What is the Global Pet Insurance Market Size?

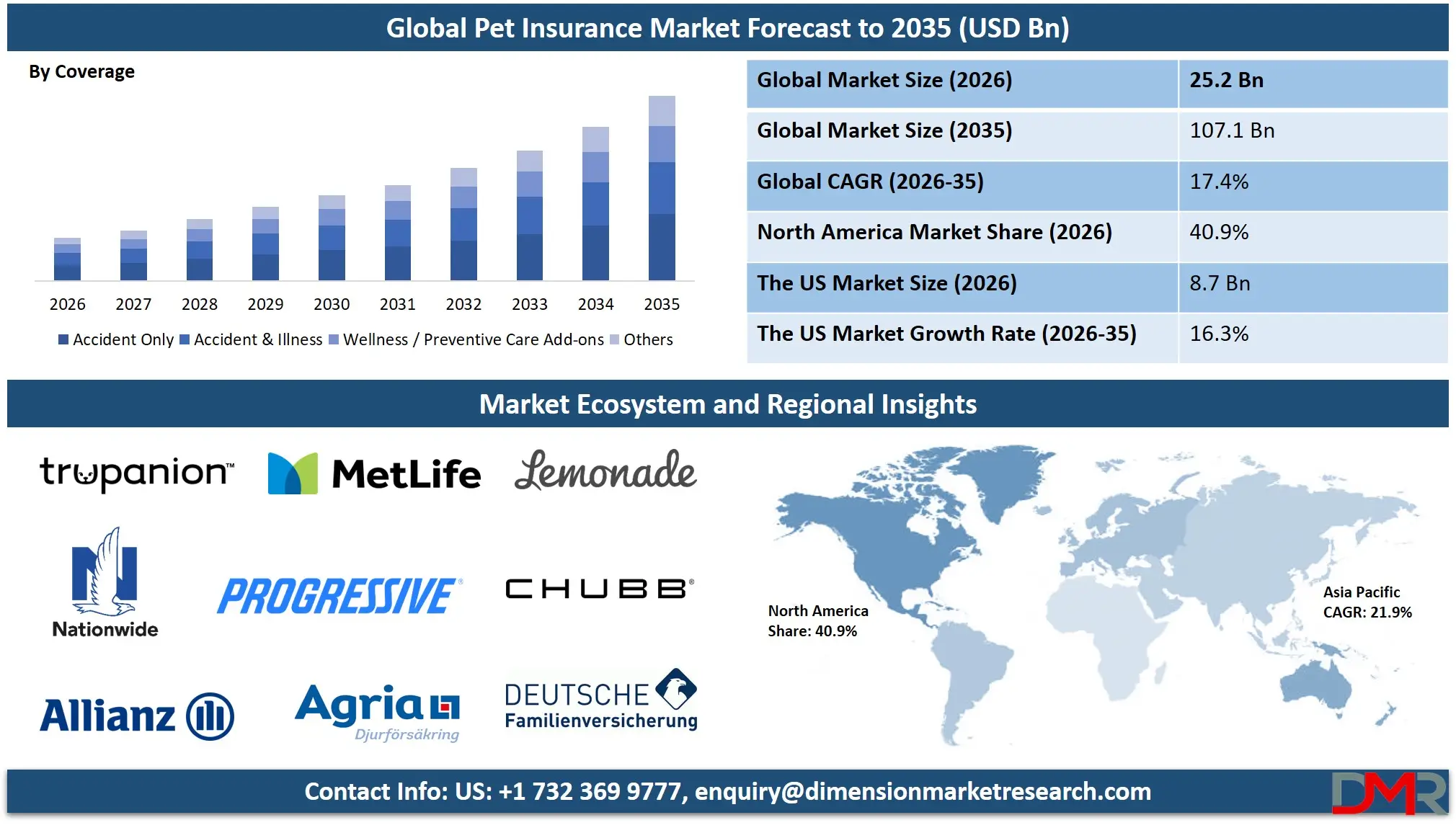

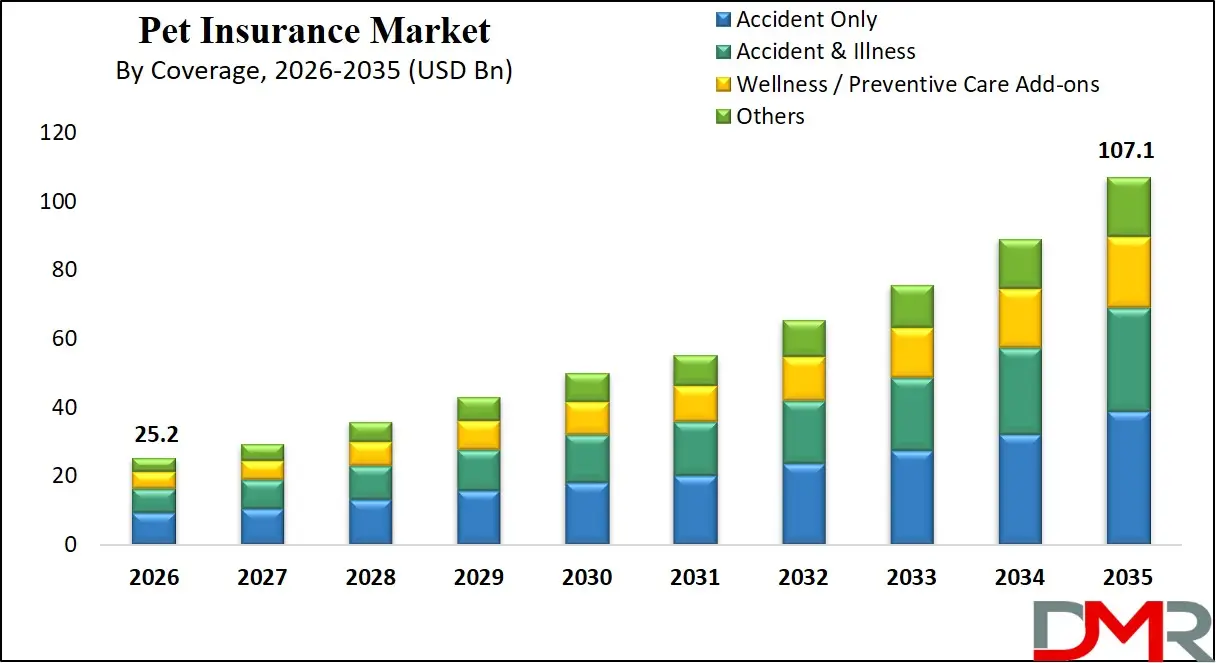

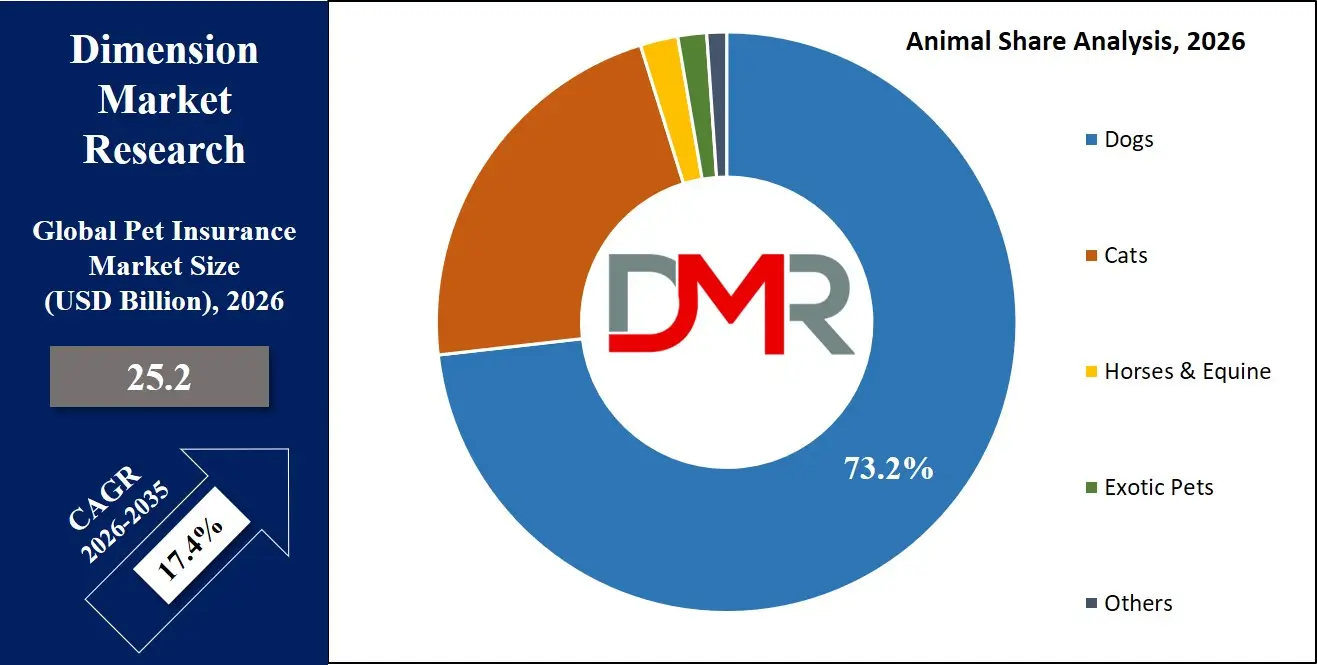

The Global Pet Insurance Market size is estimated at USD 25.2 billion in 2026 and is projected to reach USD 107.1 billion by 2035, exhibiting a CAGR of 17.4% during the forecast period, driven by the rising use of artificial intelligence in claims processing, veterinary care automation, and integrated pet health management in animal healthcare.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Global Pet Insurance Market is expanding because of increasing use of machine learning in detecting and analyzing medical claims and treatment patterns; increasing approvals which reduce the probability of claim denials during underwriting and speed up the reimbursement process for veterinary services; and greater funding in automating the application of pet health data.

Some other reasons for expansion in this market are technological innovations in real-time claim settlement, pet health risk prediction, automated medical record processing, and high-throughput digital platforms along with better data integration standards. The digital revolution in pet care and veterinary service companies has been helpful in speeding up claim processing and making pet healthcare management easier. This includes wellness tracking research. In addition, national policies focusing on the bio-economy and animal welfare have ensured sustainable research in pet health insurance.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Pet Insurance Market

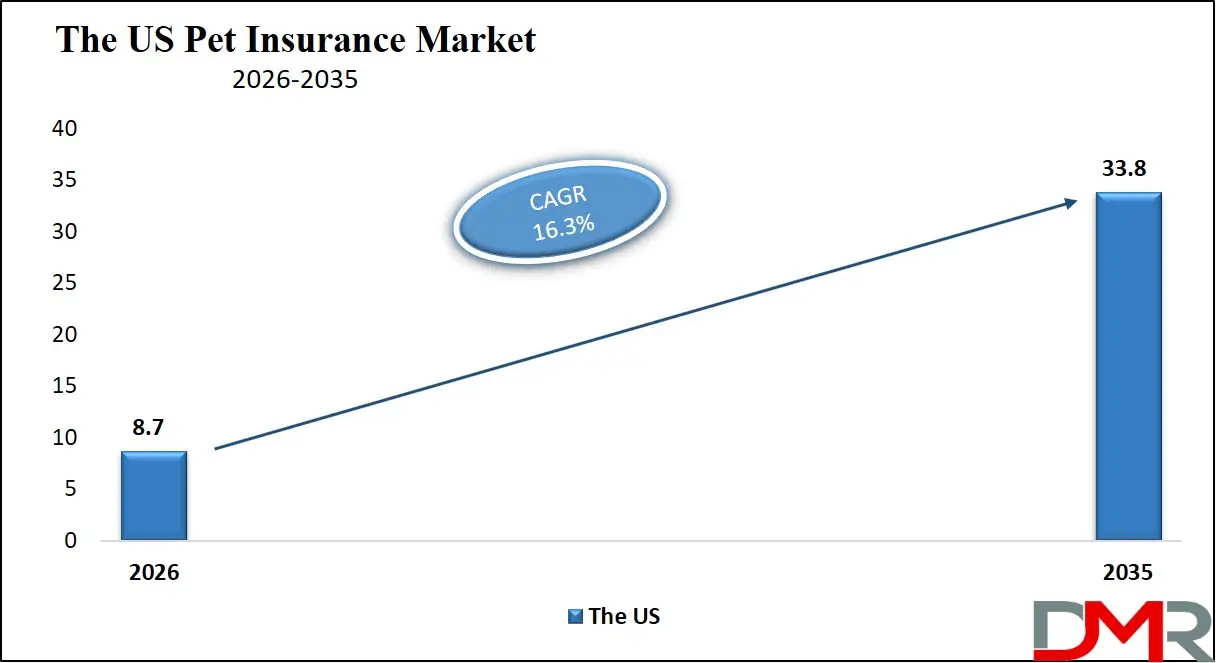

The US Pet Insurance Market is estimated to grow to USD 8.7 billion in 2026 with a compound annual growth rate of 16.3% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US market is shaped by major federal and state-level initiatives promoting pet wellness, veterinary care affordability programs supported by the AVMA, and NIH-led companion animal health initiatives. These programs encourage the use of AI-driven claims processing, real-time veterinary data analysis, and predictive underwriting software. Automated claims platforms are being rapidly adopted, and the US continues to invest in better data sharing between veterinary hospitals, pet health record systems, and reliable AI tools for pet insurance. Service providers are also influenced by laws like the Pet Insurance Model Act and national digital health strategies to offer services that ensure data security, compliance, and smooth integration across veterinary clinics and pet owner portals.

Europe Pet Insurance Market

The Europe Pet Insurance Market is estimated to be valued at USD 7.6 billion in 2026, witnessing growth at a CAGR of 15.8%, during the forecast period.

Europe's pet insurance market is mature, shaped by EU-wide policies such as the EU Animal Health Strategy, the European Horizon Europe research program and national policies to support digital pet health (e.g., France's national pet wellness plans and Germany's Tiergesundheitsstrategie 2030). Countries are also making insurance processes more modular to align veterinary and pet owner demands and enable the sharing of claims data across national borders. The market grows due to new tools like software for real-time claim validation and scoring systems for wellness add-ons. Use is facilitated by public-private collaborations and data standards. Insurers have access to technologies such as cloud computing and encryption, and Europe is at the forefront of the digitisation of safe and efficient pet insurance operations.

Japan Pet Insurance Market

The Japan Pet Insurance Market is projected to be valued at USD 860.2 million in 2026, progressing at a CAGR of 14.9%, during the period spanning from 2026 to 2035.

Japan's pet insurance market is well developed, with high-quality digital claims platforms, integrated veterinary management systems, and a wide array of AI-powered pet health risk analysis software tools. National focus on automation, efficiency and process integrity is delivered via predictive health models and smart policy management. Growth opportunities are aided by government measures under the Society 5.0 program by Japan's Ministry of Economy, Trade and Industry (METI), and continued investment in digital pet healthcare. Veterinary R&D, industrial pet health analysis for breed-specific condition development and clinical pet insurance all need effective AI to keep pace with data analysis. Higher costs for validating new claims automation systems and integrating them with legacy veterinary systems are significant, but there are opportunities for the export of Japanese pet insurance technologies to the Asian and Pacific markets.

Key Takeaways

- Market Size & Forecast: The Global Pet Insurance Market is estimated to be valued at USD 25.2 billion in 2026 and is expected to grow to USD 107.1 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 17.4% in the forecast period.

- Primary Growth Drivers: The availability of new claims processing technologies that use machine learning, the need to accelerate veterinary care reimbursement and improve success rates of pet treatments, and more government investment in national animal health infrastructure are key growth drivers.

- Key Market Trends: The predictive profiling of pet health risks, real-time claims data processing and the shift to cloud-based pet insurance and policy management platforms are key market trends.

- By Coverage: Accident & Illness policies are expected to occupy the largest revenue share in 2026 in the global pet insurance market.

- By Animal: Dogs are expected to occupy the largest revenue share in 2026 in the pet insurance market.

- By Sales Channel: Direct-to-Consumer is estimated to take the lead in 2026 with the largest share in the pet insurance market, owing to digital adoption and ease of policy purchase.

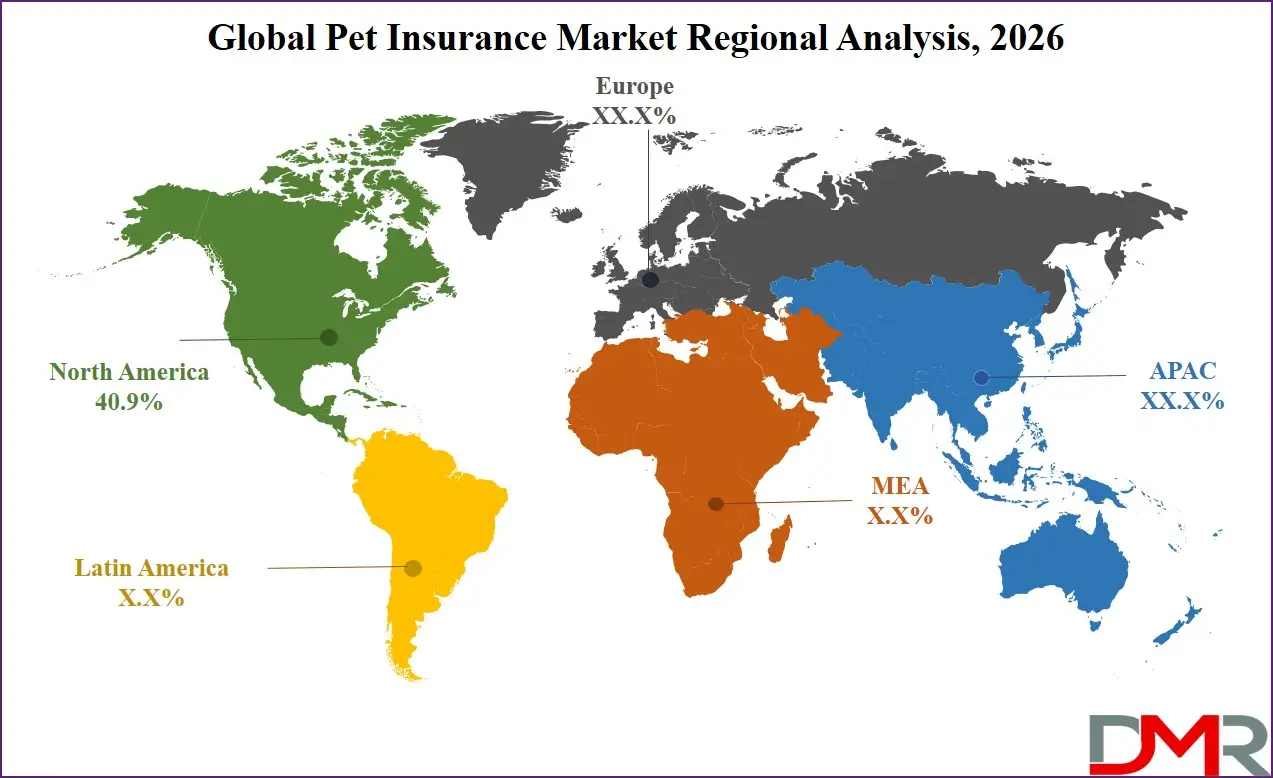

- Regional Leadership: North America is estimated to take the lead in 2026 with 40.9% share in the pet insurance market, owing to significant investment in pet healthcare and insurance technologies.

What is Pet Insurance?

Pet insurance is a type of health insurance for pets that covers their medical treatments, surgeries, medications, and preventive care on a reimbursement basis. It leverages sophisticated systems such as online claims, practice management software, and telemedicine to manage, authenticate, and localize pet health events and treatments. To enhance the pet health outcomes, manage chronic conditions and breed-specific conditions programs, and expand pet insurance into wellness coverage to support personalized veterinary care and promote development of pet wellness and preventive care products.

Use Cases

- Accident & Illness Coverage for Veterinary Emergencies: Pet insurance can cover emergency veterinary treatment, surgery, hospitalization, and prescription drugs to treat a fracture, poisoning, or infection in days, as compared to weeks that it would take with traditional manual reimbursement plans.

- Chronic Condition Management: Long-term data on chronic diseases in pets, including diabetes, arthritis, or kidney disease, are modeled to understand more about disease progression to assist in planning long-term care.

- Wellness & Preventive Care Tracking: Preventive care add-ons (like vaccinations, dental cleanings, flea/tick control) are processed via digital platforms and machine learning in clinical and home settings.

- Population Health & Government Programs: Faster pet insurance assists veterinary innovation and development of rare disease treatments for animals; government programs through smart monitoring of pet health data advance national animal welfare strategies and assist adoption of care standards.

How AI Is Transforming the Global Pet Insurance Market?

Artificial intelligence is being applied more and more often to pet insurance to enhance claims forecasting, identify fraud trends, and automatically identify anomalies in veterinary billing data. It also facilitates quicker claim validation as it allows processing of digital submissions on a large scale. Veterinary records and electronic invoices are easier to analyze and assist insurers to detect billing anomalies, minimize errors, and enhance the overall accuracy of claims. This has resulted in claims processing being cost effective, quicker and more efficient than the traditional manual review method.

AI is also strengthening underwriting processes by improving risk assessment and enabling more accurate policy structuring. It helps insurers anticipate claim volumes, identify potential processing delays, and monitor the performance of provider networks more effectively. In addition, automation of routine checks and performance monitoring is reducing operational workload, lowering administrative costs, and improving overall efficiency. This is contributing to better financial performance and more stable insurance operations across the pet insurance value chain.

Market Dynamics

Key Drivers of the Global Pet Insurance Market

Rapid Acceleration in Digital Claims Processing and Data Integration

The market is growing with the rise of digital tools to validate and process claims, better management of veterinary data, and closer integration of electronic medical records and insurance systems. Veterinary practice management platforms provide real-time data that allows monitoring the claims workflow, allowing to identify discrepancies early, and checking policies much faster. This has enhanced efficiency in operations and minimized the human factor as well as the administrative expenses. Simultaneously, demand for more automated insurance operations is being facilitated by increased activity in predictive analytics for the assessment of pet health risks, as veterinary practice is further digitalizing fundamental clinical and billing operations.

Growing Focus on Regulatory Compliance and Standardization in Pet Healthcare

There is increasing emphasis on transparency, data accuracy, and compliance within the pet insurance ecosystem. Regulatory frameworks such as the EU Animal Health Strategy and veterinary modernization initiatives in key markets are encouraging improved data handling practices and more structured insurance processes. These advancements are underpinning the need to have systems that can offer consistent monitoring of claims and standardized reporting. Concurrently, an active process of enhancing the interoperability of veterinary data and curbing billing inconsistencies is strengthening the necessity of more effective insurance administration systems in both governmental and private care providers.

Restraints in the Global Pet Insurance Market

High Costs of System Integration and Operational Setup

The deployment of pet insurance platforms remains cost-intensive, requiring significant investment in system integration, testing, and alignment with veterinary workflows. In addition, compliance with data privacy regulations such as GDPR and other regional frameworks adds to implementation complexity. These factors increase upfront costs and can limit adoption, particularly among smaller insurers and new market entrants.

Limited Standardization Across Veterinary and Insurance Systems

There is still fragmentation in the market in terms of data formats and claims processing processes. Although there are areas that have implemented organized veterinary practice management systems, numerous insurers continue to work in both digital and manual systems. Lack of standards causes interoperability between veterinary providers and insurers to be constrained and results in inefficiencies in claims processing and system integration.

Growth Opportunities in the Global Pet Insurance Market

Expansion of Emerging Pet Insurance Markets

Emerging economies such as Brazil, Indonesia, Nigeria, the UAE, and Vietnam are gradually developing their pet healthcare and insurance ecosystems. These regions have long-term growth prospects, with more people owning pets, and with more people becoming more aware of pet health insurance and gradually digitalizing the veterinary care. These markets have few legacy insurance systems and can be exploited with new, technology-driven insurance systems to be scaled up.

Rising Demand for Cloud-Based Insurance Infrastructure

The transition to remote veterinary care, distributed pet health networks, and real-time claims is creating the uptake of cloud-based insurance systems. These systems facilitate centralized data access, enhanced coordination of veterinary providers and insurers, and expedited policy administration. Cloud-based deployment is increasingly becoming a trend among contemporary pet insurance providers as operational efficiency becomes one of the competitive factors.

Global Pet Insurance Market Trends

Advancement of Predictive Risk Modeling in Pet Insurance

The pet insurance platforms are gradually integrating data-driven technology to determine risk trends and enhance accuracy in underwriting. These systems enable the insurers to evaluate their claims behavior better, simplify the management of their policies, and improve their overall performance in terms of the portfolio. The move is slowly turning the industry more proactive and data-driven in insurance management as opposed to being purely reactive in claims management.

Increasing Adoption of Cloud-Based Policy and Claims Management Systems

The use of cloud infrastructure is currently emerging as a fundamental part of present-day pet insurance functionality. The systems facilitate real-time claims, centralized policy administration, and enhanced network coordination among the veterinarians. Cloud-based platforms are enhancing the efficiency and responsiveness of insurance providers that operate in various regions by eliminating the need to depend on physical infrastructure and facilitating scalable operations.

Research Scope and Analysis

The global pet insurance market is driven by rising demand for comprehensive accident & illness coverage, increasing dog insurance adoption, strong dominance of private providers, and rapid digitalization across direct-to-consumer sales channels, supported by faster claims processing and flexible policy customization.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Coverage Analysis

The Accident & Illness segment is likely to continue dominating the market in 2026, with 62.3% of the global pet insurance market share. This is due to its integral part in covering veterinary emergencies, surgeries, and chronic condition management, and its versatility in various pet owner environments where comprehensive medical protection is needed. The Accident Only segment is also growing rapidly, with increasing demand for basic injury coverage required in budget-conscious pet owner segments that require affordability and simplicity. They are also driven by the improvement of claims processes, real-time reimbursement, and flexibility through modular platforms that combine several coverage types for improved versatility and user convenience.

By Animal Analysis

The Dogs segment is expected to account for 73.2% share in 2026, due to higher veterinary costs, breed-specific conditions, and greater owner willingness to insure dogs compared to other pets. The segment is also driven by growing adoption of comprehensive illness and wellness plans, and integrated coverage options to increase value for dog owners in clinical and home applications. It's also the fastest-growing segment in the pet insurance market, due to the rapid uptake of fully integrated pet health workflows and veterinary infrastructure. Cats are the second-largest segment, followed by Horses & Equine.

By Provider Analysis

The Private provider segment is expected to dominate with around 78.4% market share in 2026, driven by greater flexibility in policy design, faster claims processing, and broader network access compared to public providers. Private pet insurance supports customized coverage because it can offer multiple tiers of deductibles, reimbursements, and annual limits, delivering fast results while keeping data within insured systems. The Public provider segment, while smaller, is seeing strong growth in regions with government-sponsored animal welfare programs and subsidized veterinary care.

By Sales Channel Analysis

The Direct-to-Consumer segment is the largest sales channel in 2026, accounting for 41.7% share, driven by digital adoption, online comparison tools, and the ease of purchasing policies via websites and mobile apps. Insurance Agents are the second-largest segment, using personalized advice and cross-selling with other insurance products. The fastest-growing area is Bancassurance, where banks and financial institutions offer pet insurance as an add-on to existing banking products. Insurance Brokers are also emerging for complex, multi-pet or high-value animal coverage.

The Global Pet Insurance Market Report is segmented based on the following:

By Coverage

- Accident Only

- Accident & Illness

- Wellness / Preventive Care Add-ons

- Others

By Animal

- Dogs

- Cats

- Horses & Equine

- Exotic Pets

- Others

By Provider

By Sales Channel

- Direct-to-Consumer

- Insurance Agents

- Insurance Brokers

- Bancassurance

- Others

Regional Analysis

Leading Region in the Pet Insurance Market

It is projected that North America will take the lead in the global pet insurance market (by value), covering a market share of about 40.9% in the year 2026. The region's dominance is driven by strong pet healthcare spending funded by private and public sources, higher average premiums relative to other regions, a mature digital insurance supply chain for advanced data sharing, and the presence of major pet insurance providers and veterinary networks. The widespread adoption of advanced claims processing and automation for wellness coverage, accident & illness policies, and chronic condition management further strengthens North America's leading position. Additionally, ongoing investments in AI-powered claims monitoring and system interoperability further reinforce the region's technology leadership.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Region in the Pet Insurance Market

Asia-Pacific is the fastest-growing region, supported by strong digital insurance infrastructure targets in China, India, and Japan, increasing pet ownership and awareness initiatives, rising investments in local pet insurance capabilities, and growing adoption of automated claims analysis systems. The region benefits from well-established digital payment infrastructure for insurance products, increasing commercial activity, and alignment with national pet welfare roadmaps. Countries across the region are actively deploying pet insurance platforms to improve reimbursement efficiency and strengthen veterinary infrastructure. Growing emphasis on pet health insurance R&D and structured data development further accelerates market expansion. Moreover, increasing government support and commercial pet care commitments are expected to sustain high growth momentum.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The pet insurance market is highly competitive, with innovation and strategic alliances shaping the competitive environment. To gain an advantage, companies and insurers are focused on developing better digital platforms (such as AI-powered claims engines, automated underwriting systems, and mobile apps for policy management), AI-powered data analysis, and digital platform-based claims monitoring. There are high barriers to entry due to the large capital needed for regulatory approval, specialized actuarial expertise, and the need for mature software ecosystems and regulatory compliance.

Strategic approaches to increase market presence include partnerships with veterinary clinics and pet retailers, mergers between insurers and technology providers, and long-term support contracts with pet owners and animal hospitals. Additionally, research and development in data-sharing standards and scalable software architectures are important for staying competitive and meeting the changing needs of the pet insurance community.

Some of the prominent players in the Global Pet Insurance Market are:

- Trupanion, Inc.

- Nationwide Mutual Insurance Company

- Lemonade, Inc.

- MetLife Services and Solutions, LLC

- The Progressive Corporation

- Chubb Limited

- Allianz SE

- Agria Djurförsäkring AB

- Deutsche Familienversicherung AG

- Direct Line Insurance Group plc

- RSA Insurance Group Limited

- Animal Friends Insurance Services Limited

- ManyPets Limited

- Waggel Limited

- Getsafe GmbH

- Pet Protect Limited

- Anicom Holdings, Inc.

- ipet Insurance Co., Ltd.

- PetSure Pty Ltd.

- Embrace Pet Insurance Agency, LLC

- Other Key Players

Recent Developments

- March 2026: Trupanion, Inc. announced a strategic partnership with the Human Animal Bond Research Institute (HABRI) to advance research on the human–animal bond, focusing on data-driven insights to improve pet healthcare access, veterinary outcomes, and insurance innovation across companion animal populations.

- January 2026: Nationwide Mutual Insurance Company launched a new customizable pet insurance plan in the United States, offering expanded coverage options for chronic and hereditary conditions, along with flexible wellness add-ons, strengthening its competitive positioning in the North American pet insurance market.

- October 2025: Agria Djurförsäkring AB launched a UK initiative supporting retired service animals, partnering with a UK-based foundation to cover veterinary and medical costs for police, military, and service animals, reinforcing its positioning in ethical and specialized pet insurance coverage segments.

- June 2025: MetLife, Inc. expanded its pet insurance distribution by partnering with Combined Insurance (a Chubb company), adding its pet insurance offerings to employer supplemental benefits portfolios in the U.S., strengthening its group benefits channel and scaling access to pet healthcare coverage.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 25.2 Bn |

| Forecast Value (2035) |

USD 107.1 Bn |

| CAGR (2026–2035) |

17.4% |

| The US Market Size (2026) |

USD 8.7 Bn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Coverage (Accident Only, Accident & Illness, Wellness / Preventive Care Add-ons, Others), By Animal (Dogs, Cats, Horses & Equine, Exotic Pets, Others), By Provider (Public, Private), and By Sales Channel (Direct-to-Consumer, Insurance Agents, Insurance Brokers, Bancassurance, Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Pet Insurance Market?

▾ The Global Pet Insurance Market size is estimated to have a value of USD 25.2 billion in 2026 and is expected to reach USD 107.1 billion by the end of 2035.

Which region held the largest share of the Global Pet Insurance Market in 2026?

▾ North America is expected to account for the largest market share in 2026, with a share of about 40.9%.

Who are the key players in the Global Pet Insurance Market?

▾ Some of the major key players in the Global Pet Insurance Market are Trupanion, Inc., Nationwide Mutual Insurance Company, ManyPets Limited, Lemonade, Inc., MetLife Services and Solutions, LLC, Anicom Holdings Inc., and many others.

What is the CAGR of the Global Pet Insurance Market from 2026 to 2035?

▾ The market is growing at a CAGR of 17.4% over the forecasted period.

What factors are driving the growth of the Global Pet Insurance Market?

▾ The market is driven by advances in machine learning-based claims processing, regulatory pressure to speed up veterinary reimbursements and reduce errors, and increased government investment in national animal health infrastructure.

What are the major trends in the Global Pet Insurance Market?

▾ The key market trends include the adoption of predictive pet health risk tracking and real-time claims data analysis, along with a growing shift toward cloud-based insurance platforms and data-enabled policy management systems.

Which region is expected to grow the fastest in the Global Pet Insurance Market?

▾ Asia Pacific is the fastest-growing region in the market during the forecast period.

How is the Global Pet Insurance Market segmented?

▾ The market is segmented by coverage, animal, provider, and sales channel.