Market Overview

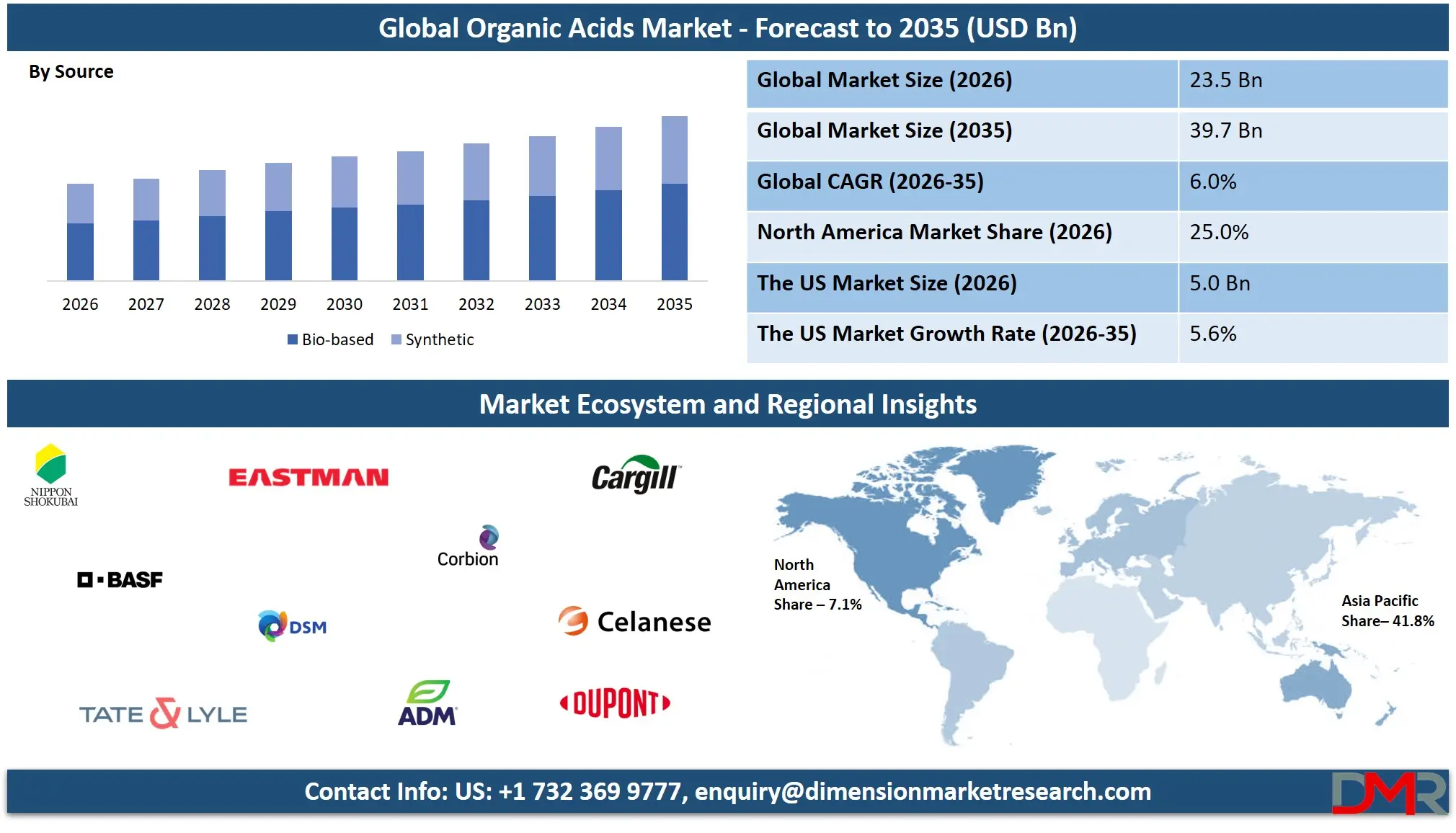

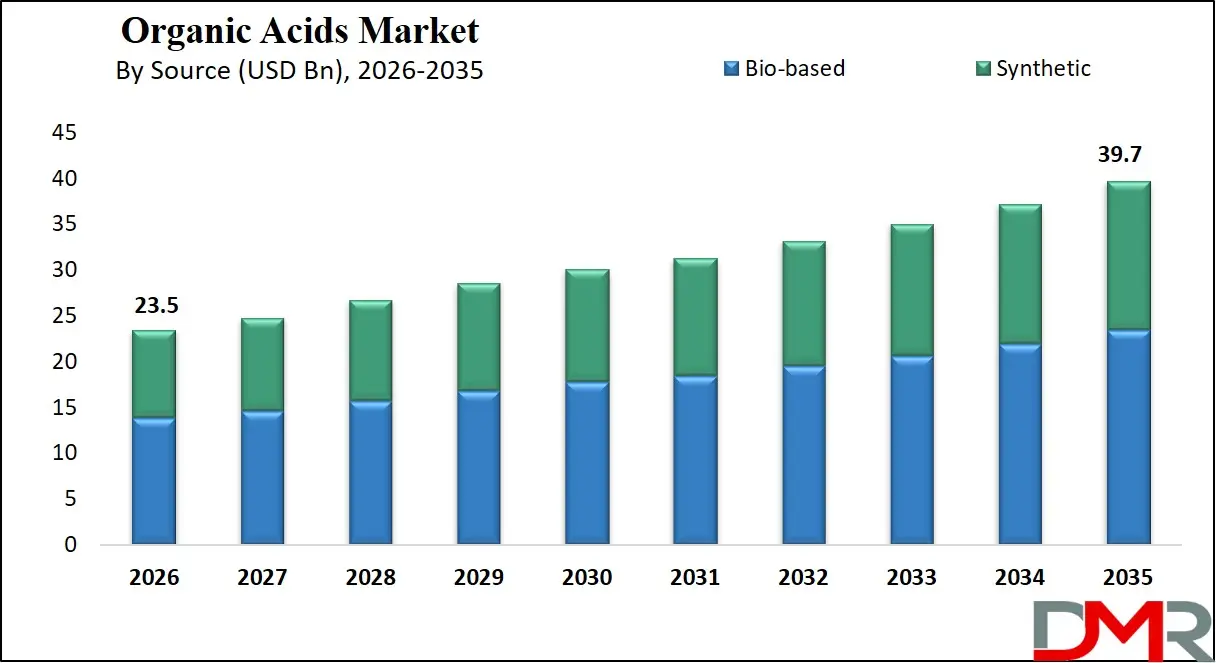

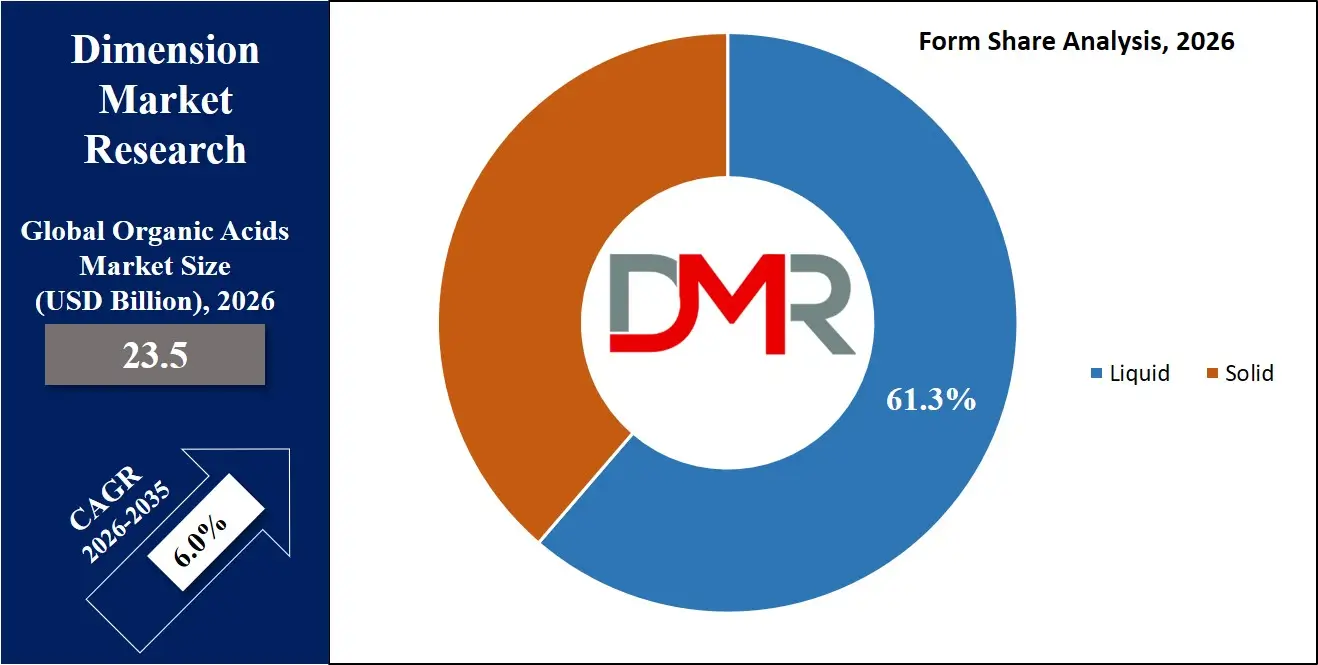

The Global Organic Acids Market size is projected to reach USD 23.5 billion in 2026 and grow at a compound annual growth rate of 6.0% to reach a value of USD 39.7 billion in 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Organic acids are naturally occurring or synthetically produced compounds characterized by the presence of one or more carboxyl groups. These acids are widely used as intermediates, preservatives, acidulants, and pH regulators across numerous industries including food processing, pharmaceuticals, animal feed, agriculture, and chemical manufacturing. Common organic acids include acetic, citric, lactic, and formic acids, which are derived either from fermentation processes using biomass or through petrochemical synthesis. Their functional properties such as antimicrobial effects, acidity regulation, and flavor enhancement make them essential components in industrial formulations. The versatility of these compounds has positioned them as vital building blocks within the broader biochemical and specialty chemicals ecosystem.

Growing demand for natural food preservatives, sustainable production methods, and bio-based chemical alternatives is influencing the broader adoption of organic acids across global industries. Fermentation technologies, biotechnology innovations, and enzyme engineering are enabling higher-efficiency production methods while reducing environmental impact. As industries shift toward green chemistry and circular economy models, bio-based organic acids are gaining increasing preference over petrochemical alternatives. This transformation is especially visible in food preservation, feed additives, and pharmaceutical manufacturing, where regulatory bodies are encouraging safer and more sustainable ingredients.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Several notable industry movements are shaping the trajectory of the organic acids landscape. Companies are expanding fermentation capacity, investing in biotechnology platforms, and forming strategic partnerships to strengthen supply chains. Innovation in microbial fermentation and waste-based feedstock utilization has improved yield efficiency and cost competitiveness. In addition, increasing investments in bio-refineries and sustainable chemical manufacturing infrastructure are enabling large-scale production of organic acids. These developments are reinforcing the role of organic acids as critical ingredients in the evolving bio-economy and sustainable chemical industry.

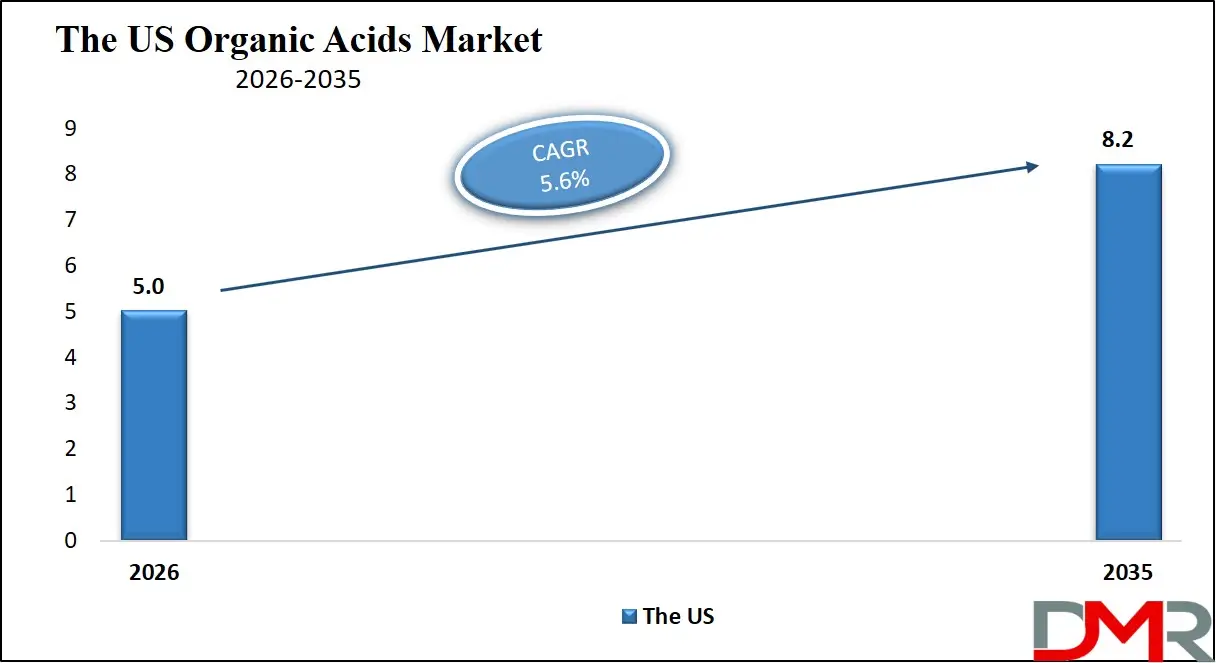

The US Organic Acids Market

The US Organic Acids Market size is projected to reach USD 5.0 billion in 2026 at a compound annual growth rate of 5.6% over its forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US represents a mature and technologically advanced market for organic acids due to its strong food processing, pharmaceutical, and biotechnology sectors. High consumption of processed foods, beverages, and dietary supplements supports significant demand for citric, lactic, and acetic acids. Advanced fermentation technologies and established biotechnology infrastructure enable domestic manufacturers to maintain competitive production capabilities. Regulatory oversight from agencies such as the Food and Drug Administration encourages the use of safe food preservatives and additives, which further supports organic acid utilization. Additionally, the expansion of bio-based chemical production and sustainable manufacturing initiatives is encouraging investment in fermentation-derived organic acids. Increasing adoption in animal nutrition, pharmaceutical formulations, and industrial chemicals also continues to stimulate market growth across the United States.

Europe Organic Acids Market

Europe Organic Acids Market size is projected to reach USD 4.2 billion in 2026 at a compound annual growth rate of 5.5% over its forecast period.

Europe remains a prominent market for organic acids, driven by strong regulatory frameworks, sustainability initiatives, and advanced food and beverage industries. Regional policies such as the European Green Deal and circular economy strategies are encouraging the shift toward bio-based chemicals and fermentation-derived ingredients. Organic acids are widely used in food preservation, pharmaceutical manufacturing, and industrial processing across countries such as Germany, France, and the Netherlands. The region's strong biotechnology ecosystem supports innovation in microbial fermentation and green chemical production. Additionally, the rising demand for clean-label food products has accelerated the adoption of natural preservatives such as citric and lactic acids. Increasing research investments, collaborations between biotechnology firms, and sustainability-focused manufacturing practices are further strengthening Europe's position within the global organic acids landscape.

Japan Organic Acids Market

Japan Organic Acids Market size is projected to reach USD 1.6 billion in 2026 at a compound annual growth rate of 5.4% over its forecast period.

Japan's organic acids market is supported by its advanced chemical industry, strong food manufacturing sector, and growing pharmaceutical research ecosystem. The country emphasizes high-quality ingredients and precision chemical production, which encourages the use of organic acids in food processing, nutraceuticals, and pharmaceuticals. Urbanization, changing dietary habits, and demand for packaged foods are increasing the utilization of acidulants and preservatives such as citric and lactic acids. Government initiatives promoting biotechnology research and sustainable chemical production are encouraging innovation in fermentation-based organic acids. Japan's strong industrial infrastructure and emphasis on technological efficiency provide opportunities for advanced production methods. However, challenges such as limited domestic raw materials and reliance on imported feedstocks can influence supply chain dynamics within the country.

Organic Acids Market: Key Takeaways

- Market Growth: The Organic Acids Market size is expected to grow by USD 15.0 billion, at a CAGR of 6.0%, during the forecasted period of 2027 to 2035.

- By Source: The bio-based segment is anticipated to get the majority share of the Organic Acids market in 2026.

- By Form: The liquid segment is expected to get the largest revenue share in 2026 in the Organic Acids market.

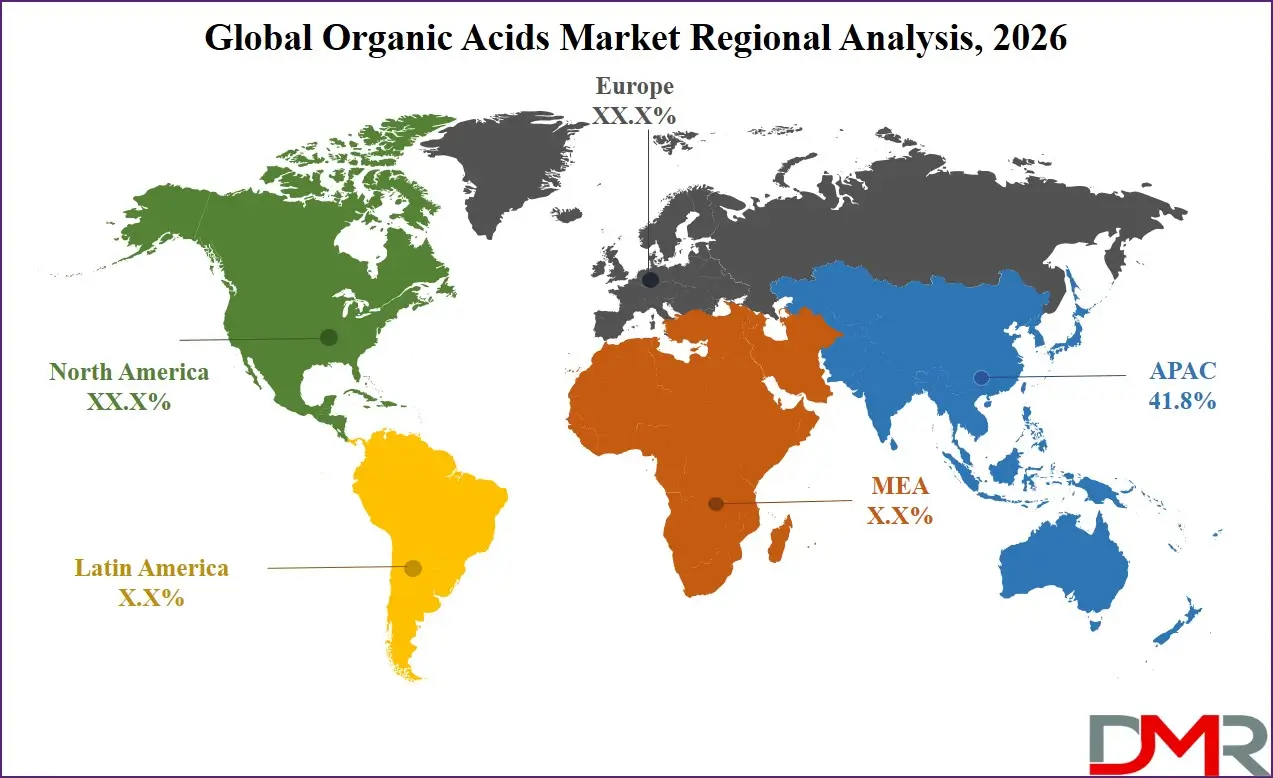

- Regional Insight: Asia Pacific is expected to hold a 41.8% share of revenue in the global Organic Acids market in 2026.

- Use Cases: Some of the use cases of Organic Acids include food preservation, personal care products, and more.

Organic Acids Market: Use Cases:

- Food Preservation: Organic acids such as citric, lactic, and acetic acids are widely used as preservatives in food and beverages. They inhibit microbial growth, enhance shelf life, and maintain product safety while supporting clean-label formulations.

- Animal Feed Acidification: In livestock nutrition, organic acids act as feed acidifiers that improve digestion and nutrient absorption. They also help control pathogenic bacteria in animal feed, supporting better animal health and productivity.

- Pharmaceutical Formulations: Organic acids function as excipients and active ingredients in drug formulations. They help stabilize medicines, adjust pH levels, and improve the solubility and bioavailability of pharmaceutical compounds.

- Industrial Chemical Intermediates: Several organic acids serve as essential intermediates in the production of plastics, solvents, coatings, and synthetic fibers. Their chemical properties enable efficient synthesis of complex industrial compounds.

- Personal Care Products: In cosmetics and skincare products, organic acids regulate pH levels and provide exfoliating or antimicrobial benefits. Lactic acid and citric acid are commonly used in skincare formulations.

- Agricultural Applications: Organic acids are used in crop protection formulations and silage preservation. They help prevent microbial spoilage in stored animal feed and improve agricultural productivity.

- Textile and Cleaning Solutions: These acids are utilized in textile processing and industrial cleaning agents due to their ability to regulate pH, remove impurities, and improve processing efficiency.

Stats & Facts

- United States Department of Agriculture (USDA) reports that the U.S. food processing industry accounted for over 17% of total manufacturing shipments in 2024, significantly supporting demand for food additives including organic acids.

- European Commission stated that the EU biotechnology sector received over EUR 13 billion (USD 15 billion) in public and private investments in 2024, strengthening bio-based chemical production.

- Food and Agriculture Organization (FAO) indicates global meat production reached approximately 366 million tonnes in 2024, increasing the need for feed acidifiers used in animal nutrition.

- International Energy Agency (IEA) noted that bio-based chemical production capacity increased by around 6% globally in 2024 due to expanding fermentation technologies.

- U.S. Food and Drug Administration (FDA) reported in 2025 that more than 3,000 food additives are approved for use in processed foods, including numerous organic acid compounds.

- Eurostat recorded that the European food and beverage manufacturing sector generated over EUR 1.2 trillion (USD 1.4 trillion) in turnover in 2024, driving ingredient demand.

- Japan Ministry of Economy, Trade and Industry (METI) reported Japan's chemical industry produced over JPY 45 trillion (USD 283.9 billion) worth of chemical products in 2024.

- Organisation for Economic Co-operation and Development (OECD) estimated that bio-based chemicals could account for up to 20% of specialty chemical production by 2030.

- World Health Organization (WHO) reported that antimicrobial preservatives are used in over 60% of packaged food products globally in 2025.

- International Feed Industry Federation (IFIF) reported global compound feed production exceeded 1.3 billion metric tonnes in 2024.

- United Nations Industrial Development Organization (UNIDO) stated that global chemical manufacturing output increased by around 4.2% in 2024.

- International Trade Administration (ITA) recorded that the U.S. chemical sector contributed approximately USD 500 billion to GDP in 2024.

Market Dynamic

Driving Factors in the Organic Acids Market

Growing Demand for Natural Food Preservatives

The increasing consumer preference for clean-label and natural food ingredients is a significant driver supporting the demand for organic acids. Food manufacturers are actively replacing synthetic preservatives with naturally derived compounds that provide antimicrobial and pH-regulating properties. Organic acids such as citric, lactic, and acetic acids help extend shelf life, enhance flavor stability, and maintain food safety without introducing harmful chemical additives. As global consumption of processed and packaged foods continues to rise, food companies are increasingly integrating these acids into their formulations. Regulatory agencies across several regions also encourage the use of safe and naturally derived additives, further strengthening the adoption of organic acids in the food and beverage sector.

Expansion of Bio-Based Chemical Production

The growing transition toward sustainable chemical manufacturing is another important factor accelerating the organic acids industry. Biotechnology advancements have enabled efficient fermentation-based production methods using renewable feedstocks such as corn, sugarcane, and agricultural waste. Bio-refineries are being developed to convert biomass into organic acids and other specialty chemicals, reducing dependence on petrochemical processes. This shift aligns with environmental policies aimed at reducing greenhouse gas emissions and promoting circular economy principles. As industries adopt green chemistry practices, demand for fermentation-derived organic acids continues to grow across pharmaceuticals, agriculture, and industrial applications, strengthening their role in the sustainable chemicals ecosystem.

Restraints in the Organic Acids Market

High Production Costs for Bio-Based Organic Acids

Despite strong demand, the production of bio-based organic acids often involves higher operational and capital costs compared with petrochemical-derived alternatives. Fermentation processes require specialized equipment, controlled environments, and microbial cultures that must be carefully maintained. Feedstock costs, purification processes, and energy consumption can further increase manufacturing expenses. These factors may limit adoption among small-scale manufacturers or industries operating with narrow margins. Additionally, fluctuations in agricultural feedstock availability can influence production stability. Although technological improvements are gradually reducing costs, price competitiveness with synthetic alternatives remains a challenge for several producers within the market.

Supply Chain Limitations and Raw Material Dependency

The organic acids industry is closely linked to agricultural raw materials such as corn, molasses, and sugarcane used in fermentation processes. Variability in crop yields, climate conditions, and global trade dynamics can affect feedstock availability and pricing. Supply chain disruptions may influence production capacity and lead to price volatility for certain acids. Additionally, limited infrastructure for large-scale fermentation facilities in developing regions may restrict supply expansion. These constraints can impact manufacturers' ability to maintain stable production levels and meet growing industrial demand, particularly in markets where domestic feedstock supply is insufficient.

Opportunities in the Organic Acids Market

Expansion of Sustainable Biorefineries

The rapid development of bio-refinery infrastructure presents significant opportunities for the organic acids industry. Bio-refineries are capable of converting biomass into multiple high-value products including organic acids, biofuels, and specialty chemicals. This integrated production model enhances resource efficiency and reduces waste. Governments and private investors are increasingly funding projects aimed at expanding sustainable chemical manufacturing. As these facilities scale up, they can significantly increase the availability of fermentation-derived organic acids while lowering production costs. This development creates new growth potential for suppliers serving food, pharmaceutical, and industrial chemical markets.

Increasing Applications in Pharmaceutical and Nutraceutical Products

Organic acids are gaining greater importance in pharmaceutical and nutraceutical applications due to their role in drug stabilization, formulation, and pH control. The global rise in healthcare spending and pharmaceutical production is increasing demand for excipients and functional ingredients used in medicine manufacturing. Additionally, organic acids are widely incorporated into dietary supplements, probiotic formulations, and functional foods. As pharmaceutical companies continue to develop advanced therapies and nutraceutical products, the demand for high-purity organic acids is expected to expand significantly across multiple healthcare applications.

Trends in the Organic Acids Market

Adoption of Advanced Fermentation Technologies

Modern fermentation technologies are transforming the production landscape for organic acids. Biotechnology companies are using genetically engineered microorganisms, enzyme optimization, and precision fermentation techniques to increase production yields and reduce processing time. These innovations allow manufacturers to produce organic acids more efficiently while lowering environmental impact. The integration of automation and digital monitoring systems in fermentation facilities also enhances process control and quality assurance. As these technological advancements continue to evolve, fermentation-based organic acids are becoming increasingly competitive with petrochemical alternatives.

Increasing Shift Toward Green Chemistry

Green chemistry principles are playing a major role in shaping the future of organic acid production and applications. Industries are actively seeking environmentally friendly chemical solutions that minimize waste generation and energy consumption. Organic acids derived from renewable feedstocks align well with these sustainability goals. Companies are redesigning manufacturing processes to reduce carbon emissions and utilize biodegradable intermediates. This shift is particularly evident in sectors such as food processing, personal care, and agriculture, where environmentally responsible ingredients are becoming a key requirement for both regulatory compliance and consumer acceptance.

Impact of Artificial Intelligence in Organic Acids Market

- Process Optimization: AI systems analyze fermentation data in real time to optimize temperature, pH levels, and microbial activity, improving organic acid production efficiency and yield.

- Predictive Maintenance: Machine learning algorithms monitor industrial equipment and predict failures before they occur, reducing downtime in fermentation plants and chemical production facilities.

- Feedstock Optimization: AI models evaluate different biomass feedstocks and processing conditions to determine the most efficient raw material combinations for organic acid production.

- Quality Control Automation: AI-powered imaging and analytical systems detect impurities or inconsistencies during production, ensuring high-purity organic acid products.

- Supply Chain Forecasting: AI-based demand forecasting tools help manufacturers predict fluctuations in industrial demand and manage inventory more effectively.

- Research & Development Acceleration: Artificial intelligence assists researchers in identifying new microbial strains and fermentation pathways that enhance organic acid productivity.

- Energy Efficiency Improvement: AI-driven process simulations allow companies to reduce energy consumption in chemical production facilities.

- Market Demand Prediction: Machine learning models analyze industry data and consumer trends to anticipate demand for organic acids across food, pharmaceutical, and industrial sectors.

- Waste Reduction: AI-enabled monitoring systems help minimize by-products and optimize resource utilization in bio-refinery operations.

Research Scope and Analysis

By Type Analysis

Acetic acid represents the dominant segment within the organic acids market due to its extensive use across food preservation, chemical manufacturing, textiles, and pharmaceutical applications. It is widely utilized as a key raw material for producing vinyl acetate monomer, purified terephthalic acid, and various acetate esters used in industrial solvents and coatings. In the food and beverage sector, acetic acid functions as a preservative and acidity regulator, particularly in vinegar-based products and pickled foods. Industrial demand remains strong because acetic acid serves as a critical intermediate in multiple chemical production processes. Continuous growth in the chemical manufacturing and food processing sectors has significantly strengthened this segment's position. In addition, the expansion of bio-based acetic acid production using fermentation technologies is improving sustainability and reducing environmental impact. These combined factors are expected to maintain the segment's strong market position, with acetic acid projected to hold approximately 24.6% of the organic acids market share in 2026, making it the most widely utilized organic acid globally.

Citric acid is emerging as the fastest-growing segment within the organic acids market due to its widespread application in food, beverages, pharmaceuticals, and personal care products. It is commonly used as an acidulant, preservative, and flavor enhancer in carbonated drinks, fruit-based beverages, candies, and processed foods. The increasing global demand for packaged foods and beverages has accelerated the consumption of citric acid. In addition, the compound is widely used in pharmaceutical formulations to regulate pH levels and stabilize active ingredients. Growth in the personal care sector has also increased its use in skincare products due to its exfoliating and antioxidant properties. The expansion of fermentation-based production methods using renewable feedstocks further supports its rapid adoption, making citric acid one of the most versatile and rapidly expanding organic acids across industries.

By Source Analysis

Bio-based organic acids produced through fermentation processes represent the leading source segment in the market. This production method uses renewable feedstocks such as corn, sugarcane, molasses, and agricultural waste to produce acids through microbial fermentation. The increasing emphasis on sustainability and environmental protection has significantly boosted demand for bio-based chemicals. Governments and regulatory authorities across multiple regions are encouraging the development of renewable chemical production technologies that reduce greenhouse gas emissions and minimize petrochemical dependence. Fermentation-derived organic acids are widely used in food, pharmaceutical, and animal feed applications due to their natural origin and high purity levels. Technological advancements in biotechnology and microbial engineering have improved fermentation yields, reducing production costs and increasing scalability. These advantages have strengthened the dominance of bio-based production, which is expected to account for approximately 58.9% of the organic acids market share in 2026, making it the preferred production method for many manufacturers.

Synthetic organic acids derived from petrochemical processes remain an important segment due to their cost efficiency and large-scale industrial production capabilities. These acids are commonly used in industrial chemical manufacturing, textiles, plastics, and coatings where high production volumes are required. Petrochemical-based production often offers consistent quality and lower manufacturing costs compared to some fermentation-based alternatives. Additionally, certain specialized acids used in chemical intermediates are more efficiently produced through synthetic methods. As industrial chemical demand continues to grow globally, synthetic organic acids maintain strong demand in sectors that prioritize cost efficiency and high production capacity. Although sustainability concerns are encouraging a shift toward bio-based alternatives, synthetic acids still play a crucial role in meeting large-scale industrial requirements.

By Form Analysis

Liquid organic acids dominate the market due to their ease of handling, faster absorption, and efficient integration into industrial processing systems. Liquid formulations are widely used in food and beverage production, animal feed acidification, and chemical manufacturing processes. In livestock nutrition, liquid acids are commonly added directly into feed mixtures or water systems to improve digestion and control harmful bacteria. In industrial environments, liquid organic acids can be easily transported, blended, and stored using existing chemical handling infrastructure. Their rapid solubility and consistent concentration levels make them ideal for large-scale production environments. Furthermore, liquid acids are frequently preferred in pharmaceutical manufacturing and fermentation processes because they can be easily incorporated into formulations. Owing to these advantages, the liquid segment continues to dominate the market and is projected to hold around 61.3% of the organic acids market share in 2026.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Solid organic acids, available in powder or granule form, are witnessing rapid growth due to their convenience in packaging, transportation, and long-term storage. These forms are particularly popular in animal feed additives, nutraceutical supplements, and food ingredient manufacturing. Powdered acids can be easily blended with dry feed formulations and processed food ingredients, improving stability and shelf life. In addition, solid acids are widely used in pharmaceutical tablets, dietary supplements, and effervescent formulations. Their extended shelf life and reduced risk of leakage during transportation make them attractive for international trade and distribution. As global demand for packaged foods, nutraceuticals, and feed additives continues to increase, the adoption of solid organic acid formulations is expected to grow steadily.

By Application Analysis

The food and beverage industry represents the largest application segment for organic acids due to their essential role in food preservation, flavor enhancement, and acidity regulation. Organic acids such as citric, acetic, and lactic acids are commonly used as acidulants, preservatives, and flavor enhancers in processed foods, beverages, dairy products, and confectionery items. They help extend product shelf life by inhibiting microbial growth while maintaining the desired taste and texture. Increasing global consumption of packaged foods and ready-to-drink beverages has significantly boosted demand for these functional ingredients. Additionally, the rising preference for natural preservatives and clean-label products is encouraging manufacturers to replace synthetic additives with fermentation-derived organic acids. Due to their wide applicability and regulatory approval in food processing, the food and beverage segment is expected to account for approximately 38.7% of the organic acids market share in 2026, maintaining its leadership position.

The pharmaceutical sector is emerging as the fastest-growing application area for organic acids due to their critical role in drug formulation and medical research. Organic acids are widely used as excipients, buffering agents, stabilizers, and active pharmaceutical ingredients. They help regulate pH levels, improve drug solubility, and enhance the bioavailability of medications. The rapid expansion of the global pharmaceutical industry, increasing demand for nutraceutical supplements, and ongoing research into new therapeutic formulations are driving the demand for high-purity organic acids. Additionally, advancements in biotechnology and pharmaceutical manufacturing are enabling the development of specialized acid-based compounds used in advanced drug delivery systems.

By End-Use Industry Analysis

The food processing industry remains the largest end-use sector for organic acids due to their widespread use in food preservation, flavor enhancement, and product stabilization. Organic acids play an important role in maintaining food safety by inhibiting microbial growth and extending product shelf life. Processed foods such as baked goods, dairy products, beverages, sauces, and ready-to-eat meals frequently incorporate citric, lactic, and acetic acids. The rising global demand for convenience foods and packaged products has further strengthened the use of these acids in industrial food production. In addition, increasing regulatory approvals for natural preservatives have encouraged food manufacturers to adopt fermentation-derived acids. As the global food processing industry continues to expand with urbanization and changing lifestyles, this sector is expected to hold around 34.2% of the organic acids market share in 2026, making it the most significant end-use segment.

The pharmaceutical and nutraceutical industry is witnessing rapid adoption of organic acids due to their functional roles in drug formulation and dietary supplements. These acids act as buffering agents, excipients, stabilizers, and bioavailability enhancers in pharmaceutical products. The growing demand for health supplements, vitamins, and functional foods is also increasing the use of organic acids in nutraceutical formulations. Pharmaceutical manufacturers rely on high-purity acids to maintain the stability and effectiveness of medicines. As global healthcare expenditure continues to rise and pharmaceutical innovation accelerates, this sector is expected to remain one of the fastest expanding end-use industries for organic acids.

The Organic Acids Market Report is segmented on the basis of the following:

By Type

- Acetic Acid

- Citric Acid

- Lactic Acid

- Formic Acid

- Propionic Acid

- Ascorbic Acid

- Fumaric Acid

- Gluconic Acid

- Malic Acid

- Tartaric Acid

- Succinic Acid

- Others

By Source

- Bio-based (Fermentation)

- Synthetic (Petrochemical-based)

By Form

By Application

- Food & Beverages

- Acidulants

- Preservatives

- Flavor Enhancers

- Animal Feed

- Feed Acidifiers

- Preservatives

- Pharmaceuticals

- Drug Formulation

- Excipient Applications

- Industrial Applications

- Chemical Intermediates

- Cleaning Agents

- Textile Processing

- Personal Care & Cosmetics

- pH Regulators

- Skin Care Ingredients

- Agriculture

- Silage Additives

- Crop Protection Formulations

By End-Use Industry

- Food Processing Industry

- Feed Industry

- Pharmaceutical & Nutraceutical Industry

- Chemical & Industrial Manufacturing

- Personal Care & Cosmetics Industry

- Agriculture Industry

Regional Analysis

Leading Region in the Organic Acids Market

Asia Pacific is the leading region in the organic acids market due to its rapidly expanding food processing, chemical manufacturing, and pharmaceutical industries. Countries such as China, India, Japan, and South Korea have established strong industrial bases that consume large volumes of organic acids for various applications. The region's large population and rising urbanization levels are driving significant demand for packaged foods, beverages, and animal protein products, which in turn increases the need for food preservatives and feed additives.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Additionally, Asia Pacific has become a global hub for fermentation-based chemical production due to the availability of agricultural feedstocks and cost-efficient manufacturing infrastructure. Governments across the region are supporting biotechnology research and bio-refinery development to strengthen sustainable chemical production. Owing to these factors, Asia Pacific is expected to account for approximately 41.8% of the global organic acids market share in 2026, making it the dominant regional market.

Fastest Growing Region in the Organic Acids Market

North America is projected to be the fastest-growing region in the organic acids market due to increasing investments in biotechnology, bio-based chemicals, and advanced fermentation technologies. The region has a strong presence of food processing companies, pharmaceutical manufacturers, and chemical producers that rely heavily on organic acids as functional ingredients and industrial intermediates. Growing consumer demand for natural preservatives and clean-label food products is encouraging food manufacturers to adopt fermentation-derived acids. In addition, government initiatives promoting sustainable chemical production and renewable bio-based materials are driving investments in bio-refineries and biotechnology research. The expansion of nutraceutical products, dietary supplements, and pharmaceutical formulations is also contributing to increased demand for high-purity organic acids across the region.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The organic acids market is characterized by intense competition driven by technological innovation, production efficiency, and global supply chain capabilities. Companies operating in this sector focus heavily on expanding fermentation capacities, improving microbial strain efficiency, and developing cost-effective bio-based production processes. Strategic partnerships, joint ventures, and collaborations with biotechnology firms are common strategies used to strengthen research capabilities and accelerate product innovation. Manufacturers are also investing significantly in sustainable chemical production technologies to align with global environmental regulations and consumer demand for eco-friendly products. Market entry barriers are relatively high due to the capital-intensive nature of fermentation facilities, strict regulatory requirements for food and pharmaceutical ingredients, and the need for advanced biotechnology expertise. As competition intensifies, companies are focusing on product diversification, regional expansion, and supply chain optimization to strengthen their market positions.

Some of the prominent players in the global Organic Acids are:

- BASF SE

- Cargill, Incorporated

- Archer Daniels Midland Company

- Celanese Corporation

- Eastman Chemical Company

- DuPont de Nemours, Inc.

- Tate & Lyle PLC

- Corbion N.V.

- DSM-Firmenich AG

- Jungbunzlauer Suisse AG

- Weifang Ensign Industry Co., Ltd.

- RZBC Group Co., Ltd.

- Cofco Biochemical (Anhui) Co., Ltd.

- Henan Jindan Lactic Acid Technology Co., Ltd.

- Nippon Shokubai Co., Ltd.

- Roquette Frères

- Mitsubishi Chemical Group Corporation

- Daicel Corporation

- Chang Chun Group

- LyondellBasell Industries

- Other Key Players

Recent Developments

- In March 2025, BASF announced a strategic investment aimed at strengthening its sustainable organic acid production capabilities in Europe. The company revealed plans to upgrade its biotechnology infrastructure to support the development of fermentation-derived chemical intermediates used in food, pharmaceuticals, and industrial applications. The initiative includes collaborations with biotechnology research institutions to develop high-efficiency microbial strains that improve organic acid yields while reducing energy consumption.

- In January 2025, Cargill announced the expansion of its fermentation-based organic acid production facility in the United States to meet the growing demand for sustainable food ingredients and industrial chemicals. The expansion project includes the installation of advanced fermentation reactors and downstream purification systems designed to improve production efficiency and reduce environmental impact. The upgraded facility will primarily focus on increasing the output of lactic and citric acids used in food preservation, pharmaceuticals, and biodegradable plastics manufacturing.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 23.5 Bn |

| Forecast Value (2035) |

USD 39.7 Bn |

| CAGR (2026–2035) |

6.0% |

| The US Market Size (2026) |

USD 5.0 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Type (Acetic Acid, Citric Acid, Lactic Acid, Formic Acid, Propionic Acid, Ascorbic Acid, Fumaric Acid, Gluconic Acid, Malic Acid, Tartaric Acid, Succinic Acid, Others), By Source (Bio-based (Fermentation), Synthetic (Petrochemical-based)), By Form (Liquid, Solid), By Application (Food & Beverages, Animal Feed, Pharmaceuticals, Industrial Applications, Personal Care & Cosmetics, Agriculture), By End-Use Industry (Food Processing Industry, Feed Industry, Pharmaceutical & Nutraceutical Industry, Chemical & Industrial Manufacturing, Personal Care & Cosmetics Industry, Agriculture Industry) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

BASF SE, Cargill, Incorporated, Archer Daniels Midland Company, Celanese Corporation, Eastman Chemical Company, DuPont de Nemours, Inc., Tate & Lyle PLC, Corbion N.V., DSM-Firmenich AG, Jungbunzlauer Suisse AG, Weifang Ensign Industry Co., Ltd., RZBC Group Co., Ltd., Cofco Biochemical (Anhui) Co., Ltd., Henan Jindan Lactic Acid Technology Co., Ltd., Nippon Shokubai Co., Ltd., Roquette Frères, Mitsubishi Chemical Group Corporation, Daicel Corporation, Chang Chun Group, LyondellBasell Industries, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Organic Acids Market?

▾ The Global Organic Acids Market size is expected to reach USD 23.5 billion by 2026 and is projected to reach USD 39.7 billion by the end of 2035.

Which region accounted for the largest Global Organic Acids Market?

▾ Asia Pacific is expected to have the largest market share in the Global Organic Acids Market, with a share of about 41.8% in 2026.

How big is the Organic Acids Market in the US?

▾ The US Organic Acids market is expected to reach USD 5.0 billion by 2026.

Who are the key players in the Organic Acids Market?

▾ Some of the major key players in the Global Organic Acids Market include BASF, Cargill, ADM, and others.

What is the growth rate in the Global Organic Acids Market?

▾ The market is growing at a CAGR of 6.0 percent over the forecasted period.