Market Overview

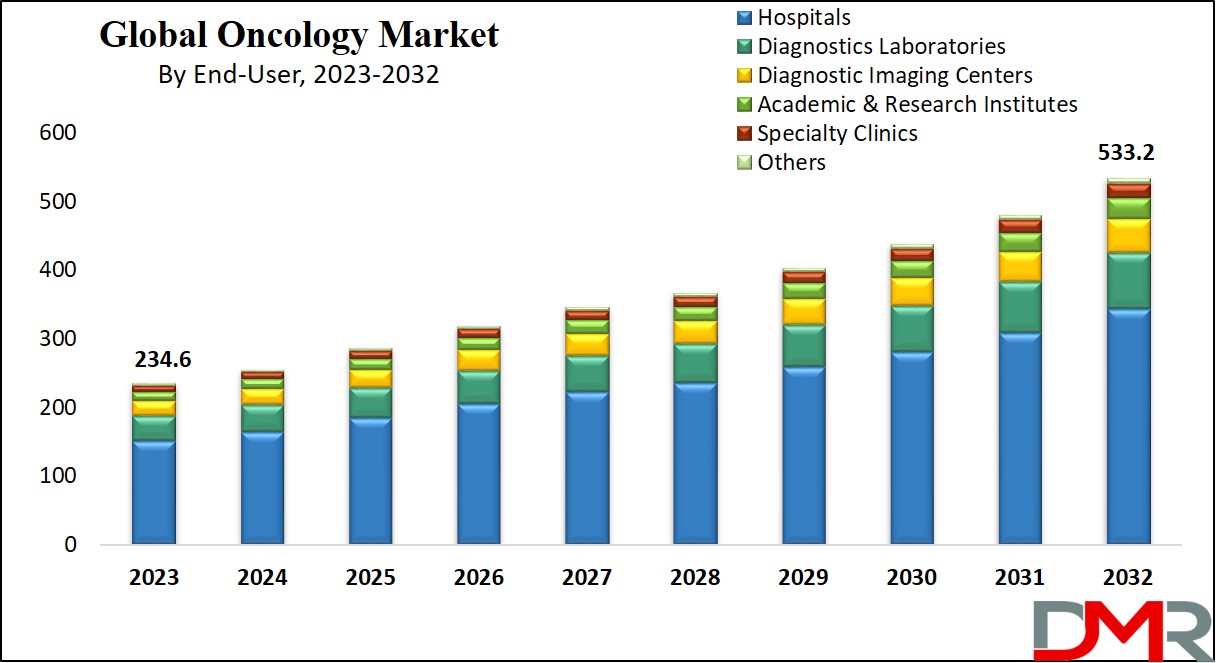

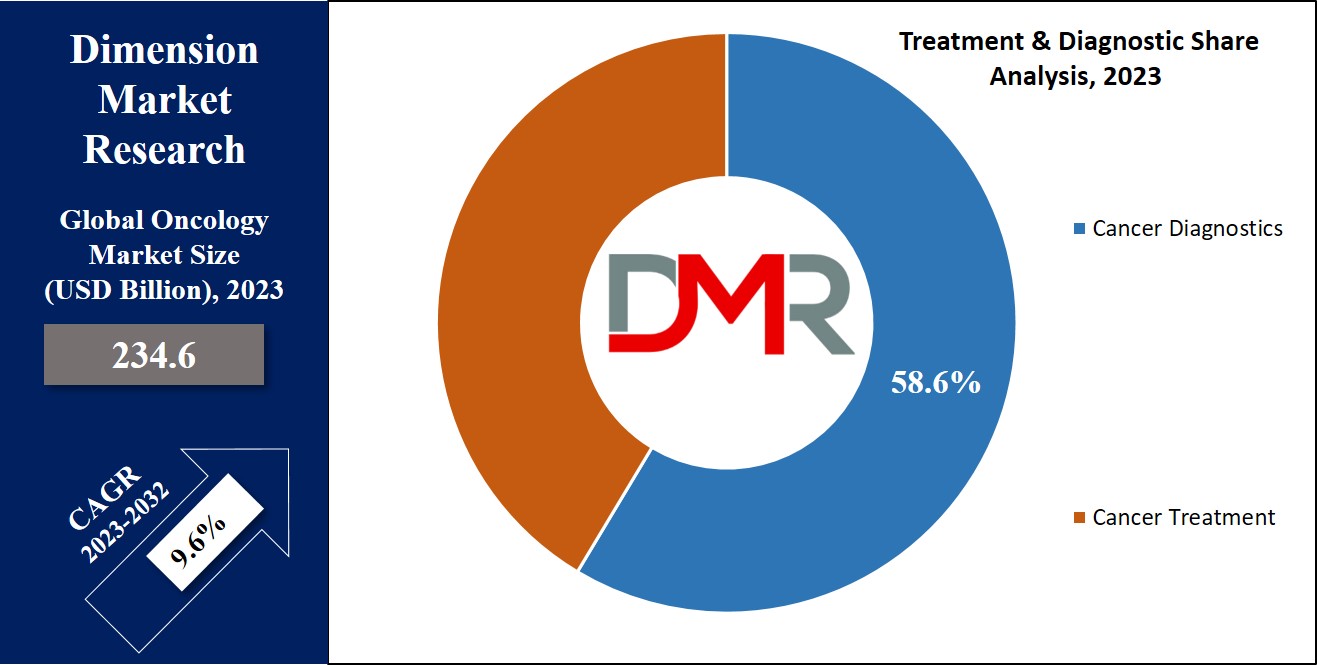

The Global Oncology Market is expected to reach a value of USD 234.6 billion in 2023, and it is further anticipated to reach a market value of USD 533.2 billion by 2032 at a CAGR of 9.6%.

The global oncology market refers to the collective economic ecosystem that is involved in the development, production, distribution, and consumption of products and services related to the prevention, diagnosis, and treatment of cancer worldwide. This market comprises a wide range of pharmaceutical products, medical devices, diagnostic tools, treatment modalities, and supportive care services dedicated to addressing the complicated nature of cancer.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The rising consumption of tobacco and smoking remains one of the major contributors to the increasing prevalence of cancer cases worldwide. The global oncology market encompasses extensive research and development efforts aimed at discovering innovative cancer therapies, conducting clinical trials to assess the efficacy and safety of cancer drugs and medical devices, and enhancing healthcare facilities that provide oncology services. Additionally, Healthcare Analytics plays a critical role in this space by enabling data-driven insights for early detection, personalized treatment planning, and improved patient outcomes, alongside supportive care services designed to enhance the quality of life for cancer patients.

Key Takeaways

- The Global Oncology Market is valued at USD 234.6 billion in 2023 and is projected to reach USD 533.2 billion by 2032, growing at a CAGR of 9.6%.

- By Treatment & Diagnostics, cancer diagnostics dominate with 58.6% share in 2023, fueled by early detection initiatives, molecular diagnostics, imaging techniques, and liquid biopsy innovations.

- By Cancer Type, lung cancer leads the segment in 2023, driven by its high global prevalence, smoking-related incidence, and need for advanced diagnostic & treatment methods.

- By End-User, hospitals hold 51.2% share in 2023, owing to their integrated oncology services, advanced facilities, and ability to manage multifaceted cancer treatments.

- North America dominates the global oncology market with 47.4% share in 2023, supported by strong R&D infrastructure, leading pharmaceutical companies, regulatory frameworks, and advanced healthcare facilities.

- The competitive landscape is shaped by pharma giants (Roche, Merck, Pfizer, Bayer, AstraZeneca) and emerging biotech firms, with rising emphasis on immunotherapy, gene therapy, precision medicine, and AI-driven drug discovery.

Use Cases

- Early Cancer Detection & Screening: Advanced diagnostics such as liquid biopsies, molecular testing, and imaging tools help in identifying cancer at earlier stages, improving survival rates.

- Personalized & Precision Medicine: Tailoring cancer treatment plans based on genetic profiles and biomarkers, leading to higher efficacy and reduced side effects.

- Immunotherapy & Targeted Therapies: Harnessing the body's immune system and targeted drug delivery to improve treatment outcomes in lung, breast, and colon cancers.

- Hospital-Centric Care: Hospitals provide integrated oncology services—from surgery and chemotherapy to radiation therapy and emergency care, ensuring comprehensive cancer management.

- AI & Digital Health in Oncology: Use of artificial intelligence, big data, and analytics in drug discovery, diagnostics, and treatment planning, accelerating the development of new therapies.

Market Dynamic

Global Oncology Market is poised for notable growth in the forthcoming years. The global oncology market consists of various factors that shape this market. The rising number of cancer patients pushed by the ageing population is boosting the growth of this market. Technological breakthroughs in cancer diagnostics and treatments, such as immunotherapy and precision medicine, contribute to this ever-evolving market. Additionally, increased awareness, early detection initiatives, and personalized medicine trends amplify the demand for oncology products and services. Collaborations and partnerships between pharmaceutical companies, academic institutions, and research organizations fuel research endeavours and clinical trials.

Regulatory frameworks, reimbursement policies, and healthcare infrastructure variations across regions also influence market dynamics. Additionally, economic factors, including healthcare expenditure and funding availability, further impact this market's trajectory, creating a landscape characterized by constant innovation, strategic alliances, and responsiveness to emerging healthcare challenges.

Research Scope and Analysis

By Treatment & Diagnosis

In this Treatment & Diagnosis segmentation, cancer diagnostics dominates this segment as it holds 58.6% of the market share in 2023 and is expected to show significant growth in the upcoming years of 2023 to 2032. It dominates this segment as diagnosing cancer at an early stage is crucial for successful treatment outcomes. Cancer diagnostics play a vital role in the early detection of cancer cells, allowing for timely treatment that potentially allows healthcare professionals to customize an effective treatment plan for the patient. There are many screening programs that can detect cancer cells in their early stages among at-risk populations. These screening efforts heavily rely on diagnostic tools such as imaging (e.g., mammography, colonoscopy) and laboratory tests (e.g., Pap smears, PSA tests) to identify potential cases before symptoms of the cancer manifest.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Moreover, cancer diagnostics in recent times has seen rapid advancements in diagnostic technologies such as imaging techniques, molecular diagnostics, and liquid biopsies. These innovations and new advancements in these technologies enable more accurate and precise cancer detection, contributing to the dominance of cancer diagnostics in this segment.

By Cancer Type

Lung cancer dominates the cancer type segment in 2023 and is expected to grow significantly in the upcoming years of 2023 to 2032. Lung cancer is one of the leading causes of cancer-related deaths and is the most commonly diagnosed cancer globally. Its high incidence and the rising number of cancer patients contribute to its dominance in the global oncology market. Tobacco smoking is a major cause of lung cancer, and the widespread prevalence of smoking habits globally contributes to the rising cases of lung cancer.

Many groups and organizations are working and putting efforts to raise awareness among individual about the harmful effects of smoking and tobacco on their lungs. Lung cancer's association with smoking has prompted public health campaigns and initiatives to reduce tobacco use, emphasizing the importance of prevention and early detection. These efforts further underscore the significance of lung cancer in the broader context of public health. Lung cancer poses multiple challenges to the healthcare industry, if it's not detected in the early stages, it is hard to treat in the chronic stage.

Patients diagnosed with lung cancer are often in the advanced stages, making their treatment more complex and challenging. The need for advanced diagnostic tools for the identification of cancer cells, such as imaging and molecular testing, adds to the significance of lung cancer in the global oncology market. This condition affects a large portion number of individuals, which is why it requires extensive research on diagnostics methods and treatment plans.

By End-User

Hospitals dominate the oncology market in terms of end users due to their central role in cancer diagnosis, treatment, and patient care. They also hold 51.2% of the market share in 2023 and are expected to show substantial growth in the upcoming years of 2023 to 2032. Hospitals provide comprehensive and integrated services to cancer patients, offering a wide range of services from diagnosis and surgery to chemotherapy, radiation therapy, and follow-up care. This holistic approach to cancer treatment is crucial in managing the complex and multifaceted nature of cancer. Hospitals and the healthcare sector consist of healthcare professionals, including oncologists, surgeons, radiologists, pathologists, nurses, and support staff. Their collaborative coordinated approach allows for specialized care, ensuring that patients receive proper treatment for their conditions.

Moreover, Hospitals often have advanced diagnostic facilities, including imaging technologies, pathology labs, and genetic testing capabilities that enable an accurate and timely cancer diagnosis which is essential in determining the appropriate treatment strategies for the patient. Also, hospitals are equipped with all the necessary equipment to handle emergencies and critical situations, making them essential for cancer patients who may require urgent medical attention. The availability of intensive care units (ICUs) and emergency services is crucial in managing potential complications during cancer treatment.

The Oncology Market Report is segmented on the basis of the following:

By Treatment & Diagnostics

- Cancer Diagnostics

- Cancer Treatment

By Cancer Type

- Lung Cancer

- Prostate Cancer

- Colon & Rectal Cancer

- Gastric Cancer

- Brest Cancer

- Others

By End-User

- Hospitals

- Diagnostics Laboratories

- Diagnostic Imaging Centers

- Academic & Research Institutes

- Specialty Clinics

- Others

Regional Analysis

North America dominates the global oncology market as it accounts for 47.4% of the market share in 2023 and is expected to show subsequent growth in the upcoming years of 2023 to 2032. North America has a well-developed ecosystem of world-renowned academic institutes, medical centres, universities, and life science societies that are making major contributions to the growth of the global oncology market. These research institutions are collectively contributing to the development of new cancer treatments and therapies, which play a crucial role in the growth of this market.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Furthermore, this region is the home of many leading pharmaceutical and biotechnology companies, which are actively engaged in drug development & often collaborate with diagnostic firms to create new cancer treatments. The strong presence of these pharmaceutical companies in this region highly contributes to its leading position in the global oncology market.

This region also has a well-established regulatory framework for the companion diagnostics market such as the U.S. Food and Drug Administration (FDA), which provides guidelines and pathways for the approval of new treatments and therapies for cancer patients along with specific drugs, making it easier for pharmaceutical companies to bring their products to market. While North America is currently dominating the global oncology market, other regions, including Europe and Asia, are also gaining prominence.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive landscape of the global oncology market has experienced dynamic shifts amid the COVID-19 pandemic and economic recession. As many major established pharmaceutical companies continue to dominate, leveraging their research and development capabilities to introduce novel cancer therapies. Emerging biotechnology firms have also played a significant role, in driving innovation and challenging traditional treatment paradigms. Collaboration and partnerships between pharmaceutical giants and smaller biotech companies have become more prevalent, fostering a synergistic approach to drug development.

The emphasis on precision medicine and targeted therapies has intensified competition, with companies striving to create therapies tailored to specific cancer types and genetic profiles. Moreover, the rise of immunotherapy and gene therapies has opened new avenues for competition, with companies vying to secure leadership positions in these groundbreaking fields. The pandemic has accelerated digital transformation, prompting companies to invest in technologies such as artificial intelligence and data analytics for drug discovery and development. As the market continues to evolve, strategic alliances, technological advancements, and a focus on patient-centric approaches will most likely to define the competitive dynamics in the oncology sector.

Some of the prominent players in the Global Oncology Market are

- F. Hoffmann-La Roche

- Merck & Co. Inc.

- Abbott

- Pfizer

- Bayer Ag

- Thermo Fischer Scientific

- Gilead Science Inc.

- GE Healthcare

- Biocartis

- AstraZeneca

- Bio-Rad Laboratories

- Other Key Players

Recent Developments

- September 2025: GSK re-entered India's oncology market by launching two precision cancer therapies — Jemperli (dostarlimab) and Zejula (niraparib) — targeting certain gynecological cancers.

- May 2025: NeoGenomics unveiled its PanTracer Family of genomic profiling tests (including tissue-based, liquid biopsy, and HRD variants) and the Paletrra spatial proteomics platform at ASCO 2025, aimed at improving diagnostics for advanced solid tumors and the tumor microenvironment.

- September 2025: Genmab agreed to acquire Merus, a biotech focused on cancer drug petosemtamab, for approximately US$8 billion. This move gives Genmab access to a late-stage oncology asset in head-and-neck cancer, with possible expansion into colorectal cancer.

- March 2025: Sun Pharmaceutical acquired Checkpoint Therapeutics (USA) for about US$355 million, gaining UNLOXCYT (cosibelimab), a treatment for advanced skin cancer, thus strengthening its immuno-oncology offerings.

Report Details

| Report Characteristics |

| Market Size (2023) |

USD 234.6 Bn |

| Forecast Value (2032) |

USD 533.2 Bn |

| CAGR (2023-2032) |

9.6% |

| Historical Data |

2017 - 2022 |

| Forecast Data |

2023 - 2032 |

| Base Year |

2022 |

| Estimate Year |

2023 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Treatment & Diagnostics (Cancer Diagnostics and Cancer Treatment), By Cancer Type (Lung Cancer, Prostate Cancer, Colon & Rectal Cancer, Gastric Cancer, Brest Cancer and Others), By End-User (Hospitals, Diagnostics Laboratories, Diagnostic Imaging Centers, Academic & Research Institutes, Specialty Clinics and Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

F. Hoffmann-La Roche, Merck & Co. Inc., Abbott, Pfizer, Bayer Ag, Thermo Fischer Scientific, Gilead Science Inc., GE Healthcare, Biocartis, AstraZeneca, Bio-Rad Laboratories, and Other Key Players |

Frequently Asked Questions

How big is the Global Oncology Market?

▾ The Global Oncology Market size is estimated to have a value of USD 234.6 billion in 2023 and is

expected to reach USD 533.2 billion by the end of 2032.

Which region accounted for the largest Global Oncology Market?

▾ North America has the largest market share for the Global Oncology Market with a share of about 47.4%

in 2023.

Who are the key players in the Global Oncology Market?

▾ Some of the major key players in the Global Oncology Market are F. Hoffmann-La Roche, Merck & Co.

Inc., Abbott, Pfizer, Bayer Ag, Thermo Fischer Scientific, Gilead Science Inc., GE Healthcare, Biocartis,

AstraZeneca, Bio-Rad Laboratories and many others.

What is the growth rate in the Oncology Market?

▾ The market is growing at a CAGR of 9.6 percent over the forecasted period.