Market Overview

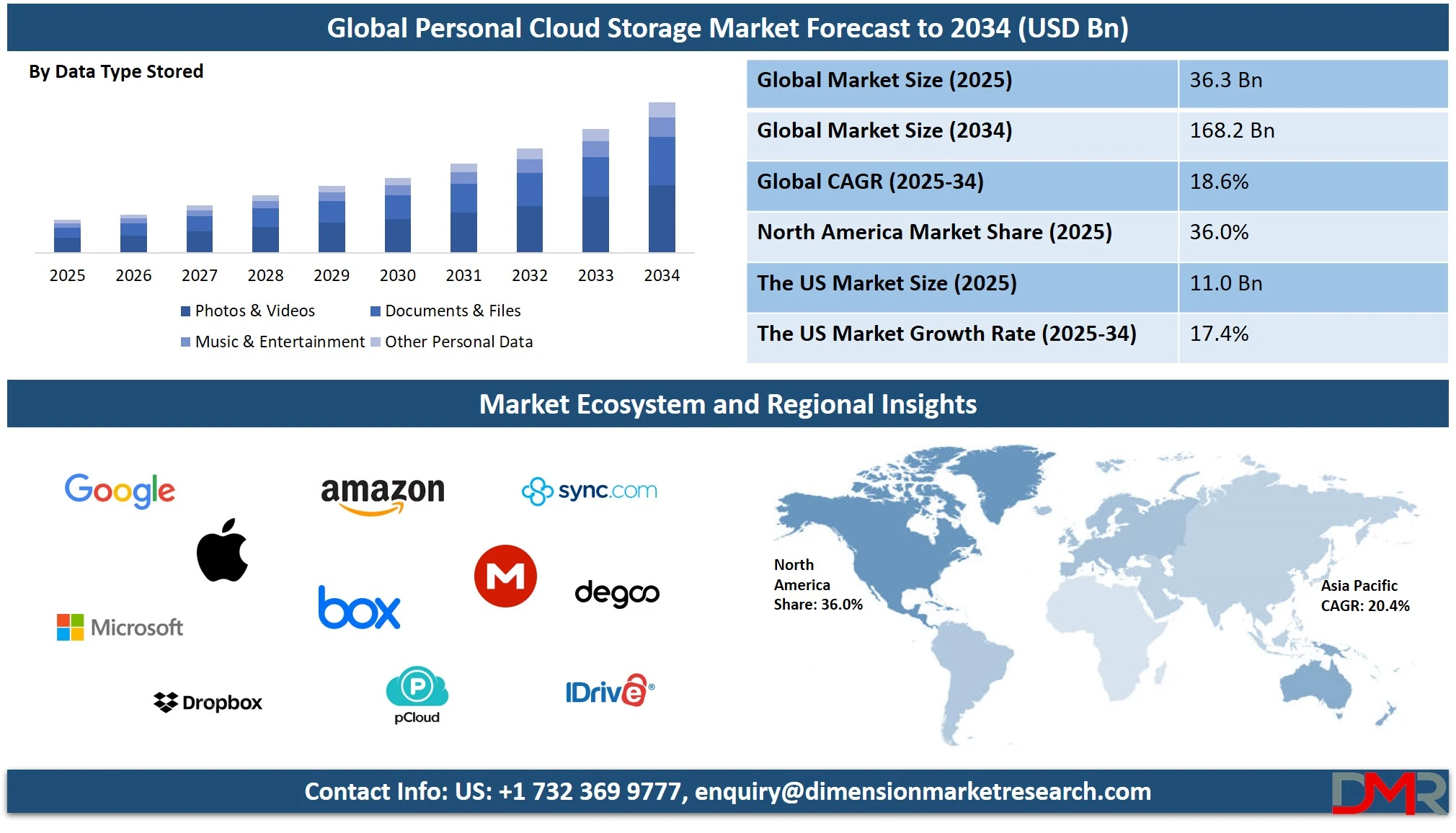

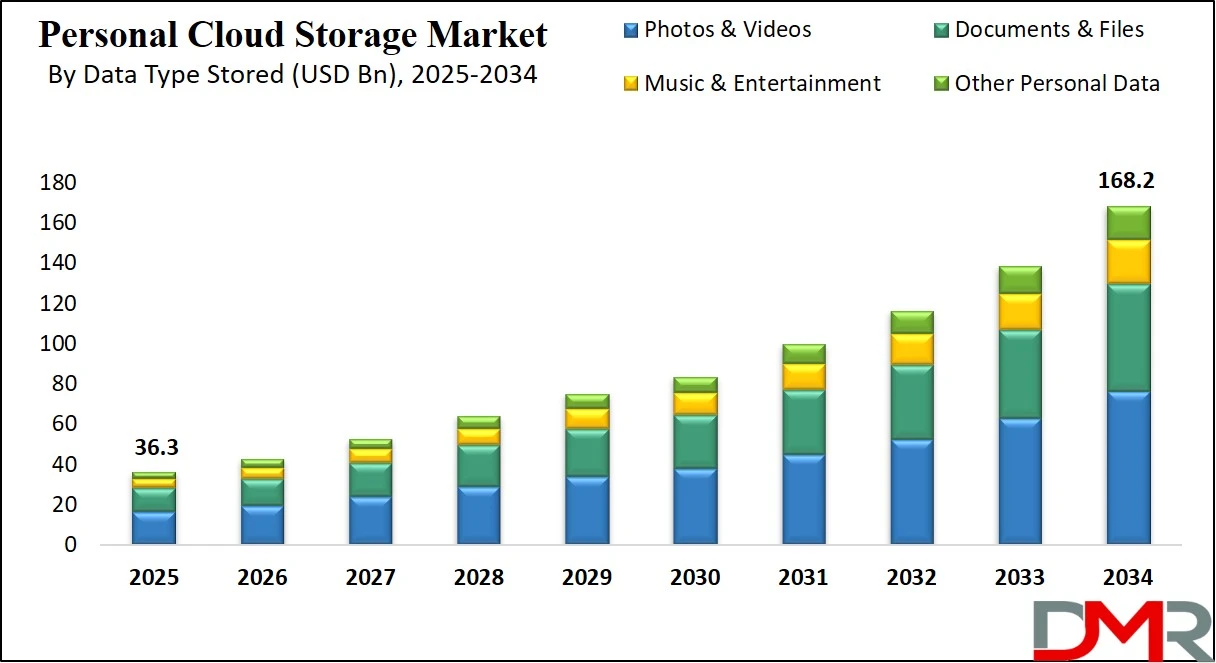

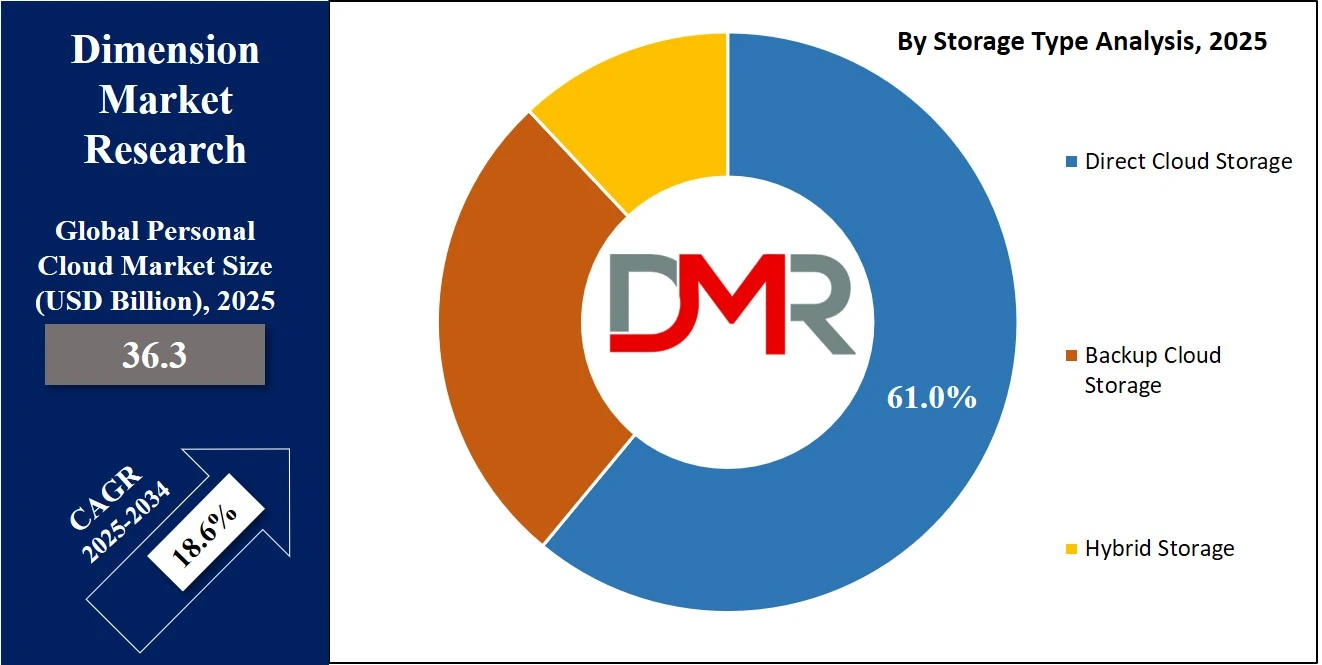

The global personal cloud storage market is projected to reachn USD 36.3 billion in 2025 and is expected to grow to USD 168.2 billion by 2034, expanding at a CAGR of 18.6%. This growth is driven by rising demand for secure data backup, multi-device file access, and increasing adoption of cloud-based personal storage solutions across consumers and professionals.

Personal cloud storage refers to a digital storage model where individuals can securely store, manage, and access their data over the internet from multiple devices. It typically involves services offered through cloud platforms that enable users to save personal files such as photos, videos, documents, and music, while maintaining privacy and ownership of their data.

Unlike traditional external drives, personal cloud storage solutions provide real-time synchronization, automatic backup, and accessibility from smartphones, laptops, tablets, and even smart TVs. These platforms are especially valuable for users looking to reduce dependency on physical storage and enhance convenience through cross-platform accessibility, automatic file organization, and remote sharing capabilities.

The global personal cloud storage market has seen substantial growth due to the increasing use of digital devices and the rising need for data backup and real-time access. With the surge in mobile device usage and the explosion of multimedia content generation, consumers are shifting towards online storage solutions that offer scalability, security, and ease of use.

The adoption of cloud-based file sharing and collaboration tools is also gaining momentum, especially among freelancers, students, and professionals working remotely. Moreover, the growing awareness of data loss prevention and the ability to retrieve content at any time are further propelling the demand for personal cloud solutions globally.

Furthermore, market expansion is being fueled by technological advancements in storage encryption, AI-powered file management, and integration with productivity suites. Providers are increasingly offering freemium models, family-sharing plans, and enhanced security features to cater to users who prioritize privacy.

Regions like the Asia Pacific are emerging as high-growth zones due to the proliferation of smartphones and the expansion of internet infrastructure. Meanwhile, markets in North America and Europe are focusing on enhancing data sovereignty and compliance with data protection regulations. The convergence of convenience, privacy, and accessibility is shaping the future trajectory of the personal cloud storage industry.

The US Personal Cloud Storage Market

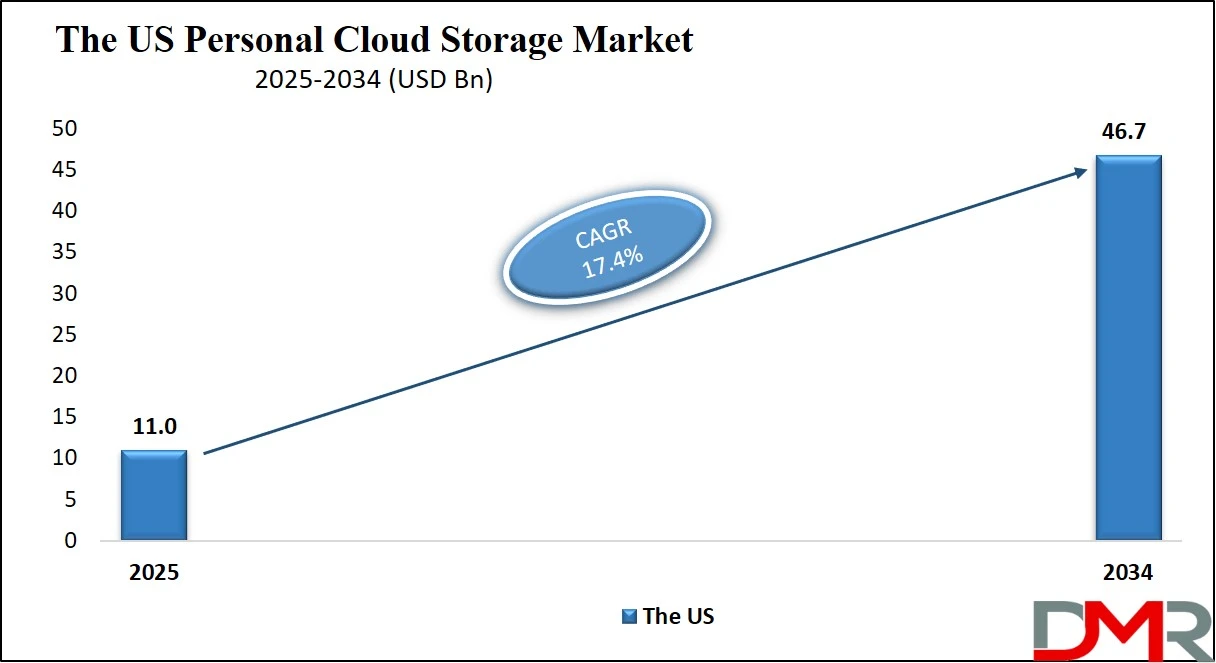

The U.S. Personal Cloud Storage market size is projected to be valued at USD 11.0 billion by 2025. It is further expected to witness subsequent growth in the upcoming period, holding USD 46.7 billion in 2034 at a CAGR of 17.4%.

The United States personal cloud storage market is one of the most mature and competitive globally, driven by high internet penetration, widespread use of digital devices, and early adoption of cloud technologies. American consumers rely heavily on cloud platforms for storing and managing their data, including photos, documents, videos, and app backups. The popularity of services such as Google Drive, iCloud, OneDrive, and Dropbox reflects the growing need for seamless cross-device synchronization, automated backups, and large-scale data storage solutions.

The rise of remote work, digital learning, and online content creation has significantly accelerated personal cloud storage adoption in the US, as users increasingly demand instant access to their files from smartphones, laptops, tablets, and desktops. Freemium storage plans, bundled cloud services with device purchases, and increased awareness of data recovery benefits are also contributing to steady market expansion.

Security, privacy, and user control are key differentiators in the US personal cloud storage landscape. Consumers are becoming more conscious of protecting their digital assets from cyber threats, leading to higher demand for encrypted cloud storage, two-factor authentication, and zero-knowledge platforms. In response, vendors are integrating advanced security protocols and AI-powered file organization tools into their offerings.

Additionally, growing interest in decentralized storage systems and hybrid cloud solutions is reshaping consumer preferences. The US market is also influenced by regulatory frameworks like the California Consumer Privacy Act (CCPA), which encourages companies to offer greater transparency and user rights over personal data. With increased use of smart home devices, wearable tech, and media streaming, the volume of personal data continues to grow, reinforcing the country’s leadership in the global personal cloud storage ecosystem.

Europe Personal Cloud Storage Market

Europe’s cloud storage market is projected to reach a value of approximately USD 9.0 billion in 2025, reflecting strong adoption across both individual and professional user bases. This growth is driven by a combination of high digital literacy, widespread use of smartphones and connected devices, and increasing reliance on cloud-based tools for managing personal data.

European consumers are highly engaged with services like Google Drive, iCloud, and Dropbox, while also showing growing interest in privacy-first providers such as pCloud, Tresorit, and Internxt, many of which are headquartered in Europe and adhere strictly to GDPR. The preference for secure, encrypted, and locally compliant cloud storage solutions is shaping market dynamics, especially in countries like Germany, the UK, France, and the Nordics, where digital safety is a key consumer concern.

The market is anticipated to grow at a robust CAGR of 17.2% from 2025 to 2034, fueled by rising demand for cloud-based backups, increasing multimedia content creation, and expanding hybrid work models across the continent. As European businesses adopt bring-your-own-device (BYOD) policies and remote work becomes more normalized, employees are increasingly turning to personal cloud accounts to store and access work-related data securely.

Additionally, advancements in 5G connectivity, increasing smart device usage, and integration of AI for automated file organization and syncing are expected to further enhance user experience and encourage long-term subscription growth. The presence of strong regulatory frameworks and a competitive vendor landscape makes Europe one of the most stable and privacy-conscious markets in the global personal cloud storage ecosystem.

Japan Personal Cloud Storage Market

Japan’s personal cloud storage market is expected to reach approximately USD 2.0 billion in 2025, driven by its mature digital ecosystem, high smartphone penetration, and widespread use of advanced consumer electronics. Japanese users often rely on cloud storage services bundled with their existing ecosystems, such as Apple iCloud, Google Drive, and domestic providers integrated with telecom carriers or smart device platforms.

The country’s strong culture of data safety and digital organization makes cloud-based backups for photos, documents, and application data a routine part of daily digital life. Additionally, Japan’s tech-savvy population, especially urban professionals and students, actively uses personal cloud accounts for seamless file access across devices, contributing to sustained market expansion.

The market is projected to grow at a CAGR of 14.8% from 2025 to 2034, reflecting steady adoption among both younger users and working professionals. As remote work becomes more accepted and lifestyle digitization continues, cloud storage is being increasingly utilized not only for media and documents but also for backing up settings, contacts, and device data.

Growth is further supported by the availability of localized user interfaces, high-speed internet infrastructure, and integrated cloud offerings through consumer electronics brands and mobile carriers. While Japan’s market is smaller in volume compared to regions like North America or Europe, it stands out for its high-value user base, strong data privacy awareness, and willingness to pay for reliable, secure, and seamlessly integrated cloud storage solutions.

Global Personal Cloud Storage Market: Key Takeaways

- Market Value: The global personal cloud storage market size is expected to reach a value of USD 168.2 billion by 2034 from a base value of USD 36.3 billion in 2025 at a CAGR of 18.6%.

- By Component Segment Analysis: Solutions are anticipated to dominate the component segment, capturing 68.0% of the total market share in 2025.

- By Deployment Mode Segment Analysis: Public Cloud mode is expected to maintain its dominance in the deployment mode segment, capturing 76.0% of the total market share in 2025.

- By Storage Type Segment Analysis: Direct Cloud Storage is poised to consolidate its dominance in the storage type segment, capturing 61.0% of the market share in 2025.

- By User Type Segment Analysis: Individual Users will dominate the user type segment, capturing 81.0% of the market share in 2025.

- By Platform Segment Analysis: Mobile Devices will account for the maximum share in the platform segment, capturing 52.0% of the total market value.

- By Subscription Model Segment Analysis: Freemium-based models are expected to consolidate their dominance in the subscription model segment, capturing 63.0% of the market share in 2025.

- By Data Type Stored Segment Analysis: Photos & Videos will dominate the data type stored segment, capturing 45.0% of the market share in 2025.

- By Access Type Segment Analysis: App Access type is expected to maintain its dominance in the access type segment, capturing 50.0% of the market share in 2025.

- By Age Group Segment Analysis: The 18-30 Years age group will hold the maximum market share in the age group segment, capturing 41.0% of the market share in 2025.

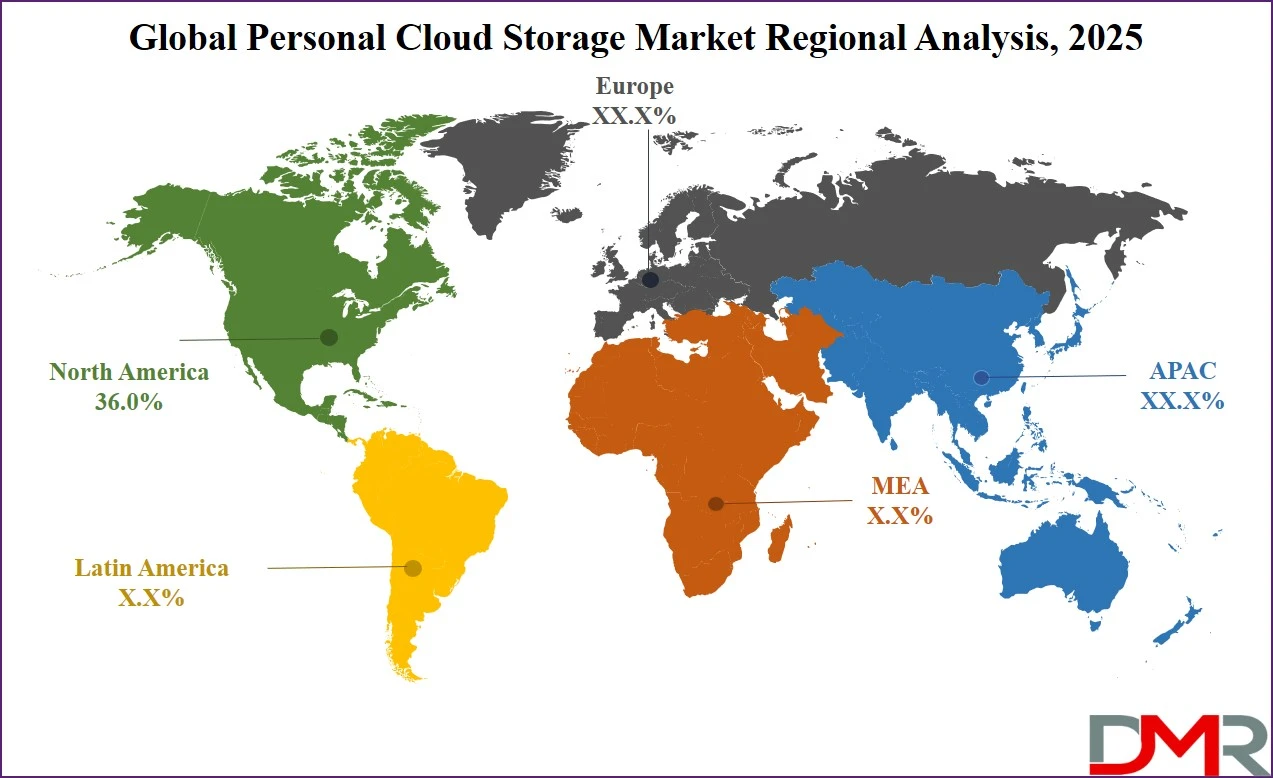

- Regional Analysis: North America is anticipated to lead the global personal cloud storage market landscape with 36.0% of total global market revenue in 2025.

- Key Players: Some key players in the global personal cloud storage market are Google, Apple, Microsoft, Dropbox, Amazon, Box, pCloud, Sync.com, MEGA, IDrive, Degoo, NordLocker, Tresorit, Internxt, SpiderOak, Zoolz, Tardigrade (Storj), Icedrive, and Others.

Global Personal Cloud Storage Market: Use Cases

- Remote Work and File Collaboration: With the rise of hybrid and remote workforces, personal cloud storage has become essential for professionals needing access to work-related documents anytime, from any location. Users utilize cloud platforms such as OneDrive, Google Drive, and Dropbox to create, edit, and share documents across multiple devices. Features like real-time synchronization, version history, and multi-user editing enable seamless collaboration. Employees working remotely can securely store confidential files in encrypted personal cloud accounts and share them with colleagues through permission-controlled links. This use case has seen massive adoption in industries like IT, consulting, media, and education, where productivity tools are often integrated with cloud storage solutions to streamline workflows.

- Photo and Video Backup for Mobile Users: One of the most widespread use cases of personal cloud storage is the automatic backup of photos and videos taken on smartphones. With high-resolution image and video files consuming increasing amounts of device storage, users rely on cloud storage services like iCloud, Google Photos, and Amazon Photos to store media content securely without compromising local storage space. These platforms offer mobile cloud sync, allowing content to be accessed across multiple devices instantly. Personal cloud systems also use AI-based features for organizing photos by location, date, and subject, making them easy to retrieve and manage. This functionality is highly valued by everyday users, travelers, social media influencers, and digital creators who need fast and reliable access to visual content.

- Secure Archiving of Personal Documents: Consumers around the world use personal cloud storage to safeguard critical personal documents such as medical records, identification proofs, legal papers, tax filings, and financial statements. This use case is particularly relevant for users who seek encrypted storage solutions with privacy-first features. Services like pCloud, MEGA, and NordLocker offer zero-knowledge encryption, meaning only the user has access to the stored content. Users benefit from the peace of mind that their sensitive documents are protected against device failure, theft, or loss. In addition, many cloud providers offer features like digital vaults, two-factor authentication, and secure folder sharing, which are essential for individuals managing high-value personal data or living in regions with strong data protection regulations.

- Media Streaming and Content Access on the Go: Personal cloud storage is increasingly being used for storing and streaming large media libraries, including music, movies, and personal video collections. Platforms like Plex, Synology Drive, and even Google Drive support media access from any device connected to the internet. This is especially useful for users who travel frequently, work in creative fields, or prefer to maintain their library outside of subscription-based services. Instead of using up local memory, users can upload content to their cloud drive and stream it directly to smartphones, tablets, or smart TVs. This use case supports both personal entertainment and professional media review, particularly in regions with widespread 4G/5G connectivity and growing reliance on cloud-based digital lifestyles.

Impact of Artificial Intelligence on Personal Cloud Storage Market

Artificial Intelligence (AI) is significantly transforming the personal cloud storage market by enhancing user experience, optimizing storage efficiency, and strengthening data security. One of the most noticeable impacts is in intelligent file organization and management. AI algorithms automatically categorize files such as images, documents, and videos by analyzing metadata, file content, and usage patterns. For example, Google Photos uses AI to group pictures by people, locations, and events, allowing users to search using natural language (e.g., “photos from Paris 2022”). This intelligent tagging and smart search functionality makes personal cloud storage more intuitive and less reliant on manual file sorting.

In addition, AI plays a crucial role in storage optimization and predictive file access. Machine learning models can analyze storage habits and pre-load frequently accessed files, leading to faster access and reduced latency across devices. AI also helps in identifying duplicate or unused files, allowing users to clean up their storage space without manual review. Another growing application is AI-powered data protection and anomaly detection. AI can monitor login patterns, detect suspicious activity, and alert users to potential security breaches. This enhances the reliability and trustworthiness of cloud platforms, especially in an era where privacy and data integrity are key concerns. As AI continues to evolve, its integration with personal cloud storage services will further improve personalization, automation, and cybersecurity, ultimately shaping the next generation of cloud-based digital lifestyles.

Global Personal Cloud Storage Market: Stats & Facts

Eurostat (European Commission)

- In 2023, 45.2% of EU enterprises purchased cloud computing services, up from 42.5% in 2021.

- In 2023, 68% of those enterprises used cloud services specifically for file storage.

- In 2023, 77.6% of large enterprises, 59% of medium enterprises, and 41.7% of small enterprises in the EU adopted cloud computing solutions.

- In 2025, the European Commission aims for 75% of EU businesses to adopt cloud computing, big data, and AI technologies under the Digital Decade targets.

OECD (Referencing Eurostat Data)

- In 2023, approximately 65% of EU enterprises had more than 20% of their IT workloads running on cloud platforms.

- In 2025, cloud usage is expected to exceed 70% across the EU business ecosystem, aligning with the Digital Europe Programme’s infrastructure goals.

Japan Ministry of Economy, Trade and Industry (METI)

- In 2023, Japan’s public sector migrated core government systems to shared cloud infrastructure to improve efficiency and reduce costs.

- In 2025, the Japanese government expects full integration of administrative services into the national cloud framework, covering nearly all central ministries.

JETRO (Japan External Trade Organization) / Digital Agency of Japan

- In 2023, over 60% of Japanese enterprises reported using cloud services for file storage and remote work support.

- By 2025, Japan aims for over 80% cloud adoption in enterprise IT environments as part of its national digital transformation (DX) roadmap.

Global Personal Cloud Storage Market: Market Dynamics

Global Personal Cloud Storage Market: Driving Factors

Rapid Increase in Digital Content Creation

The explosive growth in smartphone usage, high-resolution photography, video blogging, and content sharing has led to an unprecedented surge in personal digital data. Users are capturing and creating more content than ever, which requires scalable and secure storage solutions. Personal cloud platforms like Google Drive, iCloud, and Dropbox offer real-time cloud backup and mobile data sync to help users manage this growing content volume without physical storage limitations. The demand for automatic uploads, cross-device access, and file versioning is fueling widespread adoption.

Rise in Remote Work and BYOD Culture

The growing trend of remote and hybrid work models, combined with the bring-your-own-device (BYOD) movement, has increased the need for reliable cloud-based file access. Employees are seeking flexible tools that enable secure file storage, document sharing, and collaboration from home or on the go. Personal cloud services meet this demand by allowing individuals to store work-related documents in private accounts while maintaining control over their data. Integration with productivity apps and encrypted file storage capabilities further enhances the relevance of personal cloud solutions in today’s decentralized work environment.

Global Personal Cloud Storage Market: Restraints

Concerns around Data Privacy and Unauthorized Access

Despite advancements in security, many users remain concerned about how their data is stored, accessed, and used by cloud providers. Issues such as third-party data sharing, server-side access, and insufficient end-to-end encryption have raised questions around user privacy. Personal cloud storage platforms without zero-knowledge architecture can leave sensitive information vulnerable to breaches, reducing trust among privacy-conscious consumers.

Limited Free Storage and Pricing Barriers

Most leading cloud storage providers operate on a freemium model, offering a small amount of free storage (typically 5GB to 15GB) with paid upgrades. However, users with high storage needs, such as content creators or families, often find these free plans inadequate and the premium pricing unappealing. This cost barrier can hinder adoption, especially in emerging markets where affordability is a key decision factor.

Global Personal Cloud Storage Market: Opportunities

Growth in AI-Driven Personal Storage Solutions

Artificial intelligence presents vast opportunities for enhancing user experience in the personal cloud space. Features like smart file suggestions, automatic organization, duplicate detection, and intelligent search powered by AI can differentiate offerings. Providers investing in AI-enhanced platforms can attract tech-savvy users looking for personalized, hassle-free storage management without manual intervention.

Rising Demand for Encrypted and Decentralized Storage

With growing awareness about cybersecurity and data ownership, there’s a rising demand for personal cloud storage platforms offering encrypted file storage and decentralized architecture. Solutions like MEGA, Internxt, and Tardigrade (Storj) cater to users seeking privacy-first alternatives to mainstream providers. As more consumers become aware of surveillance risks and data compliance requirements (e.g., GDPR, CCPA), the market for secure, transparent, and decentralized cloud storage is expected to expand rapidly.

Global Personal Cloud Storage Market: Trends

Multi-Device and Cross-Platform Synchronization

Modern users operate across multiple devices, smartphones, tablets, laptops, and smart TVs. A key trend in personal cloud storage is the focus on seamless file synchronization across ecosystems. Whether accessing music playlists from a tablet or editing documents across devices, users expect a consistent experience. This has led to the rise of mobile-first cloud apps and integrated device-cloud ecosystems, especially among tech giants like Apple and Microsoft.

Integration with Lifestyle and Smart Home Applications

Personal cloud storage is becoming more than just a place to save files. It is increasingly integrated with smart home systems, fitness trackers, media servers, and even IoT-enabled security systems. This trend expands the utility of cloud storage beyond traditional use cases, enabling automatic uploads of CCTV footage, health records, and smart device logs. As digital lifestyles become more interconnected, cloud storage will serve as the central repository for managing personal digital ecosystems.

Global Personal Cloud Storage Market: Research Scope and Analysis

By Component Analysis

In the personal cloud storage market, solutions are expected to account for the majority share, capturing 68.0% of the total component segment in 2025. This dominance is driven by the widespread use of cloud-based platforms such as Google Drive, iCloud, Dropbox, and OneDrive, which offer scalable and user-friendly storage solutions.

These platforms enable users to automatically back up photos, documents, videos, and other digital files across devices without the need for physical storage devices. With increasing smartphone adoption and the rise of digital content creation, users are relying more on integrated storage solutions that offer features like real-time synchronization, file sharing, cross-device access, and AI-based file organization. The growing preference for cloud-native applications and the seamless integration of storage with productivity tools and operating systems have further solidified the position of storage solutions as the preferred component among consumers.

On the other hand, the services segment plays a crucial supporting role in the personal cloud storage market by ensuring users can fully utilize and manage their storage platforms effectively. These services include technical assistance, onboarding support, data migration, troubleshooting, customization, and storage optimization.

As more users adopt cloud solutions for both personal and work-related needs, service providers are offering tailored support packages to help them with secure data transfers, account setup, and privacy configurations. For consumers unfamiliar with cloud technologies, professional guidance on managing storage limits, syncing devices, or activating backup features adds significant value.

Additionally, premium services often include advanced features like encrypted file recovery, secure file sharing, and regulatory compliance support. These service offerings not only enhance user satisfaction but also strengthen brand loyalty by providing a seamless and secure cloud experience.

By Deployment Mode Analysis

Public cloud deployment is expected to remain the most widely adopted mode in the personal cloud storage market due to its convenience, scalability, and widespread accessibility. This model is typically offered by large service providers such as Google, Apple, Microsoft, and Amazon, allowing users to store, access, and manage their data over the internet without having to maintain any physical infrastructure.

The public cloud is favored by individual users for its seamless integration with devices, user-friendly interfaces, and cost-effective freemium models. Features such as automatic backups, cross-device synchronization, and built-in sharing options make it the go-to choice for storing photos, videos, documents, and other personal files. Its high availability and compatibility across operating systems and applications further reinforce its dominance, especially among mobile and remote users who prioritize accessibility and simplicity.

In contrast, the private cloud deployment model caters to users who prioritize greater control, customization, and enhanced data security. This model involves hosting storage on dedicated servers or personal hardware, often within a user’s environment or through a trusted third party with restricted access. While less common among general consumers due to higher setup complexity and cost, private cloud solutions are increasingly popular among privacy-conscious users, tech enthusiasts, and small businesses that seek to safeguard sensitive information.

These setups often support encryption, limited user access, and advanced configuration options, making them suitable for storing confidential documents, financial records, or family archives. Though adoption is lower compared to the public cloud, private cloud deployments are gradually gaining attention from users seeking alternatives to mainstream providers with more control over where and how their data is stored.

By Storage Type Analysis

Direct cloud storage is set to lead the storage type segment as it continues to be the most preferred option for users seeking instant access to their data from any device. This type of storage allows users to upload and access files directly in the cloud without relying on local device storage, making it ideal for individuals who work across multiple platforms such as smartphones, laptops, and tablets.

Services like Google Drive, Dropbox, and OneDrive offer seamless integration with operating systems and mobile apps, enabling users to easily store, sync, and share documents, photos, and media in real time.

The appeal of direct cloud storage lies in its simplicity, speed, and accessibility, allowing users to organize and manage their digital content with minimal effort. It supports collaboration, cross-device continuity, and space-saving benefits, which have become crucial as the volume of personal data continues to grow globally.

Backup cloud storage, on the other hand, is primarily used for safeguarding files by automatically copying data from devices to the cloud in case of system failure, theft, or accidental deletion.

It is particularly valued by users who want peace of mind that their information is securely preserved without needing to manage the files actively. Platforms like iCloud and IDrive are commonly used for this purpose, offering scheduled or continuous backup options that run in the background.

This type of storage is often chosen by users who prioritize data protection and recovery rather than frequent interaction with stored content. Backup cloud storage also supports version history and encrypted archives, which are beneficial for maintaining long-term data integrity.

While it doesn’t offer the same level of active usage as direct cloud storage, it remains an essential segment of the market, especially for users with important documents, device settings, and personal data they want to keep safe over time.

By User Type Analysis

Individual users are expected to dominate the user type segment in the personal cloud storage market, accounting for a substantial share due to the widespread use of smartphones, tablets, and personal computers. This user group includes students, freelancers, families, and casual users who rely on cloud platforms to store and manage everyday digital content such as photos, videos, documents, and app backups.

The increasing volume of personal data generated through social media, mobile photography, digital communication, and streaming content has made cloud storage a convenient and essential tool for everyday digital life.

Services like iCloud, Google Drive, and Dropbox are particularly popular among individual users due to their ease of use, mobile accessibility, and free storage plans. Features like automatic uploads, real-time sync, and easy sharing further enhance the user experience, driving continued adoption among consumers looking for a reliable way to back up and access their data across devices.

Work-based users, while a smaller segment, play a vital role in shaping the personal cloud storage market through their demand for functionality that supports productivity and security. These users often include remote employees, small business owners, and consultants who use personal cloud storage to manage professional documents, collaborate with clients, and access files while working outside traditional office environments.

Personal cloud solutions offer these users flexibility and control, allowing them to integrate with productivity apps, share large files securely, and maintain encrypted access to sensitive work data. In many cases, employees prefer using their cloud storage accounts due to familiarity or limitations in enterprise-provided tools.

As the boundary between personal and professional device usage continues to blur, especially in BYOD (bring your own device) environments, this segment is expected to grow steadily, with increasing interest in secure, efficient, and mobile-friendly storage options tailored for professional use.

By Platform Analysis

Mobile devices are projected to lead the platform segment in the personal cloud storage market, accounting for the largest share as smartphones and tablets have become the primary tools for content creation and consumption.

Users increasingly rely on mobile cloud storage apps like Google Photos, iCloud, and OneDrive to back up their photos, videos, messages, and documents in real time. The widespread availability of high-speed internet, growing camera capabilities, and ease of mobile app access have significantly contributed to the dominance of this platform.

Cloud storage on mobile devices enables users to instantly capture, store, and share files without worrying about local storage limits. The auto-sync and auto-backup functionalities available on mobile operating systems ensure that users’ data is protected continuously without manual effort. The convenience of accessing and managing files from any location directly through apps makes mobile cloud storage indispensable in today’s digitally connected lifestyle.

Desktops and laptops continue to play a key role in the personal cloud storage ecosystem, particularly for users who manage large files, work on content creation, or engage in document-heavy tasks.

Cloud services on these platforms are deeply integrated with operating systems like Windows and macOS, allowing users to drag and drop files directly into cloud folders or sync entire directories for real-time updates. Desktop-based cloud storage is commonly used for backing up work documents, academic projects, financial records, and multimedia content.

It also enables seamless collaboration through linked file sharing and multi-device access. While the usage share is lower than mobile platforms, desktops and laptops remain critical for users who require more robust file organization, detailed editing, and larger screen real estate for managing and reviewing content. This platform segment continues to grow among professionals, students, and home office users who depend on cloud access for both personal and productivity purposes.

By Subscription Model Analysis

Freemium-based models are expected to dominate the subscription model segment in the personal cloud storage market as they offer an accessible entry point for users with basic storage needs. These models provide a limited amount of free cloud space, typically ranging from 5GB to 15GB, which is often sufficient for casual users to store photos, documents, and essential files.

Platforms like Google Drive, iCloud, and Dropbox have popularized the freemium approach by attracting users with free storage and then encouraging upgrades through convenience features, such as additional space, advanced sharing tools, and automatic backups. This model is particularly appealing to students, families, and users in emerging markets where affordability is a key factor. The ability to test the service before committing financially also boosts user confidence and drives widespread adoption across diverse demographics.

Paid plans, while a smaller segment by volume, represent a significant portion of revenue in the personal cloud storage market. These subscriptions cater to users with higher storage demands or advanced usage requirements, such as digital creators, remote professionals, and users managing multiple devices. Paid plans typically offer larger storage capacities, priority customer support, extended file history, and enhanced security features, including encrypted file sharing and access control.

Many services also bundle cloud storage with other offerings, such as productivity tools, music or photo services, and device integration, adding further value to the subscription. As personal and professional data usage continues to grow, many users find the added reliability and space of paid plans essential, leading to steady growth within this segment despite the dominance of freemium models.

By Data Type Stored Analysis

Photos and videos are anticipated to dominate the data type stored segment in the personal cloud storage market, driven by the growing use of high-resolution smartphone cameras, increased content creation, and the need for safe and accessible media storage. With mobile photography and video sharing becoming a daily activity for millions of users globally, cloud storage platforms like Google Photos, iCloud, and Amazon Photos offer convenient solutions for automatic media backups, seamless organization, and cross-device accessibility.

These services allow users to free up device space while ensuring that their memories are preserved and easily retrievable. Features such as AI-powered tagging, facial recognition, and timeline-based sorting enhance user experience, making cloud storage an integral part of managing personal media libraries. The dominance of this segment reflects a broader trend of individuals relying on the cloud to store their growing volumes of visual content securely and effortlessly.

Documents and files also represent a significant portion of data stored in personal cloud platforms, particularly among students, professionals, and remote workers who require constant access to their work and academic materials. Cloud storage services enable users to upload, edit, and share files like PDFs, Word documents, spreadsheets, and presentations from any device, which is crucial in both educational and work-from-home settings.

Platforms such as OneDrive, Dropbox, and Google Drive offer document collaboration tools, file version history, and secure sharing options that make personal cloud storage essential for productivity and organization. While not as dominant as media storage in terms of volume, the documents and files segment plays a vital role in daily digital life, supporting task management, project tracking, and digital learning needs with reliable and synchronized access to important content.

By Access Type Analysis

App access is expected to maintain its dominance in the access type segment of the personal cloud storage market, as users increasingly prefer the convenience and speed of dedicated mobile and desktop applications. These apps are optimized for seamless navigation, automatic syncing, and background uploads, enabling users to manage their files without needing to open a browser or manually initiate uploads.

Services like Google Drive, iCloud, Dropbox, and OneDrive have robust apps designed for Android, iOS, Windows, and macOS, making it easy for users to access and manage their data with just a few taps or clicks.

App-based access supports features such as push notifications, offline file availability, biometric authentication, and integrated sharing options, enhancing user experience and engagement. As more users shift to mobile-first and app-centric digital habits, especially in emerging markets, this access mode continues to grow in popularity and usability.

Web access remains a vital and complementary mode of interaction in the personal cloud storage market, especially for users accessing files on shared or public devices, or when app installation is not preferred. Through web browsers, users can log in to their cloud accounts from virtually any internet-enabled device and manage their files with full functionality, including uploading, downloading, organizing, and sharing content.

Web portals also provide advanced file previews, collaborative editing tools, and settings configuration without requiring software installation. This access type is particularly useful in office environments, libraries, and educational institutions where browser-based platforms offer flexibility and quick access.

Although it may lack some of the speed and offline capabilities of dedicated apps, web access remains an important option for users who value versatility and cross-platform functionality in managing their data.

By Age Group Analysis

The 18–30-year age group is expected to lead the age group segment in the personal cloud storage market, primarily due to their high engagement with digital technologies and frequent content generation. This demographic includes students, young professionals, social media users, and digital content creators who extensively use smartphones, laptops, and tablets for capturing and storing photos, videos, assignments, resumes, and other personal files.

With an active presence on social platforms and a strong inclination toward mobile-first solutions, this age group relies heavily on cloud storage for automatic backups, file sharing, and easy access to content across multiple devices. The availability of free storage plans and integration with popular apps and productivity tools also appeal to this tech-savvy segment, making cloud storage a daily utility for organizing both personal and academic or work-related data.

The 31–50 years age group represents another significant portion of the market, consisting of working professionals, parents, and small business owners who use personal cloud storage for both personal and professional purposes.

Individuals in this segment often require more storage space for managing family photos, work documents, financial records, and collaborative projects. They tend to value security, reliability, and multi-device synchronization, especially as many in this group juggle personal responsibilities and remote work.

Cloud platforms offering family-sharing plans, encrypted file protection, and productivity suite integration resonate well with their lifestyle and needs. Additionally, users in this age group are more likely to opt for paid plans, seeking long-term storage solutions with advanced features like extended file history, device backup, and priority support, contributing to both market volume and revenue growth.

The Personal Cloud Storage Market Report is segmented based on the following:

By Component

By Deployment Mode

- Public Cloud

- Private Cloud

- Hybrid Cloud

By Storage Type

- Direct Cloud Storage

- Backup Cloud Storage

- Hybrid Storage

By User Type

- Individual Users

- Work-Based Users

By Platform

- Mobile Devices

- Desktops/Laptops

- Other Devices

By Subscription Model

By Data Type Stored

- Photos & Videos

- Documents & Files

- Music & Entertainment

- Other Personal Data

By Access Type

- App Access

- Web Access

- Other Access

By Age Group

- 18-20 Years

- 31-50 Years

- 51+ Years

Global Personal Cloud Storage Market: Regional Analysis

Region with the Largest Revenue Share

North America is projected to lead the global personal cloud storage market in 2025, capturing 36.0% of the total market revenue, driven by high digital penetration, advanced cloud infrastructure, and early adoption of technology across the region. Consumers in the United States and Canada are heavily reliant on smartphones, laptops, and smart home devices, all of which generate large volumes of personal data requiring efficient and secure storage solutions.

The presence of major cloud service providers such as Google, Apple, Microsoft, and Dropbox, along with widespread use of mobile apps and high-speed internet, further strengthens the region’s dominance.

Additionally, growing awareness around data security, integrated with the increasing adoption of subscription-based digital services and productivity tools, has reinforced the demand for scalable, encrypted, and easily accessible personal cloud storage across both individual and professional user bases in North America.

Region with significant growth

The Asia Pacific region is expected to witness the most significant growth in the personal cloud storage market over the coming years, fueled by rapid digitalization, increasing smartphone penetration, and expanding internet connectivity across countries such as China, India, Indonesia, and the Philippines.

As millions of new users come online, there is a growing demand for affordable and accessible cloud storage solutions to manage the surge in personal digital content, particularly photos, videos, and mobile app data.

The popularity of mobile-first services, rising adoption of freemium cloud models, and growing awareness about data backup and privacy are key factors contributing to the region’s accelerated market expansion. Additionally, increased investments in cloud infrastructure by global tech giants and the rising middle-class population with disposable income are expected to drive long-term growth in the Asia Pacific's cloud storage landscape.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Personal Cloud Storage Market: Competitive Landscape

The global competitive landscape of the personal cloud storage market is characterized by the dominance of major technology giants such as Google, Apple, Microsoft, Amazon, and Dropbox, which collectively hold a substantial share due to their vast user bases, integrated ecosystems, and strong brand loyalty. These companies offer seamless cloud storage solutions bundled with their hardware, operating systems, or productivity suites, giving them a significant competitive advantage.

At the same time, a growing number of specialized providers like pCloud, MEGA, Sync.com, Tresorit, and Internxt are gaining traction by focusing on privacy-centric features, zero-knowledge encryption, and secure file sharing.

Competition is also intensifying through innovations in AI-driven file organization, flexible pricing models, cross-platform compatibility, and decentralized storage systems. As user concerns around data privacy and ownership continue to rise, vendors are differentiating themselves by enhancing security protocols and offering more personalized experiences, resulting in a highly dynamic and evolving market environment.

Some of the prominent players in the global personal cloud storage market are:

- Google

- Apple

- Microsoft

- Dropbox

- Amazon

- Box

- pCloud

- Sync.com

- MEGA

- IDrive

- Degoo

- NordLocker

- Tresorit

- Internxt

- SpiderOak

- Zoolz

- Tardigrade (Storj)

- Icedrive

- Koofr

- Nextcloud

- Other Key Players

Global Personal Cloud Storage Market: Recent Developments

- August 2025: Barracuda introduced Entra ID Backup Premium, a SaaS offering designed to strengthen identity data protection for Microsoft Entra ID environments beyond native retention limits.

- July 2025: Hitachi Vantara released its Virtual Storage Platform One (VSP One) software-defined storage solution on Google Cloud Marketplace, enabling two-way replication, thin provisioning, and advanced compression for hybrid cloud data management.

- July 2025: Hewlett-Packard Enterprise completed its acquisition of Juniper Networks, expanding its cloud-native, AI-driven networking and storage portfolio.

- April 2025: Salesforce announced plans to acquire data-security startup Own Co. for approximately USD 1.9 billion, enhancing its data protection and compliance capabilities.

Report Details

| Report Characteristics |

| Market Size (2025) |

USD 36.3 Bn |

| Forecast Value (2034) |

USD 168.2 Bn |

| CAGR (2025–2034) |

18.6% |

| Historical Data |

2019 – 2024 |

| The US Market Size (2025) |

USD 11.0 Bn |

| Forecast Data |

2025 – 2033 |

| Base Year |

2024 |

| Estimate Year |

2025 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors, etc. |

| Segments Covered |

By Component (Solutions and Services), By Deployment Mode (Public Cloud, Private Cloud, and Hybrid Cloud), By Storage Type (Direct Cloud Storage, Backup Cloud Storage, and Hybrid Storage), By User Type (Individual Users and Work-Based Users), By Platform (Mobile Devices, Desktops/Laptops, and Other Devices), By Subscription Model (Freemium and Paid Plans), By Data Type Stored (Photos & Videos, Documents & Files, Music & Entertainment, and Other Personal Data), By Access Type (App Access, Web Access, and Other Access), and By Age Group (18–30 Years, 31–50 Years, and 51+ Years) |

| Regional Coverage |

North America – US, Canada; Europe – Germany, UK, France, Russia, Spain, Italy, Benelux, Nordic, Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, Rest of MEA |

| Prominent Players |

Google, Apple, Microsoft, Dropbox, Amazon, Box, pCloud, Sync.com, MEGA, IDrive, Degoo, NordLocker, Tresorit, Internxt, SpiderOak, Zoolz, Tardigrade (Storj), Icedrive, and Others |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days, and 5 analysts working days respectively. |

Frequently Asked Questions

The global personal cloud storage market size is estimated to have a value of USD 36.3 billion in 2025 and is expected to reach USD 168.2 billion by the end of 2034.

The US personal cloud storage market is projected to be valued at USD 11.0 billion in 2025. It is expected to witness subsequent growth in the upcoming period as it holds USD 46.7 billion in 2034 at a CAGR of 17.4%.

North America is expected to have the largest market share in the global personal cloud storage market, with a share of about 36.0% in 2025.

Some of the major key players in the global personal cloud storage market are Google, Apple, Microsoft, Dropbox, Amazon, Box, pCloud, Sync.com, MEGA, IDrive, Degoo, NordLocker, Tresorit, Internxt, SpiderOak, Zoolz, Tardigrade (Storj), Icedrive, and Others.

The market is growing at a CAGR of 18.6 percent over the forecasted period.