What is the Photonic Integrated Circuits (PIC) Market Size?

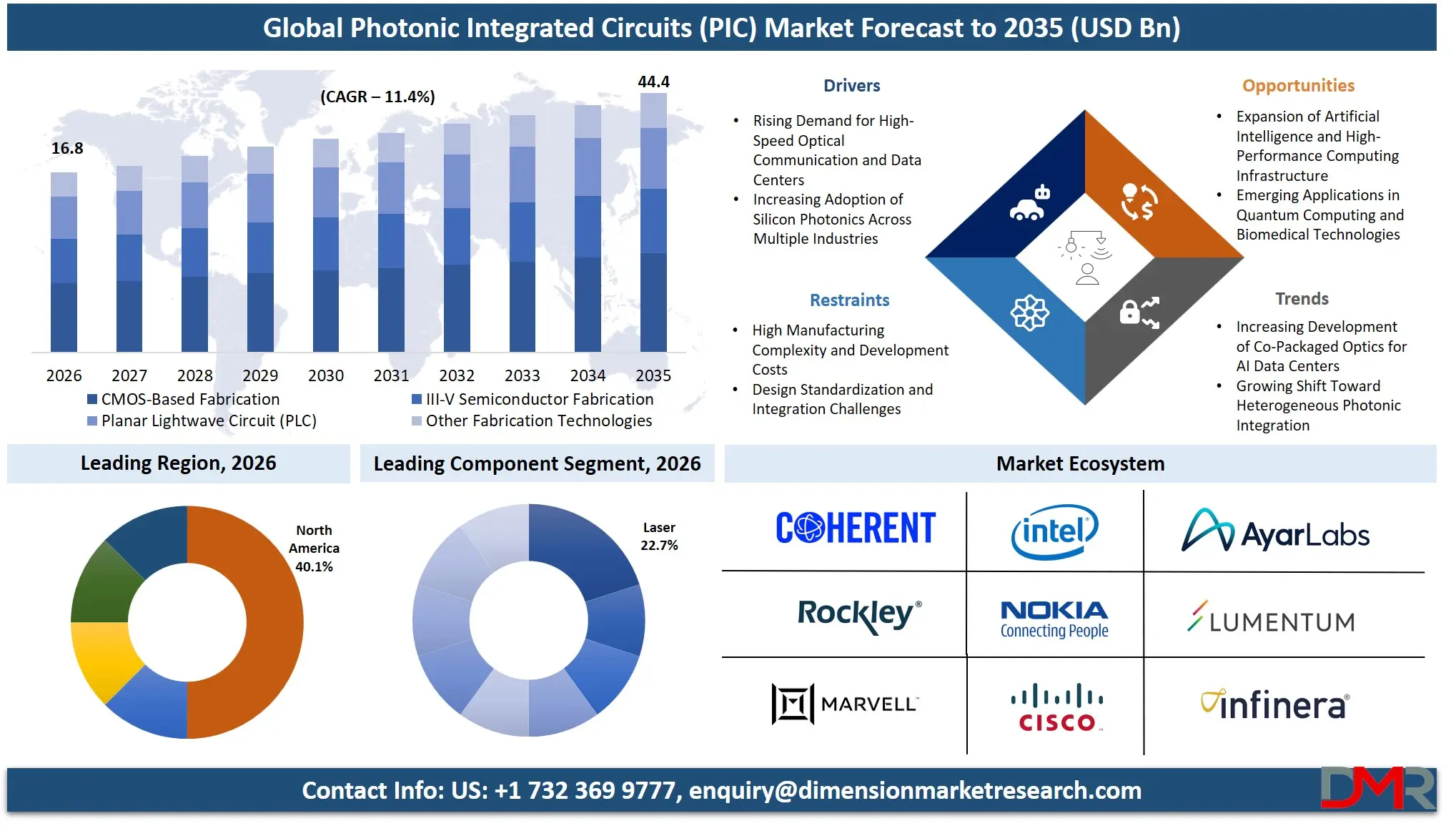

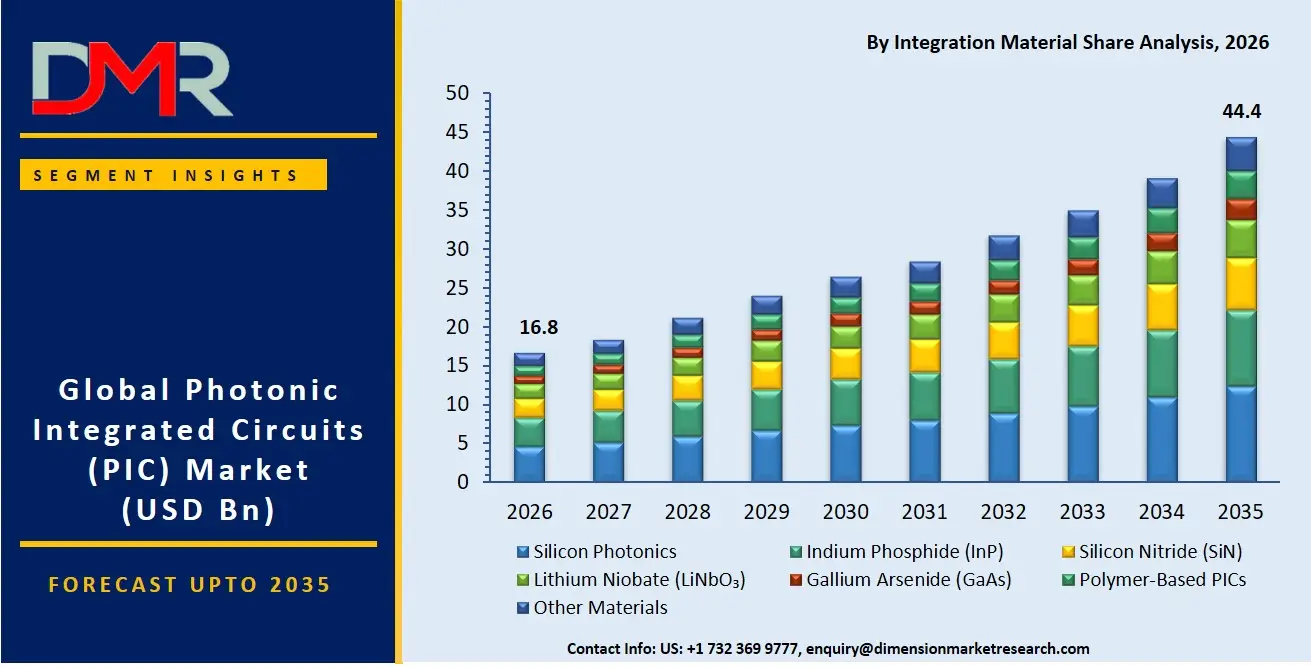

The Global Photonic Integrated Circuits (PIC) Market is expected to reach a value of USD 16.8 billion in 2026, and it is further anticipated to reach USD 44.4 billion by 2035, growing at a CAGR of 11.4% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The photonic integrated circuits market has been growing at a high rate, driven by the insatiable demand for bandwidth and energy-efficient data transmission, moving beyond traditional electronic bottlenecks. The market consists of the design and fabrication of chips that integrate multiple photonic functions, such as lasers, modulators, and photodetectors, onto a single substrate. The increasing deployment of 800G and 1.6T optical networks, the miniaturization of LiDAR and biomedical sensors, and the exploration of photonic-based quantum computing are driving the necessity of specialized PIC architectures. Data center operators and telecommunications service providers are the most frequent adopters, with silicon photonics remaining the most popular material platform due to its scalability and CMOS compatibility. The telecommunications, healthcare, and automotive industries are key players as they need high-speed, low-latency, and highly reliable optical systems.

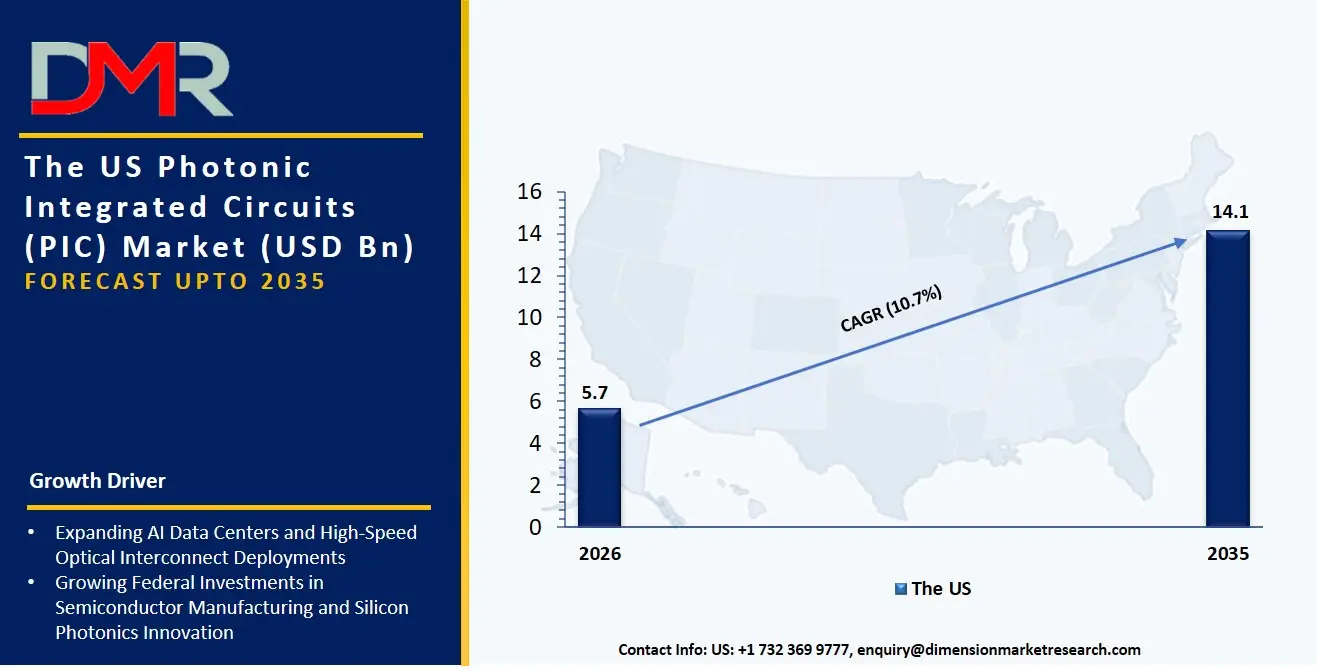

The US Photonic Integrated Circuits (PIC) Market

The US Photonic Integrated Circuits (PIC) Market is projected to reach USD 5.7 billion in 2026 at a compound annual growth rate of 10.7% over its forecast period, culminating in a value of USD 14.1 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US continues to be the largest and most developed market for PICs due to aggressive R&D spending by hyperscale cloud providers and the presence of a robust fabrication and packaging ecosystem. The market has been typified by high demand for indium phosphide (InP) and silicon photonics components, where organizations are aimed at integrating lasers and modulators for next-generation coherent pluggable optics. Besides, the push for photonic quantum computing is producing a parallel need for specialized photodetectors and low-loss waveguides capable of operating at cryogenic temperatures.

The Europe Photonic Integrated Circuits (PIC) Market

The Europe Photonic Integrated Circuits (PIC) Market is estimated to be valued at USD 4.9 billion in 2026 and is further anticipated to reach USD 12.6 billion by 2035 at a CAGR of 11.0%. The industrial policy of the European Union, focused on digital sovereignty and advanced manufacturing, has a significant impact on the market and drives the need for pilot lines for silicon nitride (SiN) and indium phosphide-based PICs. Accelerated growth of LiDAR and automotive sensing applications is also being experienced in the region as automotive OEMs in Germany and France seek to achieve a balance between high-performance laser integration and strict eye-safety and reliability standards. In addition, efforts such as the PhotonDelta ecosystem are challenging PIC foundries to create dedicated process design kits (PDKs) to provide a path to volume production and interoperability across European research institutes and industrial players.

The Japan Photonic Integrated Circuits (PIC) Market

The Japan Photonic Integrated Circuits (PIC) Market is projected to be valued at USD 2.0 billion in 2026. It is further expected to witness robust growth, holding USD 5.0 billion in 2035 at a CAGR of 10.2%. The Japanese market is unique, with a corporate drive to integrate cutting-edge optics into consumer electronics and industrial automation in response to a mature telecommunications market and legacy semiconductor leadership. Heterogeneous integration of lithium niobate (LiNbO₃) and InP lasers makes up a large part of the spending as large conglomerates miniaturize optical engines for augmented reality and high-density fiber sensing. There is also a strong need to integrate deeply in the local market to bridge the gaps between traditional optical networking components and new micro-optics for biomedical and healthcare applications, which forms a niche in high-precision modulators and optical filters.

Key Takeaways

- Market Size & Forecast: The Global Photonic Integrated Circuits market is projected to reach USD 16.8 billion in 2026, expanding dramatically to USD 44.4 billion by 2035, fueled by the dual drivers of explosive data center traffic and the transition from discrete optics to chip-scale integration.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 11.4%, driven by the critical need to overcome the I/O bottleneck in high-performance computing (HPC) and the escalating complexity of managing thermal and signal integrity in co-packaged optics.

- Primary Growth Drivers: Key forces include the widespread migration to 400G/800G and terabit-scale optical communication, the miniaturization of optical sensing and LiDAR systems for autonomous platforms, and the integration of photonic chiplets requiring specialized heterogeneous integration skills.

- Key Market Trends: Major trends include the rise of application-specific PICs (e.g., biosensors, quantum photonic processors), the use of AI-powered tools within fabrication and testing to auto-correct process variations, and the shift toward monolithic integration to reduce assembly costs for high-volume consumer applications.

- By Integration Material Analysis: Silicon Photonics is expected to dominate volume discussions due to its leverage of existing CMOS infrastructure. However, Indium Phosphide and Lithium Niobate platforms are increasingly required to build high-performance optical amplifiers and high-bandwidth modulators that silicon alone cannot provide efficiently.

- By Application Analysis: Optical Communication & Data Centers and Telecommunications are the most lucrative applications due to relentless bandwidth demands. Optical Sensing and LiDAR are the fastest-growing sectors as complex beam steering and signal processing require robust photonic-electronic co-design.

- Regional Leadership: North America is poised to dominate this market with 40.1% of the market share in 2026 due to its well-developed technological ecosystem that leverages hyperscale data center investments and makes it a leader in this market.

What is the Photonic Integrated Circuits (PIC)?

Photonic Integrated Circuits are the semiconductor chips that process and transmit light, integrating multiple optical components offered by specialized foundries and design houses to assist organizations across the entire product development lifecycle. These circuits, unlike discrete fiber-optic modules, are related to the miniaturization and co-packaging of optical functions. This involves Monolithic Integration to create compact, single-chip transceivers, Hybrid Integration to combine the best performance of different material platforms like InP lasers with silicon photonics circuits, and Heterogeneous Integration to bond different materials directly, ensuring photonic systems can effectively replace power-hungry electronic interconnects. With data centers exceeding 50% of network traffic inside the facility, PIC-based solutions are needed to achieve energy-per-bit governance, signal integrity, and bandwidth density, making optical investments translate into a tangible improvement in compute efficiency, as opposed to technical complexity.

Use Cases

- Co-Packaged Optics for AI Clusters: Data center operators hire the integration of InP lasers and silicon photonics modulators to transition from pluggable modules to co-packaged optics directly adjacent to switch ASICs, providing ultra-high bandwidth density and energy efficiency for AI/ML training clusters.

- Photonic Biosensing on a Chip: Healthcare institutions use monolithic SiN-based photodetectors and on-chip optical filters to migrate laboratory-scale diagnostics onto portable, reusable lab-on-a-chip platforms, preparing the diagnostic landscape for point-of-care infectious disease detection.

- Quantum Photonic Processors: Government organizations and research institutes use specialized fabrication technologies to deploy architectures that manipulate single photons for quantum computing, ensuring qubit fidelity and scalability that cannot be achieved with bulk optical components.

- Solid-State Automotive LiDAR: Automotive manufacturers use heterogeneous integration of LiNbO₃ modulators and multi-channel lasers to integrate complex beam-steering mechanisms with FMCW ranging engines and then provide long-range, interference-immune perception for autonomous driving.

How AI is Transforming the Photonic Integrated Circuits (PIC) Market?

AI is changing the photonic integrated circuits market by accelerating the process of designing complex optical structures, as well as enhancing fabrication yield. In component design, AI-based inverse design tools have the potential to automatically generate non-intuitive waveguides, couplers, and filters with superior performance, greatly minimizing the number of manual simulation cycles and design timelines, and project risk. Meanwhile, AI-powered features in wafer-scale testing allow foundries to better control fabrication outcomes by detecting subtle process drifts, predicting and classifying defects, and suggesting corrective actions like lithography tuning to reinforce zero-defect manufacturing methods.

End-system performance and novel computing paradigms are also revolving around AI. In the application space, intelligent photonic tensor cores are being developed to continuously process matrix multiplications within optical neural networks, identifying patterns at the speed of light while bypassing the von Neumann bottleneck. Moreover, generative AI assistants are complementing photonic design automation by simulating process variations and modeling fabrication tolerances to give engineers a visualization of the performance yield before committing expensive tape-outs.

Market Dynamics

Key Drivers in the Global Photonic Integrated Circuits (PIC) Market

Rising Demand for High-Speed Optical Communication and Data Centers

The rapid growth of cloud computing, artificial intelligence, 5G networks, and hyperscale data centers is significantly driving demand for photonic integrated circuits. Traditional electrical interconnects are increasingly unable to meet the bandwidth, speed, and energy efficiency requirements of modern communication infrastructure. PICs enable ultra-fast optical data transmission with lower latency, reduced power consumption, and compact device integration. Data center operators and telecommunications providers are heavily investing in optical networking technologies to support exponential growth in internet traffic. Continuous expansion of digital infrastructure worldwide positions photonic integrated circuits as essential components for next-generation communication systems and high-capacity optical interconnects.

Increasing Adoption of Silicon Photonics Across Multiple Industries

Silicon photonics technology is becoming a primary growth driver due to its compatibility with mature CMOS semiconductor manufacturing processes. This compatibility enables cost-effective, large-scale production of high-performance photonic integrated circuits for telecommunications, AI computing, healthcare, automotive LiDAR, and industrial sensing applications. Major semiconductor companies continue investing in silicon photonics research and commercial production to improve processing speed, reduce energy consumption, and enhance chip integration. Continuous technological advancements, expanding foundry capabilities, and increasing industry collaborations are accelerating commercialization. Growing demand for compact, energy-efficient optical devices further strengthens silicon photonics adoption across global markets.

Restraints in the Global Photonic Integrated Circuits (PIC) Market

High Manufacturing Complexity and Development Costs

Photonic integrated circuits require sophisticated design methodologies, advanced semiconductor fabrication facilities, and precision manufacturing processes, resulting in high development and production costs. Designing integrated optical components while maintaining low signal loss and high device reliability requires specialized engineering expertise and expensive testing equipment. Limited availability of dedicated photonic foundries further increases production expenses and extends commercialization timelines. Smaller companies often face barriers in accessing advanced fabrication infrastructure due to high capital requirements. These technical and financial challenges continue limiting widespread adoption, particularly for emerging applications and cost-sensitive industries seeking affordable photonic integration solutions.

Design Standardization and Integration Challenges

The absence of universally accepted design standards presents a major challenge for photonic integrated circuit development. Manufacturers frequently utilize proprietary materials, fabrication processes, and packaging techniques that reduce interoperability between devices from different vendors. Integrating photonic components with conventional electronic circuits requires complex heterogeneous packaging, thermal management, and signal optimization techniques. These integration challenges increase engineering complexity, development time, and overall project costs. Limited standardization also slows ecosystem development and broad commercial adoption across industries. Addressing compatibility, manufacturing consistency, and scalable integration remains essential for accelerating global photonic integrated circuit market expansion.

Growth Opportunities in the Global Photonic Integrated Circuits (PIC) Market

Expansion of Artificial Intelligence and High-Performance Computing Infrastructure

The rapid growth of artificial intelligence, machine learning, and high-performance computing creates substantial opportunities for photonic integrated circuits. AI data centers require ultra-fast, energy-efficient communication between processors and memory systems, where optical interconnects significantly outperform traditional electrical connections. PICs provide higher bandwidth, lower latency, and reduced power consumption, supporting increasingly complex AI workloads. Technology companies continue investing in optical computing infrastructure to overcome communication bottlenecks within advanced computing systems. As AI adoption accelerates globally, demand for high-performance photonic technologies is expected to expand significantly across cloud computing and enterprise data center applications.

Emerging Applications in Quantum Computing and Biomedical Technologies

Photonic integrated circuits are increasingly being adopted in quantum computing, biomedical diagnostics, and advanced sensing technologies, creating significant long-term market opportunities. PICs enable precise manipulation of photons for quantum information processing, secure communications, and highly sensitive measurement systems. In healthcare, integrated photonic devices support compact biosensors, medical imaging systems, and point-of-care diagnostic platforms with improved accuracy and miniaturization. Ongoing investments in quantum research, precision medicine, and next-generation sensing technologies continue expanding commercial applications. These emerging high-value sectors are expected to become major contributors to future growth in the global photonic integrated circuits market.

Trends in the Global Photonic Integrated Circuits (PIC) Market

Increasing Development of Co-Packaged Optics for AI Data Centers

Co-packaged optics is emerging as a major trend in the photonic integrated circuits market as hyperscale data centers seek higher bandwidth and lower energy consumption. This technology integrates optical engines directly with switching and processing chips, significantly reducing power loss and improving communication efficiency. AI workloads continue increasing data transfer requirements, making co-packaged optics an attractive solution for future computing architectures. Semiconductor manufacturers, cloud providers, and networking companies are accelerating investments in this technology to support next-generation AI infrastructure. Growing commercialization efforts are expected to drive widespread adoption across advanced optical networking environments.

Growing Shift Toward Heterogeneous Photonic Integration

Heterogeneous integration is gaining momentum as manufacturers combine multiple semiconductor materials such as silicon, indium phosphide, and silicon nitride onto a single photonic platform. This approach enables superior optical performance while maintaining manufacturing flexibility and improved device functionality. Heterogeneous photonic integration supports advanced applications requiring integrated lasers, modulators, detectors, and optical amplifiers within compact chip architectures. Continuous innovation in packaging technologies, wafer bonding, and semiconductor fabrication is improving manufacturing scalability. Increasing industry collaboration between foundries, semiconductor companies, and research institutions continues accelerating adoption of heterogeneous photonic integrated circuit technologies worldwide.

Research Scope and Analysis

The Global Photonic Integrated Circuits (PIC) Market Report is segmented by Component, Integration Material, Integration Type, Fabrication Technology, Application, and End User. These segments comprehensively analyze photonic technologies, material platforms, manufacturing methods, integration approaches, application areas, and industry adoption, providing detailed insights into market dynamics, competitive landscape, technological advancements, and future growth opportunities.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Component Analysis

The Lasers segment is projected to dominate the Photonic Integrated Circuits (PIC) market because lasers serve as the primary light source required for optical signal generation in communication, sensing, and computing applications. High-performance integrated lasers are essential for enabling high-speed data transmission, low power consumption, and compact photonic devices. Their widespread adoption in optical transceivers, hyperscale data centers, 5G infrastructure, and telecommunications networks continues to drive demand. Continuous advancements in semiconductor laser technology, improved integration with silicon photonics, and increasing deployment in AI-driven data processing further strengthen market leadership. As optical networking expands globally, integrated lasers remain the cornerstone component of PIC solutions.

By Integration Material Analysis

Silicon Photonics is expected to dominate the integration material segment because it combines optical functionality with mature CMOS semiconductor manufacturing processes, enabling high-volume, cost-effective production of photonic integrated circuits. The technology supports high-speed optical communication, low power consumption, and seamless integration with existing electronic chips. Major semiconductor companies and hyperscale cloud providers increasingly invest in silicon photonics for data center interconnects, AI computing infrastructure, and next-generation telecommunications. Continuous improvements in manufacturing scalability, device performance, and integration capabilities further reinforce its leadership. Strong ecosystem support and commercial adoption position silicon photonics as the leading material platform within the global PIC market.

By Integration Type Analysis

Monolithic Integration is poised to dominate the integration type segment because it enables multiple photonic components to be fabricated on a single semiconductor substrate, reducing manufacturing complexity, device size, and production costs.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

This approach delivers superior reliability, lower optical losses, improved energy efficiency, and enhanced signal performance compared to multi-chip alternatives. Increasing demand for compact, high-speed optical communication systems and large-scale production has accelerated adoption across telecommunications, data centers, and sensing applications. Ongoing advancements in semiconductor fabrication technologies continue improving monolithic integration capabilities, making it the preferred architecture for commercially deployed photonic integrated circuits worldwide.

By Fabrication Technology Analysis

CMOS-Based Fabrication is expected to dominate the fabrication technology segment because it leverages the well-established semiconductor manufacturing ecosystem to produce photonic integrated circuits efficiently and economically. CMOS compatibility enables mass production, high manufacturing yields, reduced fabrication costs, and seamless integration of photonic and electronic components on the same chip. Leading semiconductor manufacturers increasingly adopt CMOS processes for silicon photonics targeting AI infrastructure, optical networking, and hyperscale data centers. Continuous investments in advanced semiconductor foundries and process optimization further improve device performance and scalability. These advantages make CMOS-based fabrication the dominant manufacturing technology for commercial PIC production.

By Application Analysis

Optical Communication & Data Centers is projected to dominate the application segment because rapidly increasing internet traffic, artificial intelligence workloads, cloud computing, and hyperscale data center expansion require ultra-high-speed optical connectivity. Photonic integrated circuits provide higher bandwidth, lower latency, reduced power consumption, and improved signal integrity compared to conventional electrical interconnects. Cloud service providers and telecommunications companies increasingly deploy PIC-enabled optical transceivers to meet growing data transmission requirements. Continuous expansion of 5G, AI infrastructure, and edge computing further accelerates adoption. Their critical role in supporting modern digital infrastructure firmly establishes optical communication and data centers as the leading application segment.

By End User Analysis

Data Center Operators & Cloud Providers is anticipated to dominate the end-user segment because they require high-capacity optical networking solutions to support rapidly expanding cloud services, artificial intelligence, machine learning, and high-performance computing workloads. Photonic integrated circuits enable faster data transmission, lower energy consumption, reduced latency, and greater network scalability within hyperscale data centers. Continuous investments by leading cloud companies in next-generation optical interconnect technologies are accelerating commercial deployment. Increasing global demand for digital services, AI processing, and cloud infrastructure continues driving adoption. As hyperscale computing expands, data center operators remain the largest consumers of photonic integrated circuit technologies worldwide.

The Global Photonic Integrated Circuits (PIC) Market Report is segmented on the basis of the following:

By Component

- Lasers

- Modulators

- Photodetectors

- Multiplexers/Demultiplexers

- Optical Amplifiers

- Waveguides

- Optical Filters

- Couplers & Splitters

- Other Components

By Integration Material

- Silicon Photonics

- Indium Phosphide (InP)

- Silicon Nitride (SiN)

- Lithium Niobate (LiNbO₃)

- Gallium Arsenide (GaAs)

- Polymer-Based PICs

- Other Materials

By Integration Type

- Monolithic Integration

- Hybrid Integration

- Heterogeneous Integration

By Fabrication Technology

- CMOS-Based Fabrication

- III-V Semiconductor Fabrication

- Planar Lightwave Circuit (PLC)

- Other Fabrication Technologies

By Application

- Optical Communication & Data Centers

- Telecommunications

- Optical Sensing

- LiDAR

- Biomedical & Healthcare

- Quantum Computing

- High-Performance Computing (HPC)

- Aerospace & Defense

- Industrial Automation

- Consumer Electronics

- Other Applications

By End User

- Data Center Operators & Cloud Providers

- Telecommunications Service Providers

- Healthcare & Life Sciences

- Automotive

- Aerospace & Defense

- Industrial Manufacturing

- Consumer Electronics Companies

- Research & Academic Institutes

- Government Organizations

- Other End Users

Regional Analysis

Leading Region by Market Share

ℹ

To learn more about this report –

Download Your Free Sample Report Here

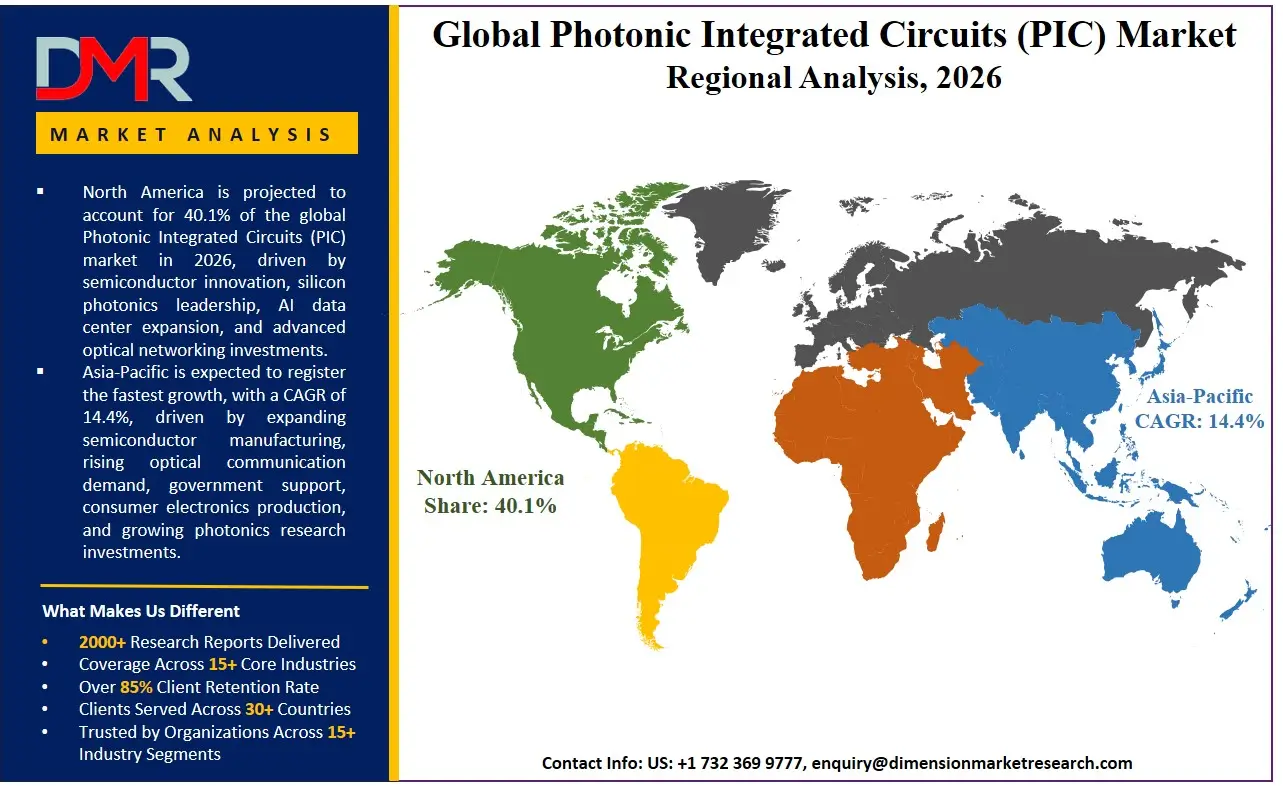

North America is poised to dominate the global photonic integrated circuits market as it is projected to hold 40.1% of the market share by the end of 2026. The United States, which dominates North America, has the highest share in the PIC market because of the unmatched concentration of hyperscale data center operators, the aggressive technology roadmaps of AI compute providers, and the deep R&D focus of DARPA-funded photonics programs. The area has an established ecosystem of global semiconductor tool vendors, boutique integrated photonic foundries, and a rich pool of talent in electronic-photonic design automation. Enterprise investment in artificial intelligence, advanced LiDAR, and the retirement of copper-based interconnects contribute to the continued demand for silicon photonics transceivers and heterogeneous laser integration along with continuous design-for-manufacturability optimization. Moreover, a vibrant venture capital climate persistently finances upcoming quantum photonics companies that need expert foundry access to achieve expeditious tape-outs and secure yield maturity.

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding photonic integrated circuits market, driven by government-led sweeping photonics infrastructure initiatives in China, Japan, South Korea, and Taiwan. The fast-paced deployment of 5G/6G base stations, the rise of a sophisticated consumer electronics manufacturing base, and the dynamic expansion of the autonomous mobility ecosystem are compelling established semiconductor conglomerates and telecom operators to move away from discrete optical assemblies. Monolithic and heterogeneous integration consulting is in high demand to help these large organizations head in the direction of fully integrated photonic chips for high-speed transceivers and compact sensing modules. There is also a severe lack of qualified PIC design talent in the region, and it is necessary to outsource design services and multi-project wafer runs to bridge the skills gap and enable faster investments in PIC-based product roadmaps.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global photonic integrated circuits market has become highly dynamic with a heterogeneous array of pure-play PIC foundries, large-scale semiconductor fabrication giants, and niche fabless design houses. The key to success will be the profound strategic alliances with CMOS foundries and material providers because they will open the necessary co-design opportunities and early access to new process design kits (PDKs). The movement towards market consolidation is rapidly progressing with traditional ASIC design houses acquiring optical simulation and III-V bonding specialists to stay afloat. Proprietary intellectual property, including automated inverse design algorithms and application-specific component libraries, is becoming a more important basis of competitive differentiation than just generic wafer fabrication or assembly approaches.

Some of the prominent players in the Global Photonic Integrated Circuits (PIC) Market are:

- Broadcom Inc.

- Intel Corporation

- Cisco Systems

- Nokia

- Lumentum Holdings Inc.

- Coherent Corp.

- Infinera Corporation

- Marvell Technology

- Ayar Labs

- Rockley Photonics

- EFFECT Photonics

- POET Technologies

- Ligentec

- SMART Photonics

- DustPhotonics

- Source Photonics

- Ranovus

- NeoPhotonics

- Hamamatsu Photonics

- Tower Semiconductor

- Other Key Players

Recent Developments

- December 2025: Ayar Labs and Alchip Technologies demonstrated the industry's first TSMC COUPE-based optical I/O engine, integrating Ayar Labs' TeraPHY photonic integrated circuit to deliver optical connectivity of up to 100 Tb/s for AI accelerators.

- April 2025: Intel Corporation showcased its Optical Compute Interconnect (OCI) chiplet at the 2025 Optical Fiber Communication (OFC) Conference. The solution integrates silicon photonics with CPUs to enable high-bandwidth, low-power optical connectivity for AI infrastructure and next-generation data centers.

- April 2025: Intel Corporation announced that its high-volume Silicon Photonics platform has shipped more than 8 million photonic integrated circuits and 32 million on-chip lasers, supporting hyperscale cloud providers with high-bandwidth optical networking solutions for AI-driven data centers.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 16.8 Bn |

| Forecast Value (2035) |

USD 44.4 Bn |

| CAGR (2026–2035) |

11.4% |

| The US Market Size (2026) |

USD 5.7 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Component, By Integration Material, By Integration Type, By Fabrication Technology, By Application, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Photonic Integrated Circuits (PIC) Market?

▾ The Global Photonic Integrated Circuits market is poised to be valued at USD 16.8 billion in 2026 and is projected to reach USD 44.4 billion by 2035, driven by the universal need to overcome electronic I/O bottlenecks with chip-scale optical integration in data centers, sensing, and AI compute fabrics.

What is the CAGR of the Global Photonic Integrated Circuits (PIC) Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 11.4% from 2026 to 2035, reflecting the accelerating complexity of high-bandwidth interconnects and the persistent push for heterogeneous integration of lasers, modulators, and photodetectors onto a single substrate.

What factors are driving the growth of the Global Photonic Integrated Circuits (PIC) Market?

▾ Key drivers include the end of Moore’s Law for electrical I/O, the imperative to miniaturize optical systems for LiDAR and biosensing, the fabrication complexity of combining III-V materials with silicon, and the surge in demand for quantum photonic processors amid evolving secure communication needs.

Which region held the largest share of the Photonic Integrated Circuits (PIC) Market in 2026?

▾ North America is projected to hold 40.1% of the market share in 2026, driven by a mature hyperscale data center ecosystem and aggressive enterprise investment in Silicon Photonics and InP-based coherent optical engines.

Which region is expected to grow the fastest in the Photonic Integrated Circuits (PIC) Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid 5G deployment and manufacturing scale-up in China, Japan, and South Korea, where CMOS-based fabrication and photonic integration are critical for transitioning large telecom OEMs to next-generation optical products.

What are the major trends in the Global Photonic Integrated Circuits (PIC) Market?

▾ Major trends include the integration of AI-driven inverse design into photonic workflows, the rise of co-packaged optics and chiplet architectures, the demand for LiNbO3 thin-film modulators, and the focus on automated wafer-scale testing within complex heterogeneous integration environments.

Who are the key players in the Global Photonic Integrated Circuits (PIC) Market?

▾ Key players include semiconductor giants like Intel and NVIDIA (Mellanox), network system makers like Cisco and Nokia, pure-play photonics firms like Lumentum and Coherent Corp., and specialized foundries like GlobalFoundries, SMART Photonics, and Tower Semiconductor.

How is the Global Photonic Integrated Circuits (PIC) Market segmented?

▾ The market is segmented by Component, Integration Material, Integration Type, Fabrication Technology, Application, and End User.