What is the Personal Cloud Market Size?

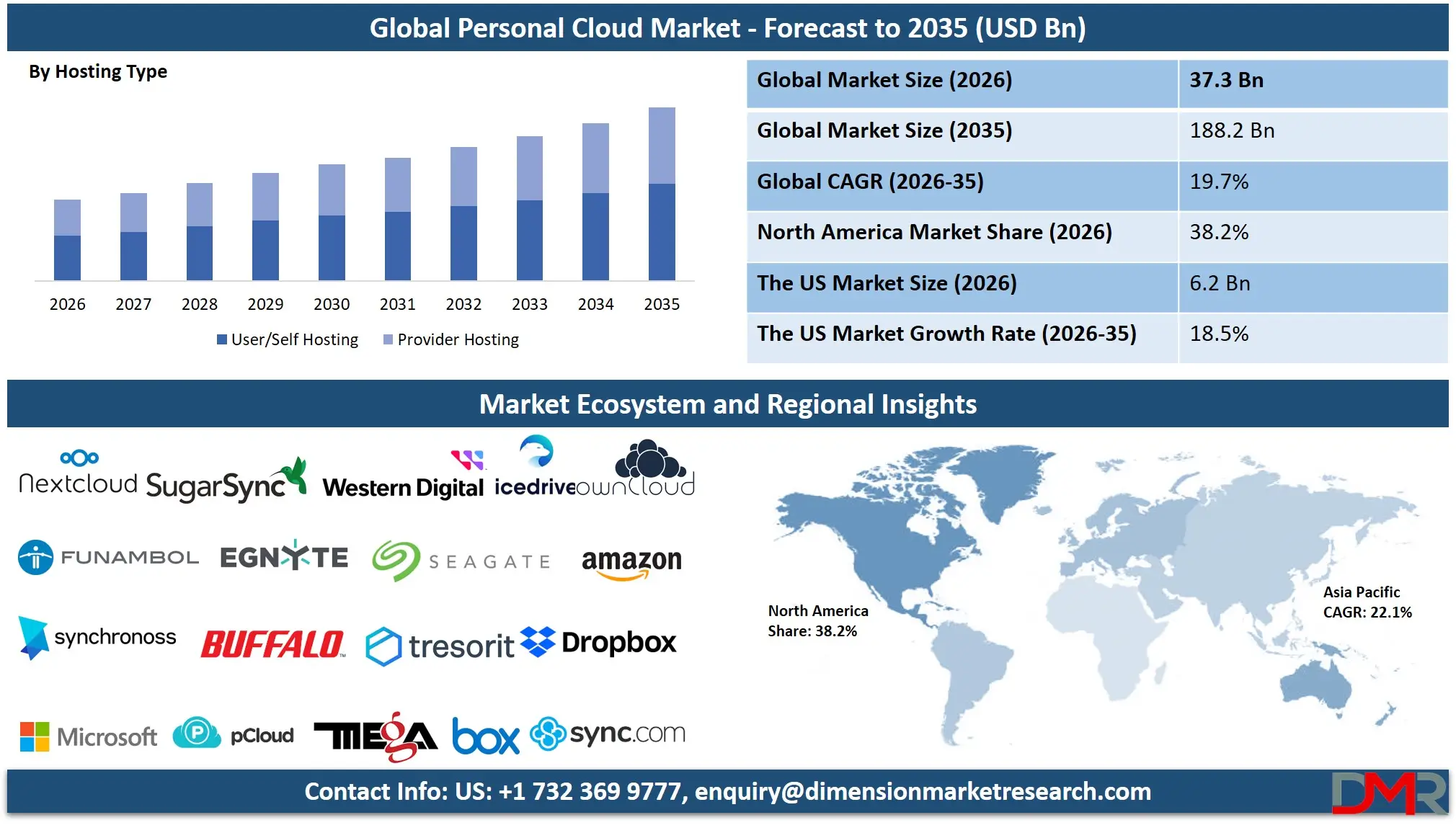

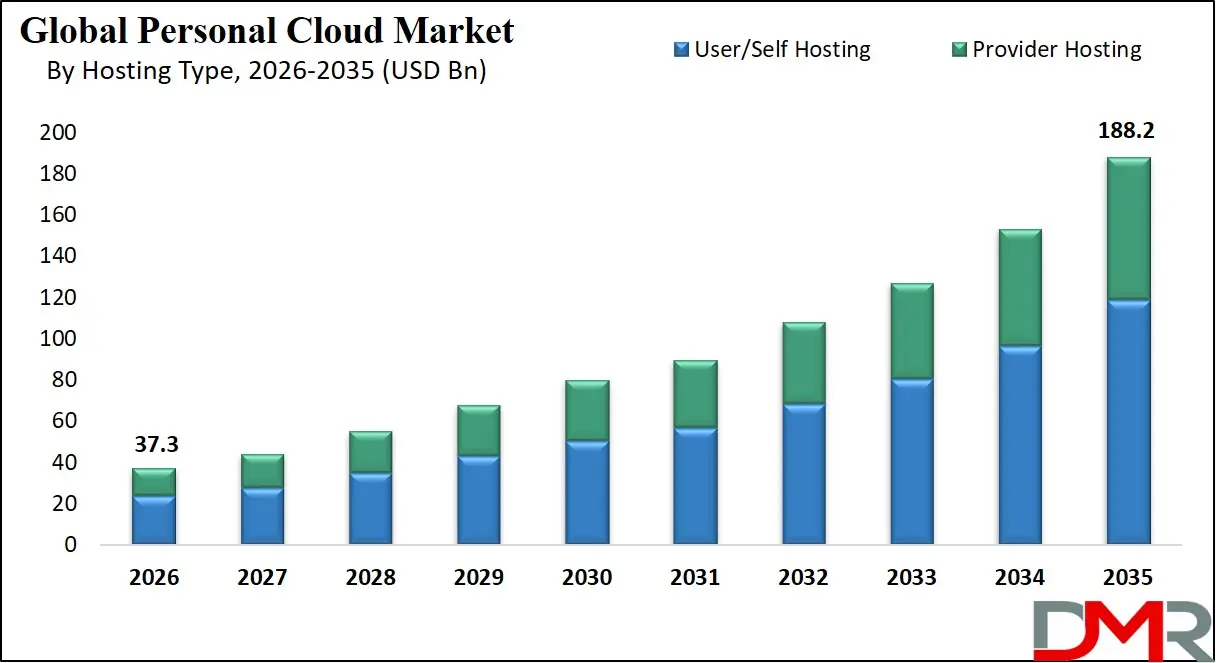

The Global Personal Cloud Market is expected to reach a value of USD 37.3 billion in 2026, and it is further anticipated to reach USD 188.2 billion by 2035, growing at a CAGR of 19.7% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Personal clouds have been witnessing exponential growth in recent times due to the increased use of decentralization in data storage and accessing solutions. This market segment includes personal clouds through online cloud storage, NAS cloud, server-based cloud system, and DIY cloud setups which provide the ability to synchronize, backup and remotely access data from any device.

With the increasing number of mobile phones and smart devices and the exponential production of digital data, there is growing demand for a safe and accessible form of personal cloud storage solutions. Nowadays consumers prefer personal cloud storage solutions over the traditional device-specific solutions, whereas on the other side, enterprises make use of personal cloud technology for enabling remote work and safe file-sharing solutions.

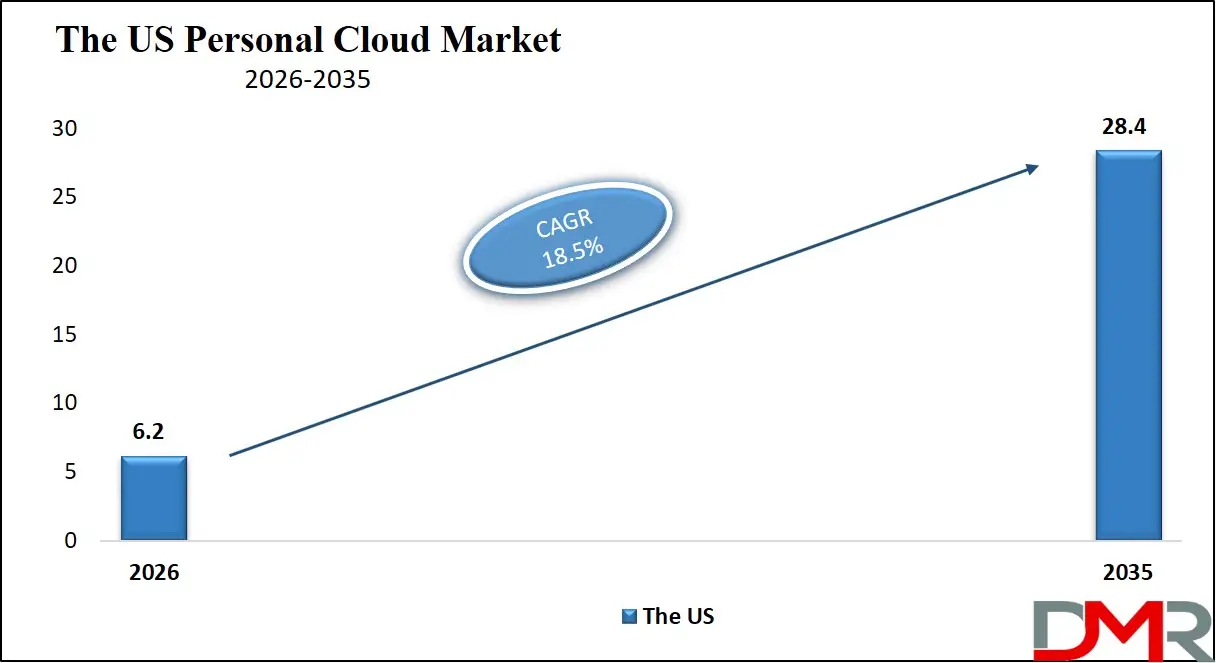

The US Personal Cloud Market

The US Personal Cloud Market is projected to reach USD 6.2 billion in 2026 at a compound annual growth rate of 18.5% over its forecast period, which is further expected to reach a value of USD 28.4 billion by 2035.

The USA remains dominant in terms of personal cloud due to advanced digital infrastructure, widespread use of smartphones, and adoption of smart home appliances. In this regard, there is an active demand for Online Cloud products, which are compatible with leading ecosystems due to Americans' preferences of seamless integration of devices and media streaming.

Moreover, the growing popularity of remote/hybrid work models has triggered enterprise interest in NAS Cloud and Server Device Cloud services that allow secure and easy access to files similar to clouds. Furthermore, increasing concerns about privacy have led to a rising demand for Home-Made Cloud services that enable individuals to manage personal clouds.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Europe Personal Cloud Market

The Europe Personal Cloud Market is estimated to be valued at USD 11.6 billion in 2026 and is further anticipated to reach USD 56.5 billion by 2035 at a CAGR of 19.2%. The European market has been characterized by strict data protection laws, including GDPR, which has created awareness among consumers about data protection and data citizenship. This has increased the demand for Provider Hosting, which includes hosting in EU countries and transparent data handling, as well as User Hosting using NAS Cloud, which keeps the data within the home or office walls. The region is experiencing rapid deployment of personal cloud services in Healthcare and Life Science, as well as Government and Public sectors, where there is an utmost need for compliance and safe document management. In addition, European telecommunication companies are starting to provide personal cloud backups with mobile or internet bundles, thus generating indirect income from the service.

The Japan Personal Cloud Market

The Japan Personal Cloud Market is projected to be valued at USD 4.3 billion in 2026. It is further expected to witness robust growth, holding USD 19.2 billion in 2035 at a CAGR of 18.1%. The Japanese market features certain peculiarities resulting from their cultural approach towards information security, small residential areas, and fondness for advanced consumer electronic products. NAS Cloud products made by local suppliers have found great popularity in households all around Japan, functioning as centralized hubs for audiovisual content and being linked to TVs, gaming consoles, and smartphones. On the other side, the corporate sector, especially in Manufacturing and IT & ITeS, is adopting Server Device Cloud offerings to allow for safe remote access to technical design files and documents without risking confidential information by using third-party cloud services. Finally, owing to the elderly population in Japan, there is considerable demand for personal cloud solutions that can be used to store health-related information and exchange it between family members.

Key Takeaways

- Market Size & Forecast: The Global Personal Cloud market is projected to reach USD 37.3 billion in 2026, expanding dramatically to USD 188.2 billion by 2035, fueled by the exponential growth of digital content creation and the universal need for anywhere, anytime data accessibility.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 19.7%, primarily influenced by growing dependency on multi-device digital life style of consumers, rise in high definition media capture and usage of personal clouds for remote secure collaboration in enterprises.

- Primary Growth Drivers: Major factors driving growth include increasing amounts of user-generated digital contents such as pictures, videos and documents, migration towards device agnostic computing experiences, realization of need for backups, and use of artificial intelligence enabled data management and search capabilities.

- Key Market Trends: Prominent trends that are driving the growth of this market include convergence of personal cloud services with smart homes, creation of Privacy focused Home-Made Clouds, bundled cloud services with telecommunication and device purchase, and use of NAS Cloud for superior performance of local media streaming.

- By Cloud Type Analysis: The Online Cloud will emerge as the leader in terms of consumer adoption due to convenience, while the NAS Cloud and Server Device Cloud will continue to see rapid growth among enterprises and prosumers, who desire sovereignty over their data, lower latencies, and more predictable costs.

- By Hosting Type Analysis: The provider-hosting will poised to dominate this as it is most popular type for regular mass market consumers due to easy deployment and zero maintenance needs. On the other hand, self-hosting has been seeing considerable gains among consumers who seek full control over their data and no recurring payments.

- By User Type Analysis: Consumers represent the largest user segment by volume, due to the necessity of smartphone photo backup and media streaming. The fastest growing segment is the enterprises especially the SMEs which have implemented personal cloud based solutions to share files securely, enable remote working and to manage their data in cost-effective ways.

- By Revenue Type Analysis: Direct Revenue is projected to dominate the revenue type segment as it hold the high market share through subscription fees and premium storage plans are the most common monetization models which offer service providers predictable recurring revenues.

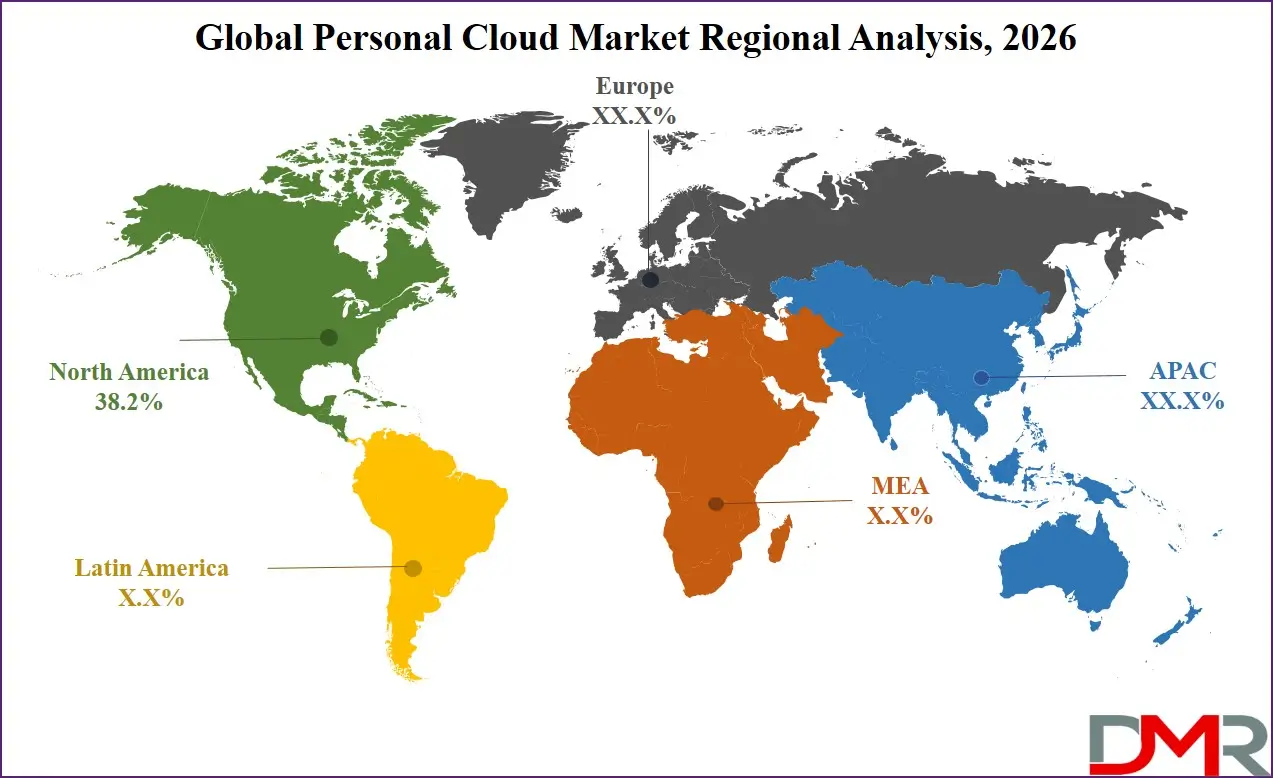

- Regional Leadership: North America is poised to dominate this market with 38.2% of the market share in 2026 as it has an established digital ecosystem, a high disposable income, and the large personal cloud service providers that will capitalize on vast data center infrastructure and brand loyalty.

What is the Personal Cloud Market?

Personal Cloud is a specialty ecosystem of hardware and software, through which individuals and organizations can store, synchronize, stream, and share digital content across various devices and locations without necessarily depending on local device storage. In contrast to traditional cloud computing services, which are used to host enterprise applications, personal cloud services are tailored to user-centric data management, which is the seamless access of photos, videos, music, documents, and personal files on smartphones, tablets, laptops, and smart home devices. These solutions include online cloud solutions provided by major technology companies, NAS (Network Attached Storage) Cloud devices installed on homes and in small offices, server device cloud-based solutions in large business environments, and even home-made cloud solutions developed with open-source software on modified hardware.

Use Cases

- Automated Smartphone Media Backup: The Online Cloud technology serves consumers for automatic backup of data captured via smartphones. Photos and videos captured by smartphones are backed up using Online Cloud technology, and even if the device gets stolen or lost, their user datas remain safe, and space remains available.

- Home Media Server and Streaming Hub: Households deploy NAS Cloud devices as centralized media repositories, store movies, music, and video content to stream it across the home network or anywhere through smart TVs, consoles, tablets, and smartphones, thus saving space locally for more personal usage.

- Secure Remote Work File Access: SMEs and distributed teams use server device cloud and NAS cloud technology for allowing employees access to work data and project files in a secure manner, irrespective of their location. However, all this happens securely without the involvement of a virtual private network (VPN).

- Family Digital Vault and Legacy Planning: Individuals build home-made clouds to create private, encrypted repositories of save valuable family records, financial data, estate planning files and other personal digital data, which are controlled by authorized family members and are not visible to commercial services.

- Telecommunications Value-Added Services: Mobile network operators and internet service providers offer personal cloud storage as a feature of a subscription package, providing customers with a seamless backup and sync as a differentiator to reduce churn and maximize average revenue per user by indirect revenue models.

How AI is Transforming the Personal Cloud Market

The application of artificial intelligence fundamentally transforms the experience associated with personal cloud storage through the use of intelligent algorithms designed to take action proactively as opposed to the traditionally passive nature of such storage solutions. In Online Cloud and NAS Cloud scenarios, the application of AI technology entails the automatic analysis of photographs and video recordings using computer vision algorithms, including facial recognition in order to sort content according to individual people, as well as scene understanding and object detection to categorize the information according to the depicted scenes or objects. Moreover, artificial intelligence allows one to overcome issues related to inefficient data management and possible security breaches. Intelligent algorithms automatically scan all uploaded content to detect potentially sensitive files, such as identification papers, bank statements, or any other type of confidential correspondence.

Market Dynamics

Key Drivers in the Global Personal Cloud Market

Growth of User-Generated Digital Content Amount

The proliferation of high-resolution cameras in smartphones, the mainstream adoption of 4K and 8K video recording, and the average consumer is creating gigabytes of new information by taking photos, videos, screenshots, and downloads monthly. Personal cloud services solve this requirement by offering virtually infinite scale of expansion with subscription charges and high storage packages, so that users never have to experience the irritation of "storage full" messages, which interrupts the capture of content and the use of apps.

Multi-Device Digital Lifestyle Proliferation

Everyday consumers and knowledge workers are actively moving through ecosystems of three, four, or more devices that are connected, such as smartphones, tablets, laptops, desktop computers, smart TVs, and wearable technology. Such fragmentation of devices causes a lot of friction when files, photographs, or documents that have been prepared in one device are required in another. Personal cloud solutions overcome this friction by seamlessly synchronizing files that ensure that the file states of all registered devices remain consistent. The fact that you can start a document on a work computer, check it on a smartphone during a commute, and finish it on a home tablet has shifted to convenience to expectation and has been behind the continued need to have Online Cloud and NAS Cloud synchronization features.

Restraints in the Global Personal Cloud Market

Recurring Subscription Fatigue and Cost Sensitivity

The rise of subscription-based services in every sector of digital life, streaming entertainment, productivity applications, fitness applications, and cloud storage, has created an increasing consumer of resistance to further recurrent charges. Numerous customers complain about the accumulating monthly price of online subscriptions and are eager to reduce or unify recurrent costs. Online Cloud services based on subscription models and high-tier storage solutions are under renewed pressure to demonstrate value in continuing operations, especially as device vendors provide free limited storage options that meet the backup requirements of many unsophisticated users.

Bandwidth and Connectivity Limitations

Personal cloud functionality cannot be achieved without high-speed and dependable internet connectivity in order to synchronize data, and to be able to access it remotely. The practical usefulness of personal cloud solutions is greatly reduced in areas with inadequate broadband infrastructure, metered data plans, or patchy mobile network access. Posting of high-resolution video or sizey collections of documents can use up huge amounts of data allowance, attract overage charges, or just crash before completion.

Growth Opportunities in the Global Personal Cloud Market

Privacy-First and Decentralized Personal Cloud Solutions

The rising consumer mistrust of large technology platforms and regulation of data practices present a significant opportunity to privacy-friendly personal cloud solutions. End-to-end encryption, zero-knowledge architecture, with service providers having no access to user data, and transparent privacy policies strike a chord with an increasing group of privacy-conscious Consumers and Enterprises. Home-Made Cloud platforms that are open source software based, and easy to install hardware appliances that enable self-hosting, can fill this market niche as individuals can be in full control of their data without having advanced technical knowledge.

AI-Enhanced Content Monetization and Discovery

The addition of advanced AI features to personal clouds opens the possibility of differentiating features and generating new revenue sources. In addition to fundamental organization AI can drive sophisticated content discovery, automated video editing and highlight creation, smart photo book creation, and personalized content suggestions based on media libraries stored. Such value-added services will warrant higher-priced storage plan upgrades and will provide chances to one-time purchase add-ons or feature-specific subscription plans.

Trends in the Global Personal Cloud Market

Convergence of Personal Cloud with Smart Home Ecosystems

Personal cloud platforms are increasingly evolving beyond isolated storage services to become central hubs within broader smart home and digital lifestyle ecosystems. NAS Cloud devices have become media servers of smart television, a repository of surveillance footage of a network of security cameras, automation controllers of IoT devices, and a central management console of the digital life of the family. This trend of convergence turns personal cloud into a utility service into a critical infrastructure element, making switching more expensive and enhancing platform loyalty.

Emergence of Decentralized and Web3 Personal Storage

Decentralized storage networks are a new variant of blockchain-based storage networks that are an alternative to the traditional centralized Online Cloud services. These networks spread encrypted, file fragments through globally distributed networks of nodes, removing single points of failure and dependencies on any single service provider. Still in its early stages, decentralized storage provides interests to technically advanced users who need the highest level of data resilience and censorship resistance. The adoption of cryptocurrency-based payment systems opens up new monetization options in which users have the opportunity to get tokens by providing additional storage capacity to the system.

Research Scope and Analysis

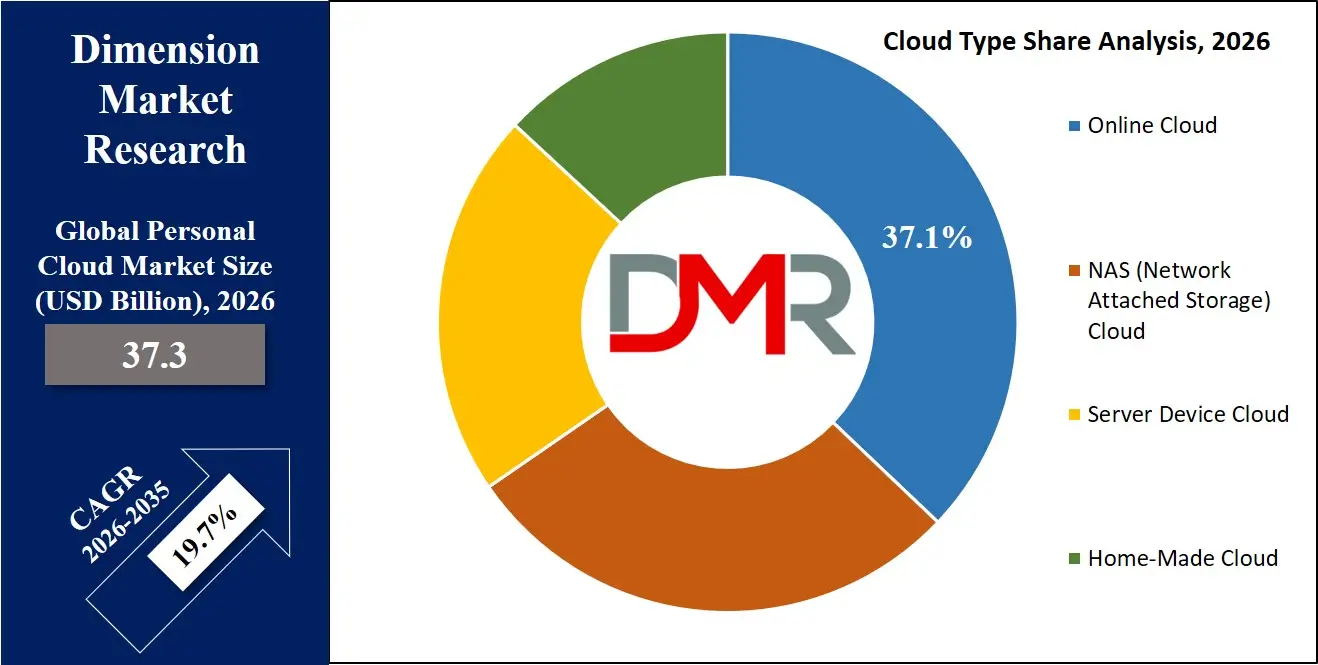

By Cloud Type Analysis

Online Cloud services are poised to dominate the personal cloud market by cloud type because of their unmatched convenience, zero hardware cost of investment, and seamless integration with key mobile and desktop operating system ecosystems. These provider-managed platforms are simple to set up, automatically update software and security patches, and have ubiquitous accessibility on any device connected to the internet.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The freemium approach that most Online Cloud providers use provides a low-friction entry barrier, enabling users to get a taste of the core functionality before committing to premium storage plans. Major technology platform operators take advantage of Online Cloud as a strategic ecosystem lock-in mechanism, where storage services are closely coupled with email, productivity suites, photo management, and device backup, thus making it more challenging to migrate to a new platform to the invested user.

By Hosting Type Analysis

Provider hosting is poised to become the dominant hosting model in the personal cloud market, as it shows the wide consumer interest in turnkey solutions that remove the infrastructure management burden. This model has service providers who run and maintain the storage infrastructure, perform data replication and backup, provide service availability, and make security updates transparently. Provider Hosting corresponds directly to the Online Cloud service model and is especially common with Consumers, who prioritize convenience over completely owning the data. This model has advantages of economies of scale that allow providers to provide large amounts of free storage space as customer acquisition vehicles and collect predictable recurring revenue in the form of subscription charges to increase capacity and other premium features.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By User Type Analysis

Consumers is poised to represent the highest market share in the user segment in the personal cloud market, as they have universal requirement of photo backup, file synchronization among personal devices and media streaming in household networks. The uptake of Online Clouds provided by large platform providers is greatly concentrated and freemium models are the main channel of acquiring customers. These consumer preferences are described in terms of anticipation of smooth integration into the existing device ecosystem, low-level configuration needs, and clear and predictable pricing. The consumer market is very price sensitive when it comes to subscription rates and is actively considering package deals by Telecommunications companies and device vendors.

By Revenue Type Analysis

Direct Revenue is projected to dominate this segment in this market it includes subscription fees and high-end storage plans as the main monetization strategies in the personal cloud market, which offer predictable and recurrent revenue streams which allow the infrastructure investment and service development to continue. Subscriptions have also developed beyond the rudimentary capacity-based levels to more advanced subscriptions that include storage and additional benefits such as advanced AI-assisted organization, increased security features, family sharing, and priority technical support. The subscription model aligns incentives between the provider and the customer on the long-term quality of service and the improvement of its features since retention of customers directly affects lifetime value calculations.

By Vertical Analysis

BFSI is expected to dominate the personal cloud solutions market in context of vertical, where secure document management, client file sharing, and regulatory compliance documentation is essential. Financial institutions use Server Device Cloud and NAS Clouds to offer their relationship managers and advisors safe access to client materials remotely whilst retaining stringent data governance and audit trail functionality. IT and ITeS organizations are not only consumers but also providers of personal cloud technologies. NAS Cloud and Server Device Cloud services are used by IT services companies to facilitate the internal projects cooperation, code files, and secure delivery of projects to clients.

The Global Personal Cloud Market Report is segmented on the basis of the following:

By Cloud Type

- Online Cloud

- NAS (Network Attached Storage) Cloud

- Server Device Cloud

- Home-Made Cloud

By Hosting Type

- User/Self Hosting

- Provider Hosting

By User Type

By Revenue Type

- Direct Revenue

- Subscription fees

- Premium storage plans

- Indirect Revenue

- Advertising

- Bundled telecom or device services

- Freemium upgrades

By Vertical

- BFSI

- IT & ITeS

- Telecommunications

- Retail & E-commerce

- Government & Public Sector

- Manufacturing

- Healthcare & Life Sciences

- Energy & Utilities

- Media & Entertainment

- Others

Regional Analysis

Leading Region by Market Share

North America is poised to dominate the global personal cloud market, projected to hold 38.2% of the market share by the end of 2026. This dominance is due to multiple advantageous conditions in this market, which include relatively high levels of disposable income, high penetration rates of smartphones, highly developed broadband infrastructure, and an ingrained culture of using digital services.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

As the location of the headquarters of some key Online Cloud service providers, North America has been characterized by integration into their ecosystems that ensure continuous consumer uptake. The American consumers' high tolerance for cost in the pursuit of convenient services translates to a viable model of charging fees and premiums for subscriptions and storage plans. On the corporate end, there is also significant adoption of NAS cloud and server device cloud services among SMEs and large enterprises aiming to manage remote workers.

Fastest-Growing Regional Market

Asia-Pacific is expected to be the fastest expanding personal cloud market, due to the combination of widespread use of smartphones, rising incomes among the middle classes, and the rapid adoption of digitalization by consumers and enterprises. In China, India, and Southeast Asian countries, there is a huge increase in digital content created by users, especially with the proliferation of smartphone cameras that provide the primary method for first-time internet users to document their activities. Personal cloud storage solutions are increasingly being offered by telecommunications companies bundled with mobile phone service, making them commonplace in the minds of consumers. The SME sector of the Asia-Pacific region is quickly adopting the use of NAS Clouds as collaborative tools that enable more dispersed work arrangements. Moreover, domestic personal cloud storage providers based in China and India are creating solutions that cater to the languages used and modes of payments in these markets.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The global personal cloud market is strongly competitive with a wide range of players that include global technology platform operators, specialized NAS Cloud hardware vendors, telecommunications providers, and new privacy-centered solutions. Large Online Cloud providers take advantage of deep integration of the ecosystem, large amounts of free storage, and AI-enabled capabilities to retain leading roles in the consumer segment. Such platform operators enjoy the benefit of network effects where personal cloud utilization solidifies the interactions on email, productivity, photo management, and device ecosystems, generating high switching costs on invested users. Competitors that are emerging with privacy and data sovereignty in mind are becoming popular with Consumers and Enterprises that are security-conscious. These providers underline end-to-end encryption, zero-knowledge architecture, open-source transparency, and jurisdictional benefits of privacy-friendly regulation frameworks. Although they are not yet a significant share of the market, these privacy-oriented products put pressure on mainstream providers to improve data protection disclosure and user control choices.

Some of the prominent players in the Global Personal Cloud Market are:

- Amazon

- Apple

- Google

- Microsoft

- Dropbox

- Box

- pCloud

- Sync.com

- Icedrive

- MEGA

- Tresorit

- Seagate

- Western Digital

- Buffalo Technology

- SugarSync

- Egnyte

- Synchronoss

- Funambol

- ownCloud

- Nextcloud

- Other Key Players

Recent Developments

- February 2026: Apple announced significant expansion of iCloud AI capabilities, introducing on-device and private cloud processing for advanced photo and video analysis features that organize personal media libraries without compromising user privacy, reinforcing the company's differentiation around data protection.

- December 2025: Synology launched a new generation of consumer-focused NAS Cloud devices featuring integrated AI processors capable of on-device facial recognition, object detection, and natural language search, enabling advanced personal cloud capabilities without reliance on provider-hosted AI services.

- October 2025: Google enhanced Google One subscription tiers with Gemini AI integration across personal cloud storage, enabling conversational search of stored photos, documents, and emails, and introducing automated content summarization and organization features powered by generative AI.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 37.3 Bn |

| Forecast Value (2035) |

USD 188.2 Bn |

| CAGR (2026–2035) |

19.7% |

| The US Market Size (2026) |

USD 6.2 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Cloud Type (Online Cloud, NAS Cloud, Server Device Cloud, and Home-Made Cloud), By Hosting Type (User/Self Hosting, and Provider Hosting), By User Type (Enterprises, and Consumers), By Revenue Type (Direct Revenue, and Indirect Revenue), By Vertical (BFSI, IT & ITeS, Telecommunications, Retail & E-commerce, Government & Public Sector, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Media & Entertainment, and Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Personal Cloud Market?

▾ The Global Personal Cloud market is poised to be valued at USD 37.3 billion in 2026 and is projected to reach USD 188.2 billion by 2035, driven by exponential growth in user-generated digital content and the universal need for secure, accessible data storage and synchronization.

What is the CAGR of the Global Personal Cloud Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 19.7% from 2026 to 2035, reflecting accelerating consumer reliance on personal cloud services, and enterprise adoption of accessible collaboration platform.

What factors are driving the growth of the Global Personal Cloud Market?

▾ Key drivers include the exponential growth of user-generated digital content from smartphones and connected devices, and the normalization of remote and hybrid work arrangements that demand secure, location-independent file access.

Which region held the largest share of the Personal Cloud Market in 2026?

▾ North America is poised to dominate this market with 38.2% of market share in 2026, driven by high disposable income, and strong consumer willingness to pay for digital convenience services including premium storage plans and subscription fees.

Which region is expected to grow the fastest in the Personal Cloud Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid smartphone adoption, rising middle-class disposable income, aggressive Telecommunications bundling strategies, and the expansion of domestic personal cloud providers offering localized services tailored to regional preferences.

What are the major trends in the Global Personal Cloud Market?

▾ Major trends include the convergence of personal cloud with smart home ecosystems, the emergence of privacy-focused and decentralized storage alternatives, and the growing adoption of NAS Cloud and User/Self Hosting solutions among privacy-conscious consumers and SMEs.

Who are the key players in the Global Personal Cloud Market?

▾ Key players include global platform operators such as Apple, Google, Microsoft, and Amazon; specialized NAS Cloud hardware manufacturers including Synology, QNAP, and Western Digital; independent Online Cloud providers like Dropbox and Box; and emerging privacy-focused alternatives including Proton, pCloud, and MEGA.

How is the Global Personal Cloud Market segmented?

▾ The market is segmented by Cloud Type, Hosting Type, User Type, Revenue Type, and Vertical.