What is the Global Physical Security Market Size?

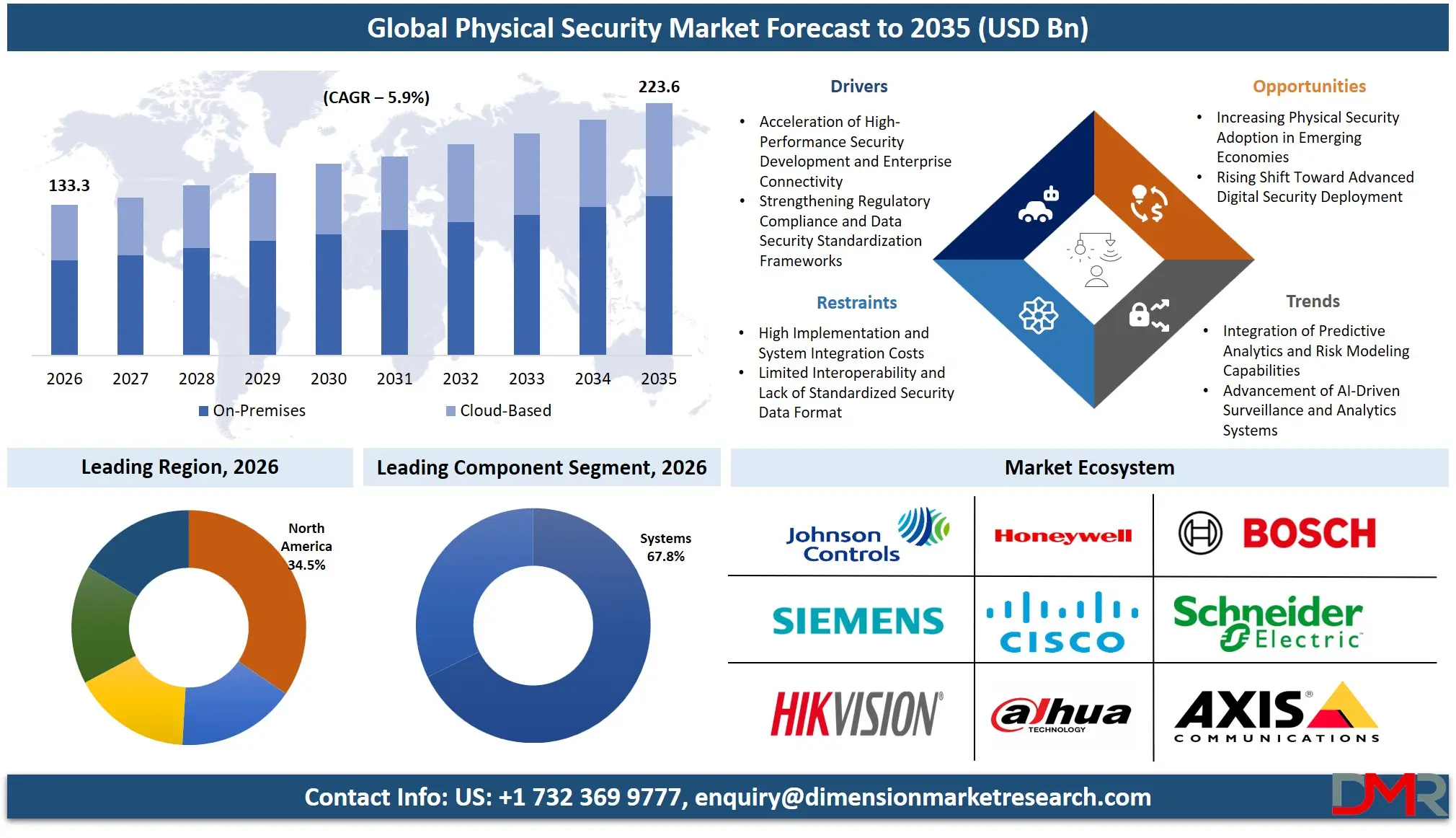

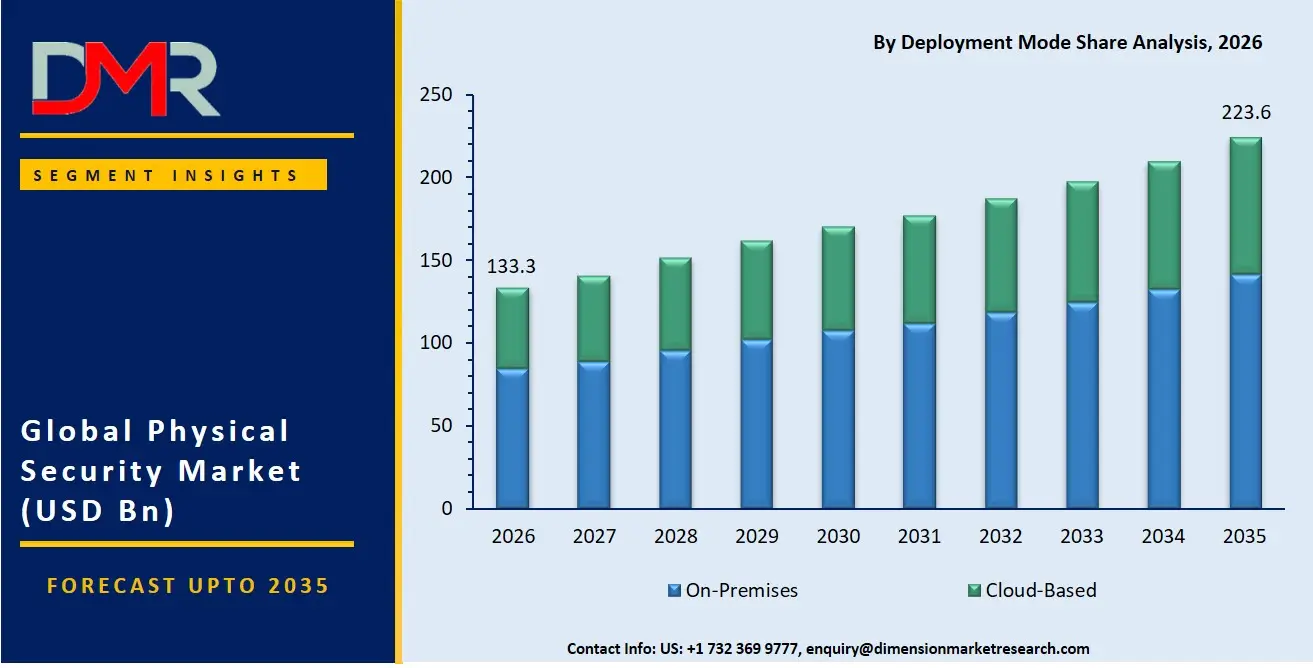

The Global Physical Security Market size is estimated at USD 133.3 billion in 2026 and is projected to reach USD 223.6 billion by 2035, exhibiting a CAGR of 5.9% during the forecast period, driven by the rising use of AI-powered video analytics and automated incident response, decentralized security deployment patterns in hybrid architectures, and connected digital governance and compliance management systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The global Physical Security Market is expanding because of increasing use of high-accuracy sensor fusion and behavioral profiling in detecting and analyzing anomalous activity patterns, increasing regulatory mandates (e.g., GDPR, NDAA), which reduce the chance of security breaches during cross-site system integration and speed up compliance audits for new public safety projects, and more funding in automating privacy-preserving video logging.

Some other reasons for expansion in this market include new technologies in runtime system stability management, video anomaly prediction through behavior analytics, automated event-driven threat handling, high-volume streaming video platforms, and improved cross-supplier security data-sharing rules. The digital shift in hybrid and cloud-based security management has been helpful in speeding up product development and making sensitive access management easier. This includes biometric encryption research. In addition, government plans focusing on preventing security breaches and the secure digital economy have ensured steady research in physical security systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

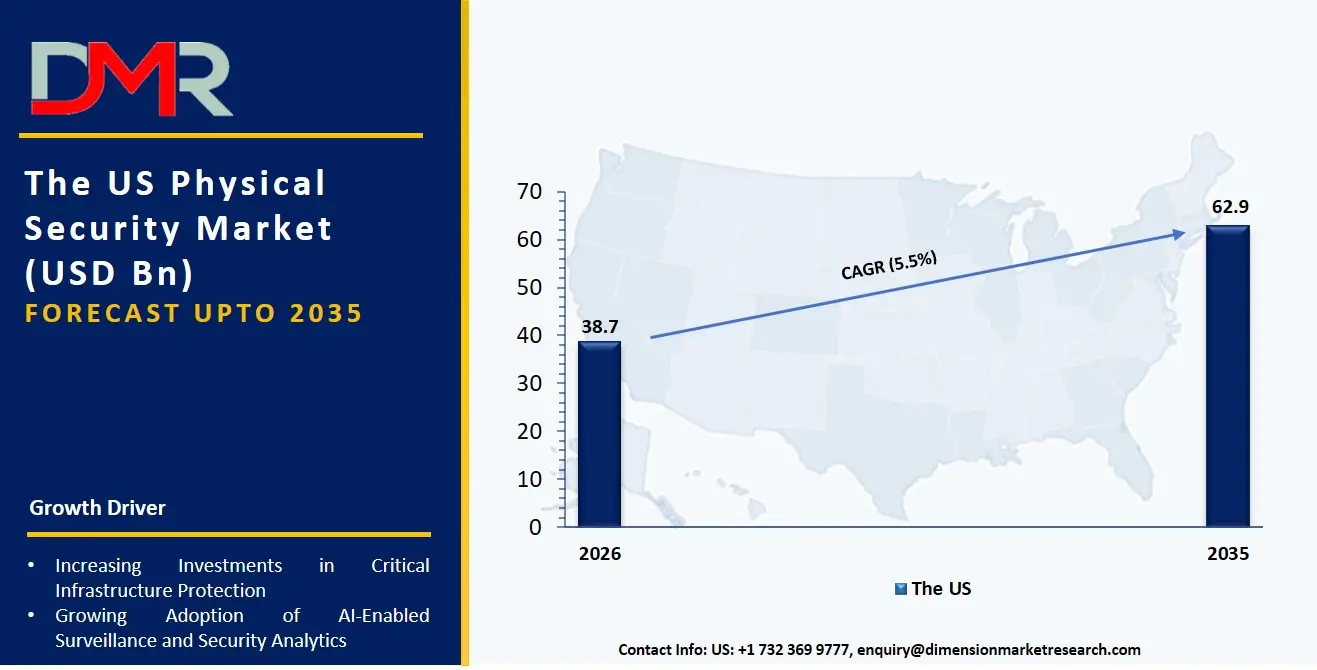

The US Physical Security Market

The US Physical Security Market is estimated to grow to USD 38.7 billion in 2026 with a compound annual growth rate of 5.5% during the forecast period.

The US market is shaped by major federal and state-level programs promoting secure security architectures, digital adoption supported by DHS and CISA, and DOD-led critical infrastructure modernization initiatives. These programs encourage the use of AI-powered surveillance, real-time video-in-transit protection, and predictive compliance software for security workflows. Automated security monitoring platforms are being rapidly adopted, and the US continues to invest in better data sharing between federal agencies, encrypted audit systems, and reliable threat detection tools for physical security platforms. Service providers are also influenced by laws like HIPAA, SOX, and national infrastructure strategies to offer services that ensure data security, rule-following, and smooth integration across hybrid and multi-site environments.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Europe Physical Security Market

The European Physical Security Market is estimated to be valued at USD 35.9 billion in 2026, witnessing growth at a CAGR of 5.4%, during the forecast period.

Europe's physical security market is well-established, shaped by EU-wide policies such as the Smart City Strategy, the General Data Protection Regulation (GDPR), and national policies to support sustainable security markets (e.g., Germany's industrial video surveillance plans and France's national public safety strategies). Countries are also making security data management more flexible to align platform operators and customer demands and enable the sharing of anonymized surveillance data across borders. The market grows due to new tools like software for real-time video validation and risk scoring systems for access control stability. Teamwork between public and private groups and shared security regulations make deployment easier. Manufacturers have access to technologies such as AI-based threat fine-tuning, access control interaction modeling, and secure audit logging, and Europe is at the forefront of the digitalization of safe and efficient security operations.

Japan Physical Security Market

The Japan Physical Security Market is projected to be valued at USD 5.0 billion in 2026, progressing at a CAGR of 5.1%, during the period spanning from 2026 to 2035.

Japan's physical security market is well developed, with high-precision biometric data platforms, connected secure access management systems, and a wide array of system aging simulation software tools. National focus on automation, efficiency, and public safety is delivered via video analytics models and smart perimeter protection. Growth opportunities are helped by government measures under the Digital Transformation Strategy by Japan's Ministry of Economy, Trade and Industry (METI), and continued investment in smart city modernization. AI-driven surveillance research, multi-party analytics for city-wide data sharing, and virtualized secure environments all need effective physical security software to keep pace with high-volume video integration. Higher costs for validating new security systems and connecting them with older infrastructure are significant, but there are opportunities for the export of Japanese security technologies to the Asian and Pacific markets.

Key Takeaways

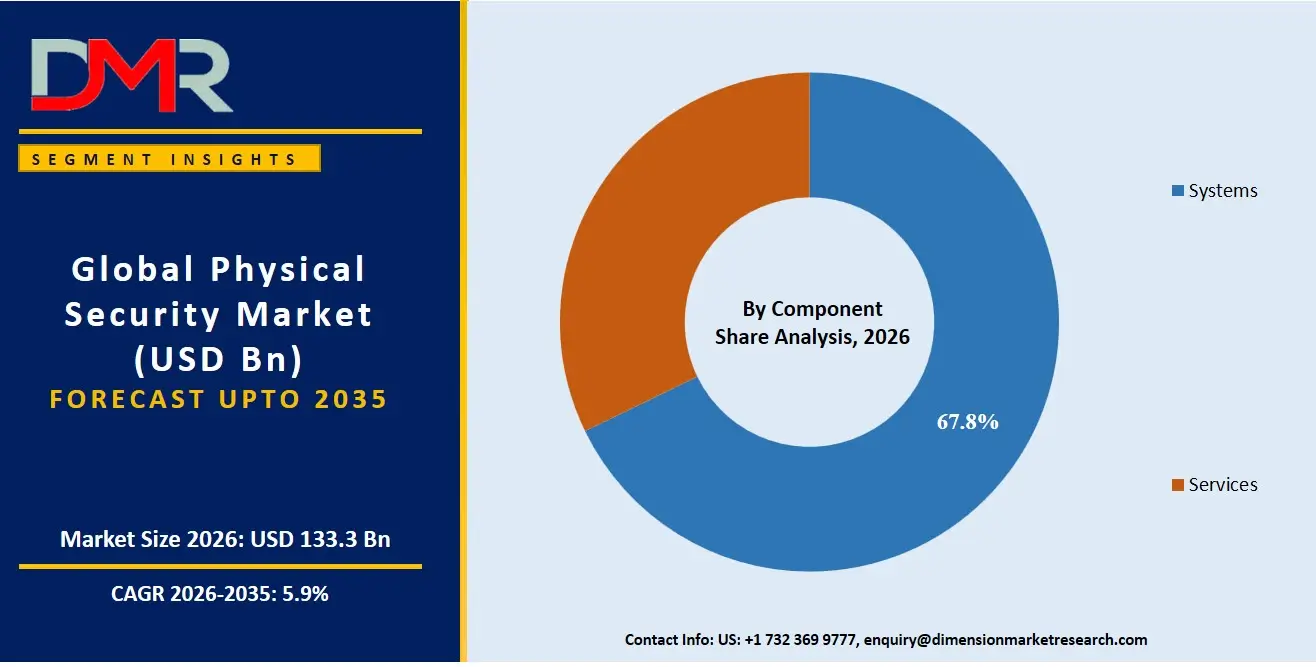

- Market Size & Forecast: The Global Physical Security Market is estimated to be valued at USD 133.3 billion in 2026 and is expected to grow to USD 223.6 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a CAGR of 5.9% in the forecast period.

- Primary Growth Drivers: The availability of new security technologies that use real-time threat detection, the need to speed up compliance results and improve success rates of public safety data sharing, and more government investment in national critical infrastructure protection are key growth drivers.

- Key Market Trends: The real-time profiling of access control stability risks, encrypted video data handling, and the shift to AI-driven surveillance platforms and automated security asset inventory management are key market trends.

- By Component: The Systems segment is expected to take the largest revenue share in the global physical security market in 2026.

- By Deployment Mode: On-Premises is expected to take the largest revenue share in 2026 in the physical security market.

- By End-Use Vertical: The Government segment is estimated to take the lead in 2026 with the largest share in the physical security market.

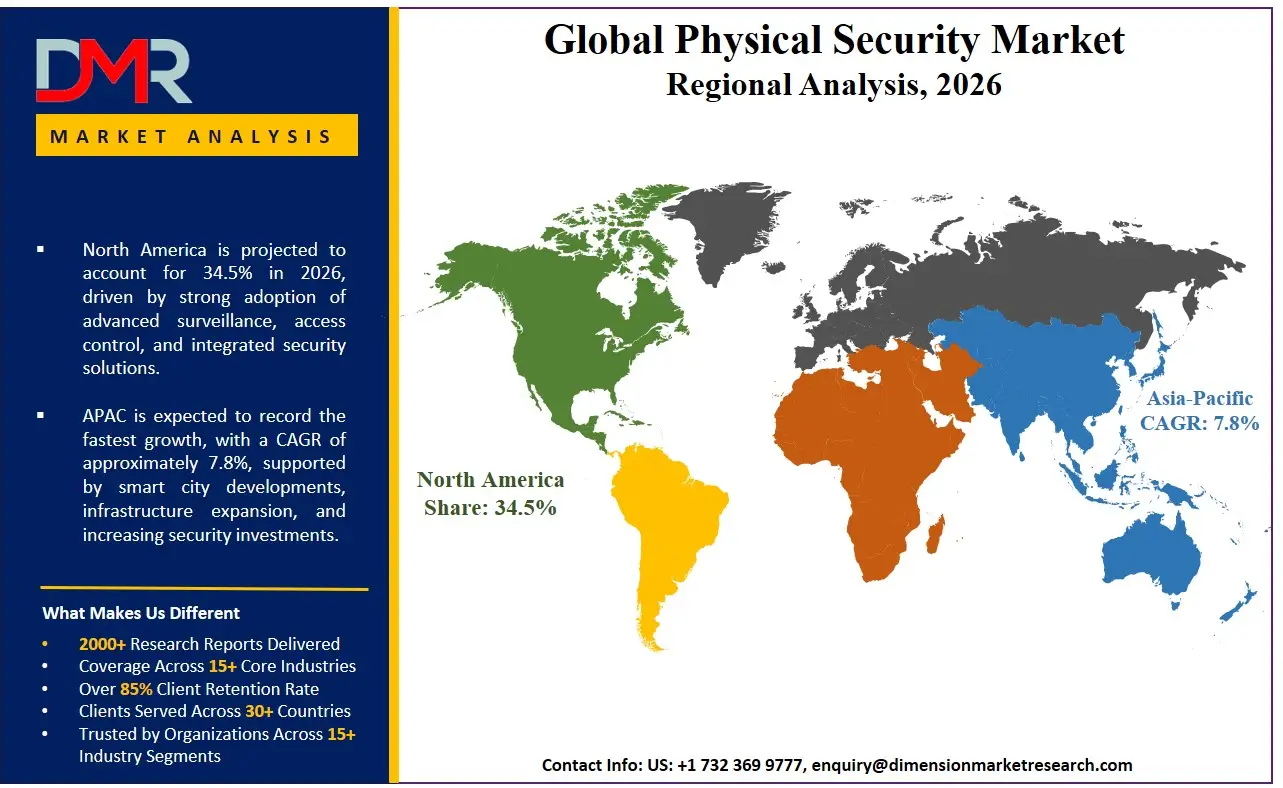

- Regional Leadership: North America is estimated to take the lead in 2026 with 34.5% share in the physical security market.

What is Physical Security?

Physical Security refers to a combination of hardware-based and real-time monitoring technologies that provide security teams, facility operators, and compliance entities with enhanced capabilities beyond basic access control, including helping to protect assets during transfer, preventing system failures via sensor engineering, and enabling secure multi-site security analytics. They include video surveillance systems, access control platforms, perimeter intrusion detection tools, and PSIM software. These platforms use modern systems such as real-time video validation, security asset inventory management software, and remote security advisory to manage, verify, and track sensitive security events and results. To improve security outcomes, manage site variability and application-specific programs, and expand protection into customized coverage to support individual enterprise designs and promote the development of secure integrated security streams.

Use Cases

- Perimeter Protection for Daily Operations: Physical security platforms can provide perimeter protection benefits through software (encrypted video analytics, attestation) and control systems to reduce system failure risk and support resolution of security incidents in minutes, compared to hours that it would take with only manual process handling.

- Long-Term Security Asset Management: Long-term data on ongoing security stability issues, including camera intermittency, threat patterns, or system degradation, are studied to better understand security performance and to help plan long-term software-based maintenance.

- Workload Load Balancing: Security data is handled through physical security platforms and smart software in hybrid and multi-cloud settings to support capacity balance for high-volume video surveillance workloads.

- Government & Regulated Programs: Faster physical security software development helps public safety innovation and development of targeted secure security programs; government programs, through smart monitoring of national critical infrastructure, advance national protection strategies and help the adoption of operational standards.

How AI Is Transforming the Global Physical Security Market?

Artificial intelligence (AI) is being used progressively more often in physical security platforms to improve threat detection, find security quality trends in access control activity patterns, and automatically spot unusual behavior patterns in video data. It also allows faster video verification because it can handle digital video submissions on a large scale. Encrypted audit logs are easier to study and help registries find security issues, reduce mistakes, and improve the overall accuracy of threat certification. This has resulted in operations being cost-effective, quicker, and more efficient than the old manual review method.

AI is also strengthening R&D by improving security risk assessment and enabling more accurate capacity planning for video processing. It helps security teams predict how many cameras will be needed, find possible system delays, and monitor the performance of security networks more effectively. In addition, automation of routine compliance checks and performance tracking is reducing operational workload, lowering administrative costs, and improving overall efficiency. This is leading to better financial results and more stable operations across the physical security production chain.

Market Dynamics

Key Drivers of the Global Physical Security Market

Acceleration of High-Performance Security Development and Enterprise Connectivity

The market is growing with the rise of advanced digital formulations for cloud-based video surveillance, better management of sensitive access streams, and a closer connection between performance monitoring and secure system integration. Physical security platforms provide real-time data that allows monitoring of video activity, helping to spot degradation early, and checking security performance much faster. This has improved operational efficiency and reduced human errors and production costs. At the same time, demand for more automated R&D is being helped by more activity in predictive analytics for the assessment of individual security risks, as data science further digitizes workflow formulation and video processing tasks.

Strengthening Regulatory Compliance and Data Security Standardization Frameworks

There is increasing emphasis on data privacy, video purity, and rule-following within the physical security system. Rules and frameworks such as GDPR, NDAA, HIPAA, and digital modernization efforts in key markets are encouraging better data handling practices and more structured security processes. These advances are supporting the need for systems that can offer steady monitoring of sensitive video data and standardized reporting. At the same time, active work to improve the sharing of security performance data and reduce verification issues is strengthening the need for more effective management systems in both government and private market participants.

Restraints in the Global Physical Security Market

High Implementation and System Integration Costs

The rollout of physical security systems remains costly, requiring significant investment in surveillance cameras, access control technologies, system integration, testing, and alignment with existing security workflows. In addition, following data regulations such as GDPR and other regional laws adds to setup complexity. These factors increase upfront costs and can limit adoption, especially among smaller enterprises and new companies entering the market.

Limited Interoperability and Lack of Standardized Security Data Format

There is still fragmentation in the market in terms of video data formats and access control procedures. Although some areas have put in place organized security management systems, many enterprises continue to work with both legacy systems and modern AI-based systems. Lack of standardized sensor protocols limits the ability to share security performance data between IT teams and security platform suppliers and results in inefficiencies in production, deployment, and system integration.

Growth Opportunities in the Global Physical Security Market

Increasing Physical Security Adoption in Emerging Economies

Newly developing economies such as Brazil, Indonesia, Nigeria, the UAE, and Vietnam are slowly building their digital security and physical protection systems. These regions have long-term growth possibilities, with more people adopting advanced cloud-based surveillance, and with more companies becoming aware of public safety programs and slowly modernizing security infrastructure. These markets have fewer older systems and can be used with new, technology-driven physical security platforms that can grow over time.

Rising Shift Toward Advanced Digital Security Deployment

The move to cloud-based security systems, decentralized IT networks, and real-time performance checks is driving the adoption of advanced physical security systems. These systems allow centralized video access, better coordination between security teams and market participants, and faster security asset inventory management. Advanced digital setups are increasingly becoming a trend among modern security providers as operational efficiency becomes one of the competitive factors.

Global Physical Security Market Trends

Integration of Predictive Analytics and Risk Modeling Capabilities

Physical security platforms are gradually adding AI-driven technology to find system degradation trends and improve accuracy in security asset inventory management. These systems allow security teams and enterprise operators to study their surveillance units' video activity behavior better, simplify the management of their security portfolios, and improve their overall security performance. This move is slowly turning the industry more proactive and data-driven in threat prevention instead of being purely reactive in security operations.

Advancement of AI-Driven Surveillance and Analytics Systems

The use of AI-based surveillance systems is currently becoming a basic part of today's cloud-based security operations. These systems allow real-time access control stability monitoring, centralized security asset administration, and better network coordination among market participants. Advanced physical security platforms are improving the efficiency and responsiveness of platform providers that operate in different regions by reducing dependence on manual security processes and allowing operations to grow more easily.

Research Scope and Analysis

The global physical security market is witnessing strong growth driven by rising adoption of advanced surveillance technologies, site-wide optimization, and increasing demand for high-security and high-efficiency asset protection processes. The market is segmented based on component, deployment mode, organization size, and end-use vertical.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Component Analysis

The Systems segment is likely to continue dominating the market in 2026, accounting for approximately 67.8% of the global physical security market share. This dominance is driven by widespread deployment of video surveillance systems, physical access control systems (PACS), perimeter intrusion detection and prevention systems (PIDS), and fire & life safety solutions across commercial, industrial, government, and transportation environments. Growing investments in AI-enabled surveillance, biometric authentication, and integrated security platforms are further supporting demand for advanced physical security systems. Within the Systems segment, Video Surveillance Systems hold the largest share, driven by increasing adoption of IP-based cameras, cloud-connected monitoring, and AI-powered video analytics for real-time threat detection and situational awareness. The Services segment continues to expand steadily, driven by increasing demand for system integration, managed monitoring, maintenance, and security consulting services.

By Deployment Mode Analysis

The On-Premises segment is likely to continue holding the lead in 2026, accounting for approximately 56.0% of the global physical security market share, driven by strong demand for high-control, compliance-ready security, regulatory flexibility, and flexible processing across government and defense sectors. This segment reflects the continued preference for air-gapped and auditable security operations. The Cloud-Based segment is the second-largest and fastest-growing, supported by enterprise scalability needs and government incentives for remote monitoring services such as VSaaS and ACaaS. On-Premises remains a mature segment focused on regulated industries where data security and compliance are critical.

By Organization Size Analysis

The Large Enterprises segment is expected to dominate with around 68.5% market share in 2026, driven by the need for enterprise-wide digital transformation, multi-site standardization, and significant capital budgets. Large-scale enterprises are adopting integrated security platforms to optimize global security networks and ensure operational excellence. The Small & Medium Enterprises (SMEs) segment is the fastest-growing, supported by lower entry costs, subscription-based pricing (VSaaS, ACaaS), and increasing awareness of automation benefits.

By End-Use Vertical Analysis

The Government segment is the largest end-use vertical in 2026, accounting for approximately 26.0% share, driven by the need for consistent real-time threat data, critical infrastructure protection, and public safety performance. This segment reflects the continued shift toward digitalization of large-scale continuous security operations. The Transportation & Logistics segment is the second-largest and fastest-growing, supported by regulatory mandates for cargo and passenger security (e.g., TSA, AEO), high-traffic data requirements, and traceability needs. Retail & E-commerce and Industrial represent specialized segments with dedicated physical security requirements for loss prevention and asset protection.

The Global Physical Security Market Report is segmented based on the following:

By Component

- Systems

- Physical Access Control Systems (PACS)

- Video Surveillance Systems

- Perimeter Intrusion Detection and Prevention Systems (PIDS)

- Physical Security Information Management (PSIM)

- Physical Identity and Access Management (PIAM)

- Security Scanning, Imaging & Metal Detection Systems

- Fire & Life Safety Systems

- Services

- System Integration & Professional Services

- Managed & Remote Monitoring Services

- Other Services

By Deployment Mode

By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

By End-Use Vertical

- Transportation

- Government

- Retail

- Residential

- Industrial

- BFSI

- Others

Regional Analysis

Largest Region in the Physical Security Market

It is projected that North America will take the lead in the global physical security market, covering a market share of about 34.5% in the year 2026. The region's dominance is driven by the presence of major physical security vendors, strong regulatory frameworks such as HIPAA, SOX, and state-level video privacy mandates, and early adoption of AI-driven surveillance and predictive maintenance technologies across the government and BFSI sectors. North America benefits from significant investment in enterprise digitalization, the highest concentration of cloud modernization projects in the US, and strong government support through DHS and NIST funding for secure integration. The region is also home to major security platform providers and system integrators, enabling rapid deployment of enterprise-wide PSIM. Additionally, ongoing investments in workforce training using AR/VR and operator training simulators further strengthen North America's leading position. The widespread adoption of AI-based video analytics for threat detection, security optimization, and site-wide surveillance continues to reinforce the region's market leadership.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Region in the Physical Security Market

Asia-Pacific is the fastest-growing region, supported by aggressive domestic security expansion in China and India, substantial government funding for smart city and Safe City initiatives, and increasing investments in greenfield security complexes that integrate AI surveillance from the initial design phase. The region is witnessing rapid growth in cloud-based security deployments, driving demand for cloud-based video management and analytics software. Asia-Pacific is also at the forefront of AI-driven security deployment in high-growth sectors like transportation and retail. The region benefits from lower installation costs, driving faster ROI on automation, along with rising corporate commitments to operational excellence and security compliance. Growing focus on video data protection for export markets further accelerates market expansion. Moreover, increasing data privacy regulations and the need to reduce security breaches in rapidly industrializing economies are expected to keep Asia-Pacific's growth momentum as the highest CAGR region during the forecast period.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The Physical Security market is highly competitive, with new ideas and strategic partnerships shaping the competitive environment. To gain an advantage, companies and providers are focused on developing better security platforms (such as AI-powered video analytics, automated threat detection systems, and software development kits for security management), smart video analytics, and cloud-based system monitoring. There are high barriers to entering the market due to the large amount of money needed for regulatory approval, specialized security knowledge, and the need for mature software systems and rule-following.

Strategic approaches to increase market presence include partnerships with digital research groups and public safety agencies, mergers between software providers and system integrators, and long-term support contracts with customers and government institutions. Additionally, R&D in video data-sharing rules and flexible surveillance designs are important for staying competitive and meeting the changing needs of the physical security community.

Some of the prominent players in the Global Physical Security Market are:

- Johnson Controls International plc

- Honeywell International Inc.

- Robert Bosch GmbH

- Siemens AG

- Schneider Electric SE

- Cisco Systems, Inc.

- Hangzhou Hikvision Digital Technology Co., Ltd.

- Zhejiang Dahua Technology Co., Ltd.

- Axis Communications AB

- ASSA ABLOY AB

- Allegion plc

- Motorola Solutions, Inc.

- Genetec Inc.

- Hanwha Vision Co., Ltd.

- Milestone Systems A/S

- Verkada Inc.

- ADT Inc.

- SECOM Co., Ltd.

- Securitas AB

- Allied Universal Holdco, LLC

- Other Key Players

Recent Developments

- March 2026: Johnson Controls International announced next-generation upgrades across its physical security portfolio at ISC West 2026, including enhancements to the C•CURE IQ platform, integrated video management capabilities, AI-driven incident management tools, and expanded interoperability across access control and surveillance ecosystems. The development strengthens the company’s position in enterprise-grade integrated physical security solutions.

- March 2026: Motorola Solutions, Inc. announced the acquisition of Exacom, a provider of cloud-native recording and logging solutions for emergency communications and public safety operations. The acquisition enhances Motorola Solutions’ command center and physical security ecosystem by improving incident recording, evidentiary management, and AI-enabled emergency response workflows.

- March 2026: Hanwha Vision Co., Ltd. launched BLAZE Hybrid AI Video Management System (VMS), a next-generation platform integrating AI-powered analytics, hybrid cloud architecture, centralized multi-site management, and seamless interoperability with Hanwha surveillance devices. The launch supports the company’s strategy of expanding software-driven and AI-enabled physical security ecosystems.

- February 2026: Verkada Inc. introduced its AI-Powered Deterrence platform, leveraging large vision, language, and audio models to proactively identify suspicious behavior, automate threat detection, and generate contextual voice-based warnings before security incidents occur. The launch reflects the growing integration of generative AI and autonomous response capabilities within cloud-based physical security systems.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 133.3 Bn |

| Forecast Value (2035) |

USD 223.6 Bn |

| CAGR (2026–2035) |

5.9% |

| The US Market Size (2026) |

USD 38.7 Bn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Component, By Deployment Mode, By Organization Size, By End-Use Vertical |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Physical Security Market?

▾ The Global Physical Security Market is estimated to be valued at USD 133.3 billion in 2026 and is expected to reach USD 223.6 billion by the end of 2035.

What is the CAGR of the Global Physical Security Market from 2026 to 2035?

▾ The market is growing at a CAGR of 5.9% over the forecasted period.

What factors are driving the growth of the Global Physical Security Market?

▾ The market is driven by advances in real-time threat detection and automated security enforcement, regulatory pressure to speed up security compliance results and reduce system failure mistakes, and increased government investment in national critical infrastructure protection.

What are the major trends in the Global Physical Security Market?

▾ The key market trends include the adoption of real-time access control stability tracking and encrypted video analysis, along with a growing shift toward AI-driven surveillance platforms and automated security asset inventory management systems.

Which region held the largest share of the Global Physical Security Market in 2026?

▾ North America is expected to account for the largest market share in 2026, with a share of about 34.5%.

Which region is expected to grow the fastest in the Global Physical Security Market?

▾ Asia Pacific is the fastest-growing region in the market during the forecast period.

Who are the key players in the Global Physical Security Market?

▾ Some of the major key players in the Global Physical Security Market are Johnson Controls International plc, Honeywell International Inc., Robert Bosch GmbH, Motorola Solutions Inc., Axis Communications AB, and many others.

How is the Global Physical Security Market segmented?

▾ The market is segmented by component, deployment mode, organization size, and end-use vertical.