandatory enforcement of FDA’s FSMA preventive controls, the escalating number of food recalls due to undeclared allergens, and the consumer-driven explosion of "free-from" and "clean-label" claims that require independent validation.

What are the major trends in the North America Third Party Food Chemistry Labs Market?

▾ Major trends include the integration of AI-enabled data analysis for rapid, non-targeted contaminant screening, the shift toward automated laboratory platforms for high-throughput efficiency, and a booming demand for advanced authenticity testing to combat increasingly sophisticated food fraud.

Who are the key players in the North America Third Party Food Chemistry Labs Market?

▾ Key players include Eurofins Scientific, SGS SA, Bureau Veritas, Intertek Group, ALS Limited, Mérieux NutriSciences, and NSF International, driving industry consolidation and technological advancement through massive investments, strategic acquisitions, and the expansion of specialized analytical service portfolios.