Market Overview

The nuclear power plant equipment market covers all hardware systems required to construct, operate, and maintain nuclear reactors. Scope includes reactor core components, steam generators, reactor vessels, pressurizers, heat exchangers, and both island and auxiliary equipment systems. Nuclear fuel fabrication, uranium mining, and waste management services as standalone revenue categories fall outside Nuclear Power Plant Equipment Market's boundaries.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

As reported by the World Nuclear Association, 440 operable nuclear reactors worldwide held total capacity of 398 GWe at end-2024, up 6 GWe on 2023. Every operating reactor requires scheduled maintenance, component replacement, and periodic refurbishment. World Nuclear Association data shows Asia hosts approximately 75% of all reactors under construction worldwide, concentrating procurement volume in a single region and reshaping global supply chain flows accordingly.

Three demand channels now operate simultaneously: government reactor construction programs, utility life-extension contracts, and corporate power purchase agreements from the technology sector. Microsoft committed to a 20-year PPA for the 835 MW Three Mile Island Unit 1 restart. Amazon signed a 1.9 GW Susquehanna agreement and Google contracted up to 500 MW from Kairos SMRs. In May 2025, GE Vernova Hitachi began construction of the Western world's first SMR, the 300 MW BWRX-300, at Ontario Power Generation's Darlington site, establishing the first commercial SMR equipment manufacturing and delivery benchmark and confirming that new reactor formats are entering procurement pipelines ahead of regulatory systems designed to process them.

Market Size and Forecast

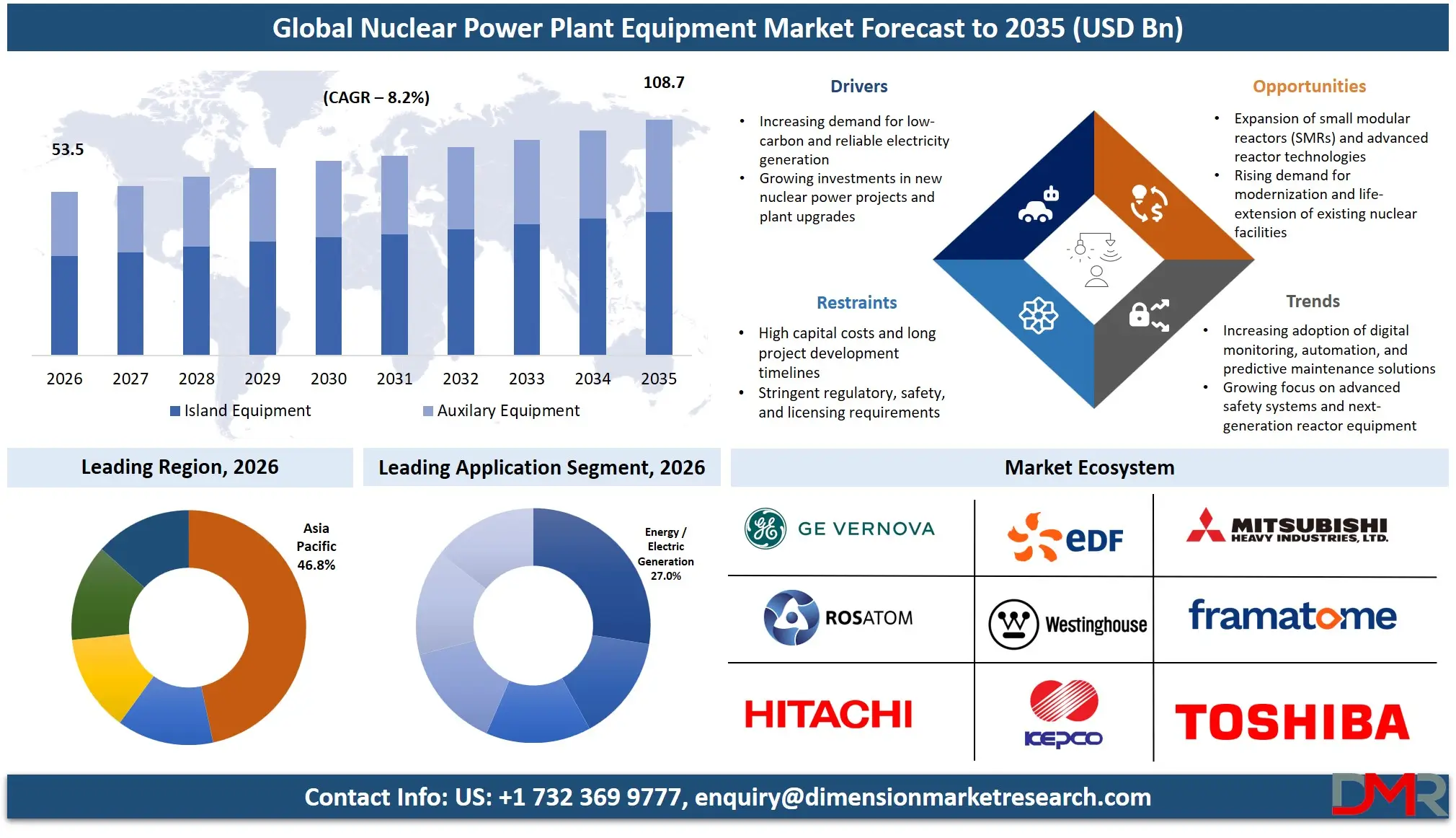

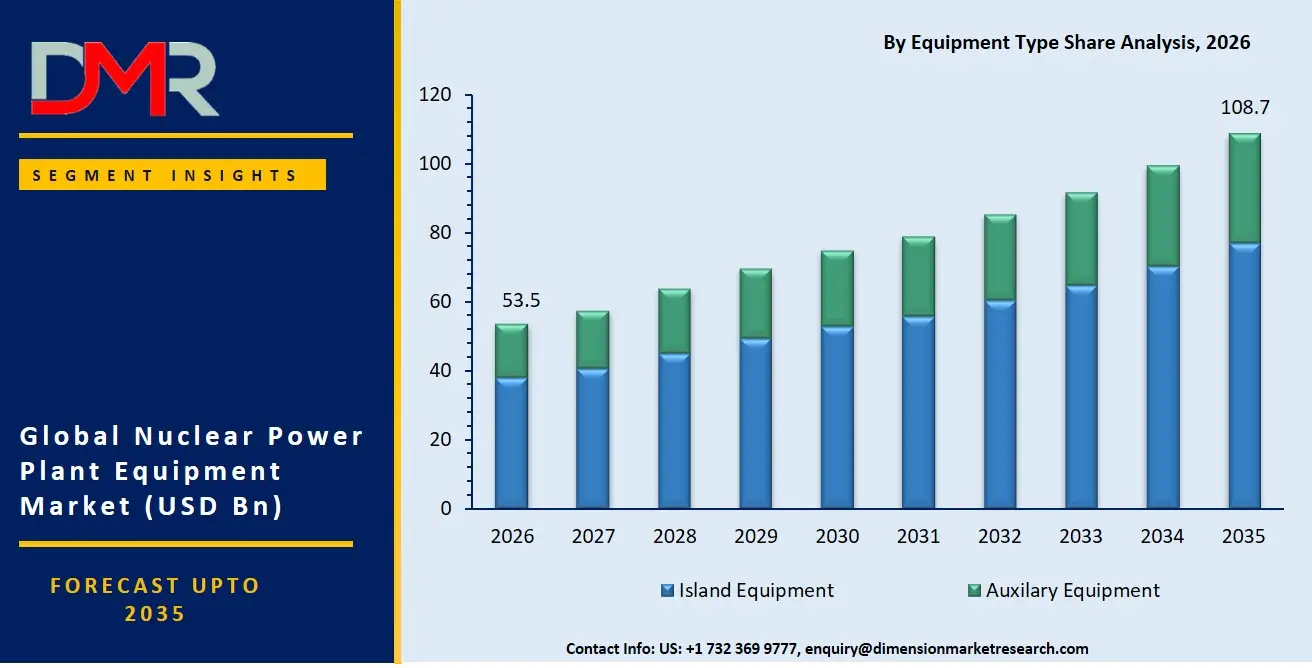

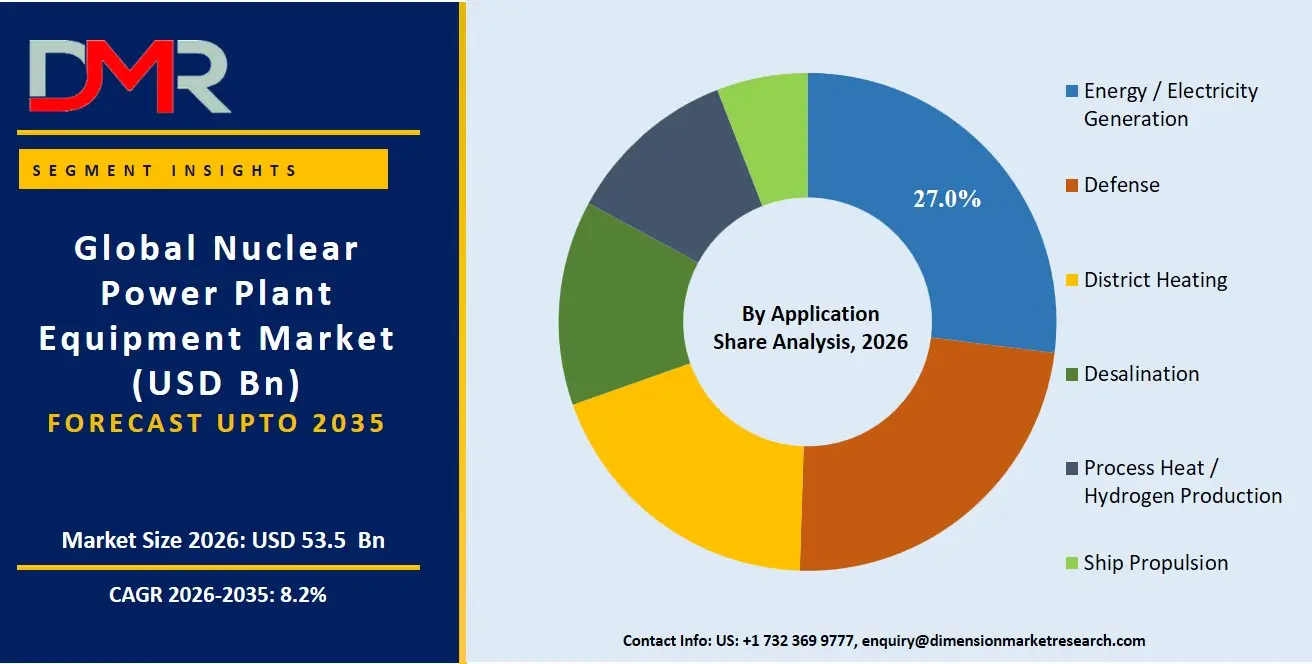

The Global Nuclear Power Plant Equipment Market size is estimated at USD 53.5 Billion in 2026 from USD 49.3 Billion in 2025, and is projected to reach USD 108.7 Billion by 2035, exhibiting a CAGR of 8.2% during the forecast period.

Per IAEA PRIS, 72 reactors with combined net capacity of 75,474 MWe are currently under construction globally, representing contracted equipment demand rather than speculative future orders. IEA data projects global nuclear capacity expanding from 420 GWe in 2024 to 563 GWe by 2030, a 34% capacity increase that translates directly into equipment procurement across reactor systems, balance-of-plant, and component replacement programs. Framatome recorded new orders of EUR 21,230 Million in FY2024, driven by contracts for the first six EPR2 reactors in France and two Sizewell C units in the UK, a single-year order intake that illustrates how concentrated procurement events shift the market's revenue trajectory.

In October 2025, the US Government announced an USD 80 Billion strategic partnership with Westinghouse, Brookfield, and Cameco to deploy AP1000 and AP300 reactors across the US, converting speculative AP300 orders into a funded procurement program with a defined two-decade runway. The downside scenario centers on regulatory delay and cost overrun risk. If NRC licensing timelines extend further, equipment delivery schedules slip and defer revenue recognition across the supply chain, compressing manufacturer margins on projects where capital is already deployed.

Equipment Type Analysis

Island Equipment led the By Equipment Type segment with a 70.6% share in 2026.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Island equipment encompasses all primary systems directly involved in the nuclear steam supply cycle: reactor vessels, steam generators, pressurizers, and core internals. These components carry the highest unit values, longest manufacturing lead times, and most stringent quality certifications of any equipment category. This regulatory intensity restricts the qualified supplier base, sustains premium pricing, and structurally concentrates revenue at the island equipment level across every reactor construction program.

Auxiliary equipment covers all balance-of-plant systems supporting reactor operation without participating in the nuclear steam cycle. Cooling water systems, electrical distribution infrastructure, instrumentation networks, and waste handling equipment all fall within this category. Auxiliary systems generate procurement demand across both new builds and operating plant maintenance cycles, making this segment a steady revenue contributor even when large construction programs pause between approval tranches.

Reactor Type Analysis

With a commanding share in 2026, Pressurized Water Reactor outpaced all other reactor type categories.

PWRs represent the majority of the global operating fleet and account for the bulk of reactors currently under construction, including China's CAP1000 and CAP1400 programs and Westinghouse's AP1000 deployments. The concentration of procurement in PWR-compatible components gives established PWR equipment manufacturers a structural scale advantage over suppliers serving smaller reactor categories. NPCIL commissioned RAPP-7, a 700 MW indigenous Pressurized Heavy Water Reactor built entirely with domestically manufactured equipment in March 2025. Once RAPP-7 and RAPP-8 reach full operation, Rajasthan Atomic Power Project capacity will rise from 1,180 MW to 2,580 MW, confirming that PHWR procurement demand is durable within national energy security programs.

Boiling Water Reactor technology underpins GE Vernova Hitachi's BWRX-300 program, whose simplified passive safety design reduces component count relative to conventional BWRs, lowering per-unit equipment cost while creating new manufacturing specifications that incumbent large-reactor suppliers must adapt to serve. Light Water Graphite Reactor demand remains concentrated in Russia's operating fleet, with Leningrad 2-4 at 1,066 MW recording a construction start in March 2025. Small Modular Reactor equipment is the fastest-evolving procurement category, with India's BSMR-200 demonstration unit actively engaging private vendors and opening procurement channels that did not exist under the previous state-monopoly equipment model.

Component Analysis

Nuclear Reactor Core Components accounted for approximately 45.6% of By Component demand in 2026, the highest of any category.

Core components including fuel assemblies, control rod drive mechanisms, reactor internals, and core support structures carry the most stringent nuclear safety classifications of any equipment category. This regulatory intensity restricts the qualified supplier base, sustains premium pricing, and makes replacement economically prohibitive once a plant's core specification is set. Heat exchangers and condensers transfer thermal energy from the primary nuclear circuit to the secondary steam cycle without allowing radioactive fluid to cross system boundaries, generating maintenance-driven replacement demand throughout a reactor's operating life.

Doosan Enerbility's KRW 2.9 Trillion contract with KHNP for Shin Hanul Units 3 and 4 specifically includes steam generator supply as a core deliverable, illustrating how steam generator contracts anchor the overall equipment procurement value for large PWR projects. Reactor vessels are the most capital-intensive single forgings in any reactor project, produced by a globally limited number of heavy manufacturing facilities. Pressurizers maintain primary circuit pressure in PWR systems and are procured as part of the nuclear steam supply system package for every PWR build, meaning pressurizer demand scales directly with the global PWR construction pipeline.

Application Analysis

Energy and Electricity Generation captured the dominant share across By Application categories in 2026.

Nuclear plants supplied 2,667 TWh of electricity in 2024 across 31 countries, up from 2,601 TWh in 2023, as reported by the World Nuclear Association. Fourteen countries produced at least one-quarter of their electricity from nuclear in 2024, with France at approximately 70%, confirming that electricity generation is the structurally irreplaceable application for most national energy systems. Defense applications operate on sovereign procurement timelines insulated from commercial utility investment cycles, serving naval propulsion programs and weapons-related nuclear infrastructure through a narrow base of specialized manufacturers.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Desalination applications pair reactor thermal output with water production in water-stressed regions, most notably the Middle East, where co-located nuclear-desalination configurations may shape future equipment specifications. District heating, process heat, and hydrogen production remain early-stage commercially but carry strategic significance as industrial decarbonization mandates tighten. High-temperature reactor designs capable of supplying industrial process heat open equipment procurement requirements distinct from standard light water reactor component specifications.

Key Market Segments

By Equipment Type

- Island Equipment

- Auxiliary Equipment

By Reactor Type

- Pressurized Water Reactor (PWR)

- Pressurized Heavy Water Reactor (PHWR)

- Boiling Water Reactor (BWR)

- Light Water Graphite Reactor (LWGR)

- Gas-Cooled Reactor (GCR)

- Fast Breeder Reactor (FBR)

- Small Modular Reactor (SMR)

By Component

- Nuclear Reactor Core Components

- Heat Exchangers & Condensers

- Steam Generators

- Reactor Vessels

- Pressurizers

By Application

- Energy / Electricity Generation

- Defense

- District Heating

- Desalination

- Process Heat / Hydrogen Production

- Ship Propulsion

Regional Analysis

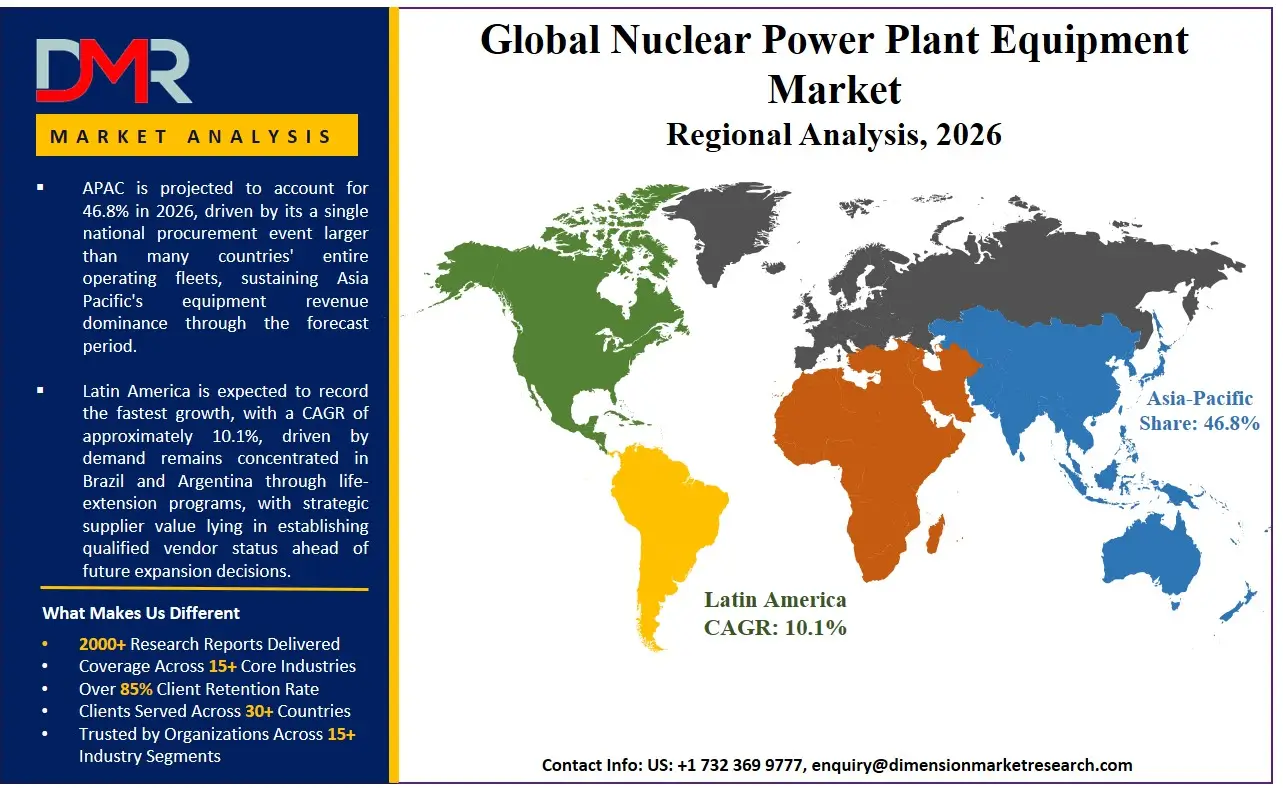

Asia Pacific held a 46.8% share in 2026, valued at USD 25.0 Billion.

Asia Pacific's dominance reflects the concentration of active construction programs in the region. China alone operates 60 reactors at 58,721 MWe net with 32 more under construction as of July 2025 per IAEA PRIS. China's State Council approved 11 new reactors totaling approximately 13 GW in August 2024, a single national procurement event larger than many countries' entire operating fleets, sustaining Asia Pacific's equipment revenue dominance through the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

North America is transitioning from a maintenance-and-life-extension market to an active new-build and recommissioning market. The US generated 816 TWh from nuclear in 2024, representing 18% of national electricity output per WNA data, providing the demand foundation that justifies recommissioning and new-build capital commitments now entering the procurement pipeline. The Emirates Nuclear Energy Company and GE Vernova Hitachi signed an MoU in May 2025 on international BWRX-300 deployment, marking the UAE's entry into SMR equipment procurement planning and establishing the Middle East as an emerging procurement geography. Europe's equipment market is anchored by France's fleet maintenance requirements and high-value new-build programs across Central and Eastern Europe, while Latin America's demand remains concentrated in Brazil and Argentina through life-extension programs, with strategic supplier value lying in establishing qualified vendor status ahead of future expansion decisions.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Fleet Expansion, Energy Security Mandates, and AI Demand Drive Simultaneous Procurement

Government fleet expansion programs generate the largest single tranches of equipment demand. India's FY 2025–26 budget allocated Rs 20,000 Crore for SMR development, and NPCIL targets 22 GW by 2032. Per April 2025 Enerdata data, India already operates 25 reactors with 8,880 MW installed capacity and has 11 more under construction totaling 8,700 MW, making it a high-volume, long-duration procurement market with a policy mandate for domestic content. NPCIL commissioned RAPP-7 in March 2025, a 700 MW indigenous PHWR built entirely with domestically manufactured nuclear equipment, validating India's domestic supplier base and demonstrating that state-directed procurement programs can deliver on construction timelines even as Western projects slip.

The technology sector's power requirements have become a direct procurement signal for equipment manufacturers. Microsoft committed USD 1.6 Billion to restart the 835 MW Three Mile Island Unit 1 under a 20-year PPA. Amazon signed a 1.9 GW Talen/Susquehanna agreement, and Google contracted up to 500 MW from Kairos SMRs. In April 2025, the US DOE granted Holtec International 10CFR810 authorization to sell the SMR-300 for deployment in India, opening a US-origin SMR supply channel into India that did not previously exist. China's approval of 11 reactors across 5 sites, anchored by the KRW 5.6 Trillion Doosan Enerbility contract with KHNP for Dukovany Units 5 and 6, illustrates how state-directed procurement concentrates equipment spend into single contracting events that restructure supplier order books overnight.

NRC Licensing Delays and Cost Overrun History Constrain Deployment Timelines

IEA and METI 2025 analysis documents that recent US and EU nuclear projects averaged 8 years of delay and 2.5x cost overruns against initial estimates. These outcomes elevate risk premiums across the equipment supply chain, increase insurance and financing costs, and create hesitation among utility off-takers evaluating new procurement commitments. The restraint is a delivery credibility problem that the industry has not resolved at scale, and one that regulatory acceleration alone cannot fix without concurrent improvements in project execution discipline.

SMR Manufacturing and Tech-Sector Pipelines Open New Equipment Demand Channels

Small Modular Reactors represent the most structurally distinct equipment opportunity in Nuclear Power Plant Equipment Market. The IEA projects SMR investment rising from under USD 5 Billion today to USD 25 Billion annually by 2030, with cumulative investment reaching USD 670 Billion through 2050. In December 2025, TVA and Holtec received up to USD 800 Million in US federal funding to support SMR construction programs, converting speculative development commitments into funded procurement pipelines with defined capital timelines and shifting SMR from a policy aspiration to a contracted construction program.

Reactor lifetime extension programs create a distinct and less cyclical equipment revenue stream. The IEA documents lifetime extensions for 60+ reactors worldwide, each requiring systematic replacement of pressure vessels, steam generators, heat exchangers, and control systems. Amazon's X-energy partnership targets 5+ GW, Energy Northwest plans 4 SMRs totaling 320 to 960 MW in Washington State, and Meta issued an RFP for 1 to 4 GW of new nuclear. These buyers operate on corporate capital allocation cycles rather than utility rate-case timelines, compressing equipment lead times and creating premium pricing opportunities for manufacturers with available capacity.

Market Trends

SMR Standardization and Recommissioning Are Redefining Equipment Investment Logic

Rolls-Royce SMR was selected as winner of the Great British Energy Nuclear SMR competition in June 2025, having received GBP 210 Million in UK government funding supplemented by GBP 280 Million in private capital and achieved GDA Step 2 for its 470 MW design in July 2024. Standardized designs allow component manufacturers to invest in tooling and capacity with greater confidence, shifting equipment production from custom fabrication toward serial manufacturing. In December 2025, Holtec International received a DOE Generation III+ SMR Tier 1 First Mover award for its SMR-300 at the Palisades site, confirming that recommissioning and SMR deployment are converging at single project locations and that manufacturers serving both segments simultaneously hold a structural procurement advantage over single-segment suppliers.

Market Competition Overview

The nuclear power plant equipment market is moderately consolidated at the tier-one level, where a small group of vertically integrated heavy engineering companies controls access to the most safety-critical components. Approximately 85% of one leading supplier's revenues derive from recurring services tied to its installed equipment base, as reported by Westinghouse Electric, confirming that competitive advantage in Nuclear Power Plant Equipment Market is not just winning new-build contracts but locking in decades of follow-on service procurement. Suppliers without large installed bases face a structural revenue ceiling regardless of their new-build order intake.

The USD 80 Billion US Government partnership with Westinghouse, Brookfield, and Cameco to deploy AP1000 and AP300 reactors illustrates that governments are actively shaping which technology platforms and therefore which equipment supply chains will dominate the next build cycle. Share is shifting toward suppliers positioned in active construction geographies, with Korean manufacturers extending geographic reach into European new builds. The SMR segment is creating a second competitive tier where new entrants can establish positions before incumbents lock in design specifications, compressing the geographic insulation that previously moderated rivalry intensity among established tier-one players.

Company Profiles

General Electric Company, through GE Vernova Hitachi Nuclear Energy, holds a structurally significant position as the only Western company with an SMR currently under construction. BWX Technologies reported record 2025 revenue of USD 3.2 Billion, up 18% year-over-year per February 2026 financial results, with commercial operations delivering 63% growth, validating a deliberate strategy of scaling physical production infrastructure ahead of SMR and defense reactor demand. In December 2025, Doosan Enerbility signed a KRW 5.6 Trillion contract with KHNP for Dukovany Units 5 and 6, its largest international equipment contract to date, demonstrating that Korean manufacturers are now competing directly against European and American incumbents across multiple geographies simultaneously.

Westinghouse Electric Company LLC operates the most commercially resilient business model in Nuclear Power Plant Equipment Market. Westinghouse's 2025 adjusted EBITDA outlook was raised to USD 525–580 Million, with EBITDA projected to grow at 6% to 10% CAGR over five years, anchored by approximately 85% of revenues derived from recurring fuel and services. GE Vernova Hitachi's BWRX-300 project at OPG's Darlington site gives it a first-mover advantage in establishing manufacturing benchmarks, supply chain qualifications, and cost reference points for all subsequent BWRX-300 orders, a position that compounds in value as the global SMR order pipeline grows.

Key Players

- General Electric Company

- Mitsubishi Heavy Industries Ltd.

- Toshiba Corporation

- Doosan Corporation

- Shanghai Electric Group Co. Ltd.

- BWX Technologies Inc.

- Westinghouse Electric Company LLC

- Larsen & Toubro Limited

- Alstom

- Korea Electric Power Corporation (KEPCO)

- Dongfang Electric Corporation Ltd.

- AREVA (Framatome)

- Rosatom State Atomic Energy Corporation

- Bharat Heavy Electricals Limited (BHEL)

- Hindustan Construction Company

- GE Hitachi Nuclear Energy

Supply Chain and Value Chain Analysis

The nuclear power plant equipment supply chain originates with specialty steel mills and precision forging facilities producing reactor-grade materials: pressure vessel steel, zirconium alloy for fuel cladding, and high-purity nickel alloys for heat exchanger tubing. These raw material inputs come from a globally restricted number of qualified facilities, placing the supply chain's most acute bottleneck at its foundation rather than at the assembly or integration stage. Suppliers controlling access to nuclear-qualified forgings exercise disproportionate pricing power relative to all downstream value chain participants.

The highest value in the chain is created at the nuclear steam supply system level, where reactor vessels, steam generators, and pressurizers are fabricated and integrated into qualified nuclear assemblies. The value chain's mid-section covering balance-of-plant systems, instrumentation, electrical distribution, and auxiliary equipment is served by a broader supplier base with lower barriers to qualification. Microsoft's 20-year Three Mile Island PPA and Amazon's 1.9 GW Susquehanna agreement create defined demand visibility that equipment suppliers can use to justify capacity investment, reducing the speculative risk that historically prevented manufacturers from expanding heavy fabrication facilities ahead of confirmed orders.

Regulatory Landscape

Nuclear power plant equipment operates under the most stringent regulatory framework of any industrial sector. In the United States, the NRC governs equipment qualification, manufacturing standards, and reactor licensing under 10 CFR 50 and related appendices. Holtec's Palisades restart received a USD 1.52 Billion DOE loan guarantee in September 2024 while NRC approval remained pending into 2026, a decoupling that forces manufacturers to absorb carrying costs on staged components with no confirmed revenue date. Export authorization adds a second regulatory layer, with the 10CFR810 process functioning as a market access gate that shapes competitive dynamics between US-origin and non-US-origin equipment suppliers.

In the United Kingdom, the Generic Design Assessment process governs reactor technology approval before any site-specific equipment procurement can begin. China's State Council approval of 11 reactors in August 2024 triggered immediate equipment procurement at the state enterprise level, a regulatory-commercial integration model that compresses the approval-to-order cycle relative to Western jurisdictions. India's AERB governs indigenous reactor equipment qualification under NPCIL oversight, while BWX Technologies' approximately USD 1.5 Billion NNSA contract operates under classified procurement standards that functionally exclude non-US suppliers, illustrating how defense-adjacent regulatory segmentation creates parallel supplier ecosystems with entirely separate qualification requirements.

Investment and White Space Analysis

Investment is flowing most heavily into SMR development and manufacturing infrastructure. BWX Technologies identified the heavy component manufacturing white space and addressed it through the Precision Components Group acquisition in April 2026, adding over 500,000 sq ft of heavy manufacturing floor space. No other publicly announced transaction has targeted this specific bottleneck at comparable scale, meaning the gap between contracted construction demand and available fabrication throughput remains largely unaddressed by the broader market.

The US Government's USD 800 Million federal funding commitment to TVA and Holtec for SMR builds, combined with Rolls-Royce SMR's GBP 490 Million combined public-private funding, confirms that sovereign capital is actively pre-positioning in SMR supply chains ahead of commercial scale deployment. India presents the clearest geographic combination of high construction volume and underdeveloped private supplier participation, with the 10CFR810 authorization creating a first-mover window for qualified US suppliers before European and Asian competitors establish vendor relationships. The reactor recommissioning segment carries no established competitive structure, no standardized refurbishment equipment specification, and no pricing benchmark. Manufacturers that develop recommissioning-specific component packages now can define the market's commercial terms rather than compete within them.

Recent Developments

- April 19, 2026 BWX Technologies. Acquisition. Announced a definitive agreement to acquire Pennsylvania-based Precision Components Group, adding over 500,000 sq ft of heavy manufacturing capacity to support nuclear reactor vessel and component production.

- February 18, 2026 Doosan Enerbility. Contract. Signed an approximately KRW 320 Billion agreement with Doosan Skoda Power for steam turbine and control systems for Dukovany Units 5 and 6 in the Czech Republic.

- April 6, 2026 AFRY. Partnership. Signed a non-exclusive collaboration agreement with GE Vernova Hitachi Nuclear Energy to support BWRX-300 SMR deployment across multiple international markets.

- May 9, 2025 Hitachi-GE Nuclear Energy. Supply Agreement. Confirmed supply of Reactor Internals, FMCRD, and Hydraulic Control Units for the first BWRX-300 unit at OPG's Darlington New Nuclear Project in Canada.

- October 7, 2025 GE Vernova Hitachi Nuclear Energy and Samsung C&T. Strategic Alliance. Formed a partnership to advance global deployment of the BWRX-300 SMR across multiple international markets.

- September 16, 2025 BWX Technologies. Contract. Secured an approximately USD 1.5 Billion, 10-year contract from the US NNSA to establish a domestic high-purity depleted uranium enrichment facility in Erwin, Tennessee.

- May 26, 2025 Emirates Nuclear Energy Company and GE Vernova Hitachi Nuclear Energy. MoU. Signed an agreement on international BWRX-300 SMR deployment, marking the UAE's formal entry into SMR equipment procurement planning.

- October 27, 2025 US Government and Westinghouse. Strategic Partnership. Announced an USD 80 Billion program with Brookfield and Cameco to deploy AP1000 and AP300 reactors across the US, with the government receiving a 20% participation interest in cash distributions exceeding USD 17.5 Billion.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 49.3 Billion |

| Market Value (2026) |

USD 53.5 Billion |

| Forecast Revenue (2035) |

USD 108.7 Billion |

| CAGR (2026 to 2035) |

8.2% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020 to 2024 |

| Forecast Period |

2026 to 2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Equipment Type (Island Equipment, Auxiliary Equipment), By Reactor Type (Pressurized Water Reactor, Pressurized Heavy Water Reactor, Boiling Water Reactor, Light Water Graphite Reactor, Gas-Cooled Reactor, Fast Breeder Reactor, Small Modular Reactor), By Component (Nuclear Reactor Core Components, Heat Exchangers & Condensers, Steam Generators, Reactor Vessels, Pressurizers), By Application (Energy / Electricity Generation, Defense, District Heating, Desalination, Process Heat / Hydrogen Production, Ship Propulsion) |

| Regional Analysis |

North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape |

General Electric Company, Mitsubishi Heavy Industries Ltd., Toshiba Corporation, Doosan Corporation, Shanghai Electric Group Co. Ltd., BWX Technologies Inc., Westinghouse Electric Company LLC, Larsen & Toubro Limited, Alstom, Korea Electric Power Corporation (KEPCO), Dongfang Electric Corporation Ltd., AREVA (Framatome), Rosatom State Atomic Energy Corporation, Bharat Heavy Electricals Limited (BHEL), Hindustan Construction Company, GE Hitachi Nuclear Energy |

| Customization Scope |

Customization for segments and region or country level will be provided. Additional customization can be done based on requirements. |

| Purchase Options |

Three license options: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |

Frequently Asked Questions

What is the biggest investment opportunity in Nuclear Power Plant Equipment Market?

▾ Heavy component manufacturing capacity for reactor vessels and large forgings is the most underserved investment segment today. Sovereign capital is pre-positioning aggressively in SMR supply chains, yet fabrication throughput has not kept pace with the contracted construction pipeline. Manufacturers that capitalize this manufacturing layer before the 72-reactor global pipeline matures will hold structural pricing power through the forecast period.

Who are the top companies in Nuclear Power Plant Equipment Market?

▾ Leading players include General Electric Company, Westinghouse Electric Company LLC, Doosan Corporation, BWX Technologies Inc., Framatome (AREVA), Mitsubishi Heavy Industries Ltd., and Rosatom State Atomic Energy Corporation. Korean manufacturers Doosan Enerbility and KEPCO are extending their geographic reach beyond domestic programs into European and North American new-build competitions, intensifying rivalry among established tier-one suppliers.

Which segment is growing fastest in Nuclear Power Plant Equipment Market and why?

▾ Small Modular Reactor equipment is the fastest-growing procurement category in Nuclear Power Plant Equipment Market. Corporate PPA demand from hyperscalers, sovereign capital commitments, and the first Western SMR construction start at OPG's Darlington site in May 2025 have collectively converted SMR from a policy aspiration into a contracted construction program. Standardized SMR designs are shifting equipment production from custom fabrication toward serial manufacturing, compressing per-unit costs as order volumes grow.

Which region is growing fastest in Nuclear Power Plant Equipment Market and why?

▾ Asia Pacific leads in volume, anchored by China's 11-reactor approval program and India's 22 GW capacity target by 2032. North America is re-entering active capital equipment procurement at scale for the first time in over a decade, driven by the USD 80 Billion Westinghouse partnership, the Palisades recommissioning program, and GE Vernova Hitachi's Darlington SMR construction start, collectively signaling a structural demand inflection point not seen since the 1970s build cycle.

What is the biggest challenge holding Nuclear Power Plant Equipment Market back?

▾ Regulatory licensing delays are the market's primary structural constraint. This delivery credibility problem forces manufacturers to absorb carrying costs on staged equipment while awaiting regulatory clearance that arrives on no fixed timeline. Until the industry resolves the decoupling between financing authorization and licensing approval, execution risk will continue to compress margins and deter utility off-takers from committing to new procurement programs.